PDF 原檔:報告_SemiAnalysis_800VDC與CPO延遲_20260608_original.pdf

原始內容

June , 202

Powered Down, Lights Off. 800VDC Pushout and CPO Deays // Muti-Vertica Note

8 minutes

By , , , and Konrad Wang Nige Chiang Nick Doye Doug OLaughin Danie Nishba

Executive Summary

- Mass adoption of Nvidiaʼs native singe-ended 800VDC design , with 800VDC voume shipments pushed to 2028. 00VDC, a separate HVDC architecture, remains on schedue for hyperscaerʼs ASC depoyments.

- ndustry chatter suggests that hyperscaers are pushing back on adoption of the singe-ended 800VDC architecture driven by Nvidia, given that 800VDC is not a necessity for Rubin which wi sti take 50VDC. They beieve that taking grid power at 5050VDC, stepping up to 800VDC and back down to 50VDC to

- feed the compute tray is inefficient. nstead, we see hyperscaers increasingy pushing for power to be deivered at a higher votage before being stepped down to the compute tray.

- 00VDC is sti set to proceed in 2H2 as expected, primariy for hyperscaersʼ in-house ASC depoyments. We expect 00VDC sidecar orders to and ate this year, with manufacturing ramping in Q1 2027.

- Net-net, this means that sidecar voumes that were initiay going to be driven by Rubin Utra/Kyber deiveries wi be moved into the 2028 window.

- 2027 CPO expectations ook too aggressive Co-Packaged Optics CPO wi be deayed versus current Street expectations . We expect to revise down scae-out CPO shipments in 202 and 2027 meanwhie we have aways had Scae-up CPO ramping in earnest from 202 even though the street has been caing for 2028 or even 2027 ramp timeines for Scae-up CPO. nstead - many NPO projects wi be ramping, but this may pay more into the hands of transceiver vendors.

- F or Scae-out CPO switches, CPO System-eve integration is the gating concern with yied economics remaining a major barrier. At an optimistic 5% optica-engine attach yied and 2 COUPEs per ASC, system yied is ony 1% . The Street modes 70100k+ Scae-out CPO switches produced annuay by 2027, but these issues are eading to much ower current production eves - putting us off track with respect to those numbers. We wi ikey revise down Scae-out CPO switch shipments in upcoming Networking mode updates.

- Overa, we came away from Computex incrementay more positive on Ampheno, Vertiv, Forgent Power Soutions, Legrand and FormFactor. Conversey, we are incrementay more negative on Lumentum, Himax, Navitas, and Wofspeed.

Recent Winners become NearTerm Losers and Vice Versa

800VDC and CPO are two themes which have been dominating the semiconductor market narrative this year. Weʼve been positive on both, with dedicated Newsetters on & . CPO 800VDC

With this note, we expect to reset investor expectations and especiay sentiment. We think positioning is stretched to a degree that matters more than the fundamentas here. The 'botteneckˮ trade (especiay in photonics/optics and power semis) has become the most crowded ong in the A compex, ikey funded by shorts against the argecap patform owners NVDA, AVGO.

Many of these names sit at or near a-time highs on momentum, with sentiment extremey buish and risk toerance maxed. That asymmetry is the opportunity: when the most-extended, most-evered part of a trade gets a negative timing confirmation, the unwind is vioent, and the funding shorts squeeze back, independent of the ong-term bu case , which we sti hod. We do not beieve this dynamic appies to memory, which is a consistent botteneck with tighter suppy-demand.

Our biggest Computex 202 takeaway is that both CPO and 800VDC have a high ikeihood of deays compared to origina ramp expectations. CPO system eve integration is more compicated than the market appreciates, and we beieve shipments wi be meaningfuy beow prior expectations. ndustry chatter suggests hyperscaers are pushing back on the singe-ended 800VDC architecture driven by Nvidia, given it is not a necessity for Rubin, with voume shipments now pushed to 2028.

HVDC roadmap in fux 00VDC sti happening 2H2 as expected, but 800VDC is pushed out

Contrary to our prior expectation of 800VDC being a 2027 story, we now 800VDC, and the underying ogic sti hods: increased rack power, centraized power deivery, and reduced conversion osses by stepping see adoption pushed out to 2028. Nvidia is sti pushing the industry toward votage down coser to the compute tray. However, penetration wi be ow in 2H2/2027 because it is not necessary for Vera Rubin. Rubin Utra and Feynman are more ikey to be where 800V becomes necessary, with Rubin Utra designs ony being finaized ater this year.

- ndustry chatter suggests that hyperscaers are pushing back on the adoption of 800VDC given that Nvidia seems to have mutipe power architecture options for the Rubin generation, and 800VDC is not a necessity. n their view, taking grid power at 5050VDC, stepping up to 800VDC and back down to 50VDC to feed the compute tray is highy inefficient. We beieve that hyperscaers are increasingy pushing for power to be deivered at higher votage before being stepped down to the compute tray.

