PDF 原檔:JPM_Innostar_Service_The_2026-06-22_5259886_original.pdf

原始內容

J.Л.

norgan

Innostar Service

The next shining star driven by innovation; initiate at OW

We initiate coverage of Innostar Service at OW with a Dec-27 PT of NT$4,000, based on 25x 2028E P/E. Innostar is the leading MEMS probe card automation equipment supplier globally, with dominance in the needle assembly market. Given the strategic partnership/ investment by Technoprobe (TP, TPRO IM, Not Covered), one of the top-two probe card vendors worldwide, Innostar's probe card business outlook and exposure has been lifted to the next level, gathering steam to accelerate growth in 2026-28, with a multi-times increase of higher-spec needle assembly machine orders and TAM expansion to material kits and OEM services of needle assembly/repair. Innostar Service's penetration and smooth progress into the glass core substrate (GCS) market with its TGV (Through Glass Via) copper pillar mass transfer technology/product applied in advanced packaging should also become a new driver for the company from late 2027, followed by mass production schedule of US tier-1 networking customer's next-gen switch ASIC. We model an EPS CAGR of 200% in 2025-28, significantly above market expectations, as we believe the Street has underestimated the continued upward revision of probe card equipment orders from TP and the decent content of its TGV copper pillar in glass core substrate. With an undemanding valuation, these catalysts should continue to drive share price outperformance. Key risks include: TP's share loss, slower chip probing spec upgrade, and delay in GCS adoption.

- Strong probe card equipment orders, driven by TP's accelerated capacity expansion for rising ASIC and advanced node demand. We model the company's probe card equipment revenue to grow 2x/3x YoY in 2026/27 and another 2x YoY in 2028, backed by continued upward revisions of higher-end needle assembly machine shipment orders for TP's accelerated probe card capacity expansion, along with the material ASP growth from equipment spec upgrades (from single-arm to a dual-arm solution). We believe the stronger demand will be driven by TP's rising high-end probe card orders for new CSP ASIC and advanced node demand from foundry customers.

- New copper pillar mass transfer business for glass core substrate TGV to drive the next wave of multi-times growth. Innostar is engaging with a US tier-1 networking chip vendor to enable glass core substrate adoption in its next-gen switch ASIC, expected from late 2027/28, as it could become the sole supplier of the copper pillars applied for the TGV metallization of glass core substrates. With the high content and solid volume of the switch ASIC, we model the new copper pillar business to contribute 8%/20% of revenue in 2027/28, while there could be upside from another US GPU vendor that is also working with Innostar for its future networking chip.

- Undemanding valuation. Our Dec-27 PT of NT$4,000 is based on 25x 2028E P/E, largely in line with probe card and glass core/TGV peers' 2028E-based valuation of 20-30x. With its leadership in probe card needle assembly and future TAM expansion to TGV, we believe Innostar Service could deliver accelerated earnings growth in 2026-28, which should support its valuation.

Sources for: Style Exposure - J.P. Morgan Global Markets Strategy; all other tables are company data and J.P. Morgan estimates.

See page 27 for analyst certification and important disclosures, including non-US analyst disclosures.

Initiation

Overweight

7828.TWO, 7828 TT

Price (22 Jun 26):NT$2,040.00

Price Target (Dec-27):NT$4,000.00

Technology

William Yang AC

(886-2) 2725-9899 william.yang@jpmorgan.com

J.P. Morgan Securities (Taiwan) Limited

Megan Hsueh (886-2) 2725-9249

megan.hsueh@jpmorgan.com

J.P. Morgan Securities (Taiwan) Limited

Gokul Hariharan

(852) 2800-8564 gokul.hariharan@jpmorgan.com J.P. Morgan Securities (Asia Pacific) Limited/ J.P.

Morgan Broking (Hong Kong) Limited

| Quarterly Forecasts (FYE Dec) | Quarterly Forecasts (FYE Dec) | Quarterly Forecasts (FYE Dec) | Quarterly Forecasts (FYE Dec) |

|---|---|---|---|

| Adj. EPS (NT$) | 2025A | 2026E | 2027E |

| Q1 | 0.46 | 1.02A | 2.33 |

| Q2 | (0.45) | 3.39 | 6.69 |

| Q3 | 1.37 | 3.72 | 20.36 |

| Q4 | 4.92 | 6.33 | 34.59 |

| FY | 6.32 | 14.46 | 63.97 |

Flice Ferrormance

3k

J.P. Morgan

2k

NT$

1k

0

Jul 25

Oct 25

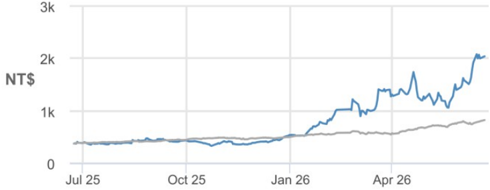

Price Performance

Jan 26

Apr 26-

— TSE (rebased)

| Company Data | |

|---|---|

| Shares O/S (mn) | 37 |

| 52-week range (NT$) | 2,155.00-300.00 |

| Market cap ($ mn) | 2,369 |

| Exchange rate | 31.58 |

| Free float (%) | 48.8% |

| 3M ADV (mn) | 0.50 |

| 3M ADV ($ mn) | 22.3 |

| Volatility (90 Day) | 104 |

| Index | TAIEX |

| BBG ANR (Buy | Hold | Sell) | 2|0|0 |

Key Metrics (FYE Dec)

| NT$ in millions | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|

| Financial Estimates | ||||

| Revenue | 716 | 1,620 | 5,604 | 12,849 |

| Adj. EBIT | 278 | 683 | 3,133 | 7,903 |

| Adj. EBITDA | 319 | 758 | 3,397 | 8,381 |

| Adj. net income | 228 | 531 | 2,347 | 5,955 |

| Adj. EPS | 6.32 | 14.46 | 63.97 | 162.32 |

| BBG EPS | - | 18.08 | 43.18 | 100.76 |

| Cashflow from operations | (86) | 235 | 3,289 | 6,550 |

| FCFF | (400) | (670) | 2,216 | 5,151 |

| Margins and Growth | ||||

| Revenue Growth Y/Y (%) | 76.4% | 126.2% | 245.9% | 129.3% |

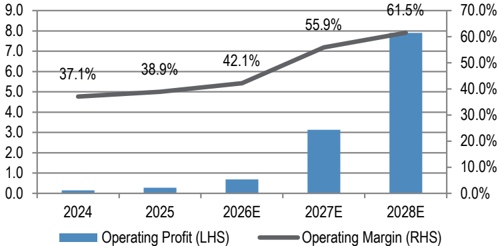

| EBIT margin | 38.9% | 42.1% | 55.9% | 61.5% |

| EBIT Growth Y/Y (%) | 84.9% | 145.4% | 358.8% | 152.2% |

| EBITDA margin | 44.6% | 46.8% | 60.6% | 65.2% |

| EBITDA Growth Y/Y (%) | 69.8% | 137.2% | 348.3% | 146.7% |

| Net margin | 31.8% | 32.7% | 41.9% | 46.3% |

| Adj. EPS growth | 19.8% | 128.8% | 342.4% | 153.7% |

| Ratios | ||||

| Adj. tax rate | 17.8% | 23.6% | 25.0% | 25.0% |

| Interest cover | NM | NM | 795.9 | NM |

| Net debt/Equity | NM | 0.3 | NM | NM |

| Net debt/EBITDA | NM | 0.6 | NM | NM |

| ROE | 25.0% | 41.4% | 100.8% | 111.9% |

| Valuation | ||||

| FCFF yield | (0.5%) | (0.9%) | 3.0% | 6.9% |

| Dividend yield | 0.1% | 0.2% | 0.6% | 2.5% |

| EV/Revenue | 101.7 | 45.6 | 12.9 | 5.3 |

| EV/EBITDA | 228.0 | 97.4 | 21.2 | 8.2 |

| Adj. P/E | 322.7 | 141.1 | 31.9 | 12.6 |

Source: J.P. Morgan Global Markets Strategy for Performance Drivers; company data, Bloomberg Finance L.P. and J.P. Morgan estimates for all other tables. Note: Price history may not be complete or exact.

Summary Investment Thesis and Valuation

Investment Thesis

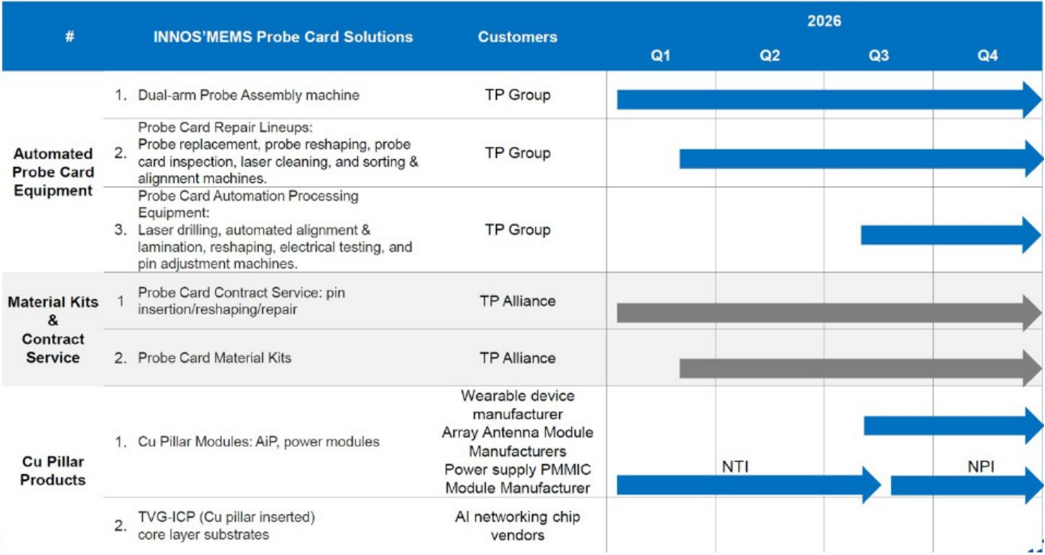

We rate Innostar Service OW, as we anticipate further stock outperformance to be driven by the next wave of earnings upgrade cycle in the next 2-3 years, with three solid growth drivers ahead: 1) probe card needle assembly machine order shipment to increase multiple times in 2026-28, thanks to the largest customer's surging demand, 2) TAM expansion by providing probe card material kits (mainly pins/needles) and needle assembly/repair OEM services, and 3) new TGV (Through Glass Via) copper pillar mass transfer business for the advanced packaging process of future-gen networking and AI chips (applying in CoWoS substrate for an ongoing networking project).

