PDF 原檔:報告_Nomura_AI半導體伺服器循環是否見頂_20260630_original.pdf

野村《Asia AI Semi & Server — Is the cycle over?》Anchor Report,2026-06-30,119 頁。核心論點:SOX 自 3 月 +85%/自 2025/5 +211% 後近期回檔屬健康修正,但循環尚未見頂(hyperscaler 2027F capex 仍有上修空間、自有資料中心建置追蹤續升、greenfield 需 2 年使供給吃緊延續至 2027F)。瓶頸由 TSMC(CoW)轉向 WoS 與眾多小元件;漲價與獲利上修為最大催化劑。九檔調升目標價:2330_台積電(市)、3711_日月光投控(市)、5274_信驊(市)、2454_聯發科(市)、6488_環球晶圓(市)、2449_京元電(市)、2383_台光電(市)、6274_台燿(櫃)、4958_臻鼎科技(市)。

圖片清單(已驗證 2026-06-30)

size 篩 ≥40KB 候選後逐張 Read 驗證分類。嵌入 lib/ 頁只挑「真資料圖」,圖說照抄親眼所見。其餘未個別列出之圖多為券商評論 / 財報模型表(docling 已 OCR 成文字)或裝飾性投影片。

| 檔名 | 對應 Fig | 分類 | 親眼所見內容 |

|---|---|---|---|

| _001 | 封面 | 裝飾·banner | 馬拉松路跑者照片(封面,呼應 "Is the cycle over"),無資料 |

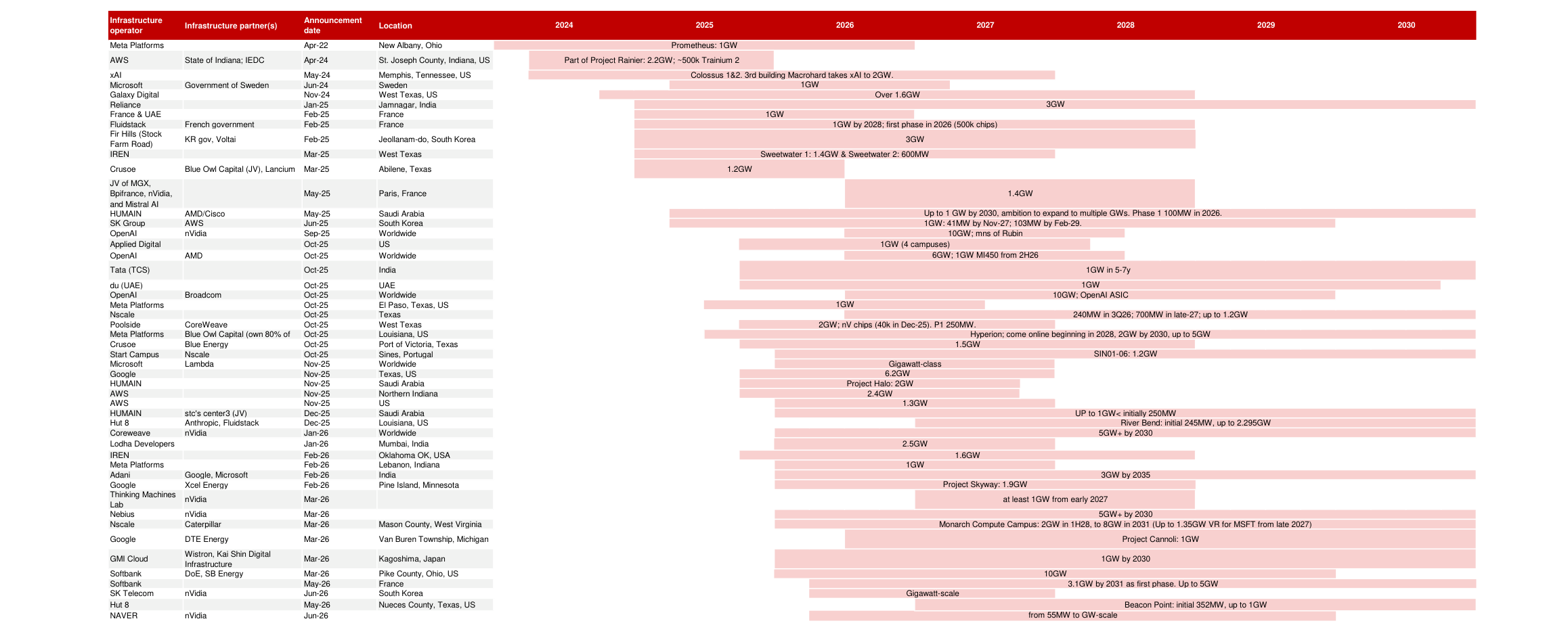

| _003 | Fig 2 | 真資料圖 | 各 CSP/neocloud 資料中心建置時程甘特圖:operator × infra partner × location × 2024–2030,標 GW 規模(如 Prometheus 1GW、Stargate、Project Rainier 等) |

| _021 | Fig 23 | 真資料圖 | Hyperscaler 自研晶片路線圖:Google/AWS/Meta/Microsoft 之 Accelerator+CPU 逐年節點(TPU v1→v9、Trainium、Inferentia、MTIA、Maia、Cobalt、Axion、Graviton) |

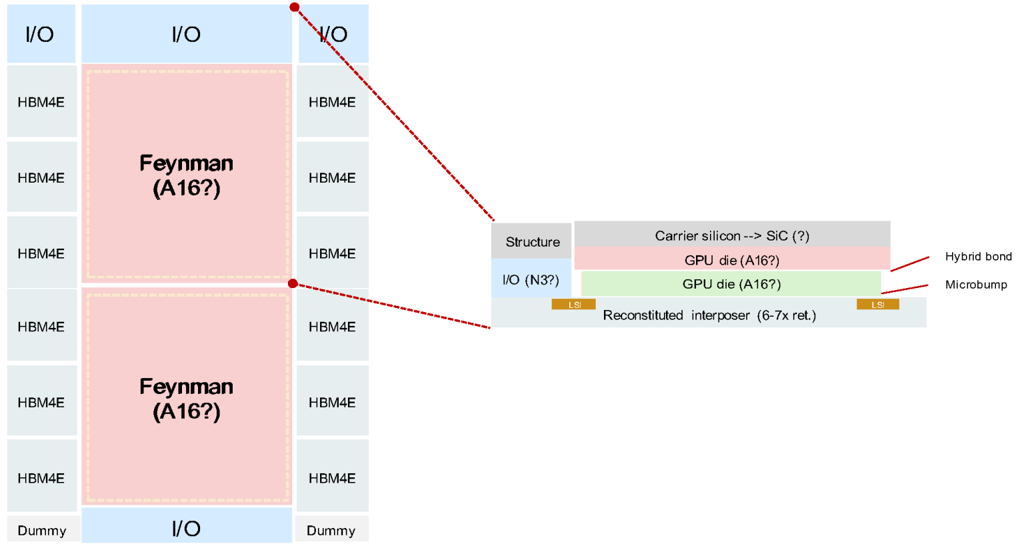

| _032 | Fig 34 | 真資料圖 | nVidia AI 平台路線圖規格表 Ampere→Hopper→Blackwell→Rubin→Rubin Ultra→Feynman:邏輯節點、電晶體數、interposer 尺寸、HBM 規格、TDP、NVLink、PCB/CCL、散熱方案 |

| _038 | Fig 42 | 真資料圖 | Intel Foundry「AI is driving Scaling of Advanced Packaging」EMIB 縮放路線圖:2023(~4x)→2026(~8x)→2028+(~12x)→Future(>24x reticle) |

| _040 | Fig 46 | 真資料圖 | TSMC 2026 技術論壇 CoWoS roadmap:3.3-reticle(8xHBM3,2024)→5.5(12xHBM3E/4,2026)→9.5(12xHBM4E,2027)→14(20xHBM5,2028)→>14(24xHBM5E,2029);5.5-reticle >98% yield in 2026 |

| _043 | Fig 50 | 真資料圖 | TSMC-SoIC roadmap:N7 9um(2023)→N5 6um(2025)→N3P/N2P 6um→A14-on-A14 4.5um(2029);56X 互連密度、5X 能效 vs CoWoS 2.5D |

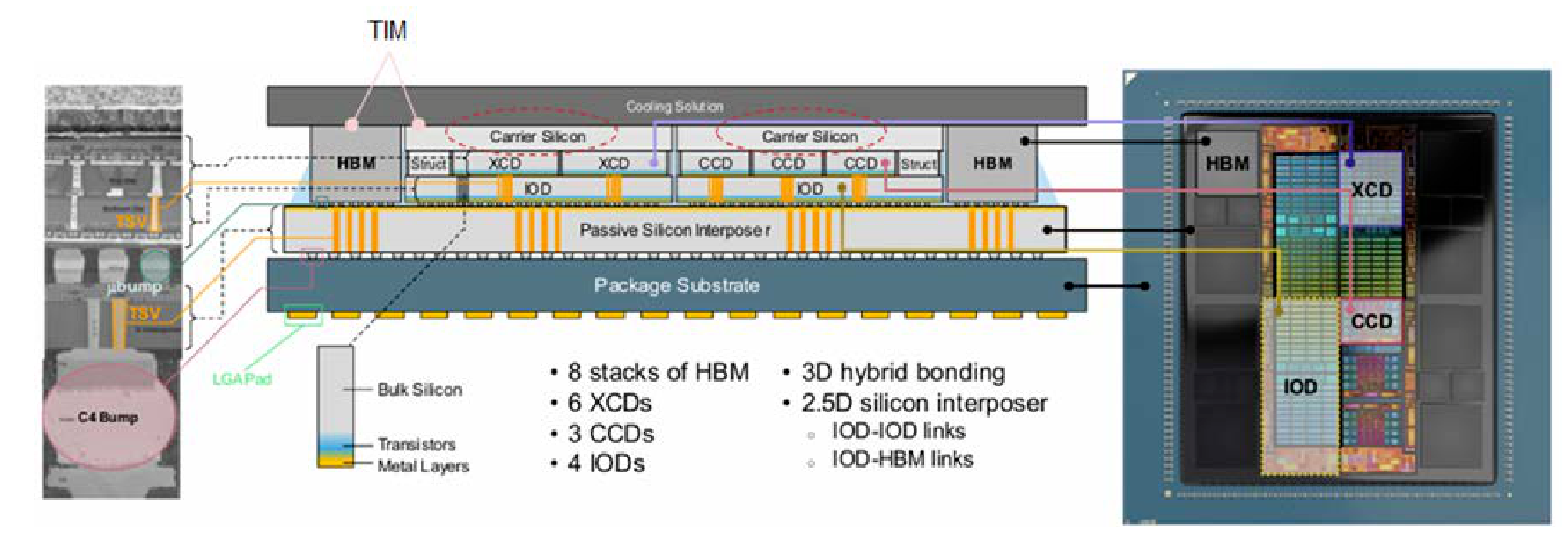

| _045 | Fig 52 | 真資料圖 | AMD MI300 剖面圖:8 stacks HBM、6 XCD、3 CCD、4 IOD、carrier silicon、passive silicon interposer、IOD-IOD/IOD-HBM links(示意 SiC carrier 替代位置) |

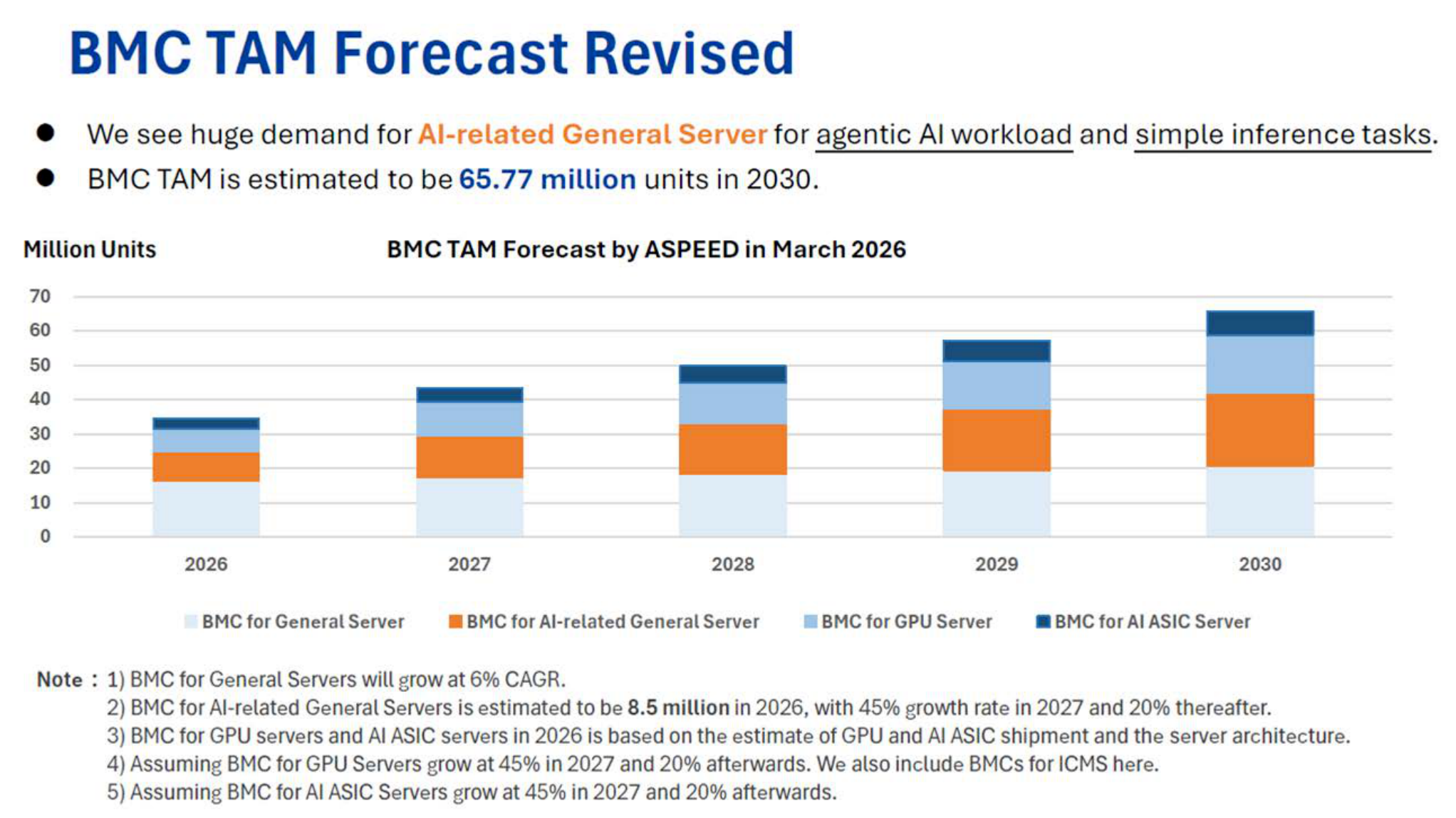

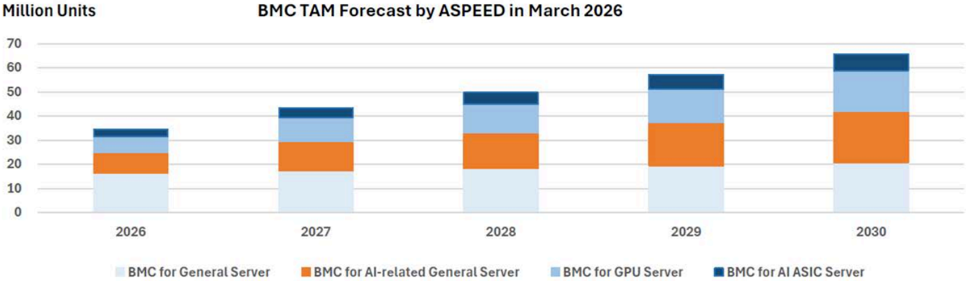

| _058 | Fig 67 | 真資料圖 | ASPEED BMC TAM 堆疊柱狀圖 2026–2030(BMC for General / AI-related General / GPU / AI ASIC server,單位百萬顆,2030 達 ~66mn) |

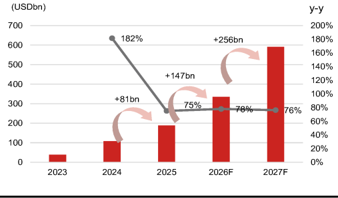

| _060 | Fig 71 | 真資料圖 | Top-5 CSP capex consensus 柱狀圖 2023–2027F,y-y 60%→72%→80%→25%,年增額 +172/+328/+182bn |

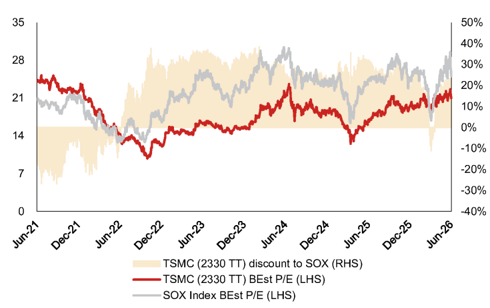

| _065 | Fig 76 | 文字卡 | SOX 走勢圖配野村多年觀點註解(歷史回顧,文字密集,低嵌入價值) |

原始內容

ANCHOR REPORT

Global Markets Research 30 June 2026

Asia AI Semi & Server

Is the cycle over?

