PDF 原檔:報告_MS_記憶體華邦南亞科旺宏力積電_20260625_original.pdf

圖片清單(已驗證 2026-06-30)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_001.png | 66KB | 裝飾·logo·banner | 藍色橫幅寫有 Asia Summer School 2026 與右側信封圖示。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_002.png | 54KB | 真資料圖 | 折線圖顯示 NOR flash demand growth 與 supply growth rates。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_003.png | 102KB | 真資料圖 | 長條與折線圖顯示 DDR4 quarterly supply and demand summary,含 supply、demand 與 oversupply/undersupply ratio。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_004.png | 85KB | 真資料圖 | 堆疊長條圖顯示 quarterly supply breakdown,圖例含 Samsung、Hynix、Micron、CXMT、Nanya、Winbond、PSMC、JHICC。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_005.png | 41KB | 真資料圖 | 長條圖顯示 NOR flash demand growth and supply growth by density。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_006.png | 117KB | 真資料圖 | 折線圖顯示 oversupply/undersupply ratio 與 Nanya、Winbond pricing Q/Q change。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_007.png | 91KB | 真資料圖 | 堆疊長條圖顯示 quarterly demand breakdown by product,圖例含 Smartphone、PC、Server、TV、Switch、Cache DRAM、Others。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_008.png | 77KB | 真資料圖 | DDR4 8Gb pricing chart,折線區分 spot 與 contract。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_009.png | 107KB | 真資料圖 | DDR5 16Gb pricing chart,折線區分 spot 與 contract。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_010.png | 117KB | 真資料圖 | Winbond historical forward P/B 折線圖,含平均值與標準差標線。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_011.png | 108KB | 真資料圖 | Winbond historical forward P/B vs ROE 折線圖。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_012.png | 139KB | 真資料圖 | Winbond earnings estimate revision breadth 與 share price performance 折線圖。 |

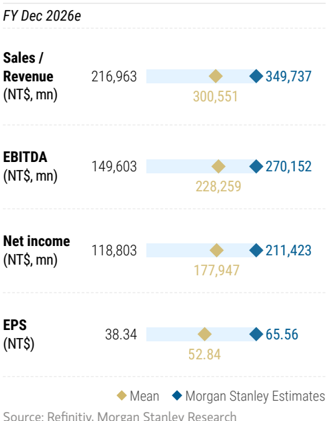

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_016.png | 43KB | 真資料圖 | MS estimates vs consensus 圖,列出 Winbond FY Dec 2026e 的 sales、EBITDA、net income、EPS 對比。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_017.png | 83KB | 真資料圖 | GigaDevice historical forward P/E 折線圖。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_018.png | 59KB | 真資料圖 | GigaDevice consensus price target distribution 與 risk reward chart。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_022.png | 214KB | 真資料圖 | Nanya Tech historical P/B band 折線圖,含 forward P/B 與標準差標線。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_023.png | 136KB | 真資料圖 | Nanya Tech historical forward P/B vs ROE 折線圖。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_024.png | 122KB | 真資料圖 | Nanya Tech earnings estimate revision breadth 與 share price performance 折線圖。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_028.png | 39KB | 真資料圖 | MS estimates vs consensus 圖,列出 Nanya Tech FY Dec 2026e 的 sales、EBITDA、net income、EPS 對比。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_029.png | 123KB | 真資料圖 | PSMC historical forward P/B 折線圖,含 forward P/B 與標準差標線。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_030.png | 94KB | 真資料圖 | PSMC historical forward P/B vs ROE 折線圖。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_034.png | 45KB | 真資料圖 | MS estimates vs consensus 圖,列出 PSMC FY Dec 2026e 的 sales、EBITDA、net income、EPS 對比。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_035.png | 116KB | 真資料圖 | Macronix forward P/B vs ROAE 折線圖。 |

| 報告_MS_記憶體華邦南亞科旺宏力積電_20260625_039.png | 41KB | 真資料圖 | MS estimates vs consensus 圖,列出 Macronix FY Dec 2026e 的 sales、EBITDA、net income、EPS 對比。 |

原始內容

M June 25, 2026 09:00 PM GMT

Greater China Semiconductors | Asia Pacific

Old Memory: Better to buy more

Unexpected persistent tightness in legacy memory supply is driving panicked purchasing by multiple enterprise customers. We reiterate our bullish view and raise PTs across our coverage.

Key Takeaways

- DDR4 buyers may build even larger demand buffers amid prolonged supply tightness.

- MLC NAND shortages are forcing enterprise HDDs to use SLC NAND, indicating stronger demand.

- NOR supply is increasingly concentrated among Taiwan vendors, given reduced output from the US.

DDR4 stronger orders from enterprise customers: We upgraded both Nanya Tech and Winbond back to OW on May 28 (link), given the ongoing tightness in DDR4. We now see enterprise customers securing supply as early as possible amid fears of shortages. Channel inventory remains low at under two weeks. This points to further DDR4 price increases into 4Q, following the double-digit monthly uptrend.

SLC NAND likely to see stronger demand from HDD: We noted that high-density SLC NAND can support datacenter eSSD (link). In addition, given the MLC NAND shortfall, enterprise HDDs are likely shifting to high-density SLC NAND. Enterprise HDDs previously used MLC NAND for firmware, hot data, and defect mapping. This shift reinforces continued pricing momentum into 4Q, following the 50-60% increase in 3Q.

NOR flash pricing increase led by Macronix, with potential supply-demand widening: We continue to see strong pricing increases from Macronix, driven by a shift toward NAND from NOR. We also see Micron reducing NOR supply into 2H, likely reallocating capacity to DRAM and NAND. At the same time, Vera Rubin rack ramp-up in 2H will require 50%+ higher NOR content versus Grace Blackwell racks. We therefore expect NOR pricing to rise 30-40% in 3Q and continue into 4Q.

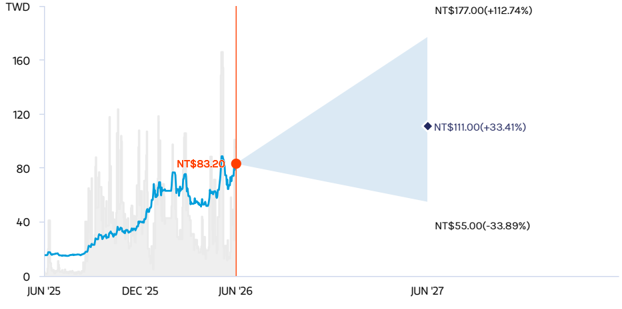

Stock implications - we raise our earnings and PTs across the board: Winbond: PT raised to NT$288; 2026/27/28 EPS raised by 4%/17%/24%. Nanya Tech: PT raised to NT$550; 2026/27/28 EPS raised by 7%/15%/14%. Macronix: PT raised to NT$220; 2026/27/28 EPS raised by 34%/20%/21%. GigaDevice: PT raised to Rmb888; 2026/27/28 EPS raised by 30%/46%/53%. PSMC: PT raised to NT$111; 2026/27/28 EPS raised by 4%/48%/62%.

Morgan Stanley Taiwan Limited+

Idea

| Daniel Yen, CFA Equity Analyst Daniel.Yen@morganstanley.com | +886 2 2730-2863 |

|---|---|

| Charlie Chan Equity Analyst Charlie.Chan@morganstanley.com Morgan Stanley Asia Limited+ | +886 2 2730-1725 |

| Daisy Dai, CFA Equity Analyst Daisy.Dai@morganstanley.com | +852 2848-7310 |

| Tiffany Yeh Equity Analyst Tiffany.Yeh@morganstanley.com | +886 2 7712-3032 |

| Ethan Jia Research Associate Ethan.Jia@morganstanley.com | +852 3963-2287 |

Greater China Technology Semiconductors

Asia Pacific

Industry View

Attractive

| What's Changed GigaDevice Semiconductor Beijing Inc (603986.SS) Price Target | From Rmb585.00 | To Rmb888.00 |

|---|---|---|

| Winbond Electronics Corp (2344.TW) Price Target | From NT$222.00 | To NT$288.00 |

| Nanya Technology Corp. (2408.TW) Price Target | From NT$380.00 | To NT$550.00 |

| Macronix International Co Ltd (2337.TW) Price Target | From NT$202.00 | To NT$220.00 |

| Powerchip Semiconductor Manufacturing Co (6770.TW) Price Target | From NT$88.00 | To NT$111.00 |

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

+= Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to FINRA restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

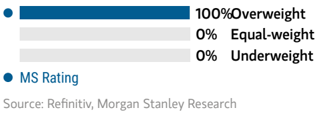

Rating

Price Target

Uluel ul vieletenue. Ou tellury

Macronix

Winbond

2337.TW

2344.TW

AP Memory

6531.TW

PSMC

6770.TW

GigaDevice

603986.SS

M

Market Cap (in USD mm)