Valuation

Our Dec-27 PT of NT$4000 is based on 25x 2028E P/E, below its historical 12M fwd P/E of ~38x since IPO in May 2025, but largely in line with probe card and glass core/TGV peers' 2028Ebased valuation of 20-30x.

rigure 1. mostal delvice s o sona growil anivels

J.P. Morgan

INNOS'MEMS Probe Card Solutions

Probe Card Repair Lineups:

Automated

Probe replacement, probe reshaping, probe

Probe Card

Equipment alignment machines.

card inspection, laser cleaning, and sorting &

Probe Card Automation Processing

- Laser drilling, automated alignment &

Equipment:

pin adjustment machines.

Probe Card Contract Service: pin insertion/reshaping/repair

-

Probe Card Material Kits

-

Cu Pillar Modules: AiP, power modules

2.

Investment summary

Q3

Q4

→

We initiate coverage of Innostar Service with an OW rating, and a Dec-27 PT of NT $4000 (based on 25x 2028E P/E). The company undertook its IPO in May 2025; its share price has surged by ~500% in the past 12 months (vs the rise in Taiwan probe card vendors, MPI [NC] ~650% and WinWay [NC] ~700%, and the TAIEX ~110%), following remarkably strong demand in high-end (high pin count) probe cards and related equipment for AI chip testing. We expect further stock outperformance by Innostar Service to be driven by the next wave of the earnings upgrade cycle in the next 2-3 years, with three solid growth drivers ahead: 1) probe card needle assembly machine order shipments to increase multiple times in 2026-28, thanks to its largest customer's surging demand, 2) TAM expansion, by providing probe card material kits (mainly pins/needles) and needle assembly/repair OEM services , and 3) new TGV (Through Glass Via) copper pillar mass transfer business for the advanced packaging process of future-gen networking and AI chips, which are applied in CoWoS substrate for an ongoing networking project, not interposer.

TVG-ICP (Cu pillar inserted)

core layer substrates

Figure 1: Innostar Service's 3 solid growth drivers

Source: Company presentation.

2.

TP Group

Material Kits 1

&

Contract

Service

Cu Pillar

Products

Customers

Q1

Q2

2026

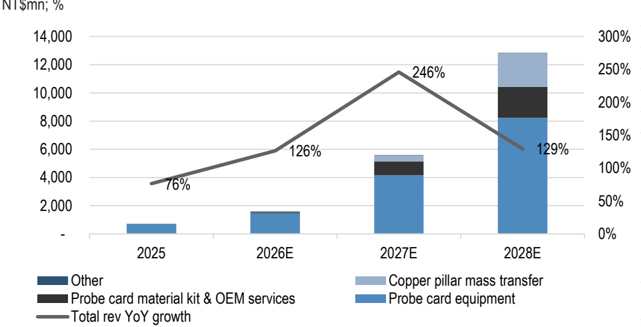

Figure 2: Strong 2026-2028E revenue growth from both existing and new businesses

Copper pillar mass transfer

Probe card material kit & OEM service

Probe card equipment

Source: Company data, J.P. Morgan estimates.

Dual-arm needle assembly machine Volume

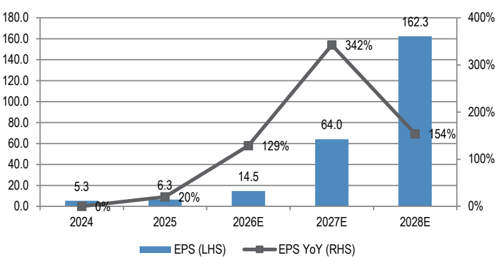

2026 revenue expected to grow sequentially, with exponential EPS growth of 130% YoY and another 340% YoY in 2026E and 2027E, driven by probe card equipment

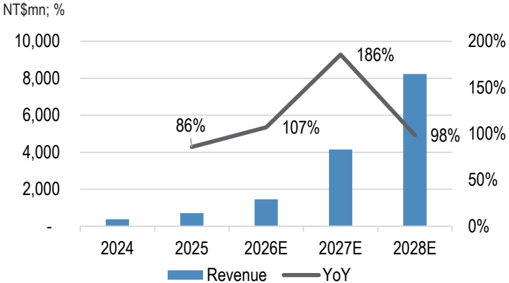

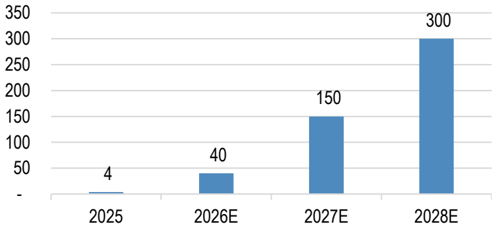

Innostar Service is currently a micro-electro-mechanical systems (MEMS) probe card needle assembly machine provider; its largest customer is Technoprobe (TPRO.MI), the second-largest probe card vendor worldwide (mainly competing with Form Factor as the leading player and MPI as the third-largest player in the probe card market). Driven by Technoprobe's multiple new AI probe card order wins (e.g., CSP ASIC) with its aggressive capacity expansion plans, followed by rising demand in MEMS probe cards with the spec upgrade in needle assembly machines, we model Innostar Service's probe card equipment revenue to grow ~100%/~200% YoY in 2026/27, with dual-arm needle assembly machine (spec upgraded version, with 2x content growth vs single-arm) shipments increasing to 40/150 units (even 300 units in 2028), based on our conservative estimates.

Further strong EPS growth in 2028 of 150% YoY (and likely more in 2029) with a meaningful contribution from TGV copper pillar business in advanced packaging

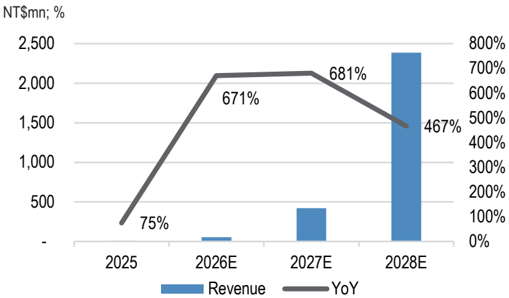

Post strong earnings growth of 2x and 4.5x YoY in 2026E and 2027E, we forecast Innostar Service to deliver a further 2.5x YoY EPS growth in 2028, driven by its new business contribution from the TGV copper pillar in advanced packaging (e.g. CoWoS). Based on our industry checks, the company is now working with a leading US fabless company for glass core substrate adoption in its next-gen switch ASIC solution, which is expected to enter mass production in late 2027-2028. Innostar Service will function as the sole supplier of the copper pillars in the TGV metallization process for the glass core substrate, if adopted. With the high content value (US$200-300/glass core substrate) and the dominant supply position for this project, we model Innostar Service's TGV copper pillar mass transfer business revenue to grow from NT$400mn in 2027 to NT$2.4bn in 2028, reaching ~20% revenue contribution with a solid GM at 70+%.

With the more aggressive TGV copper pillar capacity expansion plan by another 3x in 2028-29 (to 120k/month, merely for one customer's demand forecasts), we think it is worth monitoring whether another potential customer will kick-in in 2029. If this were to happen, 2029 would be another meaningful growth year for Innostar Service as we also see a US tier-1 GPU brand is working with Innostar Service for some samples. This could be a source of potential upside to Innostar Service's 2029 earnings and onward.

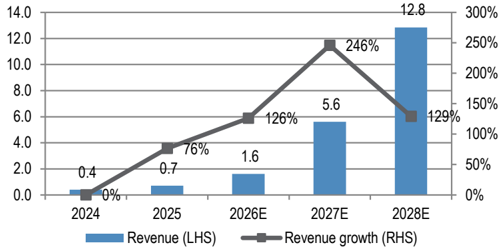

Figure 3: Innostar Service's revenue and revenue YoY growth

NT$bn, %

Source: Company data, J.P. Morgan estimates.

Figure 5: Innostar Service's OP and OPM

NT$bn, %

Source: Company data, J.P. Morgan estimates.

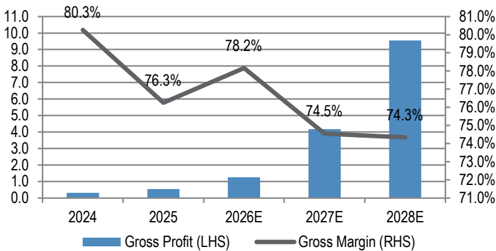

Figure 4: Innostar Service's GP and GPM

NT$bn, %

Source: Company data, J.P. Morgan estimates.

Figure 6: Innostar Service's EPS and EPS YoY growth

NT$, %

Source: Company data, J.P. Morgan estimates.

Key downside risks to our earnings estimates include a slowdown in chip probing density/spec upgrades, market share shift of Technoprobe in the MEMS probe card market given high customer concentration (~50% revenue concentration in 2025), and any delayed adoption of glass core substrate in advanced packaging (due to any potential manufacturing issues during qualification).

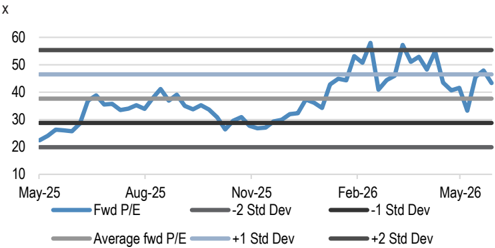

Valuation

Our Dec-27 PT of NT$4,000 is based on 25x 2028E P/E, below its one-year trading average of ~38x 12-month forward P/E, but largely in line with its peers' valuation on a 2028 basis, based on Bloomberg consensus estimates. We believe our target multiple for Innostar Service is undemanding, given our estimated earnings CAGR of ~200% in 2025-28, backed by the company's stronger probe card business growth with TAM expansion and new contribution from the glass core substrate TGV business for CoWoS applications.

