PDF 原檔:報告_GS_ODM品牌廠_20260703_original.pdf

圖片清單(已驗證 2026-07-06)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

2026-07-03 260703_gs_ODM-brands_001.png |

12KB | 裝飾·logo·banner | <40KB,未讀 |

2026-07-03 260703_gs_ODM-brands_002.png |

12KB | 裝飾·logo·banner | <40KB,未讀 |

2026-07-03 260703_gs_ODM-brands_003.png |

77KB | 真資料圖 | Exhibit 6 鴻海月營收(NT$m),Jan-25–Aug-26E,含 YoY% 折線;2Q26E NT$2.35 兆、3Q26E NT$2.96 兆 |

2026-07-03 260703_gs_ODM-brands_004.png |

43KB | 真資料圖 | 廣達月營收(NT$m),Jan-25–Aug-26E,含 YoY% 折線;Jun-26E +98% YoY |

2026-07-03 260703_gs_ODM-brands_005.png |

39KB | 真資料圖 | 奇鋐(AVC)月營收(NT$m),Jan-25–Aug-26E,含 YoY% 折線;Jun-26E +75% YoY |

2026-07-03 260703_gs_ODM-brands_006.png |

46KB | 真資料圖 | 緯穎月營收(NT$m),Jan-25–Aug-26E,含 YoY% 折線;2Q26E NT$257,843m(+17% YoY)、3Q26E +23% QoQ |

2026-07-03 260703_gs_ODM-brands_007.png |

41KB | 真資料圖 | 華碩月營收(NT$m),Jan-25–Aug-26E,含 YoY% 折線;Jun-26E +24% YoY |

2026-07-03 260703_gs_ODM-brands_008.png |

52KB | 真資料圖 | 仁寶月營收(NT$m),Jan-25–Aug-26E,含 YoY% 折線;Jun-26E +23% YoY |

分類只有三類:

真資料圖/裝飾·logo·banner/文字卡。

原始內容

For the exclusive use of KEVINLU@LENOVO.COM

Taiwan ODM/Brands: 3-month preview: June revenue fl at MoM on avg but YoY remains strong; AI servers/smartphone new models key drivers

We preview 3-month revenues for the seven companies under our coverage in the AI server/PC supply chain and update our estimates for Quanta. Across the supply chain, we are positive on: (1) Apple's supply chain on the back of a ramp-up of new models with form factor changes (i.e., foldable phones in 2026, and the iPhone 20 in 2027) to support end demand; (2) AI server components riding on speci fi cation upgrades; and (3) ASIC AI servers' rising penetration rate.

Buy: Hon Hai, Wiwynn, AVC; Neutral: Quanta, Inventec, Compal, ASUS

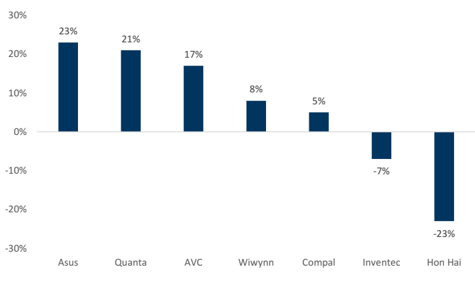

On a MoM basis, we expect the average revenue growth of the seven companies to come in at +6%/-5%/+0% in Jun/Jul/Aug 2026 (Exhibit 1). We expect fl at MoM growth in coming months, re fl ecting AI server ODMs undergoing model transition and PC consumption pull-in in 1H26 under high memory costs, which would weigh on PC supply chain shipment growth.

