PDF 原檔:報告_SemiAnalysis_NvidiaCCL供應鏈洗牌_20260703_original.pdf

原始內容

senianalysis

Juy 2, 202

Nvidiaʼs CCL Suppy Chain Shake Up

2 minutes

By and Tony Chien Wega Chu

Executive Summaries

- EMC 28.TT is set to take the eading CCL suppier position at Nvidia, driven by a shift of product and aggressive capacity expansion strategy for 2027/2028.

- There wi be a massive gap between EMC and the remaining CCL vendors. EMC wi hod 050% more of Nvidiaʼs CCL procurement vaue than Doosan 000150.KS.

- Nan Ya Pastic 10.TT coud be a potentia second source CCL suppier for NVLink Switch Rosaind) and CX (Orchid .

$45,000

$40,000

$35,000

$30,000

$25,000

$20,000

$15,000

$10,000

$5,000

$O

EMC Overtake Doosan in 2H2

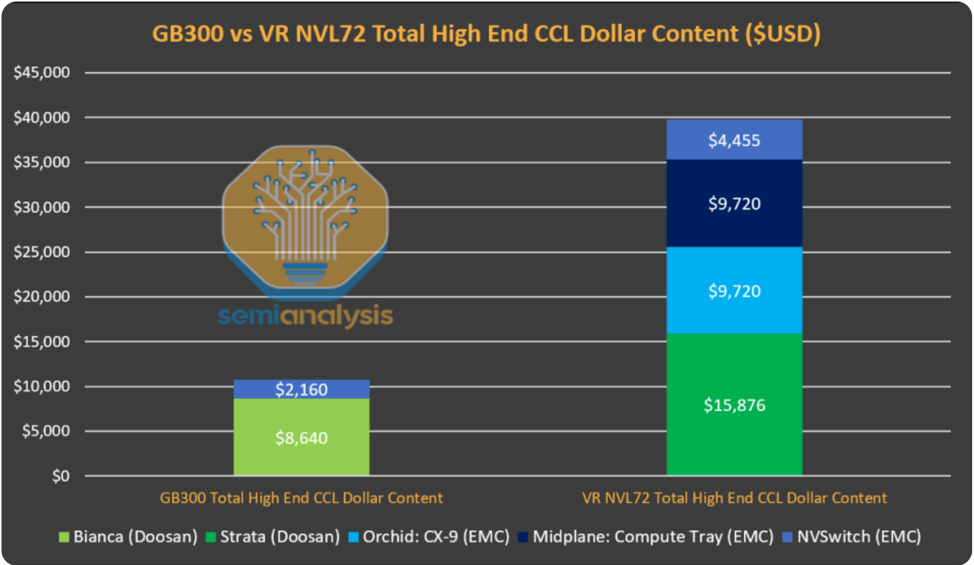

There wi be a significant shift in Nvidiaʼs CCL Copper Cad Laminate) suppier andscape in terms of share of vaue. Over the past 12 months June 2025May 202, Doosan Corporation Eectro-Materias 000150.KS hed the top position among Nvidiaʼs CCL vendors. However, this is set to change significanty starting in June 202.

$2,160

To understand the big shift, it is important to understand which suppier within the Nvidia suppy chain is responsibe for which board. n GB00, Doosan is suppying the Bianca board, and Eite Materia Co 28.TW is suppying the NVSwitch Rosaind) board. For VR NVL72, Doosan is suppying the Strata board, and EMC is suppying the CX (Orchid), Buefied-, Midpane, and NVSwitch Rosaind) boards.

Source: SemiAnaysis VR NVL72 BoM Mode

n this bar chart, we compare the tota CCL doar content per rack of GB00 and VR NVL72. We aso identified the contribution from each different board as we as the responsibe suppier. The vaue captured by EMC is identified by bue bocks, and the vaue captured by Doosan is identified by green bocks. For GB00, the green bock is bigger than the bue bocks by

x, meaning that Doosanʼs content is times higher than that of EMC. However, this changes with VR NVL72, where the bue bocks in aggregate are bigger than the green bocks by 1.51x. t is evident that EMCʼs content has overtaken that of Doosan in VR NVL72.

