PDF 原檔:報告_MS_AI供應鏈CoWoS分配_20260708_original.pdf

圖片清單(已驗證 2026-07-09)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_MS_AI供應鏈CoWoS分配_20260708_002.png |

166KB | 真資料圖 | Exhibit 1:2027e AI HBM 需求表,各廠商 CoWoS 產能配置(k wafers)/每片晶圓顆數/隱含出貨量/HBM 用量細項;MI450(for Meta) 列標紅:35k wafers、14 顆/wafer、490k 顆出貨、HBM4 12hi 6 顆/216GB;總計 2,664k wafers、33,996k 顆出貨、HBM 總需求 48,618mn Gb |

報告_MS_AI供應鏈CoWoS分配_20260708_008.png |

172KB | 真資料圖 | Exhibit 12:Rubin 晶片出貨量(LHS, mn units) vs NVL72 機櫃出貨量(RHS, k racks) 曲線圖,2Q26e-4Q27e,標註「3k NVL72」約落在 4Q26e、「12-13k NVL72」約落在 1Q27e |

報告_MS_AI供應鏈CoWoS分配_20260708_009.png |

74KB | 真資料圖 | Exhibit 13:AI 半導體 P/E 倍數趨勢圖(GP GPU NVIDIA/Alternative AI Semis/AI Semi Enablers 三條線),Nov-22 至 Jun-26 |

報告_MS_AI供應鏈CoWoS分配_20260708_010.png |

81KB | 真資料圖 | Exhibit 14:「Data center/HPC semi revenue: NVIDIA + AMD」長條圖(US$mn) + YoY% 曲線,1Q14-3Q27e |

報告_MS_AI供應鏈CoWoS分配_20260708_011.png |

44KB | 真資料圖 | Exhibit 15:「TSMC AI revenue breakdown」堆疊長條圖 2021-2029e,標註 2024-2029e CAGR 60%箭頭,分 General-purpose AI/Custom AI chips(ASICs)/CoWoS/wafer test/AI server CPU |

報告_MS_AI供應鏈CoWoS分配_20260708_012.png |

38KB | 真資料圖 | Exhibit 16:AI GPU H100 每小時租金追蹤圖,GCP H100(A3-HIGH) vs AWS H100(p5.48xlarge),3/2024 至約 2026 |

報告_MS_AI供應鏈CoWoS分配_20260708_014.png |

54KB | 真資料圖 | Exhibit 18:NVIDIA 遊戲顯卡中國價格圖,4090/5090D 淘寶經銷價 vs 官方標價(Rmb),2024/7-2026/6 |

報告_MS_AI供應鏈CoWoS分配_20260708_001.png |

65KB | 裝飾·banner | 「Asia Summer School 2026」廣告 banner,泳池圖片+信封圖示 |

<40KB 未逐張列出者(003/004/005/006/007/013)預設為版面裝飾或與 Exhibit 1-3/5 文字表格重複之圖表,未 Read。

原始內容

M July 8, 2026 06:45 AM GMT

Asia-Pacific Technology | Asia Pacific

AI Supply Chain: Further Updates on 2027 CoWoS Allocation and ASIC Dynamics

AMD's 2027 CoWoS allocation remains at 240k for now, with combined MI455/MI450 shipments at 1.5mn. TPU MP timing skews toward 4Q. Blackwell chip "inventory" turned out to be a supply chain buffer and will be fully consumed by 2026. We expect ~7mn Rubin chips and 90k NVL72 racks in 2027.

Further updates on our AMD CoWoS allocation: We published our preliminary 2027 CoWoS allocation last week and received many investor queries on AMD's (covered by Joe Moore) CoWoS number. Some MI300 series and upcoming MI500 production will still run in 2027. However, the MI400 series will come in two versions: (1) MI455: the standard version with 2 compute dies and 12 HBM4 12hi, paired with the Helios rack (18 CPUs and 72 GPUs), with Microsoft, AWS, and Oracle as key customers; (2) MI450: a Meta-customized, half-size chip paired with 1 compute die and 6 HBM4 12hi (9 CPUs and 36 GPUs). We still expect AMD's 2027 CoWoS at 240k, but do not rule out execution risk, given its prior record of trimming CoWoS bookings in 2026. 2027 chip shipments: MI455 1mn and MI450 500k. For CPU, Venice is AMD's first CPU adopting CoWoS, and we see CoW production concentrated in OSATs-ASE/SPIL, Amkor, and Powertech. Total CPU chip shipments could reach 5.7-6mn units in 2027 vs. 1mn in 2026.

Google TPU progress update: Our industry checks suggest KYEC's 3Q26 revenue could grow close to 10% Q/Q, below our initial 15% Q/Q expectation, mainly due to slight Rubin and Sunfish delays and MediaTek's smartphone SoC order trim. We do see Sunfish shipments largely in 4Q, with full-year volume at 960k units. With Sunfish and Rubin pushed out, we believe more revenue will concentrate in 4Q26 or 1Q27 without order cuts. Many investors asked about Zebrafish delays; we still see its 4Q26 volume ramp unchanged.