Historical trading multiples

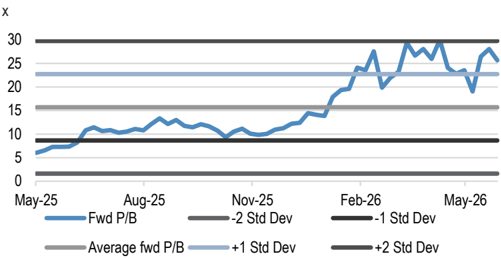

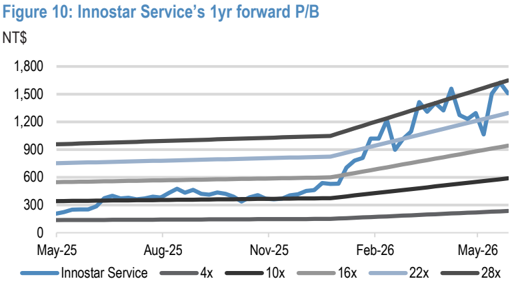

Table 1: Innostar Service's trading multiples since IPO in May 2025

| x | 12M trailing P/E | 12M fwd P/E | 12M trailing P/B | 12M fwd P/B |

|---|---|---|---|---|

| Standard deviation | 40.8 | 8.9 | 11.6 | 7 |

| Max | 175.9 | 58 | 47 | 30 |

| Minimum | 36.3 | 22.4 | 8.8 | 6 |

| Median | 72.3 | 35.7 | 15.5 | 12.1 |

| Average | 92.5 | 37.6 | 21.6 | 15.7 |

Source: Bloomberg Finance L.P., J.P. Morgan estimates.

Figure 7: Innostar Service's 1yr forward P/E vs mean

Source: Bloomberg Finance L.P., J.P. Morgan estimates.

Figure 9: Innostar Service's 1yr forward P/B vs mean

Source: Bloomberg Finance L.P., J.P. Morgan estimates.

Figure 8: Innostar Service's 1yr forward P/E

Source: Bloomberg Finance L.P., J.P. Morgan estimates.

Source: Bloomberg Finance L.P., J.P. Morgan estimates.

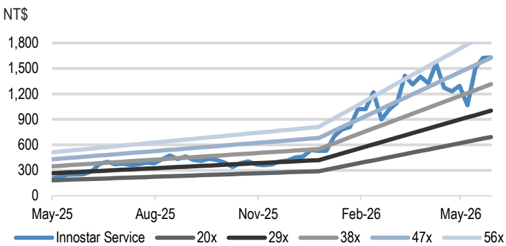

Table 2: Innostar Service's peer valuations

| Company | Ticker | Price | Mkt Cap | P/E (x) | P/E (x) | P/E (x) | P/BV (x) | P/BV (x) | P/BV (x) | EPS growth (%) | EPS growth (%) | EPS growth (%) | ROE (%) | ROE (%) | ROE (%) | Price |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (LC) | ($Mn) | FY26E | FY27E | FY28E | FY26E | FY27E | FY28E | FY26E | FY27E | FY28E | FY26E | FY27E | FY28E | 12M | ||

| Innostar Service | 7828 TT | 2,000 | 2,323 | 138.3 | 31.3 | 12.3 | 53.6 | 22.3 | 10.0 | 128.8 | 342.4 | 153.7 | 41.4 | 100.8 | 111.9 | 517% |

| Technoprobe | TPRO IM | 38 | 28,281 | 89.1 | 57.4 | 44.6 | 15.9 | 12.7 | 10.0 | 178.3 | 55.1 | 28.6 | 19.2 | 22.5 | 23.1 | 433% |

| FormFactor | FORM US | 150 | 11,658 | 60.7 | 46.9 | 51.7 | N/A | N/A | N/A | 89.5 | 29.5 | -9.4 | 15.4 | 18.7 | N/A | 359% |

| MPI | 6223 TT | 6,415 | 19,900 | 99.2 | 51.0 | 27.7 | 32.4 | 19.5 | 13.0 | 92.1 | 94.6 | 83.9 | 38.6 | 49.7 | 56.9 | 640% |

| Winway | 6515 TT | 9,450 | 10,782 | 101.1 | 51.9 | 30.0 | 41.4 | 24.3 | 15.8 | 103.8 | 94.7 | 73.0 | 43.8 | 53.1 | 62.8 | 704% |

| CHPT | 6510 TT | 3,610 | 3,748 | 51.1 | 29.1 | 20.6 | 10.8 | 8.2 | N/A | 125.4 | 75.9 | 41.4 | 21.9 | 31.8 | 56.0 | 328% |

| Median of chip probing (probe card) and final testing (SLT) vendors | Median of chip probing (probe card) and final testing (SLT) vendors | Median of chip probing (probe card) and final testing (SLT) vendors | Median of chip probing (probe card) and final testing (SLT) vendors | 94.2 | 48.9 | 28.9 | 32.4 | 19.5 | 11.5 | 114.6 | 85.3 | 57.2 | 30.2 | 40.8 | 56.9 | 475% |

| Ingentec | 4768 TT | 382 | 574 | 1475.0 | 37.6 | 23.7 | 11.1 | 3.3 | 1.9 | -33.3 | 3825.0 | 58.7 | 2.8 | 45.3 | 8.1 | 301% |

| LPKF Laser & Electronics | LPK GY | 26 | 730 | N/A | 92.2 | 34.7 | 14.8 | 10.9 | 8.0 | 56.8 | 225.5 | 165.6 | -8.2 | 10.3 | 24.0 | 214% |

| AGC (Asahi) | 5201 JP | 7,564 | 10,188 | 19.3 | 16.2 | 13.9 | 1.1 | 1.0 | 1.0 | 21.7 | 19.3 | 16.3 | 5.7 | 6.6 | 7.2 | 77% |

| Corning | GLW US | 195 | 167,439 | 61.1 | 46.8 | 34.1 | 12.9 | 11.9 | 9.8 | 26.5 | 30.6 | 37.4 | 21.2 | 25.5 | 30.5 | 287% |

| Median global glass core substrate/TGV supply chain names | Median global glass core substrate/TGV supply chain names | Median global glass core substrate/TGV supply chain names | Median global glass core substrate/TGV supply chain names | 61.1 | 42.2 | 28.9 | 12.0 | 7.1 | 4.9 | 24.1 | 128.0 | 48.1 | 4.2 | 17.9 | 16.0 | 250% |

Source: Bloomberg Finance L.P., J.P. Morgan estimates (for Innostar Service). Priced as of 18 June 2026.

Peer valuations

Innostar Service's stock has traded at 25-55x 12-month forward P/E since its IPO in May 2025 with the average at ~38x, slightly below its probe card (and TGV) peers' valuation of >40x 12M fwd P/E, as the company is regarded as an equipment name that generally trades lower vs semi material/component names, while it is still not well covered by the Street given its new presence in the market (IPO in May 2025 and OTClisted in April 2026).

We have assigned a 25x 2028E P/E target multiple, which is within the range of peers' valuation at 20-30x on a 2028E basis. We believe Innostar Service's stronger-than-peers earnings growth of ~130%/350%/150% YoY in 2026E/27E/28E (vs peers' average of 115%/85%/60% YoY, per Bloomberg consensus, see table below) should support its valuation, and may even deserve a premium or re-rating potentially in the future when this name is more known to the Street.

Driver 1: Copper Pillar Mass Transfer in TGV - key to Glass Core Substrate from 2H27

Glass core substrate adoption in advanced packaging could be faster than expected, Innostar Service the main beneficiary

We are more constructive on the glass core substrate adoption timeline, compared to the Street, as we believe a leading US networking fabless company is aggressively working with the TGV (Through-Glass Via) supply chain to develop and test the glass core substrate product for its future switch ASIC solution. Based on the current smooth qualification process within the supply chain (with substrate vendors qualifying/doing RDL on the TGV-completed glass core substrate now), we think the first official glass core substrate adoption could take place in 2H27, with next-gen switch ASIC entering mass production.

We believe Innostar Service could become one of the major beneficiaries of the switch ASIC's potential glass core substrate adoption, as the company will function as the key enabler of the TGV metallization process by applying its copper pillar mass transfer technology (into the vias). Given the high content value of TGV copper pillar (JPMe US $200-300 of content per glass core substrate/per chip) along with Innostar Service's dominant supply position, we forecast the company to see meaningful revenue contribution from this new TGV copper pillar mass transfer business from 2H27 and materially ramp in 2028 with 4x of new capacity expected to kick in, followed by the chip's mass production schedule.

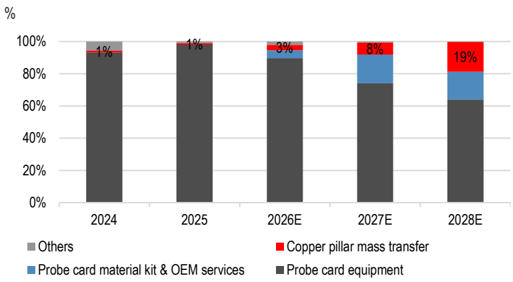

We model TGV copper pillar business to contribute ~NT$400mn of revenue in 2027 and increase 6x to ~NT$2.4bn in 2028, accounting for 8% and ~20% of revenue, driving Innostar Service's corporate revenue to grow by ~250% YoY in 2027 and another ~130% YoY in 2028. Of note, our revenue forecasts merely factor in 1 switch IC project from its first TGV customer.

Figure 11: Copper pillar mass transfer business revenue and YoY growth

Source: Company data, J.P. Morgan estimates.

Figure 12: Copper pillar revenue contribution to increase to 20% in 2028E

Source: J.P. Morgan estimates.

