260521_nmr_semi-renaissance

PDF 原檔:260521_nmr_semi-renaissance_original.pdf

原始內容

ANCHOR REPORT

Global Markets Research 21 May 2026

Greater China Semi

A guide to Semi renaissance in 2026-30F

As metal pitch scalability of advanced chips has not been able to keep up with demanding AI functions, we believe more transistor complexity and heterogeneous integration will be required. In our view, this will not only benefit Semi production equipment (SPE), but also the Semi material sector. We expect ALD (atomic layer deposition), etching, CMP (chemical mechanical planarization), wafer thinning, wafer-to-wafer/chip-to-wafer bonding, and materials related to photoresist, semi wafer, InP, SOI (silicon-on-insulator) wafer, glass core substrate to see strong growth over 2026-30F, as long as AI demand does not fade away. We initiate coverage with Buy ratings on AEMC (4749 TT), Kinik (1560 TT), and Ingentec (4768 TT); maintain our Buy ratings on Besi (BESI NA), Soitec (SOI FP), Dinglong (300054 CH), and Anji (688019 CH); and upgrade GWC (6488 TT) to Buy (from Neutral).

Key themes and analysis in this Anchor report:

- Updates on semi market trends and TSMC’s (2330 TT, Buy) localization plan ·

- High-NA EUV (high numerical aperture extreme ultraviolet lithography), metal-oxide resist and dry deposition/etching process ·

- 3D transistor, backside power delivery and SoIC (system on integrated chips) ·

- Wafer-bonded NAND and DRAM-on-logic ·

- InP (indium phosphide), photonics SOI, and glass core substrate ·

Research Analysts

Asia Technology

Donnie Teng - NIHK donnie.teng@nomura.com +852 2252 1439

Frank Fan - NIHK frank.fan@nomura.com +852 2252 2195

Aaron Jeng, CFA - NITB aaron.jeng@nomura.com

+886(2) 21769962

Anne Lee, CFA - NITB anne.lee@nomura.com

+886(2) 21769966

Eric Chen, CFA - NITB eric.chen@nomura.com +886(2) 21769965

Vivian Yang - NITB vivian.yang@nomura.com

+886(2) 21769970

Production Complete: 2026-05-20 21:56 UTC

EQUITY: TECHNOLOGY

Greater China Semi

EQUITY: TECHNOLOGY

A guide to Semi renaissance in 2026-30F

Revolution in Semi materials, spare parts and SPE being driven by rapid migration in advanced technology

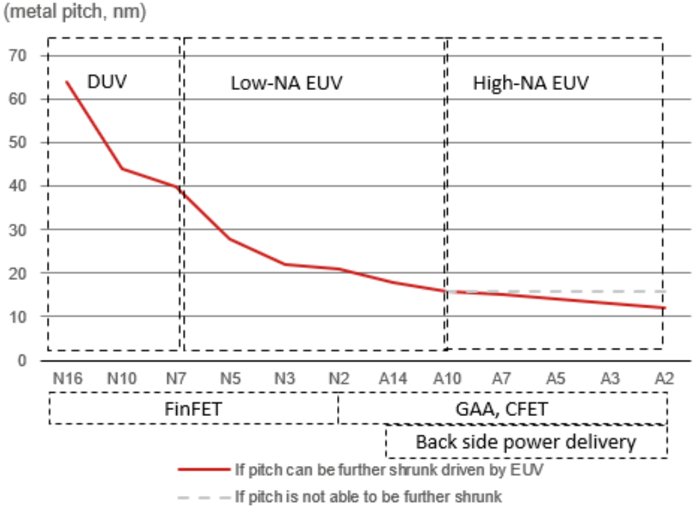

When metal pitch scalability can’t keep up with demanding AI functions, more transistor complexity and heterogeneous integration are required

AI infrastructure and Agentic AI demand are driving evolution of already fast-moving Semi technologies at a speed that has never been seen before in history. We believe advanced node migration alone can’t fulfill the requirements from all perspectives, which include not just computing performance, but also more efficient power saving, better heat dissipation, wider data process bandwidth, faster electrical and optical signal transmission speed, and more responsive reaction time at the physical AI interfaces. As a result, in our view, complicated 3D transistor designs and backside power delivery (BPD), with heterogeneous integration and different types of materials have quickly started playing a more important role. We believe this is changing the landscape of the Semi market’s growth that used to be mainly driven by transistor pitch scalability, which primarily follows the Moore’s Law. We initiate coverage with Buy ratings on AEMC, Kinik, and Ingentec; maintain Buy on Besi, Soitec, Dinglong, and Anji; and upgrade GWC to Buy (from Neutral).

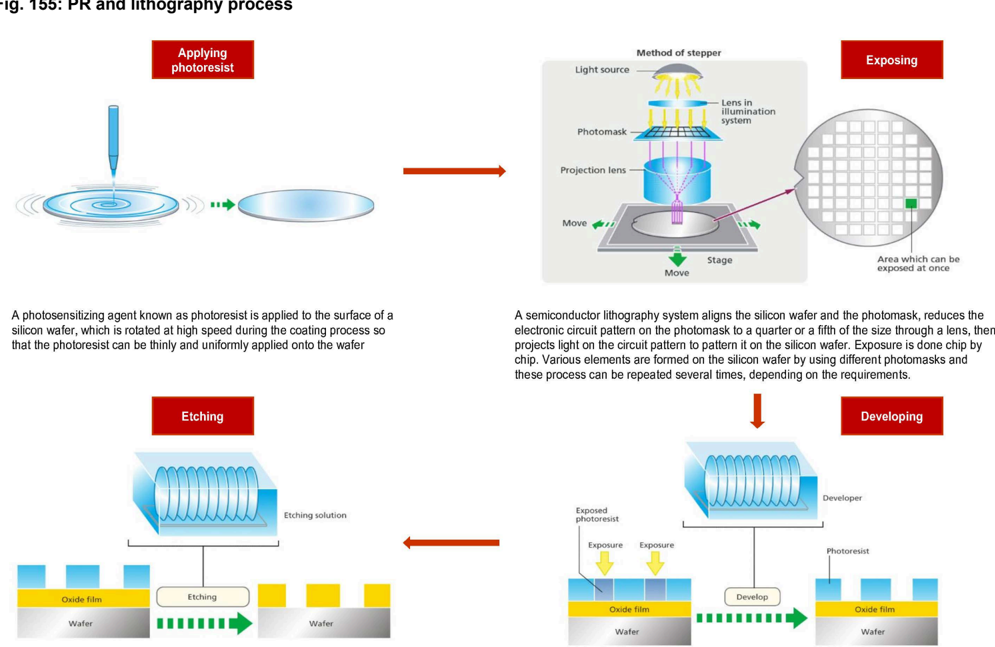

Photoresist and lithography process upgrade is necessary when high-NA EUV is available in the market

With a higher NA (numerical aperture) light source, the thinner photoresist layer reduces the risk of pattern collapse, but also requires more advanced photoresist material that can better capture photons, with an improved etching process. As a result, we believe this will lead to the adoption of new metal-oxide resists (MOR), while dry deposition and etching could replace the existing wet process. In our view, from TSMC’s perspective, Lam Research (LRCX US, Not rated) could be the ultimate winner as it can provide dry deposition and etching equipment with JSR (unlisted) being the major supplier of MOR material. We expect this will increase the total addressable market (TAM) for photoresist and photoresist auxiliary due to the upgrade in materials.

3D transistor, BPD and SoIC will play more important role

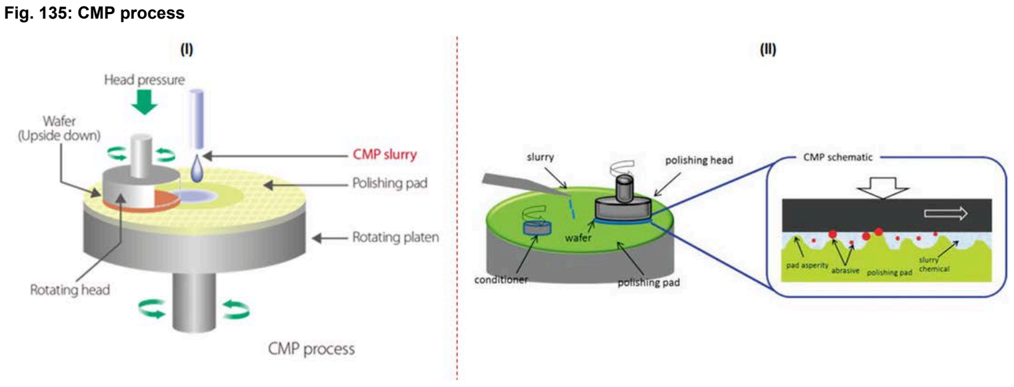

Besides pitch scalability, we believe the Semi industry is focusing more on device/transistor structure innovation, particularly on more complicated 3D transistors, such as the current gate-all-around FET (GAAFET); while in the future, transistors will be stacked on top of each other which is called a complementary FET (cFET) device. At the same time, BPD has also been introduced that allows both additional space for logic transistors and power saving. While a SoIC (system on integrated chips) leaves room for design flexibility so that IC designers can vertically integrate ICs with different functions. We expect ALD, etching, CMP, wafer thinning, wafer-to-wafer bonding and chip-to-wafer hybrid bonding demand to grow rapidly. Hence, in our view, Semi wafer consumption would increase as well.

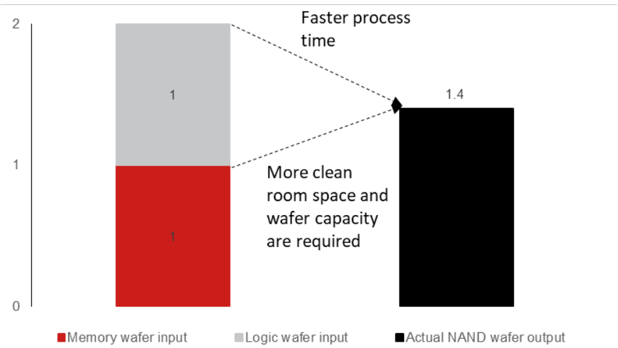

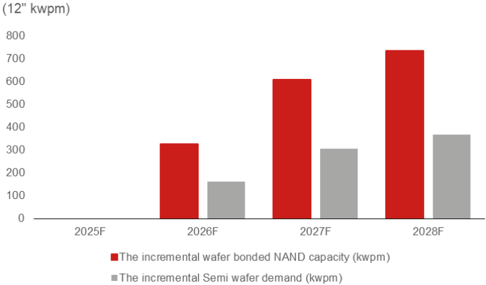

Wafer-bonded NAND and DRAM-on-logic to improve the performance of memory

Density and bandwidth requirements are growing considerably across memory hierarchies in both cloud and physical AI applications. A wafer-bonded NAND increases the NAND storage density per memory die while the DRAM-on-logic unlocks the memory bandwidth between DRAM and a logic SoC. Hence, we believe the demand for CMP, wafer thinning, and wafer-to-wafer bonding should grow, along with more Semi wafer consumption.

Combinations of materials are critical in SiPh and glass core substrates

Materials such as silicon photonics (SiPh) and glass core substrates have quickly emerged to meet the demand for AI networking. SiPh makes a compact optical transceiver with better integration and scalability, while glass core substrates achieve better heat dissipation and lower warpage. Hence, the demand for multiple materials such as InP, photonics SOI and glass core substrates should grow rapidly, in our view.

Research Analysts

Asia Technology

Donnie Teng - NIHK donnie.teng@nomura.com +852 2252 1439

Frank Fan - NIHK frank.fan@nomura.com +852 2252 2195

Aaron Jeng, CFA - NITB aaron.jeng@nomura.com

+886(2) 21769962

Anne Lee, CFA - NITB anne.lee@nomura.com +886(2) 21769966

CW Chung - NIHK cwchung@nomura.com +852 2252 6075

Eric Chen, CFA - NITB eric.chen@nomura.com +886(2) 21769965

Vivian Yang - NITB

vivian.yang@nomura.com +886(2) 21769970

Japan technology

Manabu Akizuki - NSC manabu.akizuki@nomura.com +81 3 6703 1185

Atsushi Yoshioka - NSC

atsushi.yoshioka@nomura.com +81 3 6703 1176

Virginia Wang - NSC virginia.wang@nomura.com +81 3 6703 1215

Japan chemicals & textiles

Shigeki Okazaki - NSC shigeki.okazaki@nomura.com +81 3 6703 1170

Daiki Ban - NSC daiki.ban@nomura.com +81 3 6703 1124

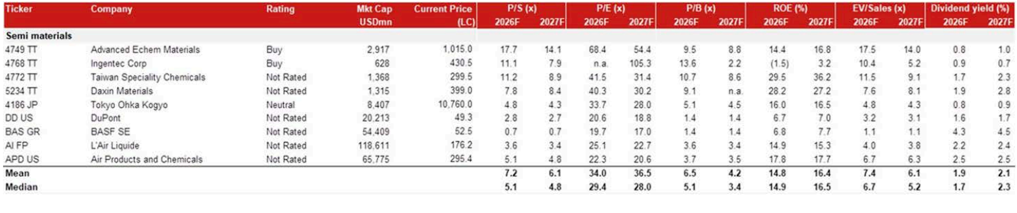

Ticker

Semi materials

4768 TT

4749 TT

4772 TT

4186 JP

5234 TT

DD US

BAS GR

AI FP

Mean

APD US

Median

1560 TT

ENTG US

8028 TT

MMM US

300054 CH

6140 JP

688019 CH

Mean

Median

6488 TT

688126 CH

SOI FP

3532 TT

002428 CH

AXT US

Mean

Median

Advanced Echem Materials

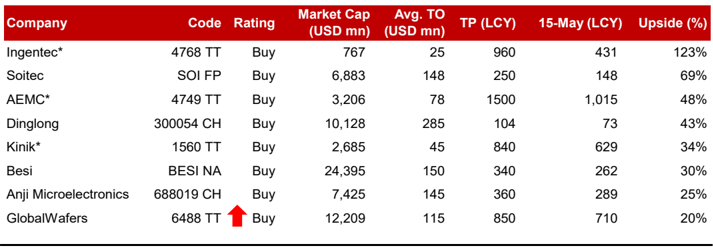

Fig. 1: Stocks for action

Rating

Buy

Buy

Not Rated

PIE (x)

2026F

2027F

68.4

n.a.

41.5

54.4

105.3

31.4

Mkt Cap

USDmn

2,917

628

1,368

Current Price

(LC)

1,015.0

430.5

299.5

P/S (x)

2026F

2027F

17.7

11.1

11.2

14.1

7.9

8.9

P/B (x)

2026F

2027F

9.5

13.6

10.7

8.8

2.2

8.6

9.2

31.7

| Company | Code | Rating | Market Cap (USD mn) | Avg. TO (USD mn) | TP (LCY) | 15-May (LCY) | Upside (%) |

|---|---|---|---|---|---|---|---|

| Ingentec* | 4768 TT | Buy | 767 | 25 | 960 | 431 | 123% |

| Soitec | SOI FP | Buy | 6,883 | 148 | 250 | 148 | 69% |

| AEMC* | 4749 TT | Buy | 3,206 | 78 | 1500 | 1,015 | 48% |

| Dinglong | 300054 CH | Buy | 10,128 | 285 | 104 | 73 | 43% |

| Kinik* | 1560 TT | Buy | 2,685 | 45 | 840 | 629 | 34% |

| Besi | BESI NA | Buy | 24,395 | 150 | 340 | 262 | 30% |

| Anji Microelectronics | 688019 CH | Buy | 7,425 | 145 | 360 | 289 | 25% |

| GlobalWafers | 6488 TT | Buy | 12,209 | 115 | 850 | 710 | 20% |

8.0

6.3

41.0

Note: Stocks on which we are initiating coverage in this Anchor report are marked with an *; closing price as on 15 May 2026 Note 2: n.a. 91.1 3.5

Source: Bloomberg Finance L.P., Nomura estimates

Ingentec: Leading specialty gas supplier with (Through-Glass Via) TGV capability in Taiwan

AEMC: Leading photoresist and photoresist auxiliary supplier in Taiwan

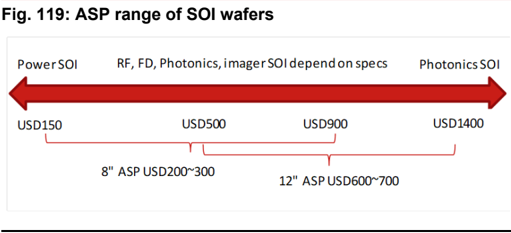

Soitec: Largest SOI wafer company in the world

Dinglong: Leading CMP-related material supplier in China

Besi: Leading hybrid bonding tool company in the world

Kinik: Leading CMP pad conditioner and reclaim wafer supplier in Taiwan

Anji Microelectronics: Leading CMP-related material supplier in China

GlobalWafers: Third largest Semi wafer supplier in the world

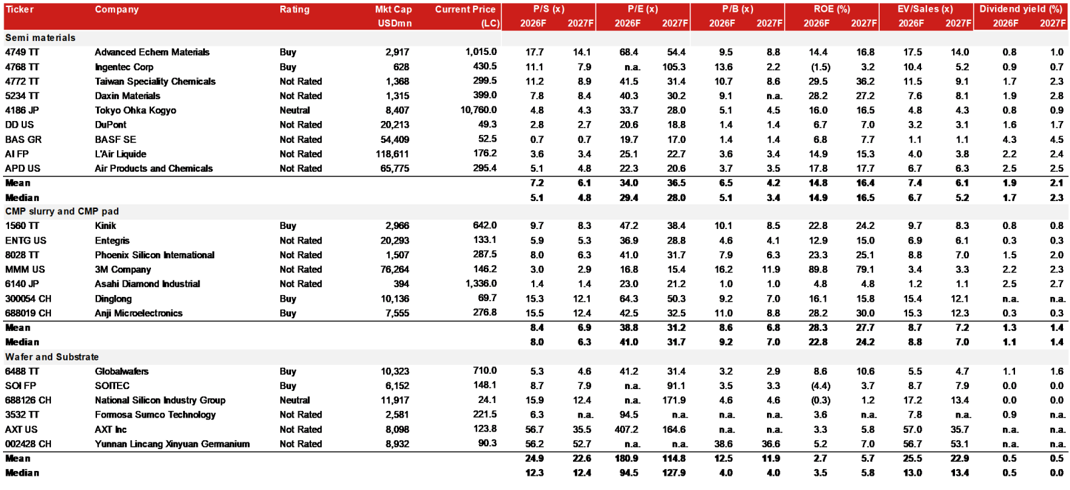

Fig. 2: Valuation comparison table

Note: Bloomberg consensus for Not rated stocks; data as on 15 May 2026

Source: Bloomberg Finance L.P., Nomura estimates

6.3

56.7

56.2

24.9

12.3

n.a.

35.5

52.7

22.6

12.4

n.a.

94.5

407.2

n.a.

180.9

94.5

171.9

n.a.

164.61

n.a.

114.8

127.9

4.6

n.a.

n.a.

38.6

12.5

4.0

7.0

2.9

3.3

4.6

n.a.

n.a.

36.6

11.9

4.0

ROE (%)

2026F

2027F

14.4

(1.5)

29.5

28.2

16.0

6.7

6.8

14.9

17.8

14.8

14.9

22.8

12.9

23.3

89.8

4.8

‘6.1

28.2

28.3

22.8

8.6

(4.4)

(0.3)

3.6

3.3

5.2

2.7

16.8

3.2

36.2

27.2

16.5

7.0

7.7

15.3

17.7

16.4

16.5

24.2

15.0

25.1

79.1

4.8

15.8

30.0

27.7

24.2

10.6

3.7

1.2

n.a.

5.8

7.0

5.7

5.8

EV/Sales (x)

2026F

2027F

17.5

10.4

11.5

7.6

4.8

3.2

1.1

4.0

6.7

7.4

6.7

9.7

6.9

8.8

3.4

1.2

15.4

15.3

8.7

8.8

5.5

8.7

17.2

7.8

57.0

56.7

25.5

13.0

14.0

5.2

9.1

8.1

4.3

3.1

1.11

3.8

6.3

6.1

5.2

8.3

6.1

7.0

3.3

1.1

12.1

12.3

7.2

7.0

4.7

7.9

13.4

n.a.

35.7

53.1

22.9

13.4

0.8

0.9

1.7

1.9

0.8

1.6

4.3

2.2

2.5

1.9

1.7

0.8

0.3

1.5

2.2

2.5

n.a.

0.3

1.3

1.1

1.1

0.0

0.0

0.9

n.a.

n.a.

0.5

0.5

1.0

0.7

2.3

2.8

0.9

1.7

4.5

2.4

2.5

2.1

2.3

0.8

0.3

2.0

2.3

2.7

n.a.

0.3

1.4

1.4

1.6

0.0

0.0

n.a.

n.a.

n.a.

0.5

0.0

2026

2027

Executive summary

Mentioned in this report

Yes

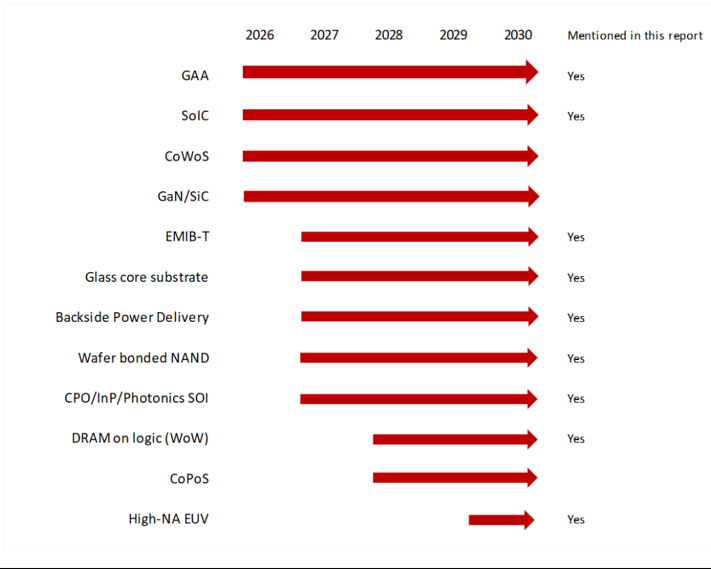

Guide to the evolution of key Semi processes and materials in 2026-30F

AI infrastructure and Agentic AI demand are driving the evolution of already fast-moving Semi technologies at a speed that has never been seen before in history. The advanced node migration alone can’t fulfill the requirements from all perspectives, which include not just computing performance, but also more efficient power saving, better heat dissipation, wider data process bandwidth, faster electrical and optical signal transmission speed, and more responsive reaction time at the physical AI interfaces. As a result, in our view, 3D transistor design and BPD, with heterogeneous integration across 2.5D/3D packaging and different types of materials have quickly started playing a more important role. We believe this is changing the landscape of Semi market growth that used to be mainly driven by transistor density growth, which follows the Moore’s Law. But it is slowing down quickly, particularly when the next-generation EUV and high-NA EUV are not likely to be widely adopted by the Semi industry until 2029-30F at the earliest, in our view. In this report, we will discuss the evolution of most key Semi technologies over 2026-30F (Fig. 3 - 4 ).

