PDF 原檔:報告_GS_ABF載板_20260712_original.pdf

圖片清單(已驗證 2026-07-13)

公司代號對照:NYPCB=8046_南電(市)、Unimicron=3037_欣興(市)、Kinsus=3189_景碩(市)、ZDT(Zhen Ding)=4958_臻鼎科技(市)(本次 ingest 範圍外,僅供對照)。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_GS_ABF載板_20260712_001.png |

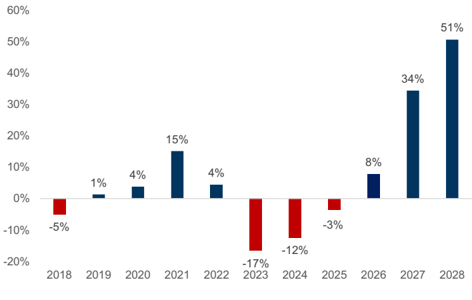

18.9KB | 真資料圖 | ABF 供需缺口率長條圖 2018-2028E(紅=供過於求、藍=供不應求;2028E 缺口 51%) |

報告_GS_ABF載板_20260712_002.png |

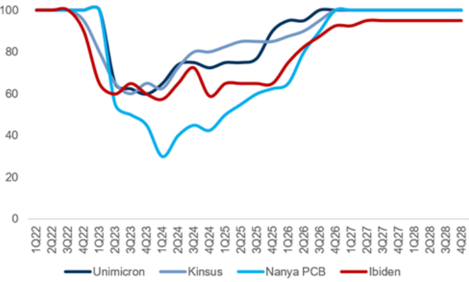

50.6KB | 真資料圖 | Unimicron/Kinsus/Nanya PCB/Ibiden 稼動率(UTR)趨勢線圖 1Q22-4Q28 |

報告_GS_ABF載板_20260712_003.png |

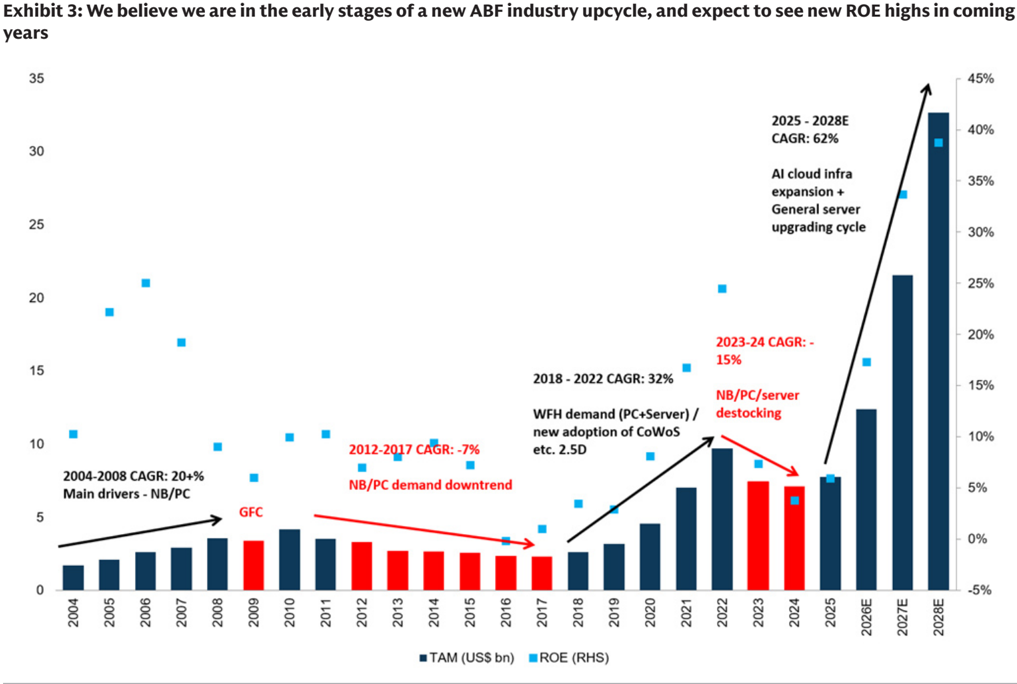

199.7KB | 真資料圖 | Exhibit 3:ABF TAM 歷年+預估長條圖疊 ROE 散點圖 2004-2028E,標示各週期 CAGR 與驅動因素 |

報告_GS_ABF載板_20260712_004.png |

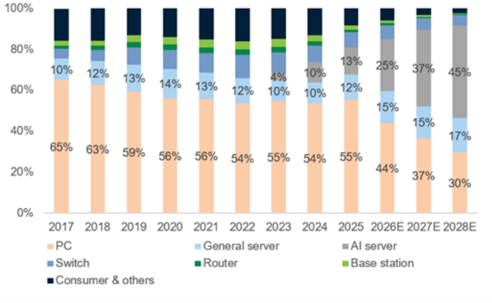

51.7KB | 真資料圖 | ABF 需求依應用別堆疊長條圖 2017-2028E(PC/一般伺服器/AI 伺服器/交換器/路由器/消費性) |

報告_GS_ABF載板_20260712_005.png |

17.7KB | 真資料圖 | AI 伺服器/一般伺服器/交換器/PC 別 2025-28E CAGR 長條圖 |

報告_GS_ABF載板_20260712_006.png |

50.9KB | 真資料圖 | 與 002 相同之 UTR 趨勢線圖(Exhibit 6 重複引用) |

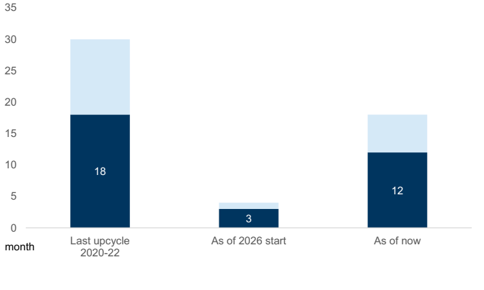

報告_GS_ABF載板_20260712_007.png |

10.6KB | 真資料圖 | ABF 交期長條圖:上輪週期 2020-22(18 個月)/2026 年初(3 個月)/現在(12 個月) |

報告_GS_ABF載板_20260712_008.png |

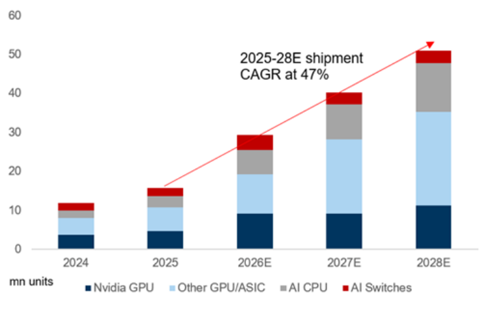

27.8KB | 真資料圖 | AI 晶片出貨量依類型堆疊長條圖 2024-2028E(Nvidia GPU/其他 GPU-ASIC/AI CPU/AI 交換器) |

報告_GS_ABF載板_20260712_009.png |

47.7KB | 真資料圖 | Exhibit 10:AI 晶片出貨 YoY vs AI ABF 需求 YoY 對比長條圖 2025-2028E |

報告_GS_ABF載板_20260712_010.png |

39.5KB | 真資料圖 | 一般伺服器 CPU 出貨依廠商堆疊長條圖 2020-2028E(Intel/AMD/ARM) |

報告_GS_ABF載板_20260712_011.png |

30.5KB | 真資料圖 | CPU 出貨 YoY vs 一般伺服器 ABF 需求 YoY 對比長條圖 |

報告_GS_ABF載板_20260712_012.png |

34.4KB | 真資料圖 | 全球 ABF 供應商市占率堆疊長條圖 2020-2028E(Unimicron/Kinsus/Nanya PCB/Zhen Ding/Ibiden/SEMCO/Others) |

報告_GS_ABF載板_20260712_013.png |

73.0KB | 真資料圖 | ABF 供應商合計資本支出堆疊長條圖+YoY 折線 2020-2028E |

報告_GS_ABF載板_20260712_014.png |

28.7KB | 真資料圖 | Exhibit 16:AI IC substrate TAM 成長長條圖 2023-2028E |

報告_GS_ABF載板_20260712_015.png |

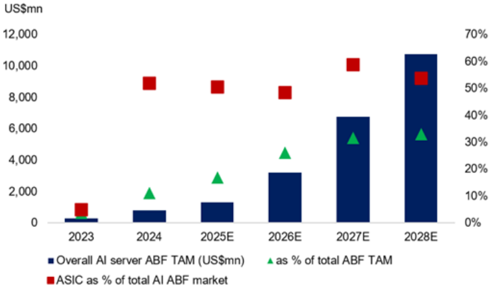

35.5KB | 真資料圖 | AI 伺服器 ABF TAM 長條圖疊 ASIC 占比標記 2023-2028E |

報告_GS_ABF載板_20260712_016.png |

27.4KB | 真資料圖 | Exhibit 18:Kinsus AI ABF 營收占比長條圖(Unimicron/NYPCB/Kinsus AI 營收占比走勢) |

報告_GS_ABF載板_20260712_017.png |

38.5KB | 真資料圖 | Exhibit 19:AI ABF substrate 市占率堆疊長條圖 2024-2028E(Unimicron/NYPCB/Kinsus/Others) |

報告_GS_ABF載板_20260712_018.png |

296.4KB | 真資料圖 | Exhibit 20:各公司 OPM 歷史趨勢線圖 2004-2029E(NYPCB/Kinsus/Unimicron/Zhen Ding/Ibiden/SEMCO),標註各景氣週期驅動因素 |

報告_GS_ABF載板_20260712_019.png |

56.0KB | 真資料圖 | 2028 AI ABF TAM 瀑布圖(舊估→NVIDIA AI GPU 出貨增量→AI ASIC substrate 出貨→組合變化→新估 10,754) |