With SOX surging by 85% since our last cycle update in March and up 211% since we revisited the AI theme in May 2025, we have noticed a share price collapse of late. To us, a pullback is healthy following such a surge, particularly when some risks have to be digested. However, we do not seem to have reached the cycle peak yet, given hyperscalers' spending upside into 2027F (despite having insufficient FCF), and our global new data center build tracking showing further upside. More importantly, the two years of greenfield build for new capacity from late-2025 suggests insufficient supply heading into 2027F. Price hikes and earnings revision remain the biggest catalysts, in our view.

Key analyses included in this report:

- Update of our proprietary global new data center build tracking ·

- CoWoS 2027F allocation considering the severe shortages of WoS vs CoW ·

- Unprecedented component supply-mismatch from 2H26F with potential to worsen further into 2027F ·

- xPU/ASIC 2027F outlook: when the elephants fight, the grass get trampled ·

- Renewal of our latest view on the AI and general server market outlook ·

- CPU demand upside and (benefiting) OSATs' CoWoS-like process ·

- SoIC and CoPoS to counter EMIB-T; and benefit to relevant supply chains ·

Research Analysts

Asia Technology

Aaron Jeng, CFA - NITB aaron.jeng@nomura.com

+886(2) 21769962

Anne Lee, CFA - NITB anne.lee@nomura.com +886(2) 21769966

Donnie Teng - NIHK donnie.teng@nomura.com +852 2252 1439

Vivian Yang - NITB vivian.yang@nomura.com +886(2) 21769970

Eric Chen, CFA - NITB eric.chen@nomura.com +886(2) 21769965

Carol Hu - NITB carol.r.hu@nomura.com +886(2) 21769963

Production Complete: 2026-06-29 20:51 UTC

EQUITY: TECHNOLOGY

Asia AI Semi & Server

EQUITY: TECHNOLOGY

Is the cycle over?

Research Analysts

There could be a few valid factors that may explain the recent share price pullback, but likely we have not yet reached the peak of this cycle

Where are we in this AI infra investment cycle?

With SOX surging by 85% since our last cycle update in March (report ) (and up 211% since we revisited the AI theme in May 2025; Fig. 76 ), we have noticed a share price collapse of late. To us, a pullback is healthy following such a surge over such a short period, particularly when we see some risks that have to be digested, e.g., the likely biggest-ever component supply mismatch, hyperscalers' 2027F free cash flow (FCF) issue, execution of many cutting-edge technologies beyond 2027F, and macro risks related to a yield uptrend. However, we do not seem to have reached the cycle peak yet given that hyperscalers' spending may need to show upside further into 2027F (despite insufficient FCF particularly driven by surging memory costs, as this might be a 'go big or go home' competition), and our proprietary global new data center build tracking suggesting further upside from our March update . On the supply side, the two years for greenfield build for new capacities from late-2025 suggests insufficient supply into 2027 (and very likely the supply bottleneck shifting from tech giants such as TSMC [2330 TT, Buy] to other, smaller component makers). Furthermore, price hikes and ongoing earnings upward revision would still be the biggest catalysts. As such, we would still be buyers into weakness. We raise target prices for nine AI tech companies (mentioned below) with this Anchor Report.

TSMC turning aggressive on CoW plan, but the bottleneck could shift to WoS

We now expect TSMC to 'target' chip-on-wafer-on-substrate (CoWoS) capacity of 2,000kpcs in 2027F, from 1,100kpcs in 2026F, and forecast that it would need 2,5003,500kpcs of CoWoS output by 2029F, depending on the scale of annual price hikes, to achieve its 'high-50%' AI revenue CAGR over 2024-29E. In addition, if Feynman production fully migrates to chip-on-panel-on-substrate (CoPoS) in 2029F, TSMC would need to build 700-800kpcs CoPoS capacity by 2029F. However, our contrarian view is that 'WoS' and many other small components would very likely become a bigger bottleneck than 'CoW' in the remaining of 2026F and also into 2027F - which is not a bad reading for long-term cycle sustainability, in our view, but would likely drive short-term share price volatility. As such, we only 'model' 1,800kpcs of CoWoS output in 2028F - which would have profound implications for different GPU/ASIC vendors in 2027F, i.e. when the elephants (nVidia [NVDA US, Not rated] and Google [GOOGL US, Not rated]) fight, the grass (other xPU/ASIC) would get trampled, we think. Separately, outsourced semiconductor assembly and test (OSAT) vendors would not only benefit from TSMC's growing WoS outsourcing but also from further price hikes (given ongoing material cost inflation) and upside from their own CoWoS-like full process (driven by CPUs).

SoIC and CoPoS to counter EMIB-T; relevant supply chains to benefit

Intel's (INTC US, Not rated) embedded multi-die interconnect bridge with TSV (EMIB-T) appears to be emerging as potentially the biggest threat to TSMC's advanced packaging. During TSMC's 2026 North America Symposium in April, TSMC launched its 14x reticle size CoWoS roadmap (2028E) vs a prior roadmap for an interposer size up to 9.5x reticle (2027E). However, our view is that system-on-integrated-chips (SoIC) and CoPoS are two equally critical technologies for TSMC to stay ahead of its competition in advanced packaging. We expect Feynman to target the first-ever GPU-on-GPU SoIC stack. In our view, there would be multiple implications from this: First, the bigger footprint and high thermal design power (TDP) of Feynman would start to drive the adoption of silicon carbide (SiC) carrier. Second, SoIC capacity demand would skyrocket through 2028-29F.

Asia Technology

Aaron Jeng, CFA - NITB aaron.jeng@nomura.com +886(2) 21769962

Anne Lee, CFA - NITB anne.lee@nomura.com +886(2) 21769966

Donnie Teng - NIHK donnie.teng@nomura.com

+852 2252 1439

Vivian Yang - NITB vivian.yang@nomura.com +886(2) 21769970

Eric Chen, CFA - NITB eric.chen@nomura.com +886(2) 21769965

Carol Hu - NITB carol.r.hu@nomura.com +886(2) 21769963

TSMC

Delta

Hon Hai

ASE

EMC

Unimicron

Quanta

Lenovo

AVC

BESI

Wiwynn

Zhen Ding

Rating

Market cap

(USDmn)

Target price (LCY)

New

Old

Stocks for action: Raising target prices across nine AI semi/hardware companies

5,800.0

2,800.0

352.0

730.0

6,880.0

1,350.0

479.0

417.0

524.0

35.0

3,130.0

We reiterate our Buy ratings with higher target prices on:

- TSMC: AI chip enabler ·

Buy

Buy

147,569

109,420

- ASE (3711 TT): upside from WoS and CoW ·

- ASPEED (5274 TT): outright CPU beneficiaries ·

- MediaTek (2454 TT): TPU upside ·

45,836

45,810

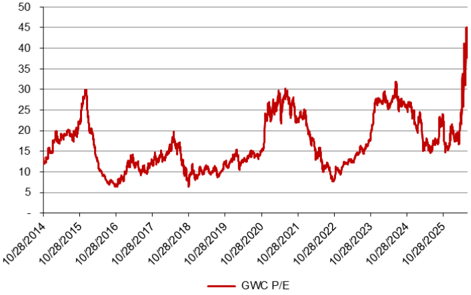

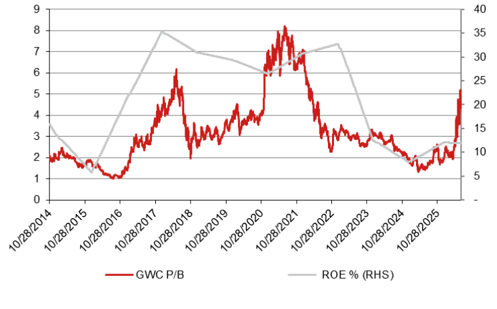

- GWC (6488 TT): SiC opportunities in Feynman ·

- KYEC (2449 TT): beneficiary of AI chip testing ·

3,400.0

2,800.0

352.0

575.0

5,285.0

1,350.0

479.0

417.0

524.0

35.0

3,130.0

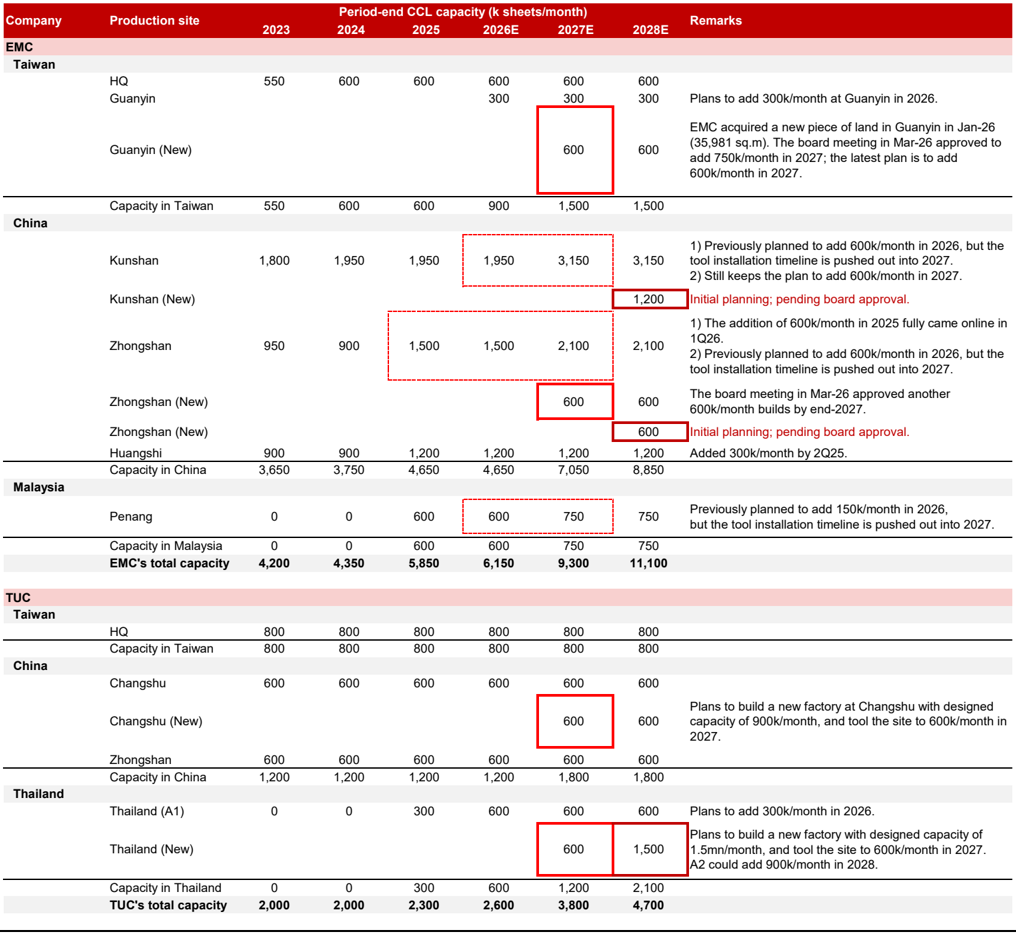

- EMC (2383 TT)/TUC (6274 TT): CCL benefiting from AI upgrade trends and more price upside from being one of the major supply bottlenecks · 720.0 510.0

ASPEED

Wistron

TUC

GWC

KYEC

Bizlink

Soitec

280.0

- ZDT (4958 TT): an emerging AI PCB/HDI maker ·

19,100.0

280.0

We also like the following Buy-rated stocks: BESI (BESI NA; CPO and GPU-on-GPU SoIC), Soitec (SOI FP; SOI wafer for CPO), Unimicron (3037 TT; substrate also benefiting from multiple trends and more price upside from being another major supply bottleneck), Victory Giant (300476 CH / 2476 HK; AI PCB beneficiary), Compeq (2313 TT), Delta (2308 TT; power top pick), AVC (3017 TT; thermal top pick), Samsung Electronics (005930 KS; memory leader), Bizlink (3665 TT; rack power and data upgrades), as well as Hon Hai (2317 TT) and Lenovo (992 HK) in ODMs.

Fig. 1: Stocks for action

Note: Priced as of 26 June 2026.

Source: Bloomberg Finance L.P., Nomura estimates

11,500.0

1

Last close

(LCY, as of

26 June 2026)

2,340.0

339,000.0

3,880.0

1,810.0

248.5

632.0

5,255.0

975.0

342.4

319.6

362.0

23.4

2,255.0

282.7

4,280.0

580.0

15,615.0

153.0

1,580.0

936.0

308.0

1,855.0

222.5

114.4

Downside

46.4%

97.6%

49.5%

54.7%

41.6%

15.5%

30.9%

38.5%

39.9%

30.5%

44.8%

49.3%

38.8%

20.3%

98.6%

24.1%

22.3%

83.0%

33.9%

28.2%

26.6%

72.5%

55.1%

118.6%

Executive summary

Big picture: We believe there are growing signs of the cycle peaking using conventional signals such as price hikes, LTAs, and possible overbooking. However, given our view that AI demand is real (report ) and AI's impact is dramatic, we have refrained from leveraging conventional cycle wisdom (which has helped us come to the correct conclusions during semi cycle peaks and bottoms over the past decade; Fig. 76 ) during this AI-driven cycle over the past two years. Since 4Q25, we have tracked global new data center build plans as a leading demand indicator for the Asia semi hardware supply chain - which enhanced our conviction on AI amid market concerns/noise in December 2025 (report ) and March 2026 (report ), respectively. In this report, we would like to refresh where we are in the AI cycle. On the supply side , it generally takes two years to build new greenfield capacity (which began in late-2025, when all hyperscalers significantly raised their chip/hardware forward demand outlooks; the earliest signal in our coverage was BMC; refer to our August 2025 ASPEED [5274 TT, Buy] report ), which suggests still likely constrained supply over the next year (e.g., TSMC's next big jump in front-end capacities will be in 2028F; Fig. 20 ). What's more, we have noted that WoS (Wafer-on-Substrate) and many other small components could become a bigger bottleneck than CoW (Chip-on-Wafer) in 2027F - which might not be a bad reading for long-term cycle sustainability, but would likely drive short-term share price volatility.

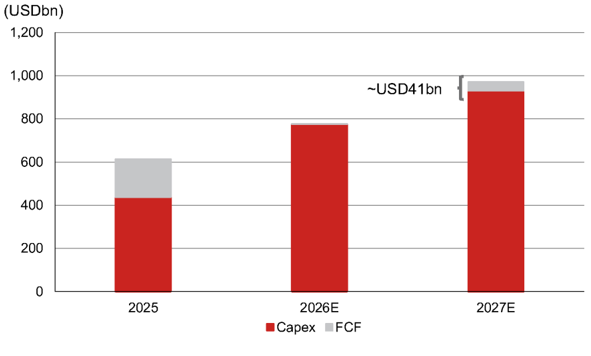

With demand side factors (hyperscalers' capex upside, our global data center tracking, token consumption trends, etc., see Appendix: CSP comments on AI and investments ) sustaining, across-the-supply-chain price hikes will likely continue, we think. Sustainable upward consensus earnings estimate revisions for Asia semi hardware supply chain companies would still be the biggest catalyst in driving share prices higher - as we predicted to happen through 2026 (report ) - in our view. Risk-wise , we believe AI infrastructure investment momentum is critical (so far, so good based on our tracking), while new technology breakthroughs will be needed from 2028F. We believe lots of cutting -edge technologies need to happen beyond 2027F before the AI chip hardware roadmap can be extended further, including, but not limited to: EMIB-T, CoPoS, GPU-onGPU SoIC, microchannel lid (MCL), co-packaged optics (CPO), 336G/448G SerDes, M9Q/M10Q PCB, PTFE, and new tools/materials for high-density interconnect (HDI) PCB. Owing to surging memory costs, hyperscalers could start facing insufficient FCF in 2027F (Fig. 71 to Fig. 75 ; our latest AI server sales forecast for 2027 suggests eventual upside to hyperscaler capex) - which could cause investor concerns, particularly with the macro risk of yield on an uptrend driven by growing inflation but still decent unemployment rates in the US (report and report ).

