PDF 原檔:報告_BofA_日月光3711_20260707_original.pdf

圖片清單(已驗證 2026-07-13)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_BofA_日月光3711_20260707_001.png |

99KB | 真資料圖 | Exhibit 1:ASE 設備採購與 capex 長條圖(2021-2026),2026 設備採購與 capex 皆創高,右軸設備採購占 capex 比重折線 |

報告_BofA_日月光3711_20260707_002.png |

66KB | 真資料圖 | Exhibit 2:ASE IC ATM 銷售長條圖(2020-2027E)疊加 GM/OpM 折線,2026E/2027E 營收與利潤率同步跳升 |

報告_BofA_日月光3711_20260707_003.png |

61KB | 真資料圖 | Exhibit 3:ASE LEAP 銷售額(US$mn)與 LEAP 占 IC ATM 銷售比重折線(2021-2027E),2027E LEAP 占比達約 36-37% |

報告_BofA_日月光3711_20260707_004.png |

80KB | 真資料圖 | Exhibit 5:ASE LEAP 銷售依子業務別堆疊長條圖(Bumping/oS/Final testing/Full process/Chip-Wafer probing,2024-2028),2026 起 Full process 與 oS process 大幅放量 |

報告_BofA_日月光3711_20260707_005.png |

58KB | 真資料圖 | Exhibit 4:LEAP GMs/Non-LEAP GMs/IC ATM GMs 分季折線圖(1Q23-4Q27E),LEAP 毛利率持續高於 Non-LEAP 並逐季擴大差距 |

報告_BofA_日月光3711_20260707_006.png |

48KB | 真資料圖 | Exhibit 6:ASE Capex/IC ATM 銷售長條圖與資本密度(Capex/IC ATM Sales)折線(2023-2028E),資本密度維持 40%+ |

報告_BofA_日月光3711_20260707_007.png |

50KB | 真資料圖 | Exhibit 7:ASE Capex/Net debt 長條圖與 FCF 折線(2023-2028E),FCF 於 2026-2027E 轉負後 2028E 回升 |

報告_BofA_日月光3711_20260707_008.png |

54KB | 真資料圖 | ASE 普通股(TWD)評等與目標價沿革圖(2023-2026),最新 24-Jun PO NT$750 |

報告_BofA_日月光3711_20260707_009.png |

61KB | 真資料圖 | ASE ADR(US$)評等與目標價沿革圖(2023-2026),最新 24-Jun PO US$48 |

原始內容

ASE Technology Holding

YTD investment tracking ahead of its '26 guide backed by solid AI CPU/ASIC demand

Reiterate Rating: BUY | PO: 750.00 TWD | Price: 679.00 TWD

YTD equipment buys tracks 66% of its '26 capex guidance

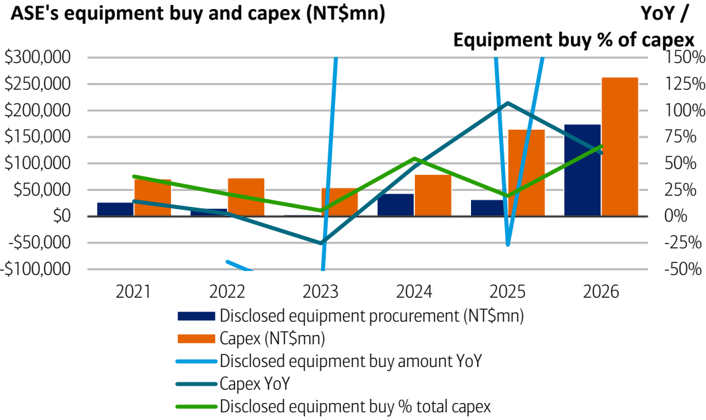

ASE has filed 82 equipment buys and 64 facility construction announcements through early July. While the filing may only capture the major payment, on the like for like basis, the spending on equipment has reached NT$175bn (Exhibit 1), booking 66% of its ' 26 capex guidance of US$8.5bn which is already revised up from the original US$7bn target. Specifically, the equipment mix is skewed toward 2.5D packaging (TSV, metrology, wet cleaning, flux coating, dispensing, molding, grinding, AOI and dicing) and testing (tester & prober). The limited space for further expansion also drove facility and clean room construction contracts to NT$82bn YTD mostly set to complete by 4Q28.