報告_GS_ABF載板_20260712_020.png |

110.6KB | 真資料圖 | Exhibit 22:台灣四大 ABF 廠季度毛利率趨勢線圖 1Q20-3Q28E(NYPCB/Kinsus/Unimicron/Zhen Ding) |

報告_GS_ABF載板_20260712_021.png |

76.7KB | 真資料圖 | Zhen Ding(4958.TW)GS 評等與目標價沿革圖(股價/指數雙軸,2023-2026) |

報告_GS_ABF載板_20260712_022.png |

78.6KB | 真資料圖 | NYPCB(8046.TW)GS 評等與目標價沿革圖(股價/指數雙軸,2023-2026),最新目標價 1,115 |

報告_GS_ABF載板_20260712_023.png |

81.5KB | 真資料圖 | Unimicron Technology(3037.TW)GS 評等與目標價沿革圖(股價/指數雙軸,2023-2026),最新目標價 630 |

報告_GS_ABF載板_20260712_024.png |

87.2KB | 真資料圖 | Kinsus(3189.TW)GS 評等與目標價沿革圖(股價/指數雙軸,2023-2026),最新目標價 555 |

全數 24 張皆為報告內產業/公司數據圖表,無 logo/封面/文字卡。

原始內容

ASIA TECHNOLOGY

ABF price hikes to outpace our estimates, with solid GM expansion from 2Q26; revise up TPs for all our TW ABF substrate players by 81% to 112%

Following up on our ABF upgrade report from early this year (see here), we are seeing ABF substrate demand grow much faster than our original expectation. We now expect the ABF TAM to expand at a 62% 2025-28E CAGR to US$33bn in 2028, up from US$7.7bn in 2025 (Exhibit 3, vs. our prior estimate of a 33% CAGR) . Moreover, we expect the S/D gap for ABF substrates to widen from an 8% undersupply in 2026 to 34/51% in 2027/28 (Exhibit 1 vs. 5%/21%/42% undersupply in 2026/27/28 previously) , driven by stronger than expected demand from AI servers and general server CPU substrates, which together accounted for 26% of ABF industry demand in 2025, and should increase to 41/53/62% of demand in 2026/27/28; Exhibit 4). As a result, we expect the ABF substrate LTA/Spot prices to increase by 10-15%/20%+ QoQ per quarter from 3Q26 through at least the end of 2027, with shortages likely extending into 2028 or possibly beyond as ABF lead times have lengthened from 3-4 months at the start of the year to more than 12 months currently.

Given our bullish view on the ABF substrate pricing/pro fi tability outlook, we raise our TPs for NYPCB/Kinsus/Unimicron/ZDT to NT$2,310/1,120/1,140/824 from NT$1,115/555/630/388 with 4-22%/10-38% upward earnings revisions in 2027/28 and introduce our 2029 earnings estimates. Maintain our Buy rating on NYPCB (on CL)/Kinsus/ZDT, but stay Neutral on Unimicron.

ABF substrates could become a key bottleneck for the overall AI/server industry, supporting a solid price hike outlook

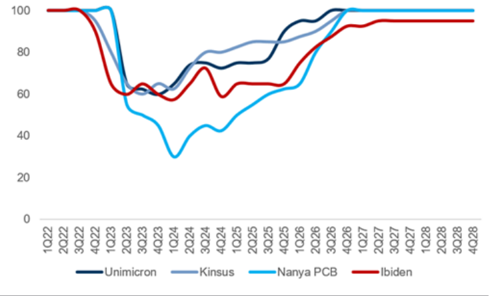

We began to see NYPCB/Kinsus UTR pick up rapidly (Exhibit 2) in 1H26, following Ibiden's nearly full utilization for GPU applications from 2H24 and Unimicron's full utilization from 2H25, and started seeing spot price hikes from April, which implies that shortages of substrate supply likely began much earlier than our original expectation, as we had expected them to emerge only from 2H26, thanks to the stronger than anticipated demand.

Our latest industry checks suggest that the ABF substrate lead times have now reached 12 months (vs. only 3-4 months as of early 2026), with more customers asking for ABF substrate capacity beyond 2029. Moreover, we started to see some tier 2/3 ABF substrate suppliers selling their on-hand capacity based on bidding, suggesting a much more favorable pricing/pro fi tability outlook for the spot price for

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi ed as research analysts with FINRA in the U.S.

Chao Wang

+886(2)2730-4195 | kuanchao.wang@gs.com Goldman Sachs (Asia) L.L.C., Taipei Branch

Daiki Takayama

+81(3)4587-9870 | daiki.takayama@gs.com Goldman Sachs Japan Co., Ltd.

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Al Wang

+886(2)2730-4081 | al.wang@gs.com Goldman Sachs (Asia) L.L.C., Taipei Branch c45a43530f604d12bcb9a82b5aa6b9f6

ABF substrate suppliers.

All the above industry signs and data-point suggests to us that the ABF substrate shortage could last for more than 30 months, and our supply demand analysis suggests the shortage ratio of ABF substrates could reach 14%/34%/51% in 2H26/2027/2028, indicating potential for an even faster pace of price increases for ABF substrates. We expect the market to eventually recognize that substrate supply constraints could impact the overall AI server ramp up speed. Overall, we expect substrate LTA/spot prices to increase 10-15%/20%+ QoQ from 3Q26 through to the end of 2027, suggesting a solid upside potential to our GM estimate for all 4 ABF substrate players in Taiwan.

AI ASIC servers and general server CPUs are the key drivers of stronger than expected demand growth

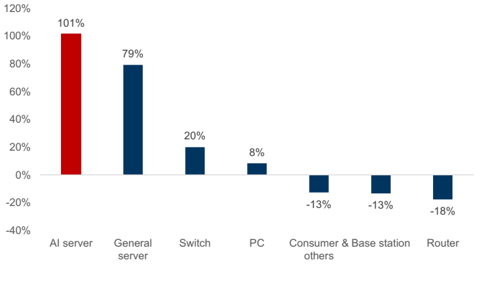

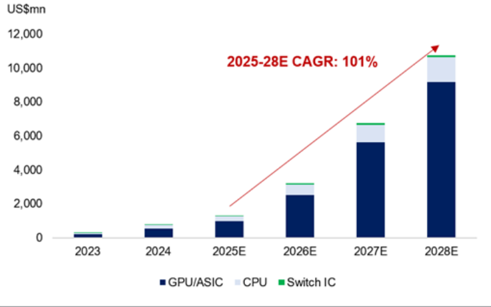

We now see the overall ABF substrate TAM expanding at a 62% 2025-28E CAGR vs. our original expectation of a 33% 2025-28E CAGR, with the stronger than expected demand growth mainly driven by (1) the stronger than expected AI ASIC substrate volume/pricing growth, and (2) much more favorable than expected server CPU substrate demand growth. We expect AI server demand (25% of ABF demand in 2026E) to grow at a 101% 2025-28E CAGR, bene fi ting Ibiden/Unimicron the most, as the two companies together still account for 74% of the AI server share in 2026. We also expect general server demand (15% of ABF demand in 2026E) to grow at a 47% 2025-28E CAGR, bene fi ting Kinsus the most, as server CPUs could account for 40%+ of the company's total ABF revenue in 2028, thanks to rising demand for high computing performance ICs and IC substrate technology migration.

For the other applications, we expect switches to grow the fastest, at a 20% 2025-28E CAGR, driven by solid expansion in ABF substrate size and layer count following the adoption of 1.6T/3.2T switch ICs starting in 2H26/2028. This should bene fi t NYPCB the most given the company's current 40%+ ABF revenue exposure to high-end networking ICs.

2Q26 preview and 3Q26 outlook: Spot price player to strongly outperform with a signi fi cant jump in GM/OPM

For the upcoming 2Q results, we believe all four TW ABF substrate companies will report better than expected earnings, 4-38% above BBG consensus , mainly driven by much stronger ABF substrate shipment volumes and better ASP/pricing. We also expect key spot price supplier, NYPCB, to enjoy the strongest GM/OPM expansion, from 15.8%/12.1% in 1Q26 to 26.3%/23.2% in 2Q26 (vs. consensus of 19.8%/17.5%) , supported by the 40%+ spot price hikes in 2Q26.

Going into 3Q, we expect all four TW ABF substrate suppliers to deliver even stronger earnings growth, while our 3Q26 operating income estimates for all 4 ABF substrate suppliers are 9-53% above BBG consensus . We expect the 4 TW ABF players' GM/OPM to expand by 3.5ppt/4.7ppt in 3Q26 , considering the even more positive ABF substrate ASP/price hike trend from 3Q26. For NYPCB, we believe GM/OPM will again expand the most in 3Q26, by +6.7ppt/+7.2ppt GM/OPM QoQ , further supported by our more favorable ABF substrate spot price outlook.

c45a43530f604d12bcb9a82b5aa6b9f6

100

80

60

40

20

0

ABF substrate supply/demand gap to widen to 14%/34%/51% in 2H26/2027/2028, with a much stronger pricing outlook

1Q24

— Unimicron

—Kinsus

We revise up our ABF substrate TAM 2025-28E CAGR from 33% to 62%, driven by (1) our faster than expected AI IC substrate demand outlook, mainly from ASIC volume growth, as well as solid progress on speci fi cation upgrades, and (2) solid demand for agentic AI server CPUs. We also see NVDA's launch of the new Vera standalone rack suggesting further upside demand potential for server CPU substrate suppliers in the coming years.

On the other hand, we are starting to see all ABF substrate players' capacity located in Japan/Korea/Taiwan become fully utilized, thanks to the solid demand outlook and the comparatively slower capacity expansion plans from key suppliers. Also, we have started to see ABF substrate lead times reach 12+ months currently vs. 3-4 months at the beginning of this year, which further echos our view on the solid demand growth since 2Q25.