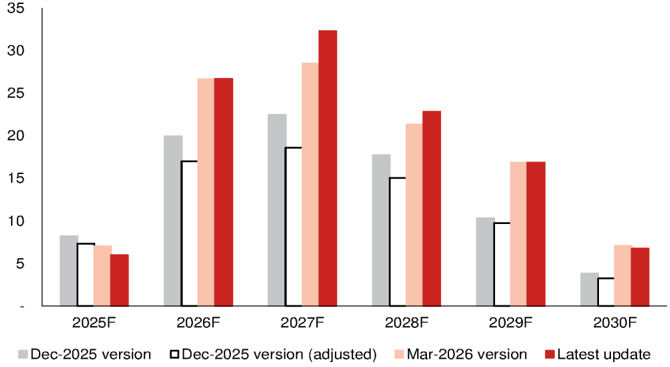

Our latest Global new data center build tracking suggests further upside from our March update three months ago. The total number of projects has increased to 280 (from 240), while the gigawatt (GW) level project number has increased to c.50 from 40+. The incremental capacity deployment in 2027F, measured in GW, would grow to 32GW (from 28GW) from 26GW (unchanged) in 2026F. We do not have full-year visibility yet, but the tracking so far suggests 23GW demand in 2028F (up from 21GW). Fig. 2 - Fig. 4 compile our latest findings. Given the surge of AI chip/hardware share prices over the past three months, we hope to see growing 2028 visibility over the next 3-6 months.

We have noticed quite a few interesting points to highlight with respect to TSMC's CoWoS capacity-expansion plan. First, TSMC has turned aggressive in responding to surging AI chip demand and is likely to defend itself from competition from EMIB-T and fanout panel-level packaging (FOPLP), in our view. We thus now expect TSMC to target CoWoS capacity of 2,000kpcs in 2027F, from 1,100kpcs in 2026F. Though we do not have 2028-29F visibility, our back-of-the-envelope calculation suggests that TSMC would need somewhere from 2,500-3,500kpcs of CoWoS output by 2029F, depending on the scale of annual price hikes, to achieve management's goal of a 'high-50% AI revenue CAGR' (Fig. 21 and Fig. 22 ). Another interesting exercise we have done in terms of long-term CoWoS plans is asking, ' How would CoPoS affect the CoWoS capacity plan? '. A year ago, our view on TSMC's CoPoS plan (report ) was that we expected CoPoS to enter mass production only from 2029F (much later than the Street estimate). Despite this, we hope that TSMC could pull forward its schedule to meet nVidia's Feynman GPU timeline (2H28). With our 'napkin math' assuming nVidia Feynman production fully migrates to CoPoS in 2029F, TSMC would need to build 700800kpcs CoPoS capacity by 2029F (How will TSMC's CoWoS capacity shape up

through 2029F? ). We believe 50% of CoWoS capacity in 2029F would need to find new customers in this scenario (however, we note that in reality, product transitions do not happen overnight).

Though TSMC has turned aggressive in its CoWoS plan (precisely, its CoW plan), our tech team's contrarian view is that 'WoS' (not controlled by TSMC) and many small components would very likely become a bigger bottleneck than 'CoW' (controlled by TSMC) into 2027F - which is not a bad reading for long-term cycle sustainability, but would likely drive short-term share price volatility. Taking these new factors into consideration, we only model 1,800kpcs of CoWoS output in 2027F (despite our view of TSMC's target of 2,000kpcs) - which would have profound implications for different GPU/ASIC vendors in 2027F, in our view.

We believe there will be an unprecedented component supply-mismatch period in 2H26F, and we expect it will get worse in 2027F , as in 2H25 many component suppliers still underestimated (more so than TSMC) the order upside potential from AI when they made their capacity expansion plans. In addition to the well-known advanced node/packaging, memory, and CPU shortages, PCB/CCL, IC substrate, higher-end capacitors, power management IC (PMIC), and optical components, are also already in shortage currently, and we forecast demand-supply conditions will further deteriorate when Rubin and Trainium 3 ramp from 2H26. This could further affect the supply for nonAI subsectors such as consumer and auto, in our view. Also, supply chain price hikes could continue or increase with worsening shortages , we think.

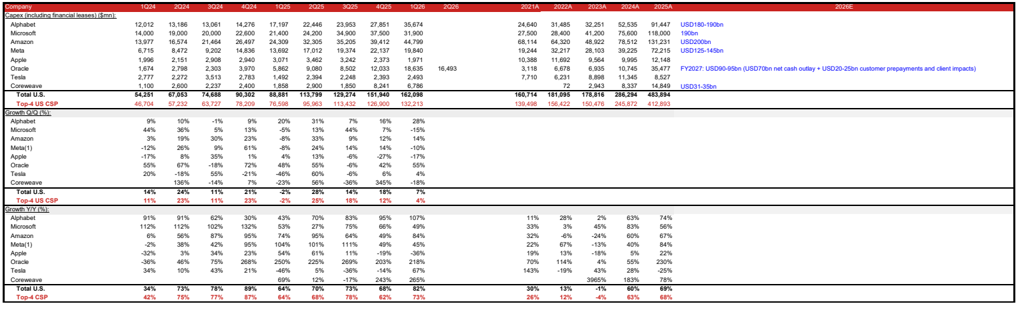

In view of our assumptions and observations above, we are raising our 2026-27F server market forecasts on stronger AI and general/CPU server sales (Fig. 69 ). We now forecast global server revenue growth of 74%/65% y-y for 2026F/2027F (vs 43% y-y for 2026F previously), with AI server revenue growth rates at 78%/76% y-y for 2026F/2027F (previously 58% y-y for 2026F) and general/CPU server revenue growth rate at 67%/43% y-y for 2026F/2027F (previously 16% y-y for 2026F). For 2026F, considering rising capex guidance from top US CSPs YTD and increase in neoclouds, we raise our GB/VR rack shipment assumption from 50k units to 54.5k units for 2026F (Fig. 69 ). Of this, we assume VR200 to account for 15-20% in 2026F, with concentration in 4Q26F . We assume a transition from GB300 to VR200 during late-2Q26F to 3Q26F, as top CSPs will likely prefer to wait for VR200, instead of continuing to install more GB300s. In the transitional period, we expect neoclouds to play a bigger role in buying more systems to support the continued token demand growth at AI companies. We also introduce our forecast of 62k racks for 2027F , with a potential transition from Rubin to Rubin Ultra happening in 2Q27F.

In 2H25, we concluded in our AI Semi & Server Anchor Report that nVidia would continue to secure 60% of CoWoS allocation (along with other key materials such as T-glass), as nVidia had booked 'strategic resources' well ahead of its peers to crowd out competitors. This strategy has worked out well, in our view - e.g., Google, despite Geminis' impressive breakthrough from late 2025 (news ), hasn't been able to acquire much more support in 2026. AMD's (AMD US, Not rated) GPU and AWS's (AMZN US, Not rated) ASIC have progressed through 2026 with downside to beginning-of-the-year expectations. Looking into 2027F CoWoS allocation, we expect the following dynamics (many of which are contrarian). First, CoW capacity allocation would be less critical than whether GPU/ASIC vendors can secure support from substrates and other smaller components (e.g., CCL, capacitors); Second , Google's tensor processing unit (TPU) share in CoWoS could rise further to 26% in 2027 from 23% in 2026 (nearly double y-y growth) on its proven Gemini performance, complete Google ecosystem and share gain; Third , despite our view that nVidia would continue to strive for 60% allocation, our models build in our assumption that nVidia's share in CoWoS would slide to c.55% in 2027F given the squeeze by TPU; Fourth , the other GPU/ASIC vendors would be squeezed even more, e.g., we assume AMD's CoWoS capacity share would only marginally improve y-y despite a low base, while AWS's CoWoS capacity share might even fall y-y in 2027F; Fifth , we raise our AI revenue growth estimate for TSMC to 77%/67% for 2026F/27F (from 69%/24% previously), vs the company's target of a 'high-50% revenue CAGR over 2024-29E' (Fig. 26 ); Sixth , despite our c.55% CoWoS allocation assumption for nVidia in 2027F, we see upside to consensus revenue forecast if it can sell out all those booked capacities (Fig. 72 ); Seventh , though we expect TPU to enjoy the fastest growth in 2027F among AI logic semi, the majority of growth would be taken by MediaTek (its share in TPU could more than double to 30%+ in 2027F from c.15% in 2026).

TSMC's more aggressive attitude on expanding CoW capacity would benefit OSATs directly, in our view, given TSMC's current full outsourcing of WoS. Though we believe WoS supply constraints could limit shipment upside for OSATs, the likely ongoing price hikes for substrates could drive OSAT packaging prices higher, too. Separately , we expect the next growth catalyst for OSATs to shift to their own CoWoS-like full processes. Other than technology readiness, we believe another key factor hindering OSATs from engaging in CoW processes is the enormous losses that would be incurred if there were to be immature assembly yield. That, in our view, is the reason why the high-performance computing chips using OSATs' CoW to ramp up volume from 2H26 are mostly CPUs (Fig. 37 ; which do not carry expensive HBM content), such as AMD's Venice CPU by ASE/SPIL or nVidia's Vera CPU by Amkor (AMKR US, Not rated) . Fig. 57 summarizes the skyrocketing TAM outlook for the server CPU market; also see Appendix: other critical developments and key quotes from major server CPU players for more details.

In the meantime, Intel's (INTC US, Not rated) EMIB-T appears to be emerging as potentially the biggest threat to TSMC's advanced packaging given its capability of large-reticle size packaging. The most closely watched EMIB-T project now is Google's v9 TPU in collaboration with MediaTek given its high complexity and large volume (set to ramp-up in 2028, according to our industry survey). The >9x reticle-size chip-level footprint (details in our February 2026 MediaTek report ) is something that could not be addressed by TSMC's CoWoS roadmap by the time when Google's decision was made, we suppose. Also, TSMC probably was not looking to expand CoWoS capacity that much at end-2025 (refer to our December 2025 Anchor Report ). Fig. 44 summarizes our view on EMIB-T supply chain beneficiaries.

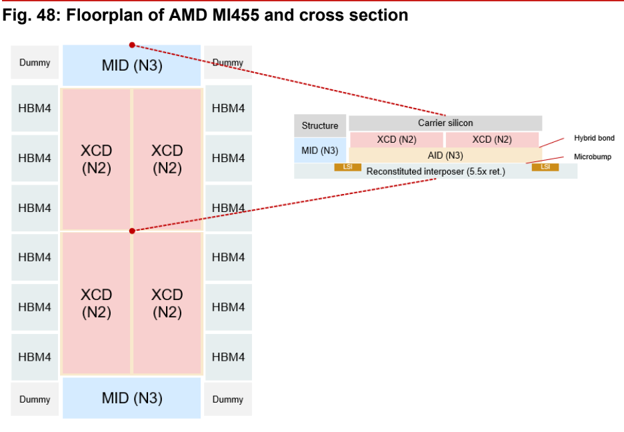

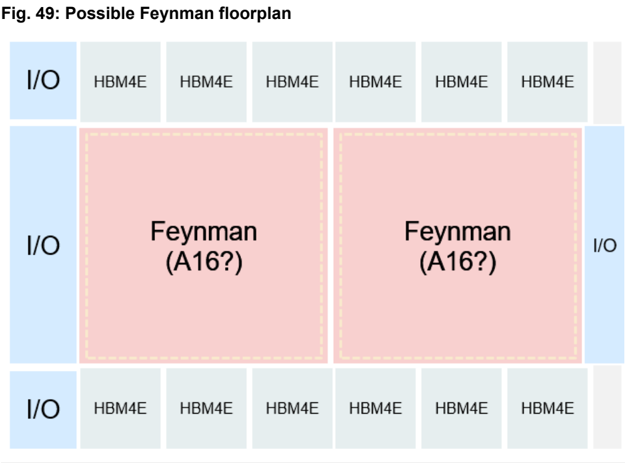

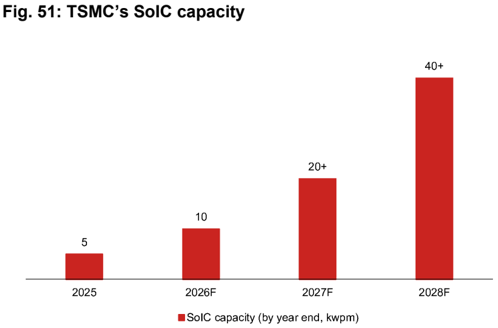

Now, it appears to us that TSMC has turned more aggressive on its advanced packaging investments. C.C. Wei, the company's chairman, made it clear during TSMC's April 2026 earnings call that the company 'works very hard to meet all the demand' and 'doesn't leave any business on the table'. During its 2026 North America Symposium in Apr i l , TSMC launched its 14x reticle size CoWoS roadmap (by 2028E; Fig. 46 ) vs a prior roadmap of up to 9.5x reticle size (2027E; Fig. 45 ). However, our view is that SoIC and CoPoS are two equally critical technologies for TSMC to stay ahead of its competition in advanced packaging. We previously wrote that the CoPoS will enter mass production in 2029F, but we hope TSMC could pull this forward and ramp it along with the Feynman timeline (2H28F). What's more, we expect Feynman to target the first-ever GPU-on-GPU SoIC stack -which would lead to higher computational power even with limited growth in interposer reticle stitching size. Our latest study suggests a Feynman interposer reticle size at c.6x (footprint in Fig. 49 ; up from c.5x from Rubin) by using SoIC. We believe there would be multiple implications from this: first, the bigger footprint and high TDP of Feynman would start to drive the adoption of SiC (an upgrade of carrier silicon - concept and location illustrated in Fig. 52 , a cross-sectional view of AMD MI300); second, SoIC capacity demand would skyrocket through 2028-29F. We expect SoIC capacity to double in 2027F (mainly driven by nVidia's CPO) and double again in 2028F (mainly driven by nVidia's Feynman, see Fig. 51 ).

All together, we largely keep our structurally bullish stance and reiterate our Buy ratings on TSMC, ASE, MediaTek, ASPEED, GWC, KYEC, EMC, TUC, and ZDT with higher target prices. We would be mindful about rising volatility from component supply mismatches and the macro yield rate outlook. Structurally, we look forward to full-year 2028F global new data center build visibility over the next 3-6 months. In the upstream semiconductor space, we also like BESI for CPO and GPU-on-GPU SoIC opportunities, Soitec for SOI wafers in CPO, and Samsung Electronics for its memory leadership.

Within the downstream space, we reiterate our Buy rating on Unimicron, as we think its IC substrate business will be a top beneficiary of multiple future trends, such as EMIB-T, CoPoS, and CPO. We like CCL companies, such as EMC and TUC, as we expect them to continue to benefit from supply tightness (with price-hike potential), material upgrades from low-loss requirements for future AI PCBs, and increasing numbers of peripheral boards such as CPUs and switches in addition to AI GPU/ASIC boards.

For the PCB sector, we reiterate our Buy ratings on ZDT and Compeq. We think the strong growth of optical module mSAP boards will be margin-accretive growth drivers for Unimicron, ZDT and Compeq. For AI PCB/HDI, we believe the increasing number of boards for AI GPU/ASIC/networking/CPU and spec upgrades will fuel the growth of the AI PCB market, benefiting ZDT and Unimicron. ZDT is an emerging AI PCB/HDI maker, and is well positioned to penetrate into nVidia, Google, and AWS's PCB/HDI more

meaningfully from 2H26F, in our view.

For the power supply sector, we believe recent concerns about a delay in 800VDC shipments have been overdone and reiterate our Buy rating on Delta, as we believe it will be a leading supplier for the upcoming +/-400VDC project ramp-up from 2H26F and we believe the +/-400VDC volume, if ramped up smoothly, will be substantial enough to beat market expectations on HVDC in 2027F (not much contribution needed from 800VDC). For thermal plays, our top pick is AVC, and we expect the ramp-up of VR200 and Trainium 3 and its new penetration into Google's TPU will be positive catalysts in 4Q26F.

Global new data center build tracking

Steady stream of project rollouts to provide robust latent hardware demand over next 2-3 years, in our view

Projects have been announced in succession with GW-scale

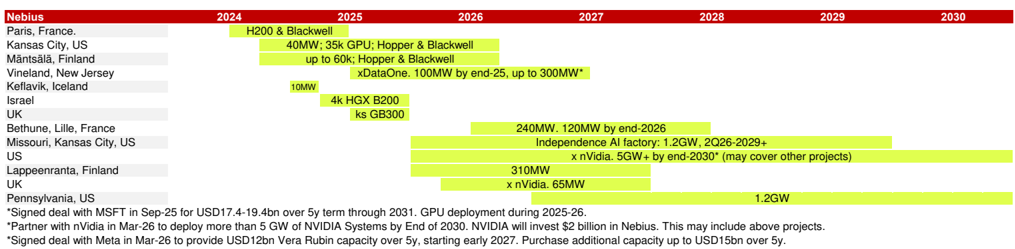

Since our last update at end-March (report ), we have continued to see more projects rolling out, and our datacenter project universe has increased from ~240 to ~280. Notably, we see some GW-scale projects such as Nebius's (NBIS US, Not rated) 1.2GW data center project in Pennsylvania (news ), Softbank's (9984 JP, Buy) 5GW project in France (press ), and SK Telecom's (SKM US, Not rated) gigawatt-scale AI cloud in Korea. By project owner, we see fewer GW-scale projects announced by the top-4 CSPs in this update. However, we still observe these hyperscalers investing globally, such as Microsoft's (MSFT US, Not rated) investment plans in Singapore, Japan, and Australia; Google's investment plans in Austria, Missouri (US) and Sweden; Meta's (Meta US, Not rated) investment plans in Tulsa, Oklahoma (US), and AWS's investment plan in France. That said, less new projects from top-4 CSPs announced with GW-scale, either no disclosure on capacity or with smaller scale.