9,780.7

26,999.2

5,685.1

11,308.3

Key Charts and Exhibits

Hold/Equal-weight

Sell/Underweight

Bull Case Value

Upside (%)|

Bear Case Value

Downside (%)|

Risk/Reward Skew

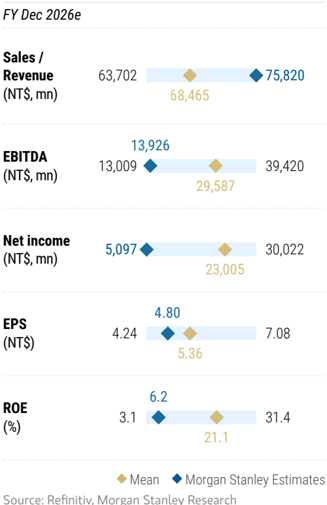

Morgan Stanley Estimates

FY26e

Sales

EBITDA

EBIT

EPS

FY27e

Sales

EBITDA

EBIT

EPS

FY26 MSe vs. Consensus Mean

Sales

EBITDA

EBIT

EPS

FY27 MSe vs. Consensus Mean

Sales

EBITDA

EBIT

EPS

Valuation Multiples at Last Close

FY26e

P/E

EV/EBIT

EV/EBITDA

EV/Sales

FCF Vield

FY27e

P/E

EV/EBIT

EV/EBITDA

EV/Sales

FCF Yield

Implied Multiples on MS Price Target

FY26e

P/E

EV/EBIT

EV/Sales

EV/EBITDA

FY27e

P/E

EV/EBIT

EV/EBITDA

EV/Sales

........=----

0%

• 10%

0%

0%

• 25% |

0%

1,830.0

64%

620.0

-44%

1.4

TWD

9,601

3,037

17.65

2,976

17,829

6,491

6,429

34.34

-3.0%

-0.9%

3.8%

1.1%

19.6%

26.0%

33.0%

27.0%

63.2x

80.6x

53.5x

16.9x

1.2%

32.5x

24.9x

24.7x

9.0x

2.2%

88.1x

80.6x

79.0x

25.0x

45.3x

40.0x

39.7x

14.4x

33%

69,101.7

1,346.6

• 94%

355.0

106%

130.0

-24%

4.4

TWD

77,854

30,271

22,733

9.84

143,216

58,187

64,657

25.02

-2.5%

-20.7%

-4.5%

•26.0%

21.4%

4.2%

-4.5%

-9.7%

17.5x

19.6x

11.9x

-11.9%

4.6x

6.9x

5.3x

4.8x

2.2x

17.5%

22.4x

19.6x

14.8x

5.7x

8.8x

7.0x

6.3x

2.8x

342.0

67%

118.0

-42%

1.6

TWD

269,908

134,605

118,994

21.27

432,740

234,811

214,635

38.29

9.2%

-2.1%

7.4%

-0.1%

25.7%

8.8%

34.2%

20.3%

9.6x

6.5x

10.3x

3.2x

2.9%

5.4x

3.3x

3.0x

1.6x

18.9%

13.5x

10.3x

9.1x

4.5x

7.5x

5.7x

5.2x

2.8x

16%

0%

Exhibit 1: Order of preference: GC memory

| 107% 119% 648.0 | 162% 305.0 |

|---|---|

| 55.0 -36% -8% | |

| -31% | |

| 3.0 14.7 | 5.2 |

| TWD CNY | TWD |

| 75,820 | 349,737 |

| 13,926 28,399 13,300 | 270,152 |

| 6,362 13,050 | 257,966 |

| 4.80 16.68 | 65.56 |

| 102,954 38,229 46,298 23,646 | 524,965 391,551 |

| 30,764 23,396 | |

| 5.61 30.27 | 368,367 93.08 |

| 10.7% 56.8% | 16.4% |

| -52.9% 77.7% | 18.4% |

| -74.4% 82.1% | 19.8% |

| -10.3% 88.0% | 24.1% |

| 95.4% | |

| 20.7% 16.2% | 26.7% |

| 148.3% | 26.7% |

| 30.6% 23.0% 147.0% 167.2% | 25.8% 32.0% |

| 17.8x 44.1x 42.3x 44.0x | 6.8x 7.4x |

| 16.1x 34.0x | 5.8x |

| 3.0x 15.9x | 4.5x |

| 28.6% 2.0% | -18.1% |

| 15.3x 5.6x 23.3x 18.7x | 4.8x 3.6x |

| 4.5x 18.5x | 3.3x |

| 2.5x | |

| 1.7x 16.2% 9.5x 3.9% | 19.3% |

| 23.1x 53.2x | 8.4x |

| 44.1x 20.1x 44.0x 43.2x | 7.4x 7.0x |

| 3.7x 20.2x | 5.4x |

| 19.8x 29.3x | 5.9X |

| 15.5x 28.3x | 4.7x |

| 12.5x 28.0x | 4.4x |

| 3.3x |

Source: FactSet (consensus mean), Morgan Stanley Research (e) estimates.

Nanya Tech

2408.TW

Overweight

TWD

550.0

443.5

24%

43,068.6

647.1

86%

N 14%|

CAmoll 4.

Exmbll e. Ivon nastl uellanlu anlu supply yrowurlaleo

CAmnoll O.

Growth rate

15%

40,000

80%

40,000

30,000

10%

35,000

60%

35,000

25,000

5%

40%

30,000

30,000

0%6

20,000

20%

25,000

25,000

-5%

20,000

20,000

15,000

-10%

15,000

0%

-15%

15,000

-20%

2012

10,000

10,000

10,000

5,000

5,000

-40%

5,000

-60%

• Samsung.

Gaursa. Aamnanu data Mlaradn Manla, Nasaarch (al aatimataa

CAIIbIl O.

density

Growth rate

20%

40%

30%

M

2013

2014 2015

2016

2017

2018

2019

2020

Total water sugely frowth

2021 2022

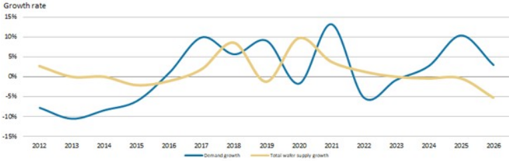

Exhibit 2: NOR flash demand and supply growth rates

-30%

-10%

-15%

CAlIrAn

Source: Company data, Morgan Stanley Research

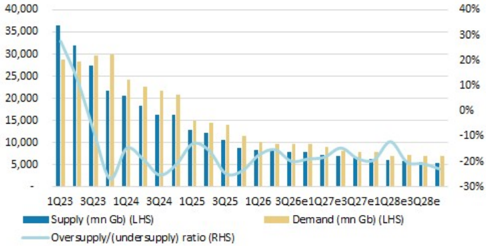

Exhibit 4: DDR4 quarterly supply and demand summary

Source: Company data, IDC, Morgan Stanley Research (e) estimates

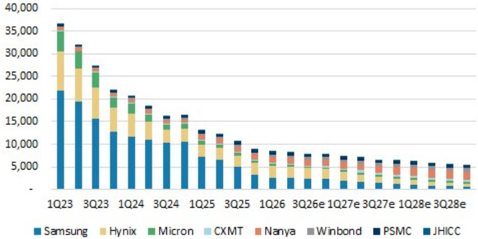

Exhibit 6: Quarterly supply breakdown (mn Gb)

Source: Company data, Morgan Stanley Research (e) estimates

2023

2024

2025

2026

yuarlehy supply bi canuowir (tllrow)

Junt yuartery supply anu delane summary

Ivun Hlasll uelllanlu yrowull allu suppiy yrowurky

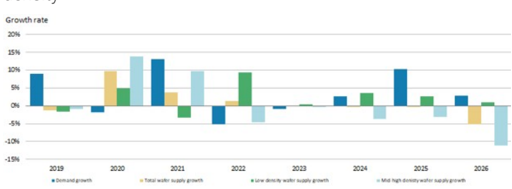

Exhibit 3: NOR flash demand growth and supply growth by

density

Source: Company data, Morgan Stanley Research

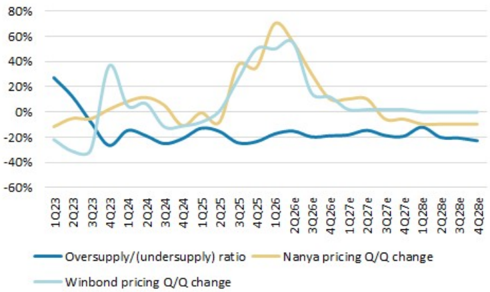

Exhibit 5: Quarterly oversupply/undersupply ratio vs. Nanya and Winbond pricing Q/Q change

Source: Company data, IDC, Morgan Stanley Research (e) estimates

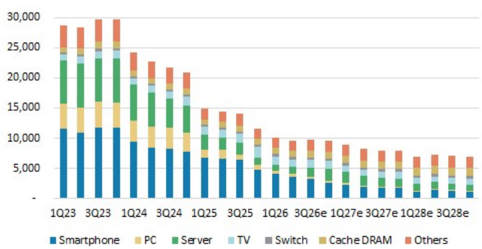

Exhibit 7: Quarterly demand breakdown by product (mn Gb)

Source: IDC, Morgan Stanley Research (e) estimates

CxmIbIl O.

USS

35

30

25

20

15

10

5

Jan-19

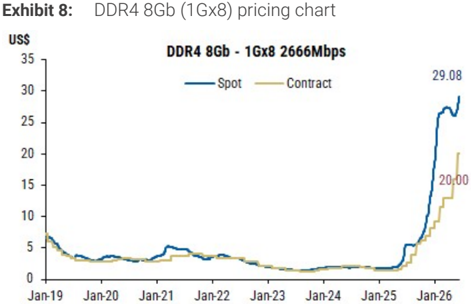

Junt oun ('ono) pricinly chlalt

DDR4 8Gb - 1Gx8 2666Mbps

29.08

M

20,00

Source: DRAMeXchange, Morgan Stanley Research. Data as of Jun 2026.

callvlt ?.

USS

48.0

38.0

23.0

18.0

13.0 -

8.0 1

3.0 -

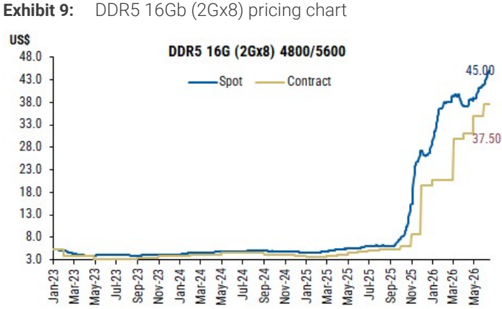

Junv lool (<oxo) priullly Cllatt

DDR5 16G (2Gx8) 4800/5600

- Spot

Contract

45.00

37.50

Source: DRAMeXchange, Morgan Stanley Research. Data as of Jun 2026.

Lanbe1l. vmlbunlu. Yuattelly mlanlulat

NTS in million

1Q25

New '26E

Total Revenues

NTS mn

Sequential Change

Net sales

COGS

Change vs Year Ago

Cost of Sales

Percent of Revenues

Gross Margin

Gross profit

Total Opex

Operating Income

Taxes

Profit Before Taxes

Net income

New '27E

2, 01.

264

Diff.

2Q26E

Old '26E

4Q25

1Q26

26,625

57,075

38,253

22.3%

258,581

43.7%|

19,993

2025

21,018

3Q25

21,771|

7.0%

5.1%

3.6%

77,

583

49.29

-0.6%

4%

269,908

(117,684)

74.4%

432,740

(182,017)|

4%

84

3%

,211)

250,723

New '28E

1.5%

1.5%

13.1%

8.6%

493,598

(211,407)

41.8%

282,192

Old '27E

3Q27E

5.6%

20.0%

377,335

(158,768)

(46,471) (49.174)

42.2%6

218,567

Diff.

3.0%

18.7%

15%

(49)

(50,707) |

41

15%

3%

42 2%

0622

42

88 89

42.3%

5%

*21

(52,108) (53,297)

-2.2%

21%

42.4%

91.3%

171.6%

(14,871) (16,255) (11,605) (15,479) (17,838) (25,385)

152,224

(111,702)|

58.1%

146,879

77.3%

53.3%

46.6%

44.5%

M

Taxes

Tax Rate

Reported Income (TW GAAP)

Reported EPS

Margins

Net margin

Opex %

NTS

BVPS

32.73

Old *28E Diff.

2025

2027E

89,406

269,908

432.740

493,598

9.6%

410,515

20%

(178,012)

201.9%

(58,210) (117,684)

60.3%

14.1%

(182,017) (211,407)

65.1%

43.6%

31,196

232,503

42.1%

42.8%

34.9%

(36,149)

152,224

56.4%6

250,723

57.9%

(25.662)

(33.230)

28.7%

196,354

12.3%

(36,088)

5.534

756

118,994

6.2%

(924)

8.3%6

214.635|

197,111

44.1%

49.6%

715

4,610

(40,609)

119.709

5.2%

(1,433)

776

215,411

156,488

44.4%6

(23,975)

49.856

(43,082)

31.1%

3,962

282,192

21%

57.2%

(37,465)

25%

7.6%

244,727

49.6%

756

25%

245,483

25%

49.7%

(50,284)

20.5%

195,186

21.27

20.36

13.9%|

(1,091)

10.3%

(1,312)|

24.1%|

2,943

23.0%

3,422

20.3%|

10,114

Winbond: Estimate Revisions and Quarterly Financials

35.5%

12.3%

New '26E

46.68

35.4%

12.8%

Old '26E

40.54

0.0 ppt

-0.5 ppt

Diff.

15%

39.8%

8.3%

New '27E

85.02

39.0%

1.4 ppt

0.8 ppt

39.5%

38.1%

We raise our 2026/27/28 EPS estimates by 4%/17%/24% respectively. This reflects stronger than previously expected memory pricing strength across DDR4, NOR flash, and SLC NAND. We now expect DDR4 pricing to rise further into 4Q, post the double digit monthly pricing uptrend. SLC NAND pricing uptrend is highly likely to continue into 4Q, post 50-60% hike in 3Q. NOR pricing could be hiked by 30-40% in 3Q and even into 4Q.

Exhibit 10: Winbond: Estimate revisions

Source: Morgan Stanley Research (E) estimates

Exhibit 11: Winbond: Quarterly financials

Source: Company data, Morgan Stanley Research (E) estimates

24%

20.0%

20.0%

36.09

20.0%

20

0%

4%

20.0%

38.29

20.0%

20.0%

20.0%

17%

20.0%

20

09

44.69

(41

TolUllcal lUi varu r/D

M

Winbond: Valuation Methodology

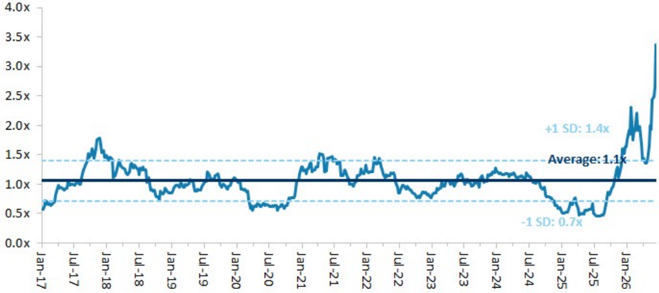

01/07/2007

Jul-17

Jul-20

Jan-20

Jul-19

Jan-19

Jul -18

Jan-18

Exmol 1o. villbone. Mistolical lowalu rid vo nuc

4.0

4.0x

3.5

3.5X

3.0

3.0x

2.5

2.5x

2.0

1.5

1.0

0.5

0.0

0.0x

Jan-17

01/07/2013

01/07/2015

— Forward PB (LHS)

CAIINAA TAMARANCATA REMAN VARIAAAAAHAR AATIMALA.

