PDF 原檔:報告_CLSA_南寶4766_20260521_original.pdf

原始內容

21 May 2026

Taiwan

Consumer

Reuters

4766.TW

Bloomberg

4766 TT

Priced on 21 May 2026

Taiwan Wtd @ 41,368.2

12M hi/lo

NT$438.50/299.00

12M price target

NT$440.00

±% potential

+18%

Shares in issue

120.6m

Free float (est.)

67.2%

Market cap

US$1.4bn

3M ADV

US$11.1m

Foreign s'holding

14.0%

Major shareholders

Ting Feng Investment Co 9.2%

SinoPac analysts:

Jimmy Chou, SinoPac jimmy.chou@cl-sec.com

+886 223 268141

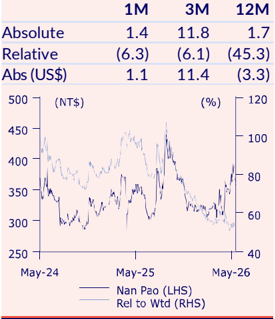

Stock performance (%)

| 1M | 3M | 12M | |

|---|---|---|---|

| Absolute | 1.4 | 11.8 | 1.7 |

| Relative | (6.3) | (6.1) | (45.3) |

| Abs (US$) | 1.1 | 11.4 | (3.3) |

Source: Bloomberg

Nan Pao

NT$372.00 - OUTPERFORM

Seeing progress

Semiconductor application process developing smoothly

Nan Pao's 1Q26 results exceeded expectations on the back of a stronger product mix and robust growth in the construction and coatings segments. We see nearterm margin headwinds from raw material pricing but expect a recovery in 2H26 as the company continues to enhance structural margins through product innovation and improved production efficiency. The JV of Advanced Pao Trusval Technology is progressing well, with testing and production ahead of schedule and already contributing to revenue. Following the 1Q26 results, we raise our 2026 EPS forecast by 3%, keep 2027SP EPS unchanged, and maintain our target price of NT$440. Reiterate Outperform.

1Q26 review

Nan Pao's 1Q26 GM and OPM beat our estimates by 1.1ppt/1.2ppt on a stronger product mix, better production efficiency, and tight Opex control. Revenue rose 5% YoY, driven by early shipment pull-in as clients advanced orders to hedge against material price volatility. Net profit increased 8% YoY, with EPS at NT$6.55.

2Q26 and 2026 outlook

Looking ahead to 2Q26, management expects slight YoY revenue growth despite early shipment pull-in in March and April. Near-term margin headwinds from raw material pricing are likely, but we anticipate a recovery in 2H26 as the company continues to optimise operations and product mix to offset profitability pressures. By segment, management guides low-single digit growth in adhesives amid cautious consumer sentiment, while remaining positive on construction and coatings growth.

Updates on joint venture

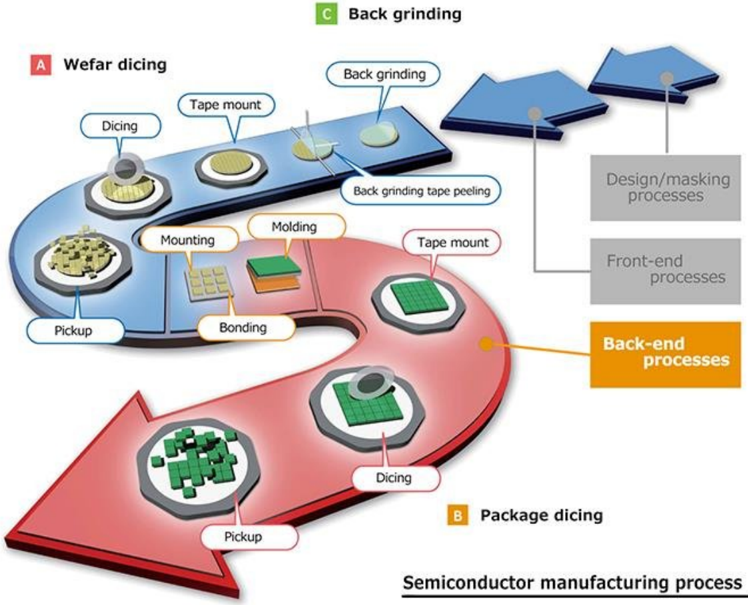

Nan Pao is making solid progress with its joint venture, Advanced Pao Trusval Technology, securing qualifications from world-class packaging leaders. The company has acquired one of its existing customers, allowing it to leverage mature production lines, while rapidly advancing testing and mass production capabilities. In this JV, Nan Pao acts as an upstream supplier, providing adhesive solvents for UV tape used in semiconductor backgrinding and dicing processes. The JV currently contributes 1-2% of revenue, and we expect this to rise to 4-5% by year-end.

Reiterate Outperform with unchanged TP of NT$440

After factoring in the 1Q26 results, we raise our 2026 EPS forecast by 3%, leave 2027SP EPS unchanged, and maintain our TP of NT$440. Reiterate Outperform.

| Financials | |||||

|---|---|---|---|---|---|

| Year to 31 December Revenue (NT$m) | 24A 22,983 | 25A 23,200 | 26SP 24,477 | 27SP 26,666 | 28SP 29,034 |