Our selected GW-scale projects increased to ~50 this time. Similar to our March update , we see more projects supporting stronger hardware deployment in 2027F, and as time goes by, we also see more projects spanning into 2028F. The incremental capacity deployment is 32GW/23GW in 2027F/2028F from these handpicked projects, on our estimates (vs 28GW/21GW last time), indicating demand for 4-6mn AI chips per year (Fig. 3 ).

To better capture potential hardware demand, we further review the rest of the projects within our sample universe. For the rest of the projects, excluding 'shell-only' projects, there are ~40 projects smaller than 1GW in scale, and ~100 projects for which power consumption has not been disclosed. The average power consumption of small projects is 300MW, and we simply assume the rest of the projects to be 100MW each, which could represent an additional 20GW+ in hardware demand. 20GW is equivalent to 3-4mn Rubin chips, or 420k CoWoS demand throughout the deployment period.

Some projects halted

However, we also note some projects have ceased: Crusoe (unlisted) announced on 10 June that it will cease the expansion of Project Jade on a client request, a 1.8GW (up to 10GW) project. We have removed this project from our calculation base. It was also reported on 10 May that Microsoft and G42's (unlisted) USD1bn data center project in Kenya had been halted on payment issues. Our simulation this time reflects these developments.

China ecosystem is also aggressively accelerating datacenter build-outs

We acknowledge the aggressive expansion intention in China, through both national strategies and massive capital expenditures by technology giants. In June 2026, Bloomberg News reported (link ) that China's government has drafted an unprecedented nationwide AI computing network plan, aiming to invest USD295bn (~CNY2tn) over the next five years to achieve a fully interconnected national grid of distributed data centers by 2028 (report ). Besides the announcement, notable datacenter infrastructure activities in China include:

- Eastern Data and Western Computing: announced in May 2021. The plan proposed a new computing network system that integrates data centers, cloud computing, and big data, as well as Eastern Data and Western Computing demonstration projects that will enable high-quality, green data centers. ·

- Chindata Group (unlisted): The company continues to announce datacenter projects. Several years ago, it announced that the Taihang Mountain Energy and Information Technology Industrial Campus in Datong, Shanxi went into operation (ba ck in Oct 2020 ). Recently, the company also announced a partnership with HEC Group (600673 SH, Not rated) for new AI compute projects. ·

However, we do not specifically include these China data center projects in our calculation base, as these projects are likely aiming to adopt domestic compute chips, which are less relevant to our CoWoS capacity estimates. Although companies such as Chindata Group have also announced data centers beyond China (in regions such as Malaysia ), the scale is relatively small, and they are not included in our selected samples.

Fig. 2: Major data center infrastructure buildouts

Source: Company data, Nomura research

Fig. 3: Our back-of-the-envelope calculation on GW deployment trends

We see growing GW deployments into 2026-28F

| 2025F | 2026F | 2027F | 2028F | 2029F | 2030F | |

|---|---|---|---|---|---|---|

| Incremental capacity deployment (GW) | 5.98 | 26.70 | 32.30 | 22.85 | 16.85 | 6.76 |

| - OpenAI | - | 3.50 | 7.50 | 8.50 | 6.50 | - |

| - OpenAI (%) | 0% | 13% | 23% | 37% | 39% | 0% |

| - Top 4 CSPs | 2.35 | 8.58 | 6.97 | 1.56 | 0.93 | 0.93 |

| - Top 4 CSPs ((%) | 39% | 32% | 22% | 7% | 6% | 14% |

| - Others | 3.63 | 14.61 | 17.83 | 12.78 | 9.43 | 5.83 |

| - Others (%) | 61% | 55% | 55% | 56% | 56% | 86% |

From GW to Chips

Computing power % as an infra

Chip (W)

GB300

VR200

Rack power incl. redundancy (kW)

GB300 NVL72

VR NVL72

70%

TDP

1,400

2,300

180

266

Racks # per GW

3,895

2,630

Chips # per GW (k)

280

189

| 2025F | 2026F | 2027F | 2028F | 2029F | 2030F | |

|---|---|---|---|---|---|---|

| Incremental capacity deployment (GW) | 5.98 | 26.70 | 32.30 | 22.85 | 16.85 | 6.76 |

| Assume all are GB300 for 2024-26F: | ||||||

| Implied chip demand (k) | 1,678 | 7,487 | ||||

| Implied CoWoS demand (k/16) | 105 | 468 | ||||

| Assume all are VR for 2027-30F: | ||||||

| Implied chip demand (k) | 6,118 | 4,327 | 3,192 | 1,280 | ||

| Implied CoWoS demand (k/9) | 680 | 481 | 355 | 142 |

Source: Nomura estimates

ve nave sechmure projeul vundoulo Uvel tie paol

35

30

25

20

15

10

5

Fig. 4: Incremental capacity deployment (GW)

We have seen more project buildouts over the past several months

Note: Adjusted: We removed same infrastructure projects for better comparison.

Source: Nomura research

CSPs are scrambling for compute capacity

Neoclouds continue to play a role

Back in March , we mentioned that nVidia had signed deals with CoreWeave (CRWV US, Not rated) and Nebius in 2026 to deploy 5GW+ AI infrastructure each by 2030. nVidia also invested USD2bn in each of the companies. We also pointed out that in March, IREN (IREN US, Not rated) only announced a purchase agreement with nVidia. Not surprisingly, in May-2026, IREN and nVidia further announced a similar deal, under which two companies will deploy up to 5GW nVidia DSX-aligned AI infrastructure overtime. Furthermore, IREN has issued a five-year right for nVidia to purchase up to 30mn shares of ordinary stock of IREN. Note that for these three deals, we record individual projects for IREN and recorded 5GW as a whole for CoreWeave and Nebius, as IREN's projects are larger and clearer, and the two others are relatively scattered. We note Meta also expanded the deal with CoreWeave in Apr-26, when it signed a long-term agreement for AI cloud capacity that will last until Dec 2032, with a USD21bn deal value (initial deployments will be nVidia Vera Rubin platforms).

We believe neocloud is in an attractive position as a favorable choice for CSPs to access computing capacity, given that CSPs can: 1) shorten lead time (compared to CSPs' own buildouts); 2) gain faster access to the latest technologies (some neoclouds have priority to the latest AI chips); 3) mitigate risks for demand erosion; and 4) in part provides some financial flexibility. Also, during platform transition periods, CSPs may not be willing to expand more capacity for current generation chips, but still need tokens to fill the gap before new generation chips are ready, thus turning to neo clouds.

In the meantime, we see these agreements to turn into real orders. In Nov-25, when IREN announced a multi-year agreement with Microsoft (USD9.7bn), it also entered into an agreement with Dell (DELL US, Not rated; USD5.8bn) to purchase GPUs and ancillary equipment. In Mar-26, IREN announced another USD3.5bn purchase agreement with Dell. In May-26, IREN separately signed a five-year AI infrastructure cloud service contract with nVidia (USD3.4bn), and then announced to purchase USD1.6bn GPUs from Dell to support this USD3.4bn contract. These announcements are encouraging, in our view, as they indicate real hardware demand.

Shell-only projects gradually find their tenants

We removed some shell-only projects in our March update for conservativism, and we keep the same approach this time for our calculation base. However, we note that more shell-only (campus-only) projects have found tenants. For example, Applied Digital (APLD US, Not rated) continued to announced new lease deals for its data center campuses. CoreWeave is one of the lessee named . Lodha Developers (LODHA NS, Not rated) mentioned Amazon when it announced a data center plan in Jan-26, and Meta also announced that it had signed a lease deal with Reliance (RELIANCE NS, Not rated) for

168MW capacity within two years in June-26. These lease agreements boost confidence in potential hardware demand.

Cipher (CIFR US, Not rated) is another name frequently mentioned, and we also classified the company's projects as 'shell-only'. That said, we see more engagements between the company and hyperscalers. Its Barber Lake campus partners with Google and Fluidstack (unlisted), and the company has also signed lease contract with Amazon ( press ). Cipher also further announced that it had signed a new 15-year data center campus lease in Mar-26 with an undisclosed hyperscale tenant. As of June-26, Cipher already contracted 700MW capacity.

Similar to Core Scientific (CORZ US, Not rated) and Hut 8 (HUT US, Not rated), Cipher is pivoting from crypto mining companies to AI/HPC datacenter landlords. Hut 8 also announced AI data center lease deal for its River Bend Campus and Beacon Point Campus . These companies have competitive advantages in securing land, robust grid interconnections, and power capacities. IREN is another similar player that has transformed from Bitcoin miner to AI infra player, but IREN not only acts as colocation landlord, it also purchases GPUs directly.

From our understanding, the supply chain could be:

Power and land developers secure land/water/electricity as well as authority approval, then infrastructure companies build shells and facilities (Level L0/L1). ODMs are L2. Hardware buyers such as CSPs/Neo clouds/LLM players are L3/L4. In a neo-cloud leasing business model, companies such as CoreWeave become L0/L1 companies' tenants, purchase hardware (either through or not through L2), and then sign computing power deals with hyperscalers/LLM players (L3/L4). Note that the distinctions between each layer have been blurring, and some companies such as IREN operate hybrid business models in different projects. The simple classification (L0-L4) is just for better understanding of business model and supply chain.

Some examples of the value chain:

- Applied Digital builds campus, CoreWeave leases campus, purchases GPUs from nVidia, and sells computing power to hyperscalers. We only record CoreWeave's agreement with nVidia's 5GW GPU as a ceiling. ·

- IREN, through Dell, built its own data center, and sold computing power to Microsoft and nVidia. We record individual projects given scale (>1GW) and clarity. ·

In our sample collection for CoWoS demand calculation, we do not include projects without tenants, and do not necessarily include all L0/L1 projects with lease contracts to avoid double count. That said, we view more tenants disclosed a positive sign for future hardware demand.

SpaceX - a new source of computing power?

As discussed in our Global Satellites report , SpaceX (SPCX US, Not rated) has entered into computing capacity supply agreements with third-parties to fully utilize/monetize its datacenter capacity. This kind of business model may become more common, in our view. Companies with more capital/resources on hand may aggressively build own datacenter, while if not fully utilized for internal operations and models, they can in turn rent this capacity out to those who urgently need immediate access of computing power, and enhance the clusters' Model FLOPS Utilization (MFU).

SpaceX entered into Cloud Service Agreements with Anthropic (unlisted) in May 2026. Anthropic is able to access the compute capacity across Colossus and Colossus II, paying USD1.25bn per month through May 2029, with capacity ramping up in May and June 2026 at a reduced fee. SpaceX would retain its ownership and intellectual property rights in its content, AI models, and related data. Through the structure, SpaceX could still reallocate the capacity for its own internal initiatives if needed in the future, according to the prospectus. SpaceX believes that it has sufficient capacity to provide compute for its AI models, and expects to enter into more similar contracts for compute capacity with third parties.

On 5 June 2026, SpaceX announced that it had signed multi-year Cloud Service Agreements with Alphabet, in which Google would pay USD920mn each month starting October 2026 to June 2029 to lock in SpaceX's compute capacity.

MO UI MUI LU<U

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

— Other

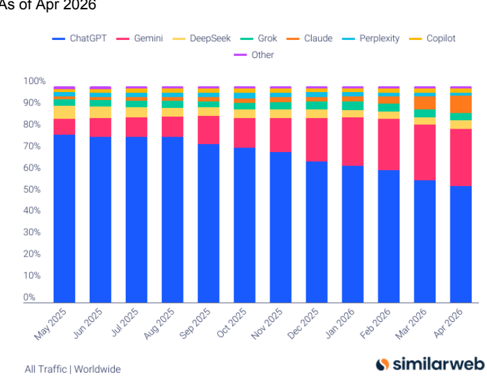

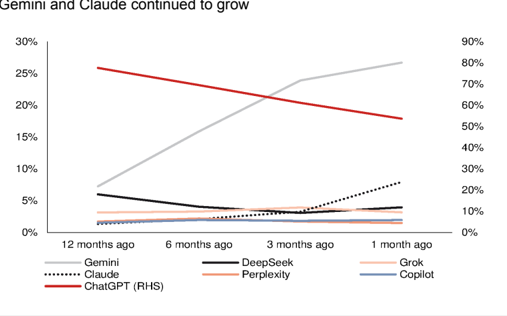

Anthropic is growing strongly and worth tracking

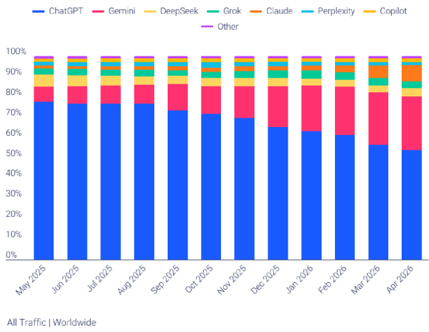

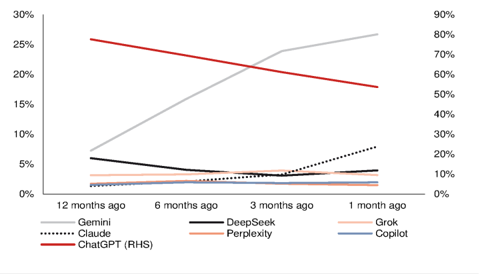

Following ChatGPT's strong breakthrough and Gemini's emergence, Claude is also gaining traction in the market (Fig. 5 - Fig. 6 ). This is also reflected in Anthropic's revenue the run-rate of which surged from USD9bn at the end of 2025 to >USD47bn in May 2026. We also see increasing engagements with a sizable amount of deals between Anthropic and other key players in the AI world. Just as OpenAI's (unlisted) aggressive Stargate announcement, Anthropic in Nov-25 announced a USD50bn investment in American computing infrastructure, building datacenters with Fludistack in Texas and New York. The investment amount shall cover most below computing power purchase agreements, as well as its collaboration with Hut 8 and Fluidstack, in our view.

AWS and Anthropic's relationship can be traced back to 2023-24, when Amazon made USD4bn investments each in 2023 and 2024. Since then, AWS has continued to be Anthropic's major cloud partner. One of AWS's key data center projects, Project Rainier , was the result of this collaboration. Anthropic actively used Project Rainier (featuring 500k Trainium 2 chips) to build and deploy Claude. In Apr-26, it expanded the deal, and Anthropic signed a new agreement with Amazon to secure up to 5GW capacity for training and deploying Claude. In the same agreement, Anthropic is to commit more than USD100bn over the next ten years to AWS technologies, spanning Graviton and Trainium 2/3/4, with the option to purchase future generations when available. Built on the existing USD8bn investments, Amazon is investing USD5bn in Anthropic along with the announcement in Apr-26, up to an additional USD20bn in the future.

Google was also an early investor of Anthropic from 2023 to early 2025. The relationship extended when Anthropic announced it would expand adoption of Google Cloud technologies, including up to 1mn TPUs (over 1GW capacity online in 2026) in Oct-25. In Apr-26, Anthropic announced that it signed a new agreement with Google and Broadcom (AVGO US, Not rated) for multiple gigawatts of next-generation TPU capacity coming online starting in 2027. While not officially announced, Google reportedly will invest up to USD40bn in Anthropic, and Anthropic is committed to spending USD200bn with Google Cloud over five years.

Note that besides AWS and Google ASICs, Anthropic also bonded relationship with other players on nVidia GPU platforms.