In addition, we believe some US GPU vendors also have some TGV projects working with Innostar Service, mainly for its networking/switch chips as well. If the first glass core substrate project for the switch ASIC can successfully go into mass production in 2H27 and 2028, we think the US tier-1 GPU company could likely become the 2 nd TGV copper pillar customer from 2029 or 2030, starting from its future-gen networking chip adoption of glass core substrates. We have not factored the potential second customer in Innostar Service's model, but we believe the company has already started looking for new manufacturing sites for the 4 th TGV copper pillar capacity expansion plan, in order to prepare for these potential opportunities with very strong expected demand in the next 3-5 years.

Why adopt Glass Core Substrate? To fundamentally address warpage and data transmission loss issues for larger-sized chips

Potential bottleneck to future advanced packaging: more severe warpage issues from CTE mismatch of materials

As the packaging size continues to get larger, the chip is more likely to undergo warpage and deformation issues under high temperature during the advanced packaging process (e.g., CoWoS). The core issue lies in the massive mismatch in the Coefficient of Thermal Expansion (CTE) between the materials of silicon interposer and organic substrates.

W hen a large-sized packaged chip is heated, the expansion of the bottom organic substrate will be much greater than that of the silicon interposer, so this intense stress mismatch could cause severe chip warpage (increasingly significant as the packaged size gets larger). This could be a fundamental physical limitation that currently prevents a yield breakthrough in large-sized advanced packaging.

Current solution: Glass fiber cloth as the mainstream, but still with a physical ceiling in the long term

To suppress warpage, the industry has started to adopt glass fiber cloth into the core layer of the substrate to enhance its mechanical strength. However, glass fiber cloth essentially serves only as a reinforcing skeleton for the organic resin. As long as resin material exists, the entire substrate will still expand when heated. Consequently, although the adoption of high-end glass fiber cloth in organic substrates could contribute to a reduction in CTE, the stress gap between them and the silicon interposer will still become harder to mitigate as the packaging size continues to get larger.

We believe glass fiber cloth could remain the mainstream solution for the strengthening of organic substrates for the next few years. However, from a longer-term perspective, there should still be a physical ceiling for its effectiveness to suppress warpage if chip packaging size is enlarged to some extent. Hence, we expect the industry should gradually trend to the adoption of glass core substrates, in order to 'fundamentally' deal with the warpage issues for the breakthrough to the next stage of large-sized advanced packaging.

Figure 10. lov giaoo bule suvotale vo cullelli Ul galle suvolate Il vorro structure

Traditional organic substrates tend to warp due to large differences in the coefficients of thermal expansion (CTE) among

J.P. Morgan their multilayer materials.

++4

Interposer

Conventional Substrate zero warpage.

++--

-++-

Interposer

TGV - ICP

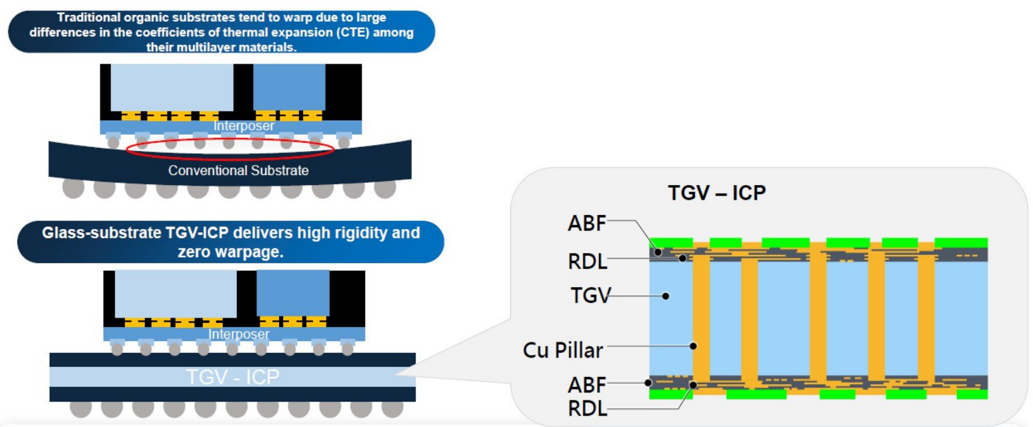

Glass core substrate the next big thing - the long-term solution to fundamentally deal with warpage and enables higher I/O density meanwhile

Glass core substrates could potentially become the long-term solution for advanced packaging, by offering superior mechanical, electrical, and optical properties. This could 'fundamentally' deal with the warpage issues derived from CTE mismatch, which would be increasingly indispensable when chip/substrate sizes get larger more rapidly with higher TDP (Thermal Design Power).

RDL

Mechanically, its Coefficient of Thermal Expansion (CTE) closely matches silicon , which minimizes thermal stress and eliminates the catastrophic warpage seen in organic substrates. This exceptional flatness enables ultra-fine line spacing and a significantly higher copper pillar density , allowing for a massive increase in I/O routing. Electrically, the low dielectric constant (Dk ) and ultra-low loss tangent (Df ) of glass drastically reduce signal attenuation and propagation delay at high frequencies. Furthermore, its rigid structure allows for high-density Through-Glass Vias (TGVs) to optimize power delivery, while its optical transparency could be an optimal solution that enables seamless integration for co-packaged optics (CPO) in the future. Consequently, glass bridges the gap between mechanical reliability and high-speed performance for next-generation AI and networking chips.

Figure 13: TGV glass core substrate vs current organic substrate in CoWoS structure

Source: Company presentation.

"gure 17. Ciaoo bure subouate lor supply chiam map

Glass material , Laser modification

J.P. Morgan

• Corning

Other leading supply chain

vendors

• LPKF

• AGC (Asahi)|

• Nippon Electric Glass

(NEG)

• Schott

• TW peers e.g. E&R

Engineering

Etching (TGV formation)

• RENA (wet etching equipment)

• TEL (dry etching equipment)

Metallization

• Innostar Service (copper pillar made by Finecs)

• Amkor (copper pillar bump flip chip)

• MKS/Atotech (plating chemicals)

RDL (ABF build-up)

venture with Toppan)

• Toppan SGP (future)

• Ibiden

• Semco

• DNP

• TW peers e.g. Unimicron,

Copper Pillar Mass Transfer vs Copper Plating for TGV: the key process to enable signaling in glass core substrate

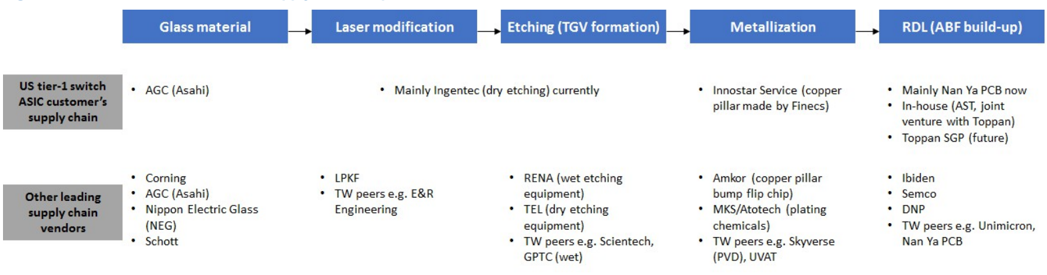

After securing glass from the glass vendors, it will need to go through the TGV (Through Glass Via) manufacturing process to enable the glass (dielectric) with power/ electricity and signal/data transmission capabilities.

TGV manufacturing process

Through-glass vias (TGVs) are the vertical pathways/connections for power and data/ signal transmission in glass (or glass core substrate here). To make TGVs, the process includes adopting laser technology to first chemically alter the molecular structure inside the glass (to create a laser-modified zone), and using etching to hollow out the materials of the laser-modified zones to form the 'vias' through the glass, then followed by the metallization step - either by coating the via sidewalls with copper and then electroplating the remaining space or by directly filling the vias with copper pillars.

After all the-above process, which are simplified with the few steps below, the TGVs become functional conductive pathways with metal (copper) through glass, and can be sent to substrate vendors for RDL (to do RDL and build up ABF layers on the top and bottom of the glass core substrate with TGVs).

- Laser modification: Uses ultra-fast lasers to induce physical-chemical changes inside the glass, defining the via positions

- Etching: Uses selective chemical etching solution (wet or dry) to remove the modified regions, forming high-aspect-ratio vias.

- Metallization: Fills the vias with copper pillars or creates a seed layer deposition, establishing vertical electrical connections.

- RDL: Integrates ABF build-up films and subsequent routing processes, completing substrate fabrication.

Figure 14: Glass core substrate TGV supply chain map

Source: Company data, J.P. Morgan.

Copper pillar mass transfer an enhanced method for TGV metallization vs the current mainstream copper plating, accelerating glass core substrate MP timing

Currently, the mainstream metallization process in glass core substrate TGV is by copper (electro)plating (as it is already a mainstream metallization technology adopted in TSV (Through Silicon Via) process for current packaging). However, we believe there are quite a few bottlenecks during the TGV copper plating process, which makes the copper pillar mass transfer technology a more effective (higher yield) method in TGV metallization, especially when the glass size continues to increase with the chip size.

Aspect ratio (with increasing glass size and higher thickness requirement)

- Copper plating: Currently, (electro)plating for TGVs can only achieve an aspect ratio of <10:1 (depth vs width), much lower than that for TSVs (Through Silicon Vias) given smaller pitch size/fine pitch. As the bump pitch continues to shrink, the aspect ratio of the photoresist template will eventually reach its physical limit. Furthermore, it becomes incredibly difficult for the plating solution to flow and react inside such microscopic cavities, leading to void defects.

- Copper pillar mass transfer: According to Innostart Service, its mass-transferred copper pillar for TGVs can already achieve an aspect ratio of 30:1 now, meeting the thickness requirement of the glass core substrate (1.7-1.8mm now) . As the glass size continues to increase along with the chip size, the thickness requirement will also be lifted, which makes this technology a more indispensable solution for future TGV metalization. The company's technology demonstrates superior control at the ultra-fine pitch level given supreme precision (based on the company's decadelong technology and expertise in needle assembly for probe cards).