| Rev forecast change (%) | - | - | (1.0) | (0.1) | 0.0 |

| Net profit (NT$m) | 2,684 | 2,442 | 3,007 | 3,347 | 3,825 |

| NP forecast change (%) | - | - | 2.8 | 0.5 | (0.1) |

| EPS (NT$) | 22.26 | 20.25 | 24.94 | 27.76 | 31.72 |

| SP/consensus (2) (EPS%) | - | - | 104 | 103 | 100 |

| EPS growth (% YoY) | 10.5 | (9.0) | 23.1 | 11.3 | 14.3 |

| PE (x) | 16.7 | 18.4 | 14.9 | 13.4 | 11.7 |

| Dividend yield (%) | 5.1 | 4.8 | 5.4 | 6.0 | 6.8 |

| ROE (%) | 19.4 | 17.3 | 21.2 | 22.2 | 23.7 |

| Net cash per share (NT$) | 17.19 | 14.70 | 41.93 | 46.98 | 53.32 |

Source: SinoPac

Financials at a glance

| Year to 31 December | 2024A | 2025A | 2026SP | (% YoY) | 2027SP | 2028SP |

|---|---|---|---|---|---|---|

| Profit & Loss (NT$m) | ||||||

| Revenue | 22,983 | 23,200 | 24,477 | 5.5 | 26,666 | 29,034 |

| Cogs (ex-D&A) | (14,726) | (14,501) | (15,246) | (16,361) | (17,684) | |

| Gross Profit (ex-D&A) | 8,257 | 8,700 | 9,232 | 6.1 | 10,305 | 11,351 |

| SG&A and other expenses | (3,930) | (4,100) | (4,209) | (4,562) | (4,937) | |

| Op Ebitda | 4,327 | 4,600 | 5,022 | 9.2 | 5,743 | 6,414 |

| Depreciation/amortisation | (734) | (784) | (805) | (866) | (927) | |

| Op Ebit | 3,593 | 3,816 | 4,217 | 10.5 | 4,877 | 5,487 |

| Net interest inc/(exp) | 9 | (10) | (20) | (20) | (20) | |

| Other non-Op items | 155 | (176) | 274 | 130 | 184 | |

| Profit before tax | 3,757 | 3,630 | 4,471 | 23.2 | 4,987 | 5,651 |

| Taxation | (970) | (985) | (1,228) | (1,396) | (1,582) | |

| Profit after tax | 2,787 | 2,645 | 3,243 | 22.6 | 3,591 | 4,069 |

| Minority interest | (103) | (203) | (236) | (244) | (244) | |

| Net profit | 2,684 | 2,442 | 3,007 | 23.1 | 3,347 | 3,825 |

| Adjusted profit | 2,684 | 2,442 | 3,007 | 23.1 | 3,347 | 3,825 |

| Cashflow (NT$m) | 2024A | 2025A | 2026SP | (% YoY) | 2027SP | 2028SP |

| Operating profit | 3,593 | 3,816 | 4,217 | 10.5 | 4,877 | 5,487 |

| Depreciation/amortisation | 734 | 784 | 805 | 2.7 | 866 | 927 |

| Working capital changes | (692) | (372) | (340) | (575) | (628) | |

| Other items | (833) | (862) | 1,870 | (853) | (1,244) | |

| Net operating cashflow | 2,802 | 3,365 | 6,553 | 94.7 | 4,315 | 4,541 |

| Capital expenditure | (511) | (648) | (1,100) | (1,300) | (1,100) | |

| Free cashflow | 2,291 | 2,718 | 5,453 | 100.6 | 3,015 | 3,441 |

| M&A/Others | (134) | (290) | 0 | 0 | 0 | |

| Net investing cashflow | (645) | (938) | (1,100) | (1,300) | (1,100) | |

| Increase in loans | 1,941 | 729 | 0 | 0 | 0 | |

| Dividends | (1,901) | (2,417) | (2,170) | (2,406) | (2,677) | |

| Net equity raised/other | (75) | (65) | 0 | 0 | 0 | |

| Net financing cashflow | (35) | (1,754) | (2,170) | 387.1 | (2,406) | (2,677) |

| Incr/(decr) in net cash | 2,122 | 674 | 3,282 | 609 | 764 | |

| Exch rate movements | 213 | (238) | 0 | 0 | 0 | |

| Balance sheet (NT$m) | 2024A | 2025A | 2026SP | (% YoY) | 2027SP | 2028SP |

| Cash & equivalents | 6,910 | 7,346 | 10,629 | 44.7 | 11,238 | 12,002 |

| Accounts receivable | 5,522 | 5,408 | 5,706 | 5.5 | 6,216 | 6,768 |

| Other current assets | 4,474 | 4,772 | 4,925 | 3.2 | 5,159 | 5,435 |

| Fixed assets | 5,840 | 5,768 | 5,768 | 0 | 5,768 370 | 5,768 |

| Investments Intangible assets | 240 | 370 0 | 370 0 | 0 | 0 | 370 0 |

| Other non-current assets | 0 4,280 | 4,068 | 1,519 | (62.7) | 1,519 | 1,519 |

| Total assets | 27,267 | 27,732 | 28,916 | 4.3 | 30,270 | 31,862 |

| Short-term debt | 3,103 | 2,710 | 2,710 | 0 | 2,710 | 2,710 |

| Accounts payable | 2,292 | 2,203 | 2,313 | 5 | 2,483 | 2,682 |

| Other current liabs | 2,245 | 2,553 | 2,553 | 0 | 2,553 | 2,553 |

| Long-term debt/CBs | 1,735 | 2,864 | 2,864 | 0 | 2,864 | 2,864 |

| Provisions/other LT liabs | 1,955 | 1,972 | 1,972 | 0 | 1,972 | 1,972 |

| Shareholder funds | 14,492 | 13,794 | 14,631 | 6.1 | 15,572 | 16,720 |

| Minorities/other equity | 1,445 | 1,636 | 1,872 | 14.4 | 2,116 | 2,360 |

| 31,861 | ||||||

| Total liabs & equity | 27,267 | 27,732 | 28,916 | 4.3 | 30,271 | |

| Ratio analysis Revenue growth (% | 2024A 11.7 | 2025A 0.9 | 2026SP | (% YoY) | 2027SP | 2028SP 8.9 |

| YoY) | 5.5 | 8.9 | ||||

| Ebitda margin (%) | 18.8 | 19.8 | 20.5 | 21.5 | 22.1 | |

| Ebit margin (%) | 15.6 | 16.4 | 17.2 | 18.3 | 18.9 | |

| Net profit growth (%) | 10.5 | (9.0) | 23.1 | 11.3 | 14.3 | |

| Op cashflow growth (% YoY) Capex/sales (%) | (10.4) 2.2 | 20.1 2.8 | 94.7 4.5 | (34.2) 4.9 | 5.2 3.8 | |

| (%) | (11.5) | (30.6) | (33.7) | |||

| Net debt/equity Net debt/Ebitda (x) | (13.0) - | - | - | (32.0) - | - | |

| ROE (%) | 19.4 | 17.3 18.0 | 21.2 21.6 | 22.2 | 23.7 | |

| ROIC (%) | 17.7 | 26.3 | 28.3 |

Source: SinoPac

Nan Pao 1Q26 Analyst Meeting Takeaways

1Q26 results

-

r Revenue: NT$5,836m, +5% YoY

-

[ ] r Gross margin: 35.1%; thanks to a better product mix and lower raw material pricing/inventory

-

[ ] r Operating profit: NT$1,029m, +13% YoY

-

[ ] r Net profit: NT$790m, +8% YoY

-

[ ] r EPS: NT$6.55

-

r Although demand remained relatively weak due to the consumer market environment, expectations of raw material price fluctuations and product price increases encouraged customers to place orders and build up inventory ahead of schedule, driving overall revenue growth compared to same period last year

2026 outlook

-

[ ] r Targeting record-high revenue this year

-

[ ] r Will continue to optimise operations and product mix to mitigate profitability impacts

-

[ ] r Has begun shipping to Advanced Pao Trusval, formally contributing to revenue; this contribution is expected to scale up throughout the year as product qualifications advance

-

[ ] r Continuing to expand R&D in electronic and semiconductor applications related to core technologies, with increased resource investment

-

[ ] r Long-term target for Opex ratio: below 15%

Revenue outlook

-

[ ] r March and April revenue reached record highs due to early shipment pull- in

-

[ ] r 2Q26 guidance: similar to last year, with a slight increase expected

Raw material and gross margin impacts

-

[ ] r Solvent costs have a direct correlation with oil price changes - accounting for about 20% of raw material Cogs

-

[ ] r Anticipates gross margin impacts in May-June, depending on client negotiations and price transfers. A more conservative outlook is expected for 2Q

Overall profit guidance

- [ ] r Profit should be higher than last year due to structural improvements within the company, although current macro conditions still present uncertainties

Updates on Advanced Pao Trusval Technology

-

[ ] r Nan Pao supplies solvents for UV tape (acts as an upstream supplier)

-

[ ] r Advanced Pao Trusval Technology converts solvents into UV tape for back grinding and dicing applications

-

[ ] r Achieved additional client certifications from OSATs

-

[ ] r Advanced Pao Trusval Technology currently operating at full capacity, requiring overtime work. Capacity expansion is planned, though the timeline remains uncertain

-

[ ] r Nan Pao currently has adequate capacity

Footwear

-

[ ] r Currently taking a conservative outlook

-

r Focused on product innovations, new clients, and new orders so far increasing market share

- r Rising oil prices may create raw material cost pressures, but negotiations with clients are ongoing

Capex

- r 2026: NT$1.1-1.2bn, higher than 2025.