- In Nov-2025, Anthropic, nVidia and Microsoft announced strategic partnerships, when Anthropic committed to up to 1GW nVidia GB/VR systems. nVidia and Microsoft were committed to invest up to USD10bn and USD5bn, respectively, in Anthropic. Although this has not yet been officially confirmed by the companies, news outlets have reported than Microsoft is negotiating with Anthropic to serve its in-house ASICs as well. ·

- Anthropic also utilized compute capacity from SpaceX/xAI's Colossus for Claude (based on nVidia GPUs), as mentioned in above paragraphs. ·

- CoreWeave announced a multi-year agreement with Anthropic in Apr-26. The collaboration between Anthropic and CoreWeave will initially focus on a phased infrastructure rollout, with the potential to expand over time. ·

Fig. 5: Gen AI website traffic share

As of Apr 2026

Source: Similarweb, Nomura research

Fig. 6: Gen AI website traffic share Gemini and Claude continued to grow

Source: Similarweb, Nomura research

— Perplexity - Copilot

Demll allu vlauue bolltmluel lu gruw

30%

1 month ago

Grok

Copilot

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

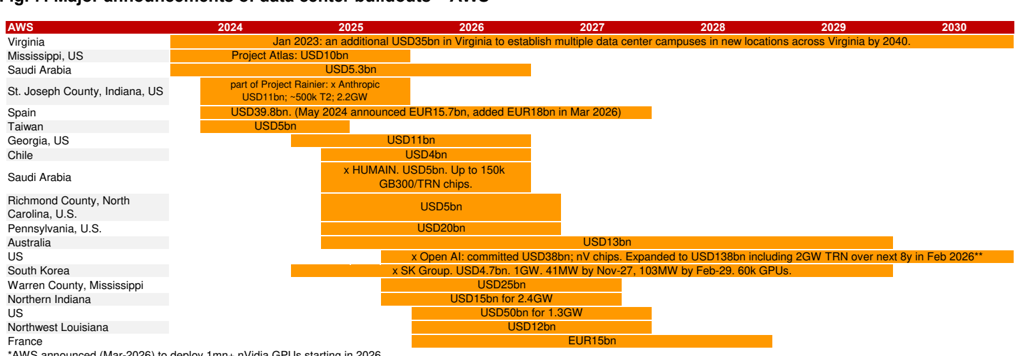

Fig. 7: Major announcements of data center buildouts - AWS

*AWS announced (Mar-2026) to deploy 1mn+ nVidia GPUs starting in 2026

Source: Company data, Nomura research

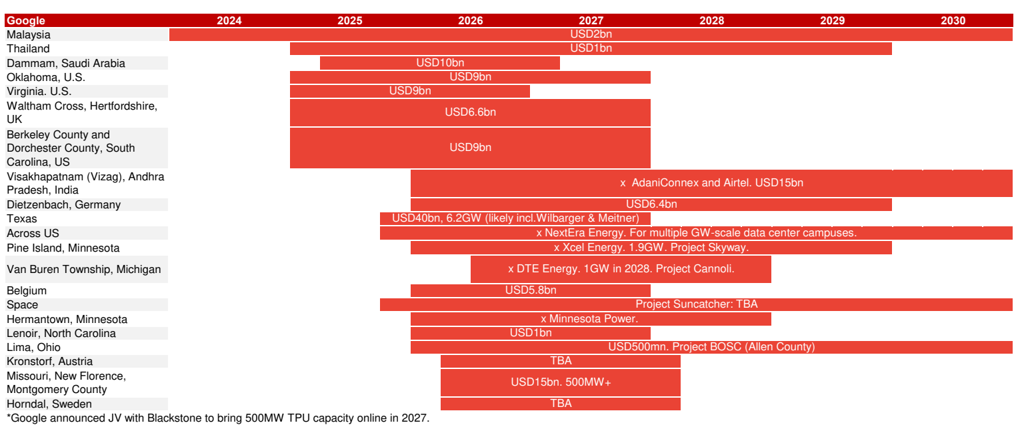

Fig. 8: Major announcements of data center buildouts - Google

Source: Company data, Nomura research

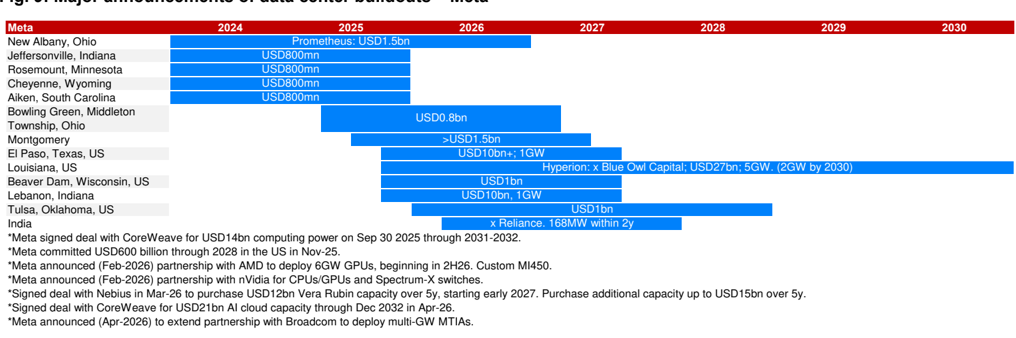

Fig. 9: Major announcements of data center buildouts - Meta

Source: Company data, Nomura research

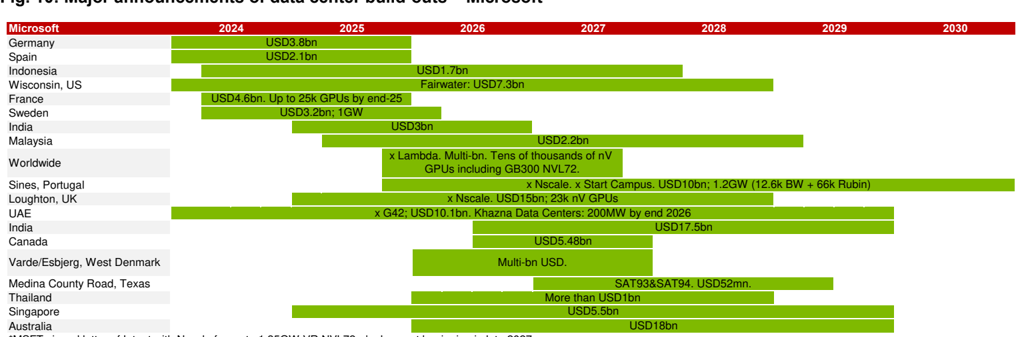

Fig. 10: Major announcements of data center build-outs - Microsoft

*MSFT signed letter of Intent with Nscale for up to 1.35GW VR NVL72, deployment beginning in late 2027.

*Crusoe announced to build 900MW datacenter for MSFT in Abilene, Texas on 27 March 2026. The first building expected to be energized in mid-2027.

Source: Company data, Nomura research

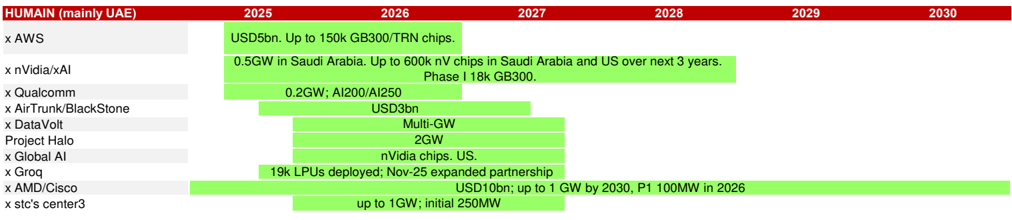

Fig. 11: Major announcements of data center build-outs - HUMAIN

Source: Company data, Nomura research

Fig. 12: Major announcements of data center buildouts - CoreWeave

Source: Company data, Nomura research

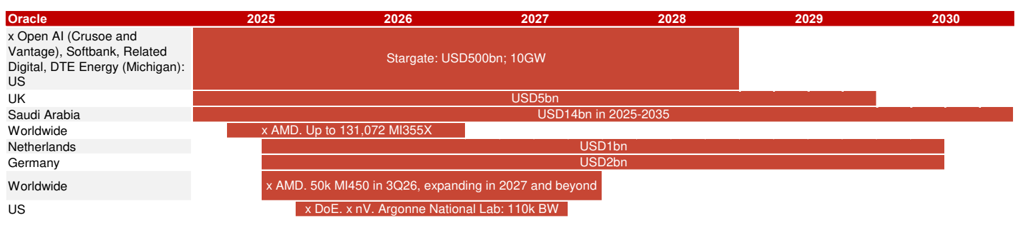

Fig. 13: Major announcements of data center buildouts - Oracle

Source: Company data, Nomura research

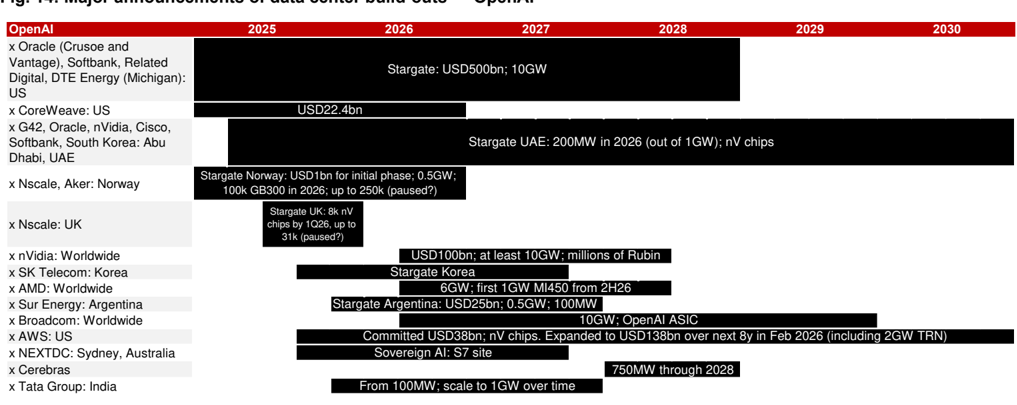

Fig. 14: Major announcements of data center build-outs - OpenAI

Source: Company data, Nomura research

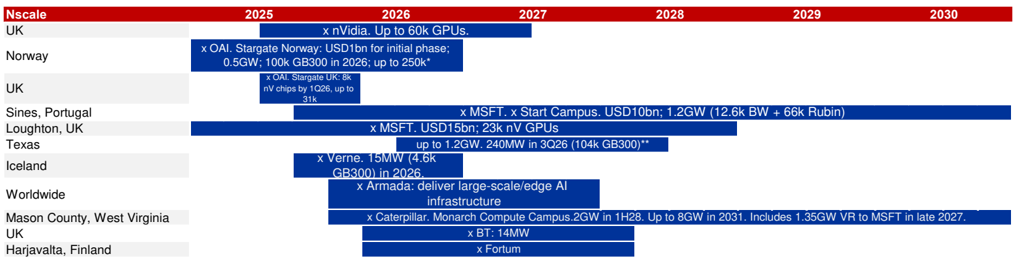

Fig. 15: Major announcements of data center build-outs - Nscale

Source: Company data, Nomura research

Fig. 16: Major announcements of data center build-outs - Nebius

Source: Company data, Nomura research

Source: Company data, Nomura research

unparlorol

(kpcs)

600

500

400

300

200

100

0

(kpcs)

2,000

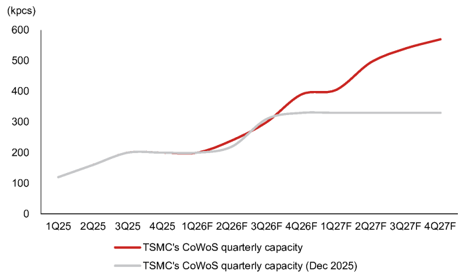

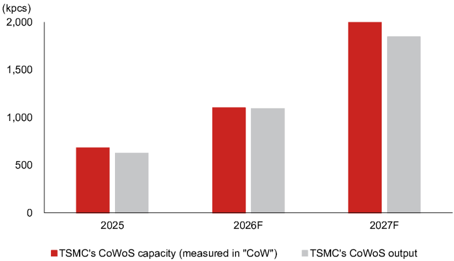

TSMC turning aggressive on 2027F CoW capacity, but WoS will become bottleneck, in our view

TSMC has turned aggressive in responding to surging demand and to defend against (future) competition

In our last update in December , we flagged TSMC's intention to dial up its CoWoS capacity build-out in 2026F by expediting equipment delivery, in response to nVidia's request (although ~60% of TSMC's CoWoS capacity has already been booked by nVidia) and ASIC customers' (led by Broadcom) eagerness to secure more capacity support. Despite this, we believe TSMC would still keep a disciplined stance on its CoWoS capacity additions and will not overreact to customers' 'potentially inflated' demand forecasts, and likewise for TSMC's fabrication capacity despite a likely 3nm demand surge in 2026F due to a somewhat 'synchronized' large-die AI chip migration cadence (e.g., nVidia's Rubin, Google's TPU v8t/v8i and AWS' Trainium 3).

To date, TSMC's supply is apparently still constrained across the front-end and the back-end given the demand strength from AI, and the company has expressed its commitment to expand its capacity in due course, citing that it 'works very hard to meet all the demand ' and 'doesn't leave any business on the table ' (see remarks from 4Q25 and 1Q26 results ). Interestingly, TSMC's management has decided to step up capex investment to increase its 3nm capacity - in contrast to its old plan, in which TSMC did not add new capacity to a node once it reached the target capacity (about 130-150kwpm, in our view) - with additions in Taiwan, Japan, and the US. TSMC has laid out its plan to drive N5/N3 combined capacity growth (a 25% CAGR over 202227E) with equipment commonality and technology integrations (see our takeaways from the Technology Symposium ).

Our latest supply chain survey suggests TSMC will likely expand its CoWoS capacity to 1,100kpcs in 2026F (or c.130kwpm by the end of 2026F) vs our previous assumption of 1,0501,100kpcs (or c.110kwpm by year-end), increasing this to 2,000kpcs in 2027F vs our previous assumption of 1,300-1,350kpcs. Although TSMC has turned more aggressive in its CoWoS plan (more precisely, its 'CoW' plan), our contrarian view is that 'WoS' (not controlled by TSMC) and many small components would very likely become a bigger bottleneck than 'CoW' (controlled by TSMC) in 2027F. We only model 1,800kpcs of CoWoS output in 2027F (despite our assumption of a TSMC target of 2,000kpcs).

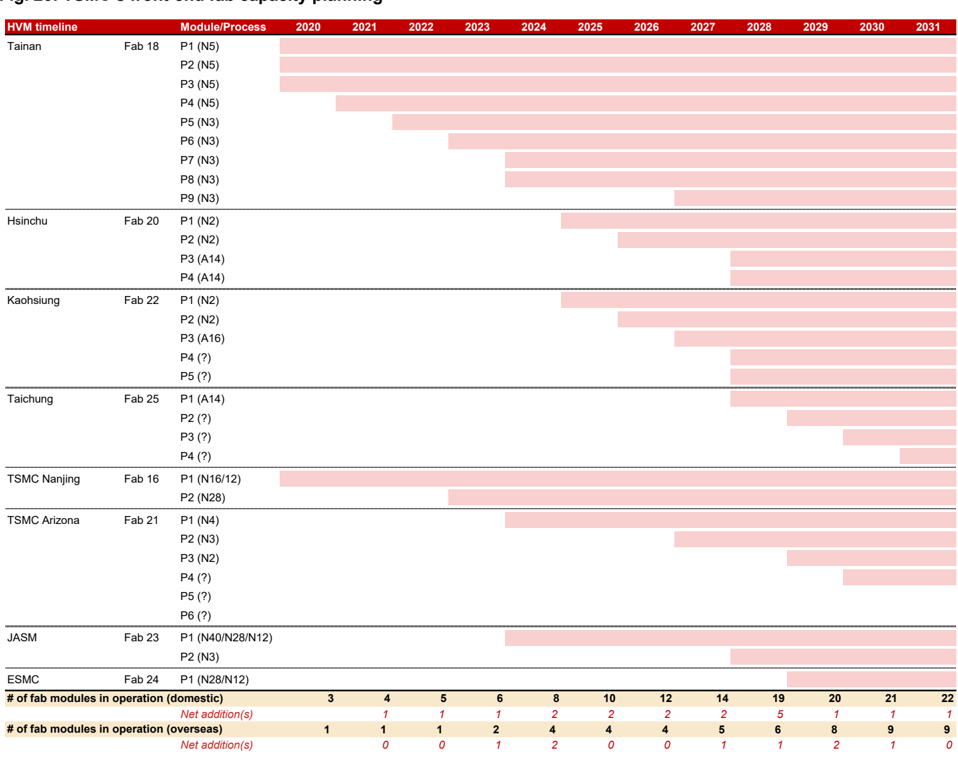

At the front end, we model TSMC to form 160kwpm 3nm capacity by end-2026F (from 130kwpm by end-2025, mostly driven by cross-node conversion) and 175kwpm by end-2027F. We expect 225kwpm of 3nm capacity by end-2028F, with the fabs in Arizona and Kumamoto joining the production lineup. All told, we reason the magnitude of capacity builds remains prudent, judged by not only the 'demand forecasts' of AI chip customers (which occasionally could be misleading against the backdrop of shortage), but more importantly by new data center build trackers (elaborated on in the 'Global new data center build tracking ' section of this report, which we view as a leading indicator beyond Asia supply chain data points). Also see the below section, 'When the elephants fight, the grass gets trampled for our refreshed view on TSMC's AI revenue, CoWoS allocation assumptions and competitive landscape observations in terms of AI chips.