01/07/2005

01/07/2009

01/07/2011

Jan-21

01/07/2017

Jul-21

Jan-22

Jul-22

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

-10%

-20%

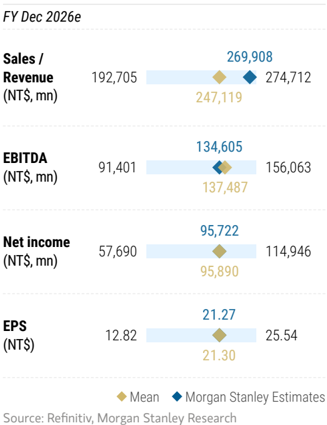

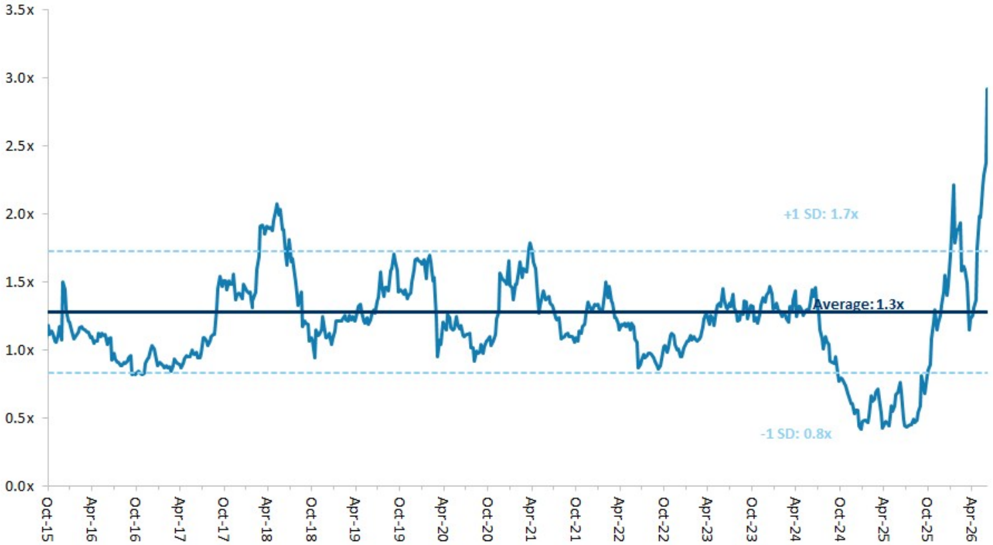

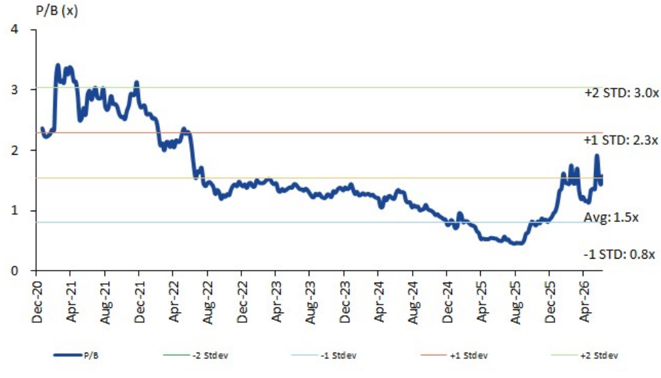

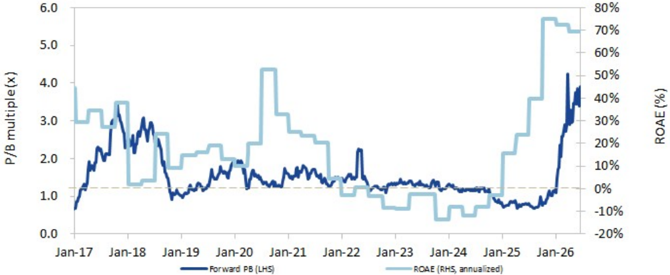

We raise our PT to NT$288 from NT$222: We continue to apply P/B multiple methodology to derive our price target, in line with our approach for Greater China memory IDM peers and in view of the industry's high earnings volatility. Our new price target (base case scenario value) implies 6.2x 2026e BVPS and 3.4x 2027e BVPS vs. our prior target multiple of 5.5x 2026e BVPS, as we think DDR4 pricing strength and SLC NAND/SiCap opportunities could drive re-rating. We raise our bull case value to NT$342 (7.3x our 2026e BVPS) and our bear case value to NT$118 (2.5x our 2026e BVPS).

Exhibit 12: Winbond: Historical forward P/B

Source: Company data, Morgan Stanley Research estimates

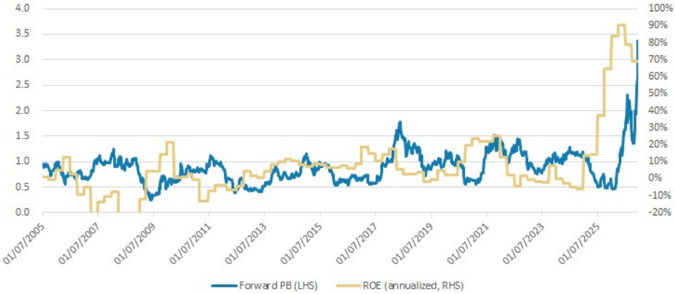

Exhibit 13: Winbond: Historical forward P/B vs ROE

Source: Company data, Morgan Stanley Research estimates

2

1.5

0.5

-0.5

-1

Jan-16 Jan-17 Jan-18 Jan-19 Jan-20 Jan-21 Jan-22 Jan-23 Jan-24 Jan-25 Jan-26

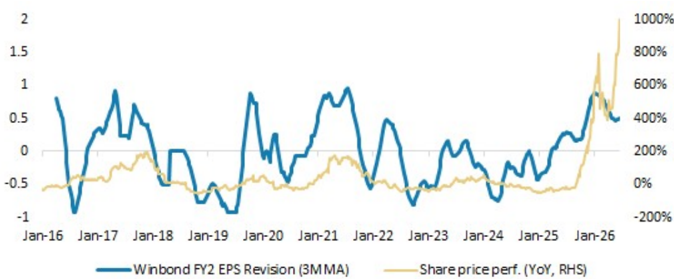

—Winbond FY2 EPS Revision (3M MA)

M

1000%

800%

600%

400%

Exhibit 14: Winbond: Earnings estimate revision breadth

0%

Source: Company data, Morgan Stanley Research estimates

M

Risk Reward - Winbond Electronics Corp (2344.TW) Risk Reward - Winbond Electronics Corp (2344.TW)

DDR, NOR and SLC NAND pricing upside; long-term opportunities in CUBE

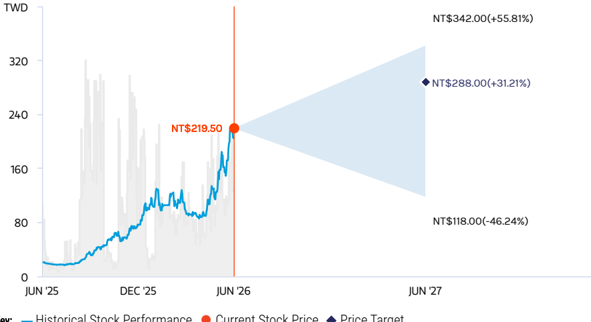

NT$288.00 PRICE TARGET

Base case, 6.2x 2026e P/B. This method is in line with the approach we adopt for Greater China memory IDM peers, in view of the industry's high volatility. We believe the stock merits a multiple beyond the high end of its historical band of 0.5-1.5x since 2017, as we are seeing DRAM pricing upside, a sustainable NOR price hike, and opportunities in SLC NAND and SiCap foundry business.

NT$180.00

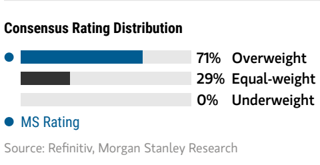

Mean

Consensus Price Target Distribution

Source: Refinitiv, Morgan Stanley Research

RISK REWARD CHART

Key:

Source: Refinitiv, Morgan Stanley Research

BULL CASE

7.3x 2026e BVPS

NOR Flash pricing and DRAM prices rebound

more in the next 12 months: NOR Flash rises dramatically. DRAM prices continue to rise drastically within the next 12 months, with 25nm accounting for >80% of sales.

NT$342.00

NT$145.00

BASE CASE

NT$288.00

6.2x 2026e BVPS

Margin expansion bene fi ting from the memory up-cycle: 1) NOR Flash pricing rises significantly in the next 12 months; and 2) DRAM prices rise significantly in the next 12 months.

NT$288.00

MS PT

Morgan Stanley Estimates

OVERWEIGHT THESIS

- We expect DDR3 and DDR4 price increases to continue in 2026. The supply/demand gap should widen into 2H26.

- We see NOR price hikes continuing throughout 2026.

- High density SLC NAND pricing is catching up, and we now expect a larger TAM from data center applications.

- We share management's view that CUBE could be meaningful in 2026, given engagement with multiple foundry partners and customers.

- We see potential for several headwinds ahead for the logic business.

- Our PT implies 3.4x 2027e P/B.

Consensus Rating Distribution

Risk Reward Themes

Pricing Power:

Positive

View descriptions of Risk Rewards Themes here

BEAR CASE

NT$118.00

2.5x 2026e BVPS

NOR Flash prices face pressure in the next 12 months; DRAM market back to oversupply, with slower technology migration: 1) NOR Flash shows price declines; and 2) DRAM prices drop in the next 12 months.