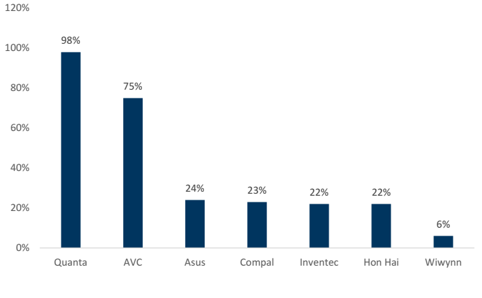

On a YoY basis, we expect the average revenue growth of the seven companies to come in at +39%/+37%/+29% in Jun/Jul/Aug 2026 (Exhibit 2), driven by the continuous ramp-up of AI servers, along with a PC product mix upgrade, new smartphone models, and high memory costs driving up the selling price.

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Verena Jeng

+852-2978-1681 | verena.jeng@gs.com Goldman Sachs (Asia) L.L.C.

Ting Song

+852-2978-6466 | ting.song@gs.com Goldman Sachs (Asia) L.L.C.

Yifan Hu +852-2978-0996 | yifan.hu@gs.com

Goldman Sachs (Asia) L.L.C.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 1: Jun 2026E revenue MoM

Exhibit 2: Jun 2026E revenue YoY

Source: Goldman Sachs Global Investment Research

Source: Goldman Sachs Global Investment Research

Mar to Aug 2026 revenue trends for Taiwan server / PC names

Exhibit 3: Taiwan PC/server names monthly revenue summary

| Rev YoY | Rev YoY | Rev YoY | Rev YoY | Rev YoY | Rev YoY | Rev MoM | Rev MoM | Rev MoM | Rev MoM | Rev MoM | Rev MoM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mar-26 | Apr-26 | May-26 | Jun-26(E) | Jul-26(E) | Aug-26(E) | Mar-26 | Apr-26 | May-26 | Jun-26(E) | Jul-26(E) | Aug-26(E) | |

| Wiwynn | 14% | 30% | 18% | 6% | 5% | 6% | 4% | -16% | 2% | 8% | -3% | 14% |

| Quanta | 88% | 121% | 94% | 98% | 90% | 68% | 68% | -6% | -8% | 21% | -20% | -15% |

| Inventec | 47% | 37% | 35% | 22% | 26% | 2% | 72% | -3% | -2% | -7% | -11% | -9% |

| Asus | 34% | 46% | 9% | 24% | 32% | 4% | 58% | -5% | -16% | 23% | -15% | -10% |

| Compal | 17% | 16% | 22% | 23% | 25% | 24% | 69% | -19% | -2% | 5% | -1% | -1% |

| Hon Hai | 46% | 30% | 40% | 22% | 21% | 38% | 35% | 4% | 3% | -23% | 13% | 12% |

| AVC | 112% | 72% | 61% | 75% | 60% | 59% | 29% | -13% | 2% | 17% | 2% | 6% |

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 4: Taiwan ODM notebook monthly shipments

| May-25 | June-25 | July-25 | Aug-25 | Sep-25 | Oct-25 | Nov-25 | Dec-25 | Jan-26 | Feb-26 | Mar-26 | Apr-26 | May-26 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Notebook shipments (m units) | 10.6 | 13.0 | 10.8 | 11.2 | 12.0 | 10.1 | 10.4 | 11.8 | 8.4 | 7.0 | 13.8 | 9.1 | 9.3 |

| Quanta | 3.8 | 5.0 | 4.0 | 4.1 | 4.6 | 3.5 | 3.5 | 3.9 | 2.7 | 2.0 | 5.3 | 3.5 | 3.5 |

| Compal | 2.4 | 2.5 | 2.3 | 2.3 | 2.5 | 2.1 | 2.3 | 2.4 | 1.6 | 1.5 | 2.8 | 1.8 | 2.0 |

| Inventec | 1.8 | 2.1 | 1.7 | 1.8 | 1.9 | 1.6 | 1.7 | 2.0 | 1.7 | 1.5 | 2.2 | 1.5 | 1.5 |

| Wistron | 1.8 | 2.4 | 2.0 | 2.2 | 2.2 | 2.1 | 2.2 | 2.6 | 1.7 | 1.6 | 2.8 | 1.8 | 1.7 |