Fig. 18: TSMC turning more aggressive on CoW capacity expansion

Source: Company data, Nomura estimates

Fig. 19: But the output will be constrained by "WoS"

Source: Company data, Nomura estimates

2027F

TSMC's CoWoS output

Fig. 20: TSMC's front-end fab capacity planning

| HVM timeline | Module/Process | 2020 2021 | 2022 2023 | 2024 | 2025 2026 | 2027 | 2028 | 2030 | 2031 | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Fab 18 | P1 | Tainan (N5) | |||||||||||

| P2 (N5) | |||||||||||||

| P3 (N5) | |||||||||||||

| P4 (N5) | |||||||||||||

| P5 (N3) | |||||||||||||

| P6 (N3) | |||||||||||||

| P7 (N3) | |||||||||||||

| P8 (N3) | |||||||||||||

| P9 (N3) | |||||||||||||

| Hsinchu | Fab 20 | P1 (N2) | |||||||||||

| Hsinchu | P2 (N2) | ||||||||||||

| Hsinchu | P3 (A14) | ||||||||||||

| Hsinchu | P4 (A14) | ||||||||||||

| Kaohsiung | Fab 22 | P1 (N2) | |||||||||||

| Kaohsiung | P2 (N2) | ||||||||||||

| Kaohsiung | P3 (A16) | ||||||||||||

| Kaohsiung | P4 (?) | ||||||||||||

| Kaohsiung | P5 (?) | ||||||||||||

| Taichung | Fab 25 | P1 (A14) | |||||||||||

| Taichung | P2 (?) | ||||||||||||

| Taichung | P3 (?) | ||||||||||||

| Taichung | P4 (?) | ||||||||||||

| TSMC Nanjing | Fab 16 | P1 (N16/12) | |||||||||||

| TSMC Nanjing | P2 (N28) | ||||||||||||

| TSMC Arizona | Fab 21 | P1 (N4) | |||||||||||

| TSMC Arizona | P2 (N3) | ||||||||||||

| TSMC Arizona | P3 (N2) | ||||||||||||

| TSMC Arizona | P4 (?) | ||||||||||||

| TSMC Arizona | P5 (?) | ||||||||||||

| TSMC Arizona | P6 (?) | ||||||||||||

| JASM | Fab 23 | P1 (N40/N28/N12) | |||||||||||

| JASM | P2 (N3) | ||||||||||||

| ESMC | Fab 24 | P1 (N28/N12) | |||||||||||

| # of fab modules in operation | # of fab modules in operation | Net addition(s) (domestic) | 3 | 5 1 | 6 1 | 8 2 | 10 2 | 12 2 | 14 2 | 19 5 | 20 1 | 21 1 | 22 1 |

| # of fab modules in operation (overseas) | # of fab modules in operation (overseas) | # of fab modules in operation (overseas) | 1 | 1 | 2 | 4 | 4 | 4 | 5 | 6 | 8 | 9 | 9 |

| Net addition(s) | 0 | 1 | 2 | 0 | 0 | 1 | 1 | 2 | 1 | 0 |

Source: Company data, Nomura estimates

How will TSMC's CoWoS capacity shape up through 2029F?

While we have no clear bottom-up estimates about how TSMC is going to expand its CoWoS capacity beyond 2027F, we try to triangulate a possible trajectory based on TSMC's AI semi growth guidance and our assumptions of manufacturing content added. See Fig. 21 for our simulation.

TSMC guided its AI accelerator revenue would grow to a high-50% CAGR over 2024-29E, implying USD115bn of revenue from AI by 2029E. Additionally, we generalize from our proprietary TSMC AI logic semi model, which analyzes major AI accelerator revenue contributions, that roughly 30-35% of its manufacturing content comes from advanced packaging. For simplicity, we assume all the advanced packaging revenue to TSMC comes from CoWoS (e.g., ignoring SoIC, which is an accretion to back-end content). Altogether, TSMC's guidance might hint to form 2,500-3,500kpcs in annual CoWoS capacity by 2029F, vs 680kpcs in 2025, and this would suggest a 40-50% capacity CAGR over 2025-29F compared to a >80% CAGR planned for 2022-27E (report ).

Fig. 21: A simulation of TSMC's long-term CoWoS capacity planning

| USD mn | 2023 | 2024 | 2025 | 2026F | 2027F | 2028F | 2029F |

|---|---|---|---|---|---|---|---|

| TSMC's revenue | 69,298 | 90,083 | 122,424 | 274,911 | |||

| Revenue from AI | 3,921 | 11,692 | 22,131 | 115,126 | |||

| AI revenue% | 6% | 13% | 18% | 42% | |||

| Content breakdown assumption | |||||||

| Fabrication | 70% | 70% | 70% | 70% | |||

| Packaging | 30% | 30% | 30% | 30% | |||

| Imputed AI packaging revenue | 1,176 | 3,508 | 6,639 | 34,538 | |||

| Assumed CoWoS price/wafer | 10,000 | 10,000 | 10,000 | 11,000 | 12,100 | 12,100 | 12,100 |

| Imputed CoWoS output (kpcs) | 118 | 351 | 664 | 2,854 |

Source: Company data, Nomura estimates

A question stemming from the above-mentioned long-run analysis is how TSMC would build its CoWoS capacity in view of an ultimate transition to CoPoS. While, again, we do not have any clear bottom-up estimates since the CoPoS platform remains in the R&D stage at this moment, we have attempted some 'napkin math' about the capacity formation trade-off. TSMC's current AI revenue guidance with our assumed 30-35% content from back-end in 2029E should imply c.USD35bn from AI chip advanced packaging, and nVidia alone could consume ~1,400kpcs of CoWoS capacity if it keeps on securing ~50% of the supply.

- If we tentatively assume the Feynman GPU has an interposer sizing up to 6x reticle (vs Rubin's ~5x reticle) and all the capacity taken by nVidia in 2029E is directed for Feynman production, then the total Feynman output would be 11.4mn units. ·

- The 6x reticle size interposer yields about 8 units on a round 300mm carrier. If the same interposer is produced on a square 300mm panel carrier, each carrier could output about 15 units. We note that AMD believes interposers at >8x reticle size are moving toward panel level packaging for better economics (report ); our 'napkin math' shows that for an 8x reticle size interposer, a round 300mm carrier outputs 5-6 units vs 9-10 units on a square 300mm panel. ·

- If all the 11.4mn Feynman unit outputs move from CoWoS to CoPoS (310x310mm), we believe TSMC would have to prepare 700-800k panels of CoPoS annual capacity instead of c.1,400kpcs of CoWoS for nVidia in 2029E. ·

Although the simulation might be radical, it explains to a certain extent why TSMC has been very prudent with its CoWoS capacity investments that may face a long-run migration to CoPoS, which could result in a huge chunk of spare CoWoS capacity.

Fig. 22: Sensitivity of TSMC's CoWoS capacity planning

| kpcs | Packaging content in AI | Packaging content in AI | Packaging content in AI |

|---|---|---|---|

| 2,854 | 30% | 35% | 40% |

| USD 12,100 | 2,854 | 3,330 | 3,806 |

| 13,100 | 2,636 | 3,076 | 3,515 |

| 14,100 | 2,449 | 2,858 | 3,266 |

| 15,100 | 2,287 | 2,668 | 3,050 |

| 16,100 | 2,145 | 2,503 | 2,860 |

| 17,100 | 2,020 | 2,356 | 2,693 |

Source: Company data, Nomura estimates

When the elephants fight, the grass gets trampled

nVidia and Google are the elephants in AI Semi

AI semi forecast refresh: nVidia and Google will compete for resources at TSMC in 2026-27F, at the cost of other AI chips, in our view

We review our AI logic semi revenue model (from the perspective of TSMC) and key assumptions to assess the demand trajectory for nVidia and ASIC following upward capacity assumption revisions (see TSMC turning aggressive on 2027F CoW capacity, but WoS will become bottleneck, in our view ).

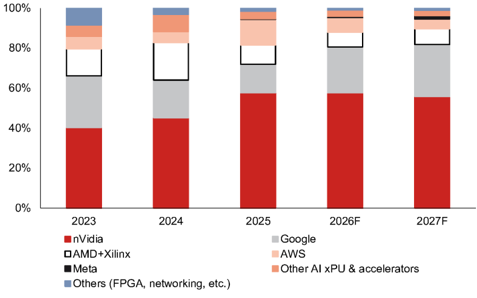

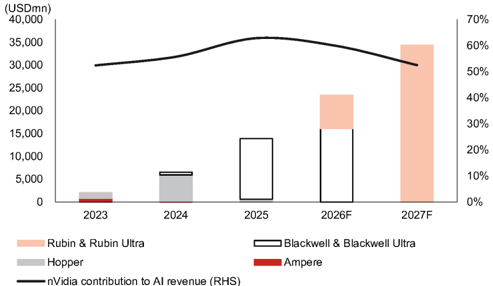

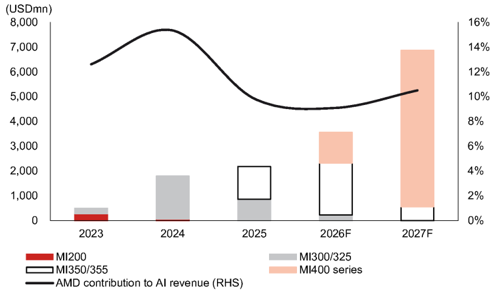

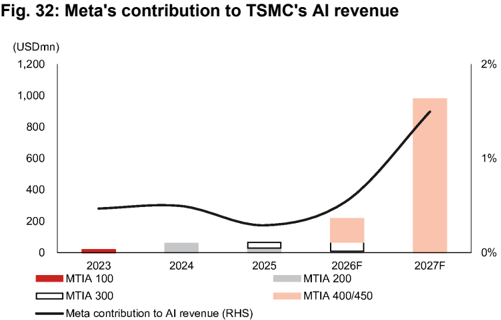

We are raising our 2026F AI semi forecast to 77% y-y growth (from 69% previously) and model 2027F growth of 67% (vs +24% y-y previously), compared to TSMC's AI revenue CAGR guidance of 'toward high-50% CAGR from 2024-29'. See Fig. 35 for a complete summary of our analysis. We estimate AI to make up mid-20% of TSMC's revenue in 2026F (from a high-teens percentage in 2025), further jumping to >30% in 2027F, with nVidia remaining the largest AI revenue contributor at 60%/53% in 2026F/27F (was 56%/51%), followed by Google's 20%/25% (previously 18%/17%). As nVidia and Google together already account for c.80% of TSMC's AI revenue (vs 70-75% a few years ago), the competition between nVidia and Google to secure capacity at TSMC (and possibly elsewhere in the Asia AI supply chain) could come at the cost of other AI chips.

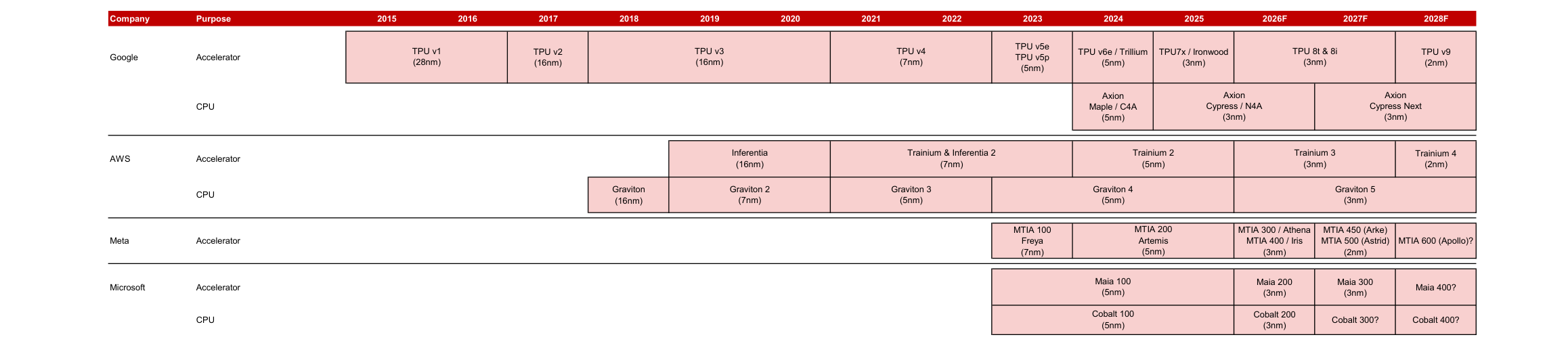

Fig. 23: Hyperscalers' custom silicon roadmap

Source: Company data, Nomura estimates

In our December 2025 projection , we expected TSMC to allocate c.60% of its CoWoS capacity to nVidia in 2026F because of the intention to retain 'strategic resource' to crowd out ASIC supply, and the production mix would shift toward more Blackwell than Rubin. We expected TSMC to allocate more CoWoS capacity to Google TPU (primarily via its design service partner Broadcom) to support the product ramp-up in 1H26F (Ironwood/TPU7x). We then also observed increasing traction in AMD's AI GPUs in the supply chain, after the October 2025 announcement of the strategic partnership between OpenAI and AMD (press release ).

With changes in TSMC's capacity expansion scale and its initial planning for 2027F capacity allocation around the corner, we offer a preview of how TSMC's 2027F AI production mix could shape up, as well as elaborate on our observations about TSMC's major AI customers below nVidia should remain as aggressive, and we suppose Google could be more proactive in securing supply.

- nVidia: We do not expect much change to nVidia's CoWoS capacity bookings at TSMC in 2026F (c.60% of capacity share), but see incrementally lower units of Rubin production, with overall output mix skewing a bit more toward Blackwell. We do not expect Rubin GPU production to ramp up significantly until 4Q26F, which implies that actual rack shipments in mass volume could be even later, and one of the bottlenecks is the HBM4 schedule (report ). Another notable change is the design of Rubin Ultra (slated for production in 2027E, according to nVidia), the floorplan of which could scale down to Rubin-like (2 GPU dies per package) vs prior expectation of two Rubin modules connected on a substrate (CoWoS-L + MCM; four GPU dies per package, see our report about a compromised architecture given unreadiness of CoPoS). Such a change is validated by nVidia's demo of the Kyber compute blade, which accommodates four GPUs (Fig. 62 ) vs the showcase of two GPUs per blade last ·

(kpcs)

2,000

1,500

1,000

500

0

100%

80%

year, implying a smaller package footprint. We assume nVidia to take c.55% CoWoS capacity allocation at TSMC in 2027F, and the AI GPU builds will be completely made of Rubin and Rubin Ultra. We therefore estimate TSMC will generate 60%/53% of its AI revenue from nVidia in 2026F/2027F, recording +68%/+47% growth.