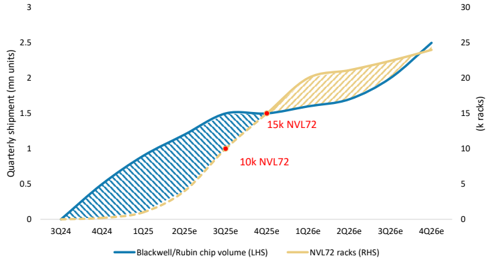

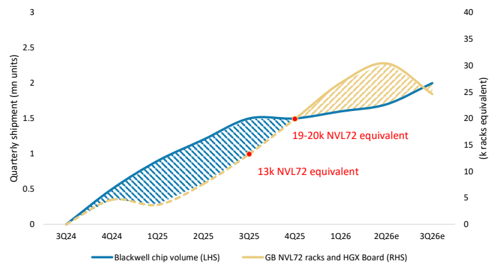

Comparing the Blackwell chip/rack shipment and Rubin chip/rack shipment: We

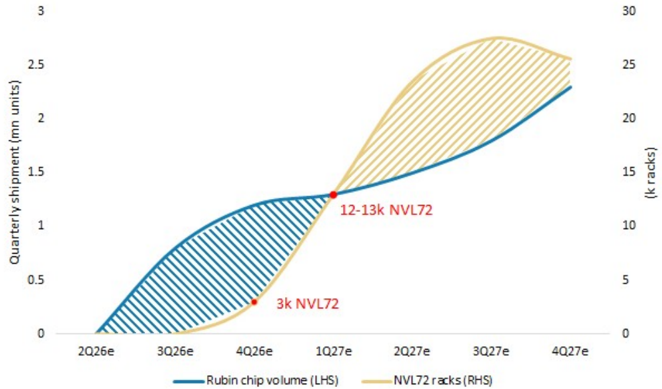

provided a chip vs. rack shipment comparison for Blackwell in last June's AI tracker. We now include HGX (8-GPU per server) in our chip consumption model, and treat 9 HGX servers as equivalent to one NVL72 rack. We expect 5.4mn Blackwell units in 2026, and chip volume could meet Grace Blackwell NVL72 demand by 2H26. Our latest checks also suggest close to 7mn Rubin and Rubin Ultra units in 2027, while total Rubin NVL72 server racks could reach 90k in 2027 ( Exhibit 12 ). All Blackwell chip "inventory" turned out to be a supply-chain buffer and will be fully consumed by 2026, so we see no need to worry about inventory issues. We think Rubin will follow a similar pattern.

(continued on the next page)

| Morgan Stanley Taiwan Limited+ Charlie Chan Equity Analyst Charlie.Chan@morganstanley.com | +886 2 2730-1725 |

|---|---|

| Daniel Yen, CFA Equity Analyst Daniel.Yen@morganstanley.com Morgan Stanley Asia Limited+ | +886 2 2730-2863 |

| Daisy Dai, CFA Equity Analyst Daisy.Dai@morganstanley.com | +852 2848-7310 |

| Morgan Stanley Taiwan Limited+ Tiffany Yeh Equity Analyst Tiffany.Yeh@morganstanley.com | +886 2 7712-3032 |

| Lucas Wang Research Associate Lucas.Wang@morganstanley.com Morgan Stanley Asia Limited+ Ethan Jia Research Associate Ethan.Jia@morganstanley.com | +886 2 2730-2875 |

| Henry Zhao Research Associate | +852 3963-2287 |

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

+= Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to FINRA restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

M

Meta ASIC progress update: On the other hand, Meta cancelled its original 2nm ASIC Olympus earlier this year; a new 2nm chip, code-named Apollo, succeeds it. Broadcom (covered by Joe Moore) will continue design services, with mass production in 1Q28. For GUC, we think it is likely to win one of the Meta ASIC projects led by the Rivos team, possibly a side project from the usual MTIA product line. The AI ASIC targets tape-out in 1H27, with potential CoWoS out by 2027 year-end or 1H28.

M

Introducing Our 2027 Global CoWoS Capacity Update And Comparing Chip Shipments vs. Racks

We published our preliminary 2027 CoWoS allocation last week and received lots of investor queries around AMD's (covered by Joe Moore) CoWoS number. There will still be some production of the MI300 series and the upcoming MI500 in 2027.

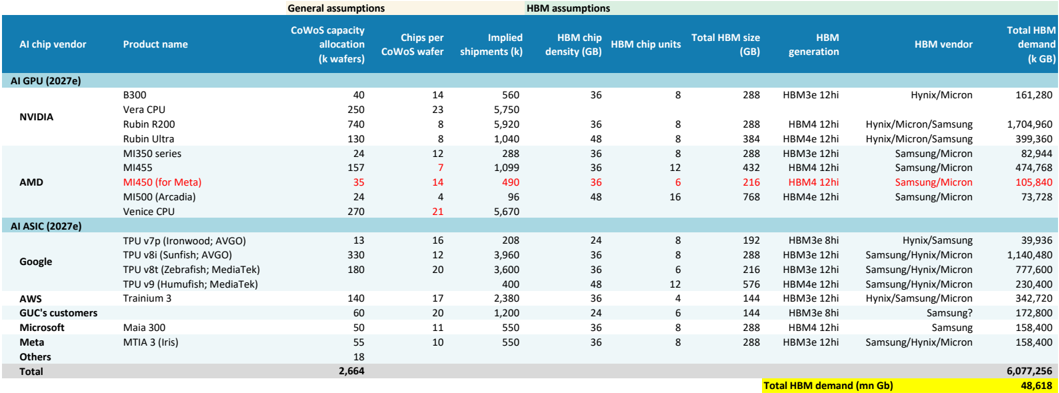

However, for the MI400 series, there will be two versions coming: 1) MI455: the standard version, including 2 compute dies and 12 HBM4 12hi, pairing with the Helios rack (18 CPUs and 72 GPUs), with key customers being Microsoft, AWS and Oracle; 2) MI450: customized version for Meta, with the chip being half size pairing with 1 compute die and 6 HBM4 12hi (9 CPUs and 36 GPUs) (see Exhibit 1 ). We still expect AMD's CoWoS to be 240k in 2027, but do not rule out execution risk, given its prior record of trimming CoWoS bookings in 2026. We estimate chip shipments in 2027 will be 1mn for MI455 and 500k for MI450.