Fig. 3: Evolution of key Semi technologies in 2026-30F

Source: Nomura research

2028

2029

2030

Fig. 4: Key Semi technologies, market growth, beneficiaries, and timeline

| Technology | 2025-2030 | Key Equipment | Key Materials | Major Beneficiaries | Note |

|---|---|---|---|---|---|

| GAA(Gate-All- Around) | CAGR >20% | ALD (Atomic Layer Deposition) Selective Etch Epitaxy (Si/SiGe Superlattice) CMP Metrology / Inspection | High-k Dielectrics (HfO₂) SiGe Superlattice Wafers Work-Function Metals (TiN, TiAl) Molybdenum (contact metal) Metal Oxide Resists | ASMInternational, Applied Materials,Lam Research, Tokyo Electron, KLA Tencor | CAGRof over 20%as part of the normal advanced node migration. Will start growing from 2026F. |

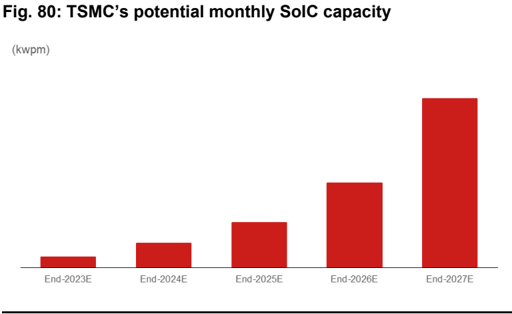

| SoIC (System on Integrated Chip) | >30% | Hybrid Bonder (D2W) TSV Etch &Fill Wafer Thinning/CMP Temp. Bond / Debond Optical Inspection RDL Deposition | Cu-Cu Bonding Interfaces SiCN / SiO₂ Dielectrics CMPSlurries (Cu) Underfill Materials | BESI, Applied Materials, Ebara, Disco, Onto Innovation, Camtek | CAGRof over 30%due to the very low base in 2025;we expect it to rapidly increase in 2026-27F due to TSMC’s SoIC capacity expansion and potential adoptionbyHBM customers. Will start growing from 2026F. |

| Glass Core Substrate | >40% | TGV Laser Drill / Etch Panel-Level Lithography RDL / Metallization (Sputter, Plate) Glass Panel Handling Metrology (Warpage, Defect) | High-Purity Glass Panels Cu / Ti / WMetallization ABF-type Dielectric Films CMPSlurries (Glass) | Ibiden, Unimicron, SEMCO, Toppan Absolics (SKC), JNTC, LG Innotek, Ingentec LPKF, DRLaser, E&R Engineering, Innostar Service Schott, AGC, Corning | CAGRof over 40%as it’s a totally new technology/material. Will start growing from 2027F at the earliest. |

| Backside Power Delivery (BSPDN) | >20% | Nano-TSV Etch &Fill Wafer Thinning/CMP Carrier Wafer Bonding Backside Litho (DUV / EUV) Backside Metal Deposition EDA Tools (P&R re-design) | CMPSlurries &Pads Cu / Ru / MoInterconnects Low-k Dielectrics Carrier Wafer Adhesive | Disco, Ebara, Applied Materials, EVG, TEL, SUSS Microtec, Entegris, CMCMaterials, Kinik,3M | CAGRof over 20%as part of the normal advanced node migration. Will start growing from 2027F. |

| Wafer Bonded NAND(Xtacking- type) | >20% | W2WHybrid Bonder High Aspect Ratio Etch (60:1+) ALD / CVD(multi-layer stack) CMP(post-bond planarize) Optical Inspection | SiO₂ / SiN Multi-Layer Stacks W/Mo(Wordline metals) Cu-Cu Bonding Interface Polysilicon Channels | EVG, TEL, SUSS Microtec, LamResearch,AMEC | CAGRof over 20%as part of the normal NANDproduction technology migration. Will start growing from 2027F. |

| DRAM-on-Logic (LPDDRW2W) | >30% | W2WHybrid Bonder TSV Etch &Fill ALD (High-k Capacitor) Wafer Thinning / Grinding Advanced Litho (EUV for Logic) Metrology (Alignment) | High-k Capacitor Dielectrics (ZrO₂, HfO₂) IGZO / Oxide Channels (future) Cu-Cu Bonding Interface Ru / MoInterconnects | EVG, TEL, SUSS Microtec | CAGRof over 30%as we believe it would not pick up meaningfully until 2028F driven by edge AI/physical AI applications. Will start growing from 2028F. |

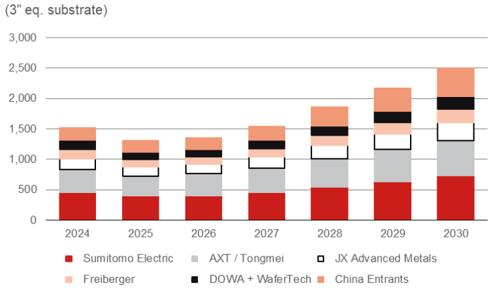

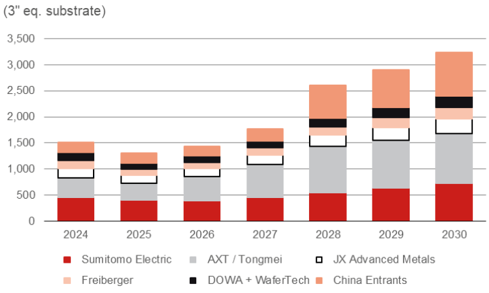

| InP-Based Lasers | >20% | MOCVD/MBEEpitaxy III-V Wafer Processing Facet Coating / Cleaving Die Bonding / Packaging Burn-In &Reliability Test | InP Substrates (2”→6”) InGaAsP / InGaAlAs Epitaxy High-Purity Indium &Phosphorus AR/HR Coatings | Lumentum, Coherent (II-VI) Sumitomo Electric, AXT, JX Metals Landmark, VPEC, Win Semi, IQE Aixtron | CAGRof over 20%as we believe growth can reach very high in 2025- 27F, but moderate in 2028-30F if more meaningful capacity is built across the industry, particularly in China. Will start growing from 2026F. |

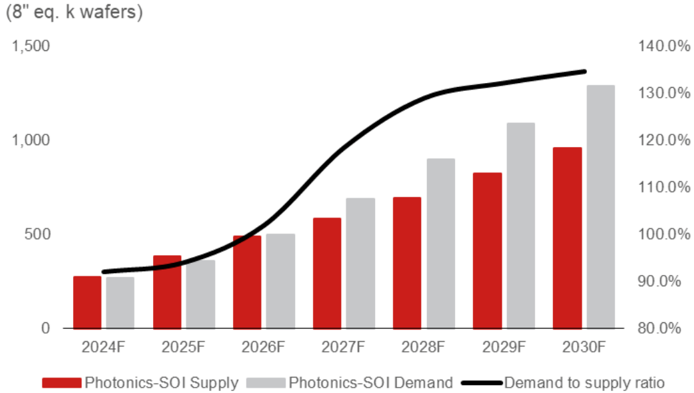

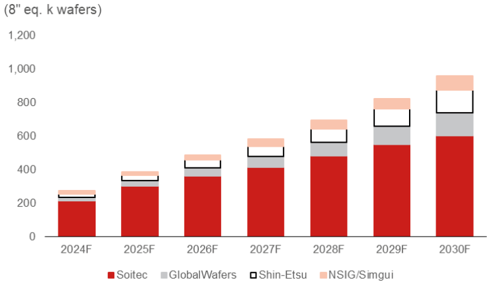

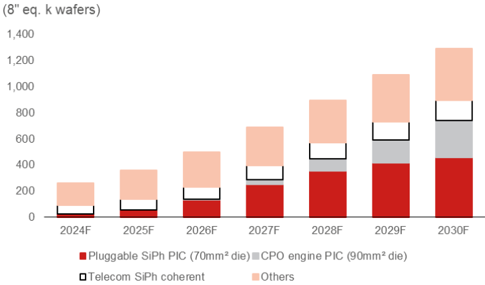

| Photonics SOI (SiPh) | >30% | SOI Wafer Fab (DUV Litho) Ge Epitaxy (Photodetectors) Edge / Grating Coupler Fab Wafer Bonding (InP-on-Si) CPOPackaging Tools | Photonic SOI Wafers (220nm/400nm Si) SiN (Low-Loss Waveguides) Ge (Photodetectors) LiNbO₃ (Modulators, emerging) | Soitec, GlobalWafers, NSIG/Simgui, Shin-Etsu | CAGRof over 30%, which is higher than that of InP material, as Photonics SOI’s (SiPh) growth momentumwill start later than that for InP substrate, mainly driven by SiPh used in CPOafter 2027F. Will start growing from 2027F. |

| High-NAEUV | >40% | High-NA EUV High-Power EUV Light Source Anamorphic Optics &Mirrors Metal Oxide / Dry Deposition NewReticle / Mask Infrastructure Advanced Metrology and Overlay | Metal Oxide Photoresist (MOR) EUV Pellicles Ru-capped Multilayer Mirrors Ultra-Low-Defect EUV Mask Blanks Hydrogen Gas Dry Resist Chemicals | ASML Carl Zeiss, Trumpf, AGC/Mitsui, Hoya/AGC, JSR/Inpria, LamResearch,AEMC KLA Tencor/Lasertec, Guden/Entegris | CAGRof over 40%depending on whether TSMCwill adopt high-NA EUV on A10 node or further push it out. Will start growing from 2029F at the earliest. |

Source: Nomura research

Lalgel tie

70

cultaul ar eao, wollel tlle vowel bullouttiytiull

3D transistor, BPD, and advanced packaging such as SoIC and CoWoS/CoPoS will play more important role

60

50

40

30

20

10

0

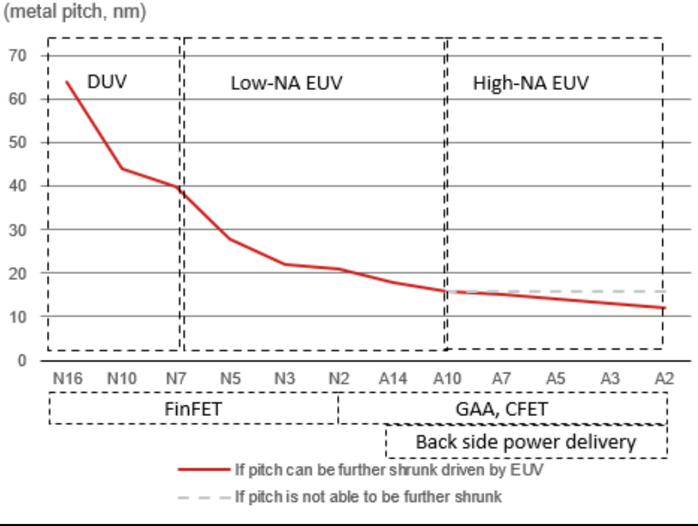

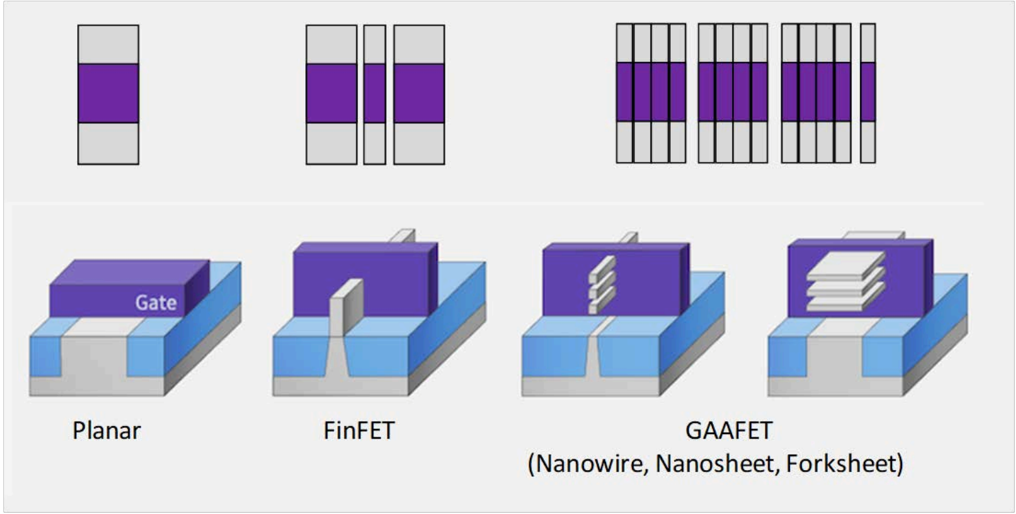

We believe the Moore’s Law may still continue along with the pitch to scale down further once the leading Semi companies start adopting high-NA EUV at around 1nm (A10). In this case, we think the Semi market giants, such as ASML (ASML US, Not rated) and TSMC, could still be able to widen their technology leadership over other Semi companies in the next decade. However, in our view, if high-NA EUV eventually proves to be less cost effective and is pushed out further, pitch scaling could no longer remain a key topic in the future, where the whole Semi industry will focus more on device/transistor structure innovation, from 2D to 3D structure and transistors that are stacked on top of each other, called a cFET device, compared to the current GAAFET type.

Fig. 5: Metal pitch scaling - historical trend

N16 N10

Source: Nomura estimates, IMEC

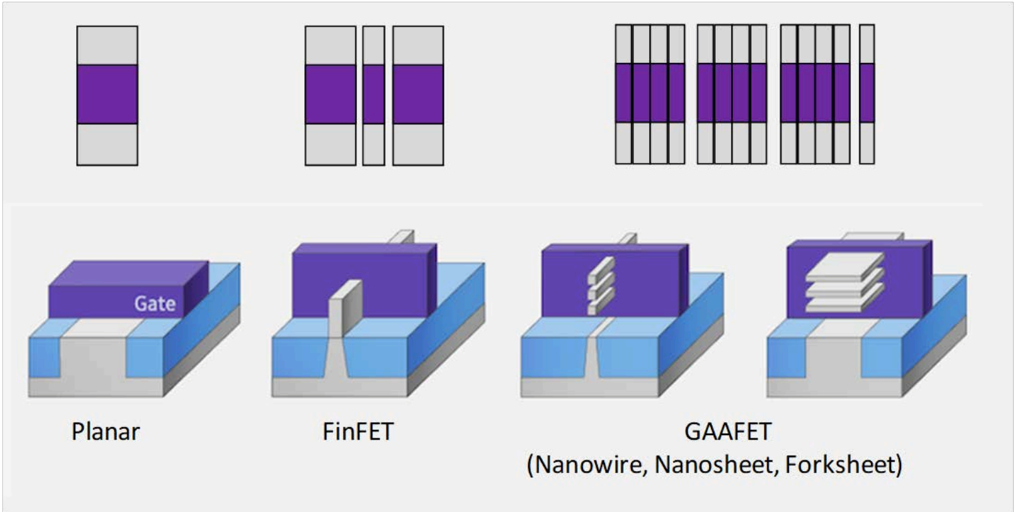

Fig. 6: Contact area between gate and source/drain electrodes

Larger the contact areas, better the power consumption

Source: Samsung, Nomura research

(Nanowire, Nanosheet, Forksheet)

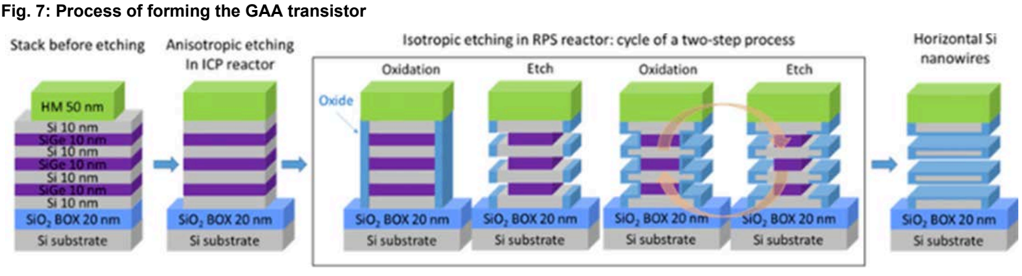

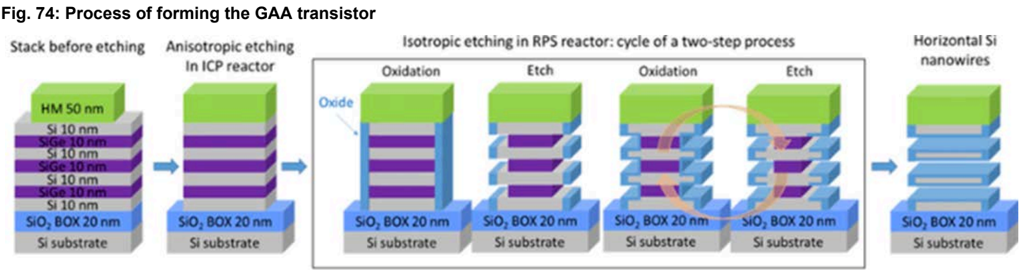

Oxide

The approach to fabricate stacked-Si nanowires for GAA (gate-all-around) devices in Fig. 7 includes: 1) a stack of Si/SiGe layers grown on a silicon wafer; 2) anisotropic plasma etching (vertical direction) achieved in an inductively coupled plasma (ICP) reactor; 3) isotropic and selective etching (both vertical and horizontal directions) of SiGe layers in an RPS (remote plasma source) reactor; 4) the cycle of a two-step process alternating oxidation (atomic layer deposition; ALD) and etch; and 5) the release of horizontal Si nanowires. As a result, we believe the deposition and etching processes will be increasing more meaningfully. Si substrate nanowires

SIO, BOX 20 nm

Si substrate

Source: Journal of Vacuum Science & Technology A Vacuum Surfaces and Films, Nomura research

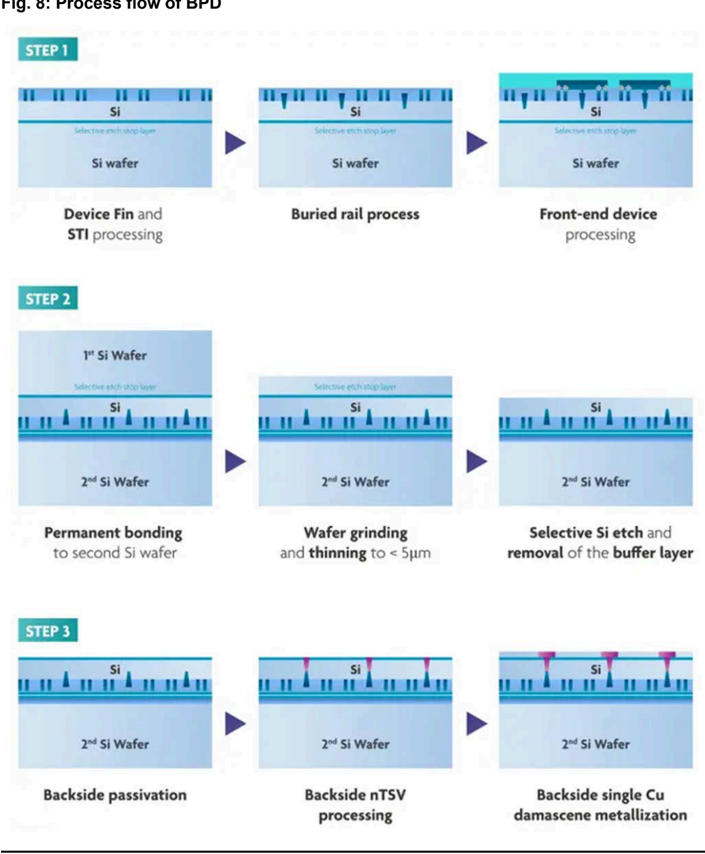

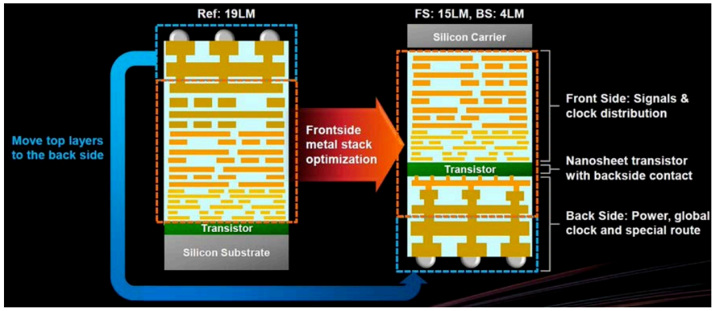

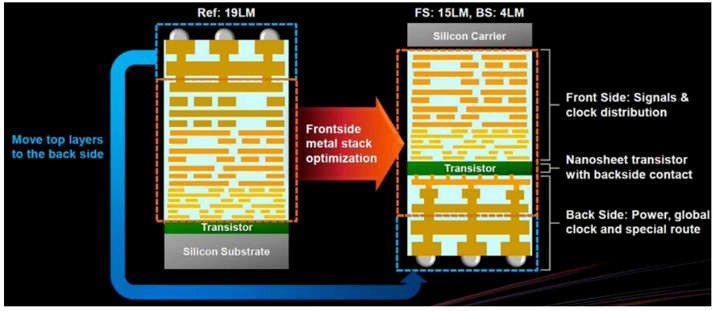

A power delivery network is designed to provide power supply and reference voltage to the active devices on a die most efficiently. A BPD network decouples the power delivery network from the signal network by moving the entire power distribution network to the backside of the silicon wafer, which today serves only as a carrier. From there, it enables direct power delivery to the standard cells through wider, less-resistive metal lines, without the electrons needing to travel through the complex BEOL stack. This approach promises to benefit the IR drop, improve the power delivery performance, reduce routing congestion in the BEOL, and when properly designed, allow for further standard cell height scaling.

As two silicon wafers will be used in the back-side power delivery process, one being the silicon wafer acting as an interposer in between the signal network, and another acting as the permanent silicon carrier of the device, we expect the usage of silicon wafers to increase along with wafer bonding. On the other hand, we believe the wafer bonding, CMP, grinding and thinning process will increase as well to form the silicon interposer in between the signal and power network.

Isotropic etching in RPS reactor: cycle of a two-step process

Oxidation

Etch

Oxidation

Etch

wIlNI

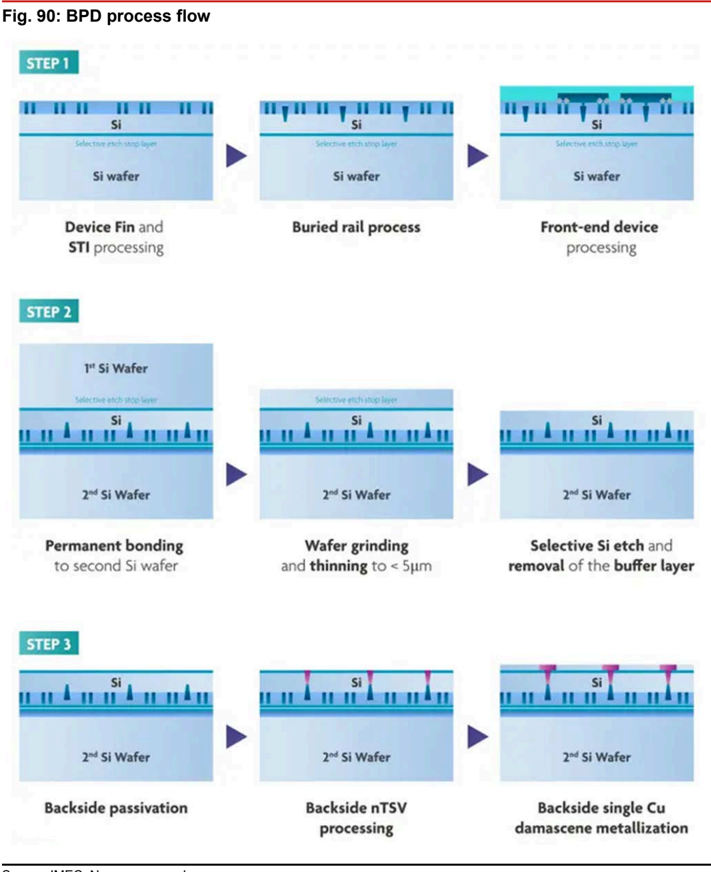

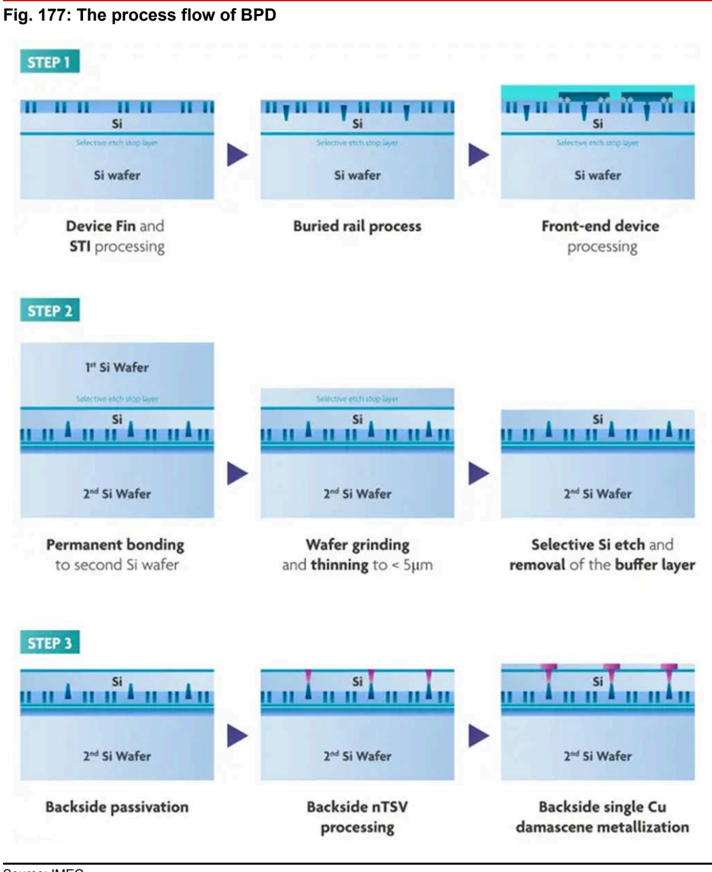

Fig. 8: Process flow of BPD

STEP 2

Permanent bonding

STEP 3

Backside passivation

Source: IMEC, Nomura research

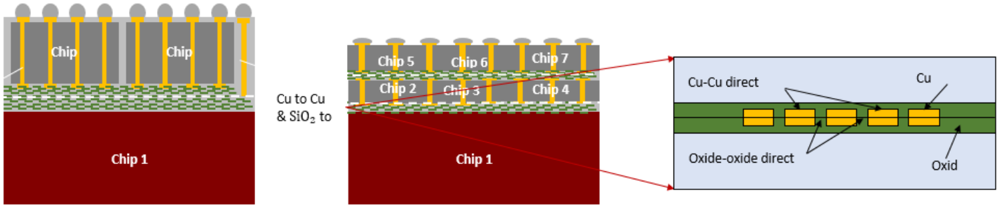

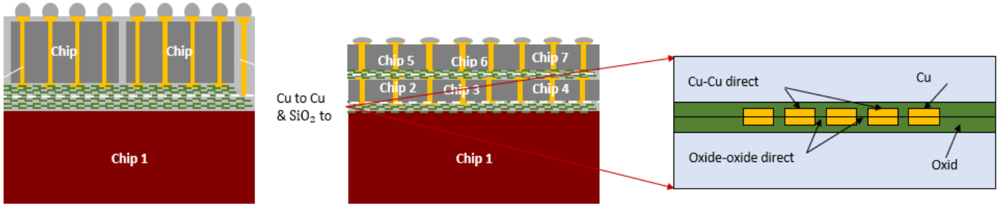

An alternative solution to the high-NA EUV stitching issue is the avoidance of large dies altogether. In advanced packaging such as SoIC, by using hybrid bonding technology, it has been proven that it is possible to maintain high performance even while separately fabricating parts of circuits that previously had been fully integrated into a single die. This is currently being done to improve the cost-effectiveness of advanced lithography. For example, the high-performance logic circuits of AMD’s (AMD US, Not rated) EPYC processor have been fabricated using 7 nm technology, while input/output functions have been fabricated using lower-cost 14 nm processes. In other applications, memory access rates are improved using advanced packaging technology. It may also be possible to achieve high levels of performance with maximum die sizes that can fit into the exposure fields of high-NA EUV exposure tools.