M

Risk Reward - Winbond Electronics Corp (2344.TW)

KEY EARNINGS INPUTS

| Drivers | Dec 2025 | Dec 2026e | Dec 2027e | Dec 2028e |

|---|---|---|---|---|

| NOR ASP (%) | 8 | 113 | 34 | 0 |

| DRAM ASP (%) | (2) | 258 | 34 | 10 |

| Mobile RAM sales (NT$, mn) | 5,302 | 21,486 | 36,103 | 40,921 |

| DRAM sales (NT$, mn) | 27,808 | 166,338 | 293,379 | 346,905 |

| Flash sales (NT$, mn) | 31,106 | 72,390 | 107,769 | 107,769 |

INVESTMENT DRIVERS

- DRAM pricing

- NOR pricing

- Technology migration

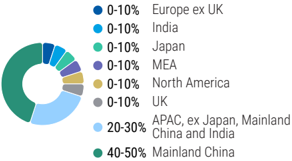

GLOBAL REVENUE EXPOSURE

Source: Morgan Stanley Research Estimate View explanation of regional hierarchies here

MS ALPHA MODELS

1/5 MOST

3 Month Horizon

Source: Refinitiv, FactSet, Morgan Stanley Research; 1 is the highest favored Quintile and 5 is the least favored Quintile

RISKS TO PT/RATING

RISKS TO UPSIDE

- NOR Flash pricing increase, driven by strongerthan-expected demand

- Stronger-than-expected DRAM pricing given ongoing supply shortage

- Faster-than-expected SLC NAND development

RISKS TO DOWNSIDE

- NOR Flash downcycle, driven by weaker demand

- Lower-than-expected DRAM pricing given ongoing oversupply

- Slower-than-expected SLC NAND development

OWNERSHIP POSITIONING

Inst. Owners, % Active

58.8%

Source: Refinitiv, Morgan Stanley Research

MS ESTIMATES VS. CONSENSUS

Sxmble lo. 1 manlulat ourtllary

Income Statement

NT$mn (Years End Dec )

Net sales

COGS

Variable Cost

Gross profit

Pre-tax income

Income tax

2027E

432,740

(182,017)

2026E

269,908

(117,684)

2028E

493,598

(211,407)

43.378

2026E

95,721

2025

11,183

3,177

M

4,610

119,709

(971)

Change of ST Inwestment

245,483

215,411

Winbond: Financial Summary

Reported EPS (NT$)

Modelware EPS (NT$)

Balance Sheet

NT$mn (Years End Dec )

Cash

Mkt Securities

ARINR

Inventory

Other

Current Assets

Long-term investments

Fixed assets

Other assets

Total Assets

SIT borrowings

APINP

Other ST liabilities

LT debt

Other LT liabilities

Total Liabilities

Common stocks

Preferred stocks

Capital Researve

Retained earning

Other shareholders' equity

Total Equity

0.88

0.88

2025

15,734

13,347

16,071

25,758

2,281

73,191

19,266

93,800

5,935

192,192

2,739

8,224

35,652

26,399

5,048

78,062

45,000

0

13,752

49,184

0

114,130

210,073

382,610

Total Liab. & Shrhldr's Equits

192,192 330,193 514,481

BVPS

25.4

46.7

85.0

21.27

21.27

2026E

40,355

13,347

56,043

104,435

2,281

216,461

19,216

88,581

5,935

330,193

2,739

28,428

57,506

26,399

5,048

120,120

45,000

13,752

145,127

38.29

38.29

2027E

202,411

13,347

67,245

125,310

2,281

410,594

19,156

78,796

5,935

514,481

2,739

33,921

63,764

26,399

5,048

131,871

45,000

0

13,752

317,664

44.69

44.69

2028E

413,030

13,347

73,054

136,134

2,281

637,847

19,116

59,010

5,935

721,909

2,739

67.003

36,765

26,399

137,955

5,048

45,000

13,752

519,008

0

583,954

721,909

129.8

Increase in SiT debt

Cash Dividend Paid

Dir& Emp Bonus Paid

Other adjustments

0

0

0

Exhibit 15: Financial summary

Exchange rate adjustment

Net change in cash

0

(330)

Financial Ratio

Growth(%)

Turnover

Margins (½)

Gross Margin

Operating Margin

EBITA Margin

Pretax Margin

Net Profit

Return (%)

ROAE

ROAA

(O)

0

| 1,633 | 24.621 162,056 | 210.620 | |

|---|---|---|---|

| 2025 | |||

| 2026E | 2027E | 2028E | |

| 9.6 | 201.9 | 60.3 | 14.1 |

| 56.4 | 57.9 | ||

| 34.9 6.2 | 57.2 | ||

| 44.1 | 49.6 | 49.6 | |

| -8.0 | 38.4 | 45.0 | 44.4 |

| 5.2 4.4 | 44.4 35.5 | 49.8 | 49.7 |

| 39.8 | 39.5 | ||

| 4.3 | 88.7 | 84.5 | 51.9 |

Gearing (%)

Net Debt/Equity

Liabilities/Equity

Ratios (X)

Currentratio

Quick ratio

Others

ARINR Turnover (days)

Inventory Turnover (days)

AP Turnover (days)

Cash Conversion (days)

2.1

31.9

36.6

40.8

31.6

5.6

(39.3)

34.5

(61.8)

23.6

| 1.,6 | 2.4 | ||

|---|---|---|---|

| 4.1 | 6.0 | ||

| 0.7 | 1.1 | 2.7 | 4.6 |

| 45 | 53 | ||

| 49 | 52 | ||

| 107 | 102 | 88 | 97 |

| 45 107 | 52 | 88 | 68 |

| 104 | 49 | 81 |

Source: Company data, Morgan Stanley Research (E) estimates

57.2

68.4

2025

89,406

Cash Flow Statement

NTSmn (Years End Dec )

Cashflow from Operations

2027E

180,812

172,315

19,785

(26,584)

15,296

(10,331)

(10,000)

0

(331)

(8,425)

0

2028E

219,376

201,121

19,785

(13,789)

12,258

9,649

(10,000)

0

0

19,649

(18,405)

0

Exul 1o. olyabevice. Lounate levoluto cambi 16. olyabevice. Guartelly mialiclais

2mb mn

3025

Total Revenues

Sequential Change

Rmb mn

Change vs Year Ago

Cost of Sales

Net sales

Percent of Revenues

COGS

Gross profit

Gross Profit

Incremental Margin

Total Opex

RAD

Diff.

29%

Current

2027E

46,298

Previous

2027E

32,133

Diff.

44%

Current Previous

2026E

2028E

2028E

57,916

Current Previous

1026

4,188

2026€

6,063

76.6%|

2026E

44.8%

119.4%

2026E

28,399

22,018

1025

1,909

11.9%

17.3%

2025

2,241

17.4%

13.1%

2,681

19.6%

31.4%

4025

2,372

-11.5%

39.0%

170.5%

M

Selling & marketing

Percent of Revenues

Taxes

Operating Income

Net income

Profit Before Taxes

873

2,150

1,408

20

2,501

28,399

37,996

17,583

20,413

3,354

17,059

20

17,079

1,568

1,187

GigaDevice: Estimate Revisions and Quarterly Financials

Margins

Taxes

Tax Rate

Gross margin

Net Income, Cont Ops

Percent of Revenues

Operating margin

Reported Income

Percent of Revenues

Pretax margin

Change va Year Ago

Reported EPS (Rmb) |

Net margin

Change va Year Agol

57.1%

46.0%

45.5%

41.2%

57.1%

43.7%

43.2%

39.0%

-0.1%

2.2%

2.3%

2.2%

58.2%

50.5%

50.6%

45.8%

57.3%

0.9%

53.9%

53.7%

0.2%

We raise our EPS estimates for 2026/27/28 by 30%/46%/53%. This reflects strongerthan-expected memory pricing across DDR4, NOR flash, and SLC NAND. We now expect DDR4 pricing to rise further into 4Q, following the double-digit monthly uptrend. SLC NAND pricing is likely to continue rising into 4Q, after the 50-60% increase in 3Q. NOR pricing could increase by 30-40% in 3Q and extend into 4Q.

Exhibit 16: GigaDevice: Estimate revisions

Source: Morgan Stanley Research (E) estimates

Exhibit 17: GigaDevice: Quarterly financials

Source: Company data, Morgan Stanley Research (E) estimates

61%

2027E

46,298

20281

57,916

Diff.

52%

53%

60%

59%

Exmblt 1o. olyabeviue. neotuuat mbotte mhouel

Rmb mn

100

Total Equity

Net Profit

ROAE

90

80

Spread

70

60

Equity Value

No. of Shares

50

10

0

2026E

30,422

11,693

2027E

48,135

21,221

54.0%

2028E

66,457

24,688

43.1%

2029E

84,789

28,724

38.0%

2030E

106,118

33,421

35.0%

2031E

130,934

159,808

38,885

32.8%

2032E

45,243

31.1%

193,403

2033E

52,640

29.8%

2034E

2035E

232,491

277,969

61,247

28.8%

M

701

GigaDevice: Valuation methodology

Oct-17

Oct-18

Oct-19

Oct-20

Oct-21

— GigaDevice 1-year Forward PIE

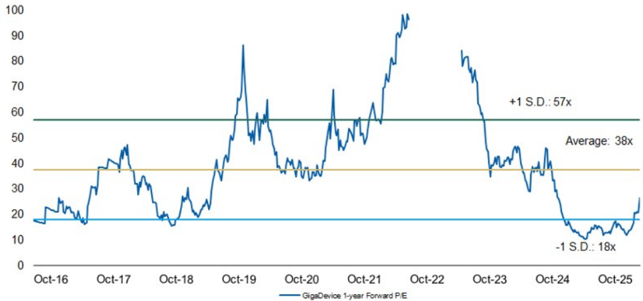

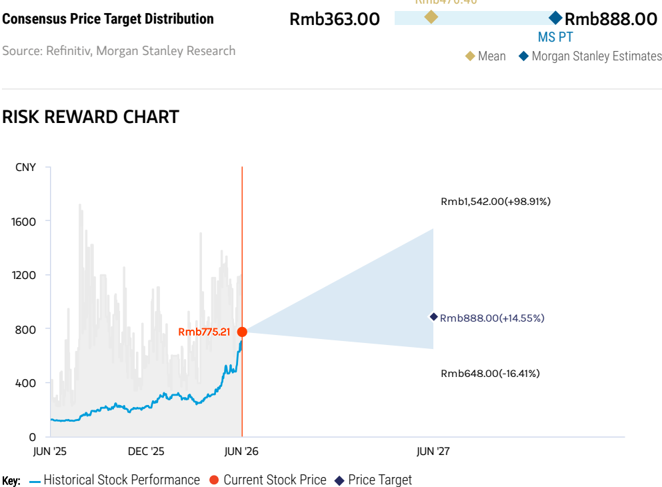

We raise our price target (base case) to Rmb888: We continue to derive our price target from a residual income model, which we believe best captures the stock's long-term value. Our key assumptions include a cost of equity of 8.9% (beta 1.1, risk-free rate 2%, and risk premium 6%), a payout ratio of 40%, a medium-term growth rate of 16.4%, and a terminal growth rate of 3.0% (all unchanged). Our new price target implies a 2026e P/E of 53x, above the historical average of 40x since 2016. Our bull case value rises to Rmb1,542 from Rmb1,016, and our bear case value increases to Rmb648 from Rmb427.

Exhibit 18: GigaDevice: Residual Income model

Source: Morgan Stanley Research (E) estimates

Exhibit 19: GigaDevice: Historical forward P/E

Source: Company data, Morgan Stanley Research estimates

71,261

27.9%

44,251

19.0%

Oct-16

2036E

330,883

82,912

27.2%

51,003

18.3%

2037E

392,449

96,468

26.7%

58,852

17.8%

M

Risk Reward - GigaDevice Semiconductor Beijing Inc Risk Reward - GigaDevice Semiconductor Beijing Inc (603986.SS)

(603986.SS) Multiple drivers ahead

Rmb888.00 PRICE TARGET

Our price target is our base case value, derived from our residual income model. Key assumptions: cost of equity of 8.9% (beta 1.1, risk-free rate 2% and risk premium 6%), a payout ratio of 40%, medium-term growth rate of 16.4%, and a terminal growth rate of 3.0%.

Rmb476.46

Morgan Stanley Estimates

Mean

Consensus Price Target Distribution

Rmb363.00

Rmb888.00

Source: Refinitiv, Morgan Stanley Research

MS PT

Source: Refinitiv, Morgan Stanley Research

BULL CASE

92x 2026e EPS

NOR/SLC NAND prices rise more sharply into 2H26, and the company increases production of mid-/high-density NOR; MCU growth accelerates; DRAM business shows signi fi cant contribution: 1) Flash sales grow 300%+ Y/Y in 2026 via price hikes and meaningful growth in demand; 2) MCU sales growth significantly exceeds 40% in 2026; 3) contribution from WoW tops expectations in 2026-28e; 4) DDR4 price hike stronger than expected; 5) gross margin above 60% in 2026.

Rmb1,542.00

BASE CASE

53x 2026e EPS

NOR/SLC NAND and DRAM pricing upside in 2026; moderate WoW contribution: 1) Flash sales rise 213% Y/Y in 2026; 2) MCU grows 28% in 2026; 3) meaningful contribution from WoW in 2026-28e; 4) significant DDR4 price hike in 2026; 5) gross margin at ~57% in 2026.