- r Mainly for China: relocating the Anqing factory to Hefei and increasing automotive application capacity

- r India capacity expansion (US$12-13m over two years), expected to be completed by year-end and contribute starting early next year for footwear adhesives

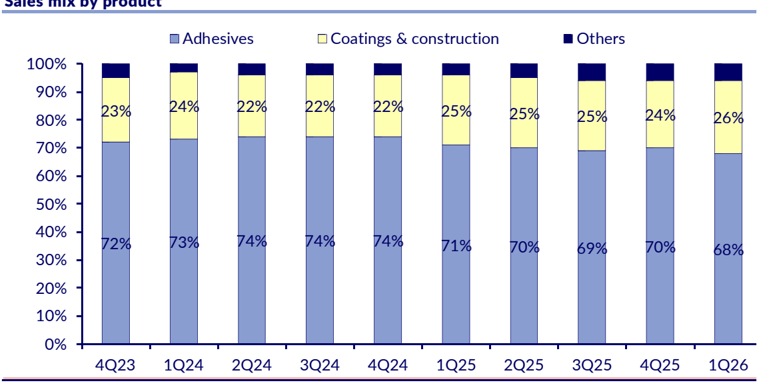

Segment outlooks

- r Adhesives: consumer sentiment remains cautious; guiding low single-digit growth

- r Construction: revenue mainly from Australia. Driven by rising local demand and continued market cultivation, market share is steadily expanding. Favourable tailwinds from an appreciating Australian Dollar support continuous growth targets

- r Coatings: targeting opportunities in government infrastructure, AI infrastructure applications, and consumer electronics-related fields expected to drive continued growth

Figure 1

Sales mix by product

Source: SinoPac

Nan Pao is structurally improving its margins and reducing the impact of raw material prices

Figure 3

| JV breakdown | JV breakdown | JV breakdown |

|---|---|---|

| Partner | Strengths | Role in JV |

| Nan Pao (4766 TT) | 60+ years of adhesive expertise and global scale | The Formulation Core: R&D of high-purity resin bases for UV- debonding tapes and temporary bonding adhesives |

| AEMC (4749 TT) | Semiconductor specialist with deep knowledge of lithography and purification | The Quality & Channel: Handles high-purity filtration, regulatory compliance, and leverages existing TSMC/OSAT relationships |

| Trusval (6667 TT) | Process system integrator specialising in chemical delivery and automated coating | The Equipment Integrator: Ensures the adhesives can be applied with sub-micron prevision on silicon wafers |

Source: SinoPac

Expected to reach US$3.3bn, with 9.7% Cagr from 2024

Figure 2

Source: SinoPac, Bloomberg

Figure 4

Source: SinoPac, Business Research Insights

Figure 5

| UV tape segment analysis | UV tape segment analysis | UV tape segment analysis |

|---|---|---|

| Segment Category | Sub-Segments | Key Insights |

| By type | ∑ UV Tape ∑ Non-UV Tape | UV Tape dominates the market due to its superior adhesive properties and controlled release mechanism. ∑ Preferred for high-precision wafer processing due to strong temporary bonding during grinding/dicing ∑ UV irradiation enables clean removal without residue, critical for advanced semiconductor nodes ∑ Material innovations focus on improving UV sensitivity while maintaining thermal stability |

| By application | ∑ Back Grinding Tape ∑ Dicing Tape ∑ Hybrid Applications | Dicing Tape holds majority application share with critical role in wafer singulation. ∑ Advanced dicing technologies require tapes with precise adhesive control to prevent chipping ∑ Emerging ultra-thin wafer formats demand tapes with exceptional dimensional stability ∑ Trend toward multi-functional tapes that support both grinding and dicing processes |

| By end user | ∑ IDMs ∑ Foundries ∑ OSAT Providers | Foundries represent the most demanding segment with specialized tape requirements. ∑ Advanced node manufacturing requires tapes compatible with extreme process conditions ∑ Volume production drives need for consistent, high-reliability tape solutions ∑ Customised tape formulations developed through close supplier partnerships |

| By technology node | ∑ >28nm ∑ 28nm-14nm ∑ <14nm | <14nm segment shows strongest innovation activity in tape development. ∑ Requires ultra-clean removal characteristics to prevent killer defects ∑ Materials must withstand high temperatures from advanced packaging processes ∑ Japanese suppliers lead in developing cutting-edge formulations for leading- edge nodes |

| By material composition | ∑ Acrylic-based ∑ Rubber-based ∑ Composite Materials | Acrylic-based formulations dominate due to their balance of performance and processability. ∑ Offer excellent UV responsiveness for controlled adhesive properties ∑ Provide superior thermal stability during back-end processes ∑ Ongoing R&D focuses on reducing outgassing for cleaner processing |

Source: SinoPac, Intel Market Research

Figure 6

| Semiconductor tape comparison | |||

|---|---|---|---|

| Features | Back Grinding Tape | Dicing Tape | Die Attach Film (DAF) |

| Application phase | Wafer thinning | Wafer dicing | Die bonding |

| Placement | Front (active) side | Back side | Between die and substrate |

| Permanence | Temporary (removed) | Temporary (removed) | Permanent |

| Primary goal | Protect circuitry | Prevent die fly-off | Bond chips to package |

| Typical material | PET/PVC with acrylic | PO/PVC with UV resin | Epoxy/acrylic resin |

Source: SinoPac

UV tape used during semiconductor manufacturing process

CLSA

Remerch merited by Gil SinoPac

Figure 7

UV tape used during semiconductor manufacturing process

Back grinding

Back grinding

Back grinding tape peeling

Tape mount

Source: SinoPac, Maxell

Figure 8

| P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly | P&L - quarterly |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (NT$m) | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 | 2Q26SP | 3Q26SP | 4Q26SP | 1Q27SP | 2Q27SP | 3Q27SP | 4Q27SP |

| Sales | 5,554 | 5,805 | 5,910 | 5,930 | 5,836 | 6,056 | 6,253 | 6,332 | 6,300 | 6,629 | 6,800 | 6,937 |

| Gross profit | 1,912 | 2,003 | 2,001 | 2,001 | 2,049 | 2,025 | 2,153 | 2,200 | 2,207 | 2,329 | 2,416 | 2,486 |

| Opex | 1,002 | 1,018 | 1,038 | 1,042 | 1,020 | 1,023 | 1,070 | 1,096 | 1,090 | 1,121 | 1,163 | 1,187 |

| Operating profit | 910 | 985 | 963 | 959 | 1,029 | 1,001 | 1,083 | 1,103 | 1,117 | 1,208 | 1,253 | 1,299 |

| Pretax profit | 1,013 | 806 | 922 | 889 | 1,138 | 1,046 | 1,128 | 1,158 | 1,147 | 1,238 | 1,278 | 1,324 |

| Tax expense | 241 | 208 | 269 | 267 | 294 | 293 | 316 | 324 | 321 | 347 | 358 | 371 |

| Net profit | 729 | 554 | 599 | 560 | 790 | 692 | 751 | 773 | 765 | 831 | 859 | 892 |

| EPS (NT$) | 6.05 | 4.59 | 4.97 | 4.65 | 6.55 | 5.74 | 6.23 | 6.41 | 6.34 | 6.89 | 7.13 | 7.40 |

| Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth |

| Sales QoQ | (19%) | 12% | 7% | 1% | (10%) | 16% | 5% | 1% | (9%) | 5% | 2% | 0% |