Fig. 9: Chip-to-chip/wafer hybrid bonding

Source: Nomura research

Chip 5

Chip 6

Chip 7

HiT i Tin

Oxide-oxide direct

Cu

Oxid

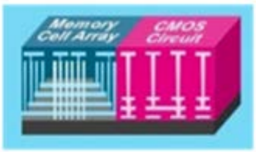

Memory

Cell Array

CMOS wafer metal VIAs(Vertical Interconnect Accesses)

Memory wafer

Cell array

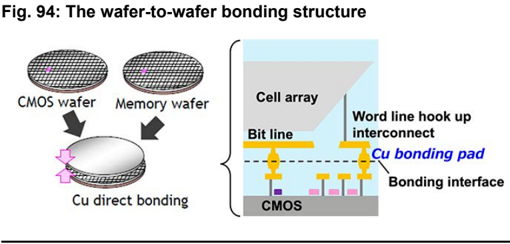

Wafer-bonded memory (wafer-bonded NAND; DRAM-on-logic) to maximize performance and bandwidth

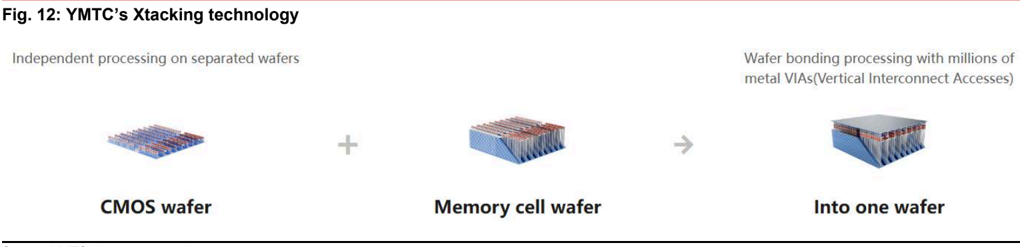

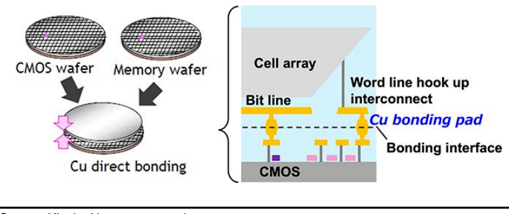

Bit line

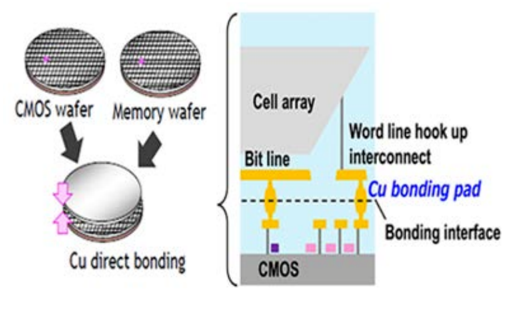

The wafer-bonded NAND technology was introduced by YMTC (unlisted) for the first time in 2018. YMTC’s wafer-bonded technology is called Xtacking, and can also be called CMOS directly bonded to array (CBA) technology, which makes it possible for the CMOS circuit (logic) wafers and memory cells array wafers to be manufactured separately and bonded together. Before the launch of CBA architecture, 3D NAND architectures in the market were divided into traditional side-by-side structure and CnA (CMOS next to Array) architecture.

Word line hook up interconnect

Cu bonding pad

Bonding interface

CMOS

Since the two types of wafers are manufactured in parallel, there is also the added benefit of shortened production times compared to the conventional method. Performing hightemperature processing solely on the memory cell array wafer makes it possible to achieve the optimal temperature to ensure reliability without having to consider the impact on the CMOS circuit. By separating the wafer manufacturing processes, the performance of the CMOS circuit and the memory cell array can be maximized.

Fig. 10: 3D NAND: CNA vs CBA structure

Source: Kioxia, Nomura research

Source: YMTC, Nomura research

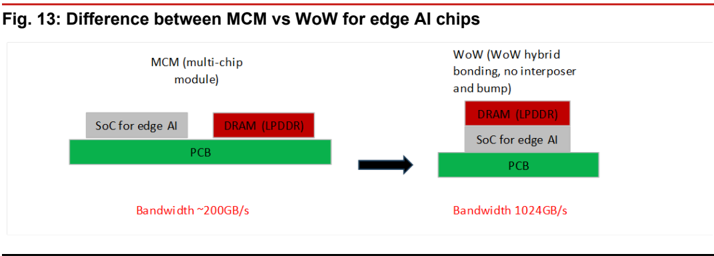

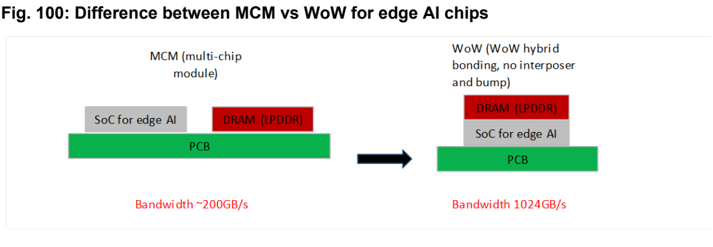

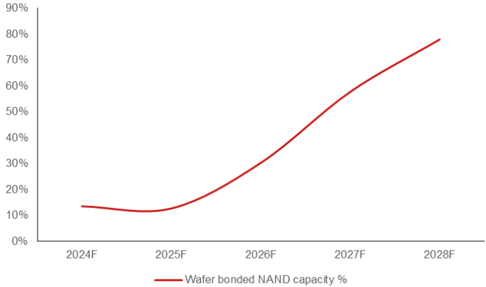

AI inference is a memory-bound task in the smart-edge domain requiring high memory bandwidth and energy efficiency with modest computing power between 45 and 100+ TOPS (trillions of operations per second). The DRAM-on-logic WoW can achieve 1TB/s bandwidth for throughput higher than 100 TPS (tokens per second). We believe the strong momentum for DRAM-on-logic could start from 2028F, led by AI agents in automotive smart cockpit, premium smartphones/PCs, and robotics.

Fig. 11: Wafer-to-wafer bonding structure

Source: Kioxia, Nomura research

Into one wafer

nm module)

WoW (WoW hybrid bonding, no interposer

0.55 NA EUV

>>10X higher etch and bump)

building blocks

0.33 NA EUV

4X more photons absorbed / volume

Source: Nomura research

Resist

Transfer layer selectivity & contrast

Si

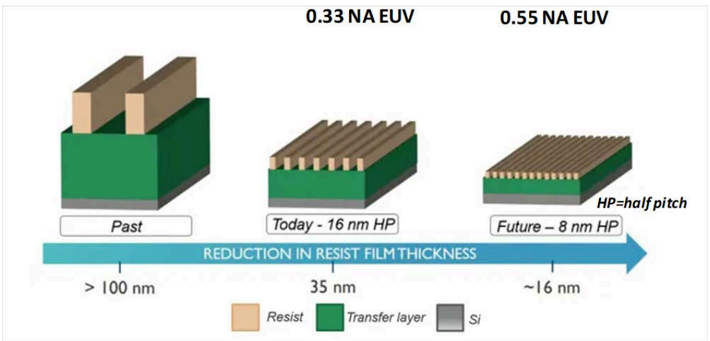

Photoresist upgrade is critical along with high-NA EUV to drive further scalability of metal pitches

With a higher NA, photons strike the wafer at a shallower angle. That requires thinner photoresist layers to avoid shadowing. The upside is that a thinner resist layer reduces the risk of pattern collapse, as the aspect ratio of resist features is smaller. However, it also provides less protection for the wafer. In addition, long etch processes used to create high-aspect ratio wafer features can erode the resist layer, ultimately degrading the transferred pattern. With less material, a thinner resist also captures fewer photons, potentially making roughness and other stochastic effects worse.

At present, metal-oxide resists are probably the leading alternative to photoacid-driven chemistries, or chemically amplified resists (CAR). Based on a metal-oxide core, surrounded by ligands that tune solubility, crosslinking, and other properties, these resists offer inherently good etch resistance. The dense core absorbs more energy, too, attenuating electron energy and reducing blur.

Fig. 14: Reduction in photoresist film thickness

Source: Cadence, Nomura research

material

Schott

AGC

Corning

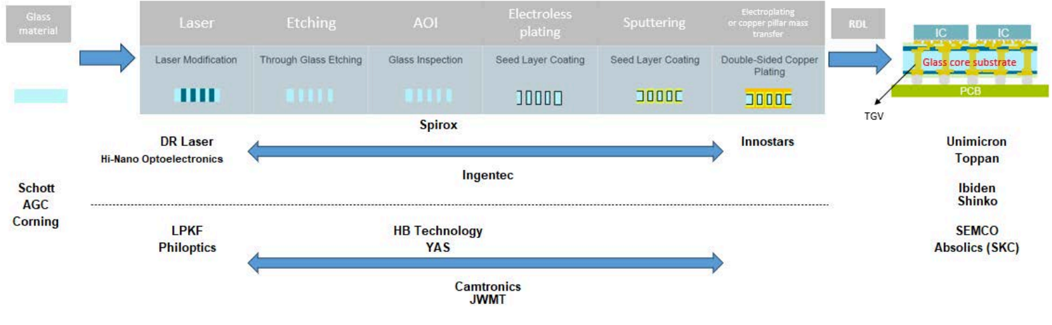

Laser Modification

Etching

Through Glass Etching

AOL

Glass Inspection

Electroless plating

Seed Layer Coating

Sputtering

Seed Layer Coating

Electroplating or copper pillar mass

transter

Double-Sided Copper

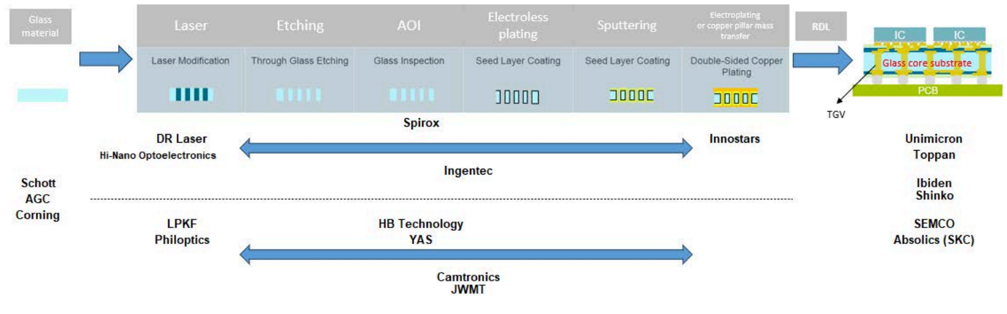

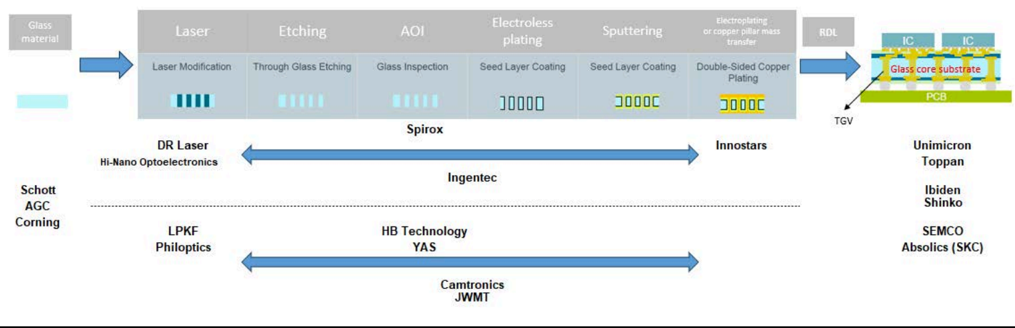

Glass core substrate is an emerging new technology amid rising demand for optical communications and tight ABF substrate supply

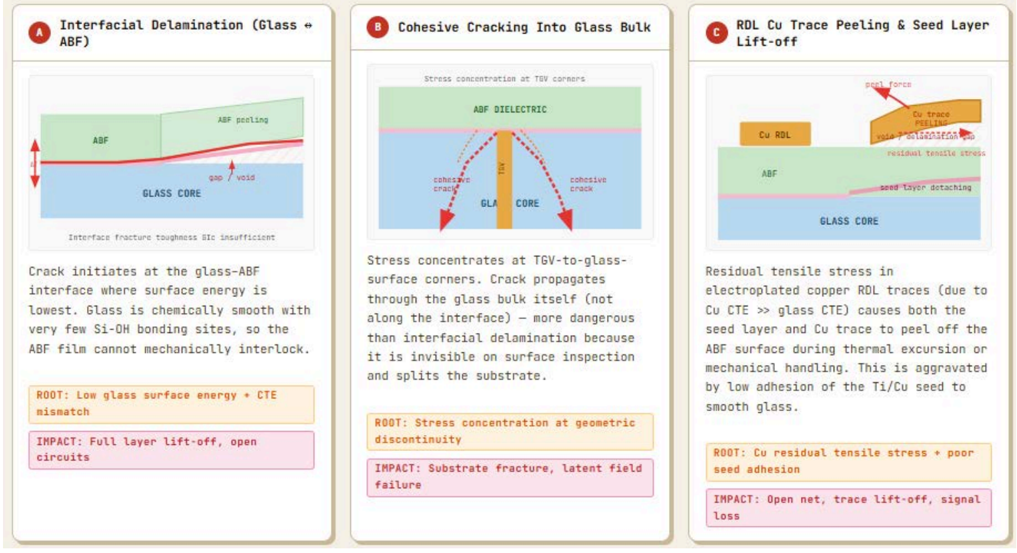

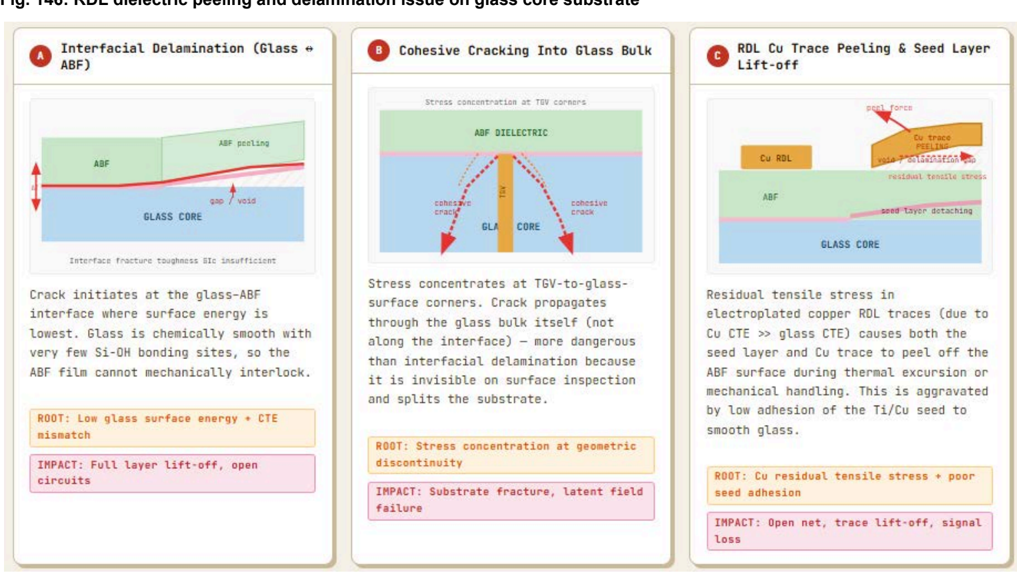

Glass core substrates and interposers are being pursued intensively by leading device makers, materials suppliers, and equipment vendors for advanced packaging applications. Intel (INTC US, Not rated) has publicly demonstrated its glass core substrates for next-generation advanced packaging, positioning the work as foundational research for the latter part of this decade rather than imminent high -volume manufacturing, which helps frame expectations for the technology’s maturity today. We believe Broadcom (BRCM US, Not rated) is likely one of the early movers of adopting glass core substrates by 2027F at the earliest, which may be firstly adopted on its switch ASIC. We think the main reason that Broadcom is considering the use of glass core substrates is mainly to avoid the heat issue which could result in the warpage of substrates. Using the glass core substrate (a good heat spreader) will lead to better heat dissipation through copper pillars, in our view. However, we see two uncertainties for the glass core substrate adoption in the coming year: 1) substrate makers are still dealing with the RDL dielectric peeling and delamination issue; 2) ABF substrate and EMIB-T demand is too strong for substrate makers to invest in glass core substrate capacity.

Fig. 16: Process of glass substrate and some supply chain names related to Broadcom