Uniformity and coplanarity (Height/Width of copper pillar)

- Copper plating: Plating could suffer from current density distribution issues, especially within fine pitch. Across a larger-sized glass, plating speeds vary between the center and the edges, or between dense and isolated patterns. This leads to height variations among the plated copper pillars, which can cause non-wetting (open circuits) or bridging (short circuits) during fine-pitch assembly.

- Copper pillar mass transfer: Since the pillars are pre-fabricated on a specialized, perfectly flat carrier, their height could be completely uniform. When transferred to a glass core substrate, every single pillar is identical in height, drastically improving assembly yield for high-density bumping.

Process speed and throughput

- Copper plating: This is a time-consuming process where thickness scales with plating time. Especially for the TGVs with higher aspect ratios, the plating time increases significantly, followed by tedious photoresist stripping and seed-layer etching steps.

- Copper pillar mass transfer: The mass transfer technology is more like parallel processing. The transfer step is a "gang transfer" (all-at-once). For now, Innostar Service can mass-transfer >10k units of copper pillars onto one piece of glass core substrate, which significantly boosts backend manufacturing throughput.

What exactly does Innostar Service's copper pillar mass transfer technology do?

What Innostar Service does is precisely insert the pre-made copper pillars into the vias all at once, which could serve as a more efficient and accurate "pre-fabricated plugin" method, instead of relying on the traditional chemical electroplating process to grow copper.

The steps Innostar Service does/provides for glass core substrate TGV metallization:

- Step 1: Procure pre-made copper pillars. Innostar Service does not make the copper pillars itself, but procures them from the metal component manufacturing vendors. We believe the company procures the customized copper pillars from Finecs , a Japanese manufacturer (C-TECH as its Taiwan agent), with perfectly uniform dimensions, lengths, and conductivity.

- Step 2: Mass Transfer & Insert copper pillars. Leveraging Innostar Service's expertise in the needle assembly for MEMS probe card and ultra-high-precision automated equipment, the company can manage to mass transfer 30-50k units of the procured copper pillars and precisely insert them into the glass core substrate's TGV simultaneously.

- Step 3: Adhesive filling. When mass-transferring the copper pillars into TGVs, Innostar Service will apply a specialized adhesive (Innostar Service's patent) between the copper pillar and the glass wall. The adhesive serves a dual purpose: securely locking the copper pillar into place and filling all the space seamlessly to ensure zero voids (to ensure smooth power/data transmission with no signal/ transmission loss from voids), and acting as a "shock absorber" to soak up thermal stress when the chip runs hot, preventing the glass matrix from cracking.

After the above three steps, the glass core substrate with TGVs formations is done, and Innostar Service will send the whole glass core substrate to substrate vendors for RDL (to complete the entire substrate fabrication with ABF layer build-up).

What is Innostar Service's edge in copper pillar mass transfer? Expertise from probe card needle assembly creating its dominance and high entry barrier The Copper Pillar Mass Transfer technology that Innostar Service demonstrates for TGV is, at its core, the scaling and evolution of its mature "automated probe card needle assembly/pin insertion" expertise the company has spent over decades perfecting, now applied to advanced packaging glass substrates.

In terms of technical essence, these two are "the same core technology applied to two different fields." We can see how seamlessly they transferred this core competence through the below two main dimensions:

From "Needle Assembly" to "Copper Pillar Insertion": Leveraging the Expertise of Micron-Scale Alignment

-

Probe card needle assembly: MEMS probe cards require tens of thousands of needles/pins, with diameters of only a few dozen microns (μm), to be stuffed into a probe head just a few centimeters square. Innostar Service originally built its reputation by developing one of the world's fastest and most precise automated needle assembly machines using proprietary "vision recognition + ultra-high precision mechanical alignment."

-

TGV copper pillar mass transfer: The TGVs drilled/etched into glass core substrates have similarly tiny micron-scale diameters, and their quantities are also up to tens of thousands and even hundreds of thousands in the future. Innostar Service directly upgraded the alignment and gripping mechanisms of their needle assembly machines into mass transfer/alignment and insertion at once with extreme precision for TGV.

Seamless Migration of "Fixation Adhesives" (This directly ties back to the core adhesive patent mentioned above)

- Probe card needle assembly: After the needles/pins are inserted into the probe head, they are secured with a special adhesive/colloid.

- TGV copper pillar mass transfer: When copper pillars are stuffed into glass vias, Innostar Service similarly utilizes a very similar customized fixation adhesive to fill the voids between the glass walls and copper pillars, while keeping the tens of thousands of pillars behaving properly in formation without shifting during the transfer process.

Multiple US tier-1 chip customers' TGV projects, expected MP from 2H27 and more in 2028-29

1 st TGV project for switch ASIC, expected MP in 2H27 with meaningful content value and rev contribution

Based on our latest industry check, the leading US networking chip company could potentially lead the shift as an early adopter of glass core substrates, likely integrating them into its next-gen switch ASIC by 2H27 . This transition is primarily driven by the need to mitigate the warpage issues from larger-size substrates when the heat rises significantly during high-speed data transmission.

We believe the US switch ASIC vendor has laid out its own glass core substrate supply chain, and Innostar Service plays a critical role as the sole TGV metallization vendor by adopting its copper pillar mass transfer technology. Currently, the glass suppliers (such as AGC (Asahi) will ship the large-sized glass to the laser modification vendors and etching vendors (currently mainly Ingentec doing 'dry' etching , instead of adopting the mainstream wet-etching technology) to form the TGVs on the glass, and then ship to Innostar Service to do the TGV metallization process by mass-transferring the copper pillars (currently made from Finecs , a Japanese copper product manufacturer) into the TGVs. After that, the glass core substrate (with metalllized TGVs in glass) is completed, so Innostar Service will ship 'the whole glass core substrate' to ABF substrate vendors (such as Nan Ya PCB) to do the RDL part.

According to Innostar Service's pre-OTC listing investor conference in 1Q26, the company's copper pillar mass transfer technology/TGV product has already been qualified by chip customer, and its first TGV project is now sampling small volume of products to substrate vendors for next step RDL and ABF substrate fabrication (NTI phase). We believe the susbtrate vendors will complete their part and have results in the next few months (around August 2026), and then ship the RDL/ABF completed substrate product (with glass core in the middle) to the CoWoS partner for the final stage of packaging, expected another 3 months at packaging side, with results out by Nov or Dec 2026. Hence, we expect the entire sampling and qualification process will be

Figure 10. mostal delviceo for coppel pillal capacity expansion plall

Before 1Q26

2026E

J.P. Morgan

2027E

20-3026E

Substrate vendor

3Q-4Q26E

2028E

+

Ship to packaging

- Phase 2

40k/month

2H27E

2029E

Enter mass

completed by the end of 2026, and then finally enter the NPI phase. The expected mass production timing is in 2H27 (if all processes are on track).

Figure 15: Current glass core substrate qualification and expected production timeline of the 1 st switch ASIC TGV project

Source: Company data, J.P. Morgan estimates.

US tier-1 GPU companies' networking chips to potentially follow suit in 2029 or 2030

The company is also engaging with some US tier-1 GPU companies for potential glass core substrate adoption in their future networking chips. Innostar Service will also support the TGV metallization process with its leading copper pillar mass transfer technology.

We believe US GPU vendors will more likely use glass core substrates from late 2028 and gradually ramp in 2029 and 2030, serving as Innostar Service's potential second customer. The progress of GPU companies' projects is worth monitoring going forward, especially with more capacity kicking in expected in 2029 (if the 4 th phase of expansion goes smoothly).

Significant TGV capacity expansion to meet strong demand, driving rapid revenue growth from 2H27 and more in 2028-29

Given the strong TGV copper pillar mass transfer demand, Innostar Service is aggressively planning its TGV capacity expansion sites and schedule. According to its pre-listing conference presentation, the company acquired land in Taichung in Aug 2025 for the new copper pillar module and TGV production lines. The 1 st phase construction was completed in 1Q26, including TGV capacity expanding to 10k/month (pieces of glass core substrate) with 12 production lines.

Based on the TGV order forecast for the next 2-3 years from the first potential customer, Innostar Service is aggressively expanding its TGV copper pillar capacity to meet the remarkably strong demand. Recently, the company started its 2 nd phase construction (also in Taichung), which will increase its TGV copper pillar capacity by 3x by the end of 2027 and 2028. Meanwhile, it is also planning for the 3 rd and 4 th phases of expansion. The company is now targeting to have a total of 40k/month in 2027-28 (up from 10k/ month now) and 120k/month of TGV copper pillar capacity in 2028-29 from the 3rd/4th phase of expansion.

Figure 16: Innostar Service's TGV copper pillar capacity expansion plan

Source: Company data.