Further capex upside for '26-27 as HPC gains accelerate

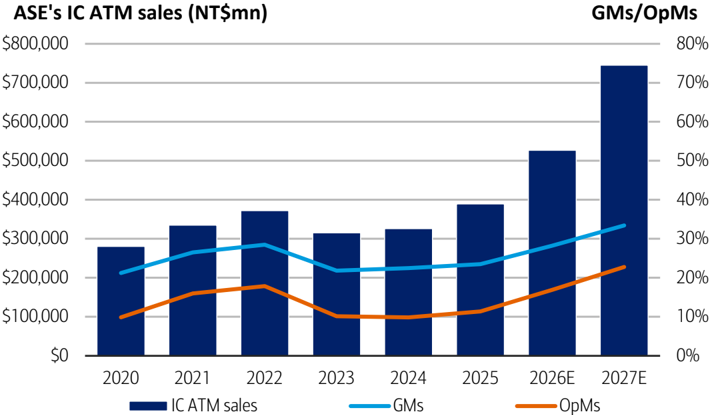

We recently lifted our expectation for ASE capex in ' 26/27 to US$8.5bn/US$12.2bn (vs. US$5.5bn in ' 25) in our CPU manufacturing report, close to TSMC ' s back-end spending, on solid AI demand and foundry outsourcing. With YTD equipment buy tracking stronger, the company might need to further lift its capex to ~US$10bn in ' 26 and US$13-15bn in ' 27, putting the capex/IC ATM sales elevated at 40% through ' 28 (vs 10-yr avg. 20%) to fulfill its customers ' demand. While depreciation could ramp and funding would be required, the high utilization and better packaging/testing pricing should lift its IC ATM sales +34% CAGR from ' 25-28 and expand GMs to 28%/33% in ' 26/27 on mix upgrade.

Improving landscape and EPS upgrades support re-rating

We keep our Buy rating on ASE with NT$750 PO on 20x 2H27-1H28 P/E and maintain EPS for ' 26/27/28 at NT$16/31/41. While the company may need to issue debt or equity in 2H26 to support its aggressive capex plan in 2027-28 for further 2.5D packaging and chip probing capacity expansion, it could secure the customer commitment while ROE from LEAP business at 25-30%+ should justify the cost of capital from the fundraising.

| Estimates (Dec) (NT$) | 2024A | 2025A | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|

| Net Income (Adjusted - mn) | 36,902 | 43,283 | 78,650 | 143,233 | 189,493 |

| EPS | 7.70 | 9.30 | 17.08 | 31.49 | 41.87 |

| EPS Change (YoY) | 4.0% | 20.8% | 83.6% | 84.3% | 33.0% |

| Consensus EPS (Visible Alpha) | 17.12 | 25.92 | 33.64 | ||

| Dividend / Share | 5.30 | 5.70 | 10.60 | 19.60 | 26.10 |

| Free Cash Flow / Share | 2.61 | (5.16) | (17.93) | (33.83) | (19.42) |

| ADR EPS (US$) | 0.480 | 0.597 | 1.07 | 1.97 | 2.62 |

| ADR Dividend / Share (US$) | 0.330 | 0.366 | 0.663 | 1.23 | 1.63 |

| Valuation (Dec) | |||||

| P/E | 88.17x | 73.00x | 39.75x | 21.57x | 16.22x |

| Dividend Yield | 0.781% | 0.839% | 1.56% | 2.89% | 3.84% |

| EV / EBITDA* | 33.96x | 28.45x | 17.89x | 10.82x | 8.03x |

| Free Cash Flow Yield* | 0.372% | -0.739% | -2.60% | -4.92% | -2.83% |

| * For full definitions of iQ method SM measures, see page 9. |

This research report provides general information only. No part of this report may be used or reproduced or quoted in any manner whatsoever in Taiwan by the press or other persons without the express written consent of BofA Securities.