As such, we now expect the overall ABF substrate supply/demand gap to reach 8/34/51% in 2026/27/28 (vs. our original expectation at 5%/21%/42%), while we see the faster than expected demand ramp up from April 2026, creating a supply shortage 1 quarter ahead of our estimate-we originally expected a shortage to begin in 2H26, with spot price product pricing hikes, but the shortage actually started in early 2Q26. The ABF substrate supply shortage beginning from April this year has directly led to a 40-60% pricing increase in the spot price market in 2Q26. We believe the pricing outlook for spot ABF substrates may accelerate in 2H26, as the shortage ratio likely rises further from 2% in 1H26 to 14% in 2H26E. Heading into 2027/28, we believe ABF substrate supply could be the IC supply chain bottleneck, potentially suggesting an even stronger pricing outlook for ABF substrates, as most all AI related customers have been focusing more on time to market timing than cost control. Accordingly, we believe the spot price of ABF substrates is poised to rise further by 60-80% YoY in both 2027 and 2028.

Exhibit 1: We expect the ABF industry S/D gap to continue expanding in coming years Supply shortage ratio

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 2: We believe the ABF substrate industry UTR will continue trending up in 2H26 and reach full UTR

Source: Company data, Goldman Sachs Global Investment Research

c45a43530f604d12bcb9a82b5aa6b9f6

years

35

30

25

20

15

10

5

2004

2025 - 2028E

CAGR: 62%

- 40%

Source: Company data, Goldman Sachs Global Investment Research

Demand update: AI servers and server CPUs are the key drivers the ABF substrate demand

We expect ABF substrate TAM to reach US$33bn by 2028, up from US$7.7bn in 2025, implying a 62% 2025-28E CAGR (vs. our prior 33% estimate). Our upward revision is mainly due to (1) strong AI ABF substrate demand, driven primarily by a stronger ASIC substrate volume/price growth than we had expected, and (2) solid demand from general server CPUs, driven by agentic AI. We expect AI servers/general servers to account for 45%/17% of total 2028E demand, up from 13/12% in 2025 (Exhibit 4), and expect AI servers/general server ABF demand to grow at a 101/47% 2025-28E CAGR (Exhibit 5).

c45a43530f604d12bcb9a82b5aa6b9f6

ion|

100%

100

80%

80

60%

60

40%

40

-18%

20%

20

Router

0%

0

4%

10%

25%

37%

45%

Exhibit 4: ABF demand by application - AI server contribution continues to increase 15%

65% 63% 59% 56% 56% 54% 55% 54%

•PC

• Switch

• Consumer & others

55%

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 5: AI servers to see strong 2025-28E demand growth, with a CAGR of 101%, followed by general servers at 79%

Source: Company data, Goldman Sachs Global Investment Research

The substrate supply shortage started much earlier than our original expectation (we had expected that shortages would only start from 2H26), which is re fl ected in (1) increasing UTR, as NYPCB and Kinsus have already seen their UTRs trend up in 1H26, and we expect all major ABF suppliers to operate at full UTR from 2H26 through at least 2028; and (2) lengthening lead times, which have now extended to 12+ months, vs. 3-4 months in early 2026, and are likely to move closer to the 18-30 months range observed during the previous upcycle in 2020-22.

Exhibit 6: We believe the ABF substrate industry UTR will continue trending up in 2H26 and reach full UTR

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 7: ABF substrate lead times have now reached 12+ months vs. 3-4 months at the start of 2026

Lead time lower end and upper end

Source: Company data, Goldman Sachs Global Investment Research

We continue to see higher layer counts and larger body sizes for ABF substrates used in general server CPUs and AI chips, resulting in higher ABF area consumption per package. The ABF speci fi cation upgrade for general server CPUs is relatively moderate, and we expect a 30%+ increase in ABF area consumption for the next generation of Intel/AMD CPUs. However, we expect AI GPU's ABF area consumption to increase the most signi fi cantly. For example, we expect Nvidia's Rubin GPU to consume 123% more ABF area compared with the current Blackwell GPU, while the corresponding AI CPU is expected to see a 47% increase in ABF area consumption when comparing Nvidia's Vera and Grace CPUs. Current ASIC and switch platform upgrades also imply more ABF area consumption, but we expect their increase to fall behind that of AI GPUs.

17%

13%

44%

c45a43530f604d12bcb9a82b5aa6b9f6

LULS LOT

Cambro. nigel dor dred consumpton unver by moms layer count anu largel bouy size

60

Company

50

Intel

40

AMD

30

Nvidia

20

10

Nvidia

Type

Server CPU

Chip

Eagle Stream

Birch Stream outpace sipments growul tor

160%

Layer count Length (mm)

16

100.0

2025-28E shipment

Oak Stream

18

140%

20

104.5

109.2

Width (mm) Body size (mm') ABF area consumption

56.5

70.5

88.0

5,650

145%

7,367

9,606

CAGR at 47%

120%

Exhibit 8: Higher ABF area consumption driven by rising layer count and larger body size

2024

mn units

Amazon

Broadcom

90,400

192,129

132,611

97,718

| Venice | 20 80.1 | 83.8 80% 66% | 6,711 | 134,224 59% | |||

|---|---|---|---|---|---|---|---|

| AI CPU | Grace | 14 | 68.0 | 73.0 60% | 4,964 | 69,496 | |

| Vera | 18 14 | 76.0 | 75.0 40% | 5,700 | 102,600 | ||

| Hopper | 60.0 | 55.0 70.0 | 3,300 | 46,200 | |||

| AI GPU | Blackwell | 16 80.0 | 20% | 5,600 | 89,600 | ||

| Rubin | 20 100.0 | 100.0 0% | 10,000 | 200,000 | |||

| ASIC 2025 | Trainium 2 2026E | 2027E | 14 87.5 2028E | 72.5 2025 | 6,344 2026E | 2027E | 88,813 2028E |

| Trainium 3 | • Nvidia GPU Other GPU/ASIC AI CPU #Al Switches | 16 100.0 | 87.5 | 8,750 • Al chip shipment YoY | •AI ABF demand YoY | 140,000 | |

| Trainium 4 | 18 120.0 | 100.0 | 12,000 | 216,000 | |||

| Tomahawk 4 | 12 77.5 | 77.5 | 6,006 | 72,075 | |||

| Switch | Tomahawk 5 | 16 87.5 | 87.5 | 7,656 | 122,500 | ||

| Tomahawk 6 | 18 | 110.0 | 120.0 | 13.200 | 237,600 |

Source: Company data, Goldman Sachs Global Investment Research

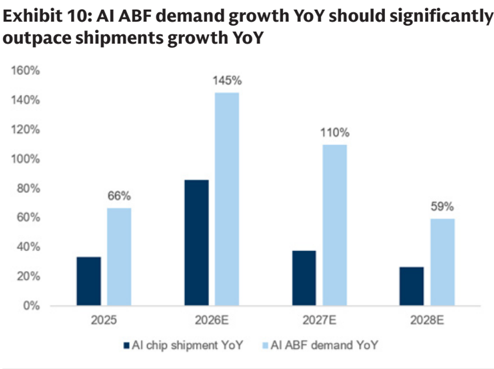

We expect AI ABF demand to grow at a 101% 2025-28E CAGR and account for 45% of total ABF demand by 2028, up from 13% in 2025, supported by strong shipment growth across all AI chips, especially for ASICs. For Nvidia GPUs, ABF demand growth is increasing driven by higher ABF content per chip, outpacing that of other AI chips. While we also expect increasing ABF content per chip for ASICs, ABF demand growth from ASICs over 2025-28E will likely be driven more by shipment volume growth, at a 58% 2025-28E CAGR. For AI CPUs, we also see NVDA's launch of the new Vera standalone rack implying more demand upside for AI CPU shipments. Overall, the increasing ABF area consumption for next gen AI chips should continue to drive overall ABF demand, and we expect AI ABF demand YoY growth to outpace AI chip shipment YoY growth in 2025-28E (Exhibit 10).

Exhibit 9: AI chip shipments to grow at a 47% CAGR from 2025-28E

Source: Company data, Goldman Sachs Global Investment Research

Source: Company data, Goldman Sachs Global Investment Research

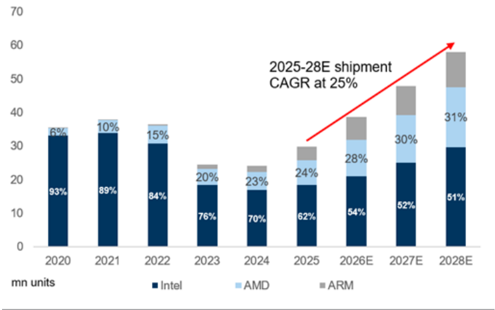

We expect general server CPU ABF demand to grow at a 47% 2025-28E CAGR and account for 17% of total ABF demand by 2028, up from 12% in 2025, with stable CPU shipments growing at a 25% 2025-28E CAGR. General server CPU demand is primarily driven by the growing adoption of agentic AI, which we could see lasting for another 3-5 years. As agentic AI applications become mainstream, we expect the GPU/CPU attach rates to move from 2x to 1.1-1.4x over time, implying that each GPU deployment will

97,718

110%

c45a43530f604d12bcb9a82b5aa6b9f6

Touciale colo chun Tune 405

70

60

50

40

30

20

10

2020

mn units

6%

93%

10%

89%

15%

84%

20%

76%

2025-28E shipment

23%

50%

43%

require more CPUs (see GS analyst Jim Schneider's Intel initiation). We expect a modest increase in ABF area consumption for general server CPUs compared with AI chips, with ABF area consumption increasing by 30%+ for next generation of Intel/AMD CPUs. As a result, we continue to expect general server CPU ABF demand YoY growth to outpace general server CPU shipments YoY in 2025-28E (Exhibit 12).