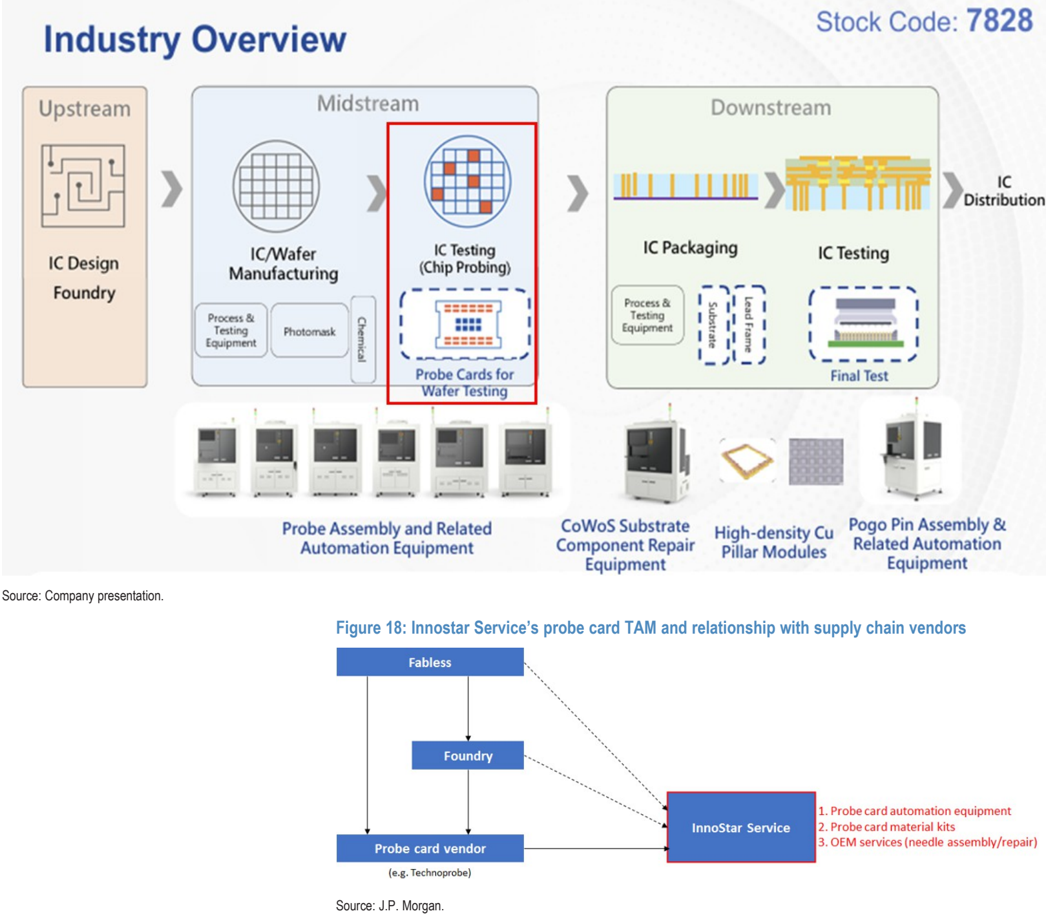

Figure 1o. mostal delvice prove card taw and telatonshp wit supply cham venuors

Fabless

Industry Overview

J.P. Morgan

Probe card vendor

(e.g. Technoprobe)

IC Design

Foundry

IC/Wafer

Manufacturing

Process &

Testing

Equipment

Photomask

InnoStar Service

-

Probe card automation equipment

-

Probe card material kits

-

OEM services (needle assembly/repair)

Distribution

Driver 2: Probe card equipment & material kit + OEM services - TAM expansion by standing at giant's (Technoprobe) shoulder

Where Innostar Service sits in the probe card supply chain

Figure 17: Innostar Service's fundamental business mainly lies in the midstream chip probing phase (probe card equipment + material kits)

Stock Code: 7828

Downstream

98%

Existing business accelerating growth: Probe card equipment to grow 2x in 2026 and another 3x in 2027

Continued upward revisions of dual-arm needle assembly machine orders from Technoprobe, with multi-times shipment increases in 2026-28

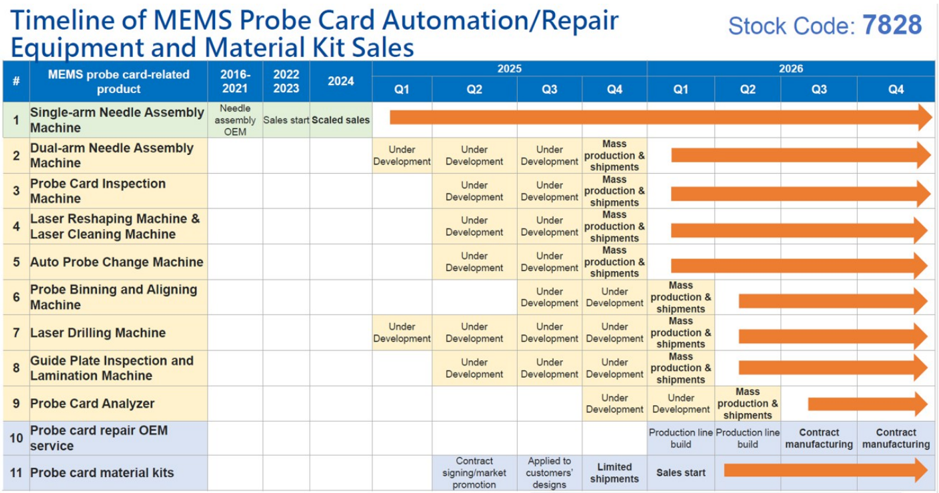

In 2025, Innostar Service reached an agreement with Technoprobe (TPRO IM, also known as TP) that the company will solely supply its MEMS probe card needle assembly machine to TP in the future. That said, Innostar Service's needle assembly machine business will only have 1 customer, Technoprobe, in the future, in order to deepen their technology and strategic partnership. Before the partnership with Technoprobe in 2025, Innostar Service had already shipped quite a few single-arm needle assembly machines to the major probe card vendors, such as MPI (6223.TW, NC), in the past 2-3 years (during late 2022 to 2025).

Innostar Service successfully developed the 'dual-arm' MEMS probe card needle assembly machine in 2025, which was an upgraded solution from its previous 'singlearm' needle assembly machine. We believe this new solution was tailored for TP's rising demand for high-end probe card/head (e.g. up to 150k needles/pins per AI chip probe card), as the dual-arm machine can assemble ~10k needles/pins a day, doubling the efficiency of the previous single-arm machine of ~5k needles per day (vs manual assembly of only ~600 needles per day).

In 4Q25, Innostar Service's dual-arm needle assembly machine officially entered mass production, with 4 units of machine shipment to TP. Coupled with the continued singlearm needle assembly machine shipment, Innostar Service's 2025 probe card equipment revenue reached NT$700mn (almost doubling from 2024). Looking forward to 20262028, we believe there have been meaningful upward revisions of Technoprobe's dualarm machine order forecast recently, given TP's aggressive probe card capacity expansion plan over the next few years. Hence, we are now modeling 2x probe card equipment revenue in 2026, and another 3x and 2x in 2027 and 2028 to meet TP's remarkably strong demand for high-end AI chip probe cards/heads (pin count per probe card also continues to increase).

Figure 19: Probe card equipment revenue to grow 2x in 2026E, 3x in 2027E and another 2x in 2028E

robe Card Equipment Revenue

86%

4,150

Source: Company data, J.P. Morgan estimates.

80%

Figure 20: Dual-arm probe card needle assembly machine shipment units

Source: Company data, J.P. Morgan estimates.

J.P. Morgan

JEM

6%

MPI Corporation

6%

Micronics Japan

12%

FormFactor

24%

Technoprobe

21%

will a voro marnet orlare)

Other

15%

JEM

5%

Nidec SV Probe

6%

MPI Corporation

10%

Riding on Technoprobe's aggressive probe card capacity expansion, underpinned by TP's new AI ASIC order win + leading share in foundry's advanced node

Technoprobe announced in its Nov 2025 conference call that it plans to double its probe card capacity by the end of 1Q27 with an increase in its capex investment. Given the recent surge in demand, the company's capacity expansion schedule has been accelerated, according to its mid-May 2026 earnings call, which implies the 2x capacity is expected to kick in by the end of this year. We believe this is in line with Innostar Service's recent upward revision of dual-arm needle assembly machine orders.

Based on our supply chain checks, Technoprobe has secured a new AI ASIC probe card project from a US tier-1 CSP customer. Given the meaningful volume along with the high pin-count of this CSP ASIC, Technoprobe has to expand and accelerate its related equipment investment significantly.

In addition, Technoprobe has a leading market share in supplying high-spec/highdensity probe cards to advanced nodes from foundry's turnkey business model, so the stronger capacity expansion of advanced nodes (as per TSMC's recent earnings call) in the next few years should drive stronger demand for both Technoprobe and Innostar Service's probe card equipment directly, in our view.

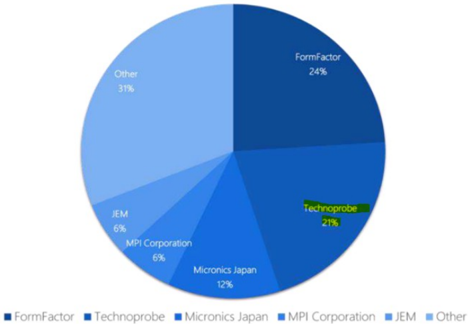

In our view, Technoprobe's new AI ASIC probe card order win and stronger advanced node demand will continue to drive upward revisions for Innostar Service's dual-arm needle assembly machine shipment in the next 2-3 years. Coupled with Technoprobe's solid market share in the MEMS probe card market (it is the second-largest supplier, as shown in the figure below), we believe Innostar Service will be the direct beneficiary and keep riding on the probe card TAM increase trend.

Please note that JPM does not cover Technoprobe (TPRO IM) and the above views are based on the company's earnings call and Bloomberg consensus estimates.

Figure 21: Overall probe card vendor market share allocation (TP is the second-largest)

Source: Techinsight (2024/12,2025E), company OTC prospectus.

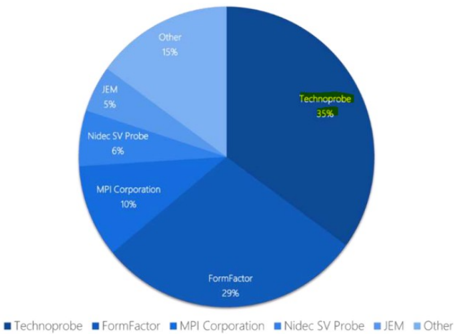

Figure 22: Global non-memory probe card vendor market share allocation (TP leads with a 35% market share)

Source: Techinsight (2024/12,2025E), company OTC prospectus.