| Pegatron | 0.8 | 1.0 | 0.8 | 0.8 | 0.8 | 0.8 | 0.7 | 0.9 | 0.7 | 0.4 | 0.7 | 0.5 | 0.6 |

| YoY | |||||||||||||

| Quanta | -5% | 11% | 18% | -5% | -6% | 9% | -3% | -9% | -4% | -35% | 8% | 6% | -8% |

| Compal | -17% | -17% | -8% | -21% | -14% | -25% | -15% | 4% | -30% | -29% | -3% | -18% | -17% |

| Inventec | 6% | 24% | 0% | 6% | 6% | -6% | 0% | 0% | 13% | -6% | 16% | -12% | -17% |

| Wistron | 6% | 33% | 25% | 29% | 16% | 17% | 29% | 44% | 13% | 7% | 47% | 6% | -6% |

| Pegatron | 6% | 28% | -3% | -6% | 0% | 41% | 12% | 23% | 15% | -26% | -4% | -14% | -26% |

| MoM / QoQ | |||||||||||||

| Quanta | 15% | 32% | -20% | 2% | 12% | -24% | 0% | 11% | -31% | -26% | 165% | -34% | 0% |

| Compal | 9% | 4% | -8% | 0% | 9% | -16% | 10% | 4% | -33% | -6% | 87% | -36% | 11% |

| Inventec | 6% | 17% | -19% | 6% | 6% | -16% | 6% | 18% | -15% | -12% | 47% | -32% | 0% |

| Wistron | 6% | 33% | -17% | 10% | 0% | -5% | 5% | 18% | -35% | -6% | 75% | -36% | -6% |

| Pegatron | 27% | 28% | -24% | 10% | 0% | -6% | -10% | 32% | -24% | -39% | 59% | -22% | 10% |

Source: Company data

e92c7a75ab8b4efbba794e6b187208c8

camont o. non narmonky revenues

NTSm

1,000,000

900,000

800,000

700,000

600,000

500,000

400,000

300,000

200,000

100,000

For the exclusive use of KEVINLU@LENOVO.COM

—YoY% (RHS)

60%

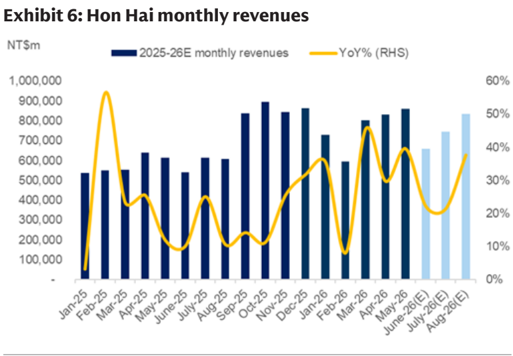

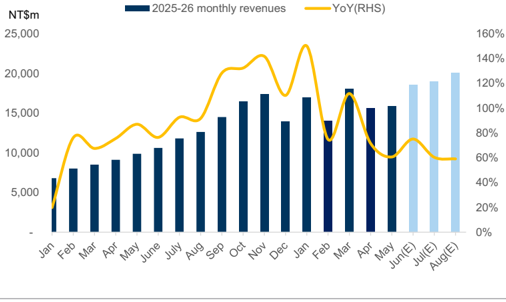

Hon Hai (2317.TW, Buy, on APAC CL): AI servers remain key growth driver

40%

30%

Hon Hai's May revenue was +40% YoY/+3% MoM to NT$859bn, or 5% higher than our previous estimates. We expect 2Q26E revenue to be +31% YoY/+11% QoQ to NT$2.4 trillion. May continued MoM growth (+3%) o ff Apr's high base, re fl ecting solid demand for AI server racks despite the typically slow seasonality of traditional electronics products in 2Q. We expect Jun revenue to grow 22% YoY (or -23% MoM) considering the high base, which is in line with historical seasonality. We expect continued shipment growth of AI server racks to support 2Q/3Q26E growth ahead.