Rmb888.00

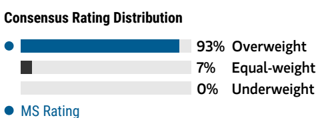

OVERWEIGHT THESIS

- We expect GigaDevice to continue to gain share in China's MCU market. Auto MCUs offer bigger opportunities as local selfsufficiency is low.

- We see further NOR Flash pricing upside, and expect GigaDevice NOR quality to catch up in the auto segment.

- Specialty DRAM pricing started to rebound in late 1Q25, and there are opportunities such as wafer-on-wafer specialty memory.

- We believe GigaDevice will ramp up 16G LPDDR4 and 32G DDR4 at CXMT's Gen 4 platform in 2027.

- Our price target implies 2026e P/E of 53x, above the historical average of 38x since 2016 but within +1 S.D. of 57x.

Source: Refinitiv, Morgan Stanley Research

Risk Reward Themes

Pricing Power: Secular Growth:

Positive Positive

View descriptions of Risk Rewards Themes here

BEAR CASE

39x 2026e EPS

NOR/SLC NAND price falls sharply into 2H26; MCU faces stronger competition from foreign and local vendors; pause in DRAM business development: 1) Flash sales grow less than expected in 2026, as ASP starts to drop towards the end of the year; 2) MCU sales decrease >10% Y/Y in 2026; 3) contribution from WoW falls below expectations in 2026-28e; 4) DDR4 price starts to decline towards the end of 2026; 5) gross margin below 35% in 2026.

Rmb648.00

M

Risk Reward - GigaDevice Semiconductor Beijing Inc (603986.SS)

KEY EARNINGS INPUTS

| Drivers | Dec 2025 | Dec 2026e | Dec 2027e | Dec 2028e |

|---|---|---|---|---|

| NOR Flash ASP growth (%) | 4 | 149 | 42 | 0 |

| MCU ASP growth (%) | (8) | 0 | 0 | 0 |

| Gross margin (%) | 40 | 56 | 58 | 54 |

INVESTMENT DRIVERS

- Beneficiary of MCU localization

- Decreasing opex burden

- Development of AI glasses market

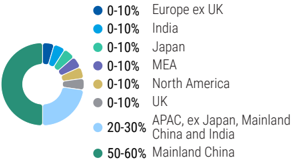

GLOBAL REVENUE EXPOSURE

Source: Morgan Stanley Research Estimate View explanation of regional hierarchies here

MS ALPHA MODELS

4/5 MOST

3 Month Horizon

Source: Refinitiv, FactSet, Morgan Stanley Research; 1 is the highest favored Quintile and 5 is the least favored Quintile

RISKS TO PT/RATING

RISKS TO UPSIDE

- NOR up-cycle driven by stronger demand

- Superior chip design, leading to increasing exposure to low-density NOR

- Faster-than-expected DRAM development

RISKS TO DOWNSIDE

- NOR down-cycle driven by weaker demand

- Inferior chip design, leading to increasing exposure to mid-/high-density NOR

- Slower-than-expected DRAM development

OWNERSHIP POSITIONING

Inst. Owners, % Active

86.1%

Source: Refinitiv, Morgan Stanley Research

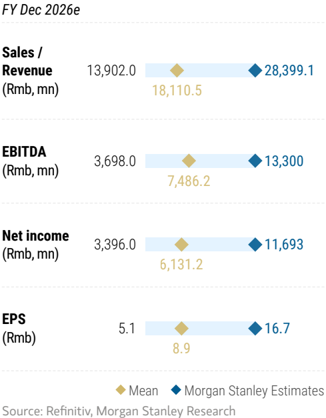

MS ESTIMATES VS. CONSENSUS

Cambre 40. 1 manual vultmlary

Income Statement

Rmb mn (Years End Dec)

Net sales

COGS

Gross profit

Income tax

2026E

28,399

2027E

46,298

2025

9,203

2028E

57,916

Cash Flow Statement

Rmb mn (Years End Dec)

Cashflow from Operations

2025

2,032

M

Minority interests

(45)

(29)

(45)

(45)

Change of ST Investment

0

GigaDevice: Financial Summary

Reported EPS (Rmb)

Balance Sheet

Rmb mn (Years End Dec)

Cash

Mkt Securities

AR/NR

Inventory

Other

Current Assets

Long-term investments

Fixed assets

Deferred assets

Other assets

Total Assets

S/T borrowings

AP/NP

Other ST liabilities

LT debt

Other LT liabilities

Total Liabilities

Common shares

Additional capital

Retained earning

Other shareholders' equity

Total Equity

2.48

2025

9,186

102

199

3,066

873

13,425

4,085

1,325

432

2,129

200

21,397

813

934

0

226

2,174

668

9,201

8,407

946

19,223

Total Liab. & Shrhidr's Equity

21,397

30.27

2027E

32,835

102

1,130

9,209

873

44,148

4,085

1,325

432

52,119

2,129

200

2,623

0

9,201

16.68

2026E

17,997

102

693

5,799

873

25,463

4,085

432

1,325

2,129

33,435

1,652

200

934

0

226

3,013

668

9,201

19,606

37,319

946

946

30,422 48,135

33,435 52,119

E = Morgan Stanley Research Estimates

Source: Morgan Stanley Research, Company Data

35.21

2028E

48,375

102

1,414

12,702

873

63,464

4,085

1,325

432

2,129

71,435

200

3,618

934

226

4,979

668

9,201

55,641

946

66,457

71,435

Increase in S/T debt

Cash Dividend Paid

(698)

0

(243)

(494)

(3,508)

2028E

22,156

24,688

250

(2,782)

(250)

(250)

(6,366)

(6,366)

Exhibit 20: Financial Summary

Other adjustments

Exchange rate adjustment

Net change in cash

Financial Ratios

Growth(%)

Turnover

Operating profits

EPS

Margins (%)

Gross Margin

Operating Margin

Pretax Margin

Net Margin

Return (%)

ROAE

ROAA

Gearing (%)

Net Debt/Equity

Liabilities/Equity

Ratios (X)

Current ratio

Quick ratio

Others

AR/NR Turnover (days)

Inventory Turnover (days)

AP Turnover (days)

Cash Conversion (days)

0

| (92) 21 | |||

|---|---|---|---|

| 146 | 8,810 14,838 | 15,540 | |

| 2025 2026E | |||

| 2027E | 2028E | ||

| 25.1 | |||

| 208.6 | 63.0 | 25.1 | |

| 88.1 755.4 | 79.3 | 16.3 | |

| 49.6 573.6 | 81.5 | 16.3 | |

| 40.2 | 57.1 58.2 | 53.9 | |

| 16.6 | 46.0 50.5 | 47.0 | |

| 18.5 | 45.5 50.6 | 47.0 | |

| 17.9 41.2 | 45.8 | 42.6 | |

| 9.2 8.1 47.1 42.7 | 54.0 | 43.1 | |

| 49.6 | 40.0 | ||

| (46.7) (58.5) | |||

| (67.8) | (72.5) | ||

| 11.3 | 9.9 8.3 | 7.5 | |

| 6.9 | 9.1 | 13.4 | |

| 11.7 | |||

| 4.8 | 6.7 9.0 | 10.5 | |

| 9 | 9 174 9 | 9 | |

| 174 | 174 | 174 | |

| 49 | 49 49 | 49 | |

| 133 | 133 133 | 133 |

2026E

9,555

11,693

250

(2,389)

0

(250)

(250)

2027E

18,596

21,221

250

(2,875)

(250)

(250)

0

cambre 41. Ivanya leull. Lottate levioluto

Exmlble ee. Ivallya leull. Quartelly mlanlulais

NTS in million

New '26E Old '26E Diff. New '27E

1Q26

2Q26E

NTS mn

Total Revenues

Sequential Change

Net sales

Change vs Year Ago

Gross profit

Cost of Sales

EPS (NTS)

Margins as a % of revenue

Gross Margin

New '28E

Diff.

2025

2024

34,132

369,398

11%

66.587

14.2%

231,930

2Q27E

1Q27E

3027E

3Q26E

4Q26E

105,308

115,925

127.613

49,087

63.1%

332,719

349,737

5%

582.9%

Old '27E

4Q27E

132.148

140,478

10.1%

524,965

76.9%

411,790

471,750

124,726

-5.9%

25.5%

359,775

-5.6%

7.6%

10.1%

160.0%

6%

14%

95.1%

32.6%

460.8%|

258,553

10.1%

285.2%

79,416

61.8%

654.5%

275,271

M

15.5%

2.9%

11.1%

2.2%

11.7%

40.7%

20.3%

Old '28E

2026e

2027e

349,737

341,113

524,965

425.2%|

205,545

Diff.

2028e

369,398

8%

50.1%

174,123

178,412

13%

-29.6%

14%

14%

(74,466) (113,175) (137,468)|

21.3%

21.6%

37.2%

144,097

44.68

(62,281)

17.8%

(12,186)

14%

(89,991) (113,063)

17.1%

30.6%

(23,184)

16.4%

3.5%

2.0%

20.5%

4.4%

14%

(24,404)

17.8%

6.6%

2.8%

2.2%

5.9%

3.8%

Nanya Tech: Estimate Revisions and Quarterly Financials

Total Opex

Percent of Revenues

Net margin

R&D

Percent of Revenues

BVPS (NTS)

Sales and Marketing

Percent of Revenues

General and Admin

Percent of Revenues

Operating Income

Percent of Revenues

EBITDA

EBITDA margin

Non-operating Income(Loss)

Profit Before Taxes

Percent of Revenues

Taxes

Tax Rate

Reported Income (TW GAAP)

Percent of Revenues

Change vs Year Ago

Reported EPS (NTS, TW GAAP)

Sequential Change

Book value per share

Maanaa

(3,205)

(3,987)

6.5%

5.0%

(2,109)

60.5%

(2,214)

(5,331) (10,329)

(4,781)

4.5%

4.6%

8.1%

59.6%

(2,325)

New '26E

4.3%

(347)

0.7%

(748)

1.5%

30,111

61.3%

33,008

67%

1,607

31,718

64.6%

(5,660)

17.8%

26,058

53.1%

-1443%|

8.08

129%

2.8%

Old '26E

(2,511)

122.12

2.2%

117.90

(562)

0.7%

(1,211)

1.5%

57,794

72.8%

60,779

77%

1,020

58,813

74.1%

(11,512)

19.6%

47,302

59.6%

-1253%

14.67

82%

2.2%

(745)

0.7%

(820)

(1,711)

1.6%

80,927

76.8%

83,973

80%

1,020

81,947

77.8%

(18,618)

22.7%

63,329

60.1%

3951%

19.64

34%

0.7%

(2,000)

1.7%

89,134

76.9%

92,391

80%

1,034

90,168

77.8%

(15,434)

17.1%

74,734

64.5%

574%

23.17

18%

(2,800)

Diff.

2.2%

4%

(2,042)

1.6%

(5,487)

4.3%

94,462

74.0%

97,325|

76%

1,070

95,531

74.9%

(17,047)

17.8%

78,484

61.5%

201%

24.34

5%

(11,228)

(11,016)|

8.0%

8.3%

57.2%

(2,940)

New '27E

(3,087)

2.1%

218.99

2.3%

(2,248)

(2,114)

1.6%

(6,041)

4.3%

104,973

74.7%

107,837

77%

1,070|

106,043

75.5%

(20,756)

19.6%

85,287

60.7%

80%

26.45

9%

1.6%

(5,814)

4.4%

95,400

72.2%

98,263

74%

1,070

96,470

73.0%

(21,917)

22.7%

74,552

56.4%

18%

23.12

-13%

(10,850)

8.7%

(10,134)

29.7%

44.4%

55.3%

42.2%

(9,741)

14.6%

(17,305)|

4.9%

(43,423)

8.3%

(33,062)

9.0%

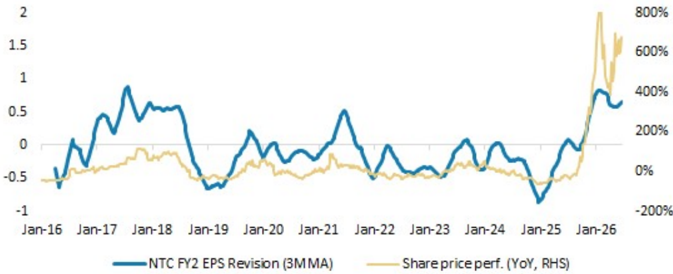

We raise our EPS estimates by 7% for 2026, 15% for 2027, and 14% for 2028. We now expect the 3Q DDR4 price increase to exceed prior expectations, with at least a 30% Q/Q rise versus the previous 20% assumption. DDR4 pricing is likely to remain elevated into 1H27, as the supply-demand gap will be difficult to close by then.