| Sales YoY | 11% | 0% | (3%) | (3%) | 5% | 4% | 6% | 7% | 8% | 9% | 9% | 10% |

| EPS YoY | 3% | (18%) | (9%) | (13%) | 8% | 25% | 25% | 38% | (3%) | 20% | 14% | 15% |

| Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin |

| Gross margin | 34.4% | 34.5% | 33.9% | 33.7% | 35.1% | 33.4% | 34.4% | 34.7% | 35.0% | 35.1% | 35.5% | 35.8% |

| Opex | 18.0% | 17.5% | 17.6% | 17.6% | 17.5% | 16.9% | 17.1% | 17.3% | 17.3% | 16.9% | 17.1% | 17.1% |

| OP margin | 16.4% | 17.0% | 16.3% | 16.2% | 17.6% | 16.5% | 17.3% | 17.4% | 17.7% | 18.2% | 18.4% | 18.7% |

| Net margin | 13.1% | 9.5% | 10.1% | 9.5% | 13.5% | 11.4% | 12.0% | 12.2% | 12.1% | 12.5% | 12.6% | 12.9% |

Source: SinoPac

A

Wefar dicing

Dicing

Tape mount

Design/masking processes

Figure 9

| P&L - annual | |||||

|---|---|---|---|---|---|

| (NT$m) | 2024 | 2025 | 2026SP | 2027SP | 2028SP |

| Sales | 22,983 | 23,200 | 24,477 | 26,666 | 29,034 |

| Gross profit | 7,522 | 7,916 | 8,427 | 9,439 | 10,424 |

| Opex | 3,930 | 4,100 | 4,209 | 4,562 | 4,937 |

| Operating profit | 3,593 | 3,816 | 4,217 | 4,877 | 5,487 |

| Pretax profit | 3,757 | 3,630 | 4,471 | 4,987 | 5,651 |

| Tax expense | 970 | 985 | 1,228 | 1,396 | 1,582 |

| Net profit | 2,684 | 2,442 | 3,007 | 3,347 | 3,825 |

| EPS (NT$) | 22.26 | 20.25 | 24.94 | 27.76 | 31.72 |

| Growth | |||||

| Sales YoY | 12% | 1% | 6% | 9% | 9% |

| EPS YoY | 11% | (9%) | 23% | 11% | 14% |

| Margin | |||||

| Gross margin | 32.7% | 34.1% | 34.4% | 35.4% | 35.9% |

| Opex | 17.1% | 17.7% | 17.2% | 17.1% | 17.0% |

| OP margin | 15.6% | 16.4% | 17.2% | 18.3% | 18.9% |

| Net margin | 11.7% | 10.5% | 12.3% | 12.6% | 13.2% |

Source: SinoPac

Figure 10

| Forecast revisions - quarterly | Forecast revisions - quarterly | Forecast revisions - quarterly | Forecast revisions - quarterly | Forecast revisions - quarterly | Forecast revisions - quarterly | Forecast revisions - quarterly | Forecast revisions - quarterly | Forecast revisions - quarterly | Forecast revisions - quarterly |

|---|---|---|---|---|---|---|---|---|---|

| 1Q26SP | 1Q26SP | 3Q26SP | 3Q26SP | 3Q26SP | 3Q26SP | ||||

| (NT$m) | old | new | % ch | old | new | % ch | old | new | % ch |

| Sales | 5,836 | 5,836 | 0% | 6,256 | 6,056 | (3%) | 6,288 | 6,253 | (1%) |

| Gross profit | 1,986 | 2,049 | 3% | 2,091 | 2,025 | (3%) | 2,171 | 2,153 | (1%) |

| Opex | 1,027 | 1,020 | (1%) | 1,057 | 1,023 | (3%) | 1,076 | 1,070 | (1%) |

| Operating profit | 959 | 1,029 | 7% | 1,034 | 1,001 | (3%) | 1,095 | 1,083 | (1%) |

| Pretax profit | 1,026 | 1,138 | 11% | 1,091 | 1,046 | (4%) | 1,132 | 1,128 | 0% |

| Tax expense | 287 | 294 | 2% | 305 | 293 | (4%) | 317 | 316 | 0% |

| Net profit | 677 | 790 | 17% | 724 | 692 | (4%) | 754 | 751 | 0% |

| EPS (NT$) | 5.62 | 6.55 | 17% | 6.01 | 5.74 | (4%) | 6.25 | 6.23 | 0% |

| Margin | |||||||||

| Gross margin | 34.0% | 35.1% | 1.1 ppt | 33.4% | 33.4% | 0 ppt | 34.5% | 34.4% | -0.1 ppt |

| OPEX ratio | 17.6% | 17.5% | -0.1 ppt | 16.9% | 16.9% | 0 ppt | 17.1% | 17.1% | 0 ppt |

| Operating margin | 16.4% | 17.6% | 1.2 ppt | 16.5% | 16.5% | 0 ppt | 17.4% | 17.3% | -0.1 ppt |

| Tax rate | 28.0% | 25.9% | -2.1 ppt | 28.0% | 28.0% | 0 ppt | 28.0% | 28.0% | 0 ppt |

| Net margin | 11.6% | 13.5% | 1.9 ppt | 11.6% | 11.4% | -0.1 ppt | 12.0% | 12.0% | 0 ppt |

Source: SinoPac

Figure 11

Source: SinoPac

| Forecast revisions - annual | Forecast revisions - annual | Forecast revisions - annual | Forecast revisions - annual | Forecast revisions - annual | Forecast revisions - annual | Forecast revisions - annual | Forecast revisions - annual | Forecast revisions - annual | Forecast revisions - annual |

|---|---|---|---|---|---|---|---|---|---|

| 2026SP | 2026SP | 2028SP | 2028SP | 2028SP | 2028SP | ||||

| (NT$m) | old | new | % ch | old | new | % ch | old | new | % ch |

| Sales | 24,725 | 24,477 | (1%) | 26,705 | 26,666 | 0% | 29,020 | 29,034 | 0% |

| Gross profit | 8,451 | 8,427 | 0% | 9,409 | 9,439 | 0% | 10,418 | 10,424 | 0% |

| Opex | 4,246 | 4,209 | (1%) | 4,568 | 4,562 | 0% | 4,934 | 4,937 | 0% |

| Operating profit | 4,205 | 4,217 | 0% | 4,841 | 4,877 | 1% | 5,484 | 5,487 | 0% |

| Pretax profit | 4,404 | 4,471 | 2% | 4,968 | 4,987 | 0% | 5,656 | 5,651 | 0% |

| Tax expense | 1,233 | 1,228 | 0% | 1,391 | 1,396 | 0% | 1,584 | 1,582 | 0% |

| Net profit | 2,926 | 3,007 | 3% | 3,332 | 3,347 | 0% | 3,827 | 3,825 | 0% |

| EPS (NT$) | 24.26 | 24.94 | 3% | 27.63 | 27.76 | 0% | 31.74 | 31.72 | 0% |

| Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin |

| Gross margin | 34.2% | 34.4% | 0.2 ppt | 35.2% | 35.4% | 0.2 ppt | 35.9% | 35.9% | 0 ppt |

| OPEX ratio | 17.2% | 17.2% | 0 ppt | 17.1% | 17.1% | 0 ppt | 17.0% | 17.0% | 0 ppt |

| Operating margin | 17.0% | 17.2% | 0.2 ppt | 18.1% | 18.3% | 0.2 ppt | 18.9% | 18.9% | 0 ppt |

| Tax rate | 28.0% | 27.5% | -0.5 ppt | 28.0% | 28.0% | 0 ppt | 28.0% | 28.0% | 0 ppt |

| Net margin | 11.8% | 12.3% | 0.5 ppt | 12.5% | 12.6% | 0.1 ppt | 13.2% | 13.2% | 0 ppt |