Source: Manz, Nomura research

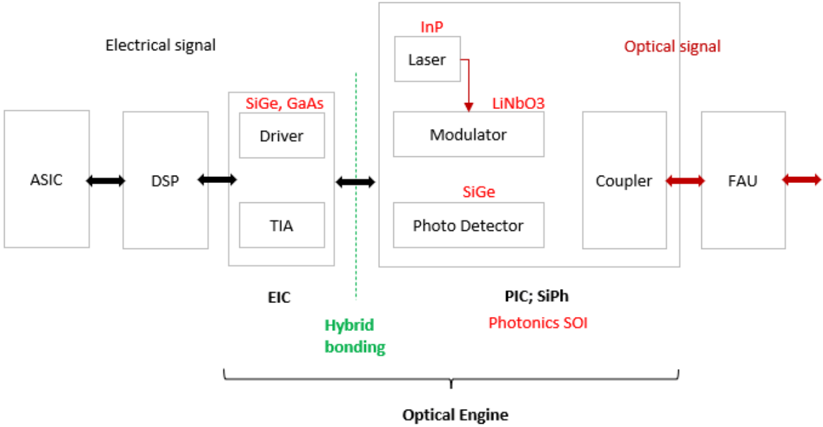

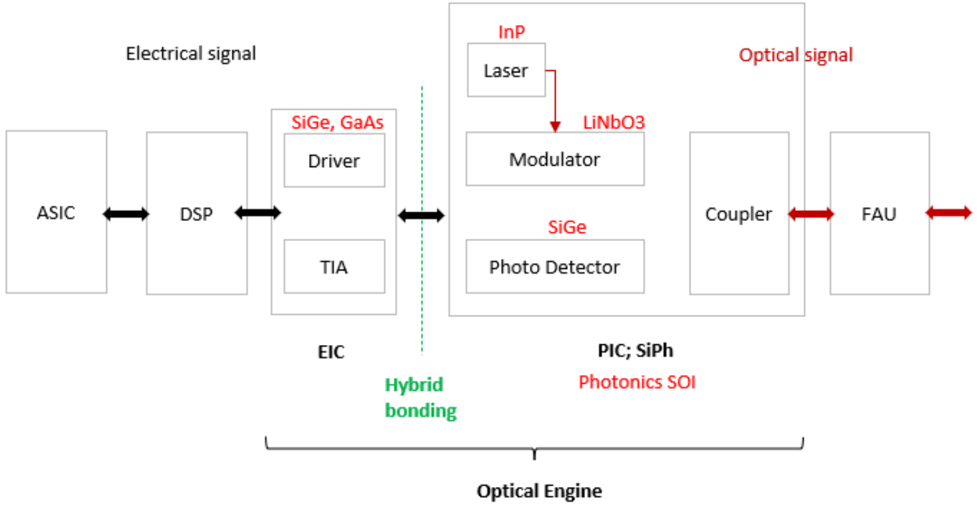

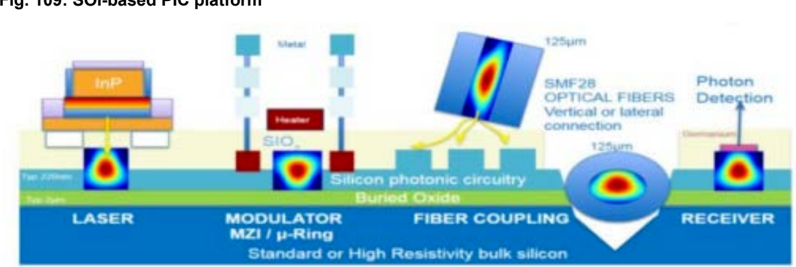

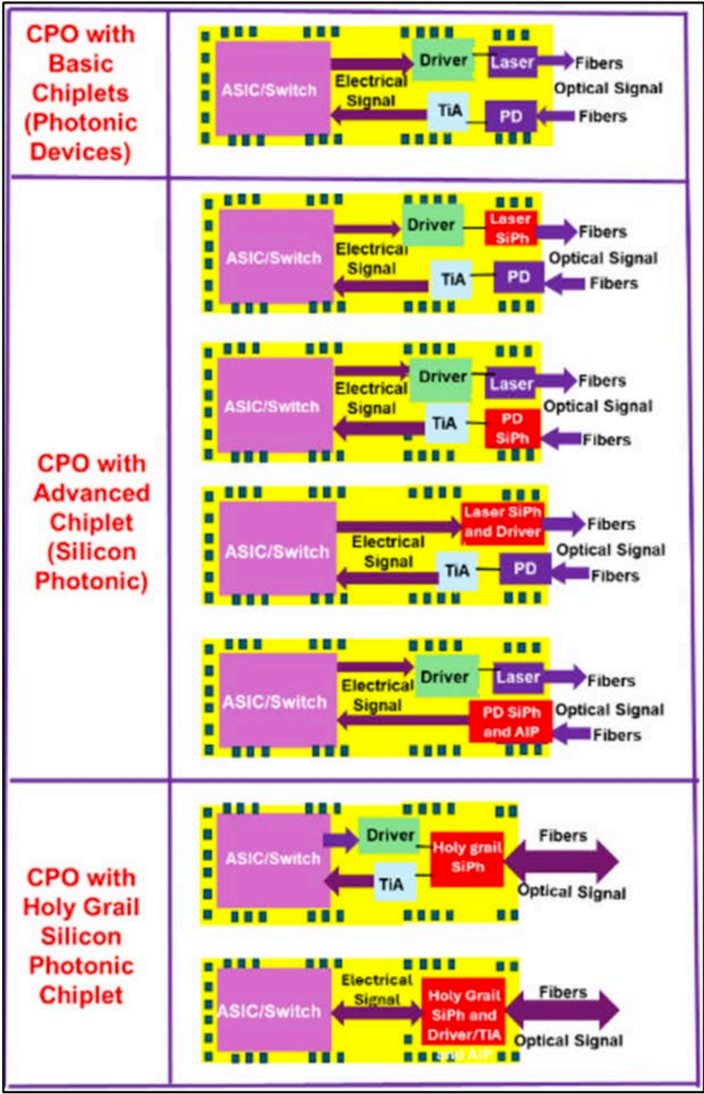

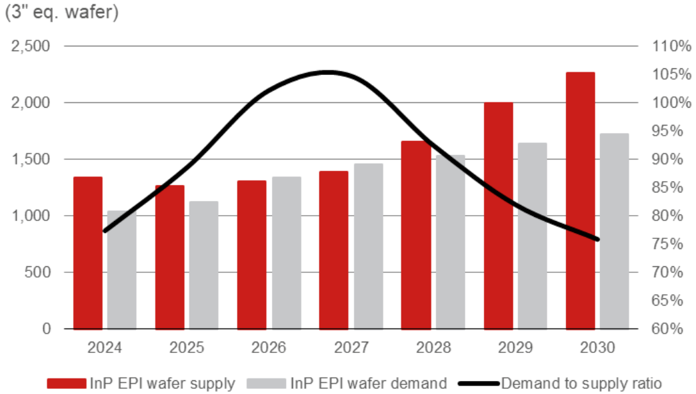

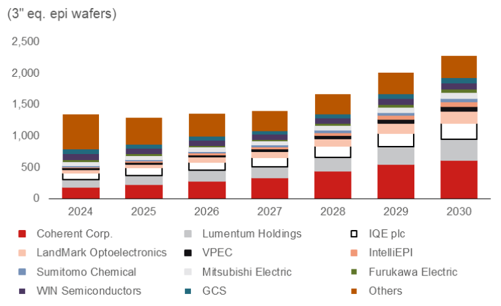

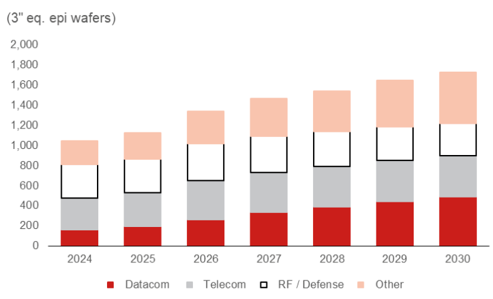

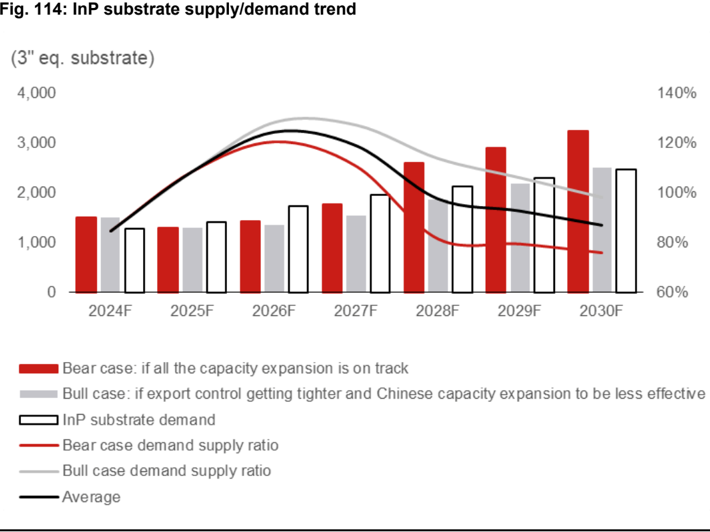

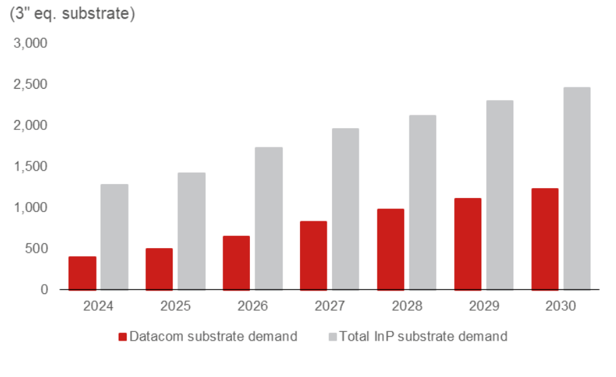

The fast-growing optical communications market is driving surging demand for InP substrate and photonics SOI wafers

Driven by global AI leaders’ buoyant demand for high-speed optical transceivers, as well as persistent component shortages (i.e., optical chips), we believe the product upcycle will continue into 2027F. Meanwhile, product innovation in the optical transceiver market is accelerating, and future technology trends including silicon photonics (SiPh), LPO/LRO, and NPO/CPO primarily target higher performance, lower energy consumption and costs. We believe the 1.6T upgrade and SiPh migration are the key drivers. We also think NPO/CPO technologies will continue to improve. In our view, if leading CPO solution providers use bundled sales strategies for their CPO switch products, then it could accelerate adoption rates in a scale-out network in the medium term, while there are more CPO use cases for the scale-up network in the long term.

Other than using silicon-based wafers to produce key ICs in optical transceivers, other critical areas where non-siIicon-based wafers/materials are used include: 1) InP for EML and CW lasers; 2) Ge (germanium) on silicon for PD; and 3) photonics SOI wafer for PIC (SiPh). Ideally, the fully-integrated PIC necessitates a monolithic III-V compound Semi and silicon platform for efficient light coupling and large dimension III-V compound Semi materials for flexible device/circuit designs. Thus, we believe a monolithic InP/photonics SOI platform for integrated photonics is becoming a better solution. These InP crystals are located right on top of the buried oxide layer and feature an in-plane configuration with the silicon device layer, which results in a unique InP-on-insulator architecture and allows for strong light confinement within the epitaxial InP.

RDL

TGV

Ie

IC

Glass core substrate

PCB

Unimicron

Toppan

Ibiden

Shinko

SEMCO

Absolics (SKC)

Mulre allu

fabs in US and Japan

Ramp up N2 and A16 with new fabs

InP

in US and Japan

Fig. 17: Structure of an advanced optical transceiver and key materials

20

15

ASIC

10

5

0

Source: Nomura research

TSMC’s strong capex and local sourcing plan will be another catalyst for Semi supply chain

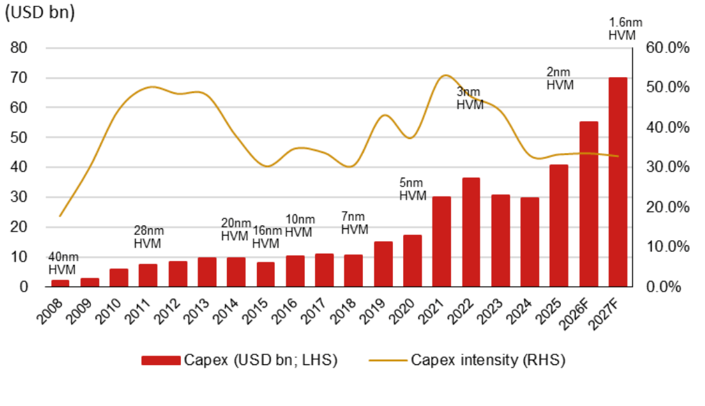

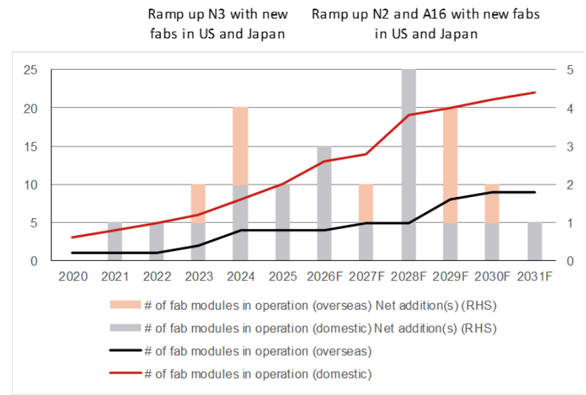

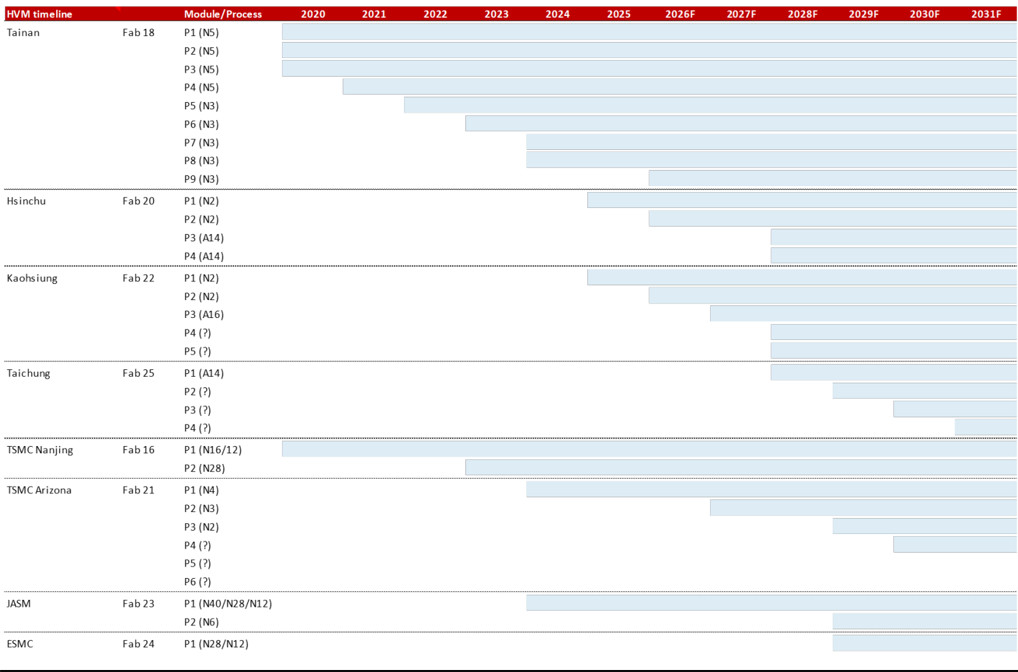

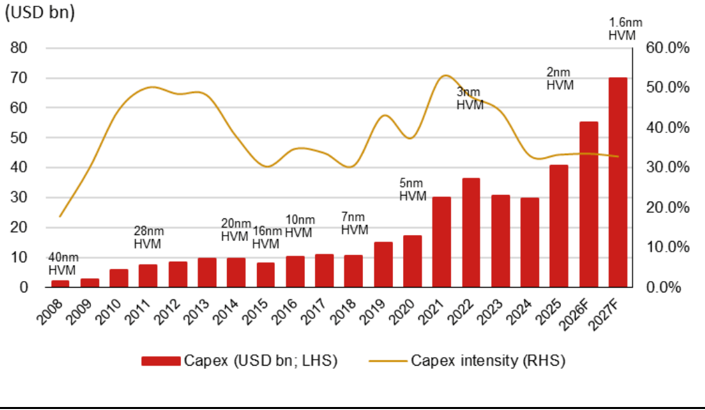

TSMC continues to build up new capacity in Taiwan and overseas. TSMC now has 26 advanced wafer fabs and advanced packaging facilities ramping up or planned globally (18 of them are in Taiwan). We formulate our high-volume manufacturing timeline assumptions in Fig. 18 , which suggests TSMC will have more fab modules coming on stream after 2027F in line with management commentary ‘… So 2026-2027 for the shortterm, we are looking to improve our productivity. 2028 to 2029, yes, we start to increase our capacity significantly’ during the earnings call in early-2026. As a result, we expect TSMC could spend up to around USD70bn of capex in 2027F considering that over 10 new fab modules would be expanded simultaneously in Taiwan and overseas.

Fig. 18: TSMC’s total no. of fab modules and net additions of fab modules

Source: TSMC, Nomura estimates

ve enpoll romeo lapen buulu teaul up tu

80

Fig. 19: TSMC’s capex and capex intensity trend

70

60

50

40

30

20

10

0

We expect TSMC’s capex could reach up to USD70bn in 2027F

HVM

40nm

HVM

Source: Company data, Nomura estimates

2nm

HVM

1.6nm

60.0%

50.0%

HVM

80%

70%

60%

50%

40%

30%

20%

10%

0%

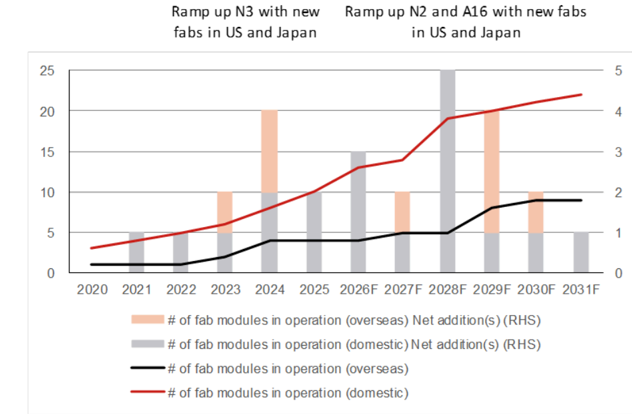

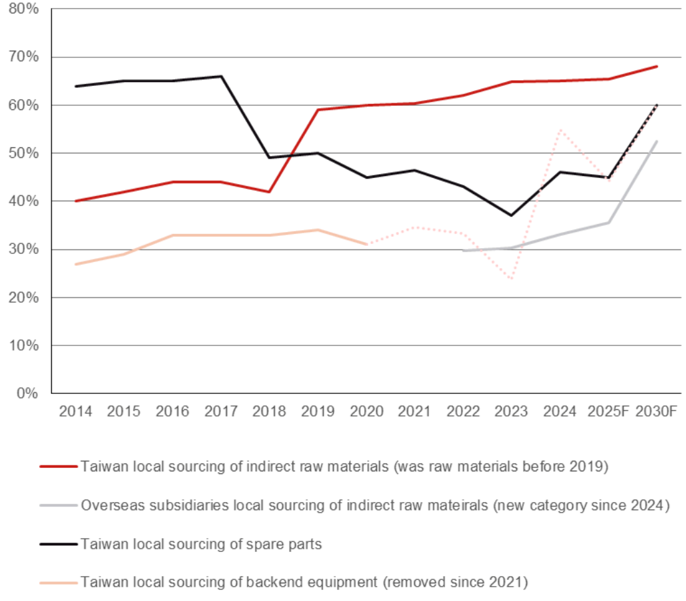

To strengthen local supply chain resilience, enhance the local economy, and reduce carbon emissions during transportation, TSMC has expanded the goal scope for local sourcing globally, encompassing six categories: equipment, components, raw materials, facility systems, automation, and goods across TSMC’s major operational production fabs in the past decade, to aid local suppliers in upgrading technology and quality, cutting costs, and diminishing carbon emissions.

Fig. 20: TSMC’s Semi material, spare parts and back-end equipment localization plan

Source: TSMC, Nomura estimates

Stocks recommended in this Anchor report

Soitec: Leading SOI wafer company in the world

Soitec is the largest SOI wafer supplier globally with around 70% market share (as per our estimates), maintaining its leadership for years (please refer to our 2019 deep-dive report ). However, we believe its growth driver is no longer RF SOI, but photonics SOI, which is likely to be adopted widely in silicon photonic (SiPh)-based photonic integrated circuits (PIC). We think Soitec’s business could return to its 2019-21 glory days. Compared with Bloomberg consensus, we are more bullish on Soitec’s sales contribution from photonics SOI wafers in the coming years. Our sales forecasts for FY27-28F are 38% higher than consensus estimates.

We have a Buy rating and a TP of EUR250 on Soitec. Our TP is based on 8x FY30F P/S with sales of EUR1.12bn, which is in line with its previous peak cycle valuation level in FY21. Risks to our rating and TP include weak optical communication, smartphone, automotive and FD-SOI demand; rising competition from other materials; and oversupply of SOI wafers.

Besi: Leading hybrid bonding tool company

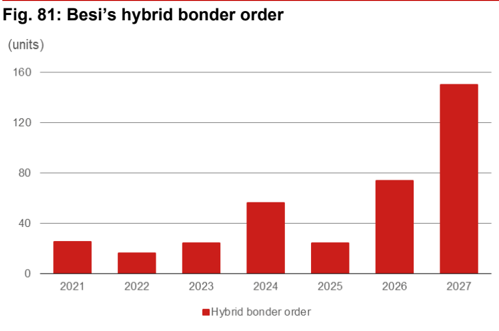

In our advanced packaging sector report published in Feb-25 (‘The evolution of CoWoS, SoIC, and InFO ’), we were conservative on HB demand in 2025. However, we now expect HB demand to surge quickly in 2026-27F on the back of strong demand driven by AI chips, optical communications, and potentially HBMs. Thus, we now believe Besi’s HB orders in 2026-27F could potentially at 70+ and 150+ units. Compared with consensus, we are more bullish on Besi’s HB orders from customers in 2026-27F. Our sales forecast for 2026F is 7% lower, but for 2027F is 8% higher than consensus estimates.

We have a Buy rating on Besi with a TP of EUR340, based on 55x 2027F EPS of EUR6.1. The P/E of 55x is between Besi’s +1 SD P/E to +2 SD of Besi’s P/E range since 2014 as its HB orders will likely reach historical high levels in 2026-27F, in our view. Downside risks: 1) slower-than-expected semi assembly equipment demand and foundry capex raise; 2) slower-than-expected HB adoption; 3) delays in new customers’ project wins and order shipments; and 4) rising competition causing valuation, ASP or gross margin erosion.

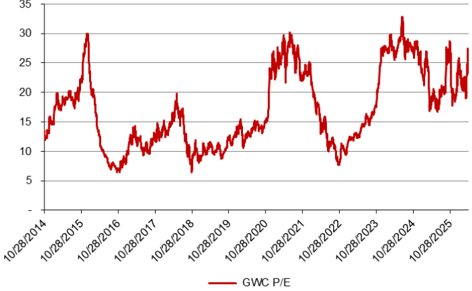

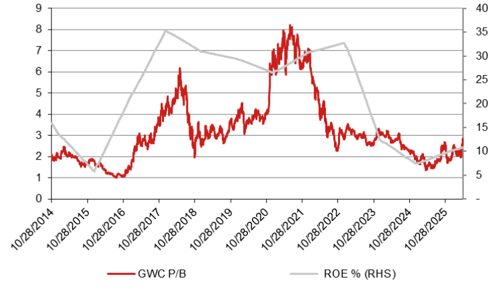

GlobalWafers: Third largest Semi wafer company in the world

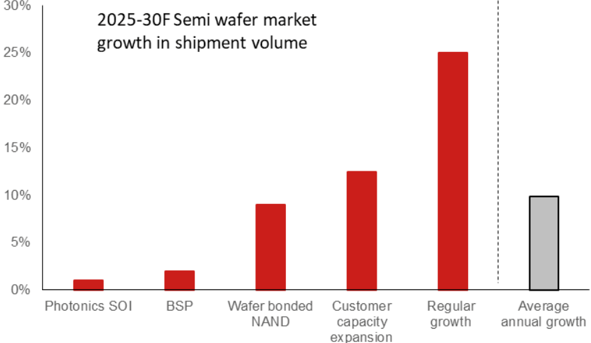

In addition to regular Semi wafer demand growth and Semi companies’ capex expansion cycles driven by strong AI demand, we see some catalysts driven by the adoption of new Semi technology, including: 1) wafer-bonded NAND; 2) backside power delivery (BPD); and 3) emerging photonics SOI demand, which we believe may drive annual Semi wafer market shipment growth of 10% in 2026-30F. Although, in our view, GlobalWafers’ profitability remains at a low level and Semi wafer prices are unlikely to be revised up meaningfully immediately as existing LTAs have not all been renewed yet, we expect Semi wafer companies’ bargaining power to recover gradually. Compared with consensus, our GPM forecasts for 2026-27F are 1.8-3.8pp lower. Our 2026-28F sales and net profit estimates are TWD61.2-83.5bn and TWD8.2-15.3bn.

We upgrade GlobalWafers to Buy and raise our TP to TWD850 (from TWD480), based on 3.2x 2028F BVPS TWD262 (increased from previously 2.1x 2026F BVPS of TWD230 to factor in the potential upcycle in 2027-28F). Downside risks include: 1) faster-thanexpected entry of China into the 12’ semi wafer market; 2) slower-than-expected market consolidation; 3) worse-than-expected end-demand for the Semi industry; 4) less favorable demand/supply dynamics in the Semi wafer industry; and 5) less-favorable FX volatility and rising material/utility costs.

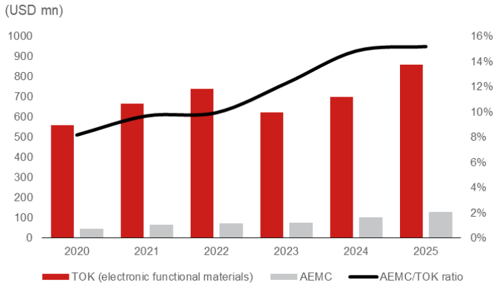

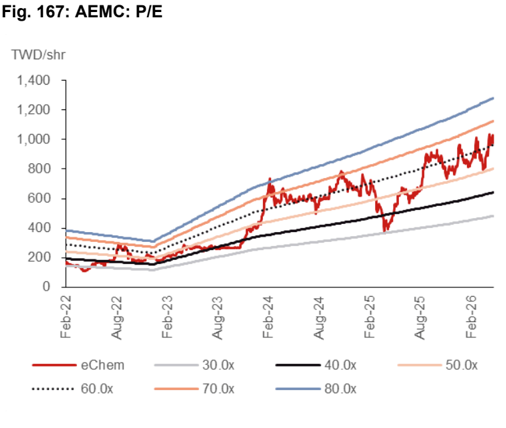

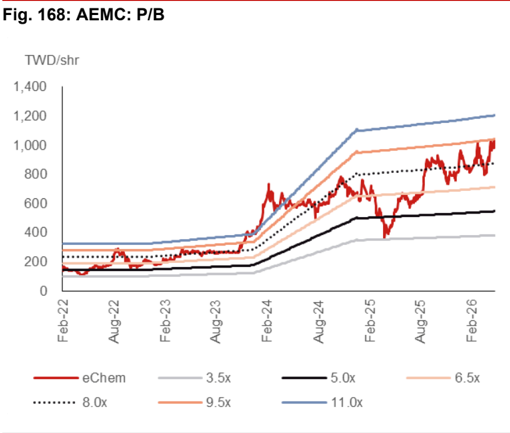

AEMC: Leading photoresist and photoresist auxiliary supplier in Taiwan

We initiate coverage of Advanced Echem Materials (AEMC) with a Buy rating and a target price of TWD1,500. AEMC is a leading Taiwan-based developer and manufacturer of specialty chemical materials for semiconductor and display applications, and is among the major photoresist (PR) auxiliary domestic suppliers for TSMC. Considering TSMC’s aggressive N3/N2 and sub-2nm capacity expansion plans from 2026-27E onwards and AEMC’s potential market share gain from global peers, we forecast 2026-30F revenue/net income CAGRs of around 30% each for AEMC. Compared with consensus, we are more bullish on AEMC’s long-term business opportunities to further broaden its product portfolio from photoresist auxiliary to photoresist. Our 2026-28F sales and net profit estimates are TWD5.2-8.4bn and

TWD1.4-2.3bn, respectively.

Our TP of TWD1,500 is based on 60x FY28F EPS of TWD25 - the target multiple of 60x reflects our expectation that AEMC would sustainably grow its business with its leading foundry customer and the TAM of PR would expand. Downside risks include: (1) product disqualifications by its leading foundry customer; (2) loss of market share to other competitors; (3) inability to supply more high-end products such as BARC (Bottom Anti-Reflective Coatings) and photoresist.