73,533

(8,294)

6,004

257,966 368,367

198,868

Exhibit 21: Nanya Tech: Estimate revisions

88,126

270.152 391,551 223,272

71%

1,067

74,600

59.8%

(12,769)

17.1%

61,830

49.6%

-17%

19.17

-17%

| 16% | 29% 77% 75% | 60% |

|---|---|---|

| 3,998 | 2,639 4,680 4,277 | 4,288 |

| (4,297) -12.6% | 8,643 13.0% 262,646 75.1% 372,644 71.0% | 203,156 55.0% |

| 1,474 | (1,269) (51,224) (72,490) (39,053) 19.5% | |

| 34.3% | 14.7% 19.5% | 19.2% |

| 60.5% 57.2% 2767% 42% | 44.4% -45% | |

| (0.91) -59% | 2.36 -359%| 65.56 2677% 93.08 42% | 50.89 -45% |

| 53.3 | 54.6 117.3 210.4 | 261.3 |

Source: Morgan Stanley Research (E) estimates

Exhibit 22: Nanya Tech: Quarterly financials

Source: Company data, Morgan Stanley Research (E) estimates

5,589

19,524

TolUllcal r/D vallu

Exmbil <o. allyd leull

3.5x

3.0x

2.5x

2.0x

0.5 x

0.0x

M

Nanya Tech: Valuation Methodology

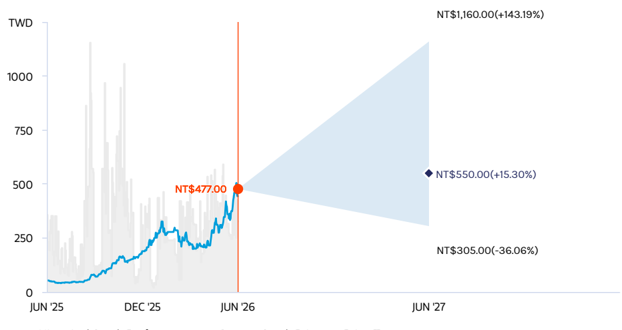

We raise our price target (base case scenario value) from NT$380 to NT$550. Our price target reflects BVPS multiples of 4.50x for 2026 and 2.51x for 2027, versus ROE of 77% for 2026 and 57% for 2027. We expect DDR4 pricing strength and LTAs to drive a rerating. We raise our bull and bear case values from NT$805 and NT$210 to NT$1,160 and NT$305, respectively, implying 9.50x and 2.50x 2026e BVPS.

Exhibit 23: Nanya Tech - Historical P/B band

Oct-15

Source: Company data, Morgan Stanley Research estimates

Cambre co. Tallya leull. Lammlyo coutate leviolut beautil

Sambleet. Tallya leull. Thotutual luwalu rio vo nur

2

1.5

1

0.5

-0.5

P/B multiple(x)

-1

Jan-16 Jan-17 Jan-18 Jan-19 Jan-20 Jan-21 Jan-22 Jan-23 Jan-24 Jan-25 Jan-26

3.5

M

2.0

1.5

1.0

0.5

0.0

Oct-15 Oct-16 Oct-17 Oct-18 Oct-19 Oct-20 Oct-21 Oct-22 Oct-23 Oct-24 Oct-25

— Forward PB

115%

800%

105%

600%

95%

85%

400%

75%

200%

65%

Exhibit 24: Nanya Tech: Historical forward P/B vs ROE

45%

Source: Company data, Morgan Stanley Research estimates

Exhibit 25: Nanya Tech: Earnings estimate revision breadth

Source: Company data, Morgan Stanley Research estimates

— NTC FY2 EPS Revision (3M MA)

- Share price perf. (Yoy, RHS)

M

Risk Reward - Nanya Technology Corp. (2408.TW) Risk Reward - Nanya Technology Corp. (2408.TW)

DDR4 S/D becoming more favorable; OW

NT$550.00 PRICE TARGET

Base case, P/B. We expect the stock to trade at 4.50x 2026, 2.51x 2027, and 2.02x 2028 BVPS, above its average since 2015. We think NTC will benefit from a supply-driven up-cycle as major memory players are exiting the DDR4 market. That should help NTC more than offset the competitive impact from CXMT in the near term.

NT$363.56

Mean

Consensus Price Target Distribution

Source: Refinitiv, Morgan Stanley Research

RISK REWARD CHART

Key:

Historical Stock Performance

Current Stock Price

Source: Refinitiv, Morgan Stanley Research

BULL CASE

NT$1,160.00

9.50x 2026e BVPS

DRAM prices strong; faster-than-expected 1a/1b nm ramp; competition from Korea and China is a non-factor: DRAM pricing becomes very strong in 2026 thanks to production cuts and relief of inventory pressure. NTC's utilization rate returns to the 100% level. Korean and Chinese competitors all exit the consumer DRAM market.

Price Target

BASE CASE

NT$550.00

4.50x 2026e BVPS

Strong DRAM cycle: Major DRAM players now plan to exit the DDR4 market, which positions Taiwanese players to benefit. We expect price -hike momentum to continue through 2026, with widened supply shortage into 2H26.

NT$150.00

NT$560.00

MS PT

Morgan Stanley Estimates

OVERWEIGHT THESIS

- Major memory suppliers are gradually exiting the DDR4 market, benefiting existing Taiwanese players, including Nanya Tech.

- We expect DDR4 shortage into 2H26 to help NTC more than offset the competitive impact from CXMT in 2026. The supply shortage appears set to widen into 2H26.

- Our price target reflects BVPS of 4.50x for 2026, 2.51x for 2027, and 2.02x for 2028.

Consensus Rating Distribution

BEAR CASE

NT$305.00

2.50x 2026e BVPS

Specialty DRAM demand becomes weak in 2026 with intensifying Chinese competition: Nanya Tech could face more pressure from pricing and technological competition amid a weak cycle. Inventory remains at historical peak levels. SK hynix and Chinese DRAM competitors take all the market share in China. Nanya Tech's utilization rate falls to the 40% level.

M

Risk Reward - Nanya Technology Corp. (2408.TW)

KEY EARNINGS INPUTS

| Drivers | Dec 2025 | Dec 2026e Dec 2027e Dec 2028e | Dec 2026e Dec 2027e Dec 2028e | Dec 2026e Dec 2027e Dec 2028e |

|---|---|---|---|---|

| 12" Wafers Out per quarter (000s) | 825.0 | 830.0 | 855.0 | 900.0 |

| Average Wafer Yield (%) | 81.8 | 108.1 | 106.5 | 95.0 |

| Total Die shipments - 2 gb equivalent (mn) | 2,368.0 | 3,178.8 | 3,244.9 | 3,090.4 |

INVESTMENT DRIVERS

- Specialty DRAM pricing

- Monthly sales momentum

- Industry outlook reported by industry peers

GLOBAL REVENUE EXPOSURE

Source: Morgan Stanley Research Estimate View explanation of regional hierarchies here

MS ALPHA MODELS

1/5 MOST

3 Month

Horizon

Source: Refinitiv, FactSet, Morgan Stanley Research; 1 is the highest favored Quintile and 5 is the least favored Quintile

RISKS TO PT/RATING

RISKS TO UPSIDE

- Sustained DRAM prices from more disciplined supply and stronger demand

- Stronger pricing environment, enabling revenue guidance to be beaten

- Faster-than-expected 1a/1b nm ramp-up progress

RISKS TO DOWNSIDE

- Slower-than-expected 1a/1b nm ramp-up

- Less demand for specialty DRAM from 4K2K TVs and smart set-top boxes

OWNERSHIP POSITIONING

Inst. Owners, % Active

51.9%

Source: Refinitiv, Morgan Stanley Research

MS ESTIMATES VS. CONSENSUS

Income Statement

NT$mn (Years End Dec)

Net sales

COGS

2025

Cash Flow Statement

NT$mn (Years

2028E

2026E

2027E

2025

M

Cashflov fror

Net profits

Depreciation

Working Capital

Other adjustmel

Nanya Tech: Financial Summary

Pre-tax income

Income tax

Reported net Income

Adj.wtd.avg.shrs(m)

Reported EPS (NT$)

EPS for consensus (NT$)

Balance Sheet

NT$mn (Years End Dec)

Cash

Mkt Securities

ARINR

Inventory

Other

Current Assets

| 211,423 | 300,154 | 164,103 |

|---|---|---|

| 3,225 | 3,225 | 3,225 |

| 65.56 | 93.08 | 50.89 |

| 65.56 | 93.08 | 50.89 |

| 2026E | 2027E | 2028E |

| 49,669 | 318,534 | 663,173 |

| 59,175 | 63,667 | 37,706 |

| 402,624 | 433,191 | 256,554 |

| 18,025 | 19,056 | 13,103 |

Long-term investments

Fined assets

Other assets

Total Assets

SIT borrowings

APINP

Other ST liabilities

LT debt

Other LT liabilities

Total Liabilities

Common stocks

Preferred stocks

Capital Researve

Retained earning

Other shareholders equity

Total Equity

Total Liab. & Shrhidr's Equity

BVPS

Change of ST Ir

Other adjustmer

Cashflov fror

Increase in L/T c

Increase in SIT.

Cash Dividend F

Dir& Emp Bonus

Proceed fmNew

Other adjustmer

Exchange rate i

Net change i

Financial Ratios

Growth(%)

Turnover

Margins (%)

Gross Margin

Operating Marg

EBITA Margin

Pretax Margin

Net Profit

18,568

7,373

14.034

5,697

(8,536)

(14,110)

(13,441)

(612)

0

(57)

2026E

(197,872)

12,186

211,423

(415,858)

(5,622)

(50,005)

(50,000)

0

0

-

2028E

394,638

164,103

24,404

201,138

4,993

(30,000)

(30,000)

0

0

| (5) 0 0 | (5) 0 0 | (5) 0 0 | (5) 0 0 | (5) 0 0 |

|---|---|---|---|---|

| (6,317) | 238.453 | 5.000 | (20,000) | |

| (6,750) | 3,600 | 0 | 0 | |

| (9,477) | 234,941 | 5,000 | (20,000) | |

| (7,000) | 0 | 0 | ||

| 16,909 | (87) | 0 | 0 | |

| 1,019 | 0 | 0 | ||

| (1,970) -3.829 | -8,405 | 268,865 | 344,638 | |

| 2025 | 2026E | 2027E | 2028E | |

| 95.1 | 425.2 | 50.1 | -29.6 | |

| 23.6 | 78.7 | 78.4 | 62.8 | |

| 9.0 | 73.8 | 70.2 | 53.8 | |

| -11.3 | 70.3 | 65.8 | 47.2 | |

| 13.0 11.1 | 75.1 | 55.0 | ||

| 71.0 |

Return (%)

Gearing (%)

Net Debt/Equity

Liabilities/Equity

Ratios (X)

Current ratio

Quick ratio

Others

ARINR Turnove

Inventory Turno

AP Turnover (da

Cash Conversio

60.5

2027E

293,865

300,154

23,184

(27,513)

(1,960)

(30,000)

(30,000)