Figure 12

| SP vs consensus - quarterly | SP vs consensus - quarterly | SP vs consensus - quarterly | SP vs consensus - quarterly | SP vs consensus - quarterly | SP vs consensus - quarterly | SP vs consensus - quarterly | SP vs consensus - quarterly | SP vs consensus - quarterly | SP vs consensus - quarterly |

|---|---|---|---|---|---|---|---|---|---|

| 1Q26 | 1Q26 | 3Q26 | 3Q26 | 3Q26 | 3Q26 | ||||

| (NT$m) | SinoPac | Con | % Diff | SinoPac | Con | % Diff | SinoPac | Con | % Diff |

| Sales | 5,836 | 5,658 | 3% | 6,056 | 6,193 | (2%) | 6,253 | 6,359 | (2%) |

| Gross profit | 2,049 | 1,902 | 8% | 2,025 | 2,069 | (2%) | 2,153 | 2,136 | 1% |

| Opex | 1,020 | 1,012 | 1% | 1,023 | 1,043 | (2%) | 1,070 | 1,057 | 1% |

| Operating profit | 1,029 | 890 | 16% | 1,001 | 1,026 | (2%) | 1,083 | 1,079 | 0% |

| Pretax profit | 1,138 | 1,060 | 7% | 1,046 | 1,015 | 3% | 1,128 | 1,073 | 5% |

| Tax expense | 294 | 315 | (7%) | 293 | 314 | (7%) | 316 | 333 | (5%) |

| Net profit | 790 | 745 | 6% | 692 | 702 | (1%) | 751 | 740 | 2% |

| EPS (NT$) | 6.55 | 6.18 | 6% | 5.74 | 5.82 | (1%) | 6.23 | 6.13 | 2% |

| Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin |

| Gross margin | 35.1% | 33.6% | 1.5 ppt | 33.4% | 33.4% | 0 ppt | 34.4% | 33.6% | 0.9 ppt |

| Operating margin | 17.6% | 15.7% | 1.9 ppt | 16.5% | 16.6% | 0 ppt | 17.3% | 17.0% | 0.4 ppt |

| Net margin | 13.5% | 13.2% | 0.4 ppt | 11.4% | 11.3% | 0.1 ppt | 12.0% | 11.6% | 0.4 ppt |

Source: SinoPac, Bloomberg

Figure 13

| SP vs consensus - annual | SP vs consensus - annual | SP vs consensus - annual | SP vs consensus - annual | SP vs consensus - annual | SP vs consensus - annual | SP vs consensus - annual | SP vs consensus - annual | SP vs consensus - annual | SP vs consensus - annual |

|---|---|---|---|---|---|---|---|---|---|

| 2026 | 2026 | 2028 | 2028 | 2028 | 2028 | ||||

| (NT$m) | SinoPac | Con | % Diff | SinoPac | Con | % Diff | SinoPac | Con | % Diff |

| Sales | 24,477 | 24,620 | (1%) | 26,666 | 26,352 | 1% | 29,034 | 29,020 | 0% |

| Gross profit | 8,427 | 8,241 | 2% | 9,439 | 9,091 | 4% | 10,424 | 10,418 | 0% |

| Opex | 4,209 | 4,180 | 1% | 4,562 | 4,474 | 2% | 4,937 | 4,934 | 0% |

| Operating profit | 4,217 | 4,061 | 4% | 4,877 | 4,617 | 6% | 5,487 | 5,484 | 0% |

| Pretax profit | 4,471 | 4,212 | 6% | 4,987 | 4,728 | 5% | 5,651 | 5,656 | 0% |

| Tax expense | 1,228 | 1,298 | (5%) | 1,396 | 1,479 | (6%) | 1,582 | 1,829 | (13%) |

| Net profit | 3,007 | 2,914 | 3% | 3,347 | 3,249 | 3% | 3,825 | 3,827 | 0% |

| EPS (NT$) | 24.94 | 23.86 | 5% | 27.76 | 26.94 | 3% | 31.72 | 31.74 | 0% |

| Margin | |||||||||

| Gross margin | 34.4% | 33.5% | 1 ppt | 35.4% | 34.5% | 0.9 ppt | 35.9% | 35.9% | 0 ppt |

| Operating margin | 17.2% | 16.5% | 0.7 ppt | 18.3% | 17.5% | 0.8 ppt | 18.9% | 18.9% | 0 ppt |

| Net margin | 12.3% | 11.8% | 0.4 ppt | 12.6% | 12.3% | 0.2 ppt | 13.2% | 13.2% | 0 ppt |

Source: SinoPac, Bloomberg

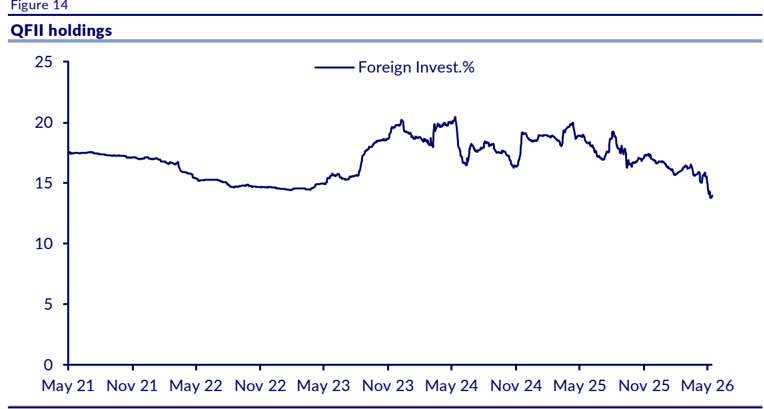

Foreign investors hold 14%

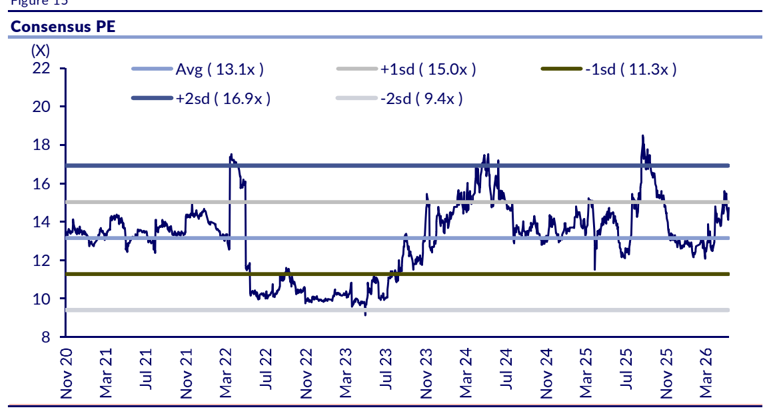

The stock currently trades at 14.7x forward 12M PE

Source: SinoPac, TEJ

Figure 15

Source: SinoPac, Bloomberg

Investment thesis

We believe Nan Pao is set to benefit from the upcoming global athletic footwear restocking cycle as one of the top suppliers of footwear adhesives. In addition, as global brands become more aware of ESG initiatives, Nan Pao will produce more ecofriendly materials, such as water-based adhesives, which should help improve overall adhesive margins. Lastly, as Nan Pao has entered into a joint venture to break into the semiconductor supply chain, we expect further margin improvements as well as historical high revenue growth.