Exhibit 5: We model Hon Hai's Jun 2026 revenue at +22% YoY or -23% MoM Hon Hai's monthly/annual revenue

| Apr 2026 | May 2026 | June 2026E | July 2026E | Aug 2026E | Sep 2026E | 2Q26E | 3Q26E | |

|---|---|---|---|---|---|---|---|---|

| Revenues (NT$m) | 832,098 | 859,409 | 659,861 | 745,642 | 835,120 | 1,377,695 | 2,351,368 | 2,958,457 |

| YoY | 30% | 40% | 22% | 21% | 38% | 65% | 31% | 44% |

| MoM/QoQ | 4% | 3% | -23% | 13% | 12% | 65% | 11% | 26% |

| GS estimates (NT$m) | 819,812 | 815,456 | ||||||

| Actual vs. GS | 1% | 5% |

Revenue lines are actual results reported by the company.

Source: Company data, Goldman Sachs Global Investment Research

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - Hon Hai

Valuation methodology: We are Buy-rated on Hon Hai. Our 12-month target price of NT$400 is based on a 21.0x 2026E P/E multiple, which is set in line with peers' PEG&M ratio (i.e., P/E vs. forward-year earnings growth and OPM).

Key downside risks: (1) slower-than-expected ramp-up of the AI server business; (2) weaker-than-expected EV total solution performance across EV assembly, design, software, and semis; (3) slower-than-expected ramp-up of capacity globally; and (4) fi ercer-than-expected competition in the consumer electronics EMS business.

e92c7a75ab8b4efbba794e6b187208c8

Ludila monty/ quarterly revenue summary

Apr-26 May-26 Jun-26(E)

Rev (NTSm)

YoY

MoM/QoQ

GS (NT$m)

For the exclusive use of KEVINLU@LENOVO.COM

311,481

376,830

121%

94%

98%

Jul-26(E) Aug-26(E) Sep-26(E)

301,464

256,244

266,276

90%

68%

45%

20,26E

1,028,232

104%

30,26E

823,985

66%

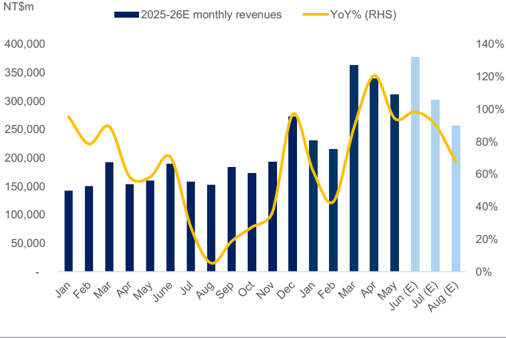

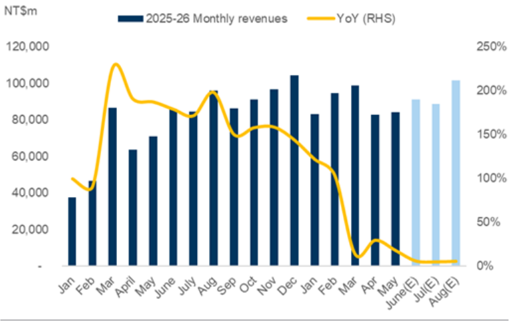

Quanta (2382.TW, Neutral): AI server ramp-up while model transition and PC pull- in may weigh on 3Q26 32% -11%

Quanta's May revenue was down 8% MoM, or 11% below our estimate, re fl ecting the impact of the AI servers model transition and PC consumption pull-in under rising memory costs. The company's PC shipments in May declined 8% YoY, or were fl at MoM. We expect 21% MoM revenue growth for Jun, considering the low base in May and improved PC consumption by the quarter-end. However, we expect the growth momentum to slow in Jul-Aug, given the AI server rack model transition in 3Q26E and a slowdown of PC shipments as consumption was pulled in in 1H26.