0

57.2

44.4

| 4.4 3.6 | 77.0 48.3 | 56.8 36.4 | 21.6 15.6 |

|---|---|---|---|

| 22.2 | 55.0 | (8.2) | (49.9) |

| (22.7) | 76.4 | 44.5 | 33.2 |

| 224 | 291 | ||

| 281 |

203,156

970,535

9,492

137,663

5,145

1,122,836

372,644

834,448

8,538

132,068

5,145

980,198

262,646

529,494

7,583

125,252

5,145

667,473

8,643

108,541

5,904

85,031

8,977

| 240,000 | 245,000 | 225,000 | |

|---|---|---|---|

| 8,576 | 16,122 | 14,662 | |

| 17,772 | 17,797 | 17,792 | ROAE |

| 17,796 | 17,796 | 17,796 | ROAA |

| 4,927 | 4,927 | 4,927 | |

| 289,072 | 301,643 | 280,177 | |

| 30,986 | 30,986 | 30,986 | |

| 33,168 | 33,168 | 33,168 | |

| 314,111 | 614,265 | 778,368 | |

| 0 | 0 | 0 | |

| 378,402 | 678,556 | 842,659 | |

| 667.473 | 980,198 | 1,122,836 | |

| 117.34 | 210.42 | 261.31 |

208,453

NTS mn)

Total Revenues

Sequental Change

Change va Year Ago

Net sales

Cost of Saies

Percent of Revenues

Gross Profit

Gross profit

Percent of Revenues

Total Opex

Percent of Revenues

RSO

Percent of Revenues

Sales and Marketngl

Percent of Revenues

Margins

Profit Before Taxes

Change vs Year Ago

Taxes

16,730

75,120

rovie. Quartelly mialicials

New 2026e Old 2026e Diff.% New 2027e Old 2027e Diff.% New 2028e Old 2028e Diff.%

11,278

12,495

11,116

13,572

17,915

11.340

15

50%

27%

(11,653)

104.8%

1.6%

(12,300)

75,820

109.1%

106.3%

16,783

887

(17,087

102,954

41,003

89,835

30,217

118,635

50,792

32.0%

17.6%

38.8%

77.9%

21,068|

4%

(14,202)

79.3%

6%

3.712

73,014

86%

12.2%

22.1%

(11,701)

(12.184)

89.68%

15,836

M

.7.74

(74)

4.5%

48,281

(59,037

91,960

103.39

(1,537)

34,579

NM

122

25,090

25,775

20,620

4.43

620

102,964

118,435

15.2%

29%

(61,951)

60

47%

(67

37

64%

62%

62%

62%

Hă ні за

685

8.1%

171

171

-150%

(1,529)

-22.7%

(41)

-58%

127

104.8%

106

PSMC: Earnings Estimate Revisions

Tax Rate

Reported Income (TW GAAP)

Percent of Revenues

Change vs Year Ago

EPS (NTS)

(NTS)

Change vs Year Ago

Weighted average shares

BVPS

(1,097)

-99%

149.8%

10.26

NM

4,179

(3,334)

-29.6%

(2.728)

-32%

(654)

14,231

104.9%

-5.2%

70.3%

-23.0%

(0.80)

NM

NM

1397.2%

56.4%

1,294

-138.8%

(0.65)

4,188

Old 2026e

2.658

12.6%

-197.4%

0.31

NM

391|

0.57

New 2027e

Diff. %

(0.16)

NM

3.36

NM

4,191

1727

NM

4,239

4,659

0.4%

52.8

4.000

4,239

42.1

42.2

4,190

natimatad

Manlo, Dassorch (C)

4,659

(12.614)

15%

36%

93.6%

(14)

13000

4.659

(1575)

(8,344

20.0%

28.1%

We raise our EPS forecasts for 2026/27/28 by 4%/48%/62%: This reflects strongerthan-expected DDR3/DDR4 memory pricing. We now expect DDR4 pricing to rise further into 4Q, following the double-digit monthly uptrend. We also incorporate a more meaningful revenue contribution from the 3D AI foundry business (including SiCap, waferon-wafer, and HBM PWF), accounting for 5%/10%/14% of total revenue in 2026/27/28.

Exhibit 26: PSMC: Earnings estimate revision summary

Source: Company data, Morgan Stanley Research (E) estimates

Exhibit 27: PSMC: Quarterly financials

Source: Company data, Morgan Stanley Research (E) estimates

cxmlivn co. Toiviu. Molullcal loi walu r/D

4.0

4

3.5

2.5

3

2.0

1.5

2

1.0

0.5

0.0

1/1/2021

30%

20%

10%

0%

+2 STD: 3.0x

-10%

-20%

+1 STD: 2.3x

PSMC: Valuation methodology

5/1/2021

Dec-20

9/1/2021

1/1/2022

Aug-21 -

P/B

5/1/2022

9/1/2022

1/1/2023

Aug-22

5/1/2023

9/1/2023

1/1/2024

— Forwrad PB (LHS)|

Dec-22

-2 Stdev

5/1/2024

Dec-23 -

-1 Stdev

-30%

-40%

-50%

We raise our price target to NT$111 from NT$88: We incorporate our revised estimates and maintain our P/B valuation methodology. Our new target is based on a 2026e P/B of 2.6x, up from 2.1x previously, and above the historical average of 1.5x since 2021, reflecting our strong conviction in shipments, ASP improvements, and the emerging 3D AI foundry business. We believe PSMC is well positioned to benefit from its Micron partnership, including front-end migration to the 1y process node and back-end opportunities in advanced DRAM production (e.g., HBM). The company is also catching up with the DRAM pricing upcycle.

Exhibit 28: PSMC: Historical forward P/B

Source: Company data, Morgan Stanley Research estimates

Exhibit 29: PSMC: Historical forward P/B vs ROE

Source: Company data, Morgan Stanley Research estimates

P/B (x)

M

Apr-21 -

Apr-23 -

Apr-24 -

M

Risk Reward - Powerchip Semiconductor Manufacturing Co Risk Reward - Powerchip Semiconductor Manufacturing Co (6770.TW)

(6770.TW) Beneficiary of mature node up-cycle and EMIB supply chain

NT$111.00 PRICE TARGET

Base case, 2.6x 2026e P/B. This method is in line with our approach for Greater China memory IDM players, in view of the industry's high volatility. Our 2.6x target P/B is higher than the historical average of 1.5x since 2021, reflecting our optimistic view on improved pricing and utilization.

NT$81.80

Mean

Consensus Price Target Distribution

Source: Refinitiv, Morgan Stanley Research

RISK REWARD CHART

Key:

Historical Stock Performance

Current Stock Price

Source: Refinitiv, Morgan Stanley Research

BULL CASE

NT$177.00

4.2x 2026e BVPS

Strong sales growth with gross margin

expansion : Our assumptions include: 1) a revenue CAGR of >40% in 2025-28; 2) gross margin expanding to 45%+ by 2028; 3) mature node foundry up-cycle longer than expected; 4) faster revenue ramp-up of 3D AI foundry business; 5) longer-than-expected specialty DRAM pricing increase .

Price Target

BASE CASE

NT$111.00

2.6x 2026e BVPS

Revenue growth with gross margin

improvement : Our assumptions include: 1) a revenue CAGR of 36.4% in 2025-28; 2) a gross margin increase to 43% by 2028; 3) a mature node foundry up-cycle; 4) additional contribution from 3D AI foundry business; 5) specialty DRAM pricing continuing to increase.

NT$60.00

NT$111.00

MS PT

Morgan Stanley Estimates

OVERWEIGHT THESIS

- We expect a mature node capacity shortage in 2H27, reflecting fast growth of AI power ICs as a key part of future AI infrastructure.

- 3D AI foundry business is expected to be a major revenue contributor - we expect it to make up 5%/10%/14% of total revenue in 2026/27/28.

- We see specialty DRAM price hikes continuing throughout 2026.

- Our new target is based on 2026e P/B of 2.6x, up from 2.1x - higher than the historical average of 1.5x since 2021, reflecting our optimistic view on improved pricing and utilization.

Risk Reward Themes

Disruption:

Positive Positive

Pricing Power:

View descriptions of Risk Rewards Themes here

BEAR CASE

NT$55.00

1.3x 2026e BVPS

Revenue decline with gross margin erosion :

Our assumptions include: 1) a revenue CAGR in the single digits (%) in 2025-28; 2) gross margin of <10% by 2028; 3) mature node foundry capacity no longer in shortage; 4) delays in revenue contribution from 3D AI foundry business; 5) decreases in specialty DRAM pricing.

M

Risk Reward - Powerchip Semiconductor Manufacturing Co (6770.TW)

KEY EARNINGS INPUTS

| Drivers | Dec 2025 | Dec 2026e | Dec 2027e | Dec 2028e |

|---|---|---|---|---|

| Wafer shipment (k 8 inch) | 2,614 | 2,881 | 2,965 | 755 |

| Wafer ASP (USD) | 457.7 | 474.7 | 517.3 | 522 |

| Utilization rate (%) (%) | 79.1 | 90.3 | 94.3 | 95 |

INVESTMENT DRIVERS

- Demand from consumer electronics clients

- Inventory in the supply chain

- Utilization rate

- Long-term agreements with clients

GLOBAL REVENUE EXPOSURE

Source: Morgan Stanley Research Estimate View explanation of regional hierarchies here

MS ALPHA MODELS

3 Month

Horizon

Source: Refinitiv, FactSet, Morgan Stanley Research; 1 is the highest favored Quintile and 5 is the least favored Quintile

RISKS TO PT/RATING

RISKS TO UPSIDE

- Pricing power is sustained in 2026.

- Listing on main board attracts investment fund flows.

- Aluminum process enjoys higher margins.

RISKS TO DOWNSIDE

- Competition from China intensifies.

- Price erosion is faster than expected.

- Demand from consumer electronics clients weakens further.

- Inventory in the supply chain takes longer to digest.

OWNERSHIP POSITIONING

Inst. Owners, % Active

21.3%

Source: Refinitiv, Morgan Stanley Research

MS ESTIMATES VS. CONSENSUS

Samble ou. 1 manual vultmlary

Income Statement

NTS mn (Years End Dec)

Net sales

COGS

Gross profit

R&D

SG&A

2027 e

2026e

2025

46,730

102,954

75,820

2028e

118,635

(48,267) (59,037) (61,951)

(67,843)

Cash Flow Statement

NTSmn (Years End Dec)

Cash flow from Operations

Net profits

2025

7,823

(7,813)

M

Pre-tax income

Income tax

Net income

Balance Sheet

NTSmn (Years End Dec)

Cash

Mkt Securities

AR/NR

Inventory

Other

Current Assets

Long-term investments

Fixed assets

Other assets

Total Assets

S/T borrowings

AP/NP

Other ST liabilities

LT debt

Other LT liabilities

Total Liabilities

Common shares

Retained earning

Other shareholders' equity

Change of ST Investment

Other adjustments

PSMC: Financial Summary

(1.87)

2025

16,789

2,800

6,550

9,557

8,451

44,148

49

122,004

12,485

178,686

0

2,997

19,789

73,900

96,685

42,259

11,792

27,950

Total Equity

82,000

Total Liab. & Shrhidr's Equity 178,686

4.80

2026e

166,284

2,800

4,846

5,748

8,451

188,129

49

109,520

12,485

310,183

4,548

34,912

73,900

113,360

46,459

97,214

53,150

196,823

310,183

E = Morgan Stanley Research Estimates

Source: Morgan Stanley Research, Company Data

5.61

2027e

49

0

7.16

2028e

284,117

2,800

7,583

6,605

8,451

309,556

49

101,547

12,485

423,637

5,226

43,650

0

73,900

122,776

46,459

201,252

53,150

300,861

423,637

003611.80.20 ватт

Cash Dividend Paid

Dir& Emp Bonus Paid

Exhibit 30: Financial Summary

Other Adjustments

(11,657)

Net change in cash

Financial Ratios

Growth(%)

Turnover

Operating profits

Pretax profits

Net profits

EPS

Margins (%)