70%

62%

Exhibit 11: General server CPU shipments to grow at a moderate 25% CAGR from 2025-28E

Source: Company data, Goldman Sachs Global Investment Research

27%

Exhibit 12: General server ABF demand YoY will continue to outpace shipments YoY

Source: Company data, Goldman Sachs Global Investment Research

Supply update: We expect ABF suppliers will start to announce more CAPEX plans in coming quarters, although new capacity will likely only come online after 2H28 Compared with our previous ABF report update, we have seen some Taiwan ABF suppliers revise up their 2026 CAPEX plans since then: ZDT raised its plan from NT$50bn to NT$80bn in April and Unimicron raised theirs from NT$25bn to NT$34bn on their 1Q26 results call). Considering ongoing upgrades in ABF substrate speci fi cations (including higher layer count, larger body size, etc.) and ABF suppliers continuing to invest in technology upgrades to support next generation packaging (including CoPoS, glass substrate, EMIB-T, etc.), customers are requesting more long-term capacity, with some already requesting capacity beyond 2029. As a result, we expect ABF suppliers to announce additional CAPEX plans over the coming quarters/years to support sustained demand growth.

However, ABF substrate capacity volume will continue to decline as packaging body sizes increase and layer counts rise. This capacity ine ffi ciency is driven by increasing production complexity associated with more advanced substrate designs; hence, we expect existing capacity e ffi ciency to continue declining by ~10% annually if speci fi cation upgrades continue at their current pace.

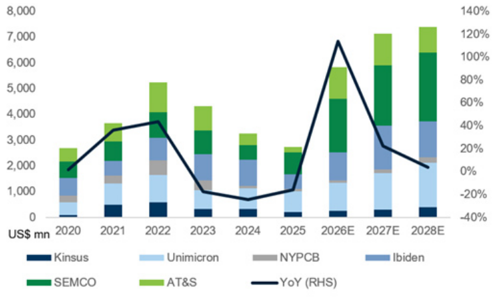

We expect overall ABF supply to reach a 15% CAGR in 2025-28E (Exhibit 14), supported by elevated CAPEX plans across the major ABF suppliers growing at 40% CAGR in 2025-28E (Exhibit 13). The current pace of capacity expansion is tracking behind CAPEX increases mainly due to (1) long equipment lead times, with some newly announced capacity becoming available only after 2028 and (2) some suppliers are also allocating CAPEX to other segment of their businesses (including MLCC, PCB, etc). However, we are seeing more ABF suppliers planning capacity beyond 2029, as their customers request more long-term capacity (Exhibit 15).

80%

60%

59%

c45a43530f604d12bcb9a82b5aa6b9f6

years

Camble 19. aersupphers capacity expansion pial Sums l0r waru

Company

8,000

Unimicron

7,000

6,000

Kinsus

5,000

Ibiden

4,000

AT&S

3,000

ZDT

2,000

1,000

TOPPAN

01

USS mn 2020

SEMCO

- Kinsus

• SEMCO

140%

30%

Time of new capacity come on-line

KF plant 1 phase 3: starts in 3Q26

120%

YM plant 2: start in mid 2028

100%

Capex

KF plant 1: NTS30bn+

YM plant 2: NT35-40bn

KF plant 2: NTS35-40bn

Yangmei K6 plant phase 2: NTS7bn in 2026

KF plant 2: start in 2H27

25%

24%

Yangmei K6 plant phase 2: 2027

Yangmei K6 plant phase 4: NTS8bn+ in 2028 per GSe

80%

Yangmei K6 plant phase 3: 2028

Yangmei K6 plant phase 4: 2029

20%

Exhibit 13: We expect ABF suppliers' combined CAPEX to remain elevated in order to meet growing capacity requirements 20% 15%

Shenzhen plant

0%

10%

Kaohsiung Al fab: MP in 2H26

Capacity expansion

KF plant 1 phase 3: Additional 15-20% of total capacity per GSe

YM plant 2: Additional 10-15% of total capacity per GSe

KF plant 2: Additional 15-20% of total capacity per GSe

Yangmei K6 plant phase 2: 10mn units

22%

Yangmei K6 plant phase 4: 15mn units

Yangmei K6 plant phase 3: 15mn units

Exhibit 14: We believe the overall pace of ABF substrate industry capacity will increase gradually in the coming years

8%

Kaohsiung: Additional 38% capacity expansion per GSe

AST Phase1 line: Mass production launch scheduled for FY27

Ishikawa (Advanced packaging) : Statup schedules for July 2026, mass production scheduled for FY28 or later

New Ishikawa FC-BGA line: Mass production scheduled for FY30 or later

AST Phase2 line : Timing TBD

Vietnam plant: operation starts in 2H27

2020

Yangmei K6 plant phase 3: NTSbn in 2027 per GSe

Capex for IC substrate at NTS12-16bn in 2026

Source: Company data, Goldman Sachs Global Investment Research

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 15: ABF suppliers' capacity expansion plan going forward

Source: Company data, Goldman Sachs Global Investment Research

Supply / demand update: We believe the overall ABF substrate industry will see shortage ratios of 14%/34%/51% in 2H26/2027/2028, leading to a favorable pricing outlook

We update our ABF industry model, and now expect the ABF TAM to grow at a 62% 2025-28E CAGR (vs. 33% over 2025-28E, previously). The upward revision is mainly driven by (1) the strong AI server growth, especially on the ASIC shipments, and (2) rapid growth in general server CPU shipments which we expect to continue ramping at a 25% 2025-28E CAGR, driven mainly by solid agentic AI demand. Furthermore, while several suppliers have announced new capacity expansion plan for the coming years and some ABF substrate suppliers are even evaluating new CAPEX plans for the long term (beyond 2029), we expect near term supply to remain constrained by long equipment lead times, resulting in overall ABF supply growing at only a 15% 2025-28E CAGR, leading to overall undersupply ratios of 14%/34%/51% in 2H26/27/28, respectively.

Expansion plant

Yangmei K6 plant c45a43530f604d12bcb9a82b5aa6b9f6

will acccica.cleuce cor

Tom Oo 70)

35%

US$mn

12,000

30%

25%

10,000

20%

8,000

15%

6,000

10%

4,000

5%

2,000

0%

0

22%

2025-28E CAGR: 101%

we Miner ma neth commis years

100%

USSmn

90%

12,000

80%

10,000

70%

Exhibit 16: We forecast key AI IC substrate TAM will continue to grow at a 101% 2025-28E CAGR (revised up from 66%) 8,000 60% 40%

4,000

30%

2023

Source: Company data, Goldman Sachs Global Investment Research

60%

Exhibit 17: ASIC to account for 50%+ of total AI ABF substrate demand in 2028E 40%

9%

30%

20%

7%

2023

2024

Source: Company data, Goldman Sachs Global Investment Research

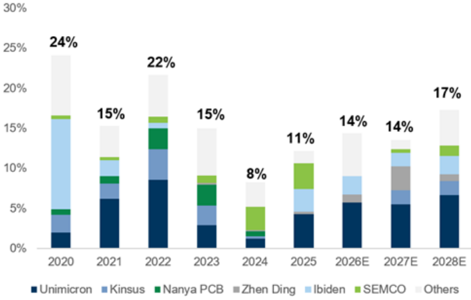

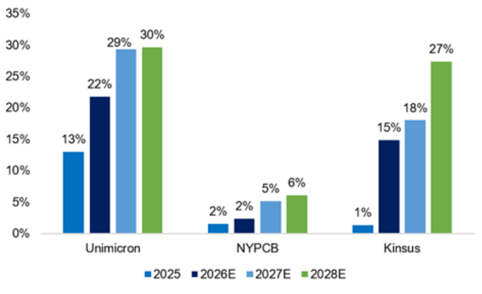

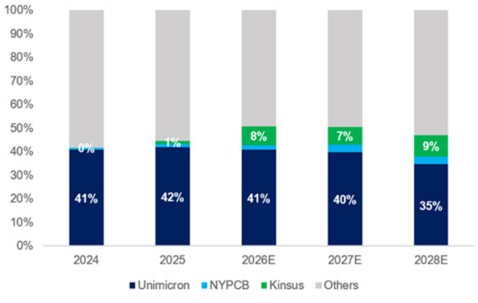

In terms of market share, we continue to see Kinsus gaining market share in the NVDA supply chain (especially for AI server CPUs and NVSwitch ICs). We expect Kinsus to hold 8/7/9% of AI substrate market share in 2026/27/28E (up from 1% in 2025E) and AI to account for 15%/18%/27% of the company's total revenue in 2026/27/28E (vs. 2% in 2025).