Catalysts

1) Margins improvement driven by better product mix and water-based adhesive adoption; 2) valuation rerating triggered by deeper penetration into the CoWoS and advanced packaging supply chains; 3) successful capacity ramp-up in India to capture footwear supply chain migration; 4) a 5.5% dividend yield acts as a defensive catalyst, offering attractive downside protection and total return potential in a volatile market environment.

Valuation details

We use PE as our valuation methodology as we believe the market will primarily focus on the earnings growth outlook, which is better reflected with PE metrics. We assign a target PE multiple of 17x to the stock, which is about +2sd of its fiveyear average. We believe the upcoming footwear restocking cycle and increasing contribution of semiconductor adhesive tapes for the company should lead to a valuation rerating, and it should be reflected through a robust 17% earnings Cagr from 25-27SP.

Investment risks

Key risks include 1) potential margin compression from sudden spikes in raw material costs; 2) slower-than-expected semiconductor certifications; 3) macro uncertainties leading to unhealthy consumer demand and unstable inflation movements.

Detailed financials

Profit & Loss (NT$m)

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Revenue | 22,004 | 20,581 | 22,983 | 23,200 | 24,477 | 26,666 | 29,034 |

| Cogs (ex-D&A) | (16,206) | (13,436) | (14,726) | (14,501) | (15,246) | (16,361) | (17,684) |

| Gross Profit (ex-D&A) | 5,798 | 7,145 | 8,257 | 8,700 | 9,232 | 10,305 | 11,351 |

| Research & development costs | (514) | (519) | (543) | (556) | (578) | (616) | (670) |

| Selling & marketing expenses | (2,032) | (1,998) | (2,158) | (2,270) | (2,402) | (2,613) | (2,815) |

| Other SG&A | (918) | (1,008) | (1,229) | (1,274) | (1,229) | (1,333) | (1,452) |

| Other Op Expenses ex-D&A | - | - | - | - | - | - | - |

| Op Ebitda | 2,335 | 3,619 | 4,327 | 4,600 | 5,022 | 5,743 | 6,414 |

| Depreciation/amortisation | (511) | (655) | (734) | (784) | (805) | (866) | (927) |

| Op Ebit | 1,824 | 2,964 | 3,593 | 3,816 | 4,217 | 4,877 | 5,487 |

| Interest income | 35 | 71 | 132 | 139 | 123 | 123 | 123 |

| Interest expense | (86) | (104) | (123) | (149) | (143) | (143) | (143) |

| Net interest inc/(exp) | (51) | (34) | 9 | (10) | (20) | (20) | (20) |

| Associates/investments | 477 | 381 | 60 | 71 | 87 | - | - |

| Forex/other income | 72 | (11) | 29 | (61) | (6) | - | - |

| Asset sales/other cash items | 64 | 93 | 66 | (185) | 193 | 130 | 184 |

| Provisions/other non-cash items | - | - | - | - | - | - | - |

| Asset revaluation/Exceptional items | - | - | - | - | - | - | - |

| Profit before tax | 2,385 | 3,394 | 3,757 | 3,630 | 4,471 | 4,987 | 5,651 |

| Taxation | (523) | (827) | (970) | (985) | (1,228) | (1,396) | (1,582) |

| Profit after tax | 1,863 | 2,566 | 2,787 | 2,645 | 3,243 | 3,591 | 4,069 |

| Preference dividends | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Profit for period | 1,863 | 2,566 | 2,787 | 2,645 | 3,243 | 3,591 | 4,069 |

| Minority interest | (121) | (138) | (103) | (203) | (236) | (244) | (244) |

| Net profit | 1,741 | 2,428 | 2,684 | 2,442 | 3,007 | 3,347 | 3,825 |

| Extraordinaries/others | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Profit avail to ordinary shares | 1,741 | 2,428 | 2,684 | 2,442 | 3,007 | 3,347 | 3,825 |

| Dividends | (761) | (1,264) | (1,901) | (2,417) | (2,170) | (2,406) | (2,677) |

| Retained profit | 981 | 1,164 | 783 | 25 | 837 | 941 | 1,147 |

| Adjusted profit | 1,741 | 2,428 | 2,684 | 2,442 | 3,007 | 3,347 | 3,825 |

| EPS (NT$) | 14.4 | 20.1 | 22.3 | 20.3 | 24.9 | 27.8 | 31.7 |

| Adj EPS [pre excep] (NT$) | 14.4 | 20.1 | 22.3 | 20.3 | 24.9 | 27.8 | 31.7 |

| Core EPS (NT$) | 14.4 | 20.1 | 22.3 | 20.3 | 24.9 | 27.8 | 31.7 |

| DPS (NT$) | 10.0 | 15.0 | 19.0 | 18.0 | 20.0 | 22.2 | 25.4 |

Profit & loss ratios

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Growth (%) | |||||||

| Revenue growth (% YoY) | 22.4 | (6.5) | 11.7 | 0.9 | 5.5 | 8.9 | 8.9 |

| Ebitda growth (% YoY) | 53.3 | 55.0 | 19.6 | 6.3 | 9.2 | 14.3 | 11.7 |

| Ebit growth (% YoY) | 73.4 | 62.5 | 21.2 | 6.2 | 10.5 | 15.6 | 12.5 |

| Net profit growth (%) | 98.8 | 39.4 | 10.5 | (9.0) | 23.1 | 11.3 | 14.3 |

| EPS growth (% YoY) | 98.8 | 39.4 | 10.5 | (9.0) | 23.1 | 11.3 | 14.3 |

| Adj EPS growth (% YoY) | 98.8 | 39.4 | 10.5 | (9.0) | 23.1 | 11.3 | 14.3 |

| DPS growth (% YoY) | 66.7 | 50.0 | 26.7 | (5.3) | 10.8 | 11.3 | 14.3 |

| Core EPS growth (% YoY) | 98.8 | 39.4 | 10.5 | (9.0) | 23.1 | 11.3 | 14.3 |

| Margins (%) | |||||||

| Gross margin (%) | 26.4 | 34.7 | 35.9 | 37.5 | 37.7 | 38.6 | 39.1 |

| Ebitda margin (%) | 10.6 | 17.6 | 18.8 | 19.8 | 20.5 | 21.5 | 22.1 |

| Ebit margin (%) | 8.3 | 14.4 | 15.6 | 16.4 | 17.2 | 18.3 | 18.9 |

| Net profit margin (%) | 7.9 | 11.8 | 11.7 | 10.5 | 12.3 | 12.6 | 13.2 |

| Core profit margin | 7.9 | 11.8 | 11.7 | 10.5 | 12.3 | 12.6 | 13.2 |

| Op cashflow margin | 8.7 | 15.2 | 12.2 | 14.5 | 26.8 | 16.2 | 15.6 |

| Returns (%) | |||||||

| ROE (%) | 11.7 | 17.5 | 19.4 | 17.3 | 21.2 | 22.2 | 23.7 |

| ROA (%) | 5.6 | 9.3 | 10.5 | 10.1 | 10.8 | 11.9 | 12.7 |

| ROIC (%) | 8.2 | 14.6 | 17.7 | 18.0 | 21.6 | 26.3 | 28.3 |

| ROCE (%) | 11.3 | 21.4 | 26.9 | 27.7 | 33.6 | 41.6 | 44.5 |

| Other key ratios (%) | |||||||

| Effective tax rate (%) | 21.9 | 24.4 | 25.8 | 27.1 | 27.5 | 28.0 | 28.0 |

| Ebitda/net int exp (x) | 45.4 | 107.5 | - | 451.7 | 251.9 | 288.0 | 321.6 |

| Exceptional or extraord. inc/PBT (%) | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Dividend payout (%) | 69.2 | 74.5 | 85.3 | 88.9 | 80.0 | 80.0 | 80.0 |