Given EMCʼs product and content grow significanty faster than Doosanʼs across the GB00 to VR NVL72 generation, EMC is set to overtake Doosan as Nvidiaʼs top CCL vendor starting June 202, as the ramp of Rubin.

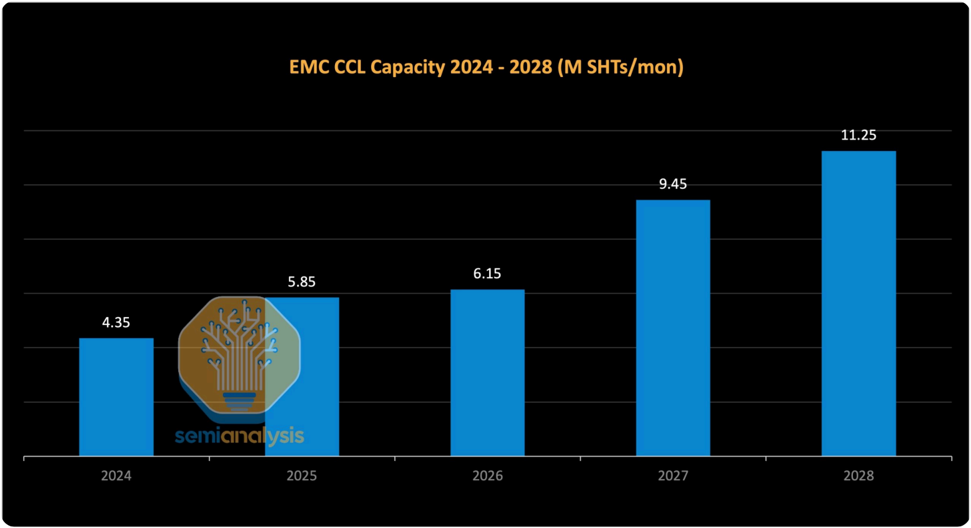

EMC Wi Doube Capacity by 2028

Capacity is another driver behind this shift. Nvidia heaviy favors vendors wiing to aggressivey expand their manufacturing footprint to meet surging future demand, and EMC has positioned itsef accordingy. The companyʼs monthy capacity is projected to grow 5%, from .15 miion sheets/month in 202 to a target of .5 miion sheets/month by the end of 2027.

n ate May 202, EMCʼs board approved the acquisition of new and in Kunshan and Zhongshan, China, expected to add another 1.8 miion sheets/month of capacity in the second haf of 2028. Together, these expansions mean that EMCʼs tota capacity wi effectivey doube by 2028.

As a bonus, EMC is aso entering the high-end A substrate CCL market, with new 00k sheets/month of dedicated capacity in Taiwan coming onine in Q2, fu conversion coud bring tota A substrate CCL capacity to 1mn sheets/month. The move positions EMC to capture share amid an industrywide suppy shortage, with an initia focus on customers in Taiwan and mainand China.

• 9:30 PM

Nvidia's CCL Supply Chain Shake Up - SemiAnalysis

Source: EMC, SemiAnaysis

Nvidia NVSwitch and CX New Payer Nan Ya Pastics Corporation

Nvidia continues to seek suppiers capabe of keeping pace with its surging demand, and Nan Ya Pastics Corporation has emerged as a highy notabe new entrant. Besides positive progress with the samping of their M10 grade CCL for the Kyber Midpane, Nanyaʼs M7 and M8 materias have passed Nvidiaʼs eectrica and reiabiity testing and added to Nvidiaʼs approved materia ist.

We beieve there is a great chance for Nvidia to use Nanyaʼs CCL on NVLink Switch Rosaind) and CX Orchid as second source besides EMC, and we beieve this wi highy benefit Nanyaʼs utra-ow oss product, incuding NPG1HK2 and NPG1K.

Discaimers

Anayst Certifications and ndependence of Research.