Ingentec: Leading specialty gas supplier with TGV capability in Taiwan

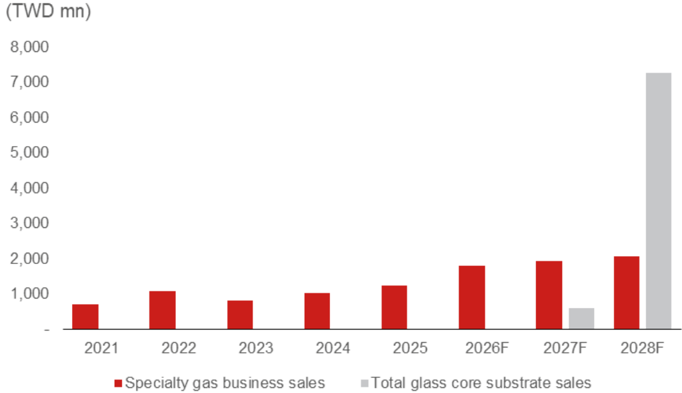

We initiate coverage of Ingentec, a Taiwanese specialty gas supplier and emerging TGV (Through-Glass Via) glass core substrate manufacturer, with a Buy rating. In our view, Ingentec is positioned at the intersection of two powerful secular trends: 1) the accelerating demand for etch gases driven by memory capacity expansion, particularly 3D NAND; and 2) emerging glass core substrate demand driven by Broadcom from 2027F. We estimate 2026F will be a year of recovery for its core specialty gas business, and its glass core substrate business could emerge from 2027F onwards at the earliest. Thus, we assume there could be more meaningful sales and earnings growth in late 2027F. Compared with consensus, we assume that the glass core substrate business will not contribute meaningful sales and profit until late-2027F with strong sales and profit surge in 2028F (consensus currently estimates strong earnings growth in 2027F already). We also assume Ingentec would need to raise funds by issuing new shares by the end of 2027F to support the rising capex for its glass core substrate business. Our 2026-28F sales and net profit estimates are TWD1.8-9.3bn and TWD46mn-1.2bn, respectively.

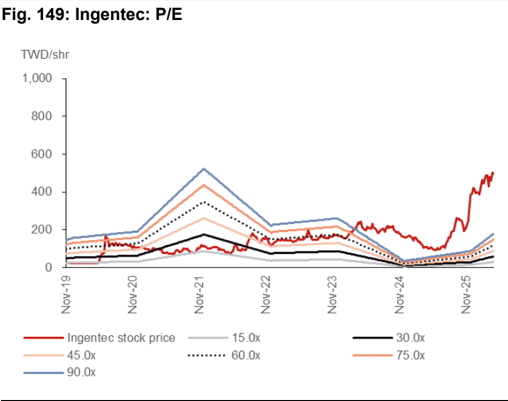

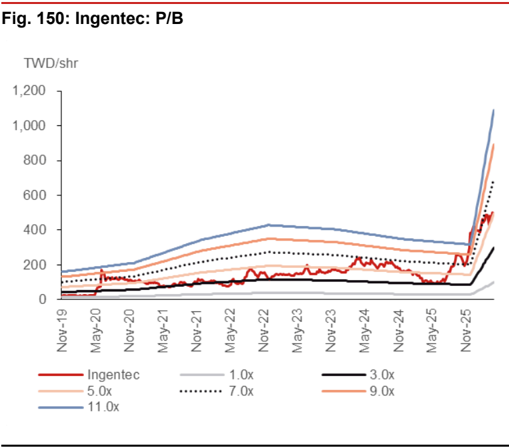

Our TP of TWD960 is based on 60x 2028F EPS of TWD16, in the mid-range of the company’s 45-75x P/E over 2021-23, when Ingentec’s specialty gas business was strong, driven by tight supply due to the Ukraine-Russia war. Downside risks include: 1) weaknening semi capex cycle; 2) loss of market share to competitors; 3) delay in the commercialization of next-generation products; and 4) slower-than-expected adoption of glass core substrate.

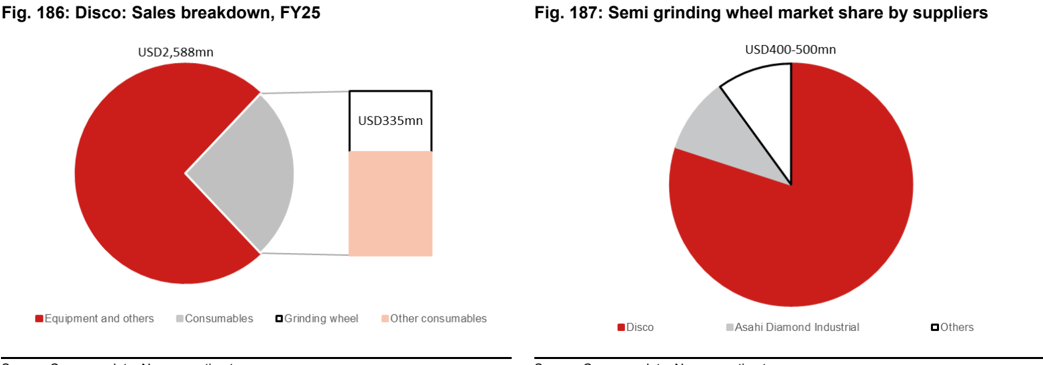

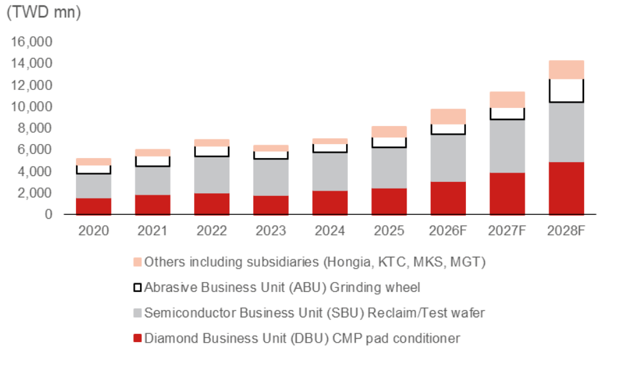

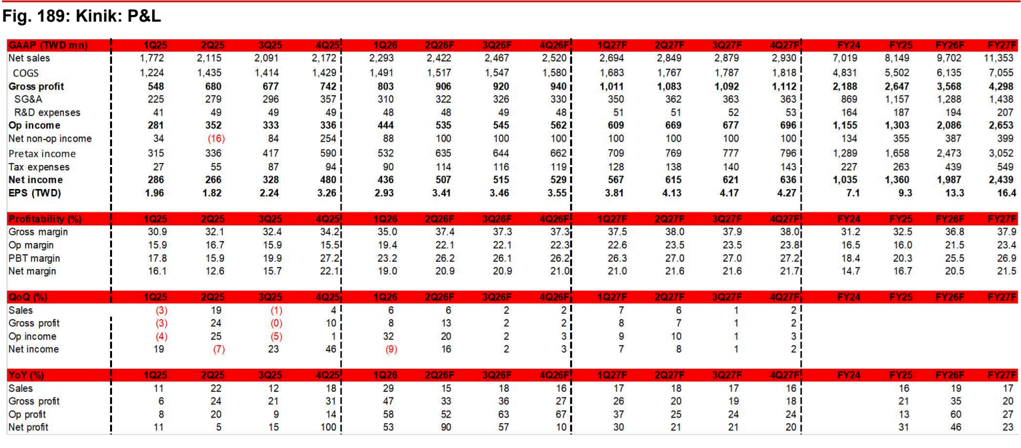

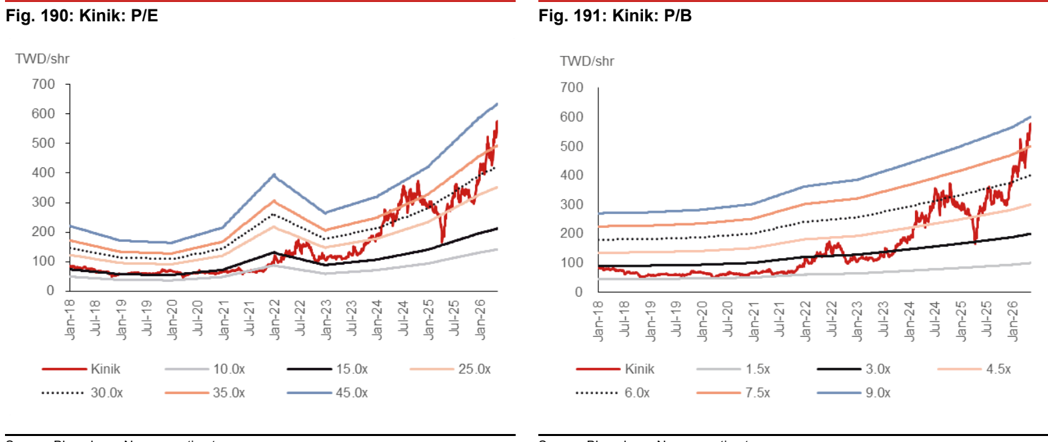

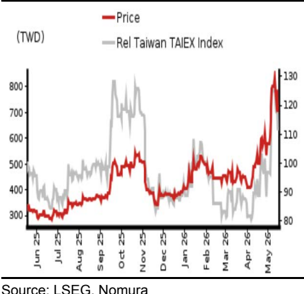

Kinik: Leading CMP pad conditioner and reclaim wafer supplier in Taiwan

Kinik is the dominant chemical mechanical polishing (CMP) pad conditioner (DBU) supplier to TSMC on advanced nodes, with an ~80% share on the N2 node through a multi-year codevelopment partnership. We believe Kinik’s reclaim/test wafer business (SBU) is also likely to grow along with the recovery of semi wafer demand. Other than these two growth engines, we expect its grinding wheel business (ABU) could be an additional lever if Kinik is able to penetrate into the leading OSAT companies in the long term. Compared with consensus, our GPM forecast for 2026F is slightly higher due to Kinik’s better product mix, and we have also factored in some more grinding wheel business opportunities in 2028F. Our 2026-28F sales and net profit estimates are TWD9.7-14.2bn and TWD2.0-3.0bn, respectively.

We initiate coverage on Kinik with a Buy rating and a TP of TWD840, based on 40x 2028F EPS of TWD21 in the upper half of its historical P/E of 10-45x, to address its stably growing business with its leading foundry customer, as well as the rising TAM across its different business units. Downside risks are: 1) disqualification of products by its leading foundry customer; 2) losing market share to competitors; 3) failure to broaden its product portfolio; and 4) weakening Semi market demand.

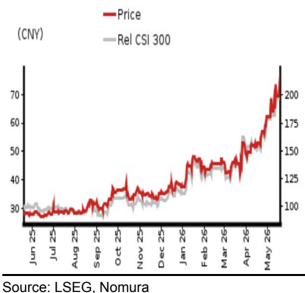

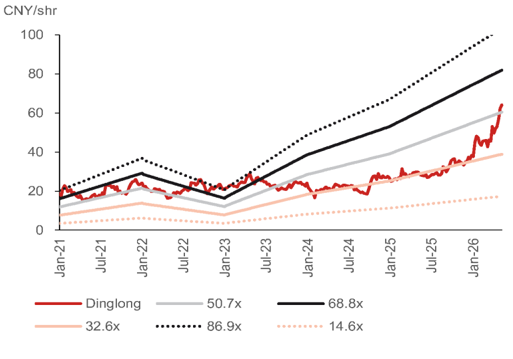

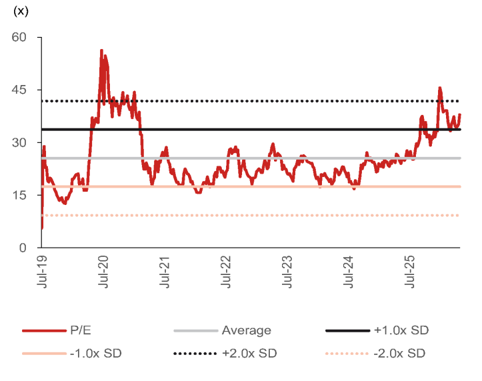

Hubei Dinglong: CMP scale-up and photoresist breakthrough

Dinglong’s investment case rests on two reinforcing growth engines: a rapidly scaling CMP consumables franchise and an inflecting photoresist business. CMP pad sales surged 71.2% y-y in 1Q26 to CNY376mn, with monthly shipments exceeding 40k pieces and capacity now at 50k/month, evidencing meaningful share gains at domestic foundries during China’s semiconductor capacity build-out. The CMP slurry segment is also broadening, with recent wins in 12-inch fine slurry, ceria slurry at a leading memory player, and TSV slurry for advanced packaging - collectively unlocking a domestic TAM of over CNY1bn currently dominated by imports. On photoresist, Dinglong has three ArF/KrF products in stable mass supply with several more order conversions expected in 2026E, supported by a completed 300 tons/annum Phase-2 line offering >5x capacity headroom versus current run-rate. With domestic localisation rates still extremely low (~15% for KrF, 2-3% for ArF) and potential export tightening in 2026-27F, the substitution opportunity is substantial - positioning Dinglong as a direct mainland competitor to AEMC’s photoresist ambitions.

We maintain our Buy rating with TP raised to CNY104 (from CNY42), based on 96x

2026F P/E (CNY1.08 EPS), at +2.5x SD of its 5-year historical average P/E of 51x. The target multiple is supported by a 33% earnings CAGR over 2025-28F, with net profit forecast at CNY1,022/1,312/1,675mn for 2026/27/28F. The stock currently trades at 64x 2026F P/E, implying 43% upside to TP. Key catalysts include continued CMP pad share gains at record shipment levels, broadening of the slurry pipeline into import-dominated categories, and accelerated ArF/KrF order conversions as domestic fabs prioritise supplychain localisation. Downside risks include slower-than-expected ArF/KrF ramp-up, customer production delays, and goodwill/integration risk from the lithium materials acquisition.

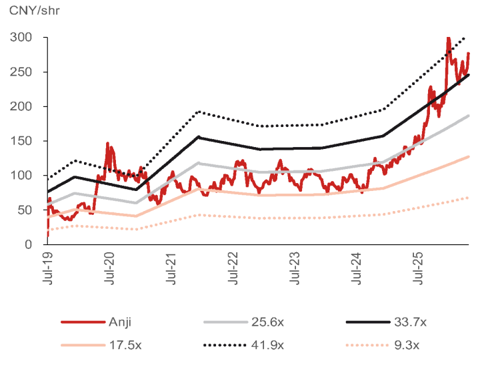

Anji Microelectronics: Sub-10nm node leader in China and gross margin recovery

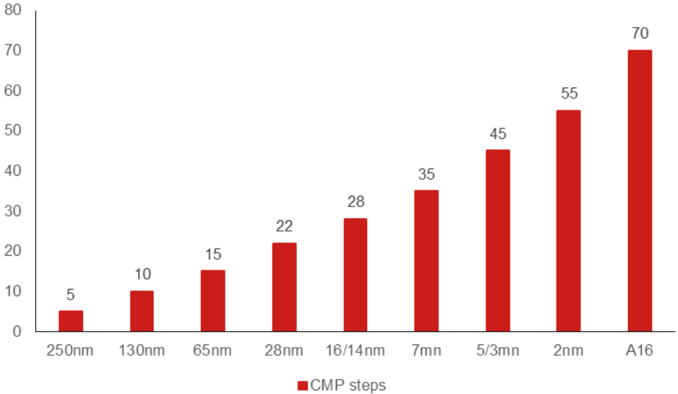

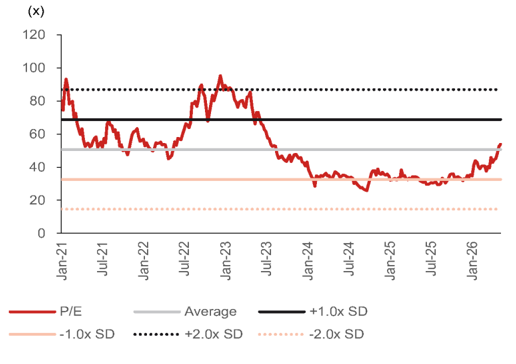

Anji is China’s leading CMP slurry supplier, differentiated by its advanced-node positioning and raw-material self-sufficiency. The company is a primary beneficiary of China’s CMP slurry market scaling to an estimated CNY10.5bn by 2028F, with growth concentrated in sub-10nm area. Copper and copper-barrier slurries at a key client have transitioned from qualification to scaled mass production, while 7nm cobalt-interconnect slurry - a greenfield category with no Cabot/DuPont benchmark - is advancing into qualification at a follow-on site. A further incremental driver is one client’s wafer-to-wafer (W2W) hybrid-bonding initiative for 3D DRAM, which increases CMP step count through pre- and post-bonding planarisation. In-house abrasives production supports slurry gross margins of 55-58% (vs. 52-55% at peers), underpinning superior profitability with ROE forecast at 28-30% through 2026-28F.

We maintain our Buy rating with TP raised to CNY360 (from CNY320), based on 42x 2027F P/E (CNY8.52 EPS), at +2x SD of its historical average P/E of 26x. The target multiple is supported by a 25% earnings CAGR over 2025-28F, with net profit forecast at CNY1,097/1,437/1,738mn for 2026/27/28F. The stock currently trades at 34x 2027F P/E, implying 25% upside to TP. Key catalysts include gross margin recovery from 2Q26F as advanced-node mix improves, incremental CMP step pull-ins from the W2W hybridbonding ramp, and continued displacement of imported slurries at sub-10nm nodes. Downside risks include ultra-high-purity silica sol remains Fuso, rising competition from Dinglong in CMP slurries, and potential fab-led vertical integration that could disintermediate third-party suppliers.

=..

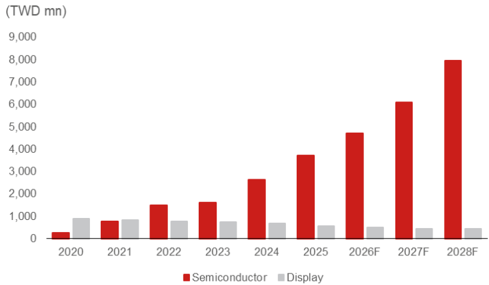

3

Can semiconductor materials close the gap with Semi and SPE market growth?

Assembly & Test

Semiconductor materials: ~USD80bn market powered by fab expansion, node migration and advanced packaging

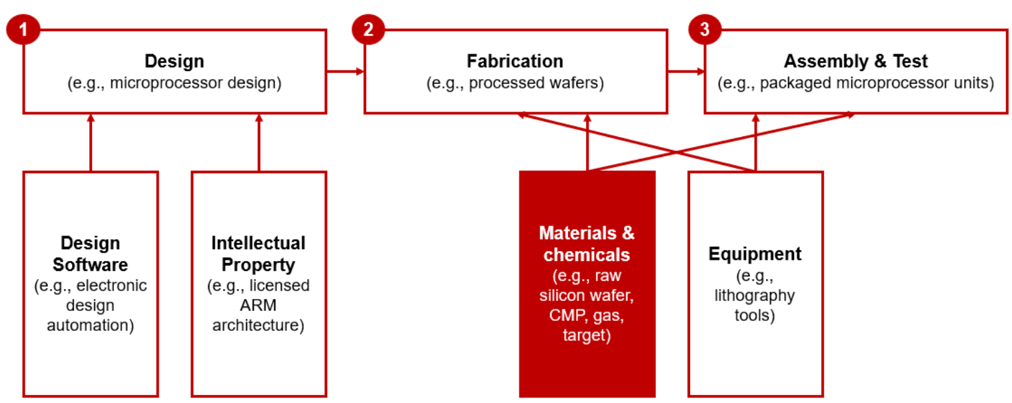

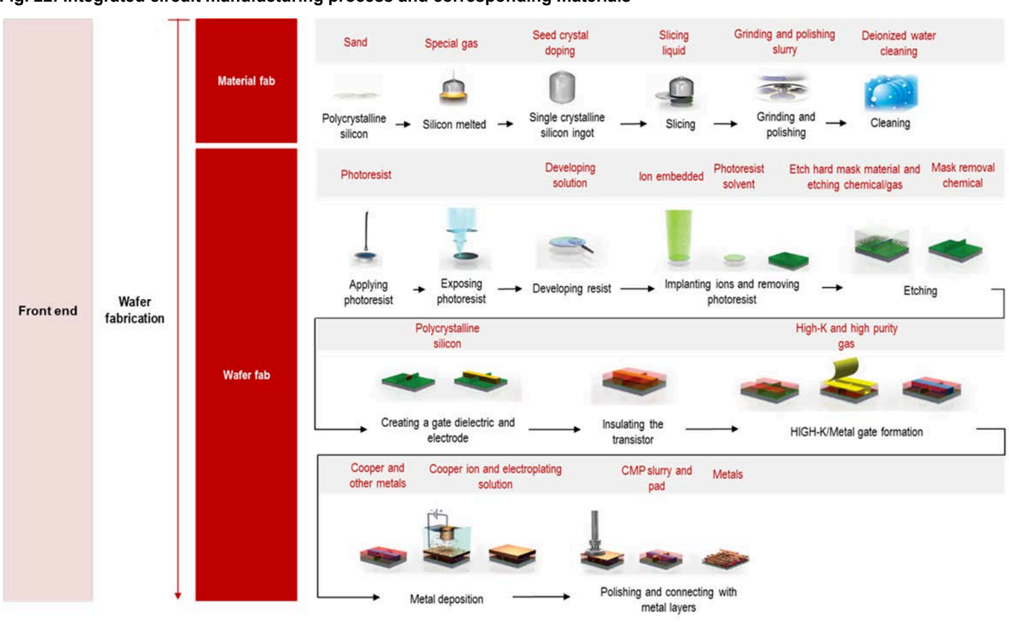

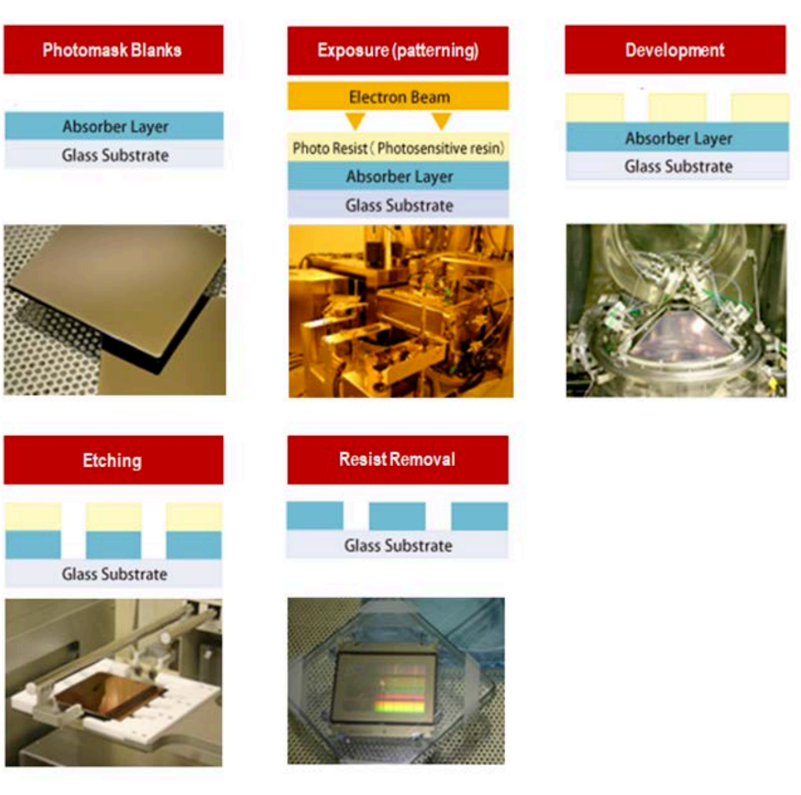

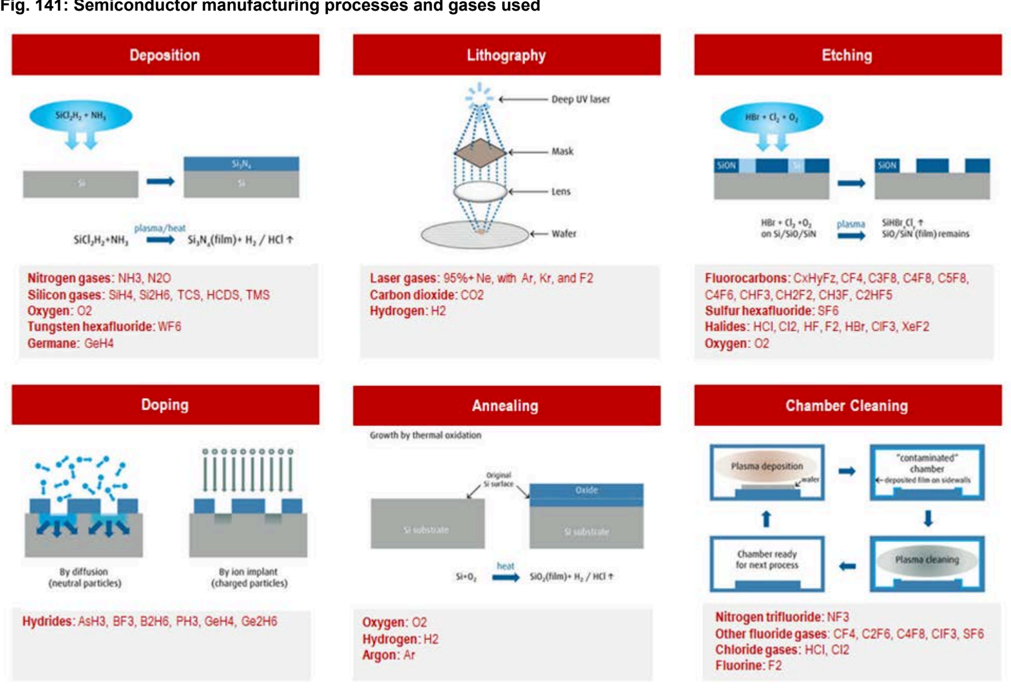

The semiconductor supply chain has been under the spotlight in terms of its importance to international relations, the attention it received from senior leaders in the government and business, and its use as a tool of foreign policy. Across a diverse range of global opportunities and geopolitical challenges, semiconductor materials are increasingly at the center of the story. Semiconductor materials, along with certain chemicals, are necessary inputs across the semiconductor manufacturing process (Fig. 21 ).