For CPU, Venice is AMD's first CPU to adopt CoWoS, and we see CoW production concentrating in OSATs, including ASE/SPIL, Amkor and Powertech. We expect total chip shipments of 5.7-6mn units in 2027 vs. 1mn units in 2026.

Exhibit 1: AI HBM consumption: up to 50bn Gb in 2027

| General assumptions | General assumptions | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| AI chip vendor | Product name | CoWoS capacity allocation (k wafers) | Chips per CoWoS wafer | Implied shipments (k) | HBMchip density (GB) HBMchip | units | Total HBMsize (GB) | HBM generation | HBMvendor | TotalHBM demand (k GB) |

| AI GPU (2027e) | ||||||||||

| B300 | 40 | 14 | 560 | 36 | 8 | 288 | HBM3e 12hi | Hynix/Micron | 161,280 | |

| NVIDIA | Vera CPU | 250 | 23 | 5,750 | ||||||

| Rubin R200 | 740 | 8 | 5,920 | 36 | 8 | 288 | HBM4 12hi | Hynix/Micron/Samsung | 1,704,960 | |

| Rubin Ultra | 130 | 8 | 1,040 | 48 | 8 | 384 | HBM4e 12hi | Hynix/Micron/Samsung | 399,360 | |

| MI350 series | 24 | 12 | 288 | 36 | 8 | 288 | HBM3e 12hi | Samsung/Micron | 82,944 | |

| MI455 | 157 | 7 | 1,099 | 36 | 12 | 432 | HBM4 12hi | Samsung/Micron | 474,768 | |

| AMD | MI450 (for Meta) | 35 | 14 | 490 | 36 | 6 | 216 | HBM4 12hi | Samsung/Micron | 105,840 |

| MI500 (Arcadia) | 24 | 4 | 96 | 48 | 16 | 768 | HBM4e 12hi | Samsung/Micron | 73,728 | |

| Venice CPU | 270 | 21 | 5,670 | |||||||

| AI ASIC (2027e) | ||||||||||

| TPU v7p (Ironwood; AVGO) | 13 | 16 | 208 | 24 | 8 | 192 | HBM3e 8hi | Hynix/Samsung | 39,936 | |

| TPU v8i (Sunfish; AVGO) | 330 | 12 | 3,960 | 36 | 8 | 288 | HBM3e 12hi | Samsung/Hynix/Micron | 1,140,480 | |

| TPU v8t (Zebrafish; MediaTek) | 180 | 20 | 3,600 | 36 | 6 | 216 | HBM3e 12hi | Samsung/Hynix/Micron | 777,600 | |

| TPU v9 (Humufish; MediaTek) | 400 | 48 | 12 | 576 | HBM4e 12hi | Samsung/Hynix/Micron | 230,400 | |||

| AWS | Trainium 3 | 140 | 17 | 2,380 | 36 | 4 | 144 | HBM3e 12hi | Hynix/Samsung/Micron | 342,720 |

| GUC's customers | 60 | 20 | 1,200 | 24 | 6 | 144 | HBM3e 8hi | Samsung? | 172,800 | |

| Microsoft | Maia 300 | 50 | 11 | 550 | 36 | 8 | 288 | HBM4 12hi | Samsung | 158,400 |

| Meta | MTIA 3 (Iris) | 55 | 10 | 550 | 36 | 8 | 288 | HBM3e 12hi | Samsung/Hynix/Micron | 158,400 |

| Others | 18 | |||||||||

| Total | 2,664 | 33,996 | 6,077,256 | |||||||

| Total HBMdemand (mn Gb) | Total HBMdemand (mn Gb) | 48,618 |

Source: Company data, Morgan Stanley Research (e) estimates. Note: Estimates are compiled using our Asian supply chain checks.

M

Exhibit 2: AI wafer consumption: at least US$47bn in 2027

| AI chip vendor | Product name | CoWoS capacity allocation (k wafers) | Chips per CoWoS wafer | Implied shipments (k) | Compute die size | Geometry | Compute die units | Wafer consumption (k wafers) | Wafer price (US$) Wafer TAM (US$ | revenue mn) |

|---|---|---|---|---|---|---|---|---|---|---|

| AI GPU (2027e) | ||||||||||

| B300 | 40 | 14 | 560 | 850 | 4nm | 2 | 44 | 23,042 | 1,024 | |

| Vera CPU | 250 | 23 | 5,750 | 850 | 3nm | 1 | 228 | 27,300 | 6,229 | |

| NVIDIA | Rubin R200 | 740 | 8 | 5,920 | 850 | 3nm | 2 | 470 | 27,300 | 12,827 |