Technoprobe

35%

mldtstlar nilo aulu rove varu Ini capalloiult te

vew ool Vluso

Timeline of MEMS Probe Card Automation/Repair

J.P. Morgan

Equipment and Material Kit Sales

2

3

Dual-arm Needle Assembly

Machine

Probe Card Inspection

Machine

4

Laser Reshaping Machine &

Laser Cleaning Machine

5 Auto Probe Change Machine

6

Probe Binning and Aligning

Machine

7 Laser Drilling Machine

8

Guide Plate Inspection and

Lamination Machine

9 Probe Card Analyzer

10

Probe card repair OEM

service

11 Probe card material kits

20722

2023

2024

2025

Under

Development

Under

Development

Q4

Mass production &

shipments

Mass

Development Development production &

Under

Under shipments

Mass

New business to drive TAM expansion with recurring rev: new material kit and OEM services as Technoprobe's Taiwan agent

Mass

Inflection point from Technoprobe's strategic investment: TAM expansion by providing material kit and needle assembly/repair OEM services to TP's customers

Technoprobe's strategic investment in Innostar Service in 2025 (with 8.4% of stake) was to better fulfill customers' demand in Taiwan and enhance the effectiveness of problem-shooting (e.g. probe card pin/needle inspection/repair), by leveraging Innostar Service's geographical advantages (cluster effect) and local connections with upstream and downstream probe card supply chain vendors.

signing/market customers'

Limited shipments

Sales start

Thanks to the partnership with Technoprobe, Innostar Service has become TP's agent in Taiwan to supply the probe card material kits (incl. TP's pins/needles) for its customers in Taiwan. For example, Keystone Microtech (also known as KSMT, 6683.TW, NC), a Taiwan-based load board and probe card vendor, procures the high-end probe heads/pins from Technoprobe and integrates them with its own load board/burn-in board. Furthermore, the other business model is with the foundries. Not only can Innostar Service provide probe equipment to the foundries, but also the material kits to the outsourced probe card customers to Technoprobe.

In addition to the material kit business, Innostar Service has another TAM expansion opportunity into the probe card OEMs services, including the needle assembly and repair, for Technoprobe's Taiwan customers as well. Leveraging Innostar Service's selfdeveloped probe card needle assembly and repair equipment, the company can serve as a total solution provider, from material kits (needles/pins) to needle assembly and even to the future repair services. This could grow into a sizeable market for Innostar Service, as probe cards become highly sophisticated for AI chips, more and more customers will require these needle assembly and repair OEM services for better yield.

Figure 23: Probe card TAM expansion to material kits and OEM services

Source: ompany presentation.

OEM

Under

Development|

Q1

Stock Code: 7828

2026

Q2

Q3

Q4

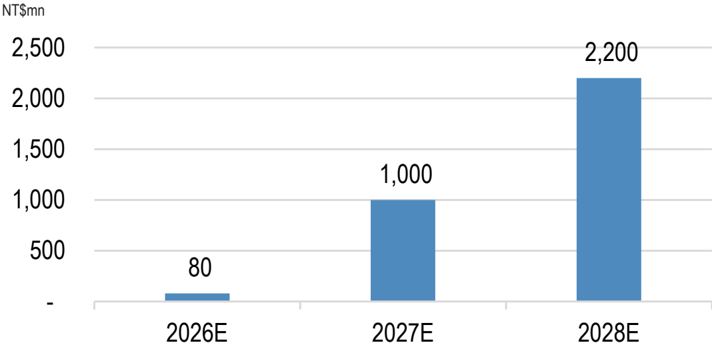

Starting from 1H26, Innostar Service will start shipping small volume of probe card material kits (pins/needles) to some TP's Taiwan customers, which would contribute ~NT$80mn revenue in 2026 (5% rev mix, based on JPMe). Looking into 2027, we believe the material kit (pins/needles) shipment volume will start ramping to ~20k pins/ needles level of shipment for the whole year (equivelant to ~500 units of probe card). Coupled with the start of the OEM production lines (both repair and needle assembly), we model ~NT$1bn revenue contribution from Innostar Service's new probe card business (material kit + OEM services), which suggests 18% rev mix in 2027.

Figure 24: Probe card material kit + OEM services revenue

Source: J.P. Morgan estimates.

Company Overview

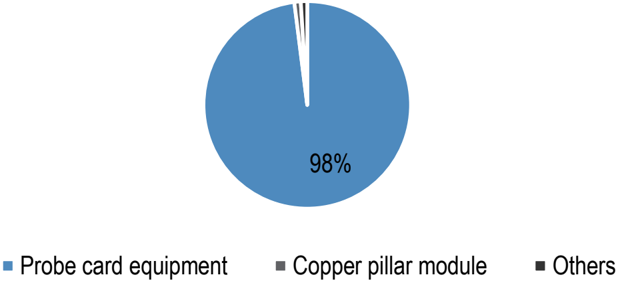

Founded in 2004, Innostar Service is a key player in the design and development of MEMS probe card automation equipment, mainly focusing on needle assembly, for the semiconductor and optoelectronics industries. In 2025, MEMS probe card automation equipment accounted for >90% of the company's revenue, primarily from the single-arm probe card assembly machine. To address the rising complexity of advanced chip probing/testing, Innostar Service successfully developed a dual-arm probe assembly machine (and full-line automation solutions), which has entered mass production since 4Q25, and will become a major driver for the company in the next few years with multiple times of shipment ramp.

Figure 25: Innostar Service 2025 revenue mix (>90% from probe card automation equipment) %

Source: Company data.

Innostar Service's largest customer is Technoprobe, which owns an approximately 8% equity stake. Technoprobe's strategic investment in Innostar Service was to expand its exposure and presence in Asian markets, especially Taiwan, which gives Innostar Service new business opportunities by selling probe card material kits (mainly pins/ needles) and providing needle assembly/repair OEM services for some Technoprobe's Taiwan customers (e.g. KSMT), which will become the 2nd revenue stream and growth driver for the company starting from 2026.

In addition to probe card businesses, InnoStar Service has expanded its business exposure to the advanced packaging (e.g. CoWoS) market through its 'copper pillar mass transfer' technology, leveraging the company's expertise in the high-precision probe card needle assembly. The copper pillar mass transfer technology will be applied in the TGV (Through Glass Via) metallization process for glass core substrates (not interposer), which should be adopted in larger-sized AI or networking chips starting from 2H27, in our view. This could become the third growth driver for the company starting in late 2027 and more meaningfully in 2028.

Overall capacity and future expansion plans

Table 3: Innostar Service's capacity and expansion plan of all product lines

| Existing | New (based on capacity expansion plan) | New (based on capacity expansion plan) | New (based on capacity expansion plan) | New (based on capacity expansion plan) | |

|---|---|---|---|---|---|

| Hsinchu Plant | Taichung Plant 1 (Dajia) | Taichung Plant 2 (near Dajia) | 3rd new plant | 4th new plant | |

| Complete timing | Before 2026 | 1Q26 | expected in late 2026 or beg 2027 | expected in 2H26-1H27 | expected in 2H27-2028 |

| Probe card equipment | V | V (1.5x vs current) (1F) | V | ||

| Probe card OEM services (needle assembly, repair, etc) | V | ||||

| Copper pillar module | V (800+k/month) (2F) | ? | V (4x? vs TC1) | ||

| TGV-ICP (copper pillar mass transfer) | V (10k/month) (2F) | V (30k/month) (2F) | ? | V (total ~120k/month) |

Source: Company data, J.P. Morgan.

Table 4: Management profile overview

| Title | Name | Selected Education and Past Positions |

|---|---|---|

| Chairman & President | Chih-MengWu | Master's Degree in Mechanical Engineering, National Central University (Taiwan) Director of R&D Department, Coretronic Corporation |

| VP of Sales Department | Chun-Chung Lin | Master's Degree in Public Affairs Management, National Sun Yat-sen University (Taiwan) GMOffice Executive Assistant, Silicon Touch Technology Inc. |

| VP of R&D | I-Jen Chang Chien | Master's Degree in Information Technology, The National Australian University (Taiwan) Project Manager of Software Development Department, Sunnet Technology |

Source: Company data.

Management profiles

Shareholder structure and QFII holding ratio

Table 5: Innostar Service's top 10 shareholders

| Shareholder list | % |

|---|---|

| Technoprobe SpA | 8.4% |

| YQ TECHNOLOGY COMPANY LIMITED | 8.4% |

| SHARP TEST TECHNOLOGY INC | 8.4% |

| MANLI INDUSTRIAL CO LTD | 6.7% |

| Powerchip Technology Corp | 6.6% |

| SBI PSMC JV FUND LP | 4.5% |

| FU CHI INVEST CO LTD | 3.5% |

| RIVER CONFLUENCE CO LTD | 2.8% |

| ART CONTROL SYSTEMS INC | 2.7% |

| WuChih-Meng | 2.6% |

| Top 10 total | 54.6% |

Source: Bloomberg Finance L.P., as of June 2026.

Figure 26: Innostar Service's QFII holding ratio post OTC-listed

Source: TEJ.

Investment risks

Slowdown in chip probing density/spec upgrades

Benefitting from the continued increasing chip probing density (higher pin count per probe card, such as for AI chips), the importance and penetration of probe card automation equipment, especially needle assembly machines, has risen rapidly in the past few years. There are even spec upgrade demands for probe card equipment (e.g. upgrading from single-arm needle assembly machine to dual-arm) in order to enhance the high-end probe card manufacturing efficiency and yield, which boosts the ASP of probe card equipment significantly. However, if the chip probing upgrade trend starts to slow down, probe card automation equipment vendors, such as Innostar Sevice that currently has >90% revenue from this business, will be negatively impacted in terms of earnings growth magnitude.

Customer concentration in probe card automation equipment business

In 2025, Technoprobe accounted for ~50% of Innostar Service's revenue and ~60% of core earnings, mainly from the single-arm probe card needle assembly machine. Looking into the next 2-3 years, with the remarkably strong demand for the upgraded dual-arm needle assembly machine customized for Technoprobe, we believe the customer concentration risk for Innostar Service will continue to rise.

Despite the rising customer concentration issue for Innostar Service, we don't think the company will lose share in Technoprobe, as Innostar Service holds a dominant position in the MEMS probe card needle assembly market with decades of technology expertise and customer experiences (e.g. provided needle assembly OEM services to foundry customers for several years previously). We believe the risk will lie in the market share shift of Technoprobe itself in the MEMS probe card market (currently the second-largest vendor with ~20% market share). Innostar Service's demand will be directly impacted by Technoprobe's customer/project wins and capacity expansion plans.