Exhibit 18: We believe Kinsus' AI ABF revenue exposure will accelerate in 2025-28E

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 19: We expect Kinsus will continue to gain share in the AI ABF market in coming years

Source: Company data, Goldman Sachs Global Investment Research

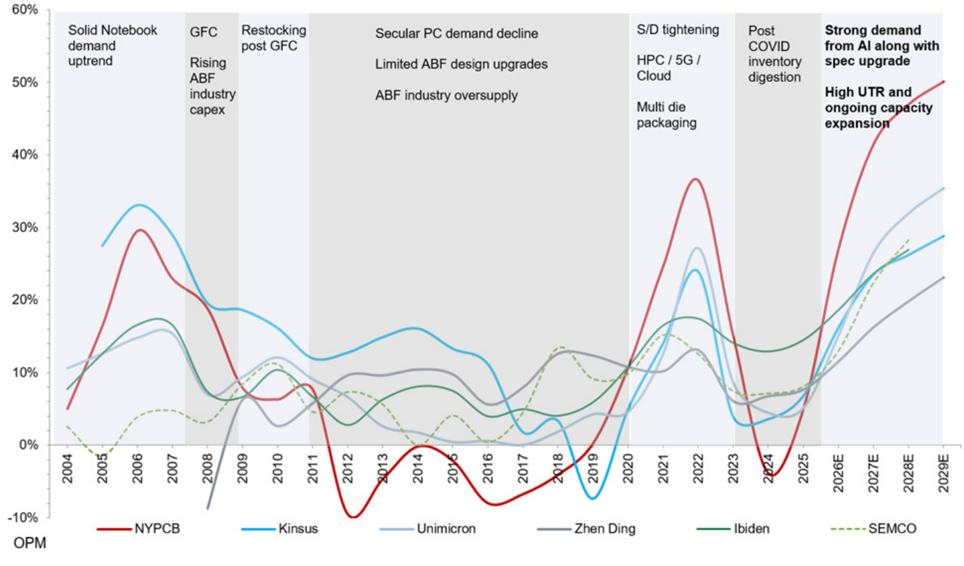

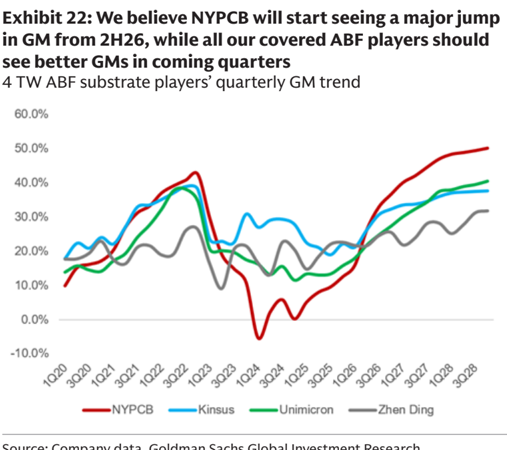

Due to the accelerating shortage ratio we anticipate in 2025-28E, we now expect the ABF substrate LTA/spot prices to increase by 10-15%/20%+ QoQ per quarter from 3Q26 through to at least the end of 2027, and expect the shortages will continue into 2028 and possibly beyond. The stronger ABF pricing environment suggests a solid upside potential to our OPM estimates for all 4 ABF substrate players in Taiwan in the coming quarters/years (Exhibit 20).

27%

c45a43530f604d12bcb9a82b5aa6b9f6

strongest orM growult coms yudrters/yedis

60%

12,000

50%

10,000

40%

8,000

30%

6,000

20%

4,000

10%

2,000

0

US$ mn

0%

2028 AI ABF TAM (old)

-10%

OPM

2004

demand uptrend

GFC

Rising

Secular PC demand decline

1,397

Limited ABF design upgrades

S/D tightening

HPC / 5G /

Post

COVID

inventory

Strong demand spec upgrade

from Al along with

10,754

Exhibit 20: We expect the ongoing OPM uptrend to continue, while we believe spot price players could deliver their strongest OPM growth in coming quarters/years Multi die packaging ongoing capacity expansion

8,269

OPMs are on a companywide basis

Source: Company data, Goldman Sachs Global Investment Research

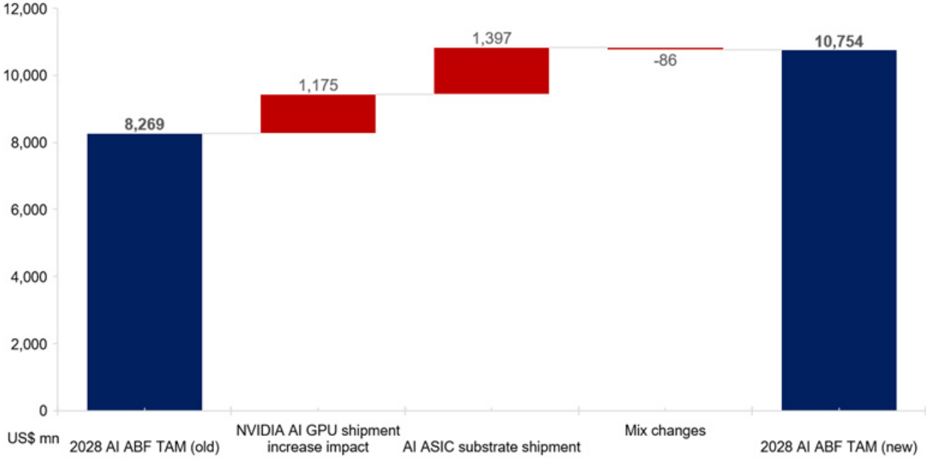

Exhibit 21: We revise up our 2028E AI ABF substrate TAM by 30% to factor in our more positive view on stronger AI substrate shipments and larger AI substrate sizes

Source: Company data, Goldman Sachs Global Investment Research

Restocking post GFC

c45a43530f604d12bcb9a82b5aa6b9f6

2Q26 & 3Q26 preview - stronger ABF substrate pricing to drive GM expansion

For the upcoming 2Q result, we believe all four TW ABF substrate companies will see better than expected earnings (4-38% higher than BBG consensus) , mainly driven by much higher ABF substrate volume shipments and stronger ASP/pricing thanks to the substrate supply tightness from 2Q.

Considering that spot prices increased by 40%+ from April, we expect key spot price player NYPCB, which had 80% exposure to the spot price market in 1Q26, to see its GM expand from <16% in 1Q26 to 26%+ in 2Q26. The 10ppt QoQ GM expansion should mainly be due to better pricing, likely allowing NYPCB to continue to outgrow all other ABF substrate suppliers who have greater LTA exposure. For Unimicron/Kinsus/ZDT, we expect the three companies' GM to surpass BBG consensus by 0.2/1.2/0.3ppt, respectively, on strengthening product mix and improving pricing conditions.

Going into 3Q, we expect all four TW ABF substrate suppliers to deliver even stronger earnings growth, while our 3Q26 operating income estimate for all 4 ABF substrate suppliers are 9-53% higher than BBG consensus . We expect the 4 TW ABF players' GM/OPM to expand by 3.5ppt/4.7ppt in 3Q26 , re fl ecting even more positive ABF substrate ASP/price hike trends in 3Q26. For NYPCB, we believe the GM/OPM will again expand the most in 3Q26 with +6.7ppt/+7.2ppt GM/OPM QoQ , again supported by a more favorable ABF substrate spot price outlook. For Unimicron/Kinsus/ZDT, we expect these three companies' OPM to surpass BBG consensus by 1.5/3.7/0.9ppt, on a stronger product mix and improved pricing conditions.

Overall, we believe the ABF substrate pricing uptrend just started in 2Q26, and we should see further acceleration in ABF substrate pricing given the shortage conditions (i.e., no IC can be packaged without a substrate), leading to a favorable pro fi tability outlook over the coming quarters/years. Within the Taiwan ABF substrate industry, we prefer the spot price players (with NYPCB (CL-Buy) as the key spot price player here), considering the potential upside to their GM/OPM outlook, which are both still 15ppt below the peak level. We believe sustained AI infrastructure investment demand and long equipment lead times will continue to drive spot prices much more strongly than LTA pricing, suggesting solid earnings upside potential, which we should start seeing in 2Q26 results.

c45a43530f604d12bcb9a82b5aa6b9f6

Calll 4t 4240 8 9240 Coe v9. boo consensus comp labie

NT$ mn

60.0%

NTS mn; GSe

GSe

Sales

Gross Profit

Sales

50.0%

Gross Profit

40.0%

EBIT

Net Income

EBIT

3,568

3,144

Net Income

EPS (NTS)

30.0%

EPS (NT$)

GM (%)

OPM (%)

20.0%

GM (%)

OPM (%)

BBG consensus sth

Sales

10.0%

0.0%

Gross Profit

EBIT

-10.0%

Net Income

EPS (NTS)

OPM (%)

-Kinsus

—NYPCB

GM (%)

Differences (GSe vs. BBG)

Sales

Gross Profit

EBIT

Net Income

EPS (NT$)

GM (%)

OPM (%)

2,755

4.26

26.3%

23.2%

7339388

NYPCB

13.575

3.144

3.568

2,755

.4.26

26.3%

23.2%

NYPCB

13.318

2,329

2,633

1.953

3.10

19.8%

— Unimicron

17.5%

NYPCB

2%

35%

35%

41%

38%

6.50pt

5.7ppt

2Q26E

Kinsus

Unimicron

12,496

1.717

42,920

5,743

9,306

ZDT

2Q26

42,920

9,306

48.431

5,743

NYPCB

17,659

5,354

5,815

10,430

3.282

3Q26E

Kinsus

Unimicron

14,756

2,814

50.138

8,474

12,435

6.225

24.8%

4.05

16.9%

3:366089

Unimicron

18.00%

11,446

7,542

6,348

4.11

23.4%

15.4%

Unimicron

3%

9%

12%

-2%

-2%

1.4ppt

1.5ppt

4,533

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 23: 4 TW ABF substrate players' 3Q26 vs 2Q26 earnings estimate, we expect solid margin expansion for NYPCB/Kinsus

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 24: 2Q26 & 3Q26 GSe vs. BBG consensus comp table

Source: Company data, Goldman Sachs Global Investment Research, Bloomberg

Earnings estimate changes: Faster than expected margin expansion driven by better ABF substrate

4,013

15,637

5,393

8,488

5.03

24.5%

13.3%

ZDT

62,737

7,802

15.367

4,899

4.50

24.5%

12.4%

ZDT

2%

2%

9%

10%

12%

0.0ppt

0.9ppt c45a43530f604d12bcb9a82b5aa6b9f6

Exmolt 4o. NTr eD edrmlings reviston labie

Exmore 4o. ninsus earmlos revision table

NYPCB P&L (NT$ mn)

Kinsus P&L (NT$ mn)

Sales

Sales

Gross Profit

Gross Profit

EBIT

EBIT

Net Income

Net Income

EPS (NT$)

pricing

Ratio analysis

EPS (NTS)

Gross margin

Ratio analysis

Gross margin

EBIT margin

EBIT margin

Net margin

Net margin

2026E New

2026E New

64,805

19,351

17,488

14,478

22.41

29.9%

27.0%

22.3%

2026E Olc

2026E Old

73,477

18,378

16,279

13,232

20.48

25.0%

2027E New

2027E New

127,361

55.812

52,764

41,783

64.66

43.8%

22.2%

Diff.