Fig. 21: Simplified semiconductor value chain

Source: CSIS, Nomura research

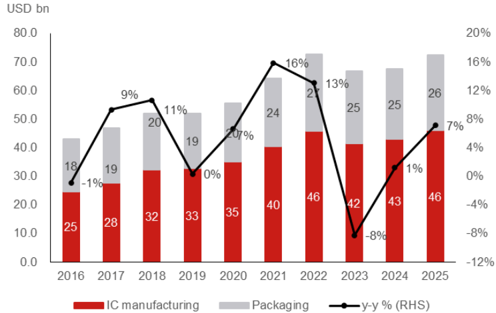

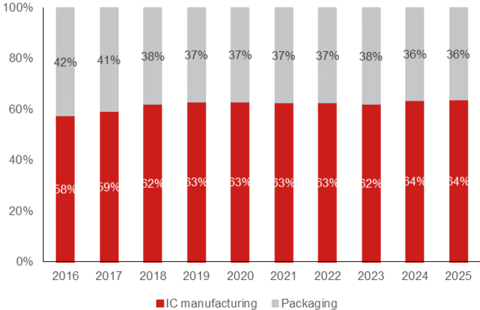

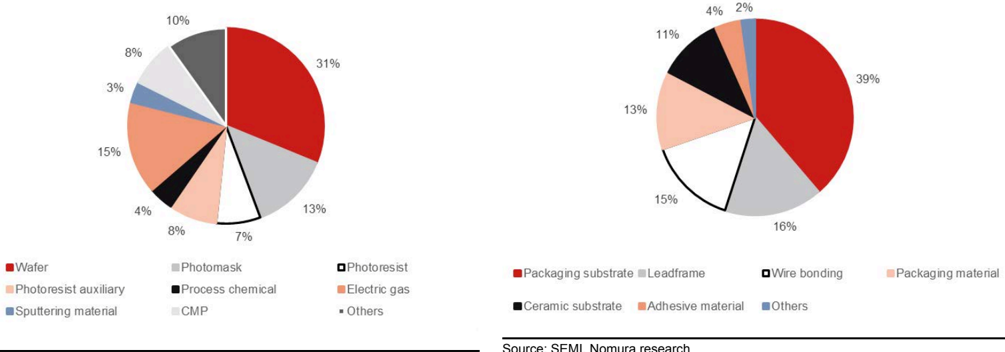

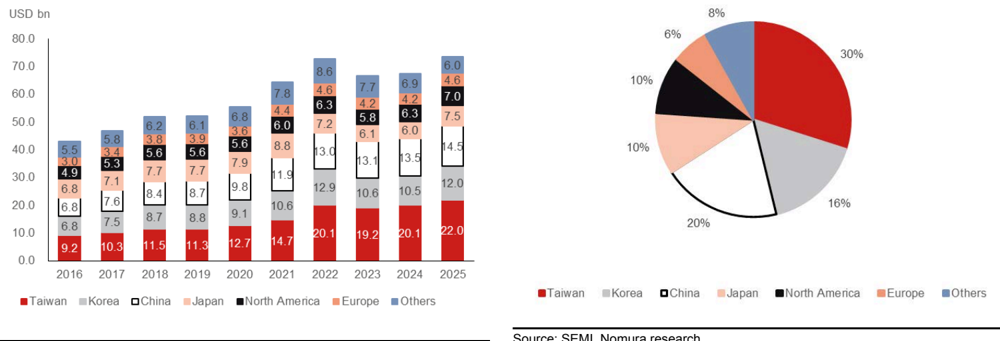

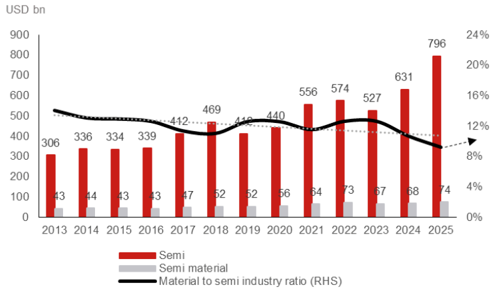

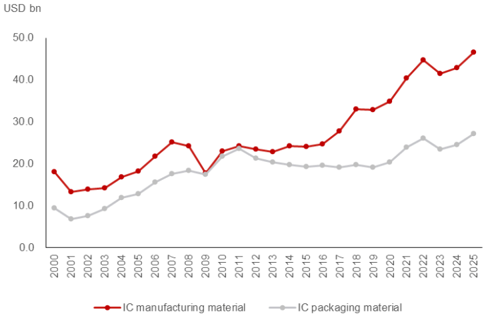

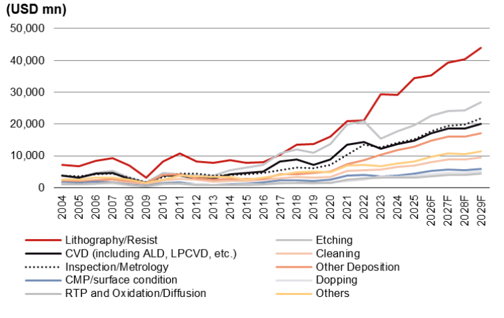

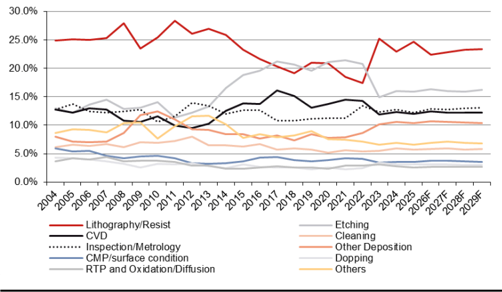

In 2025, global semiconductor sales reached USD796bn (+26% y-y), according to WSTS, while, global total semiconductor material sales merely grew 7% y-y to USD73.6bn. In general, semiconductor materials consist of two main segments - manufacturing materials and encapsulation (packaging) materials (Fig. 22 -23 ). Fabrication materials accounted for 64% of the total material market share in 2025, while packaging materials made up the remaining 36%, as per our estimates.

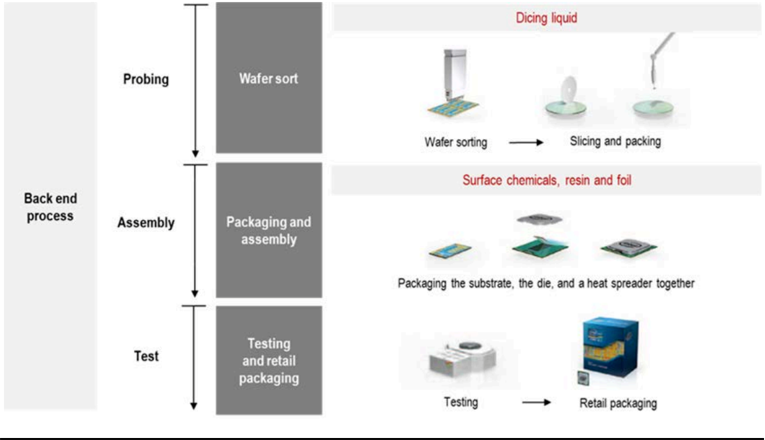

IC manufacturing materials include wafer, photomask, photoresist, photoresist auxiliary materials, process chemicals, electric gas, sputtering material, and CMP materials. According to our estimates, in 2025, wafer represented 31% of total IC manufacturing materials, followed by photo resist and photoresist auxiliary (c.15%), electric gas (c.14%), while photomask and CMP accounted for 13% and 8%, respectively. Packaging materials include packaging substrate, lead frame, ceramic substrate, wire bonding, packaging and adhesive materials, where packaging substrate accounted for the biggest portion of packaging material market with a 39% share, as per our estimates.

somedateu

Sand

Special gas

Seed crystal doping

Slicing liquid

Dicing liquid

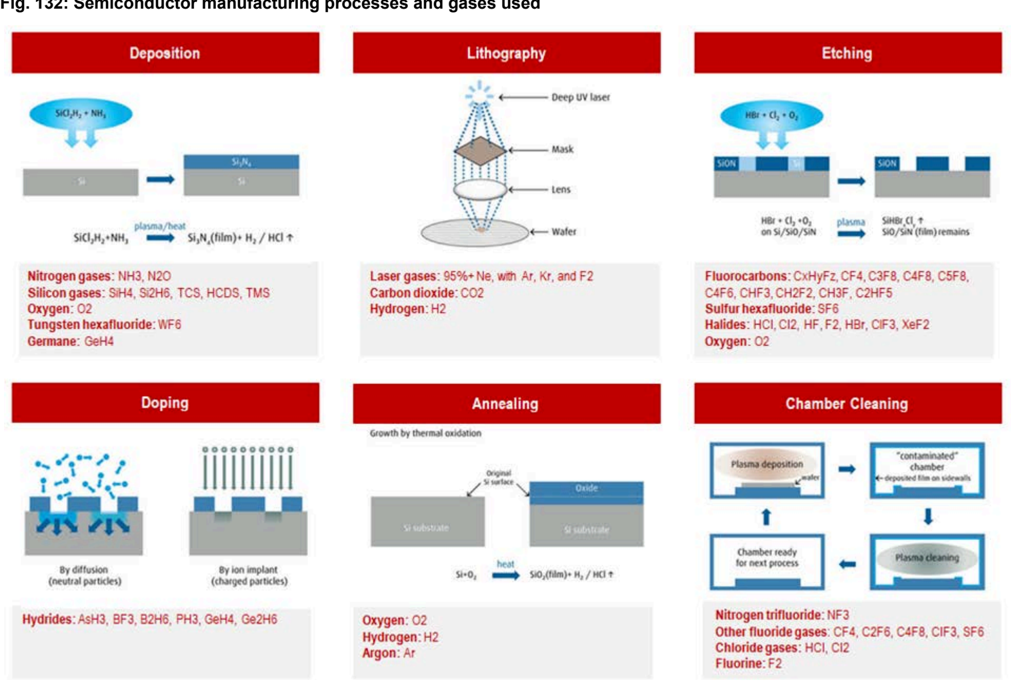

Fig. 22: Integrated circuit manufacturing process and corresponding materials

Back end process

Front end

Grinding and polishing slurry

Deionized water cleaning

Source: Nomura research

Fig. 23: Integrated circuit packaging process and corresponding materials

Source: Nomura research

Fig. 24: Semi materials market breakdown by market size

10%

percentage

80.0

70.0

60.0

50.0

40.0

30.0

20.0

10.0

25

0.0

• Wafer

2016

Photoresist auxiliary

•Sputtering material

20%

Fig. 24: Semi materials market breakdown by market size

3%

Source: SEMI, Nomura research

Fig. 26: IC manufacturing materials market breakdown by percentage

11%

Fig. 25: Semi materials market breakdown by percentage

58%

•Packaging substrate # Leadframe

• Ceramic substrate

Source: SEMI. Nomura research

Source: SEMI, Nomura research

Fig. 27: IC packaging materials market breakdown by percentage

Source: SEMI, Nomura research

Source: SEMI, Nomura research

9%

26

12%

18/

Fig. 25: Semi materials market breakdown by percentage percentage

100%

80%

60%

4%

2%

‘you mejor del materiale marnet orare

Fig. 28: Global semiconductor materials sales by market

80.0

70.0

60.0

Fig. 29: Global semiconductor materials sales breakdown, 2025

8%

Taiwan has the highest share in fabrication material consumption, whereas Japan dominates the supply

50.0

40.0

30.0

20.0

10.0

0.0

20%

By country/region, Taiwan remains the biggest semiconductor materials market owing to its large IC foundry and packaging capacities. In 2025, Taiwan accounted for 30% of global semi material sales, followed by 20% for China. South Korea and Japan were the third- and fourth-largest markets, representing 18% and 10%, respectively, of the total share, according to our estimates. The US has been growing rapidly in recent years due to the ‘Made in US’ policy, which is driving more Semi companies to build their new capacities on the US soil.

2016

2017

2020

2021

2018

2019

2022

2023

2024

2025

14%

20%

Fig. 28: Global semiconductor materials sales by market

Photomasks

CMP (slurry and pad)

Other wafer fab materials

9%

34%

Fig. 29: Global semiconductor materials sales breakdown, 2025

11%

Source: SEMI, Nomura research

54%

50%

South Korea

Source: SEMI, Nomura research

•Japan

20%

United States

30%

•Taiwan

• China

Fig. 30: Major semi materials market share of sales by country/region, 2025

Source: SEMI, Nomura research

11%

90%

RoW

5%

100%

7%

12%

40%

12%

13%

30%

8%

12%

16%

16%

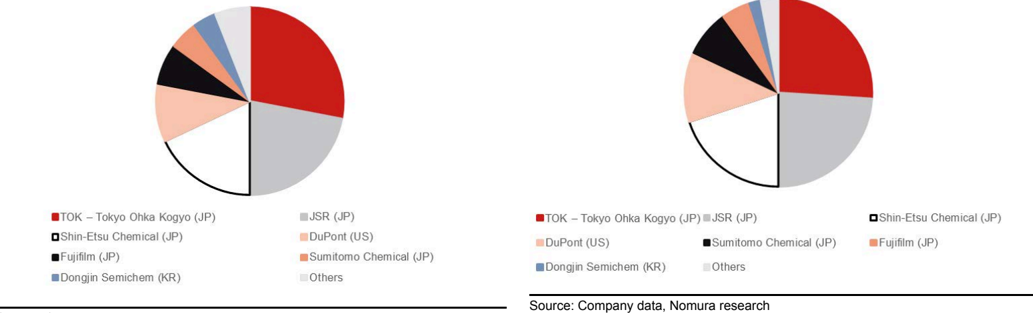

Fig. 32: Photoresist - KrF market share by company in 2025

80%

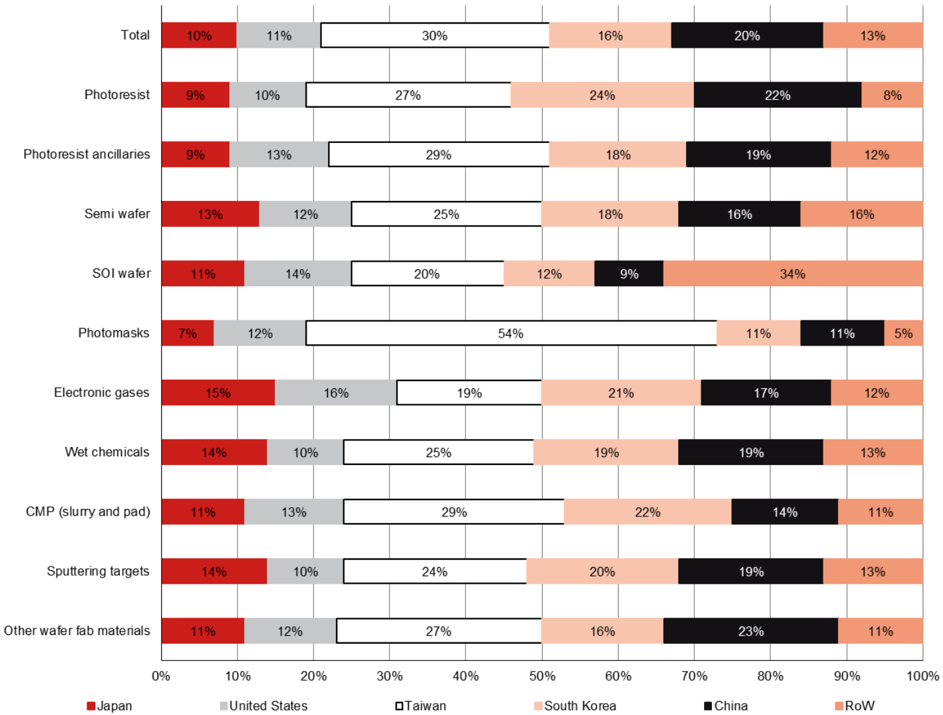

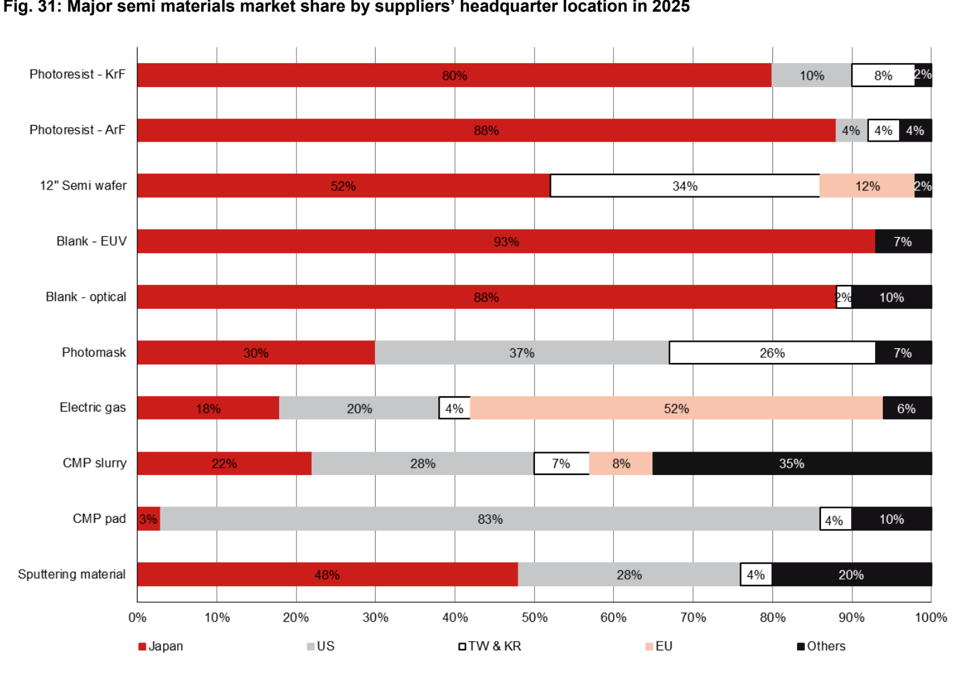

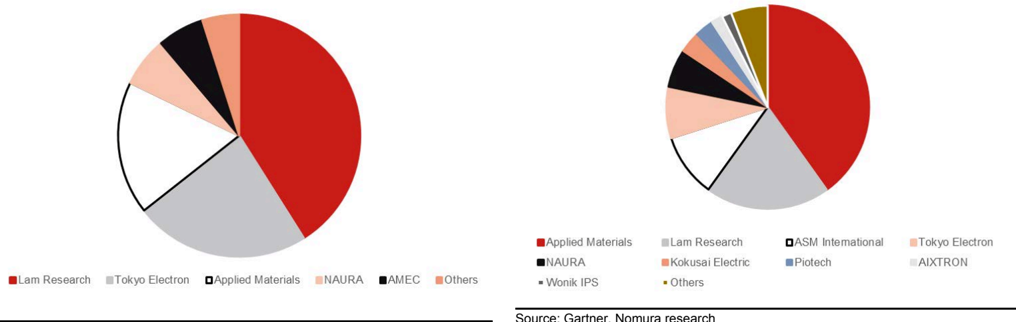

However, the supply of global semi materials is still dominated by Japan, US and EU companies (Fig. 31 -44 ). In details, Japan dominated the lithography and sputteringrelated material market, while the US and EU each have relatively higher shares in CMP and electric gas related markets.

Fig. 31: Major semi materials market share by suppliers’ headquarter location in 2025

Blank - optical

•Fujifilm (JP)

Electric gas

Sputtering material

Fig. 33: Photoresist - ArF market share by company in 2025

10%

8%

4% 4%

12%

2%

4%

2%

Source: Company data, Nomura research

Fig. 32: Photoresist - KrF market share by company in 2025

Fig. 33: Photoresist - ArF market share by company in 2025

Source: Company data, Nomura research

Source: Company data, Nomura research

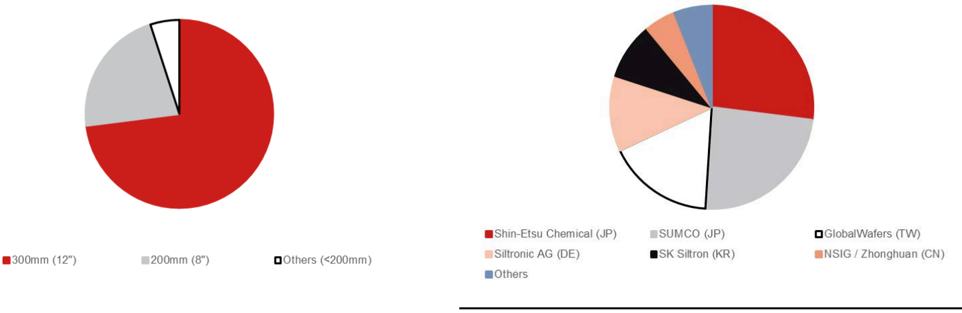

Fig. 34: Semi wafer size breakdown by area shipment in 2025

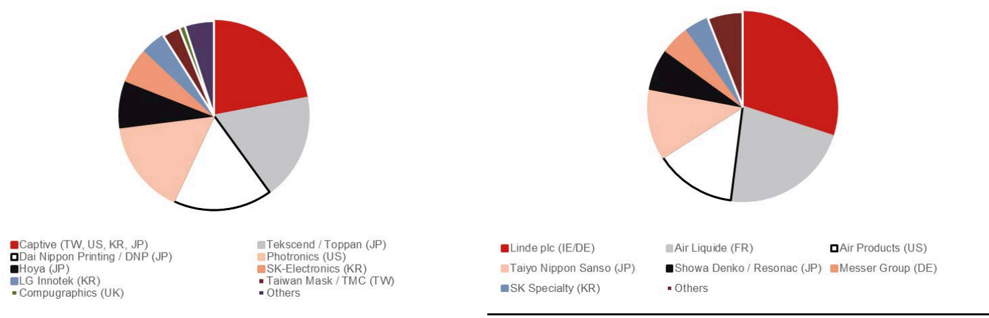

Fig. 36: Photomask market share by company, 2025

Fig. 38: Blanks (optical) market share by company in 2025

10%

Fig. 34: Semi wafer size breakdown by area shipment in 2025

20%

•Captive (TW, US, KR, JP)

•Hoya (JP)

300mm (12”)

•Dai Nippon Printing / DNP (JP)

Shin-Etsu Chemical (JP) |

•LG Innotek (KR)

•Hoya (JP).