Delayed adoption of glass core substrates in advanced packaging

Innostar Service's new TGV copper pillar mass transfer business applied to glass core substrates serves as a meaningful earnings driver from late 2027/2028 and a breakthrough for the company, given the successful entry into the advanced packaging market. Of note, we currently model 8% and 20% revenue contribution from the TGV copper pillar business for one customer's switch ASIC in 2027 and 2028, respectively. Thus, any delay in glass core substrate adoption will provide downside to our 2027 and 2028 estimates.

Figure 27: Income statement

| 2024 | 2024 | 2026E | 2026E | 2026E | 2026E | 2027E | 2027E | (NT$ in Mn, year-end December) |

|---|---|---|---|---|---|---|---|---|

Source: Company data, J.P. Morgan estimates.

Investment Thesis, Valuation and Risks

Innostar Service (Overweight; Price Target: NT$4,000.00)

Investment Thesis

We rate Innostar Service OW, as we anticipate further stock outperformance to be driven by the next wave of earnings upgrade cycle in the next 2-3 years, with three solid growth drivers ahead: 1) probe card needle assembly machine order shipment to increase multiple times in 2026-28, thanks to the largest customer's surging demand, 2) TAM expansion by providing probe card material kits (mainly pins/needles) and needle assembly/repair OEM services, and 3) new TGV (Through Glass Via) copper pillar mass transfer business for the advanced packaging process of future-gen networking and AI chips (applying in CoWoS substrate for an ongoing networking project).

Valuation

Our Dec-27 PT of NT$4000 is based on 25x 2028E P/E, below its historical 12M fwd P/E of ~38x since IPO in May 2025, but largely in line with probe card and glass core/TGV peers' 2028E-based valuation of 20-30x.

Risks to Rating and Price Target

Key downside risks include any slowdown in chip probing density/spec upgrades; a market share shift in the MEMS probe card market, given high customer concentration (~50% revenue concentration in 2025 from a key customer), and any delayed adoption of glass core substrate in advanced packaging (any potential manufacturing issues during qualification).

Innostar Service: Summary of Financials

| Income Statement | FY24A | FY25A | FY26E | FY27E | FY28E | Cash Flow Statement | FY24A | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 406 | 716 | 1,620 | 5,604 | 12,849 | Cash flow from operating activities | 321 | (86) | 235 | 3,289 | 6,550 |

| COGS | (80) | (170) | (354) | (1,426) | (3,297) | o/w Depreciation & amortization | 38 | 41 | 75 | 264 | 478 |

| Gross profit | 326 | 546 | 1,266 | 4,178 | 9,553 | o/w Changes in working capital | 136 | (353) | (367) | 688 | 134 |

| SG&A | (67) | (113) | (257) | (463) | (730) | ||||||

| Adj. EBITDA | 188 | 319 | 758 | 3,397 | 8,381 | Cash flow from investing activities | (195) | (355) | (905) | (1,071) | (1,399) |

| D&A | (38) | (41) | (75) | (264) | (478) | o/w Capital expenditure | (165) | (314) | (904) | (1,073) | (1,399) |

| Adj. EBIT | 151 | 278 | 683 | 3,133 | 7,903 | as % of sales | 40.7% | 43.9% | 55.8% | 19.1% | 10.9% |

| Net Interest | 7 | 13 | 5 | (4) | 37 | ||||||

| Adj. PBT | 167 | 277 | 694 | 3,129 | 7,940 | Cash flow from financing activities | 490 | 533 | 47 | (740) | (1,777) |

| Tax | (17) | (49) | (164) | (782) | (1,985) | o/w Dividends paid | 0 | (54) | (183) | (427) | (1,891) |

| Minority Interest | - | - | - | - | - | o/w Shares issued/(repurchased) | 0 | 0 | 0 | 0 | 0 |

| Adj. Net Income | 150 | 228 | 531 | 2,347 | 5,955 | o/w Net debt issued/(repaid) | 0 | 182 | 349 | (318) | 80 |

| Reported EPS | 5.28 | 6.32 | 14.46 | 63.97 | 162.32 | Net change in cash | 616 | 92 | (623) | 1,477 | 3,374 |

| Adj. EPS | 5.28 | 6.32 | 14.46 | 63.97 | 162.32 | ||||||

| DPS | 0.00 | 1.56 | 5.00 | 11.65 | 51.54 | Adj. Free cash flow to firm y/y Growth | 156 - | (400) (356.7%) | (670) 67.3% | 2,216 (430.9%) | 5,151 132.5% |

| Payout ratio | 0.0% | 24.7% | 34.6% | 18.2% | 31.8% | ||||||

| Shares outstanding | 28 | 36 | 37 | 37 | 37 | ||||||

| Balance Sheet | FY24A | FY25A | FY26E | FY27E | FY28E | Ratio Analysis | FY24A | FY25A | FY26E | FY27E | FY28E |

| Cash and cash equivalents | 616 | 708 | 85 | 1,562 | 4,937 | Gross margin | 80.3% | 76.3% | 78.2% | 74.5% | 74.3% |

| Accounts receivable | 42 | 321 | 824 | 3,497 | 5,275 | EBITDA margin | 46.4% | 44.6% | 46.8% | 60.6% | 65.2% |

| Inventories | 68 | 211 | 808 | 1,554 | 2,298 | EBIT margin | 37.1% | 38.9% | 42.1% | 55.9% | 61.5% |

| Other current assets | 2 | 27 | 105 | 442 | 669 | Net profit margin | 36.9% | 31.8% | 32.7% | 41.9% | 46.3% |

| Current assets | 728 | 1,267 | 1,823 | 7,054 | 13,179 | ||||||

| PP&E | 130 | 405 | 1,238 | 2,057 | 2,995 | ROE | 47.8% | 25.0% | 41.4% | 100.8% | 111.9% |

| LT investments | 0 | 0 | 0 | 0 | 0 | ROA | 33.7% | 17.3% | 21.8% | 38.1% | 46.8% |

| Other non current assets | 30 | 71 | 71 | 70 | 69 | ROCE | 43.1% | 22.9% | 31.9% | 87.0% | 106.4% |

| Total assets | 889 | 1,743 | 3,132 | 9,181 | 16,243 | SG&A/Sales | 16.4% | 15.8% | 15.9% | 8.3% | 5.7% |

| Short term borrowings | 0 | 11 | 11 | 11 | 11 | Net debt/EBITDA | NM | NM | 0.6 | NM | NM |

| Payables | 43 | 104 | 426 | 2,184 | 3,249 | ||||||

| Other short term liabilities | 206 | 238 | 728 | 3,412 | 5,232 | Sales/Assets (x) | 0.9 | 0.5 | 0.7 | 0.9 | 1.0 |

| Current liabilities | 248 | 353 | 1,165 | 5,607 | 8,491 | Assets/Equity (x) | 1.4 | 1.4 | 1.9 | 2.6 | 2.4 |

| Long-term debt | 0 | 171 | 521 | 202 | 283 | Interest cover (x) | NM | NM | NM | 795.9 | NM |

| Other long term liabilities | 13 | 27 | 78 | 84 | 117 | Operating leverage | - | 111.1% | 115.2% | 145.9% | 117.7% |

| Total liabilities | 261 | 551 | 1,764 | 5,893 | 8,891 | Tax rate | 10.3% | 17.8% | 23.6% | 25.0% | 25.0% |

| Shareholders' equity | 627 | 1,192 | 1,368 | 3,288 | Revenue y/y Growth | - | 76.4% | 126.2% | 245.9% | 129.3% | |

| 7,352 | - | 69.8% | 137.2% | 146.7% | |||||||

| Minority interests | - | - | - | - | - | EBITDA y/y Growth | - | 19.8% | 348.3% | ||

| Total liabilities & equity | 889 | 1,743 | 3,132 | 9,181 | 16,243 | EPS y/y Growth | FY25A | 128.8% FY26E | 342.4% FY27E | 153.7% FY28E | |

| BVPS | 18.01 | 32.49 | 37.30 | 89.62 | 200.40 | Valuation | FY24A | ||||

| y/y Growth | - | 80.4% | 14.8% | 140.3% | 123.6% | P/E (x) | 386.7 | 322.7 | 141.1 | 31.9 | 12.6 |

| (616) | (526) | 446 | P/BV (x) | 113.2 | 62.8 | 54.7 | 22.8 | 10.2 8.2 | |||

| Net debt/(cash) | (1,349) | (4,643) | EV/EBITDA (x) | 386.6 | 228.0 | 97.4 | 21.2 | ||||

| Dividend Yield | 0.0% | 0.1% | 0.2% | 0.6% | 2.5% |

Source: Company reports and J.P. Morgan estimates.

Note: NT$ in millions (except per-share data).Fiscal year ends Dec. o/w - out of which

request.

Innostar Service (7828. TWO, 7828 TT) Price Chart

J.P. Morgan

2250

1500

Price(NTS) 1250

1000

750

Analyst Certification: The Research Analyst(s) denoted by an 'AC' on the cover of this report certifies (or, where multiple Research Analysts are primarily responsible for this report, the Research Analyst denoted by an 'AC' on the cover or within the document individually certifies, with respect to each security or issuer that the Research Analyst covers in this research) that: (1) all of the views expressed in this report accurately reflect the Research Analyst's personal views about any and all of the subject securities or issuers; and (2) no part of any of the Research Analyst's compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the Research Analyst(s) in this report. For all Korea-based Research Analysts listed on the front cover, if applicable, they also certify, as per KOFIA requirements, that the Research Analyst's analysis was made in good faith and that the views reflect the Research Analyst's own opinion, without undue influence or intervention.

All authors named within this report are Research Analysts who produce independent research unless otherwise specified. In Europe, Sector Specialists (Sales and Trading) may be shown on this report as contacts but are not authors of the report or part of the Research Department.

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

JPM_Innostar_Service_The_2026-06-22_5259886_002.png |

306KB | 真資料圖 | 表格式時程圖,標題「INNOS'MEMS Probe Card Solutions」,列出 Automated Probe Card Equipment、Material Kits & Contract Service、Cu Pillar Products 三大類產品項目及對應客戶(TP Group、TP Alliance、Wearable device manufacturer 等),右側以箭頭標示2026年Q1-Q4時程 |