| Rubin Ultra | 130 | 8 | 1,040 | 850 | 3nm | 2 | 58 | 27,300 | 1,588 | |

| MI350 series | 24 | 12 | 288 | 110 | 3nm | 8 | 8 | 27,300 | 229 | |

| MI455 | 157 | 7 | 1,099 | 850 | 2nm | 2 | 13 | 30,000 | 400 | |

| AMD | MI450 (for Meta) | 35 | 14 | 490 | 850 | 2nm | 1 | 3 | 30,000 | 89 |

| MI500 (Arcadia) | 24 | 4 | 96 | 2nm | 30,000 | |||||

| Venice CPU | 270 | 21 | 5,670 | 2nm | ||||||

| AI ASIC (2027e) | ||||||||||

| TPU v7p (Ironwood; AVGO) | 13 | 16 | 208 | 700 | 3nm | 2 | 14 | 27,300 | 371 | |

| TPU v8i (Sunfish; AVGO) | 330 | 12 | 3,960 | 800 | 3nm | 2 | 296 | 27,300 | 8,075 | |

| TPU v8t (Zebrafish; MediaTek) | 180 | 20 | 3,600 | 800 | 3nm | 2 | 269 | 27,300 | 7,341 | |

| TPU v9 (Humufish; MediaTek) | 400 | 850 | 2nm | 2 | 32 | 27,300 | 867 | |||

| AWS | Trainium 3 | 140 | 17 | 2,380 | 700 | 3nm | 2 | 127 | 27,300 | 3,465 |

| GUC's customers | 60 | 20 | 1,200 | 645 | 4nm | 1 | 29 | 23,042 | 674 | |

| Microsoft | Maia 300 | 50 | 11 | 550 | 850 | 2nm | 1 | 29.1 | 30,000 | 873 |

| Meta | MTIA 3 (Iris) | 55 | 10 | 550 | 850 | 3nm | 2 | 44 | 27,300 | 1,192 |

| Others | 18 | |||||||||

| Total | 2,664 | 33,996 | 1,700 | 46,208 |

Source: Company data, Morgan Stanley Research (e) estimates. Note: Estimates are compiled using our Asian supply chain checks.

Exhibit 3: CoWoS allocation breakdown by CoW vendor

| (k wafer) | 2023 | 2024 | 2025 | 2026e | 2027e | 2023 | 2024 | 2025e | 2026e | 2027e |

|---|---|---|---|---|---|---|---|---|---|---|

| NVIDIA | 53 | 200 | 425 | 780 | 1,222 | 45% | 54% | 62% | 56% | 45% |

| TSMC | 390 | 680 | 1,090 | |||||||

| CoWoS-L | 390 | 650 | 910 | |||||||

| CoWoS-S | 0 | 20 | 50 | |||||||

| CoWoS-R | 0 | 10 | 130 | |||||||

| Non-TSMC | 35 | 100 | 132 | |||||||

| Amkor | 35 | 100 | 132 | |||||||

| CoWoS-S | 20 | 20 | 12 | |||||||

| CoWoS-R | 15 | 80 | 120 | |||||||

| ASE/SPIL | 0 | 0 | 0 | |||||||

| CoWoS-S | 0 | 0 | 0 | |||||||

| CoWoS-R | 0 | 0 | 0 | |||||||

| Broadcom | 23 | 68 | 85 | 300 | 484 | 20% | 18% | 12% | 22% | 18% |

| TSMC | 83 | 260 | 420 | |||||||

| CoWoS-L | 0 | 15 | 55 | |||||||

| CoWoS-S | 83 | 245 | 365 | |||||||

| ASE/SPIL | 2 | 30 | 40 | |||||||

| ㄝ | 0 | 0 | 0 | |||||||

| CoWoS-S | 2 | 30 | 40 | |||||||

| Amkor | 10 | 24 | ||||||||

| CoWoS-S | 10 | 24 | ||||||||

| AMD | 7 | 40 | 60 | 130 | 530 | 6% | 11% | 9% | 9% | 20% |

| TSMC | 60 | 80 | 240 | |||||||

| CoWoS-L | 0 | 70 | 230 | |||||||

| CoWoS-S | 60 | 10 | 10 | |||||||

| ASE/SPIL | 0 | 50 | 170 | |||||||

| CoWoS-L | 0 | 50 | 170 | |||||||

| Amkor | 0 | 120 | ||||||||

| CoWoS-L | 0 | 120 | ||||||||

| Xilinx | 3 | 10 | 10 | 10 | 10 | 3% | 3% | 1% | 1% | 0% |

| MediaTek | 40 | 180 | 3% | 7% | ||||||

| TSMC | 40 | 180 | ||||||||

| CoWoS-S | 40 | 180 | ||||||||

| AWS/Annapurna | 60 | 62 | 90 | 4% | 3% | |||||

| TSMC | 60 | 32 | 54 | |||||||

| CoWoS-R | 60 | 32 | 54 | |||||||

| ASE/SPIL | 30 | 36 | ||||||||

| CoWoS-R | 30 | 36 | ||||||||

| AWS/Alchip | 9 | 16 | 5 | 26 | 36 | 8% | 4% | 1% | 2% | 1% |

| Intel Habana | 0 | 7 | 9 | 0 | 0 | 0% | 2% | 1% | 0% | 0% |

| Marvell | 1 | 18 | 15 | 17 | 64 | 1% | 5% | 2% | 1% | 2% |

| TSMC | 5 | 50 | ||||||||

| CoWoS-L | 5 | 50 | ||||||||

| CoWoS-R | 15 | 0 | 0 | |||||||

| ASE/SPIL | 12 | 14 | ||||||||

| CoWoS-R | 12 | 14 | ||||||||

| GUC | 1 | 1 | 2 | 14 | 60 | 1% | 0% | 0% | 1% | 2% |

| Cisco | 2 | 3 | 5 | 6 | 1% | 0% | 0% | 0% | ||

| Others | 20 | 10 | 15 | 10 | 12 | 17% | 3% | 2% | 1% | 0% |

| Total demand | 117 | 372 | 689 | 1,394 | 2,694 | 100% | 100% | 100% | 100% | 100% |