- Technoogy adoption pushout, not a canceation: Rubin Utra/Kyber was designed with native 800VDC input to the GPU compute tray, but this has been deayed. We fagged this in our Computex preview, and our Acceerator Team pushed out Kyber expectations. However, 800VDC is a must when the GPU compute tray input requires 800VDC. We remain of the view that at very high tray and package power eves, native HVDC distribution becomes compeing. Whie not our base case, we note there are benefits to a Rubin Utra/Oberon design which takes 800VDC input, given that the compute tray wi ikey exceed 15kW TDP.

- 00VDC proceeding in 2H2 as expected: t is important to note that 00VDC is not the same as 800VDC. The former is a high-votage direct-current HVDC architecture that the hyperscaers are pursuing themseves to 1 centraize power deivery at higher votage for better efficiency and 2 avoid ACDCAC conversion osses with the UPS. We beieve that the 00VDC rack architecture is primariy

for hyperscaersʼ in-house ASC efforts, and this is sti on track. We expect 00VDC sidecar orders to and ate this year, with manufacturing ramping in 1Q27. That said, we are not ruing out hyperscaers using the 00VDC sidecar to support Nvidia hardware given that the DCDC power sheves shoud aow for this.

800VDC Read-Across to Stocks in our Coverage

- Power rack suppiers: We see the deay as neutra for power rack suppiers Vertiv VRT, Deta 208 TT, and Lite-On 201 TT, as the sidecar/power rack transition is happening regardess of whether the bus is 00V or singe-ended 800V.

- Vertiv is particuary we-positioned because the 800VDC deay extends the ife of their arge UPS business. At Computex, Vertiv demoed a grey space power rack design which ocates the PSU and PDUs outside of the T room to preserve precious white space, that we found compeing.

- Grey-space eectrica equipment suppiers: We see this as positive for grey space suppiers Forgent Power Soutions FPS, Legrand LR FP, Schneider Eectric SU FP, Hammond Power Soutions HPS.A CN and ABB ABBN SW that were at risk of osing LV transformer, LV switchgear and busway content. The pushout of 800VDC directy transates to increased upside and a onger growth runway for these names.

- Board-eve VRM / power semiconductors: Siicon-based passives and power semiconductors win regardess of architecture. Both 00V and 800V sidecars need superjunction MOSFETs, resistors, inductors, and capacitors for puse-oad transient absorption in power sheves, BBUs, and power racks. Vishay VSH suppies superjunction MOSFETs, resistors, and inductors. MLCC content scaes ineary with rack TDP Murata 81 JP, SEMCO 00150 KS, Yageo 227 TT, TDK 72 JP. nfineon FX GR appears to be the best-positioned power semi because they are hedged across Si superjunction, SiC, and GaN. At

the board/compute tray eve, VRM smart power stages step 8V/12V down to sub-1V at the GPU die, and this is unaffected by 800VDC deay. The 8V-to-sub-1V conversion chain stays the same whether the upstream architecture is AC, 00V, or 800V.

- Payers: MPS MPWR, Renesas 72 JP, nfineon, with TXN and ON quaifying as new entrants.

- Wide-bandgap pure-pays: We beieve this puts wide-bandgap WBG suppiers in an awkward spot. 00V uses some compound semi GaN is more efficient at that votage, though SiCʼs suppy chain is more mature), so the 00V transition is cose to neutra for the WBG vs siicon debate. 800VDC is where WBG content reay infects; a pushout means the incrementa WBG content upift that woud justify current mutipes on pure-pay names ike Wofspeed WOLF or Navitas NVTS has no meaningfu near-term catayst.

CPO Costs and Physics are More Prohibitive than Expected

We are positive about copper and puggabe optics reative to CPO. For Scae-up, we have aways seen the huge infection in voumes coming in 202 as key projects from AWS, AMD and Feynman ramp in earnest. Optica Engines on nterposers wi ony be fuy ungated and start ramping in that time period, opening the door to true ubiquity of CPO, but ony after 202

and 200.