-12%

5%

7%

9%

9%

4.8pp

4.8pp.

41.4%

Earnings revisions NYPCB

2029E New

2029E New

148,104

68,211

116,387

www

54,488

180.12

116.52

52.4%

50.1%

40.0%

28.8%

39.4%

23.0%

......•••••••••••••

We revise up our 2026/27/28E earnings estimates by 9%/22%/36% to factor in much more favorable supply/demand outlook for ABF substrate, with higher pricing driven by supply constraints. The stronger-than-expected demand pull-in for ABF substrates should continue to support pricing uplift longer term. Considering the stronger ABF substrate pricing outlook, we revise up our 2026/27/28E GM by 4.8/8.3/10.5ppt. We revise down 2026E revenue by 12% due to the weaker-than-expected shipments driven by material shortages the in near term but revise up our 2028E revenue by 9% to factor in stronger long-term demand for ABF substrates.

Also, we introduce our 2029E earnings estimates in this report.

Exhibit 25: NYPCB earnings revision table

Source: Goldman Sachs Global Investment Research

Kinsus

We revise down our 2026E net earnings by 2% after applying a more conservative margin assumption on its IC substrate business in 2Q26E but revise up our 2027/28E net earnings by 8/38%, driven by a better ABF substrate pricing outlook and a much more favorable supply demand outlook for the overall ABF substrate market. We revise up our 2027/28 revenue estimate by 9%/34% and revise up our 2028 GM by 0.5ppt.

Also, we introduce our 2029E earnings estimates in this report.

Exhibit 26: Kinsus earnings revision table

Source: Goldman Sachs Global Investment Research

Unimicron

We revise down our 2026E revenue by 1% to re fl ect weaker-than-expected shipments due to material shortages but revise up our 2027/28E revenue estimate by 2/6% to factor in the better demand visibility for ABF substrates, supporting a steeper pricing

2027E Old

2027E Old

127.932

45,427

42,363

34,166

52.88

35.5%

34.7%

23.5%

33.1%

26.7%

17.9%

Diff.

Diff.

0%

9%

23%

9%

25%

22%

9%

8%

22%

8%

8.3pp

8.3pp

6.1pp

2028E New

2028E New

194,486

95,782

154,185

57,734

91,270

71,191

40,422

110.17

31,701

67.79

49.2%

46.9%

36.6%

2028E Old

2028E Old

178.551

69,255

65,114

52,209

80.80

38.8%

36.5%

37.0%

25.7%

20.0%

29.2%

Diff.

9%

40%

38%

36%

36%

10.5pp

10.5pp

7.4pp.

c45a43530f604d12bcb9a82b5aa6b9f6

canoner emmicron carmings revision lavie

Exmoll 40. 401 earnings revision labie

ZD Tech P&L (NT$ mn)

Unimicron P&L (NTS mn)

Sales

Sales

Gross Profit

EBIT

Gross Profit

EBIT

Net Income

Net Income

EPS (NTS)

Ratio analysis

EPS (NTS)

Gross margin

Ratio analysis

Gross margin

EBIT margin

EBIT margin

Net margin

Net margin

2026E New

2026E New

2026E Old

224,680

188,516

53,140

25,882

44,333

28,373

25,490

16,363

15.27

16.58

23.7%

11.5%

23.5%

15.1%

13.5%

2029E New

2029E New

139,326

206,613

2027E Old

2027E Old

293,972

82,163

321,782

92,603

70,995

2026E Old

226,449

191,063

54,060

26,593

43,497

27,336

2028E New

2028E New

454,047

424,900

133,376

89,985

166,786

135,710

2028E Old

2028E Old

407,834

402,458

110,548

71,561

149.463

120,028

Diff.

Diff.

-1%

-1%

-2%

-3%

2%

4%

2027E New

2027E New

327,764

85,019

299,174

101,274

79,287

Diff.

Diff.

2%

2%

3%

4%

9%

12%

Diff.

Diff.

11%

21%

6%

12%

26%

13%

53,206

50,922

uplift in the longer term. We revise up our 2026/27/28E GM by 0.8/2.4/2.1ppt, resulting in 7/12/10% higher EPS estimates with improvement in operating leverage.

22.8%

0.8pp

Also, we introduce our 2029E earnings estimates in this report. 16.2% 19.8%

1.0pp

Exhibit 27: Unimicron earnings revision table

Source: Goldman Sachs Global Investment Research

ZDT

We revise down our 2026E revenue by 1% considering the material shortage, which has led to weaker-than-expected shipments and revise up our 2027/28E revenue estimates by 2/11% to factor in the stronger-than-expected ABF substrate pull-ins and a better pricing outlook. We revised down ZDT's 2026E GM by 0.2ppt due to weaker shipments, resulting in 3% lower 2026E EPS estimates, but we revise up 2027/28 GM by 0.4/2.3ppt to re fl ect a much stronger than expected ABF substrate pricing outlook, resulting in 4/25% higher EPS estimates.

Also, we introduce our 2029E earnings estimates in this report

Exhibit 28: ZDT earnings revision table

Source: Goldman Sachs Global Investment Research

Valuation NYPCB

We are Buy rated (on CL) with a new 12-month TP of NT$2,310 (from NT$1,115), based on the same 21.0x P/E on 2028E EPS (rolled over from 2027E). We believe the company could trade at 1.5x STDV above the past upcycle average P/E of 13.3x, as we continue to expect better pricing condition for ABF substrates, and factor in our latest earnings revisions.

33.9%

31.5%

24pp

39.3%

37.1%

2.1pp.

2.3pp

1.3pp

2.1pp

0.9pp

42.3%

23.1%

13.9%

27.8%

35.4%

7.3%

c45a43530f604d12bcb9a82b5aa6b9f6

calvis ou nilsus raL lavic

NTSmn

2Q25

2Q25

1Q25

1Q25

NTSmn

Revenue

Revenue

Gross profit

Gross profit

Operating expense

Operating expense

Operating income

3Q25

3Q25

10.356

10,967

1,050

1.964

(429)

620

4Q25

4Q25

10.811|

11,165

1,398

2,393

(435)

963

(403)

366

(1,396)

620

(397)

33

Operating income

Pretax income

256

907

Taxes expense

Pretax income

(227)

(1,336)

628

(1,473)

921

(1,440)

501

700

713

619

Taxes expense

Net income

1,409

1,055

Exhibit 29: NYPCB P&L table

Net income

EPS, NT$

0.32

1.12

(0.29)

EPS, NTS

Ratio analysis and assumption

As % of sales

Ratio analysis and assumption

As % of sales

Gross margin

Gross margin

Operating expense ratio

Operating margin

Operating expense ratio

Operating margin

Net margin

Net margin

QoQ growth (%)

Revenue

2024

2024

30,535

32,283

358

8,668

(1,624)

(1,267)

(7,572)

1,095

163

41

1,603

(272)

49

204

0.32

2025

2025E

40,173

39.351

3.647

8.314

(1,665)

1,982

(5,645)

2,670

3,087

2.346

(399)

1.947

(370)

1,596

2026E

2026E

54.949

64,805

19,351

(1,863)

15,529

(6,634)

17.488

8.895

18.394

(3,916)

9,168

(1,483)

6,250

14.478

22.41

2027E

2027E

127,361

95,645

55,812

33.138

(3,048)

(10,645)

52.764

22.494

52,764

(10,981)

22,579

(4,064)

17,030

41.783

64.66

2028E

2028E

154.185

194,486

95,782

57.734

(4,511)

91,270

(17,311)

40.422

91,270

(20,079)

40,507

(7,291)

31,701

71,191

110.17

2029E

2029E

236,684

295,639

(26,486)

68,211

148.104

148.824

(32,437)

68,396

(12,311)

54,488

116.387

180.12

4Q26E

4Q26E

16.592

22,393

8,197

5,365

(559)

7.638

1Q27E

1Q27E

17.988

25,209

10.106

6.037

(1,891)

3.473

7.818

(1,720)

3,473

(590)

2,543

6,098

9.44

26.8%

(635)

9.471

2Q27E

2Q27E

22.768

29,637-

7.695

12,457.

(2,065)

3,972

4,022

9.471

(706)

11.751

3Q27E

3Q27E

34,098

26.835

15,202

9,290

(2,459)

5,236

5,286

11.751

(1,800)

7.672

(724)

2,978

(2,585)

9.166

(808)

14.394

4Q27E

38,417

18,047

(2,979)

6,311

14.394

(3,167)

6.311

(952)

3,920

11.228

17,147

(899)

17,147

(3,429)

13,718

(1,136)

4.793

2Q26E

2Q26E

12.496

13,575

3.282

3,568

(424)

3.144

(1,565)

1.717

3.444

1.817

(689)

2,755

(309)

1,093

3Q26E

3Q26E

14.756

17,659

4.533

5,815

(461)

5,354

(1,719)

2.814

5.534

(1,217)

2,914

(495)