Source: Company data, Morgan Stanley Research (e) estimates. Note: Estimates are compiled using our Asian supply chain checks.

M

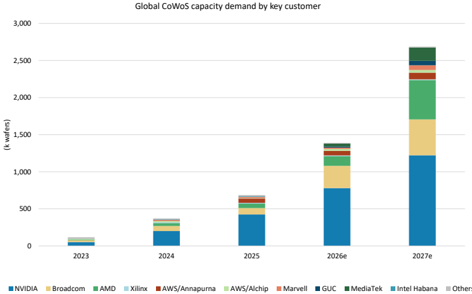

Exhibit 4: Global CoWoS demand breakdown: 2026e vs. 2027e

Global CoWoS capacity demand by key customer

Source: Company data, Morgan Stanley Research (e) estimates; note: estimates are complied using our supply chain checks

Exhibit 5: Global CoWoS demand Y/Y growth profile

| Y/Y | 2023 | 2024 | 2025 | 2026e | 2027e |

|---|---|---|---|---|---|

| NVIDIA | 119% | 280% | 113% | 84% | 57% |

| Broadcom | 56% | 191% | 25% | 253% | 61% |

| AMD | 485% | 470% | 50% | 117% | 308% |

| Xilinx | 63% | 242% | 0% | 0% | 0% |

| AWS/Annapurna | 3% | 45% | |||

| AWS/Alchip | 71% | (69%) | 420% | 38% | |

| Marvell | (22%) | 1438% | (17%) | 13% | 276% |

| GUC | (15%) | 300% | 600% | 329% | |

| Cisco | 36% | 67% | 10% | ||

| Others | 23% | (49%) | 50% | (33%) | 20% |

| Total demand | 95% | 218% | 85% | 102% | 93% |

Source: Company data, Morgan Stanley Research (e) estimates; note: estimates are complied using our supply chain checks

M

Exhibit 6: Global CoWoS capacity expansion by year end and by vendor

Source: Company data, Morgan Stanley Research (e) estimates

Exhibit 8:

AI HBM consumption: up to 30bn Gb in 2026

| AI chip vendor | Product name | CoWoS capacity allocation (k wafers) | Chips per CoWoS wafer | Implied shipments (k) | HBMchip density (GB) | HBMchip units | Total HBMsize (GB) | HBM generation | HBMvendor | TotalHBM demand (k GB) |

|---|---|---|---|---|---|---|---|---|---|---|

| AI GPU (2026e) | ||||||||||

| B300 | 390 | 14 | 5,460 | 36 | 8 | 288 | HBM3e 12hi | Hynix/Micron/Samsung | 1,572,480 | |

| Vera CPU | 90 | 23 | 2,070 | |||||||

| NVIDIA | Spectrum/CPX | 60 | - | |||||||

| Rubin R200 | 260 | 8 | 2,080 | 36 | 8 | 288 | HBM4 12hi | Hynix/Micron/Samsung? | 599,040 | |

| H200 | 20 | 27 | 540 | 24 | 6 | 141 | HBM3e 8hi | Hynix | 76,140 | |

| MI300 | 3 | 12 | 36 | 24 | 8 | 192 | HBM3e 12hi | Samsung | 6,912 | |

| MI350/375 | 7 | 12 | 84 | 36 | 8 | 288 | HBM3e 12hi | Samsung/Micron | 24,192 | |

| AMD | MI455 | 65 | 7 | 455 | 36 | 12 | 432 | HBM4 12hi | Samsung/Micron | 196,560 |

| Venice | 50 | 21 | 1,050 | |||||||

| AI ASIC (2026e) | ||||||||||

| TPU v7p (Ironwood; AVGO) | 145 | 16 | 2,320 | 24 | 8 | 192 | HBM3e 8hi | Hynix/Samsung | 445,440 | |

| TPU v8i (Sunfish; AVGO) | 80 | 12 | 960 | 36 | 8 | 288 | HBM3e 12hi | Hynix/Samsung/Micron | 276,480 | |

| TPU v8t (Zebrafish; MediaTek) | 40 | 20 | 800 | 36 | 6 | 216 | HBM3e 12hi | Hynix/Micron | 172,800 | |

| AWS | Trainium 3 | 100 | 17 | 1,700 | 36 | 4 | 144 | HBM3e 12hi | Hynix/Samsung/Micron | 244,800 |

| GUC's customers | 10 | 20 | 200 | 24 | 6 | 144 | HBM3e 8hi | Samsung? | 1,152 | |

| Microsoft | Maia 200 | 4 | 29 | 116 | 16 | 4 | 64 | HBM3 | Samsung | 7,424 |

| Maia 300 | 5 | 11 | 55 | 36 | 8 | 288 | HBM4 12hi | Samsung | 15,840 | |

| Meta | MTIA 3 (Iris) | 15 | 10 | 150 | 36 | 8 | 288 | HBM3e 12hi | Hynix/Samsung | 43,200 |

| Total | 1,424 | 18,526 | 3,741,260 | |||||||

| Total HBMdemand (mn Gb) | Total HBMdemand (mn Gb) | 29,930 |

Source: Company data, Morgan Stanley Research (e) estimates. Note: Estimates are compiled using our Asian supply chain checks.