- Compugraphics (UK)

Source: SEMI, Nomura research

Fig. 36: Photomask market share by company, 2025

Fig. 35: 300mm water market share by company

Fig. 37: Electric gas market share by company, 2025

Fig. 39: Blanks (EUV) market share by company, 2025

20%

Fig. 35: 300mm wafer market share by company

Source: SK Siltron, Nomura research

Fig. 37: Electric gas market share by company, 2025

Source: Company data, Nomura research

Fig. 38: Blanks (optical) market share by company in 2025

Source: Company data, Nomura research

Fig. 39: Blanks (EUV) market share by company, 2025

Source: Company data, Nomura research

Source: Company data, Nomura research

components in 2025

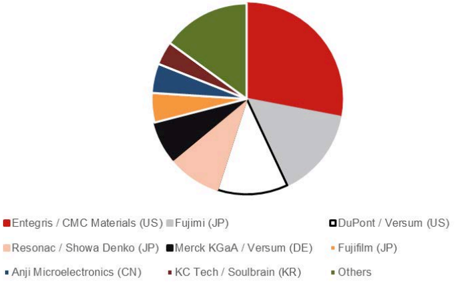

Fig. 42: CMP pad market share by company in 2025

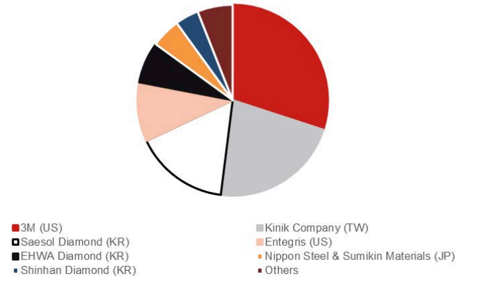

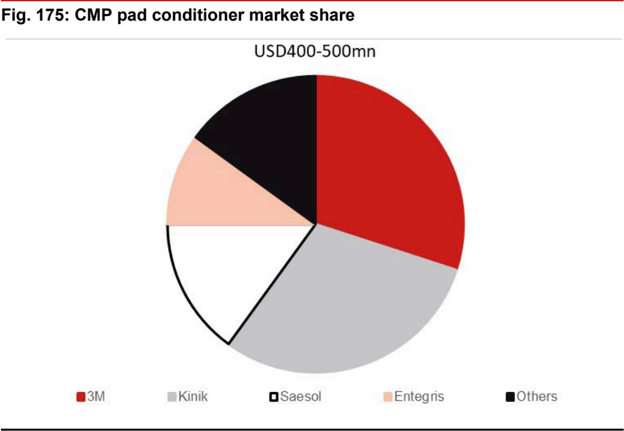

Fig. 43: CMP pad conditioner market share by company in 2025

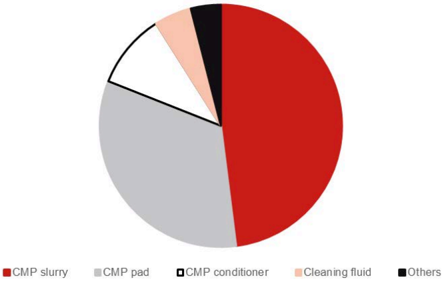

Fig. 40: CMP market breakdown by different materials and components in 2025

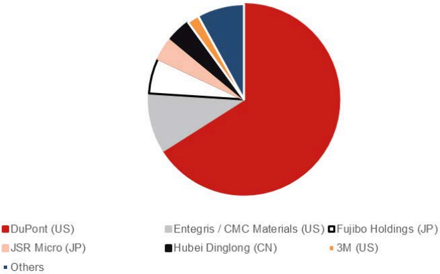

Fig. 41: CMP slurry market share by company in 2025

•Entegris / CMC Materials (US) • Fujimi (JP)

•Resonac / Showa Denko (JP) Merck KGaA / Versum (DE)

A3M (US)

•Saesol Diamond (KR)

•EHWA Diamond (KR)

• Anji Microelectronics (CN)|

• Shinhan Diamond (KR)

Source: Company data, Nomura research

Fig. 43: CMP pad conditioner market share by company in 2025

Source: Company data, Nomura research

•DuPont (US)

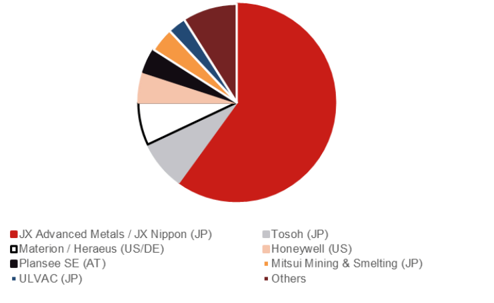

•JX Advanced Metals / JX Nippon (JP)

•Materion / Heraeus (US/DE)

CMP slurry

•JSR Micro (JP)

= Others

•Plansee SE (AT)

• ULVAC (JP)

Source: SEMI, Nomura research

Fig. 42: CMP pad market share by company in 2025

Source: Company data, Nomura research

Fig. 44: Sputtering material market share by company in 2025

Source: Company data, Nomura research

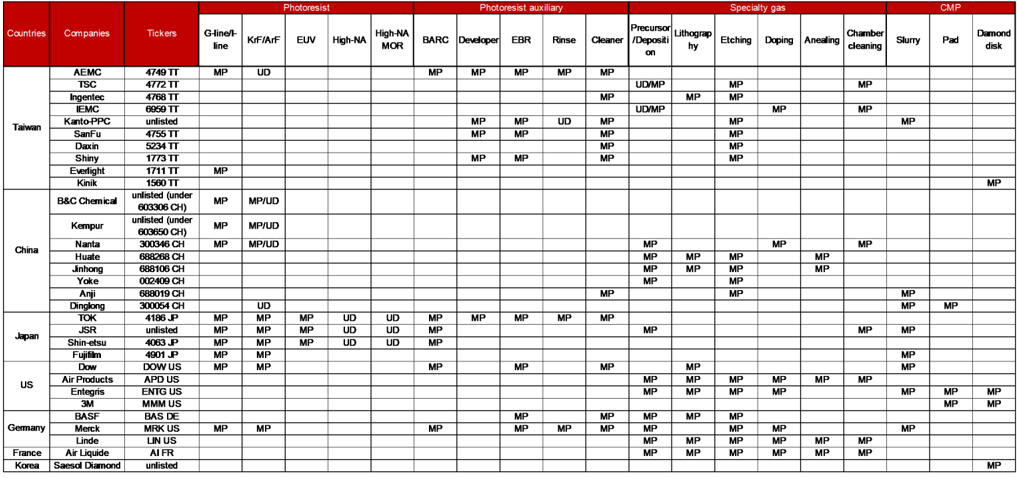

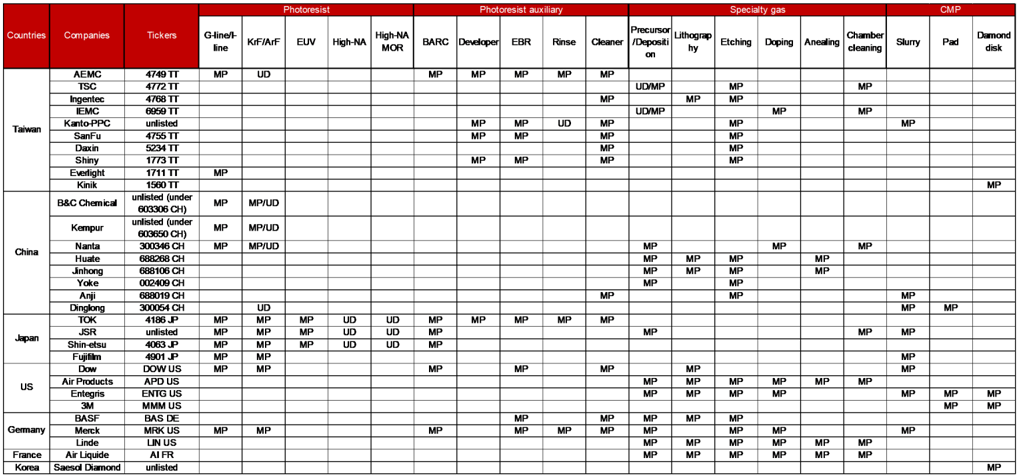

Countries

Taiwan

China

Japan

US

Germany

France

Korea

Companies

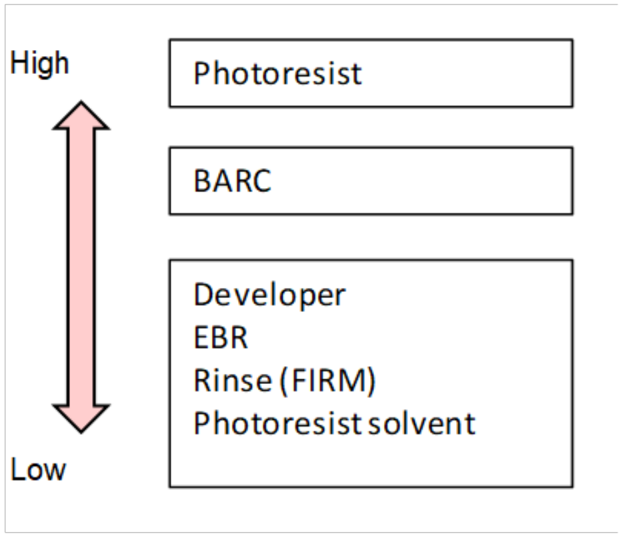

Tickers

G-line/t- line

Photoresist

EUV

High-NA

MOR

KrF/ArF

BARC

Photoresist auxiliary

Developer

EBR

Rinse

Fig. 45: Matrix of some key semi materials vs suppliers

Ingentec

Kanto-PPC

B&C Chemical

Air Products

Air Liquide

Saesol Diamond

Precursor Lithograp

Cleaner /Depositi on

MP

MP

hy

UD/MP

Specialty gas

Etching

Doping

MP

MP

Chamber cleaning

MP

| 4768 TT 6959 TT | MP 333 | MP | |||

|---|---|---|---|---|---|

| 5234 TT 1773 TT 1711 TT | MP | ||||

| 1560 TT | |||||

| unlisted (under | MP MP/UD | ||||

| 603306 CH) unlisted (under | |||||

| 603650 CH) | MP MP/UD | ||||

| MP/UD | |||||

| 300346 CH | MP | ||||

| 688268 CH | |||||

| 688106 CH 002409 CH | |||||

| 688019 CH 300054 CH 4186 JP | MP UD MP | MP | |||

| unlisted | MP MP | MP | 565 | ||

| 4063 J 4901 P | MP MP MP MP | MP | |||

| DOW US | MP MP | ||||

| APD US | |||||

| ENTG US MMM US | 33 | 333 1 33 | |||

| BAS DE | |||||

| MRK US | MP MP | ||||

| LIN US | |||||

| AI FR | |||||

| unlisted |

Source: Company data, Nomura research

Note: MP = mass production; UD = under development

Semi material market growth underperformed Semi and Semi equipment; gradual mean reversion could be seen post 2027F

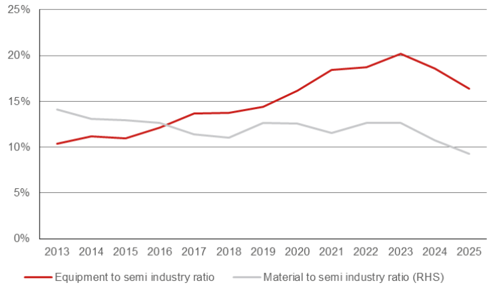

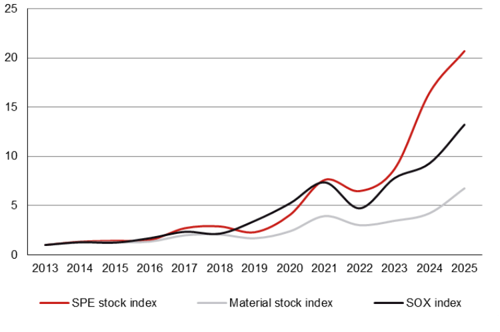

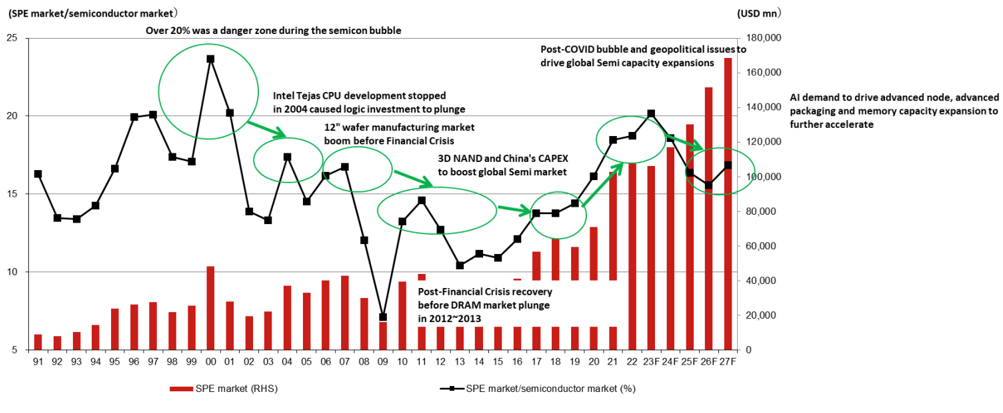

According to the Semiconductor Industry Association (SIA), SEMI, and Statista, semiconductor materials revenue represented only 9.3% of semiconductor industry market value in 2025, the lowest point since 2013. This implies a USD1bn semiconductor market value would only require USD93mn worth of semiconductor materials (Fig. 46 ). At the same time, the value of SPE has outpaced semi materials since 2017, leading to overall semi material companies’ stock price performances significantly underperforming those of SPE stocks (Fig. 48 -49 ).

The major reasons for the underperformance include:

- The rise of advanced chips such as AI accelerators, which carry significantly high ASPs ·

Since 2023, demand for AI accelerators has surged quickly. Nvidia’s (NVDA US, Not rated) H100/B200 GPUs and custom ASICs from Google (GOOGL US, Not rated) and Amazon (AMZN US, Not rated) command extraordinary price premiums. A single AI GPU can be priced at USD30,000, but the semi wafer and process chemicals inside it cost a few hundred dollars at the most. So, as AI chips boost the total semiconductor revenue figure, materials spending doesn’t keep pace.

- Moore’s Law makes the manufacturing processes more complicated than materials ·

As transistor sizes shrink, more compute cores can be included onto the same physical semi wafer area. As a result, the value of manufacturing processes (more photolithography, etching processes, etc.) extracted per semi wafer has been growing even faster. Thus, revenue per unit of material consumed has continued to rise.

- Semi oversupply cycle has more direct impact on demand for materials ·

Materials consumption tracks fab production and utilization. During downturns, fabs run at reduced capacity, materials purchases fall sharply, but the Semi market doesn’t collapse as dramatically because it includes inventories which can be sold to the market and can charge higher ASPs driven by new applications such as AI and advanced node migrations.

However, we do not rule out the possibility that semi materials market value could see a gradual mean reversal post 2027F, due to:

MP

High-NA

MP

Anealing

Slurry

CMP

Pad

Damond disk

Gate-all-around (GAA) transistors and new materials ·

Moving from FinFET to GAA at 2nm and below requires entirely new material sets nanosheet channels, high-k dielectrics, and new ALD (atomic layer deposition) precursors. Each process step demands higher-purity, more expensive chemicals. The materials cost per wafer at leading-edge nodes is rising faster than at previous transitions.

Backside power delivery and wafer-bonded NAND driving more semi wafer, wafer thinning, grinding and CMP usage ·

Backside power delivery enables power delivery from the first semi wafer’s backside to the active devices in the frontside, with an additional second semi wafer as a permanent carrier. Semi wafer usage and the wafer-thinning process, simply put, will double. Also, CMP usage will increase as well, as both backside and frontside of the first semi wafer are required to be processed.

On the other hand, the wafer-bonded NAND will also drive more semi wafer and CMP usage, in our view, as it involves creating the CMOS circuitry that controls the memory cells and the memory cell array on separate wafers, then inverting the wafer with the memory cell array and bonding the two wafers together.

Photoresist’s value increasing by at least double with the adoption of high-NA EUV ·

Metal-oxide resists are probably the leading alternative to photo acid-driven chemistries, or chemically amplified resists (CAR). These resists offer inherently good etch resistance. The dense core absorbs more energy, too, attenuating electron energy and reducing blur. Due to the change of materials, the photoresist price for high-NA EUV could be much higher than the existing EUV. According to our industry survey, the value of photoresist for high-NA EUV could go as high as USD10,00040,000 per gallon, increasing significantly from USD5,000 for existing EUV.

Advanced packaging adoption rising quickly ·

HBM stacking and chiplet architectures such as AMD’s 3D V-Cache, Intel’s Foveros, TSMC’s CoWoS and SoIC - stack multiple dies together using advanced packaging techniques. This dramatically increases material consumption per final product: more organic substrates, more underfill resins, more copper interconnects, more thermal interface materials.

Glass interposer and glass core substrate are new rising trends ·

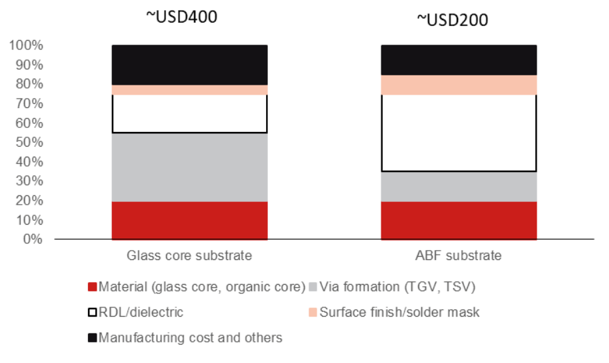

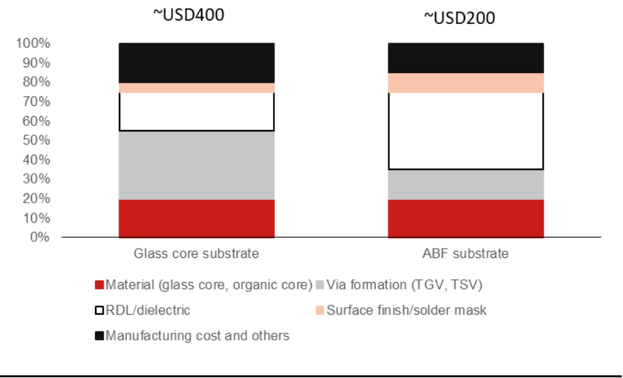

Glass core substrates and interposers are being pursued intensively by leading device makers, materials suppliers, and equipment vendors for advanced packaging applications. Taking glass core substrate as example, the cost initially should be higher than existing ABF substrate, considering it is still at an early stage. However, glass core substrate has the following advantages, including: 1) flatness and less warpage; 2) better heat dissipation; 3) low loss favorable to high-speed signaling; and 4) large-format integration; therefore, we expect glass core substrate will play a important role along with existing ABF substrate.

Compound semi and SOI wafers scaling up ·

SiC, GaN, InP and SOI substrates are now widely used for power electronics and optical communication applications and require fundamentally different and more expensive substrate materials than semi wafer.

The avelage glovai sell matchat marnet to sell market late has lanen years

25%

USD bn

900

20%

800

700

600

15%

500

400

300

10%

200

5%

100

0

0%

Source: WSTS, SEMI, Nomura research

24%

USD bn

25

50.0

Fig. 46: Global semi material market to total Semi market ratio The average global semi material market to semi market ratio has fallen below the average level of around 12% since 2024 16%

440

30.0

Source: WSTS, SEMI, Nomura research

Fig. 48: Global SPE market to semi market ratio vs global semi material market to semi market ratio

The content value of Semi materials has underperformed SPE in the past 10 years

Source: WSTS, Semi.org, Nomura research

12%

306

43

Fig. 47: Semi materials sales: manufacturing vs packaging

Source: WSTS, SEMI, Nomura research

Fig. 49: The performance of global SPE index vs Semi material index vs SOX index since 2013

Source: Bloomberg Finance L.P, Nomura research

2025 2030F

CAGR

Fig. 50: Global semi materials sales breakdown by different segment in 2025 vs 2030F

Photoresist

Photoresist auxiliary

Process chemical

Electric gas

Sputtering material

CMP

Others

Packaging substrate

Leadframe

Wire bonding

Packaging material

Ceramic substrate

Adhesive material

Others

| 7.3% | 7.8% | |

|---|---|---|

| 8.0% 7.1% | ||

| 4.1% 3.6% | ||

| 15.3% 13.6% | ||

| 3.4% 3.1% | ||

| 7.7% 8.2% | ||

| 9.9% 8.8% | ||

| Total IC manufacturing material market (USD bn) | 46.5 85.0 | 12.8% |

| 38.7% 49.9% | ||

| 16.2% 12.2% | ||

| 12.9% 12.1% | ||

| 10.7% 7.7% | ||

| 4.4% 4.5% | ||

| 2.2% 2.5% | ||

| Total IC packaging material market (USD bn) | 27.1 45.1 | 10.7% |

| Total Semi material market (USD bn) | 73.6 130.1 | 12.1% |

Source: SEMI, Nomura estimates

The evolution of TSMC’s local sourcing plan

To strengthen local supply chain resilience, enhance the local economy, and reduce carbon emissions during transportation, TSMC has expanded the goal scope for local sourcing globally, encompassing six categories: equipment, components, raw materials, facility systems, automation, and goods across TSMC’s major operational production fabs (TSMC fabs in Taiwan, TSMC (China), TSMC (Nanjing), TSMC Washington, LLC, TSMC Arizona, and JASM) over the past decade, to aid local suppliers in upgrading technology and quality, cutting costs, and diminishing carbon emissions. Concurrently, localized procurement objectives have been defined at each site to reinforce global capabilities for regional material supply.

The goal has been changed a few times since 2018, including:

- As the production capacity of silicon wafers (semi wafer) in Taiwan failed to meet TSMC requirements, the target of local sourcing was adjusted from “local sourcing of raw materials” to “local sourcing of indirect raw materials” in 2018. 1.

- For backend equipment, since the proportion of advanced packaging has increased and both quality requirements and technical specifications have become stricter, TSMC has also increased the procurement volume of domestic and foreign suppliers, and the demand for foreign suppliers is still strong; therefore, TSMC removed the target beginning in 2021. 2.

- In 2020-23, the proportion of spare parts in advanced processes increased compared to previous years. However, the localization of spare parts in advanced processes is still in the development stage, so the annual target was not reached. 3.

- To improve transparency in localized procurement information, a new management indicator for the local procurement ratio of overseas subsidiaries was introduced in 2024. 4.

Based on these changes, we summarize the read-across to TSMC’s suppliers by different sectors:

- TSMC has high specs for semi wafer, which is the largest portion of the semi raw materials market. As TSMC has still not yet brought back its target of ‘local sourcing of raw materials’, we believe the leading semi wafer companies in Taiwan, such as GlobalWafers, may still have room to strengthen its technology capability to meet TSMC’s requirements, particularly for advanced node production. 1.

- For indirect raw materials, we believe the future growth driver is likely to be TSMC’s overseas facilities, particularly TSMC Arizona, which is likely to become an important facility that will ramp up products continuously, while the localization rate in Taiwan has been increasing to a relatively high level. 2.

- TSMC indicated that the spare parts and back-end equipment localization rates were not satisfactory due to the rising requirements for advanced processes and packaging, which implies there may be still room for spare parts and back-end equipment companies to further strengthen their technology capabilities. 3.

80%

70%

60%

50%

40%

30%

20%

10%

0%

fabs in US and Japan

Ramp up N2 and A16 with new fabs in US and Japan

Fig. 51: TSMC’s semi material, spare parts and back-end equipment localization plan

20

15

10

5

0

Source: TSMC, Nomura estimates

TSMC’s capex in 2027F could exceed market expectations

TSMC continues to build up new capacity in Taiwan and overseas. TSMC now has 26 advanced wafer fabs and advanced packaging facilities ramping up or planned globally (18 of them are in Taiwan). We formulate our high-volume manufacturing timeline assumptions in Fig. 52 -53 , which suggest that TSMC will have more fab modules coming onstream in post 2027 and are consistent with management commentary: ‘… So 2026-2027 for the short term, we are looking to improve our productivity. 2028 to 2029, yes, we start to increase our capacity significantly’ during the company’s earnings call in early-2026. As a result, we expect TSMC to spend up to around USD70bn in capex in 2027F considering more than 10 new fab modules would be expanded simultaneously in Taiwan and overseas.