2,065

4.316

6.68

30.1%

| 0.61 | 0.74 0.75 | 1.41 | 2.34 | 4.42 5.44 | 6.37 | 8.38 | 10.25 | 0.11 | 3.52 13.36 | 36.42 67.79 | 116.52 | |||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 5.1% | 8.0% 9.6% | 12.5% | 15.8% | 26.3% | 32.9% | 36.6% | 42.0% | 44.6% | 47.0% | 9.1% 29.9% | 43.8% 49.2% | |||

| 4.7% 22.5% | 4.2% 3.9% 21.1% 19.0% | 22.1% | 3.8% | 3.1% 26.3% | 2.6% 30.7% | 2.5% 32.3% | 40.1% 2.5% 2.4% 33.6% 33.8% | 2.4% 34.6% | 2.3% 36.1% | 1.1% 5.0% 28.4% | 4.1% 2.9% 21.1% 28.3% | 2.4% 34.6% 37.4% | 2.3% 40.0% | 52.4% 2.4% |

| 0.4% 16.7% | 3.8% 5.7% 14.6% 12.9% | 3.9% 8.6% 13.6% | 12.1% | 23.2% 12.5% | 30.3% 11.7% | 34.1% 11.4% | 37.6% 39.6% 11.5% 10.8% | 42.2% 11.1% | 44.6% 11.2% | -3.9% 24.8% | 4.9% 27.0% 12.1% | 41.4% 11.1% 11.2% | 46.9% 11.2% | 50.1% |

| 2.5% 5.8% | 6.6% 6.5% 6.1% | 10.8% 8.5% | 11.7% | 20.3% 13.7% | 24.4% 19.1% | 27.2% 20.9% | 30.4% 30.9% 22.1% 23.0% | 32.9% 23.5% | 35.7% 24.9% | 0.6% 3.6% 14.3% 6.8% | 22.3% 16.2% | 32.8% 36.6% 26.2% | 28.8% | 39.4% |

| 3.2% | -2.0% 3.5% 3.3% | 5.9% | 4.9% | 8.7% | 14.0% | 15.3% | 16.6% 17.2% | 17.9% | 19.0% | 0.2% 4.1% | 4.8% 11.4% | 23.5% 17.8% 20.6% | 23.0% |

Revenue

Gross profit

QoQ growth (%)

Operating income

Net income

Gross profit

Operating income

Net income

YoY growth (%)

Revenue

Gross profit

Operating income

Revenue

Gross profit

Operating income

Net income

Net income

14.4%

36.5%

8.3%

0.1%

26.7%

2.7%

1.86

1.8%

33.2%

4.4%

13.3%

78.7%

11.0%

4.26

21.5%

101.4%

12.5%

7.5%

2441.0%

7.2%

11.87

12.6%

8.4%

23.3%

14.19

17.6%

23.3%

26.6%

17.38

15.1%

22.0%

17.9%

21.23

12.7%

18.7%

4.5%

| -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | -108.5% 1006.2% 69.4% 55.2% 40.4% 132.5% 70.3% 42.7% 24.0% 24.1% 22.5% 19.1% -13.6% 3.8% -2.6% 21.9% -1.8% 39.7% 38.1% 18.4% 12.5% 8.9% | |||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | 16.1% -190.3% -486.7% 65.8% 8.9% 110.5% 56.7% 41.3% 25.8% 19.5% 22.5% 22.2% 23.7% 1.3% 46.6% -3.3% 92.8% 63.9% 23.4% 14.4% 27.5% 31.8% 20.7% 20.5% 10.5% | |||||

| NM | 99.1% | ||||||||||||||||

| 19.1% 18.0% -210.7% 22.5% | 19.3% 0.3% | 41.9% 89.3% | 32.1% -14.5% | 41.7% 61.0% 88.9% | 100.6% 23.2% | 125.5% 17.1% | 118.3% 31.6% | 93.1% 22.3% | 71.6% 11.4% | -24% | 24% 61% | ||||||

| -213.1% 23.2% | 319.0% 95.2% | N.A | 311.7% 364.0% | 453.9% | 486.3% | 470.5% | 249.2% | 161.4% | 120.2% | -96% | 920% 431% | 188% | 97% | 53% 72% | 52% 62% | ||

| 396.4% 31.0% 26.3% | -346.5% 34.4% 6.5% | 3986.2% 758.8% 28.8% 21.0% | 763.1% 30.7% 62.8% 42.5% 130.8% | 693.2% 53.5% 124.2% | 600.4% 62.0% 157.0% | 273.8% 82.2% 134.5% | 168.9% 81.9% 104.9% | 124.5% | -120% 14% 28% | -257% 782% 29% -4% 40% 87% | 202% 74% 113% | 61% 74% | 73% 54% 64% | 62% | |||

| -236.1% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | 856% 644% | 189% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | 70% | 63% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% | -104 2% -276.9% -258.0% 1130.9% 2.7% -5.1% -18.4% |

| 56.0% | 74.5% 48.8% | 572.7% NM | 530.8% -1569.9% 77.7% | 495.5% 176.9% 348.1% | 407.4% 277.2% | 486.2% 346.1% | 232.7% 205.0% | 160.1% 124.3% | 125.0% | -96% 5% | 144% 233% | 153% | 80% | 69% | |||

| 1026.8% | 281.9% 83.2% | -357.5% | 98.9% | 223.2% 508.5% | 295.9% | 442.5% | 258.6% | 132.1% | 1883 | 3% | 3164% 292% | 173% | 86% | 72% |

Source: Company data, Goldman Sachs Global Investment Research

Kinsus

We are Buy rated with a new 12-month TP of NT$1,120 (from NT$555), based on the same 16.5x P/E on 2028E EPS (rolled over from 2027E). We believe the company could trade at 1.2x STDV above the average PE multiple during previous upcycle of 14.2x as we expect the company's pro fi tability to continue improving driven by increasing AI exposure and better ABF substrate pricing conditions, and factor in our latest earnings revisions.

Exhibit 30: Kinsus P&L table

Source: Company data, Goldman Sachs Global Investment Research

Unimicron

We are Neutral rated with a new 12-month TP of NT$1,140 (from NT$630), based on the same 17.4x P/E on 2028E EPS (rolled over from 2027E). We believe the company could trade at 2.7x STDV higher than past upcycle average P/E of 10.3x, and factor in our latest earnings revisions.

63.0%

18.1%

41.0%

12.4%

3.01

c45a43530f604d12bcb9a82b5aa6b9f6

NTSmn

NTSmn

Revenue

Revenue

Gross profit

Gross profit

Operating expense

Operating income

Operating expense

Pretax income

Operating income

Pretax income

Taxes expense

Taxes expense

Net income

4Q25

56.870

12,830|

(6,909)

5,921

3Q25

47.366

10.410

(5,880)

4,530

1Q25

(4,829)

1,056

1,457

5,673

2025

2Q25

(4,586)

2,425

2,272

4,661

Exhibit 31: Unimicron P&L table

Net income

EPS, NTS

EPS, NTS

Ratio analysis and assumption

As % of sales

Ratio analysis and assumption

As % of sales

Gross margin

Operating expense ratio

Gross margin

Operating expense ratio

Operating margin

Net margin

Operating margin

Net margin

QoQ growth (%)

QoQ growth (%)

Revenue

2024

171,664

32,461

(20,875)

11,586

15,045

(1,948)

9.180

2025

182,522

36,136

(22,205)

13,932

14,063

(3,458)

6,791

2026E

224,680

53,140

(27,258)

25,882

27,378

(4,182)

16,363

2027E

327,764

85,019

(31,813)

53,206

55,806

(8,736)

33,322

2029E

2029E

583,347

602,605

(39,941)

(57,767)

139,326

206,613

206,613

140,626

(43,676)

(22,308)

162.368

106.66

33%

48%

55%

54%

2028E

454,047

133,376

(43,392)

89,985

91,285

(14,310)

54.498

83,856

1Q27E

64,038

13,929

(6,480)

7,449

8,249

(1,402)

4,908

2027E

70,652

16,830

(7,542)

9,288

9,988

(1,698)

5,873

3Q27E

89,912

25,231

(8,714)

16,517

16,617

(2,493)

9,970

3Q26E

63.831

15,637

(7,149)

8,488

8,988

(1,348)

5,393

4Q26E

71.690

18.261

(7,384)

10,877

11,877

(1,782)

7,126

2Q26E

48.431

10,430

(6,417)

4,013

4,113

(699)

2,418

| 0.66 | 2.46 | 3.16 | 2.26 | 5.03 | 6.65 | 4.58 5.48 | 9.30 | 9.67 | 6.91 15.27 | 31.09 | 50.84 | 78.23 | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 13.4% | 13.1% | 21.7% | 27.3% | 32.2% | 34.3% | 13.9% 23.5% | 33.9% | 39.3% | 42.3% | |||||||

| 9.2% 14.7% | 8.4% 13.4% 22.0% | 15.8% 9.0% 22.6% | 8.3% 21.5% | 24.5% | 7.7% 25.5% | 21.8% 23.8% | 7.3% 37.3% 7.3% 28.1% | 28.1% | 18.9% | 8.9% 19.8% | 8.5% 23.7% | 25.9% | 7.3% 29.4% | 6.8% 32.7% | ||

| 12.0% | 4.6% 8.9% 12.4% | 12.1% | 13.3% | 11.2% | 10.3% | 7.3% 24.9% 10.1% 10.7% | 26.9% 30.0% 9.7% | 8.8% | 12.2% | 12.2% | 12.1% | 7.3% 9.7% | 9.6% | 35.4% 9.6% | ||

| 4.2% 3.0% 2.6% 1.6% | 0.1% 4.5% 6.5% 9.6% | 6.8% 10.2% 10.4% | 13.4% 12.4% 8.3% | 13.3% | 19.6% 15.3% 15.2% | 11.6% | 19.0% 13.1% | 23.8% 18.4% | 19.3% | 6.7% | 5.1% 5.1% 15.1% 13.5% 7.6% | 26.5% 20.5% 11.5% | 31.9% 24.2% 16.2% | 27.8% 19.8% 23.1% | ||

| 5.0% | 5.6% | 5.0% | 8.4% | 9.9% | 7.7% 8.3% | 20.4% 11.1% | 12.2% | 5.3% | 3.7% | 7.3% | 10.2% | 12.0% | 13.9% | |||

| 2.4% | 7.9% 4.7% | 7.9% | 14.6% | 15.7% | 75.8% | 11.1% 10.3% | 17.8% 13.6% 27.3% |

Gross profit

Revenue

Gross profit

Operating income

Operating income

Net income

YoY growth (%)

Net income

YoY growth (%)