Exhibit 9: AI wafer consumption: at least US$26bn in 2026

| AI chip vendor | Product name | CoWoS capacity allocation (k wafers) | Chips per CoWoS wafer | Implied shipments (k) | Compute die size | Geometry | Compute die units | Wafer consumption (k wafers) | Wafer price (US$) | Wafer revenue TAM (US$ mn) |

|---|---|---|---|---|---|---|---|---|---|---|

| AI GPU (2026e) | ||||||||||

| B300 | 390 | 14 | 5,460 | 850 | 4nm | 2 | 433 | 21,945 | 9,510 | |

| Vera CPU | 90 | 23 | 2,070 | 3nm | ||||||

| NVIDIA | Spectrum/CPX | 60 | - | |||||||

| Rubin R200 | 260 | 8 | 2,080 | 850 | 3nm | 2 | 165 | 26,000 | 4,292 | |

| H200 | 20 | 27 | 540 | 814 | 4nm | 1 | 15 | 21,945 | 331 | |

| MI300 | 3 | 12 | 36 | 110 | 5nm | 8 | 1 | 18,000 | 19 | |

| MI350/375 | 7 | 12 | 84 | 110 | 3nm | 8 | 2 | 26,000 | 64 | |

| AMD | MI455 | 65 | 7 | 455 | 110 | 2nm | 8 | 22 | 28,125 | 620 |

| Venice | 50 | 21 | 1,050 | |||||||

| AI ASIC (2026e) | ||||||||||

| TPU v7p (Ironwood; AVGO) | 145 | 16 | 2,320 | 700 | 3nm | 2 | 152 | 26,000 | 3,942 | |

| TPU v8i (Sunfish; AVGO) | 80 | 12 | 960 | 800 | 3nm | 2 | 72 | 26,000 | 1,864 | |

| TPU v8t (Zebrafish; MediaTek) | 40 | 20 | 800 | 800 | 3nm | 2 | 60 | 26,000 | 1,554 | |

| AWS | Trainium 3 | 100 | 17 | 1,700 | 700 | 3nm | 2 | 91 | 26,000 | 2,357 |

| GUC's customers | 10 | 20 | 200 | 645 | 4nm | 1 | 5 | 21,945 | 107 | |

| Microsoft | Maia 200 | 4 | 29 | 116 | 700 | 3nm | 1 | 3.0 | 26,000 | 79 |

| Maia 300 | 5 | 11 | 55 | 850 | 2nm | 1 | 2.9 | 28,125 | 82 | |

| Meta | MTIA 3 (Iris) | 15 | 10 | 150 | 850 | 3nm | 2 | 11.9 | 26,000 | 310 |

| Total | 1,424 | 18,526 | 1,066 | 25,842 |

Source: Company data, Morgan Stanley Research (e) estimates. Note: Estimates are compiled using our Asian supply chain checks.

Exhibit 7: Global CoWoS consumption, by customer

Source: Company data, Morgan Stanley Research (e) estimates; note: estimates are compiled using our supply chain checks

nuutl ulmp othutmelllo vo. vn lvvlle laun olmuttlelllo

3

2.5

2

1.5

0.5

2Q26e

3Q26e

CAurAn. Marran Ctanlau Dacnarah nntimatao

M

30

25

20

Aligning Blackwell and Rubin chip to HGX/Rack Shipments

We did an analysis of Blackwell chip shipments vs. racks in our last June AI tracker. We think TSMC's Blackwell chip output (calculated by CoWoS-L capacity) aligns more closely with strong demand (as measured by AI capex). We now include HGX (8-GPU per server) in our chip consumption model and treat 9 HGX servers as equivalent to one NVL72 rack. We expect 5.4mn Blackwell units in 2026, and chip volume could meet Grace Blackwell NVL72 demand by 2H26. Our latest checks also suggest close to 7mn Rubin and Rubin Ultra units in 2027, while total Rubin NVL72 server racks could reach 90k in 2027 ( Exhibit 12 ). All Blackwell chip "inventory" turned out to be a supply-chain buffer and will be fully consumed by 2026, so we see no need to worry about inventory issues. We think Rubin will follow a similar pattern. Rubin will start ramping in 3Q26, with rack shipments starting in 4Q26.

