PDF 原檔:報告_Daiwa_日月光3711_20260709_original.pdf

圖片清單(已驗證 2026-07-13)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Daiwa_日月光3711_20260709_001.png |

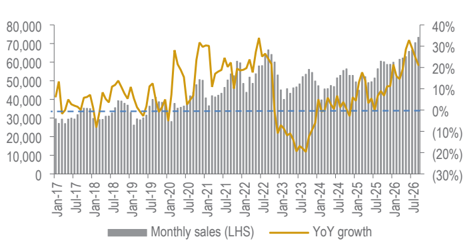

57KB | 真資料圖 | 月營收長條圖(2017-2026)疊加 YoY 成長率折線,2026 下半年月營收突破 6-7 萬(TWD mn) |

報告_Daiwa_日月光3711_20260709_002.png |

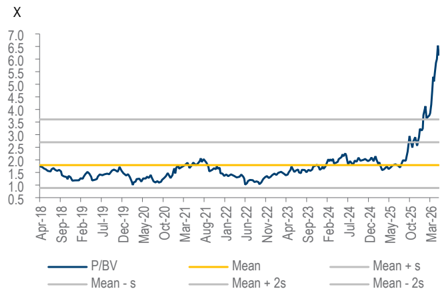

43KB | 真資料圖 | P/BV 趨勢圖(2018-2026),2025 下半年起大幅偏離歷史均值與 +1/+2 標準差區間,2026 中衝上約 6.5x |

原始內容

ASE Technology Holding (3711 TT)

Share price (9 Jul): TWD677.00

12-mth rating: Outperform (2)

Intact revenue run-rate but perhaps not valuation

Rick Hsu (886) 2 8758 6261

rick.hsu@daiwacm-cathay.com.tw

Sharon Kao

(886) 2 8758 6255 sharon.kao@daiwacm-cathay.com.tw

Summary: ASE Technology Holding (ASE) reported intact 2Q26 revenue thanks to the accelerated AI demand strength and sustained automotive & industrial (A&I) recovery. Assuming the 2 demand drivers will continue, we are comfortable with our 2Q26 bottomline estimate and forecasts for ASE's 3Q26 outlook. That said, the share price has surged c.2.7x YTD, raising our concern that it seemed to be running too far ahead of fundamentals, though we rate the stock Outperform (2). ASE is scheduled to report 2Q26 results by end-July, and we will be visiting our model in due course.

Highlight

- Revenue run-rate intact but … ASE reported June sales of TWD65.8bn, up 4% MoM (+33% YoY) which concluded its 2Q26 topline at TWD191bn, up 10% QoQ (+27% YoY) and roughly in line with our/consensus estimates of TWD188bn. Nevertheless, while the EMS revenue looks intact, we estimate its IC ATM (ie, OSAT) revenue at TWD125126bn, 2% above our estimate thanks to the accelerated AI demand strength benefiting its leading-edge advanced packaging (LEAP) business, as well as a sustained A&I recovery benefiting its mainstream OSAT business, plus pricing power (see our note on 29 April, Entering an even stronger earnings cycle ). That said, its share price seemed to be running too far ahead of fundamentals despite the LEAP strength, in our opinion.

- Near-term preview and outlook. We expect ASE to have earned net profit of c.TWD17bn for 2Q26, not varying much from the consensus estimate. Given the intact 2Q26 topline run-rate, we are comfortable with our current expectation. As for 3Q26, we forecast its consolidated revenue to advance 12% QoQ to TWD210bn (+25% YoY) for net profit of TWD21bn, up 24% QoQ (+94% YoY) which also doesn't vary much from the consensus forecast, thanks to the continued AI strength and A&I recovery backed by hyperscalers' active AI datacentre infrastructure build. ASE is scheduled to report 2Q26 results by end-July, and we will be reviewing our model in due course.

Recommendation

We rate ASE Outperform (2) against the backdrop of its business strength on the accelerated AI ramp and sustained A&I recovery. Yet, the stock has surged c.2.7x YTD, raising our concern that it seemed to be running too far ahead of fundamentals for a risk of an expectation reset, since the stock trades at 5.9x 2027E PBR and 32x 2027E PER. Key downside risk to our call would be any price hike across the supply chain inducing 'silicon inflation' for hyperscalers' AI capex cuts.

9 July 2026

Information Technology: Taiwan

ASE: monthly revenue run-rates

Source: Company

ASE: 2Q26 results preview and 3Q26 preliminary outlook

| 2Q26E | 2Q26E | 2Q26E | 3Q26E | 3Q26E | 3Q26E | |

|---|---|---|---|---|---|---|

| TWDm | Daiwa | Consensus | Variance | Daiwa | Consensus | Variance |

| Revenue | 188,319 | 188,449 | 0% | 210,381 | 207,693 | 1% |

| Gross profit | 39,943 | 45,536 | ||||

| Operating profit | 21,789 | 27,389 | ||||

| Pretax profit | 21,389 | 26,489 | ||||

| Net profit | 17,068 | 16,737 | 2% | 21,138 | 20,661 | 2% |

| Adjusted EPS (TWD) | 3.83 | 3.75 | 2% | 4.74 | 4.63 | 2% |

| Margin | ||||||

| Gross | 21.2% | 21.6% | ||||

| Operating | 11.6% | 13.0% | ||||

| Net | 9.1% | 10.0% | ||||

| Operation | ||||||

| Wirebonder utilisation | 80% | 80% | ||||

| Tester utilisation | 80% | 85% | ||||

| Bumping utilisation | 80% | 82% |

In the interests of timeliness, this document has not been edited.

Source: Bloomberg, Daiwa forecasts

ASE: PBR trend

Source: Company, TEJ, Daiwa estimates and forecasts