Source: SinoPac

Balance sheet (NT$m)

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Cash & equivalents | 3,996 | 4,575 | 6,910 | 7,346 | 10,629 | 11,238 | 12,002 |

| Accounts receivable | 4,879 | 4,751 | 5,522 | 5,408 | 5,706 | 6,216 | 6,768 |

| Inventories | 2,825 | 2,663 | 2,855 | 3,045 | 3,197 | 3,432 | 3,707 |

| Other current assets | 1,159 | 1,443 | 1,619 | 1,727 | 1,727 | 1,727 | 1,727 |

| Current assets | 12,859 | 13,432 | 16,906 | 17,526 | 21,259 | 22,613 | 24,204 |

| Fixed assets | 5,508 | 5,808 | 5,840 | 5,768 | 5,768 | 5,768 | 5,768 |

| Investments | 255 | 208 | 240 | 370 | 370 | 370 | 370 |

| Goodwill | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other intangible assets | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other non-current assets | 6,124 | 4,217 | 4,280 | 4,068 | 1,519 | 1,519 | 1,519 |

| Total assets | 24,746 | 23,664 | 27,267 | 27,732 | 28,916 | 30,270 | 31,862 |

| Short term loans/OD | 1,993 | 1,978 | 3,103 | 2,710 | 2,710 | 2,710 | 2,710 |

| Accounts payable | 2,659 | 2,177 | 2,292 | 2,203 | 2,313 | 2,483 | 2,682 |

| Accrued expenses | - | - | - | - | - | - | - |

| Taxes payable | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other current liabs | 1,684 | 2,237 | 2,245 | 2,553 | 2,553 | 2,553 | 2,553 |

| Current liabilities | 6,336 | 6,392 | 7,640 | 7,466 | 7,576 | 7,746 | 7,945 |

| Long-term debt/leases/other | 1,224 | 895 | 1,735 | 2,864 | 2,864 | 2,864 | 2,864 |

| Convertible bonds | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Provisions/other LT liabs | 1,542 | 1,830 | 1,955 | 1,972 | 1,972 | 1,972 | 1,972 |

| Total liabilities | 9,102 | 9,118 | 11,330 | 12,302 | 12,412 | 12,582 | 12,781 |

| Share capital | 1,206 | 1,206 | 1,206 | 1,206 | 1,206 | 1,206 | 1,206 |

| Retained earnings | 7,684 | 8,908 | 9,723 | 9,881 | 10,718 | 11,659 | 12,806 |

| Reserves/others | 5,662 | 3,064 | 3,563 | 2,708 | 2,708 | 2,708 | 2,708 |

| Shareholder funds | 14,552 | 13,177 | 14,492 | 13,794 | 14,631 | 15,572 | 16,720 |

| Minorities/other equity | 1,091 | 1,369 | 1,445 | 1,636 | 1,872 | 2,116 | 2,360 |

| Total equity | 15,643 | 14,547 | 15,936 | 15,430 | 16,504 | 17,689 | 19,080 |

| Total liabs & equity | 24,746 | 23,664 | 27,267 | 27,732 | 28,916 | 30,271 | 31,861 |

| Total debt | 3,217 | 2,873 | 4,838 | 5,573 | 5,573 | 5,573 | 5,573 |

| Net debt | (779) | (1,701) | (2,072) | (1,773) | (5,055) | (5,664) | (6,429) |

| Adjusted EV | 44,909 | 44,313 | 43,985 | 44,345 | 41,299 | 40,934 | 40,414 |

| BVPS (NT$) | 120.7 | 109.3 | 120.2 | 114.4 | 121.4 | 129.2 | 138.7 |

Balance sheet ratios

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Key ratios | |||||||

| Current ratio (x) | 2.0 | 2.1 | 2.2 | 2.3 | 2.8 | 2.9 | 3.0 |

| Growth in total assets (% YoY) | (4.6) | (4.4) | 15.2 | 1.7 | 4.3 | 4.7 | 5.3 |

| Growth in capital employed (% YoY) | (14.2) | (13.6) | 7.9 | (1.5) | (16.2) | 5.0 | 5.2 |

| Net debt to operating cashflow (x) | - | - | - | - | - | - | - |

| Gross debt to operating cashflow (x) | 1.7 | 0.9 | 1.7 | 1.7 | 0.9 | 1.3 | 1.2 |

| Gross debt to Ebitda (x) | 1.4 | 0.8 | 1.1 | 1.2 | 1.1 | 1.0 | 0.9 |

| Net debt/Ebitda (x) | - | - | - | - | - | - | - |

| Gearing | |||||||

| Net debt/equity (%) | (5.0) | (11.7) | (13.0) | (11.5) | (30.6) | (32.0) | (33.7) |

| Gross debt/equity (%) | 20.6 | 19.8 | 30.4 | 36.1 | 33.8 | 31.5 | 29.2 |

| Interest cover (x) | 21.5 | 29.1 | 30.2 | 26.5 | 30.4 | 35.1 | 39.3 |

| Debt cover (x) | 0.6 | 1.1 | 0.6 | 0.6 | 1.2 | 0.8 | 0.8 |

| Net cash per share (NT$) | 6.5 | 14.1 | 17.2 | 14.7 | 41.9 | 47.0 | 53.3 |

| Working capital analysis | |||||||

| Inventory days | 63.0 | 71.1 | 65.1 | 70.4 | 71.0 | 70.2 | 70.0 |

| Debtor days | 76.8 | 85.4 | 81.6 | 86.0 | 82.9 | 81.6 | 81.6 |

| Creditor days | 57.3 | 62.6 | 52.8 | 53.7 | 51.3 | 50.8 | 50.6 |

| Working capital/Sales (%) | 20.5 | 21.6 | 23.8 | 23.4 | 23.5 | 23.8 | 24.0 |

| Capital employed analysis | |||||||

| Sales/Capital employed (%) | 148.0 | 160.2 | 165.8 | 169.9 | 213.8 | 221.8 | 229.5 |

| EV/Capital employed (%) | 302.1 | 345.0 | 317.3 | 324.7 | 360.7 | 340.4 | 319.4 |

| Working capital/Capital employed (%) | 30.4 | 34.6 | 39.4 | 39.7 | 50.3 | 52.7 | 55.1 |

| Fixed capital/Capital employed (%) | 37.1 | 45.2 | 42.1 | 42.2 | 50.4 | 48.0 | 45.6 |

| Other ratios (%) | |||||||

| PB (x) | 3.1 | 3.4 | 3.1 | 3.3 | 3.1 | 2.9 | 2.7 |

| EV/Ebitda (x) | 19.2 | 12.2 | 10.2 | 9.6 | 8.2 | 7.1 | 6.3 |

| EV/OCF (x) | 23.4 | 14.2 | 15.7 | 13.2 | 6.3 | 9.5 | 8.9 |

| EV/FCF (x) | 43.1 | 17.2 | 19.2 | 16.3 | 7.6 | 13.6 | 11.7 |

| EV/Sales (x) | 2.0 | 2.2 | 1.9 | 1.9 | 1.7 | 1.5 | 1.4 |

| Capex/depreciation (%) | 171.2 | 85.2 | 69.5 | 82.6 | 136.7 | 150.1 | 118.7 |

Source: SinoPac

Cashflow (NT$m)