Exhibit 7: We model Quanta's Jun 2026E revenue at +98% YoY, or +21% MoM Quanta monthly/quarterly revenue summary

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 8: Quanta monthly revenues

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - Quanta

We are Neutral-rated on Quanta. Our 12-month target price of NT$299 is based on an 11.4x 2027E P/E , which references PC/server peers' EPS growth vs. P/E multiple correlation. We see EPS growth as a major factor for the stock's performance.

Key upside/downside risks include: 1) stronger-/weaker-than-expected PC market recovery; 2) faster-/slower-than-expected AI server ramp-up; and 3) stronger-/weaker-than-expected demand for general servers.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

AVC (3017.TW, Buy): GPU and ASIC AI servers driving liquid cooling penetration rate

AVC's May revenue was fl at MoM, or in line with our estimate. We expect the growth momentum to recover in Jun, considering the lower base in May, followed by sequential revenue growth in Jun-Sep, driven by (1) the ramp-up of liquid cooling components for new AI server racks, (2) a growing liquid cooling penetration rate in ASIC AI servers, and (3) the ramp-up of AVC's liquid cooling components for new ASIC AI servers.

Exhibit 9: AVC monthly/quarterly revenue summary

| Apr-26 | May-26 | Jun-26E | Jul-26E | Aug-26E | Sep-26E | 2Q26E | 3Q26E | |

|---|---|---|---|---|---|---|---|---|

| Rev (NT$m) | 15,631 | 15,871 | 18,570 | 18,941 | 20,077 | 21,786 | 50,072 | 60,805 |

| Rev YoY | 72% | 61% | 75% | 60% | 59% | 50% | 69% | 56% |

| Rev MoM / QoQ | -13% | 2% | 17% | 2% | 6% | 9% | 2% | 21% |

| GS estimates (NT$m) | 18,197 | 15,788 | ||||||

| Act vs. GS | -14% | 1% |

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 10: AVC monthly revenues

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - AVC

We are Buy-rated on AVC. Our 12-month target price for AVC is based on a near-term P/E, consistent with our Taiwan Technology coverage. We base our target price of NT$3,536 on a target P/E multiple of 26.7x on our forward-year EPS (2027E). Our target P/E is derived from the correlation between P/E and EPS growth of its peers in technology hardware.

Key downside risks: (1) slower-than-expected adoption of liquid cooling; (2) lower-than-expected demand for AI servers; (3) fi ercer-than-expected competition; and (4) slower-than-expected recovery of general servers.

e92c7a75ab8b4efbba794e6b187208c8

camble 11 we expect wiwyll soutrevenue growul to be to turf tormom

Exmole 14. wiwynn montmy revenues

NTSm

120,000

YoY

MoW QoQ

100,000

Act vs. GS

80,000

60,000

40,000

20,000

For the exclusive use of KEVINLU@LENOVO.COM

Apr-26

30%

May-26 June-26(E) July-26(E)

84,050

-YoY (RHS)|

18%

6%

5%

91,062

88,782

Aug-26 (E) Sep-26(E)

101,465

250%

126,831

6%

47%

2026E

257,843

17%

-7%

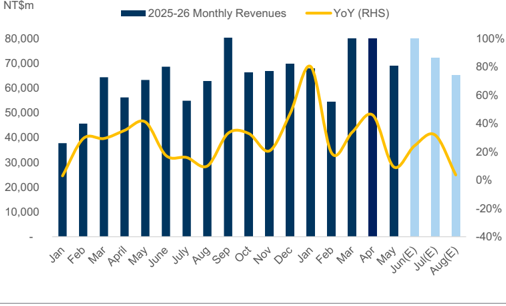

Wiwynn (6669.TW, Buy): ASIC AI servers support growth ahead

150%

Wiwynn's May revenue was fl at MoM, or 12% below our estimate, due to the switch to a consignment business model for some server projects starting from Apr (read more). Despite the business model transition being set to result in lower revenues, GM is expected to improve, which would also ease the working capital burden in the long term. For the coming June revenue, we expect a sequential increase on strong general server demand from leading US CSPs, followed by 23% QoQ growth in 3Q26 driven by an ASIC AI server ramp-up. We are positive on Wiwynn's leading market position in ASIC AI servers, diversifying into GPU AI server racks and riding on leading US CSPs' strong demand across general servers and AI servers.