n contrast, the Street has misinterpreted COUPE Optica Engine production voumes, first incorrecty assuming it was for a CPO Rubin Utra Kyber made officia that this woud not happen. We do have voumes of the VRU NVL57 in 2027 and 2028, but this wi ony use CPO from switch to switch and not to GPUs, and we donʼt see project being arge enough to move the neede and most on the Street mode too aggressive of a timeine. Overa, 202 is a more sensibe target for Scae-up CPO voume shipments and street expectations of gamechanging jumps in CPO voume in 2028 ook optimistic. took this view, and we see the significant we debunked this idea we before GTC 202ʼs announcements Our first 202 estimates from eary Apri

infections happening in 202 and beyond, coinciding with Feynmanʼs ramp. n the meantime, many NPO projects wi be ramping in decent voume, but this may pay more into the hands of transceiver vendors. Turning to Scae-out, we wi ikey revise down CPO switch forecasts in upcoming Networking mode updates. Scae-out CPO wi sti ead, but yied issues must be soved first. n addition, we had assumed 85% penetration for CPO switches at Neocouds. We continue to think that adopting CPO for Neocouds makes sense, but we have not yet found the adoption rate to be fuy universa, though we think adoption wi increase over time. The Street currenty modes 0100k+ Scae-out CPO switches shipped by 2027, driven by expectations of a sharp scae-out ramp and strong adoption rates at Neocouds, and we think todayʼs pace of scaeout production is too ow to reach this bogey. The market has been focused on . Whie asers remain an important botteneck, this framing misses other key depoyment gates, specificay COUPE deveopments. Whie COUPE deveopment remains on track for Nvidia and other adopters such as Broadcom, AMD, and Ayar Labs, system-eve integration with COUPEs remains chaenging . nP based CPO asers as a structura constraint for the ramp of CPO

- We expect Spectrum CPO output SN810, SN800 to sip by more than two quarters. NVDAʼs Spectrum CPO, the first 102.T switch with second-gen COUPEs, recenty showed .5 dB of insertion oss in on-board system-eve testing, consuming the entire optica channe budget. This is worse than Spectrum 5 CPO 'Agoraˮ), which uses the same COUPE count per ASC 2, the same connectors, FAU, and simiar system design. Neither NVDA nor TSMC has identified the source of the probem; efforts have shifted toward fundamenta assemby-process redesign.

- The yied math is punishing. ndustry chatter puts optica engine attach yied at an optimistic 5% today. At 2 COUPEs per Spectrum ASC, that compounds to 1% system yied 0.5^2. Every COUPE must be perfect post-couping; there is no rework path on a sodered switch

substrate. The industry needs .5% attach yied per engine to make voume economics work, deivering 85% system yied at 2 engines.

- NVDAʼs Quantum X50 nfiniBand CPO is in comparativey better shape: ony COUPEs per modue, so defective modues can be screened and the best ones seected for assemby. Even if rea attach yied is beow 5%, which is highy probabe, the sma modue granuarity makes the economics manageabe.

CPO deays reinforce the case that copper remains the primary interconnect for scae-up networks, with puggabe optics continuing to serve scae-out, supporting sustained demand growth for both categories. We , and noted another positive Credo deveopment. defended AECs earier this year ast week

CPO Read-Across to Stocks in our Coverage

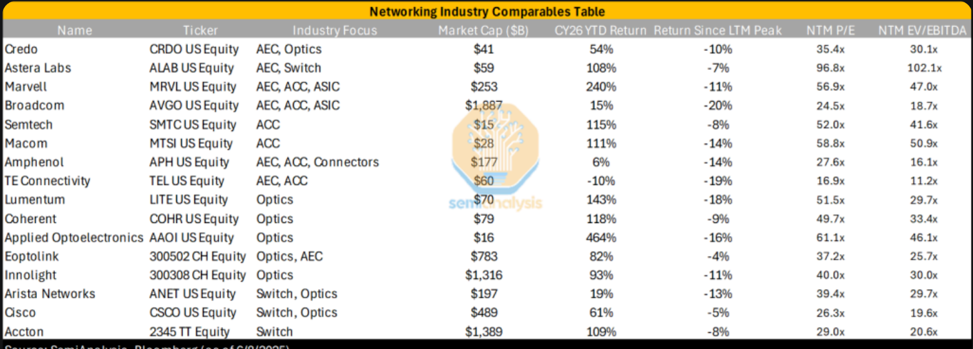

- Reative to market expectations, we are most positive on copper names Ampheno APH, Semtech SMTC, and MACOM MTS some of these Copper-exposed companies have been argey ignored despite a revenue TAM that we beieve wi ceary x in the next few years.

- We sti ike Optics companies evered to puggabe transceivers and DSPs rather than CPO, namey Marve MRVL, nnoight 0008.SZ, Eoptoink 00502.SZ, Tower Semiconductor TSEM, STMicroeectronics STM, and Astera Labs ALAB as we see the

- puggabe transceiver TAM continuing to grow at a rapid pace. The Networking Mode has discussed the growing TAM for optics at projects ike Googeʼs TPUv and v10. ndeed, many NPO projects wi aso be ramping in decent voume in the next few years, but this may pay more into the hands of transceiver vendors.