>> Employed by a non-US affiliate of BofAS and is not registered/qualified as a research analyst under the FINRA rules.

Refer to "Other Important Disclosures" for information on certain BofA Securities entities that take responsibility for the information herein in particular jurisdictions.

BofA Securities does and seeks to do business with issuers covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Refer to important disclosures on page 10 to 13. Analyst Certification on page 7. Price

07 July 2026

Equity

Haas Liu >> Research Analyst Merrill Lynch (Taiwan) +886 2 2376 3727 haas.liu@bofa.com

Mike Yang >> Research Analyst Merrill Lynch (Taiwan) mike.c.yang@bofa.com

Cathy Hsu >> Research Analyst Merrill Lynch (Taiwan) cathy.hsu3@bofa.com

Stock Data

| Price (Common / ADR) | 679.00TWD/41.87USD |

|---|---|

| Price Objective | 750.00TWD/48.00USD |

| Date Established | 24-Jun-2026/24-Jun-2026 |

| Investment Opinion | B-1-7 / C-1-7 |

| 52-WeekRange | 141.50TWD-729.00TWD |

| Market Value (mn) | 94,712 USD |

| Market Value (mn) | 3,028,906 TWD |

| Shares Outstanding (mn) | 4,460.8 / 2,230.4 |

| Average Daily Value (mn) | 602.30 USD |

| Free Float | 74.0% |

| BofA Ticker / Exchange | XSRIF / TAI |

| BofA Ticker / Exchange | ASX / NYS |

| Bloomberg / Reuters | 3711 TT / 3711.TW |

| ROE (2026E) | 18.9% |

| Net Dbt to Eqty (Dec-2025A) | 41.5% |

iQ profile SM ASE Technology Holding

| Key Income Statement Data (Dec) | 2024A | 2025A | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|

| (NT$ Millions) | |||||

| Sales | 595,410 | 645,388 | 817,427 | 1,058,162 | 1,268,875 |

| Gross Profit | 96,997 | 114,193 | 180,581 | 284,233 | 361,964 |

| Sell General &Admin Expense | (28,935) | (30,586) | (35,198) | (40,261) | (44,347) |

| Operating Profit | 39,232 | 50,756 | 105,404 | 198,241 | 267,247 |

| Net Interest &Other Income | 2,588 | 545 | (8,386) | (18,813) | (28,541) |

| Associates | NA | NA | NA | NA | NA |

| Pretax Income | 41,820 | 51,301 | 97,018 | 179,429 | 238,706 |

| Tax (expense) / Benefit | (7,756) | (9,460) | (18,536) | (34,159) | (45,545) |

| Net Income (Adjusted) | 36,902 | 43,283 | 78,650 | 143,233 | 189,493 |

| Average Fully Diluted Shares Outstanding | 4,333 | 4,462 | 4,485 | 4,485 | 4,485 |

| Key Cash Flow Statement Data | |||||

| Net Income | 32,620 | 40,658 | 76,281 | 141,221 | 187,784 |

| Depreciation &Amortization | 59,815 | 67,440 | 82,595 | 112,702 | 151,392 |

| Change in Working Capital | (3,706) | (9,449) | (18,597) | (35,616) | (26,978) |

| Deferred Taxation Charge | NA | NA | NA | NA | NA |

| Other Adjustments, Net | 2,058 | 43,600 | 12,956 | 0 | 0 |

| Cash Flow from Operations | 90,788 | 142,249 | 153,235 | 218,307 | 312,198 |

| Capital Expenditure | (79,522) | (164,643) | (232,007) | (367,200) | (397,800) |

| (Acquisition) / Disposal of Investments | 1 | (1,971) | 6,809 | 1,719 | (178) |

| Other Cash Inflow / (Outflow) | (4,387) | 969 | 303 | 0 | 0 |

| Cash Flow from Investing | (83,909) | (165,644) | (224,895) | (365,481) | (397,978) |