Each of the anaysts whose names appear in this report hereby certify that a the views expressed in this Report accuratey refect our persona views about any and a of the subject securities or issuers and that no part of our compensation was, is, or wi be, directy or indirecty, reated to the specific recommendations or views in this Report. SemiAnaysis LLC (the 'Companyˮ) is an independent equity research provider. The Company is not a member of the FNRA or the SPC and is not a registered broker deaer or investment adviser. SemiAnaysis has no other reguated or unreguated business activities which confict with its provision of independent research.

Limitation Of Research And nformation.

This Report has been prepared for distribution to ony quaified institutiona or professiona cients of SemiAnaysis LLC. The contents of this Report represent the views, opinions, and anayses of its authors. The information contained herein does not constitute financia, ega, tax or any other advice. A third-party data presented herein were obtained from pubicy avaiabe sources which are beieved to be reiabe; however, the Company makes no warranty, express or impied, concerning the accuracy or competeness of such information. n no event sha the Company be responsibe or iabe for the correctness of, or update to, any such materia or for any damage or ost opportunities resuting from use of this data. Nothing contained in this Report or any distribution by the Company shoud be construed as any offer to se, or any soicitation of an offer to buy, any security or investment. Any research or other materia received shoud not be construed as individuaized investment advice. nvestment decisions shoud be made as part of an overa portfoio strategy and you shoud consut with a professiona financia advisor, ega and tax advisor prior to making any investment decision. SemiAnaysis LLC sha not be iabe for any direct or indirect, incidenta or consequentia oss or damage (incuding oss of profits, revenue or goodwi) arising from any investment decisions based on information or research obtained from SemiAnaysis LLC.

Reproduction and Distribution Stricty Prohibited.

No user of this Report may reproduce, modify, copy, distribute, se, rese, transmit, transfer, icense, assign or pubish the Report itsef or any

information contained therein. Notwithstanding the foregoing, cients with access to working modes are permitted to ater or modify the information contained therein, provided that it is soey for such cientʼs own use. This Report is not intended to be avaiabe or distributed for any purpose that woud be deemed unawfu or otherwise prohibited by any oca, state, nationa or internationa aws or reguations or woud otherwise subject the Company to registration or reguation of any kind within such jurisdiction.

Copyrights, Trademarks, nteectua Property.

SemiAnaysis LLC, and any ogos or marks incuded in this Report are proprietary materias. The use of such terms and ogos and marks without the express written consent of SemiAnaysis LLC is stricty prohibited. The copyright in the pages or in the screens of the Report, and in the information and materia therein, is proprietary materia owned by SemiAnaysis LLC uness otherwise indicated. The unauthorized use of any materia on this Report may vioate numerous statutes, reguations and aws, incuding, but not imited to, copyright, trademark, trade secret or patent aws.

Private nvestment Discosure.

Each anayst and/or author contributing to this Report hereby discoses that they may hod, directy or indirecty, private investments in companies, sectors, or asset casses discussed or referenced herein. Such hodings, if any, are discosed externay with a third-party vendor. SemiAnaysis LLC requires that no author or anayst aow their persona investment positions to infuence the views, opinions, anayses, or concusions expressed in this Report. Readers shoud be aware that the existence of such hodings, even where discosed, may present a potentia confict of interest, and are encouraged to weigh this accordingy when evauating the contents of this Report.

圖片清單(已驗證 2026-07-03)

| 檔名 | 分類 | 親眼所見內容 |

|---|---|---|

| _001.png | 裝飾·logo·banner | SemiAnalysis 標題頁 banner |

| _002.png | 裝飾·logo·banner | 文章題圖 |

| _003.png | 真資料圖 | 長條圖「GB300 vs VR NVL72 Total High End CCL Dollar Content ($USD)」:GB300=Bianca(Doosan)$8,640+NVSwitch(EMC)$2,160;VR NVL72=Strata(Doosan)$15,876+Orchid:CX-9(EMC)$9,720+Midplane:Compute Tray(EMC)$9,720+NVSwitch(EMC)$4,455,EMC 合計 $23,895 為 Doosan 1.51x |

| _004.png | 真資料圖 | 長條圖「EMC CCL Capacity 2024-2028 (M SHTs/mon)」:2024=4.35、2025=5.85、2026=6.15、2027=9.45、2028=11.25 百萬張/月 |