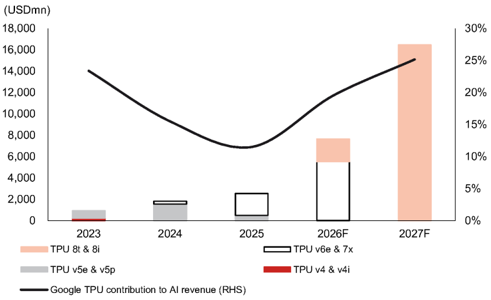

- Google TPU: We continue to expect revenue contribution upside for TSMC from TPU and raise our unit build assumption for TSMC in 2026-27F. We expect 2026F revenue/chip volume upside to come from TPU7x (codenamed Hammer) and TPU v8t (codenamed Mad Dog) vs our December projection, despite lower revenue/volume from TPU v8i (codenamed Hell Cat) because of a slower-thanexpected ramp-up. We believe MediaTek (the ASIC design partner of TPU v8t) will benefit from more aggressive TPU capacity bookings by Google in 2026-27F, while the dynamics in 2028F remain a mystery to us, subject to the execution of Google and Intel's EMIB-T. On the back of more aggressive procurement by Google in 2027F, we estimate Google's TPU contribution to TSMC's AI revenue will grow by 200% (we previously forecasted +120% y-y) in 2026F and +116% in 2027F, and the output by TSMC could translate into 4.2mn/8.3mn TPU builds by Google in 2026F/27F. · · Meta

2025

- AMD: We refresh our underlying spec assumptions for MI455X after AMD demonstrated the chip during CES 2026, featuring an even larger footprint (measured at ~5.5x reticle size CoWoS-L by our estimates) than we had previously thought, with compute chiplets built on TSMC 2nm. We have noticed more positive feedback by ODMs' clients on AMD's MI350/375 systems, and increasing ODM/component supplier interest after the partnership between OpenAI and AMD was announced in late 2025, but the CoWoS ordering momentum by AMD in 2026F turns out a bit softer than we had expected in December 2025. As the Asia AI supply chain is already busy preparing for nVidia Rubin and Google TPU, we observe that AMD might appear to be a lower priority and thus, AMD has fine-tuned its upstream demand forecasts in 2026F. That being said, our supply chain checks indicate AMD remains aggressive with 2027F planning, and could seek more CoWoS allocation at TSMC into 2027F. We project AMD's AI GPUs to contribute 9%/10% of TSMC's AI revenue in 2026F/27F. ·

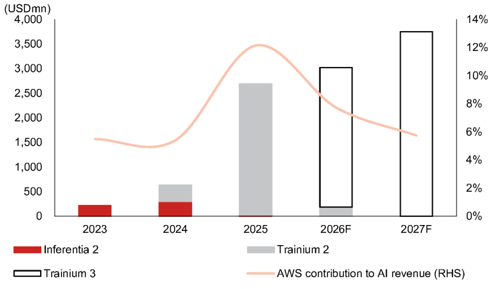

- AWS Trainium: Compared to our AI logic semi model in December, AWS Trainium appears to be another victim in the supply chain suffering from the competition for strategic resources between nVidia and Google. We lower CoWoS capacity allocation assumptions of AWS Trainium in 2026-27F, and estimate AWS's Trainium contribution to TSMC's AI revenue pool to grow 13%/24% in 2026F/2027F (was 56%/14%). ·

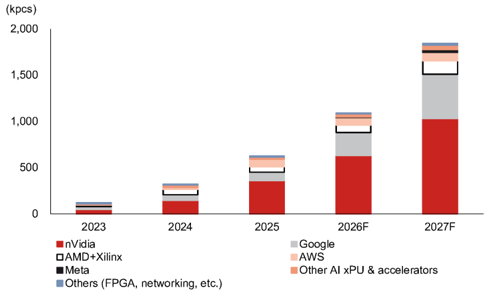

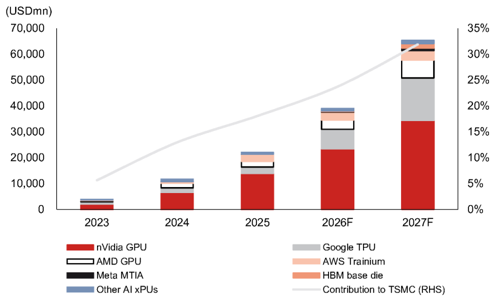

Fig. 24: TSMC's CoWoS output breakdown

Source: Company data, Nomura estimates

Fig. 25: TSMC's CoWoS output allocation

Source: Company data, Nomura estimates

AWS

Other Al XPU & accelerators

2026F

2027F

8,000

35,000

7,000

30,000

60,000

6,000

50,000

5,000

25,000

20,000

40,000

4,000

3,000

30,000

15,000

20,000

10,000

5,000

2,000

1,000

10,000

0

0

0

Rubin & Rubin Ultra

Hopper

Fig. 26: TSMC's AI revenue breakdown

| MI200

→ MI350/355

35%

70%

16%

60%

30%

14%

12%

25%

10%

20%

100%

(USDmn)

(USDmn)

18,000

4,000

3,500

80%

16,000

14,000

3,000

60%

12,000

2,500

10,000

2,000

40%

8,000

6,000

1,500

1,000

20%

500

4,000

2,000

0

0%

0

TPU 8t & 8i

• Inferentia 2

TPU v5e & v5p

— Google TPU contribution to Al revenue (RHS)

12%

Fig. 27: TSMC AI revenue mix by customer

25%

10%

8%

20%

→ Trainium 3

Source: Company data, Nomura estimates

Fig. 29: Google TPU's contribution to TSMC's AI revenue

Source: Company data, Nomura estimates

Fig. 31: AWS' contribution to TSMC's AI revenue

Source: Company data, Nomura estimates

Source: Company data, Nomura estimates

Fig. 28: nVidia's contribution to TSMC's AI revenue

Source: Company data, Nomura estimates

Fig. 30: AMD's contribution to TSMC's AI revenue

Source: Company data, Nomura estimates

novellee

Platform

Codename

Year of introduction

1,200

1,000

GPU layout

800

600

Logic fabrication

Transistors (bn)

400

Assembly

200

Interposer size

(1x reticle~830mm*)

FP8 Tensor core performance (dense)

MTIA 300

HBM specs

Max HBM capacity

DRAM layer technology

HBM I/Os

Substrate dimension (mm*)

Chip max TOP

Board level

ARM-based CPU

Superchip max TDP

LPU

DPU

NIC (max bandwidth)

Optical module

Socket usage

PCB/CCL

Rack level

Form factor

FP8 Tensor core performance (dense)

GPU-GPU NVLink

(max bandwidth)

Cable connector

Rack-Rack Infiniband

(max bandwiath/port)

Rack-Rack Ethernet

(max bandwidth/port)

ower requiremen without redundancy

Mainstream thermal solutions

10%

(USDmn)

2,000

1,500

1,000

500

Rubin Ultra

2027F

Rubin

2026F

Feynman

Feynman

2028F

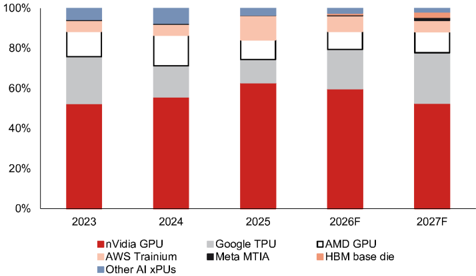

Fig. 33: HBM base die contribution to TSMC's AI revenue

25 PFLOPS (inference)

17.5 PFLOPS (training)

Source: Company data, Nomura estimates

BlueFieid-4

CX9 (1.6Tbps)

3.2Tbps

N.A.

Blackwell

Blackwel

1.000W (GH200)

Source: Company data, Nomura estimates

BlueField-3

CX6 (200Gbps)

CX7 (400Gbps)

BlueFleid-3

CX7 (400Gbps)

2,700W (GB200)

CX7 (400Gbps)

3,100W (GB300)?

CX8 (800Gbps)

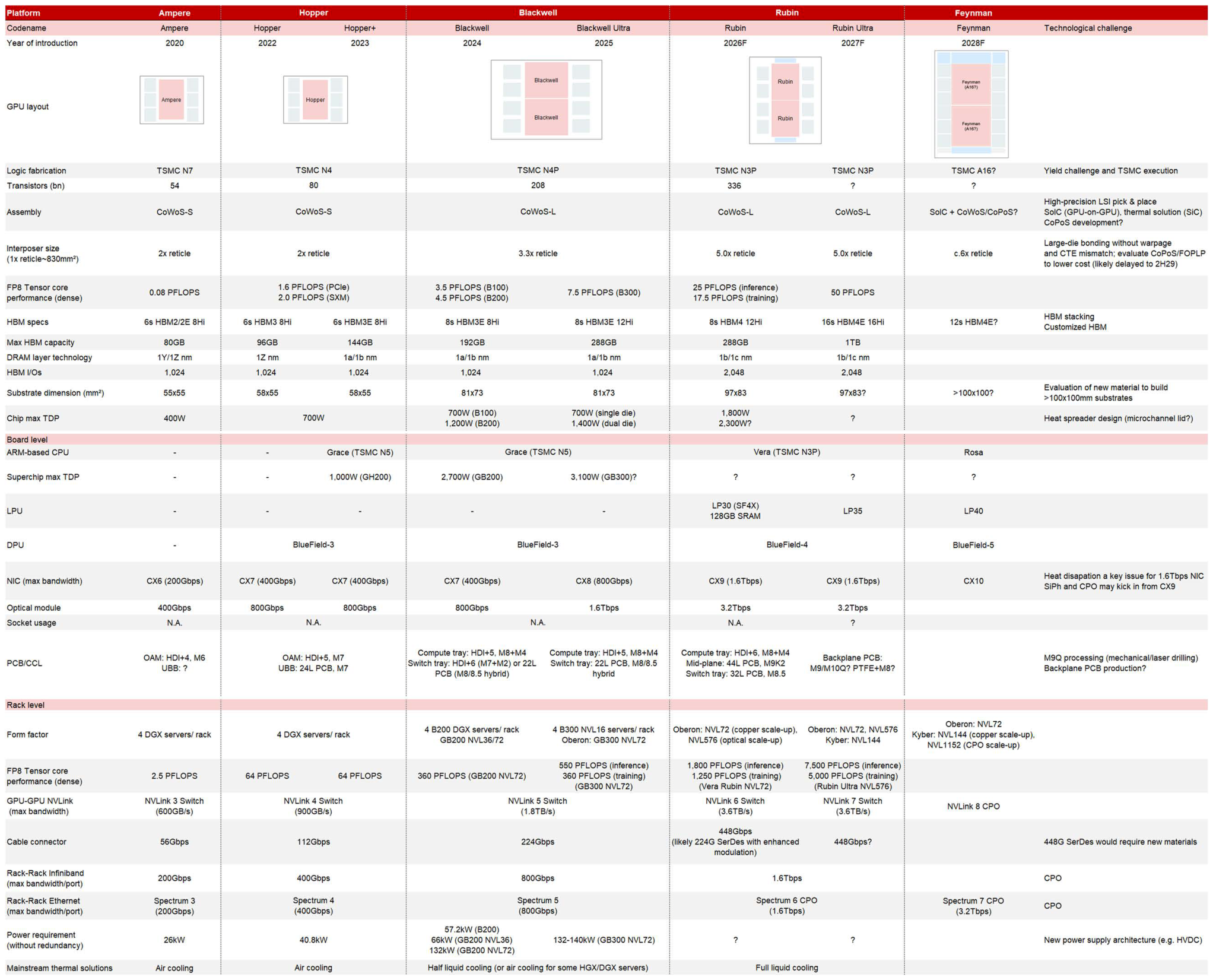

Fig. 34: Our take on the nVidia AI platform roadmap

| DAM: HDI+4, Me JBB: * | OAM: HDI+5, M7 UBB: 24L PCB, M7 | Compute tray: HDI+5, M8+M4 PCB (M8/8.5 hybrid | Switch tray: HDI+6 (M7+M2) or 22L | Compute tray: HDI+5, M8+M4 Switch tray: 22L PCB, M8/8.5 hybrid Compute tray: HDI+6, M8+M4 Mid-plane: 44L PCB. M9K2 Switch tray: 32L PCB. M8.5 | Backplane PCB: M9/M10Q2 PTFE+M8? | M9Q processing (mechanicallaser drilling Backplane PCB production? | |

|---|---|---|---|---|---|---|---|

| 4 DGX servers/ rack | 4 DGX servers/ rack | 4 B200 DGX servers/ rack GB200 NVL36/72 | 4 B200 DGX servers/ rack GB200 NVL36/72 | 4 B300 NVL 16 servers/ rack Oberon: GB300 NVL72 360 PFLOPS (GB200 NVL72) 550 PFLOPS (inference) 360 PFLOPS (training) NVL576 (optical scale-up) | peron: NVL72 (copper scale-up). Oberon: NVL72, NVL5 yber: NVL1 7,500 PFLOPS (inference Oberon: NVL72 Kyber: NVL144 (copper scale-up). NVL. 1152 (CPO scale-up) | peron: NVL72 (copper scale-up). Oberon: NVL72, NVL5 yber: NVL1 7,500 PFLOPS (inference Oberon: NVL72 Kyber: NVL144 (copper scale-up). NVL. 1152 (CPO scale-up) | |

| 2.5 PFLOPS /Link 3 Switc 600GB/- | 64 PFLOPS 64 PFLOPS VLink 4 Switc 900GB/s | Link 5 Switc | 1.8TB/s | (GB300 NVL72) 1,250 PFLOPS (training) (Vera Rubin NVL72) NVLink 6 Switc (3.6TB/s | 5,000 PFLOPS (training (Rubin Ultra NVL576) VVLink 7 Switc 3.6TB/s | NVLink 8 CPO | |

| 56Gbps | 112Gbps | 224Gbps | 448Gbps (likely 224G SerDes with enhanced modulation) | 448Gbps? | 448G SerDes would require new materials | ||

| 200Gbps | 400Gbps | 800Gbps | 1.6Tbps | CPO | |||

| Spectrum 3 (200Gbps) | Spectrum 4 (400Gbps) | 57.2KW (B200) | 57.2KW (B200) | (800Gbps) | Spectrum 6 CPO (1.6Tbps) | Spectrum 7 CPO (3.2Tbps) | CPO |

| 26KW | 40.8KW | 66KW (GB200 NVL36) | 132KW (GB200 NVL72) | 132-140KW (GB300 NVL72) ? | ? | New power supply architecture (e.g. HVDC) | |

| Air cooling | Air cooling | Haif liquid cooling (or air cooling for some HGX/DGX servers) | Full liquid cooling |

Source: Company data, Nomura estimates

1.6Tbps

CX9 (1.6Tbps)

3270p.

BlueFieid-5

CX10

2020

2022

Hopper+

2023

Blackwell|

2024

Blackwell Ultra

2%

2025

Rubin

Technological challenge

Ph and CPO may kick in from C)

eat disapation a key issue for 1.6 Tbps N

Fig. 35: TSMC - AI revenue summary

| 2023 | 2024 | 2025 | 2026F | 2027F | |

|---|---|---|---|---|---|

| TSMC AI revenue breakdown (USD mn) | |||||

| nVidia GPU | 2,055 | 6,515 | 13,898 | 23,410 | 34,358 |

| Google TPU | 918 | 1,813 | 2,548 | 7,641 | 16,472 |

| AMD GPU | 494 | 1,793 | 2,175 | 3,554 | 6,867 |

| AWS Trainium | 215 | 631 | 2,687 | 3,025 | 3,751 |

| Meta MTIA | 18 | 58 | 64 | 216 | 979 |

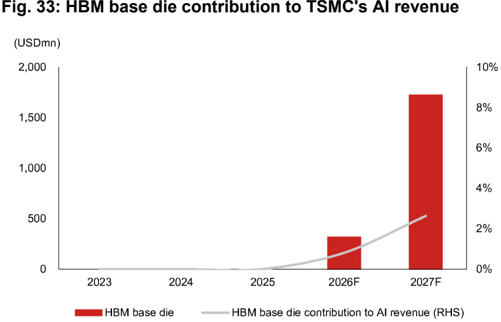

| HBM base die | 0 | 0 | 0 | 314 | 1,722 |

| Other AI xPUs | 220 | 881 | 749 | 954 | 1,255 |

| Total | 3,921 | 11,692 | 22,121 | 39,114 | 65,406 |

| Contribution to TSMC | 6% | 13% | 18% | 24% | 32% |

| TSMC's revenue (USD mn), NMRe | 69,298 | 90,083 | 122,424 | 164,742 | 205,101 |

| AI revenue from nVidia GPU | |||||

| Ampere | 844 | 94 | 0 | 0 | 0 |

| Hopper | 1,211 | 5,840 | 616 | 0 | 0 |

| Blackwell & Blackwell Ultra | 0 | 582 | 13,283 | 16,104 | 0 |

| Rubin & Rubin Ultra | 0 | 0 | 0 | 7,306 | 34,358 |

| nVidia contribution to AI revenue | 52% | 56% | 63% | 60% | 53% |

| AI revenue from Google TPU | |||||

| TPU v4 & v4i | 243 | 0 | 0 | 0 | 0 |

| TPU v5e | 173 | 346 | 0 | 0 | 0 |

| TPU v5p | 502 | 1,204 | 502 | 0 | 0 |

| TPU v6e | 0 | 264 | 369 | 0 | 0 |

| TPU7x | 0 | 0 | 1,677 | 5,535 | 0 |

| TPU 8t | 0 | 0 | 0 | 1,462 | 5,147 |

| TPU 8i | 0 | 0 | 0 | 643 | 11,325 |

| Google contribution to AI revenue | 23% | 16% | 12% | 20% | 25% |

| AI revenue from AMD GPU | |||||

| MI200 | 279 | 70 | 0 | 0 | 0 |

| MI300/325 | 215 | 1,724 | 862 | 229 | 0 |

| MI350/355 | 0 | 0 | 1,313 | 2,097 | 559 |

| MI400 series | 0 | 0 | 0 | 1,229 | 6,308 |

| AMD contribution to AI revenue | 13% | 15% | 10% | 9% | 10% |

| AI revenue from AWS Trainium | |||||

| Inferentia 2 | 215 | 299 | 30 | 0 | 0 |

| Trainium 2 | 0 | 332 | 2,657 | 183 | 0 |

| Trainium 3 | 0 | 0 | 0 | 2,842 | 3,751 |

| AWS contribution to AI revenue | 5% | 5% | 12% | 8% | 6% |

| AI revenue from Meta MTIA | |||||

| MTIA 100 | 18 | 0 | 0 | 0 | 0 |

| MTIA 200 | 0 | 58 | 29 | 10 | 0 |

| MTIA 300 | 0 | 0 | 35 | 58 | 0 |

| MTIA 400/450 | 0 | 0 | 0 | 148 | 979 |

| Meta contribution to AI revenue | 0% | 0% | 0% | 1% | 1% |

Source: Company data, Nomura estimates

OSATs' CoWoS-like full processes could start emerging from 2027F

CPUs are low-hanging fruits to capitalize on

Venice and Vera CPUs are manifestations of OSATs monetizing alternative CoW opportunities

We first wrote about TSMC's prudent approach to CoW capacity expansion in our Asia AI Semi & Server Anchor report in August 2025 , and noted that such planning was critical for OSATs as it had driven most AI chip customers to look for alternative CoW suppliers, thereby benefiting ASE (see our upgrade report ). Amkor is also an alternate CoW partner, and management highlighted over a dozen 2.5D engagements (silicon interposer-based, as per Amkor's definition) and expected high-density fan-out RDL devices (i.e., organic interposer-based) ramping up production in 2026E and bridge-type solution for AMD in 2027E (see Amkor's Investor Day 2026 ). We compare major OSATs' advanced packaging platforms with TSMC's equivalent technologies in Fig. 36 , and observe that many 2.5D/molded interposer based packages in the pipeline of OSATs are for CPUs (Fig. 37 ). In our view, the wider RDL line/space and fewer RDL layers in CPU packages than AI accelerators could possibly relax some technological requirements for OSATs to participate in advanced packaging. Other than technology readiness, we believe another key factor hindering OSATs from engaging in CoW processes is the enormous losses that would be incurred if there were to be immature assembly yield. That, in our view, is the reason why the high-performance computing chips using OSATs' CoW to ramp up volume from 2H26F are mostly CPUs, which do not carry expensive HBM content.