Revenue

Gross profit

Revenue

Gross profit

Operating income

Operating income

Net income

Net income

2.4%

18.5%

-28.6%

-48.7%

-81.0%

86.5%

1531.2%

-85.5%

14.0%

-6.2%

23.3%

10.3%

42.2%

-19.7%

-62.4%

20.1%

23.2%

30.7%

32.2%

1.3%

11.9%

6.6%

-27.5%

43501

-28.4%

7.9%

22.9%

16.5%

-31.3%

-57.7%

-54.9%

42.7%

24.4%

67.1%

1.6%

49.7%

137.1%

117.6%

451.4%

125.4%

15.7%

27.6%

12.3%

16.8%

28.1%

34.5%

42.7%

32.1%

67.2%

189.9%

26.1%

42.3%

83.7%

381.9%

151.3%

125.4%

RE0E35009

31.8%

49.9%

111.5%

123.0%

47.5%

173.4%

34.8%

50.2%

87.4%

452.9%

183.7%

125.5%

24.0%

4.7%

7.1%

-4.7%

7.9%

5.5%

19.1%

1.5%

19.1%

129.6%

-4.3%

48.5%

86.8%

295.3%

7312.1%

-96.8%

16.5%

15.3%

17.9%

65.1%

-476.8%

68.3%

-98.1%

-6.4%

7.2%

-8.0%

-21.9%

-8.7%

-23.6%

-28.7%

-35.3%

18.9%

14.6%

38.4%

108.3%

18.4%

60.3%

69.6%

5.9%

32.2%

119.2%

26.8%

48.8%

65.5%

280 5%

N/A

299.7%

24.5%

120.1%

Source: Company data, Goldman Sachs Global Investment Research

ZDT

We are Buy rated with a new 12-month TP NT$824 (from NT$388), still based on our SOTP based valuation methodology of (1) 3.5x blended P/B (was 3.0x blended P/B) for ABF & BT substrate, which is 1 STDV above early upcycle industry average, (2) 20x P/E for high-growth AI server/switch related PCB (in line with industry average), and (3) 8x P/E for low-growth consumer electronics PCB (in-line with industry downcycle average valuation), and roll over our valuation period from 4Q26-3Q27 to 2028E, and factor in our latest earnings revision.

75.8%

234.4%

-10.7%

-23.7%

-31.5%

481.6%

202.9%

-31.1%

102.7%

354.5%

57.2%

11.1%

19.2%

10.3%

20.8%

24.7%

22.6%

20.1%

19.7%

108.7%

413.9%

45.9%

58.1%

197.6%

986.1%

1070.8%

1017.3%

244.3%

17.8%

25.3%

27.3%

49.9%

77.8%

27.4%

26.4%

69.8%

134.7%

501.0%

40.9%

61.4%

13.6%

23.7%

14.7%

15.1%

20.8%

26.4%

32.9%

26.1%

161.3%

518.0%

1048.5%

1302.5%

N/A

61.4%

131.5%

94.6%

142.8%

84.9%

640.5% 510.8%

885133

23%

47%

86%

141%

Exhibit 32: ZDT P&L table

Source: Company data, Goldman Sachs Global Investment Research

13%

18%

26%

48%

6%

11%

20%

-26%

46%

60%

106%

104%

39%

57%

69%

64%

c45a43530f604d12bcb9a82b5aa6b9f6

Investment thesis, PT methodology and risks

Investment Thesis - NYPCB

NYPCB manufactures and markets printed circuit boards (PCBs) and integrated circuit (IC) substrates (including ABF and BT substrates). We are Buy-rated on NYPCB considering the company's high exposure to BT substrates and non-LTA ABF substrate (70%+ of total revenue), where we expect GM/OPM to increase signi fi cantly in the coming quarters (from breakeven in OPM in 1H25 to 27/41% in 2026/27E) due to the favorable substrate pricing outlook. Despite the company's low exposure to high-end ABF substrate industry (<20% of total revenue in 1H25), we believe the expanding demand from ASIC AI server and high-end switch IC demand will drive the company's high-end ABF revenue exposure to 40%+ by 2027E, suggesting better GM/OPM outlook in the long term. In 2H25-2H26, we believe NYPCB will continue to bene fi t from stronger ABF/BT pricing and should be a key bene fi ciary of the pricing uptrend considering the company's key focus on BT and non-LTA ABF substrate industries. Moreover, in the long term (after 2026), we expect the ABF industry to return to supply tightness, and NYPCB's expanding high-end exposure will lead to a long term earnings growth outlook (122% 2026-28E earnings CAGR). As a result, we see solid upside potential for NYPCB's earnings and stock performance.

Price Target Risks and Methodology - NYPCB

Valuation methodology: Our 12-month target price of NT$2,310 for NYPCB is based on 21x 2028 P/E, which is +1.5x STDV higher than the past upcycle average P/E (13.3x).

Key downside risks: (1) Slower-than-expected PC demand recovery, (2) Slower-than-expected ABF substrates pricing upgrading outlook, and (3) Slower-than-expected NYPCB new high-end capacity quali fi cation progress.

Investment Thesis - Kinsus

Kinsus is one of the key IC substrates suppliers globally with ~10% ABF/BT substrates market share in 2024, with ~18% of total 2025 revenue contributed by its contact lens subsidiary, Pegavision (6941.TW, Not Covered). With our view that the ABF substrate shortage started from 2Q26 (ABF substrate return to supply demand balance from late 2025), we believe Kinsus' performance will continue to improve compared with high-end ABF peers considering the company's increasing market share in the high-end ABF substrate market; however, ~36% of the company's revenue was contributed by BT substrates in 2025 and 30% of the company's ABF revenue is from non-LTA customers, which we believe will continue to enjoy a better pricing outlook. As a result, we believe Kinsus' earnings outlook should continue to be strong (~125% 2026-28E CAGR), mainly driven by better BT substrate and non-LTA ABF substrate pricing outlook, despite the unfavorable demand outlook before 2H26. We believe Kinsus is an experienced substrate supplier with a clear capacity expansion plan that can also upgrade its product portfolio in the long term. We believe we are at the beginning of an industry upcycle, making us positive on Kinsus' stock performance over the next 12 months.

Price Target Risks and Methodology - Kinsus

Valuation methodology: Our 12-month target price of NT$1,120 for Kinsus is based on c45a43530f604d12bcb9a82b5aa6b9f6

16.5x 2028E P/E, which is +1.2x STDV higher than Kinsus' past upcycle average P/E (14.2x).

Key downside risks: (1) Slower-than-expected PC demand recovery, (2) Slower-than-expected ABF substrates pricing upgrading outlook, (3) Slower/Less-than-expected AI server orders from 2H26.

Investment Thesis - Unimicron Technology

Unimicron is a key supplier of ABF substrates (25% market share in 2025) and BT substrates and also produces FPC/HDI/PCB products. We are Neutral rated on the shares given long-term growth opportunity prospects: (1) over 70% of ABF shipments are covered by long-term agreements (LTA), which limits pricing fl exibility and makes price hike less likely; (2) the company's execution track record has been weaker than peers; (3) capacity expansion plan remains slower than peers, constraining its ability to capture incremental AI demand. The current ABF substrates market is seeing more favorable supply demand outlook, and Unimicron is likely to see better pricing outlook to re fl ect rising material costs in the coming quarters. AI ABF account for 10% of the company's total revenue, but the growth is likely to be slower than peers due to the company continuing to lose market share to peers given its less favourable production yield and slow capacity expansion. Overall, we are Neutral rated on Unimicron given our outlook for the limited upside potential, barring ASIC AI servers, despite our generally positive view on the long term on pro fi tability trajectory.

Price Target Risks and Methodology - Unimicron Technology

Valuation methodology: Our 12-month target price of NT$1,140 for Unimicron is based on 17.4x 2028E P/E, which is 2.7x STDV higher than the past upcycle average P/E (10.3x).

Key upside/downside risks: (1) Slower/faster-than-expected PC demand recovery, (2) Slower/faster-than-expected ABF substrates upgrading pace, and (3) Slower/faster than-expected AI server PCB market share loss progress.

Zhen Ding Technology (ZDT) is the global leading PCB supplier (top 1 in market share in sales) with 7-10% market share, and started its ABF substrate business from 2023 in Shenzhen, China, and has the highest ABF revenue exposure to the China market compared to all other ABF substrate suppliers. We believe ZDT will hold more than 40% ABF substrate market share in China by 2027E (up from 31% in 2024) and bene fi t the most from the strong and growing China ABF substrate market (53% 2025E-27E CAGR) due to the increasing in-sourcing ratio for the AI computing ASIC/GPU market in China. We also expect the increasing foldable smartphone penetration rate in the long term to drive ZDT's FPC TAM, and account for 50% of the company's total revenue in 2027E. We see further revenue upside potential from foldable phones. We are Buy rated mainly due to our positive view on the company's China ABF substrate business opportunity, which should not only drive ZDT's revenue growth, but also improve its OPM level in the long term. We see upside for the stock price considering the company's solid growth opportunity, and our TP implied P/E multiple is still lower than the company's past 10+ year P/E average, which we believe is fair considering the potential upside from China ABF substrate market and increasing foldable phone penetration rate.

Valuation : Our 12-month TP of NT$824 is based on a SOTP valuation methodology, c45a43530f604d12bcb9a82b5aa6b9f6

including (1) 3.5x blended 2028E P/B for ABF & BT substrate, (2) 20x 2028E P/E for high-growth AI server/switch related PCB (in line with industry average), and (3) 8x 2028E P/E for low-growth consumer electronics PCB (in-line with industry downcycle average valuation).

Key downside risks include : (1) weaker-than-expected iPhone demand or slower content upgrade, (2) delay in new substrate capacity or slower-than-expected yield rate ramp up progress, and (3) fi ercer competition in China ABF market.

c45a43530f604d12bcb9a82b5aa6b9f6