| Shares Issue / (Repurchase) | 1,103 | 3,480 | 1,101 | 0 | 0 |

| Cost of Dividends Paid | (22,459) | (23,034) | (25,208) | (47,294) | (87,557) |

| Cash Flow from Financing | (7,271) | 45,269 | 82,427 | 100,683 | 40,133 |

| Free Cash Flow | 11,266 | (22,393) | (78,772) | (148,893) | (85,602) |

| Net Debt | 109,225 | 155,020 | 230,345 | 426,532 | 599,691 |

| Change in Net Debt | 20,146 | 61,690 | 92,259 | 194,468 | 173,337 |

| Key Balance Sheet Data | |||||

| Property, Plant &Equipment | 312,531 | 421,115 | 607,662 | 916,273 | 1,243,302 |

| Other Non-Current Assets | 152,881 | 154,423 | 176,572 | 196,189 | 219,926 |

| Trade Receivables | 113,420 | 125,042 | 146,820 | 193,083 | 228,140 |

| Cash &Equivalents | 84,883 | 100,223 | 124,483 | 76,273 | 30,804 |

| Other Current Assets | 76,982 | 88,530 | 93,482 | 106,849 | 119,253 |

| Total Assets | 740,698 | 889,333 | 1,149,018 | 1,488,667 | 1,841,425 |

| Long-Term Debt | 140,237 | 214,510 | 311,574 | 461,574 | 591,574 |

| Other Non-Current Liabilities | 23,735 | 57,108 | 80,308 | 80,308 | 80,308 |

| Short-Term Debt | 53,872 | 40,734 | 43,254 | 41,231 | 38,921 |

| Other Current Liabilities | 177,068 | 203,615 | 200,235 | 222,809 | 237,372 |

| Total Liabilities | 394,911 | 515,966 | 635,370 | 805,922 | 948,175 |

| Total Equity | 345,787 | 373,368 | 513,647 | 682,745 | 893,250 |

| Total Equity &Liabilities | 740,698 | 889,333 | 1,149,018 | 1,488,667 | 1,841,425 |

| iQ method SM - Bus Performance* | |||||

| Return On Capital Employed | 6.2% | 6.9% | 10.6% | 14.6% | 15.2% |

| Return On Equity | 11.9% | 12.9% | 18.9% | 25.2% | 25.0% |

| Operating Margin | 6.6% | 7.9% | 12.9% | 18.7% | 21.1% |

| EBITDA Margin | 16.6% | 18.3% | 23.0% | 29.4% | 33.0% |

| iQ method SM - Quality of Earnings* | |||||

| Cash Realization Ratio | 2.5x | 3.3x | 1.9x | 1.5x | 1.6x |

| Asset Replacement Ratio | 1.4x | 2.6x | 2.9x | 3.4x | 2.7x |

| Tax Rate (Reported) | 18.5% | 18.4% | 19.1% | 19.0% | 19.1% |

| Net Debt-to-Equity Ratio | 31.6% | 41.5% | 44.8% | 62.5% | 67.1% |

| Interest Cover | 5.8x | 6.8x | 8.0x | 10.1x | 10.0x |

Key Metrics

- For full definitions of iQ method SM measures, see page 9.

Company Sector

Semiconductors

Company Description

Established in 1984 and headquartered in Taiwan, ASE Technology Holding is the no.1 outsourced assembly and testing (OSAT) firm globally, in terms of market share by revenue. ASE acquired Siliconware Precision (SPIL) in 2018, and had acquired USI in 2010, which became its EMS business segment providing synergies in system-level packaging. 2 shares = 1 ADR.