Exhibit 10: (old) Blackwell chip vs. GB NVL72 rack shipment

Source: Morgan Stanley Research estimates

Exhibit 11: (new) Blackwell chip vs. GB NVL72 and HGX equivalent rack shipment

Source: Morgan Stanley Research estimates

Exhibit 12: Rubin chip shipments vs. VR NVL72 rack shipments

Source: Morgan Stanley Research estimates

Quarterly shipment (mn units)

3k NVL72

4Q26e

1Q27e

• Rubin chip volume (LHS)

M

AI semis - stock implications, P/E multiples, revenue exposure

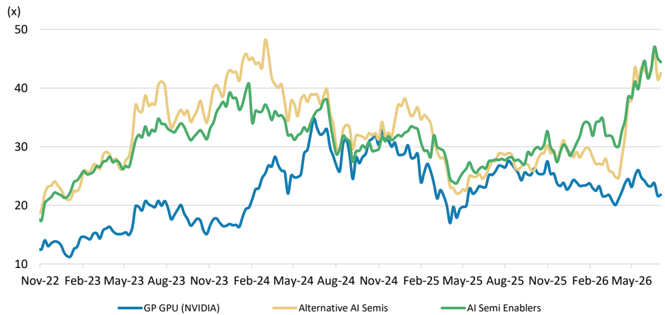

Exhibit 13: P/E multiple trend of AI semis

Note: Alternative AI semis group: AMD, Alchip, Andes, Marvell, Broadcom. AI semi enablers group: TSMC, Synopsys, Cadence, ASML, BESI, Ibiden, KYEC, Advantest. Source: Company data, Morgan Stanley Research.

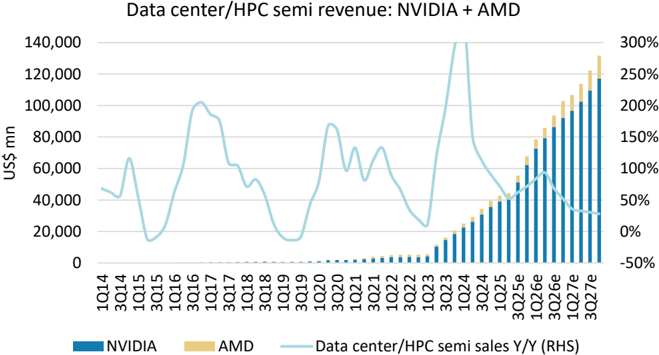

Exhibit 14: We still expect AI chip revenue to rise QoQ

Source: Company data, Refinitiv, Morgan Stanley US Research (e) estimates.

M

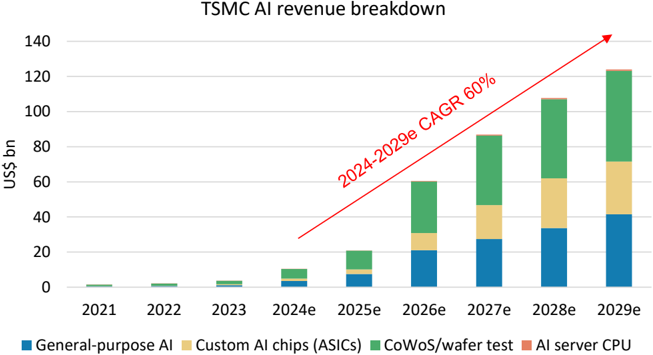

Exhibit 15: TSMC's AI-related revenue 2024-29e CAGR could reach 60%

Source: Company data, Morgan Stanley Research (e) estimates

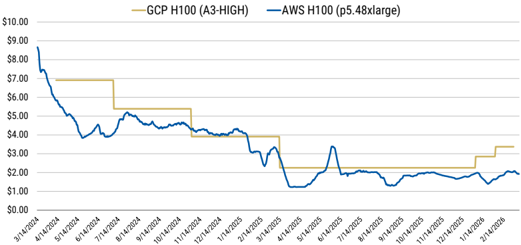

AI GPU and ASIC rental price tracker

Exhibit 16: AI GPU H100 per GPU per hour as of end-March

Source: Company data, Morgan Stanley Research

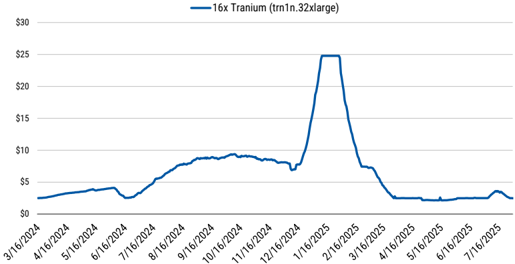

Exhibit 17: AI ASIC equivalent computing power - 16x Inferentia 2 per hour

Source: Company data, Morgan Stanley Research

M

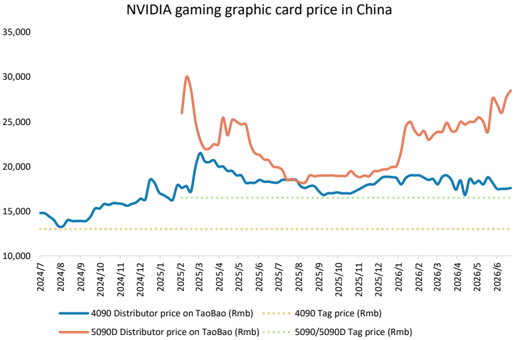

Exhibit 18: NVIDIA 5090 graphic cards pricing has rebounded recently, mainly in response to market expectations for price hikes and strong AI inference demand from China

Source: TaoBao, Morgan Stanley Research, various media (e.g., Vice, Jan. 3, 2026)

M

Key Featured Reports on the AI Supply Chain

Asia-Pacific Technology: AI Supply Chain: Preliminary 2027 TSMC CoWoS Allocation (23 Jun 2026)

Asia-Pacific Technology: AI Supply Chain: Cloud Capex Strength; More CoWoS Allocation for TPU (7 May 2026)

Asia-Pacific Technology: AI Supply Chain: Addressing Questions on Nvidia GPU/LPU and Google TPU (9 Apr 2026)