Exhibit 11: We expect Wiwynn's Jun revenue growth to be +6% YoY/ +8% MoM

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 12: Wiwynn monthly revenues

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - Wiwynn

We are Buy-rated on Wiwynn with a 12-month TP of NT$7,147 . Our target price is based on 15.8x 2027E P/E , which is derived from PC/server peers' EPS growth vs. P/E multiple correlation. We see EPS growth as a major factor for the stock's performance.

Key downside risks: 1) weaker-than-expected AI server demand growth; 2) slower-than-expected recovery in general server demand; and 3) more severe competition in the server ODM market.

3026E

317,077

19%

23%

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

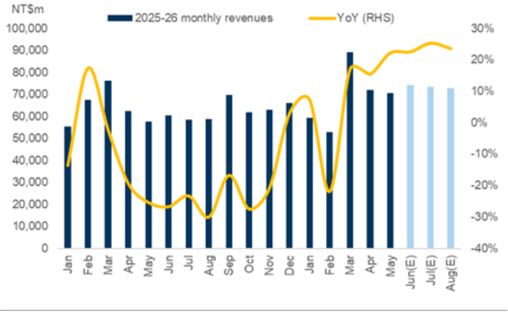

ASUS (2357.TW, Neutral): PC product mix upgrade and rack-level AI servers supporting 2H26 growth

ASUS's May revenue was down 16% MoM, or 13% below our estimate, which we attribute to the high base in Mar-Apr (monthly revenue +58% / -5% MoM). We expect Jun revenue to grow at +23% YoY, considering customer pull-in at quarter-end. Despite ongoing memory cost pressures, we expect the mix upgrade towards AI PCs and a rack-level AI server ramp-up to support 2Q/3Q26E growth at 26%/12% YoY. We model Jul/ Aug revenues to grow 32%/4% YoY to NT$72bn/ NT$65bn, with a MoM decline on the high base.

Exhibit 13: We expect ASUS Jun revenue to grow +24% YoY/+23% MoM to NT$85bn ASUS monthly/quarterly revenues

| Apr-26 | May-26 | Jun-26E | Jul-26E | Aug-26E | Sep-26E | 2Q26E | 3Q26E | |

|---|---|---|---|---|---|---|---|---|

| Rev (NT$m) | 81,915 | 69,094 | 85,089 | 72,325 | 65,093 | 86,226 | 236,098 | 223,645 |

| Rev YoY | 46% | 9% | 24% | 32% | 4% | 4% | 26% | 12% |

| RevMoM/QoQ | -5% | -16% | 23% | -15% | -10% | 32% | 22% | -5% |

| GS estimates (NT$m) | 60,259 | 79,458 | ||||||

| Act vs. GS | 36% | -13% |

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 14: ASUS monthly revenue trend

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - Asus

We are Neutral-rated on ASUS with a 12-month target price of NT$1,082 . Our target price is based on 15.8x 2027E P/E , which is derived from brand makers' average ratio of 2027E P/E to 2028E NI YoY and OPM. We see EPS growth and OPM as major factors for the stock's share performance.