Investment Rationale

We rate ASE Buy, factoring in the company's opportunity in advanced packaging and testing evidenced in TSMC's outsourcing and its own heavy capex investment. The strategy shift should allow the company to capture fast growing addressable market in high performance computing applications and improves its margins. ASE could maintain its leading position in the Outsourced Semiconductor Assembly and Test (OSAT) universe, owing to its well-established footprints and widespread service offerings.

| Stock Data | |

|---|---|

| Shares / ADR | 2.00 |

| Price to Book Value | 6.2x |

Focus charts and tables

Exhibit 1: ASE's equipment buy YTD vs. capex trend

ASE's spend on equipment through early July is already tracking 66% of its full year capex guide in '26

Source: BofA Global Research estimates

Exhibit 2: ASE IC ATM revenue and GMs/OpMs

ASE's LEAP business to drive GM expansion to 34% in 2028

Source: BofA Global Research estimates

BofA GLOBAL RESEARCH

BofA GLOBAL RESEARCH

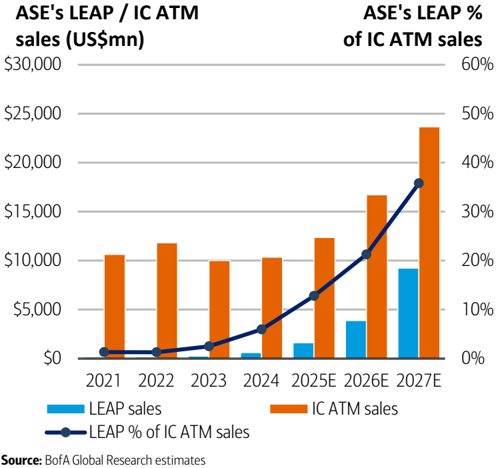

Exhibit 3: ASE LEAP/IC ATM revenue

LEAP will account for 37% of IC ATM sales in 2028

Source: BofA Global Research estimates

BofA GLOBAL RESEARCH

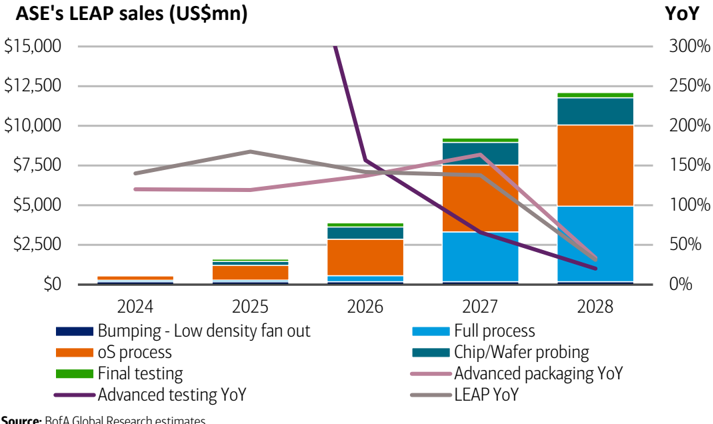

Exhibit 5: ASE LEAP sales by subsegments and YoY

ASE's full process packaging will see strong ramp from 2H26

BofA GLOBAL RESEARCH

Source: BofA Global Research estimates

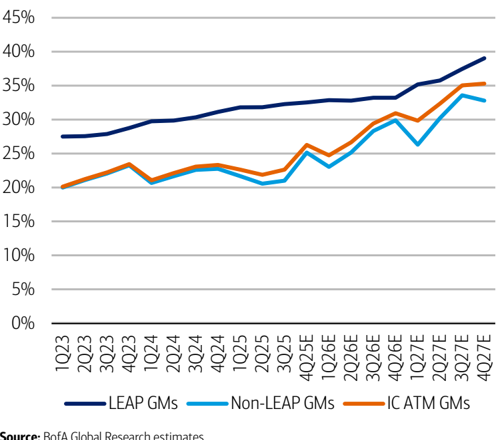

Exhibit 4: ASE LEAP/non-LEAP/IC ATM GMs

LEAP is margin accretive to IC ATM business

ASE's LEAP/Non-LEAP/IC ATM GMs

Source: BofA Global Research estimates

BofA GLOBAL RESEARCH

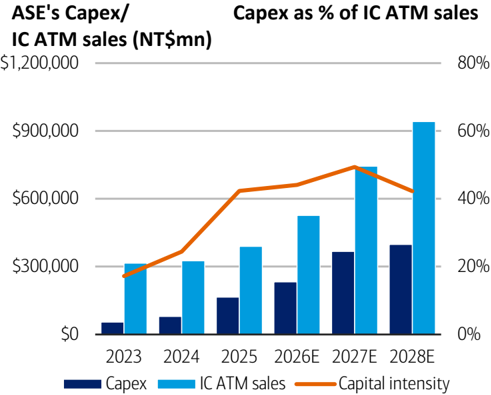

Exhibit 6: ASE Capex and IC TAM sales

ASE Capex as % of IC ATM sales remains above 40%

Source: BofA Global Research estimates

Exhibit 45: Terms and definitions

Glossary of abbreviations/acronyms

Term Definition

AI

Artificial Intelligence

AMD

Advanced Micro Devices

AOI

Automated Optical Inspection

API

Application Programming Interface

ASIC

Application Specific Integrated Circuit

ATC

Active Thermal Control

CoPoS

Chip-on-Panel-on-Substrate

CoWoS

Chip-on-Wafer-on-Substrate

CoWoS-L

Chip-on-Wafer-on-Substrate-Local Silicon Bridge