Greater China Semiconductors: AI Supply Chain Tracker: Key Investor Feedback from GTC/ OFC (23 Mar 2026)

Asia Technology: AI Supply Chain: CPO and ASIC Dynamic Update (3 Mar 2026)

Asia-Pacific Technology: AI Supply Chain: CES implications, ASIC production, China AI chips (6 Jan 2026)

Foundation

Technology: Rise of the AI Agent - Global Implications (19 Apr 2026)

Global Technology: Supply-chain Reorientation (24 Jul 2025)

Global Technology: China - AI: The Sleeping Giant Awakens (13 May 2025)

Global Technology: AI Cloud Capex in the Spotlight (26 Feb 2025)

Global Semiconductors: AI ASIC 2.0: Potential winners (15 Dec 2024)

Global Technology: Global Technology - Dawn of the AI Smartphone Era: Edge AI - Apple Intelligence Fuels Innovation - More Charts, Fewer Words (17 Jul 2024)

Global Technology: AI PCs To Usher In The Next Leg Of PC Market Growth (21 May, 2024)

Key upstream AI supply chain companies

WinWay Technology Co Ltd: AI/HPC Continue to Drive Stronger 3Q Revenue; OW (6 Jul 2026)

ASMPT Ltd: 2Q26 Preview: OSAT and PCB - Dual Growth Engines (6 Jul 2026)

Asia-Pacific Technology: Connecting Dots in Tech Supply Chain: CoPoS, T-Glass/TPU, Glassbridge/FAU (6 Jul 2026)

Greater China Semiconductors: CPO Supply Chain Updates; More on GlassBridge (5 Jul 2026)

Hygon Information Technology Co., Ltd.: Integrated CPU+GPU Compute Platform; Initiate at OW (2 Jul 2026)

Greater China Semiconductors: Old memory: Near-term outlook remains positive (1 Jul 2026)

M

Idea

This report references U.S. Executive Order 14032 and/or entities or securities that are designated thereunder. U.S. persons may be prohibited from buying certain securities of entities named in this report. Readers are solely responsible for ensuring that their investment activities are carried out in compliance with applicable laws.

This report references export controls and/or entities that may be subject to export control restrictions. Readers are solely responsible for ensuring that their investment or trade activities are carried out in compliance with applicable laws.

This report references U.S. Executive Order 14105 and/or entities that may be in scope of such order. U.S. persons may be prohibited from engaging in certain transactions or otherwise require certain other transactions be notified to the U.S. Department of Treasury. Readers are solely responsible for ensuring that their investment or trade activities are carried out in compliance with applicable laws.

M

Disclosure Section

The information and opinions in Morgan Stanley Research were prepared or are disseminated by Morgan Stanley Asia Limited (which accepts the responsibility for its contents) and/or Morgan Stanley Asia (Singapore) Pte. (Registration number 199206298Z) and/or Morgan Stanley Asia (Singapore) Securities Pte Ltd (Registration number 200008434H), regulated by the Monetary Authority of Singapore (which accepts legal responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research), and/or Morgan Stanley Taiwan Limited and/or Morgan Stanley & Co International plc, Seoul Branch, and/or Morgan Stanley Australia Limited (A.B.N. 67 003 734 576, holder of Australian financial services license No. 233742, which accepts responsibility for its contents), and/or Morgan Stanley Wealth Management Australia Pty Ltd (A.B.N. 19 009 145 555, holder of Australian financial services license No. 240813, which accepts responsibility for its contents), and/or Morgan Stanley India Company Private Limited having Corporate Identification No (CIN) U22990MH1998PTC115305, regulated by the Securities and Exchange Board of India ('SEBI') and holder of licenses as a Research Analyst (SEBI Registration No. INH000001105); Stock Broker (SEBI Stock Broker Registration No. INZ000244438), Merchant Banker (SEBI Registration No. INM000011203), and depository participant with National Securities Depository Limited (SEBI Registration No. IN-DP-NSDL-567-2021) having registered office at Altimus, Level 39 & 40, Pandurang Budhkar Marg, Worli, Mumbai 400018, India; Telephone no. +91-22-61181000; Compliance Officer Details: Mr. Tejarshi Hardas, Tel. No.: +91-22-61181000 or Email: tejarshi.hardas@morganstanley.com; Grievance officer details: Mr. Tejarshi Hardas, Tel. No.: +91-22-61181000 or Email: msic-compliance@morganstanley.com which accepts the responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research, and their affiliates (collectively, "Morgan Stanley"). Morgan Stanley India Company Private Limited (MSICPL) may use AI tools in providing research services. All recommendations contained herein are made by the duly qualified research analysts.

For important disclosures, stock price charts and equity rating histories regarding companies that are the subject of this report, please see the Morgan Stanley Research Disclosure Website at www.morganstanley.com/eqr/disclosures/webapp/generalresearch, or contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY, 10036 USA.

For valuation methodology and risks associated with any recommendation, rating or price target referenced in this research report, please contact the Client Support Team as follows: US/Canada +1 800 303-2495; Hong Kong +852 2848-5999; Latin America +1 718 754-5444 (U.S.); London +44 (0)20-7425-8169; Singapore +65 6834-6860; Sydney +61 (0)2-9770-1505; Tokyo +81 (0)3-6836-9000. Alternatively you may contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY 10036 USA.