- We are more conservative on names where CPO voume is a materia part of the bu case , incuding Lumentum LTE, Coherent COHR, Himax HMX and Appied Optoeectronics AAO, though we sti think CPO has a 'brightˮ future once infection point in 202200 is reached.

- We continue to be positive on the CPO testing theme. As we detaied in our CPO test equipment andscape note and subsequent update, CPO test equipment is a picks-and-shoves beneficiary that shoud see procurement ahead of CPO voume. We remain most constructive on Teradyne TER, the frontrunner in NVDA quaification and ficonTEC partnership; FormFactor FORM for PC wafer probing; Chroma 20.TT for die-eve and system-eve test; and Hon Precision 77.TT for hander monopoy in A/HPC fina test. This underscores why testing is so critica: with system-eve integration aready consuming the entire channe budget at 2 COUPEs, the ony ever eft is ensuring every optica engine entering assemby is fawess.

Discaimers

Anayst Certifications and ndependence of Research.

Each of the anaysts whose names appear in this report hereby certify that a the views expressed in this Report accuratey refect our persona views about any and a of the subject securities or issuers and that no part of our compensation was, is, or wi be, directy or indirecty, reated to the specific recommendations or views in this Report. SemiAnaysis LLC (the 'Companyˮ) is an independent equity research provider. The Company is not a member of the FNRA or the SPC and is not a registered broker deaer or investment adviser. SemiAnaysis has no other reguated or unreguated business activities which confict with its provision of independent research.

Limitation Of Research And nformation.

This Report has been prepared for distribution to ony quaified institutiona or professiona cients of SemiAnaysis LLC. The contents of this Report represent the views, opinions, and anayses of its authors. The information contained herein does not constitute financia, ega, tax or any other advice. A third-party data presented herein were obtained from pubicy avaiabe sources which are beieved to be reiabe; however, the Company makes no warranty, express or impied, concerning the accuracy or competeness of such information. n no event sha the Company be responsibe or iabe for the correctness of, or update to, any such materia or for any damage or ost opportunities resuting from use of this data. Nothing contained in this Report or any distribution by the Company shoud be construed as any offer to se, or any soicitation of an offer to buy, any security or investment. Any research or other materia received shoud not be construed as individuaized investment advice. nvestment decisions shoud be made as part of an overa portfoio strategy and you shoud consut with a professiona financia advisor, ega and tax advisor prior to making any investment decision. SemiAnaysis LLC sha not be iabe for any direct or indirect, incidenta or consequentia oss or damage (incuding oss of profits, revenue or goodwi) arising from any investment decisions based on information or research obtained from SemiAnaysis LLC. Reproduction and Distribution Stricty Prohibited. No user of this Report may reproduce, modify, copy, distribute, se, rese, transmit, transfer, icense, assign or pubish the Report itsef or any information contained therein. Notwithstanding the foregoing, cients with access to working modes are permitted to ater or modify the information contained therein, provided that it is soey for such cientʼs own use. This Report is not intended to be avaiabe or distributed for any purpose that woud be deemed unawfu or otherwise prohibited by any oca, state, nationa or internationa aws or reguations or woud otherwise subject the Company to registration or reguation of any kind within such jurisdiction. Copyrights, Trademarks, nteectua Property.

SemiAnaysis LLC, and any ogos or marks incuded in this Report are proprietary materias. The use of such terms and ogos and marks without the express written consent of SemiAnaysis LLC is stricty prohibited. The copyright in the pages or in the screens of the Report, and in the information and materia therein, is proprietary materia owned by SemiAnaysis LLC uness otherwise indicated. The unauthorized use of any materia on this Report may vioate numerous statutes, reguations and aws, incuding, but

not imited to, copyright, trademark, trade secret or patent aws. Private nvestment Discosure. Each anayst and/or author contributing to this Report hereby discoses that they may hod, directy or indirecty, private investments in companies, sectors, or asset casses discussed or referenced herein. Such hodings, if any, are discosed externay with a third-party vendor. SemiAnaysis LLC requires that no author or anayst aow their persona investment positions to infuence the views, opinions, anayses, or concusions expressed in this Report. Readers shoud be aware that the existence of such hodings, even where discosed, may present a potentia confict of interest, and are encouraged to weigh this accordingy when evauating the contents of this Report.

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_SemiAnalysis_800VDC與CPO延遲_20260608_002.png |

187KB | 真資料圖 | 「Networking Industry Comparables Table」數據表格,列出 Credo/Astera Labs/Marvell/Broadcom/Semtech/Macom/Amphenol/TE Connectivity/Lumentum/Coherent/AAOI/Eoptolink/Innolight/Arista/Cisco/Accton 等公司代號、市值、CY26 YTD Return、Return Since LTM Peak、NTM P/E、NTM EV/EBITDA |