We will discuss CPU architectures in detail in the section 'CPUs: different architectures & surging demand ' and focus on OSATs' advanced packaging capacity planning here. We estimate ASE could form 25kwpm of FOCoS capacity by end-2026F, from 5kwpm installed by end-2025. We believe the major consumption of ASE's FOCoS capacity will go to AMD's Venice CPUs in 2026-27F, which utilize ASE's FOCoS-B platform, and estimate USD350mn/1.4bn of revenue from this project for ASE in 2026F/27F, or 10%/20% of its leading-edge advanced packaging (LEAP) revenue. In our view, another organic interposer based package of significant volumes could be nVidia's Vera CPUs, which are assembled at TSMC (CoWoS-R) and Amkor (S-SWIFT). Our assumption is the TSMC track makes up c.40% of nVidia's Vera backend supply.

Fig. 36: 2.5D advanced packaging solution comparison

| 2.5D chip-last | TSMC | Intel Foundry | Samsung Foundry | ASE | SPIL | Amkor | Powertech |

|---|---|---|---|---|---|---|---|

| Silicon/TSV interposer | CoWoS-S (~3.3x ret.) | Foveros-S (~4x ret.) | I-CubeS H-Cube | 2.5D | 2.5D | 2.5D | 2.5D |

| Fan-out RDL | CoWoS-R (~5.5x ret.) | Foveros-R (production in 2027E) | n.a. | FOCoS | FO-MCM | S-SWIFT | CLIP (PLP) |

| Fan-out bridge (embedded in RDL) | CoWoS-L (>14x ret. by 2029E) | Foveros-B (production in 2027E) | I-CubeE | FOCoS-B | FO-EB | S-Connect | PiFO (PLP) (~9x ret. by 2028E) |

| Fan-out bridge (embedded in IC substrate) | - | EMIB (>12x ret. by 2028E) | - | - | - | - | - |

Source: Company data, Nomura research

Fig. 37: Major CoW projects at OSATs

| Fan-out RDL | Fan-out bridge | |

|---|---|---|

| ASE/SPIL | AMD Medusa? | AMD Venice |

| Amkor | nVidia GB10 nVidia Vera Microsoft Cobalt 200 | AMD Venice? (2027E) |

| Powertech | AMD Medusa? (PLP) | AMD's next gen? (PLP) |

Source: Company data, Nomura research

Fig. 38: Vera CPU packaged on TSMC CoWoS-R

Source: Company data, Nomura research

Fig. 39: Vera CPU packaged at Amkor S-SWIFT

Source: Company data, Nomura research

Die 1

Die 2

Intel's EMIB-T: major competitor to TSMC's advanced packaging

EMIB-T appears worth monitoring with increasing adoption

EMIB-T emerges as a 'must-succeed' alternative packaging solution for AI chips

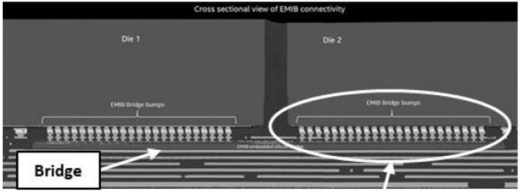

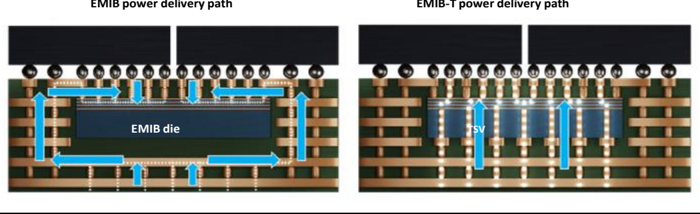

We believe certain AI ASIC customers might have started evaluating Intel's EMIB-T as a logic+HBM integration alternative because of concerns about insufficient capacity support at TSMC. We think Google's potential reliance on Intel's EMIB-T for the next-generation TPU v9 (partnering with MediaTek) could be a critical litmus test for Intel's advanced packaging capabilities. Since 2017, Intel's EMIB has utilized silicon bridges buried in the build-up layers of an IC substrate to connect chiplets on top without any interposer (Fig. 40 ). Previously, in EMIB configuration, the I/O power delivery paths of top dies are cantilevered, and power from the substrate underneath had to traverse on the perimeter of the silicon bridge and across its thin metal layers to reach the microbumps. A longer routing distance, however, could cause intermediate resistance drop (IR drop) or lower actual voltage reaching transistors which adversely affected device functionality and performance. With the most advanced AI chips moving toward HBM4, power integrity becomes a more critical issue since HBM4 doubles the I/O bump density from HBM3E, operates at a higher current and is more sensitive to IR drop.

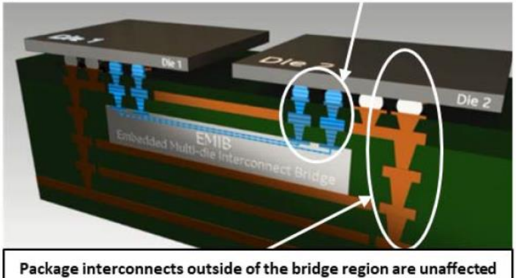

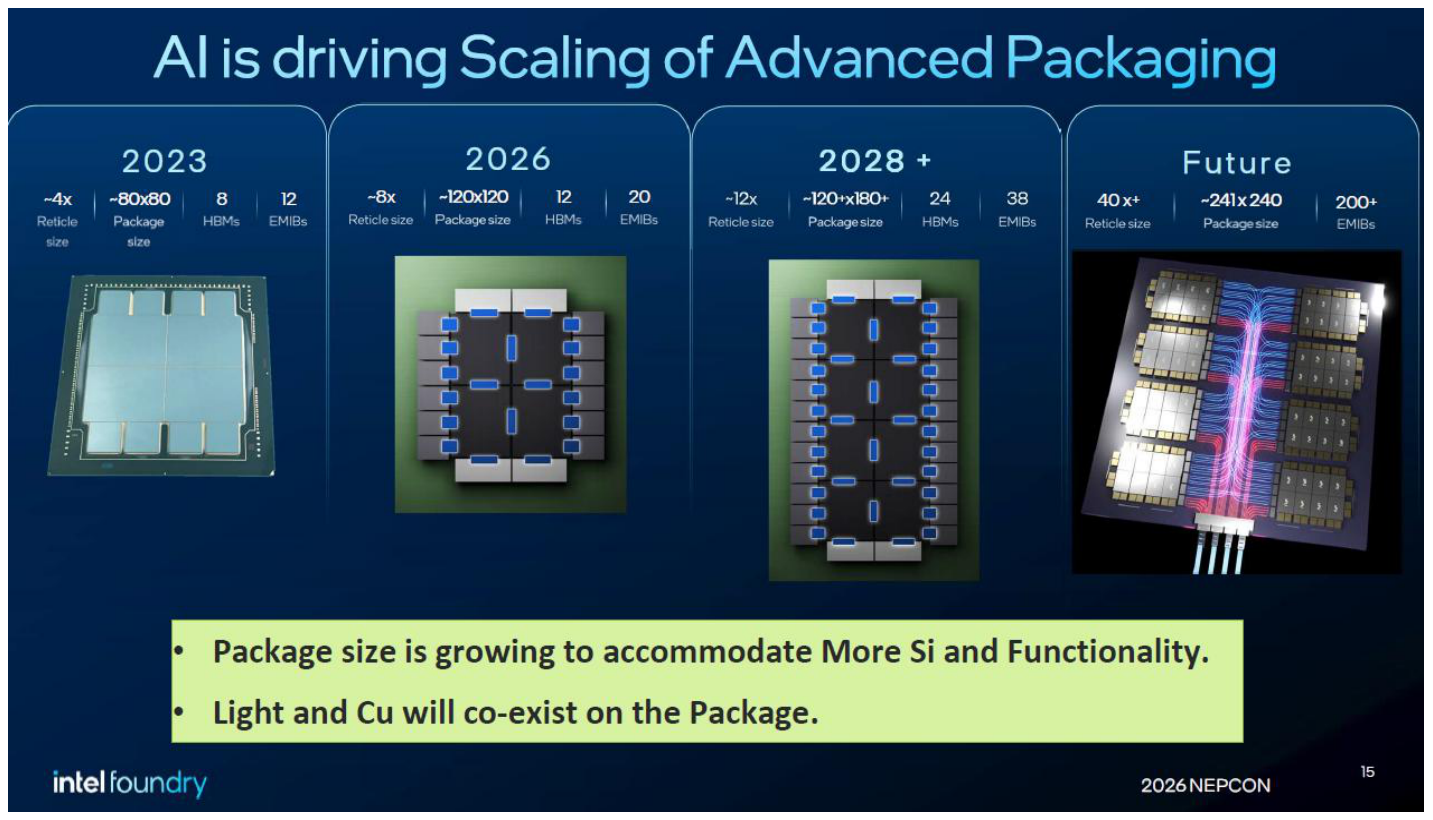

The new EMIB-T technology aims to incorporate through-silicon vias (TSVs) within the bridge die to create a vertical power delivery network, thereby shortening the routing distance to improve power delivery efficiency and performance (Fig. 41 ). According to Intel, EMIB-T targets HBM4/4E and logic chiplet interconnectivity with the lowest possible cost, and the company's roadmap is to scale to the integration of >8x reticle size total top silicon area on a ~120x120mm substrate by 2026E and >12x reticle size top silicon area on a >120x180mm substrate by 2028E (Fig. 42 ). In addition, the process flow of EMIB-T is not significantly different from the conventional EMIB, except that TSV bridge dies are placed into substrate cavities with a solder joint formation.

In our Greater China Semi Anchor Report , we highlighted Intel's strong commitment to leading substrate partners such as Ibiden (4062 JP, Buy), Unimicron, and Shinko (unlisted) to bring the EMIB-T technology into mass production, and leading substrate companies are expanding their capacities for Intel aggressively through co-investment. Nevertheless, Intel's experience of handling EMIB integration is largely grounded to internal products, with 12-14x silicon bridges in one package at max (Fig. 43 ). Our supply chain feedback indicates that the TPU v9 could have close to 30 silicon bridges buried in the large substrate, with potentially many silicon capacitors embedded as well. We believe the deviation of specs from the current AI/HPC substrate structure could lead to production yield challenges.

Fig. 40: An illustration of EMIB

-4x

Reticle size

EMIB power delivery path

2026

EMIB-T power delivery path

2028 +

Future

Fig. 41: EMIB-T shortens the power delivery routing distance to reduce IR drop

Source: Intel, Nomura research

Fig. 42: Intel's EMIB roadmap

Source: Intel, Nomura research

Fig. 43: Intel's internal products based on EMIB interconnects

| Codename | Product type | Launch time | Remarks |

|---|---|---|---|

| Kaby Lake-G | Client CPU | 2017 | Integrates Intel Kaby Lake CPU, AMD Radeon RX Vega MGPU, and HBM2. |

| Ponte Vecchio Falcon Shores | AI accelerator AI AI | 2023 | Co-EMIB (3.5D); 11 EMIB dies. |

| accelerator | Cancelled | ||

| Jaguar Shores | accelerator | 2026-27E | |

| Sapphire Rapids | Server CPU | 2023 | 10x EMIB dies in SPR XCC. 14x EMIB dies in SPR HBM. |

| Emerald Rapids | Server CPU | 2023 | 3x EMIB dies. |

| Granite Rapids | Server CPU | 2024 | 12x EMIB dies. |

| Sierra Forest | Server CPU | 2024 | |

| Diamond Rapids | Server CPU | 2026E | |

| Clearwater Forest | Server CPU | 2026E | 12x EMIB dies. |

| Coral Rapids | Server CPU | 2028-29E | |

| Stratix 10 | FPGA (Altera) | 2017 | 6x EMIB dies. |

| Agilex | FPGA (Altera) | 2019 | 5x EMIB dies. |

Source: Company data, Nomura estimates

2026 NEPCON

15

Fig. 44: EMIB supply chain

| Process | Companies involved |

|---|---|

| Flip-chip assembly | |

| Bumping | Powertech (6239 TT), Amkor (AMKR US) |

| Die bond | ASMPT (522 HK), K&S (KLIC US) |

| Laser marking | E&R (8027 TT) |

| Plasma cleaning | E&R (8027 TT) |

| EMIB substrate | |

| IC substrate | Ibiden (4062 JP), Unimicron (3037 TT), Shinko (unlisted) |

| ABF film lamination | EPM (7795 TT) |

| Bridge die bond | Toray (3402 JP) |

| Electroplating | ASMPT NEXX (unlisted) |

| Laser via drilling | Mitsubishi (6503 JP) |

| Baking oven | Group Up (6664 TT) |

| Other components | |

| Silicon capacitor | AP Memory (6531 TT), SEMCO (009150 KS) |

| Silicon capacitor foundry | Powerchip (6770 TT), UMC (2303 TT), Winbond (2344 TT) |

Source: Company data, Nomura research

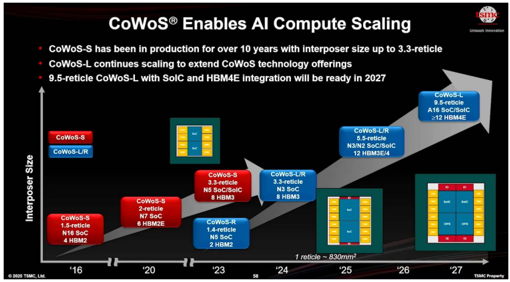

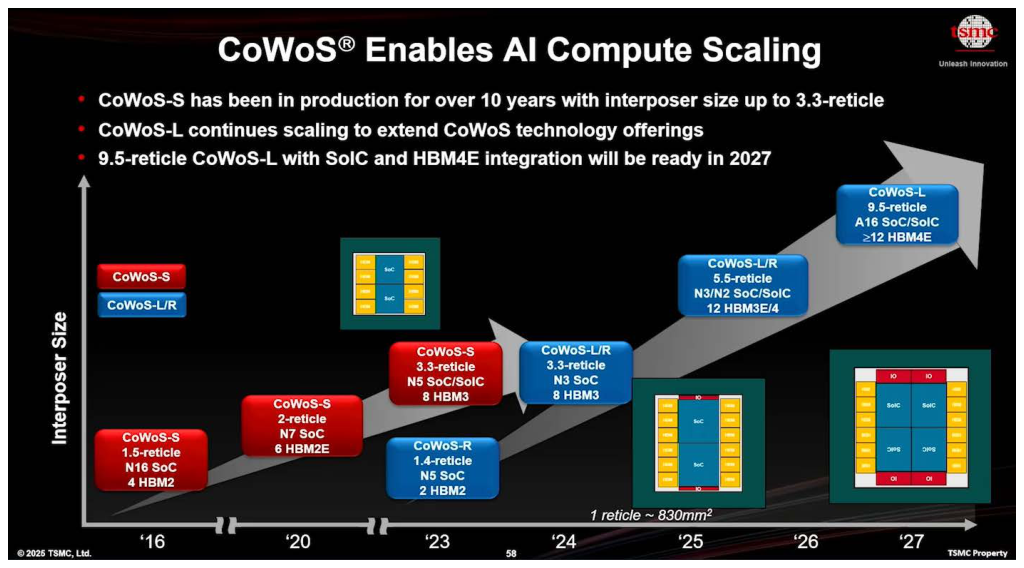

Interposer Size

• CoWos-S has been in production for over 10 years with interposer size up to 3.3-reticle cullergy can poorer

CoWos® Enables Al Compute Scaling

• World's largest 5.5-reticle size CoWoS in production with >98% yield in 2026