CPO

Co-Packaged Optics

CPU

Central Processing Unit

DC

Datacenter

EFB

Enhanced Fan-out Bridge

FoCoS

Fan-Out Chip on Substrate

FOPoP

Fan-Out Package on Package

FOSiP

Fan-Out System-in-Package

FT

Final test

GPU

Graphic Processing Unit

HBM

High Bandwidth Memory

HPC

High-Performance Computing

I/O

Input/Output

IaaS

Infrastructure as a Service

IC ATM

IC Assembly, Testing, and Material

IDM

Integrated Device Manufacturer

LEAP

Leading-Edge Advanced Packaging

MCL

Micro channel lid

MPU

Microprocessor Unit

NB

NoteBook

OSAT

Outsourced Semiconductor Assembly/Testing

PC

Personal Computer

RDL

Redistribution Layer

SLT

System level test

SoC

System on Chip

SoIC

System on Integrated Chips

SoIC-MH

System-on-Integrated-Chips-Molding-Horizontal

SWIFT

Silicon Wafer Integrated Fan-out Technology

BofA GLOBAL RESEARCH

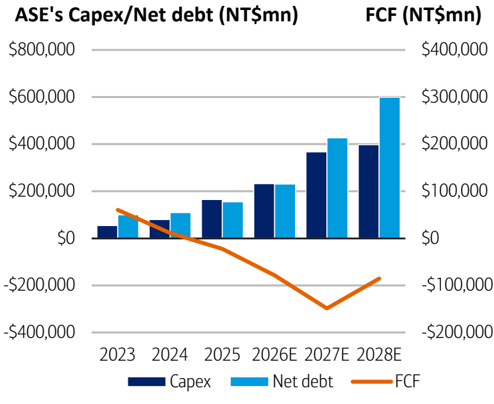

Exhibit 7: ASE Capex/Net debt/FCF

ASE needs debt to support Capex expansion

Source: BofA Global Research estimates

BofA GLOBAL RESEARCH

Exhibit 45: Terms and definitions

Glossary of abbreviations/acronyms

Term

Definition

TAM

Total Addressable Market

TPU

Tensor Processing Unit

WMCM

Wafer-level-multi-chip-module

WPM

Wafer per month

WPY

Wafer per year

XPU

Accelerating Processing Unit

Source:

BofA Global Research estimates

BofA GLOBAL RESEARCH

Price objective basis & risk

ASE Technology Holding (XSRIF / ASX)

We value ASE Technology Holding at NT$750 per share (US$48 for ADR), based on 20x 2H27-1H28E P/E, above its historical range of 5-26x, in view of its solidified industry position in AI era. We use P/E ratio to value ASE as the company has been able to maintain healthy profitability through the cycles in the past 20 years due to consolidating industry landscape supporting a more benign supply/demand and keeping pricing and margins less cyclical.

Downside risks to our PO are 1) share loss and/or ASP erosion owing to Chinese players' cannibalization and/or ASE's worsening execution, 2) weakening end demand due to uncontrollable matters, such as macro halt and/or geopolitical tensions, 3) regulatory issues that could hinder ASE from generating synergies and benefit its competitors.