Gross Margin

Operating Margin

Pretax Margin

Net Profit

Return (%)

ROAA

ROAE

Gearing (%)

Net Debt/Equity

Liabilities/Equity

Ratios (X)

Current ratio

Quick ratio

Others

AR/NR Turnover (days)

Inventory Turnover (days)

AP Turnover (days)

Cash Conversion (days)

2028e

39,674

33,370

5,594

0

710

0

0

0

| 5,860 | |||

|---|---|---|---|

| 2025 | 2026e | 2027e | |

| 2028e | |||

| 4.5 | 62.3 | 35.8 | 15.2 |

| 3.2 | (335.9) | N/A 40.4 | N/A 27.8 |

| 9.4 | (410.9) | ||

| N/A | N/A | N/A | NIA |

| N/A | N/A | N/A | N/A |

| 39.8 | 42.8 | ||

| (3.3) | 22.1 | 34.6 | |

| (20.5) | 29.8 31.0 | ||

| (16.0) | 30.7 31.7 | 35.2 |

(16.7)

(4.3)

28.2

25.4

28.1

8.7

(9.2)

69.6

15.3

(46.9)

7.8

11.8

(60.3)

8.5

12.2

(69.9)

57.6

117.9

47.8

40.8

| 1.9 1.1 | 4.8 | 5.6 | 6.3 |

|---|---|---|---|

| 4.4 | 5.3 | 6 | |

| 23.3 | 23.3 | 23.3 | 23.3 |

| 35.5 | 35.5 | 35.5 | 35.5 |

| 28.1 | 28.1 | 28.1 | 28.1 |

| 30.7 | 30.7 | 30.7 | 30.7 |

Source: Company data, Morgan Stanley Research (E) estimates

(7,477)

23,249

32,649

41,721

12,145

0

2026e

48,112

0

0

0

2027e

32,691

0

0

Exibil ol. Macrottk. Lammys Lottale neviolulls

(NTS mn)

New 2026e

(NT$ mn)

Total Revenues

Sequential Change

Net sales

Total Opex

1Q27e

Diff.%

4Q26e

32,181

34,004

54.0%

5.7%

2Q27e

New 2027e

3027e

36,865

36,197

8.4%

143,216

-1.8%

17%

3026e

Old 2026e

2Q26e

14,309

36.7%

20,894

46.0%

66,682

1Q26

10,469

35.4%

,854

77

M

Diluted EPS

R&D

20,28e

3Q28e

Diff.%

New 2028e

36,025

4Q28e

35,989

-0.1%

14%

17%

-0.5%

(17,422)

20%

(17,414)

18,642

18,611

51.7%

20%

20%

(3,583)

9.9%

20%

25.02

4027e

Old 2027e

1Q28e

36,150

36,106

-0.1%

-0.1%

12.3%

126,013

6.2%

(17,648)

61,874

(17,431)

18,502

18,674

48,496

51.2%

51.7%

48,421

(3,547)

(3,565)

9.8%

40,998

20.82

9.9%

34%

7.35

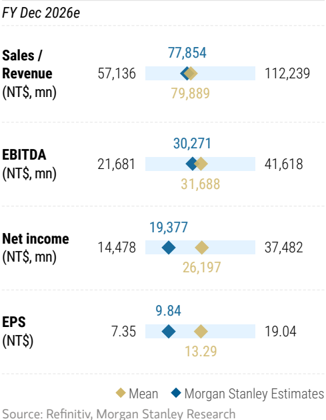

9.84

Macronix: Earnings Estimate Revisions

General and Admin

Percent of Revenues

Operating margin

Operating Income

Percent of Revenues

Pretax margin

Net margin

Total Non-operating Income(Loss)

Profit Before Taxes

Percent of Revenues

NT$

Change vs Year Ago

Taxes

BVPS

Tax Rate

-0.1%

-0.4%

144,185

74,529

60,159

(17,388)

18,601

51.7%

60,170

(3,620)

10.1%

50,950

25.88

(1,631)

4.5%

(1,461)

4.1%

51.7%

(528)

41.7%

2027e

2026e

2025

Old 2028e

28,880

11.6%

127,564

(23,749)

5,131

17.8%

(8,829)

30.6%

(5,714)

19.8%

(1,520)

5.3%

(1,594)

143,216

77,854

169.6%

84.0%

(44,185)

(71,019)

63,549

49,869

72,197

33,669

43.2%

50.4%

49,813

(10,936)

(14,010)

14.0%

9.8%

42,178

21.42

7.4%

(5,764)

(3,161)

4.1%

(6,084)

4.2%

49.8%

(2,011)

Diff.%

2028e

144,185

13%

0.7%

17%

(69,656)

21%

74,529

51.7%

21%

21%

(14,369)

10.0%

21%

(6,404)

4.4%

(5,814)

4.1%

1.9 ppt

(2,112)

39.1%

(5,854)

4.1%

(2,112)

(528)

(528)

40.6%

(528)

(528)

38.5%

We raise our 2026/27/28 EPS forecasts by 34%/20%/21%: This reflects stronger-thanexpected memory pricing across NOR flash and SLC/MLC NAND. SLC/MLC NAND pricing is likely to continue rising into 4Q, following the 50-60% increase in 3Q. NOR pricing could increase by 30-40% in 3Q and extend into 4Q. 71.17 16% -12.6% 29.4% 40.6% 41.7%

(2,027)

(503)

2.4%

25.4%

5,924

25.6%

28.4%

21.7%

(9)

5,914

28.3%

Old '26E

-720.0%

(905)

28.92

29.2%

29.4%

24.9%

New '26E

31.41

Exhibit 31: Macronix: Earnings Estimate Revisions

Percent of Revenues

Minority Interest

Reported Income (TW GAAP)

Percent of Revenues

Change vs Year Ago

Reported Diluted EPS (NTS, TW GAAP)

Reported Basic EPS (NTS, GAAP)

15.3%

(2,293)

15.3%

(2,293)

12,694

34.4%

12,692

15.3%

(2,288)

12,666

(2,293)

15.3%

12,693

35.3%

328

9.0%

(3,305)

-11.4%

15.2%

(3,468)

(8,900)

19,391

24.9%

15.3%

49,271

34.4%

(9,206)

15.3%

50,964

35.3%

| (4) (4) | (4) (4) (4) | (4) | (4) (4) | (4) (4) | (4) | (4) (3) | (14) (14) (14) |

|---|---|---|---|---|---|---|---|

| 1,776 2,845 5,006 | 9,750 11,216 | 12,690 | 12,689 12,662 | 12,795 | 12,713 12,690 | (3,308) 19,377 | 49,257 50,950 |

| 17.0% -303.4% 19.9% -322.9% 24.0% -679.9% | 30.3% -3402.5% 33.0% 531.6% | 34.4% 346.0% | 35.1% 153.5% 35.0% 29.9% | 35.4% 14.1% | 35.3% 0.2% 35.3% 0.2% | -11.5% 2.9% 24.9% -685.8% | 34.4% 154.2% 35.3% 3.4% |

| 0.90 1.44 2.54 | 4.95 5.70 | 6.44 | 6.44 6.43 | 6.50 | 6.46 6.44 | (1.78) 9.84 | 25.02 |

| 0.90 1.44 2.54 | 4.95 5.70 | 6.44 | 6.44 6.43 | 6.50 6.48 | 6.46 6.44 | (1.78) 9.84 | 25.02 25.88 25.88 |

Source: Company data, Morgan Stanley Research (E) estimates

Exhibit 32: Macronix: Quarterly financials

Source: Company data, Morgan Stanley Research (E) estimates

35.0%

35.1%

24.0%

33.0%

51.7%

10

(8)

P/B multiple(x)

6.0

M

3.0

80%

70%

60%

50%

40%

30%

Macronix: Valuation Methodology

1.0

0.0

1 vi waru r/e vo. nUML

— Forward PB (LHS)

ROAE (%)

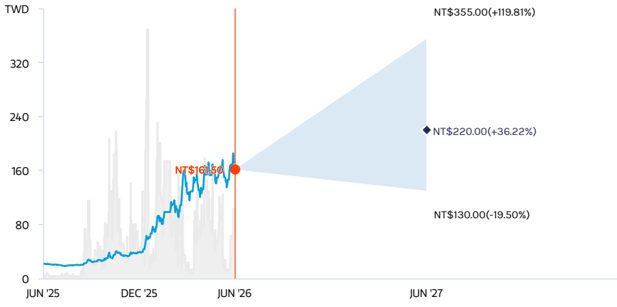

We raise our price target to NT$220 from NT$202: We continue to use a P/B multiple methodology to derive our price target, in line with our approach for Greater China memory IDM peers and in view of the industry's high volatility. Historically, forward P/B has had a similar trend vs. ROAE, and as we expect a net profit turnaround driven by elevated prices, we believe the stock will trade up to 7.0x 2026e BVPS (same as our prior target) vs. its historical band of 0.5x-1.5x since 2017.

We raise our bull case value to NT$355, which is 11.3x our 2026e BVPS, and our bear case value to NT$130, which is 4.1x our 2026e BVPS.

Exhibit 33: Forward P/B vs. ROAE

Source: Factset, Morgan Stanley Research

M

Risk Reward - Macronix International Co Ltd (2337.TW) Risk Reward - Macronix International Co Ltd (2337.TW) Top Pick

Top Pick; OW on legacy Flash opportunities

NT$220.00 PRICE TARGET

Base case, P/B, in line with our Greater China memory coverage, due to the memory industry's cyclical nature. We apply a target multiple of 7.0x to our 2026 BVPS estimate, vs. its historical average of 1.5x since 2017. We continue to believe the P/B target is justifiable, as The MLC and legacy TLC NAND could be in greater shortage into 2H26, with under supply easily going up to 40%. The only supplier which could fill the gap remains Macronix.

NT$198.87

MS PT

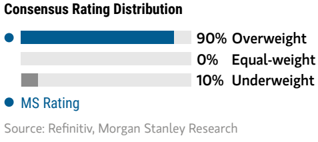

Mean

Consensus Price Target Distribution

Source: Refinitiv, Morgan Stanley Research

RISK REWARD CHART

Key:

Historical Stock Performance

Current Stock Price

Source: Refinitiv, Morgan Stanley Research

BULL CASE

NT$355.00

11.3x 2026e BVPS

Higher than expected price hike for legacy NAND, and signi fi cant price hike for NOR throughout 2026: NAND revenue grows 1200%+, and NOR flash revenue grows 150%+ Y/Y in 2026.

Price Target

BASE CASE

7.0x 2026e BVPS

Signi fi cant price hike for legacy NAND, and continued price hike for NOR throughout 2026: NAND revenue grows 833%, and NOR

flash revenue grows 130% Y/Y in 2026.

NT$80.00

NT$300.00

Morgan Stanley Estimates

NT$220.00

OVERWEIGHT THESIS

- MLC and legacy TLC NAND could be in greater shortage into 2H26, with under supply easily going up to 40%. The only supplier which could fill the gap in our view remains Macronix. Pricing for MLC and legacy TLC could could rise over 200% from 1Q26 to 4Q26.

- We expect low-single-digit NOR undersupply throughout 2026, driven by capacity cannibalization from other highmargin products.

- ROM may benefit from the Nintendo Switch 2, which started selling in June 2025. ▪ We view the current P/B valuation as

- attractive given the strong near-term outlook.

Risk Reward Themes

Pricing Power:

Positive

Secular Growth:

Positive

View descriptions of Risk Rewards Themes here

BEAR CASE

NT$130.00

4.1x 2026e BVPS

Moderate price hike for legacy NAND, and fl attish price for NOR throughout 2026:

NAND revenue grows <150%, and NOR flash revenue grows <80% Y/Y in 2026.

M

Risk Reward - Macronix International Co Ltd (2337.TW)

KEY EARNINGS INPUTS

| Drivers | Dec 2025 | Dec 2026e | Dec 2027e | Dec 2028e |

|---|---|---|---|---|