Fig. 52: TSMC’s total fab module numbers and the net additions of fab modules

Source: TSMC, Nomura estimates

4

Tainan

80

70

60

50

40

Hsinchu

30

20

10

40nm

HVM

Kaohsiung

0

Taichung

TSMC Nanjing

TSMC Arizona

JASM

ESMC

2020

2021

P2 (N5)

Fig. 53: TSMC’s fab expansion plans

2026F

60.0%

| P5 (N3) | ||

|---|---|---|

| P6 (N3) | ||

| P2 (N2) | ||

| Fab 16 | P2 (N28) | P1 (N16/12) |

| Fab 21 | P1 (N4) | |

| P4 (?) | ||

| Fab 23 Fab 24 | P1 (N40/N28/N12) P2 (N6) | P1 (N28/N12) |

Source: TSMC, Nomura estimates

Fig. 54: TSMC’s capex and capex-intensity trends

We expect TSMC’s capex could reach USD70bn in 2027F

Source: Company data, Nomura estimates

2022

2023

2024

2nm

2025

1.6nm

HVM

2027F

2028F

2029F

2030F

DUV

ArFi

NXT1980

Model year

2015

2016

Wave length

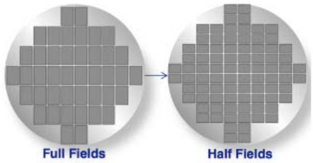

193nml

193nm

WPH

250

275

Numerical aperture

1.35

1.35

Mix-and-match overlay

Resolution (half pitch)

3.5nm

2.5nm

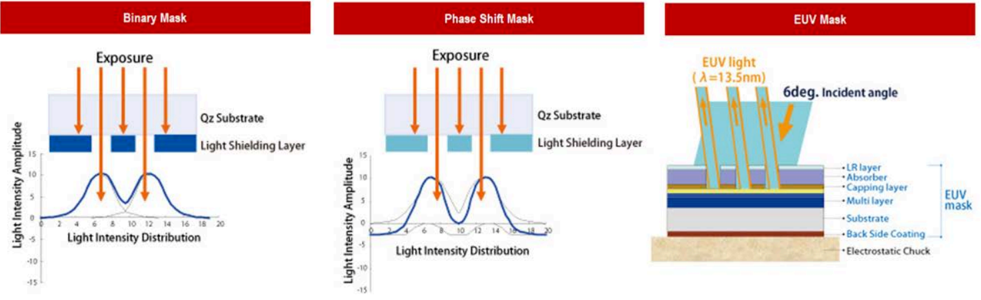

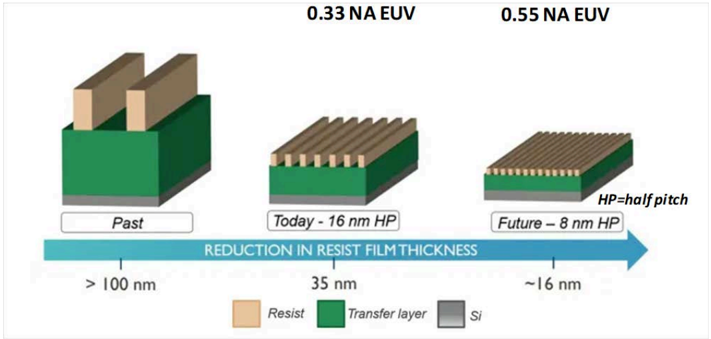

High-NA EUV - the evolution of EUV in A10 node onward 13.5nm 160 0.33 1.1nm

Currently, the most advanced chips are manufactured using EUV lithography, specifically ASML’s Twinscan NXE:3400C system, which has 0.33 numerical aperture (NA) optics, providing a 13nm resolution (half pitch). This level of resolution is sufficient for a singlepattern approach at 7nm/6nm nodes, with around 36nm metal pitches (>13nm*2=26nm), and at 5nm with around 28nm metal pitches. However, as the metal pitches decrease below 26nm (beyond the 3nm node), 13nm resolution might require double patterning. For post-3nm nodes, ASML and its partners are developing a new EUV tool called the Twinscan EXE:5000-series with a 0.55 NA (High-NA) lens that can achieve 8nm resolution, which is anticipated to eliminate multi-patterning at 3nm and beyond. Intel had already installed high-NA EUV in 2H24 for its 14A node development, and TSMC in 2025F for its 2nd-gen 1.4nm development. Although High-NA scanners are still under development and the usage for major customers’ mass production may not happen until 2029-30F (as TSMC would not use high-NA for mass production until A10), we believe high-NA EUV is expected to be extremely complex, large, and expensive, with a price tag of over USD400mn each. Additionally, these scanners will require new optics, a new light source, and even new fab buildings to accommodate them. Despite these challenges, leading makers of logic chips and memory devices are willing to adopt new technologies to keep up with the scaling of performance, power, area, and costs (PPAc) of semiconductors. Therefore, high-NA EUV scanners are crucial, in our view.

Fig. 55: Specs of ASML’s DUV and EUV

Source: ASML, Nomura research

The three factors of photolithography - wave length, numerical apertures, and k1 coefficient

The critical dimension (CD), the smallest possible feature size that can be printed with a certain photolithography-exposure tool, is proportional to the wavelength of light divided by the numerical aperture (NA) of the optics. So, smaller CDs can be achieved by using either shorter light wavelengths or larger numerical apertures, or a combination of the two. The k1 value can be pushed as close as possible to its physical lower limit of 0.25 by improving manufacturing-process control. The formula is ‘CD=k1*(wave length/NA)‘.

In general, the most economical ways to boost resolution are by increasing the numerical aperture and by improving tool and process control to allow for a smaller k1. Only after chipmakers run out of options to further improve NA and k1 do they resort to reducing the wavelength of the light source. The switch to EUV (13.5nm light) from 193nm light has done part of the job of decreasing CD. Now it looks like NA will be boosted again, from today’s 0.33 to 0.55.

How high-NA EUV works? Anamorphic optics is critical

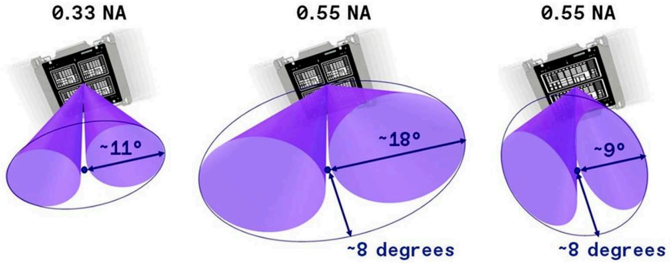

Increasing the NA from 0.33 to the target value of 0.55 inevitably entails a cascade of other adjustments. Projection systems such as EUV lithography have an NA at the wafer and also at the mask. When you increase the NA at the wafer, it also increases the NA at the mask. Consequently, at the mask, the incoming and outgoing cones of light become larger and must be angled away from each other to avoid overlapping. Overlapping cones of light produce an asymmetric diffraction pattern, resulting in unpleasant imaging effects.

⇐38nm

⇐38nm

⇐38nm

⇐38nm

⇐13nm

⇐13nm

⇐13nm

⇐13nm

⇐13nm

⇐8nm

14-28nm

7-14nm

7nm

5-7nm

5-7 nm

5-7 nm

3-5nm

1.4-3nm

1.4-3nm

1-2nm

1-2nm

The reflection decreases significantly when angle

ML reflection field printing as well

0.33 NA

0.55 NA

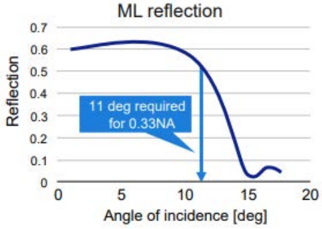

But there’s a limit to this angle. Because the reflective masks needed for EUV lithography are actually made of multiple layers of material, it is not possible to get a proper reflection above a certain reflective angle. EUV masks have a maximum reflective angle of 11 degrees. There are other challenges as well, but reflective angle is the biggest, according to ASML. ~11°

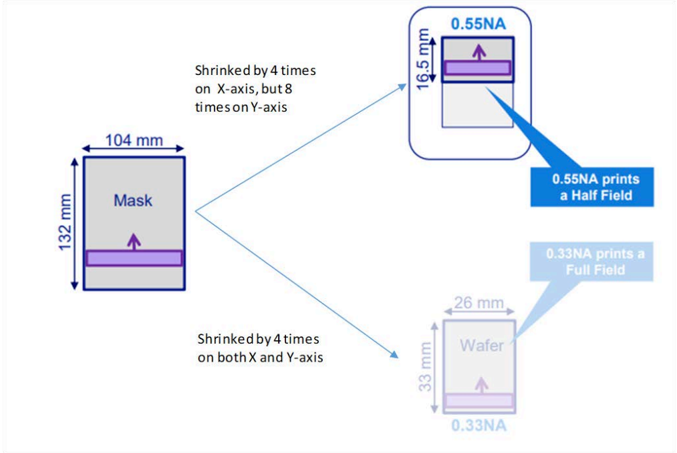

The angle of reflection at the mask in today’s EUV is at its limit of 11 degrees. Increasing the NA of EUV would result in an angle of reflection that is too wide (more than 15 degrees). So high-NA EUV uses anamorphic optics supplied by Zeiss (unlisted), which allow the angle to increase in only one direction on the X-axis. The field that can be imaged this way is half the size on the Y-axis, so the pattern on the mask must be distorted in one direction, but that’s good enough to maintain throughput through the machine. Shrinked by 4 times on both X and Y-axis

0.55NA

,26 mm,

Wafer

Fig. 57: EUV: High-NA requires an anamorphic lens

The anamorphic lens can reduce the angle of incidence on the Y-axis by half, but results in a halffield printing as well

Source: ASML, Nomura research

Fig. 59: Half-field printed chips vs full-field printed chips - 2

Source: ASML, Nomura research

0.7

0.6

0.5

0.4

0.3

0.2

0.1

0

Fig. 56: Mask multilayer reflection vs angle of incidence

The reflection decreases significantly when angle of incidence is approaching 15 degrees

Source: ASML, Nomura research

Fig. 58: Half-field printed chips vs fullfield printed chips - 1

The size of half field printed chip is half of full field’s

Source: ASML, Nomura research

0.55 NA

~9°

0.55NA prints a Half Field

0.33NA prints a

Full Field

~8 degrees

0.33 NA EUV

0.55 NA EUV

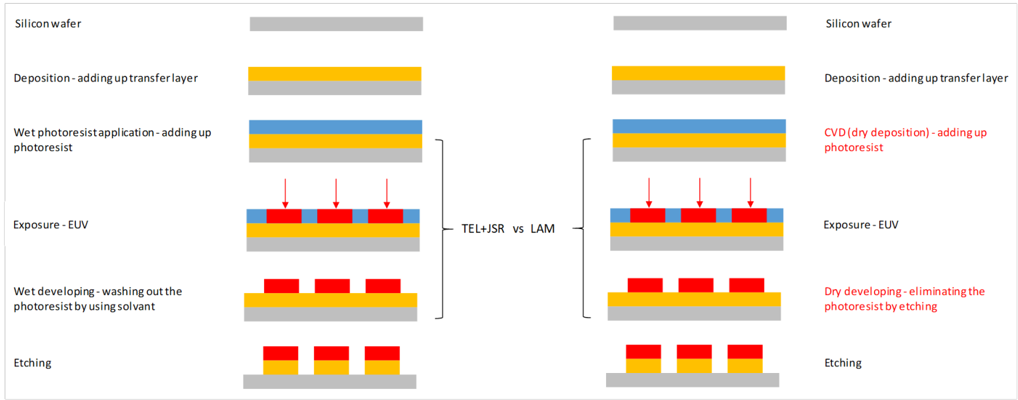

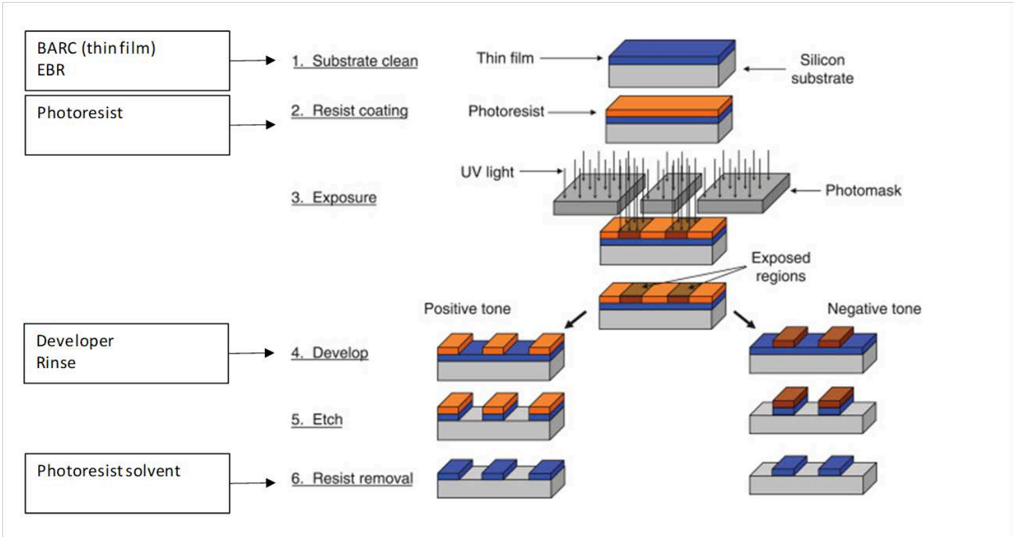

Photoresist, stitch overlay control, SoIC (hybrid bonding), and absorber for mask are also critical for high-NA EUV

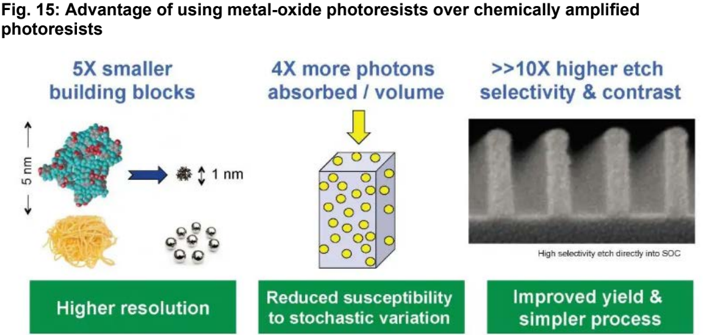

Based on the fundamentals of high-NA EUV and the difficulties found during the R&D stages, we expect there are two critical technology issues that need to be resolved: photoresist and stitch overlay.

The change of photoresist and related materials are required

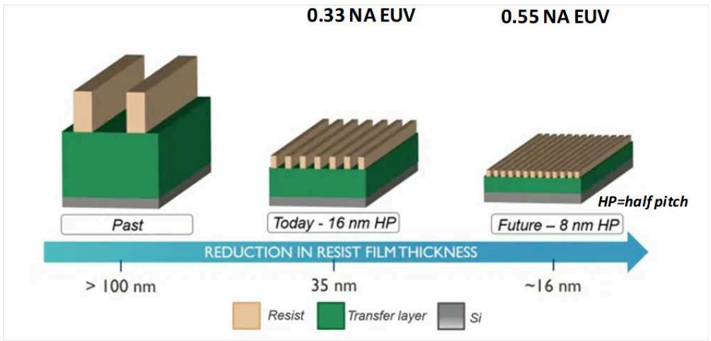

HP=half pitch

With a higher NA, photons strike the wafer at a more shallow angle. That requires thinner photoresist layers are needed to avoid shadowing. The upside is that a thinner resist layer reduces the risk of pattern collapse, as the aspect ratio of resist features is smaller. However, it also provides less protection for the wafer. In addition, long etch processes used to create high-aspect-ratio wafer features can erode the resist layer, ultimately degrading the transferred pattern. With less material, a thinner resist also captures fewer photons, potentially making roughness and other stochastic effects worse.

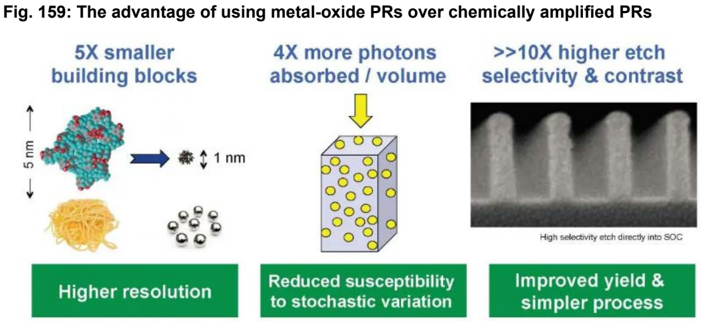

At present, metal-oxide resists are probably the leading alternative to photo acid-driven chemistries, or chemically amplified resists (CAR). Based on a metal-oxide core, surrounded by ligands that tune solubility, cross-linking, and other properties, these resists offer inherently good etch resistance. The dense core absorbs more energy, too, attenuating electron energy and reducing blur. Due to the change of materials, the photoresist price for high-NA EUV could be much higher than for the existing EUV. According to our industry survey, the value of photoresist for high-NA EUV can go up to USD10,000-40,000 per gallon, a significant increase from USD5,000 for existing EUV.

Improved etch resistance and absorption address the most serious limitations of thin resists, offering a high NA-friendly solution. Unfortunately, only negative tone metal-oxide resists are available, so they cannot be used for contact holes. Both Inpria (acquired by JSR) and Lam Research offer metal-oxide resists, differentiated in part by their approaches to development.

Lam Research is attempting to disrupt the whole stack. Instead of a wet PR technology using a spin coater, it plans to use a chemical vapor deposition process to layer on a metal PR. The throughput and patterned lines would be slower but more accurate. If using Tokyo Electron (TEL) (8035 JP, Buy) and JSR’s solution, due to the change of the PR materials, the developer would need to be changed as well. Currently,

Tetramethylammonium Hydroxide (TMAH) is widely used as developer for existing EUV. But for high-NA EUV, propylene glycol methyl ether acetate (PGMEA) with acid is likely a better solution. We expect TOK is likely the major supplier. The purity requirement of developer would be higher as well.

Although the existing wet process solution supplied by TEL and JSR will be likely more cost effective without procuring the new equipment, we expect TSMC could be more likely to adopt Lam Research’s solution in the high-NA EUV era.

Fig. 60: Reduction in photoresist film thickness

Source: Cadence, Nomura research

Lall nesear ulle bolly uly depostun allu uly uevelop eyurpment lu growemmale photoreolol

Mithough Mon cales Wighel nor, the uodge lo much smallel that legulal mighta suv photoresist

4X more photons absorbed / volume

building blocks

45000

40000

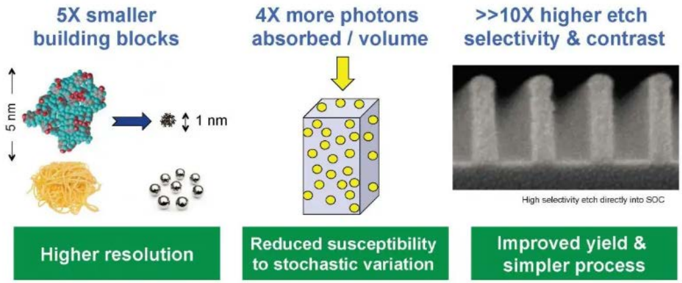

>>10X higher etch selectivity & contrast

Fig. 61: Advantage of using metal-oxide photoresists over chemically amplified photoresists

Wet photoresistapplication - adding up photoresist

35000

30000

25000

Exposure - EUV

20000

15000

Higher resolution

Wet developing - washing out the photoresist by using solvant

10000

5000

Etching

0

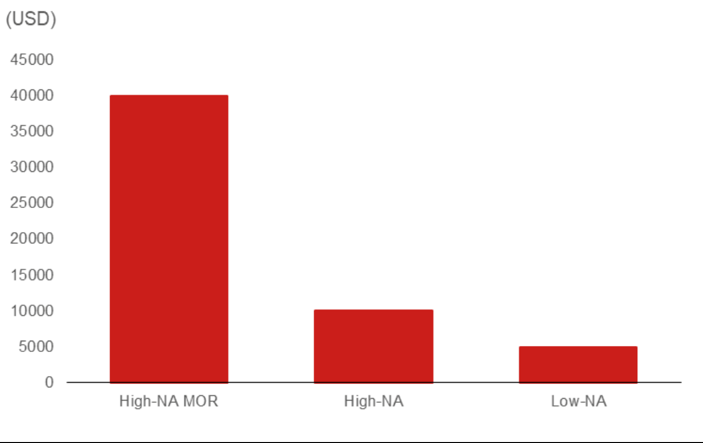

High-NA MOR

Source: Inperia, Nomura research

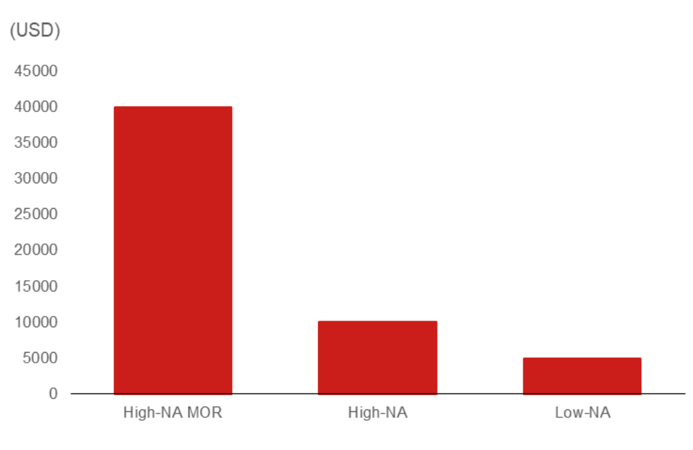

Fig. 62: Price of photoresist per gallon

Although MOR carries higher ASP, the usage is much smaller than regular high-NA EUV photoresist

Source: Nomura estimates

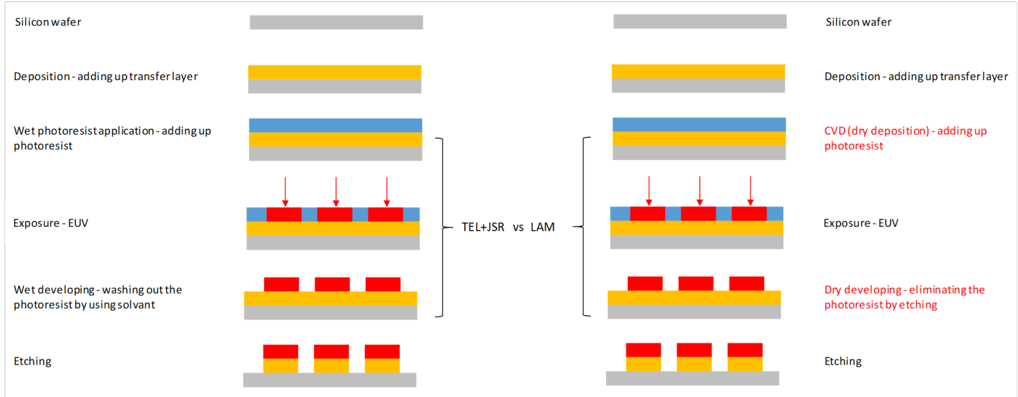

Fig. 63: TEL and JSR vs Lam Research’s solution

Lam Research is using dry deposition and dry develop equipment to grow/eliminate photoresist

Source: TEL, Lam Research, Nomura research

High-NA

LoW-NA

Silicon wafer

Deposition - adding up transfer layer

CVD (dry deposition) - adding up photoresist

Exposure - EUV

Dry developing- eliminating the photoresist by etching

Etching

ASP (USD per gallon)

Nodes (nm)

Suppliers

Note

‹100

100-1000

ArF

1000-1500

EUV

1000-5000

High-NA EUV

5000

Fig. 64: Specs of different photoresists by nodes and major suppliers

High-NA MOR (metal oxide resist)

10000

>40000 (but with low throughput)

13.5 (with 0.55 NA)

⇐1nm

| TOK | Shin-etsu | Shin-ets u | Shin-etsu TOK | Entegris | Entegris |

|---|---|---|---|---|---|

| Dow | JSR | TOK | JSR Shin-etsu | Gelest (Nanomate) | |

| Merck | Dow | Sumitomo | |||

| Fujifilm | Fujifilm | ||||

| TOK is the | TOK is the | ||||

| Market share consolidation to winner of EUV | Market share consolidation to winner of EUV | JSR could regain share in high-NA EUV technology could outpace Tokyo Electronc’s track technoloy | |||

| photoresist | photoresist | 2. Entegris and Gelest (through | |||

| market used ony 1-2nm nodes | market used ony 1-2nm nodes | Nanomate in Taiwan) could be the | |||

| new photo resist suppliers |

Source: Nomura estimates

Stitch overlay control for large-die-size ICs is critical, in our view