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Operating profit | 1,824 | 2,964 | 3,593 | 3,816 | 4,217 | 4,877 | 5,487 |

| Operating adjustments | (83) | (536) | (908) | (1,374) | (1,210) | (1,530) | (1,662) |

| Depreciation/amortisation | 511 | 655 | 734 | 784 | 805 | 866 | 927 |

| Working capital changes | (114) | (171) | (692) | (372) | (340) | (575) | (628) |

| Interest paid / other financial expenses | - | - | - | - | - | - | - |

| Tax paid | - | - | - | - | - | - | - |

| Other non-cash operating items | (222) | 217 | 76 | 512 | 3,081 | 677 | 418 |

| Net operating cashflow | 1,917 | 3,129 | 2,802 | 3,365 | 6,553 | 4,315 | 4,541 |

| Capital expenditure | (874) | (558) | (511) | (648) | (1,100) | (1,300) | (1,100) |

| Free cashflow | 1,042 | 2,571 | 2,291 | 2,718 | 5,453 | 3,015 | 3,441 |

| Acq/inv/disposals | 1,081 | (234) | (134) | (290) | 0 | 0 | 0 |

| Int, invt & associate div | - | - | - | - | - | - | - |

| Net investing cashflow | 206 | (792) | (645) | (938) | (1,100) | (1,300) | (1,100) |

| Increase in loans | (1,113) | (475) | 1,941 | 729 | 0 | 0 | 0 |

| Dividends | (761) | (1,264) | (1,901) | (2,417) | (2,170) | (2,406) | (2,677) |

| Net equity raised/others | (45) | 2 | (75) | (65) | 0 | 0 | 0 |

| Net financing cashflow | (1,919) | (1,737) | (35) | (1,754) | (2,170) | (2,406) | (2,677) |

| Incr/(decr) in net cash | 204 | 600 | 2,122 | 674 | 3,282 | 609 | 764 |

| Exch rate movements | 561 | (22) | 213 | (238) | 0 | 0 | 0 |

| Opening cash | 3,231 | 3,997 | 4,575 | 6,910 | 7,346 | 10,629 | 11,238 |

| Closing cash | 3,997 | 4,575 | 6,910 | 7,346 | 10,629 | 11,238 | 12,002 |

| OCF PS (NT$) | 15.9 | 26.0 | 23.2 | 27.9 | 54.3 | 35.8 | 37.7 |

| FCF PS (NT$) | 8.6 | 21.3 | 19.0 | 22.5 | 45.2 | 25.0 | 28.5 |

Cashflow ratio analysis

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Growth (%) | |||||||

| Op cashflow growth (% YoY) | 1,298.5 | 63.2 | (10.4) | 20.1 | 94.7 | (34.2) | 5.2 |

| FCF growth (% YoY) | - | 146.7 | (10.9) | 18.6 | 100.6 | (44.7) | 14.1 |

| Capex growth (%) | 33.9 | (36.2) | (8.4) | 26.8 | 69.9 | 18.2 | (15.4) |

| Other key ratios (%) | |||||||

| Capex/sales (%) | 4.0 | 2.7 | 2.2 | 2.8 | 4.5 | 4.9 | 3.8 |

| Capex/op cashflow (%) | 45.6 | 17.8 | 18.2 | 19.2 | 16.8 | 30.1 | 24.2 |

| Operating cashflow payout ratio (%) | 62.9 | 57.8 | 81.8 | 64.5 | 36.7 | 62.0 | 67.4 |

| Cashflow payout ratio (%) | 39.7 | 40.4 | 67.9 | 71.8 | 33.1 | 55.8 | 59.0 |

| Free cashflow payout ratio (%) | 73.0 | 49.2 | 83.0 | 88.9 | 39.8 | 79.8 | 77.8 |

DuPont analysis

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Ebit margin (%) | 8.3 | 14.4 | 15.6 | 16.4 | 17.2 | 18.3 | 18.9 |

| Asset turnover (x) | 0.9 | 0.9 | 0.9 | 0.8 | 0.9 | 0.9 | 0.9 |

| Interest burden (x) | 1.3 | 1.1 | 1 | 1 | 1.1 | 1 | 1 |

| Tax burden (x) | 0.8 | 0.8 | 0.7 | 0.7 | 0.7 | 0.7 | 0.7 |

| Return on assets (%) | 5.6 | 9.3 | 10.5 | 10.1 | 10.8 | 11.9 | 12.7 |

| Leverage (x) | 1.6 | 1.6 | 1.7 | 1.8 | 1.8 | 1.7 | 1.7 |

| ROE (%) | 11.7 | 17.5 | 19.4 | 17.3 | 21.2 | 22.2 | 23.7 |

EVA ® analysis

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Ebit adj for tax | 1,425 | 2,242 | 2,665 | 2,781 | 3,059 | 3,511 | 3,951 |

| Average invested capital | 17,328 | 15,310 | 15,024 | 15,420 | 14,155 | 13,338 | 13,940 |

| ROIC (%) | 8.2 | 14.6 | 17.7 | 18.0 | 21.6 | 26.3 | 28.3 |

| Cost of equity (%) | 7.2 | 7.2 | 7.2 | 7.2 | 7.2 | 7.2 | 7.2 |

| Cost of debt (adj for tax) | 3.1 | 3.0 | 3.0 | 2.9 | 2.9 | 2.9 | 2.9 |

| Weighted average cost of capital (%) | 5.8 | 5.8 | 5.8 | 5.8 | 5.8 | 5.8 | 5.8 |

| EVA/IC (%) | 2.4 | 8.8 | 12.0 | 12.3 | 15.9 | 20.6 | 22.6 |

| EVA (NT$m) | 414 | 1,354 | 1,797 | 1,892 | 2,244 | 2,744 | 3,149 |

Source: SinoPac

Research subscriptions

To change your report distribution requirements, please contact your CLSA sales representative or email us at cib@clsa.com. You can also fine-tune your Research Alert email preferences at https:/ /www.clsa.com/member/tools/email_alert/.

Companies mentioned

Nan Pao (4766 TT - NT$372.00 - OUTPERFORM)

Advanced Pao Trusval (N-R)

AEMC (N-R)

Maxell (N-R)

Trusval (N-R)

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_CLSA_南寶4766_20260521_003.png |

60KB | 真資料圖 | 標題「Sales mix by product」堆疊長條圖,橫軸 4Q23 至 1Q26,分 Adhesives(約68-74%)、Coatings & construction(約22-26%)、Others(小比例)三色堆疊,各柱標示百分比 |

報告_CLSA_南寶4766_20260521_006.png |

409KB | 真資料圖 | 標題「Semiconductor manufacturing process」流程示意圖,分 A Wafer dicing、B Package dicing、C Back grinding 三段,圖示 Dicing/Tape mount/Back grinding/Mounting/Molding/Bonding/Pickup 等步驟,右側標示 Design/masking processes、Front-end processes、Back-end processes 分類方框 |