Key upside/downside risks include: 1) stronger / weaker-than-expected PC market growth; 2) faster / slower-than-expected AI and gaming PC growth; and 3) faster / slower-than-expected AI server ramp-up.

e92c7a75ab8b4efbba794e6b187208c8

calivi lo collival moncily Icyclucs allu 10.

cambre 19. compare month revenue preview

NTSm

100,000

90,000

Rev YoY

80,000

70,000

Act vs. GS

60,000

50,000

40,000

30,000

20,000

10,000

For the exclusive use of KEVINLU@LENOVO.COM

Apr-26

16%

22%

24%

chu intor

May-26 Jun-26(E) Jul-26(E) Aug-26(E) Sep-26(E)

70,462

74,209

73,467

72,732

30%

25%

-YoY (RHS)

23%

44%

2Q26E

216,650

20%

3Q26E

246,733

32%

20%

Compal (2324.TW, Neutral): Global capacity ramping up to support AI servers

9%

MIAV

0%

Compal's May revenue was fl at MoM, or 9% higher than our estimate. Compal's PC shipments in May increased 11% MoM to 2mn units, and management expects QoQ growth in 2Q-3Q26. We expect MoM revenue growth in Jun, driven by customers' pull-in by quarter-end, followed by slight MoM declines in Jul-Aug, considering the high base in Jun. Overall, we expect 2Q / 3Q26E revenues to grow at 20%/32% YoY, supported by Compal's ongoing revenue mix diversi fi cation, and its new US plant, expected to start production by the end of 2Q26 (link).

Exhibit 15: Compal 3-month revenue preview

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 16: Compal monthly revenues and YoY trend (RHS)

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - Compal

We are Neutral-rated on Compal with a 12-month target price of NT$39.5 . Our target price is based on 13.6x 2027E P/E , which is derived from PC/server peers' EPS growth vs. P/E multiple correlation. We see EPS growth and market re-rating for ODM companies as major factors for the stock's performance.

Key upside/downside risks : 1) stronger-/weaker-than-expected PC market recovery; 2) faster-/slower-than-expected AI server ramp-up; and 3) stronger/weaker-than-expected demand for tablets.

100,533

e92c7a75ab8b4efbba794e6b187208c8

camore 1re mventee monty revenue preview

Exmore 10. mventec May revenue up so 70 ToT

Apr-26

Apr-26

May -26 Jun-26 (E)

May -26 Jun-26 (E)

82,808

77,003

35%

YoY

82,808

37%

35%

22%

Jul-26 (E)

Jul-26 (E)

68,533

26%

Aug-26 (E)

Sep-26 (E)

Aug-26 (E)

Sep-26 (E)

62,365

2%

2%

YoY

77,003

37%

22%

68,533

26%

62,365

Inventec (2356.TW, Neutral): Server business in expansion

Actual vs. GS

Actual vs. GS

34%

34%

30%

30%

Inventec's May revenue was up 35% YoY, or 30% above our estimate, which management attributes to the strong end demand for both AI and general servers on the global AI trend. We model sequential revenue declines for Jun-Aug, considering the PC consumption pull-in in 1H26 and rack-level AI servers entering model transition. Nevertheless, our estimate still show YoY growth for Inventec's Jun-Aug revenues, supported by its AI server capacity ramp up in the US (e.g., L10 / L11 assembly). Overall, we expect 2Q/3Q26E revenues to grow at 31%/10% YoY.

Exhibit 17: Inventec monthly revenue preview

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 18: Inventec May revenue up 35% YoY

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - Inventec

We are Neutral-rated on Inventec with a 12-month target price of NT$56.0 . Our target price is based on 13.6x 2027E P/E , which is derived from PC/server peers' EPS growth vs. P/E multiple correlation. We see EPS growth as a major factor for the stock's performance.

Key upside/downside risks : 1) stronger-/weaker-than-expected PC market recovery; 2) faster-/slower-than-expected AI server ramp-up; and 3) stronger-/weaker-than-expected demand for general servers.

63,552

63,552

5%

5%

2%

2%

For the exclusive use of KEVINLU@LENOVO.COM

2Q26E

2Q26E

244,598

31%

244,598

31%

22%

22%

3Q26E

3Q26E

10%

10%

-21%

-21%

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM