PDF 原檔:260602_hsbc_korea-ai-supply-chain_original.pdf

PDF 原檔:260602_hsbc_korea-ai-supply-chain_original.pdf

原始內容

Korea Technology

Korea tech tour -booming agentic AI supply chain while physical AI waits in the wings

- ◆ Tech companies are enjoying the AI boom; benefits from GPU/CPU processors, optical communication and 800V DC conversion

- ◆ Memory earnings are the most solid, while equipment and materials earnings are about to take off

- ◆ We prefer Samsung and EO Technics amid AI demand boom

Key takeaways: We hosted our 2026 Korea tech tour on 27-29 May, with 14 companies across memory, semi equipment, materials, and the tech hardware supply chain. Most companies expressed an upbeat outlook: 1) memory/substrate/ MLCC are benefiting from CSP capex increases for agentic AI and tech upgrades to CPUs, optical interconnect and 800v power shift; 2) IT hardware is starting to encompass the robotic momentum; and 3) semi equipment and materials companies will benefit from aggressive capex and capacity expansion at memory makers. With robust demand and tight capacity, we are more constructive on the supply chain. Our key takeaways are below.

Memory: CSP capex is soaring and demand catalysts are moving to CPU customers, as it is more feasible to manage AI agents vs GPU, and HBM3e prices will increase to narrow the gap with commodity. Robust x86 and ARM based CPU demand are boosting server and mobile DRAM prices; memory makers will enjoy output increases in 2H26 and margin expansion as more LTA agreements will stabilize the earnings trend.

Tech hardware -focus on FC-BGA: The package substrate sector is a clear AI beneficiary as well. High-end FC-BGA demand is running ahead of supply, signalling high utilisation and extending lead times; customers are seeking LTAs and co-investment to secure capacity. Structural drivers such as larger and higher layer bodies, silicon capacitor embedding, and glass core substrates are lifting content per unit, supporting a multi-year growth story.

Semi equipment & materials -plenty of runway left: The tour brought fresh datapoints across our coverage. EO Technics is seeing laser full-cut beginning to displace mechanical dicing in HBM, alongside a sharp PCB drilling ramp and a debonder co-development with a leading foundry; HPSP is broadening its reach with a new DRAM customer expected in 3Q26, and NAND customer engagements. Park Systems is winning AFM traction in hybrid bonding and advanced packaging metrology; and Hansol Chemical is advancing precursor with optionality into the late-2026 patent expiry of hafnium based high-K precursors. Given the strong capex ramp, these point to content and customer expansion independent of bit-growth; we favour these moat and pricing power names where earnings momentum looks well supported.

Our preference: We prefer Samsung Electronics in memory as we expect it to narrow the tech gap not only in HBM4 but also commodity DRAM vs peers. In semi equipment, we prefer EO Technics as it continues to see stronger demand of its laser equipment, through application expansion and new customer engagement at the front and back end.

Disclosures & Disclaimer

This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and with the Disclaimer, which forms part of it.

Equities Semiconductors & Equipment

Korea

Ricky Seo*

Head of Korea Research, Semiconductor and Display The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch rickyjuilseo@kr.hsbc.com +82 2 3706 8777

Han Kil Chang*

Research Analyst, Korea Technology The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch han.kil.chang@kr.hsbc.com +822 3706 8750

- Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is not registered/ qualified pursuant to FINRA regulations

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch

Exhibit 1. Key ratings, target prices and data points

| Company | Ticker CCY | CMP | TP | Rating | Upside | Mkt cap (USDm) | 3M ADTV (USDm) | 2026e PE(x) | 2027e PE(x) | 2026e PB(x) | 2027e PB(x) | 2026e ROE | 2027e ROE |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Samsung Elec | 005930.KS KRW | 349,000 | 450,000 | Buy | 29% | 1,353.5 | 4,561 | 8.4 | 6.2 | 3.3 | 2.3 | 53% | 49% |

| SK Hynix | 000660.KS KRW | 2,363,000 | 2,900,000 | Buy | 23% | 1,117.2 | 4,385 | 8.2 | 5.6 | 5.3 | 2.8 | 91% | 64% |

| EO Technics | 039030.KQ KRW | 450,000 | 550,000 | Buy | 22% | 3.7 | 37 | 47.5 | 34.2 | 7.1 | 6 | 16% | 19% |

| HPSP | 403870.KQ KRW | 46,600 | 65,000 | Buy | 39% | 2.5 | 105 | 28.3 | 18.1 | 9.4 | 6.9 | 38% | 44% |

| Park Systems | 140860.KQ KRW | 278,000 | 360,000 | Buy | 29% | 1.3 | 9 | 35.4 | 23.6 | 7 | 5.6 | 22% | 26% |

| Hansol Chemical | 014680.KS KRW | 260,500 | 400,000 | Buy | 54% | 2.0 | 16 | 14.6 | 11.4 | 2.3 | 1.9 | 17% | 18% |

Source: Bloomberg, HSBC estimates. Priced at close of 1 June 2026

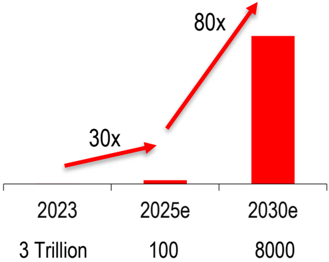

Exhibit 2. Daily token consumption from AI services is growing rapidly

Source: CIC estimates, (See: China Technology -AI optical interconnect series; how many optical transceivers do we need? , 14 May 2026)

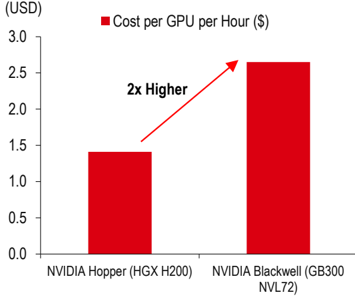

Exhibit 4. The cost per GPU has risen 2x in the latest NVIDIA GB300 …

Source: NVIDIA -Rethinking AI TCO (15 Apr 2026). Note: (NVDA US, USD211.14, Buy)

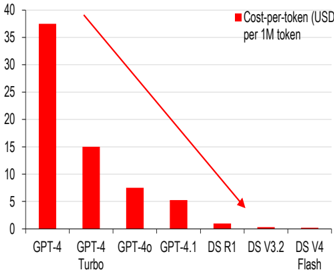

Exhibit 3. While frontier LLM API blended pricing continues to fall

Source: OpenAI, DeepSeek, HSBC Qianhai Securities. Note: *Blended cost = 75% input +25% output. (See: China Technology -AI optical interconnect series; how many optical transceivers do we need? , 14 May 2026)

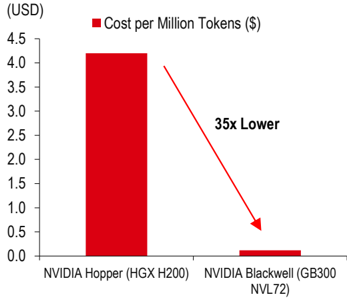

Exhibit 5. Cost per million tokens has fallen by 35x, boosting profitability at AI service providers

Source: NVIDIA - Rethinking AI TCO (15 Apr 2026)

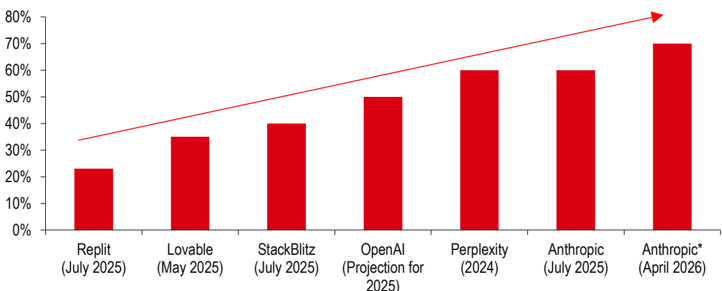

Exhibit 6. Gross profit margin estimates of AI service providers

2025)

Source: The Information, Semianalysis for Anthropic data for April 2026, Note: Perplexity, Replit, Lovable and StackBlitz do not incorporate the costs of running AI models for non-paying users in calculations, while Open AI does. Anthropic ' s accounting method is not disclosed.

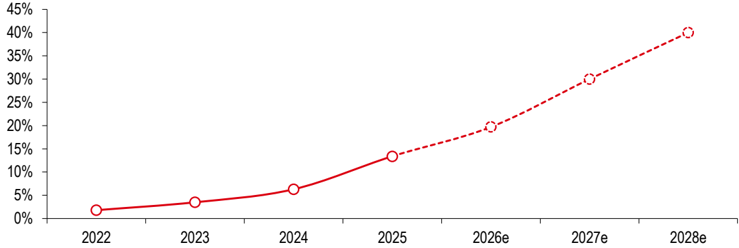

Exhibit 7. Forecast penetration rate of ARM based CPUs in the total CPU market

Penetration rate of ARM CPUs in the overall CPU market

Source: TrendForce, HSBC estimates.

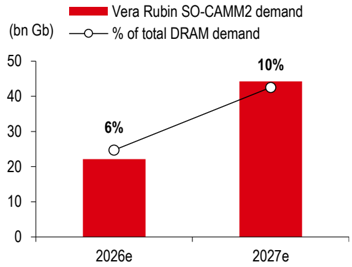

Exhibit 8. SO-CAMM2 demand estimates from the Vera Rubin platform; 6-10% of total DRAM demand

Thousands

Source: HSBC estimates

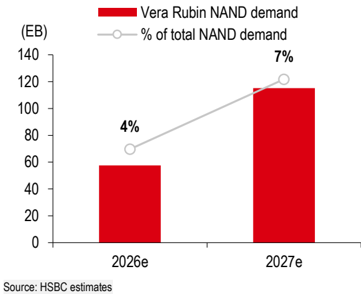

Exhibit 9. NAND demand estimates from the Vera Rubin platform; 4-7% of total NAND, opportunities from ICMS

Source: HSBC estimates

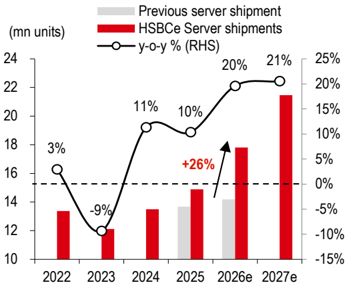

Exhibit 10. HSBC global tech team recently revised up server shipments, expecting 20%/21% y-o-y growth in 2026/27e

Thousands

Source: TrendForce, HSBC estimates (see: Global tech hardware - Agentic AI is reshaping the server market , 5 March, Carol Juan)

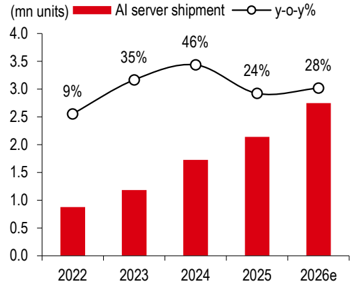

Exhibit 12. AI server shipments to grow 28% y-o-y in 2026e

Source: TrendForce

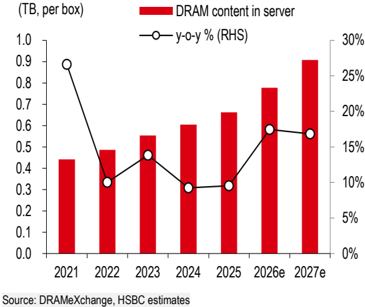

Exhibit 14. Average server DRAM content per unit; strong growth of 17% in 2026-27e

Source: DRAMeXchange, HSBC estimates

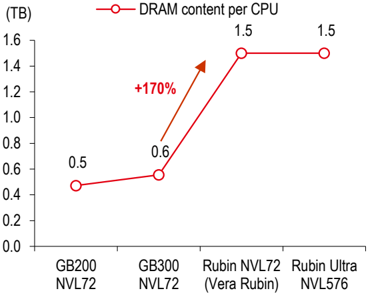

Exhibit 11. Accelerating DRAM content growth in the latest Vera Rubin servers

Source: Company data, HSBC estimates

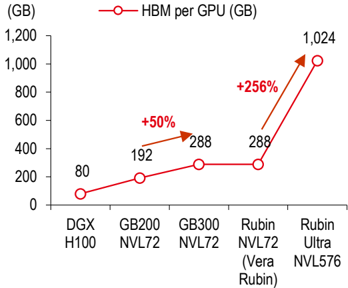

Exhibit 13. HBM content to increase significantly in the Rubin Ultra

Source: Company data, HSBC estimates

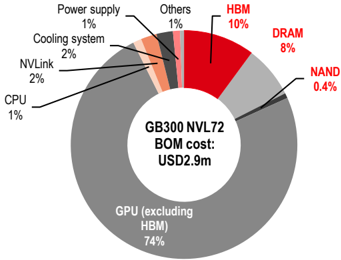

Exhibit 15. Bill of materials cost estimates for the GB300 NVL72 server system

Source: HSBC estimates

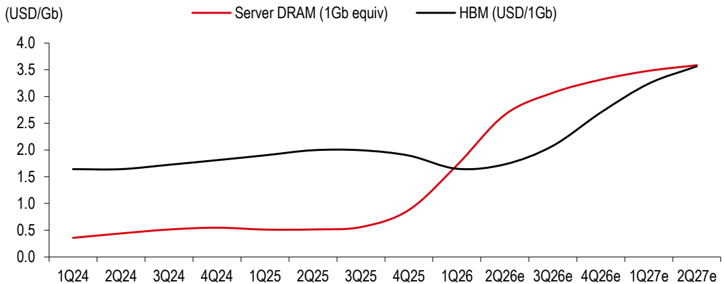

Exhibit 16. Server DRAM vs HBM blended ASP trend (calendar year base)

Source: Company data, HSBC estimates

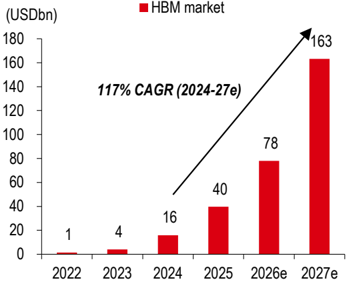

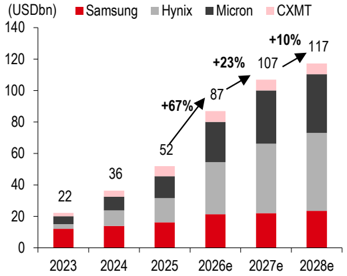

Exhibit 17. HBM market growth set to reach USD163bn by 2027e

Source: Company data, HSBC estimates

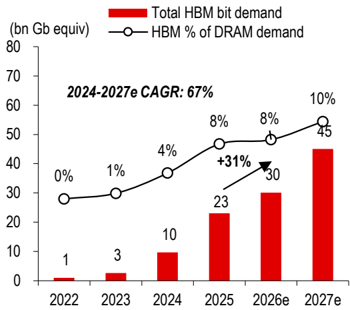

Exhibit 18. HBM bit demand growth: CAGR of 67% in 2024-27e

Source: Company data, HSBC estimates

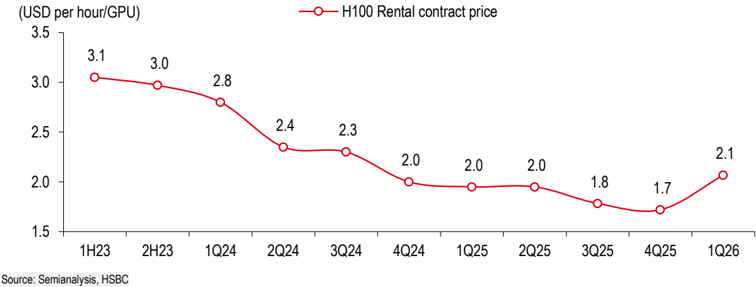

Exhibit 19. One-year contract price trend of AI GPUs (H100) for AI service providers

Source: Semianalysis, HSBC

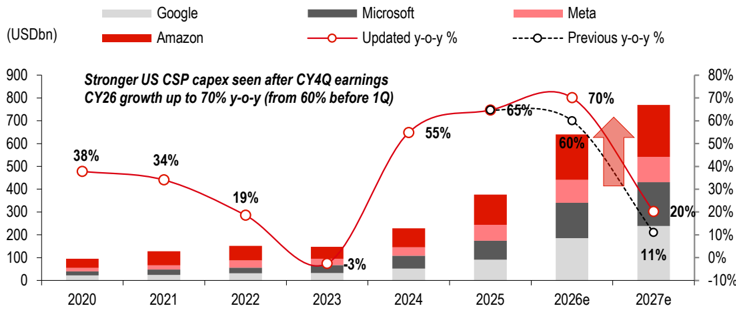

Exhibit 20. US cloud service provider (CSP) capex; robust growth to continue at key US CSPs, up 70% in 2026e

Source: Company data, Bloomberg consensus estimates. Note: Alphabet (GOOGL US, USD380.34, Buy), MSFT (MSFT US, USD450.24, Buy), Meta (Meta US, USD632.51, Buy), Amazon (AMZN US, USD270.64, Buy)

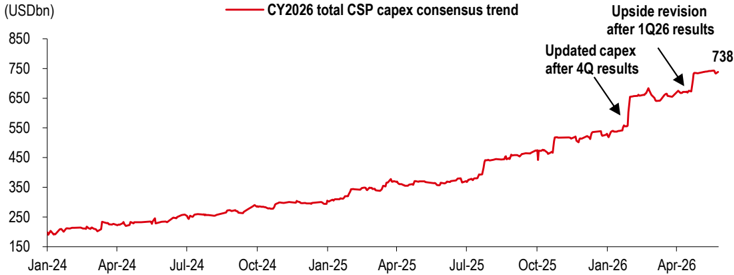

Exhibit 21. Capex consensus of key global CSPs (US & Chinese) for 2026; continued upside revisions; expected at USD738bn (+80% y-o-y)

Source: Company data, Bloomberg, HSBC.

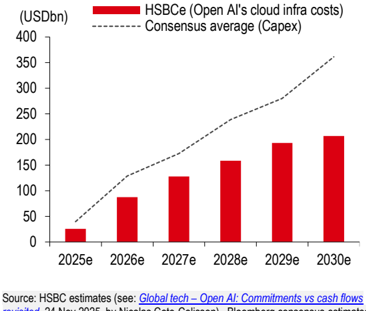

Exhibit 22. Open AI ' s cloud infra costs continue to grow

Source: HSBC estimates (see: Global tech -Open AI: Commitments vs cash flows revisited , 24 Nov 2025, by Nicolas Cote-Colisson) , Bloomberg consensus estimates

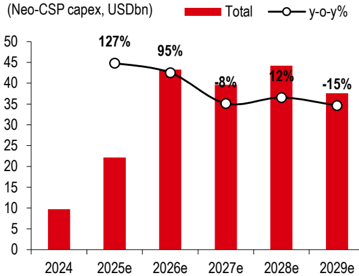

Exhibit 23. Capex estimates of key neoCSPs; strong growth in 2026e

Thousands

Source: Company data, Bloomberg consensus estimates

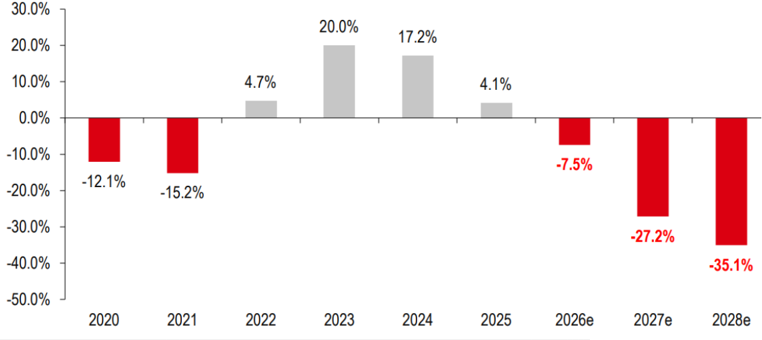

Exhibit 25. Global Abr substrate demand growth trend (k sqrt/year)

Exhibit 24. Global ABr substrate supply vs demand gap

30.0%

240,000

20.0%

210,000

180,000

10.0%

0.0%

-10.0%

150,000

120,000

-20.0%

90,000

60,000

-30.0%

30,000

-40.0%

0

-50.0%

PC

AI GPU/ASIC

4.7%

-12.1%

-15.2%

2020

2021

2022

2023

Source• TrendForce HSRC estimates /see Asia Technoloav - ARF suhstrate• Al unevcle is just heainnina 27 Anril 2026)|

2020

2021

2022

Source• TrendForce comnany data HSRC estimates (see Asia Technoloav - ARF substrate• Al unevele is just heainnina 27 Anril 2026)

Gaming GPU

- YoY (%)

-7.5%

50%

40%

30%

20%

Exhibit 24. Global ABF substrate supply vs demand gap

• 0%

Source: TrendForce, company data, HSBC estimates (see Asia Technology - ABF substrate: AI upcycle is just beginning , 27 April 2026)

Exhibit 25. Global ABF substrate demand growth trend (k sqft/year)

Source: TrendForce, HSBC estimates (see Asia Technology - ABF substrate: AI upcycle is just beginning , 27 April 2026)

Exhibit 26. Global DRAM capex trend

Source: Company data, HSBC estimates, TrendForce. Note: Micron technology (MU US, USD971, Buy.

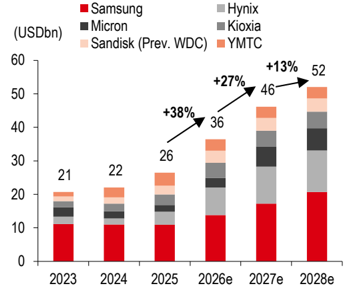

Exhibit 27. Global NAND capex trend

Source: Company data, HSBC estimates, TrendForce. Note: Kioxia (285A JP, JPY72,500, Not rated), Sandisk (SNDK US, USD1694.98, Not rated), WDC (WDC US, USD531.21, Not rated)

20.0%

Server

Others

17.2%

4.1%

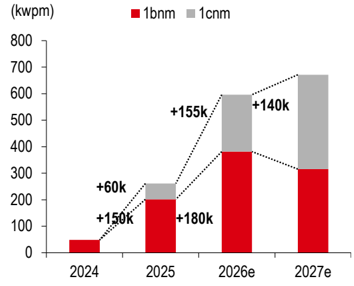

Exhibit 28. Samsung: Advanced DRAM capacity trend (1b and above)

Source: TrendForce, HSBC estimates. Note: Based on wafer input.

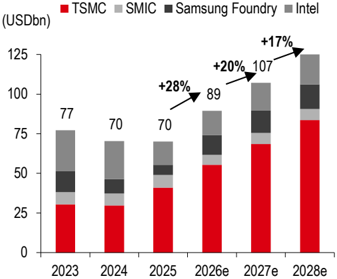

Exhibit 30. Global foundry capex of top 4 suppliers set to grow 28%/20% in 2026/27e

Source: Company data, HSBC estimates. TSMC (2330 TT, TWD2,355, Buy), SMIC (0981 HK, HKD79.45, Buy), Intel (INTC US, USD114.68, Buy)

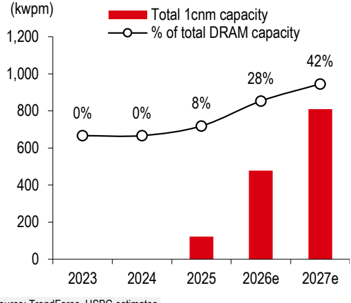

Exhibit 29. Industry total 1cnm capacity growth estimates, reaching 42% of total DRAM by 2027e

Source: TrendForce, HSBC estimates.

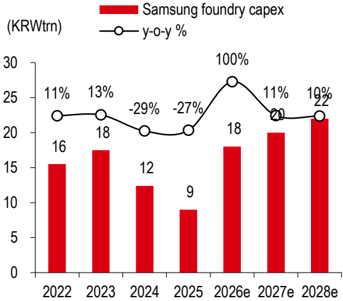

Exhibit 31. Samsung foundry capex should rise 100% y-o-y in 2026e from investments in leading edge node capacity

Source: Company data, HSBC estimates

Exhibit 32. Valuation comparison vs global peers

| Category | Ticker | CCY | Rating | TP | Price | Mkt cap (USDbn) | 26e PE | 27e PE | 26e EPSG | 27e EPSG | 26e PB | 27e PB | 26e ROE | 27e ROE |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Memory | ||||||||||||||

| Samsung Elec | 005930 KP | KRW | Buy | 450,000 | 349,000 | 1,354 | 8.4 | 6.2 | 525% | 36% | 3.3 | 2.3 | 53% | 49% |

| SK Hynix | 000660 KP | KRW | Buy | 2,900,000 | 2,363,000 | 1,117 | 8.2 | 5.6 | 361% | 47% | 5.3 | 2.8 | 91% | 64% |

| Micron | MU US | USD | Buy | 1,100.00 | 971.00 | 1,095 | 15.7 | 7.7 | 715% | 105% | 9.1 | 4.3 | 80% | 76% |

| Sandisk | SNDK US | USD | NR | 1,694.98 | 251 | 9.2 | 8.4 | 184% | 9% | 5.6 | 3.5 | 69% | 40% | |

| Kioixa Holdings | 285A JP | JPY | NR | 72,500 | 226 | 9.7 | 7.3 | 627% | 33% | 8.6 | 4.5 | 105% | 74% | |

| Nanya Tech | 2408 TT | TWD | NR | 382 | 42 | 8.3 | 7.0 | 2053% | 19% | 3.8 | 2.4 | 54% | 39% | |

| Average | 9.9 | 7.0 | 744% | 41% | 5.9 | 3.3 | 75% | 57% | ||||||

| Foundry | ||||||||||||||

| TSMC | 2330 TT | TWD | Buy | 2,800 | 2,355 | 1,943 | 24.3 | 20 | 46% | 24% | 8.2 | 6.1 | 39% | 36% |

| Intel | INTC US | USD | Buy | 100.00 | 114.68 | 576 | 97.7 | 53.2 | 176% | 84% | 4.8 | 4.4 | 5% | 9% |

| SMIC | 981 HK | HKD | Buy | 11.36 | 10.14 | 94 | 69.7 | 49.9 | 67% | 40% | 3.6 | 3.3 | 5% | 7% |

| UMC | 2303 TT | TWD | Hold | 80.00 | 146.00 | 58 | 32.7 | 31.3 | 34% | 4% | 5.4 | 4.2 | 16% | 15% |

| Global foundries | GFS US | USD | Hold | 65.03 | 79.97 | 44 | 40.7 | 33.3 | 13% | 22% | 3.8 | 3.7 | 10% | 11% |

| Average | 53.0 | 37.5 | 67% | 35% | 5.1 | 4.3 | 15% | 15% | ||||||

| Other semi | ||||||||||||||

| ST Micro | STMPA FP | EUR | Buy | 62.07 | 68.74 | 63 | 54.5 | 26.7 | 139% | 104% | 3.4 | 3.1 | 6% | 12% |

| Infineon | IFX GY | EUR | Buy | 68.00 | 81.11 | 124 | 45.9 | 31.8 | 27% | 44% | 5.8 | 5.2 | 13% | 17% |

| Texas instruments | TXN US | USD | NR | 305.68 | 278 | 39.5 | 33.2 | 31% | 19% | 15.2 | 14.2 | 40% | 44% | |

| Average | 46.6 | 30.6 | 66% | 56% | 8.2 | 7.5 | 20% | 24% | ||||||

| Semi equipment | ||||||||||||||

| ASML Holdings | ASML NA | EUR | Buy | 1,568.00 | 1,384.80 | 627 | 43.5 | 32.8 | 29% | 33% | 22.4 | 18.1 | 56% | 61% |

| LAM research | LRCX US | USD | Hold | 247.00 | 318.18 | 398 | 39.7 | 33.0 | 40% | 20% | 22.6 | 15.8 | 68% | 57% |

| Applied materials | AMAT US | USD | Buy | 522.00 | 450.06 | 357 | 35.7 | 25.0 | 34% | 43% | 13.0 | 10.2 | 42% | 45% |

| ASM International | ASM NA | EUR | Buy | 1,015.00 | 898.40 | 52 | 39.8 | 31.6 | 55% | 26% | 9.0 | 7.7 | 25% | 26% |

| BE Semiconductor | BESI NA | EUR | Hold | 240.00 | 284.40 | 27 | 58.8 | 41.1 | 192% | 43% | 32.8 | 26.5 | 69% | 71% |

| Average | 43.5 | 32.7 | 70% | 33% | 19.9 | 15.7 | 52% | 52% | ||||||

| Fabless | ||||||||||||||

| NVIDIA | NVDA US | USD | Buy | 325.00 | 211.14 | 5,110 | 24.2 | 16.2 | 82% | 50% | 15.1 | 8.3 | 86% | 67% |

| Broadcom | AVGO US | USD | Buy | 600.00 | 446.77 | 2,115 | 36.3 | 20.8 | 81% | 74% | 16.3 | 9.2 | 58% | 59% |

| AMD | AMD US | USD | Hold | 380.00 | 516.10 | 842 | 76.3 | 44.9 | 62% | 70% | 12.1 | 10.1 | 17% | 25% |

| Qualcomm | QCOM US | USD | Hold | 155.00 | 251.02 | 265 | 23.7 | 22.8 | -12% | 4% | 13.0 | 18.6 | 54% | 68% |

| Mediatek | 2454 TT | TWD | Hold | 2,605.00 | 4,555.00 | 232 | 68.4 | 44.8 | 1% | 53% | 14.1 | 10.7 | 23% | 27% |

| Marvell | MRVL US | USD | Hold | 300.00 | 205.00 | 179 | 72.3 | 50.2 | 80% | 44% | 12.5 | 10.9 | 18% | 24% |

| Average | 50.2 | 33.3 | 49% | 49% | 13.8 | 11.3 | 43% | 45% | ||||||

| Tech platforms | ||||||||||||||

| Meta | META US | USD | Buy | 905.00 | 632.51 | 1,606 | 20.2 | 18.9 | 33% | 7% | 5.5 | 4.3 | 31% | 26% |

| Alphabet | GOOGL US | USD | Buy | 435.00 | 380.34 | 4,485 | 26.0 | 26.3 | 35% | -1% | 7.7 | 5.8 | 35% | 25% |

| Microsoft | MSFT US | USD | Buy | 571.00 | 450.24 | 3,345 | 26.6 | 21.7 | 21% | 22% | 7.7 | 6.1 | 32% | 31% |

| Apple | AAPL US | USD | Hold | 260.00 | 312.06 | 4,583 | 35.4 | 32.9 | 18% | 8% | 38.2 | 30.2 | 134% | 102% |

| Average | 27.1 | 24.9 | 27% | 9% | 14.8 | 11.6 | 58% | 46% |

Source: Bloomberg consensus, HSBC estimates for covered names, Priced as of 1 June 2026 for Asian equities, otherwise priced as of 29 May 2026

Exhibit 33. Korean semi equipment & materials vs global peers

| Company | Ticker | Rating | Currency | TP | CP | Mkt cap (USDm) | 26e PE | 27e PE | 26e EPSG | 27e EPSG | 26e PB | 27e PB | 26e ROE | 27e ROE |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ISC | 095340 KQ | Buy | KRW | 350,000 | 209,500 | 2,946 | 50.9 | 35.1 | 50% | 45% | 7.2 | 6.3 | 15% | 19% |

| Leeno Industrial | 058470 KQ | Buy | KRW | 160,000 | 97,300 | 4,919 | 38.6 | 30 | 26% | 29% | 8.7 | 7.5 | 24% | 27% |

| Winway | 6515 TT | TWD | 8,705.00 | 9,999 | 91 | 46.7 | 104% | 95% | 37.2 | 21.9 | 44% | 53% | ||

| Cohu | COHU US | USD | 52.75 | 2,488 | 90.2 | 36.2 | TTB | 149% | 3.2 | 3 | 4% | NA | ||

| Average | 67.7 | 37 | 60% | 79% | 14.1 | 9.7 | 22% | 33% | ||||||

| EO Technics | 039030 KQ | Buy | KRW | 550,000 | 450,000 | 3,678 | 47.5 | 34.2 | 104% | 39% | 7.1 | 6 | 16% | 19% |

| DISCO | 6146 JP | JPY | 63,760.00 | 43,372 | 39.1 | 33 | 31% | 18% | 10.1 | 8.6 | 27% | 26% | ||

| Average | 43.3 | 33.6 | 67% | 29% | 8.6 | 7.3 | 22% | 23% | ||||||

| Wonik IPS | 240810 KQ | Buy | KRW | 165,000 | 102,700 | 3,344 | 27.5 | 20 | 116% | 38% | 4.4 | 3.7 | 17% | 20% |

| Tokyo Electron | 8035 JP | JPY | 53,060.00 | 155,727 | 34.1 | 27.3 | 24% | 25% | 10.2 | 8.6 | 32% | 35% | ||

| Kokusai Electric | 6525 JP | JPY | 7,595.00 | 11,341 | 37.6 | 28.8 | 57% | 31% | 7.1 | 6.1 | 21% | 24% | ||

| Applied Materials | AMAT US | USD | 450.06 | 357,329 | 36.4 | 27.4 | 31% | 33% | 13.9 | 11.4 | 41% | 46% | ||

| LAM Research | LRCX US | Hold | USD | 247.00 | 318.18 | 397,907 | 55.5 | 39.7 | 39% | 40% | 33.4 | 22.6 | 66% | 68% |

| ASM International | ASM NA | Buy | EUR | 1,015.00 | 898.40 | 51,673 | 39.8 | 31.6 | 55% | 26% | 9 | 7.7 | 25% | 26% |

| Average | 38.5 | 29.1 | 54% | 32% | 13 | 10 | 34% | 36% | ||||||

| HPSP | 403870 KQ | Buy | KRW | 65,000 | 46,600 | 2,544 | 28.3 | 18.1 | 83% | 56% | 9.4 | 6.9 | 38% | 44% |

| ASML | ASML NA | Buy | EUR | 1,568.00 | 1,238.00 | 626,733 | 43.5 | 32.8 | 29% | 33% | 22.4 | 18.1 | 56% | 61% |

| LAM Research | LRCX US | Hold | USD | 247.00 | 318.18 | 397,907 | 55.5 | 39.7 | 39% | 40% | 33.4 | 22.6 | 66% | 68% |

| KLA | KLAC US | USD | 1,921.71 | 251,028 | 51.8 | 38.1 | 11% | 36% | 41.9 | 29.4 | 91% | 93% | ||

| Applied Materials | AMAT US | Buy | USD | 522.00 | 450.06 | 357,329 | 35.7 | 25 | 34% | 43% | 13 | 10.2 | 42% | 45% |

| Average | 43 | 30.8 | 39% | 41% | 24 | 17.4 | 59% | 62% | ||||||

| Park Systems | 140860 KQ | Buy | KRW | 360,000 | 278,000 | 1,291 | 35.4 | 23.6 | 59% | 50% | 7 | 5.6 | 22% | 26% |

| Lasertec | 6920 JP | USD | 1,921.71 | 251,028 | 51.8 | 38.1 | 11% | 36% | 41.9 | 29.4 | 91% | 93% | ||

| Bruker | BRKR US | JPY | 38,380.00 | 22,692 | 36.6 | 29.9 | 24% | 22% | 11.3 | 9.2 | 33% | 33% | ||

| Camtek | CAMT US | USD | 171.66 | 7,991 | 49.1 | 37.7 | 7% | 30% | 9.9 | 6.9 | 24% | 23% | ||

| Average | 43.2 | 32.3 | 26% | 35% | 17.6 | 12.8 | 43% | 44% | ||||||

| Hansol Chem | 014680 KP | Buy | KRW | 400,000 | 260,500 | 1,965 | 14.6 | 11.4 | 32% | 28% | 2.3 | 1.9 | 17% | 18% |

| Mitsubishi gas | 4182 JP | JPY | 5,468.00 | 7,259 | 21.2 | 18.1 | TTB | 17% | 1.5 | 1.4 | 8% | 9% | ||

| Air Liquide | AI FP | EUR | 178.08 | 119,592 | 25.3 | 22.9 | 115% | 10% | 3.6 | 3.4 | 15% | 15% | ||

| Average | 20.4 | 17.5 | 74% | 18% | 2.4 | 2.2 | 13% | 14% |

Source: Bloomberg consensus estimates, HSBC estimates for covered stocks. Priced as of 1 June 2026 for Asian equities, priced as of 29 May 2026 otherwise.

Valuation and risks

Samsung Electronics 005930 KP

Buy

Current price: KRW349,000 Target price: KRW450,000 Up/downside: +28.9%

Current price: KRW2,363,000 Target price: KRW2,900,000 Up/downside: +22.7%

Current price: KRW450,000 Target price: KRW550,000 Up/downside: +22.2%

Current price: KRW46,600 Target price: KRW65,000 Up/downside: +39.5%

Valuation

We have a Buy rating with a TP of KRW450k . To derive our target price, we apply a target PB multiple of 2.9x, which is a 15% premium to the 2005-06 peak of 2.5x, reflecting the strong ROE expansion. We apply this to our 2027e BVPS of KRW154,478 to derive our TP of KRW450k. All our assumptions are unchanged. Our target price implies c29% upside and we reiterate our Buy rating.

We calculate a fair value target price of USD7,500 for the GDR rate of 1,500 and a GDR to Korea listed share conversion ratio of listed on the London Stock Exchange (SMSN LI, CMP USD5,335), based on our local share target price using a USD/KRW exchange 1-to-25.

Ricky Seo* | rickyjuilseo@kr.hsbc.com | +82 2 3706 8777

We have a Buy rating with a TP of KRW2.9m . We value the stock using a target PB multiple of 2.8x, which is the historical peak. We apply this to our 2027-28 average BVPS of KRW1,034,363, to derive our TP of KRW2.9m. All our assumptions are unchanged. Our target price implies c23% upside and we therefore retain our Buy rating.

We calculate a fair value target price of EUR1,731 for the GDR listed on the Frankfurt stock exchange (HY9H GR, EUR1,325) based on our local share target price using a EUR/KRW exchange rate of 1,676 and a GDR to Korea listed share conversion ratio of 1-to-1.

We calculate a fair value target price of USD2,042 for the GDR listed on the Luxembourg stock exchange (HYXS LX, USD1,585) based on our local share target price using a USD/KRW exchange rate of 1,420 and a GDR to Korea listed share conversion ratio of 1-to-1.

Ricky Seo*

| rickyjuilseo@kr.hsbc.com | +82 2 3706 8777

We have a Buy rating and a TP of KRW550k: We derive our TP by applying a target PE multiple of 42x (0.5 standard deviation above the two-year 12-month forward average during 2023-24) to our 2027e EPS of KRW13,149. Our TP implies upside of c22%; hence, we reiterate our Buy rating.

Hankil Chang* | han.kil.chang@kr.hsbc.com | +822 3706 8750

We have a Buy rating with a TP of KRW65k. We apply a target PE multiple of 31x, which is the five-year average historical PE of global peers during 2021-25, to our 2026/27e average EPS of KRW2,107 to derive our TP of KRW65k. Our target price implies 39.5% upside. We therefore maintain our Buy rating.

To determine our target PE, we use the past five years' historical average for global semiconductor equipment peers with high exposure to advanced semiconductor node technology within the wafer fabrication process. This includes ASML (ASML NA, EUR1,385, Buy), KLA (KLAC US, USD1,921.71, Not Rated), Applied Materials (AMAT US, USD450.06, Buy), Tokyo Electron (8035 JP, JPY53,060.00, Not Rated) and Lam Research (LRCX US, USD318.18, Hold).

We identify the above companies as appropriate peers to HPSP for having a leading market share within their respective equipment segments, and high exposure to advanced node technology, while having exposure to both logic and memory semiconductors.

Hankil Chang* | han.kil.chang@kr.hsbc.com | +822 3706 8750

Risks

Downside risks: 1) Further KRW appreciation, which would lead to weaker earnings and margin pressure; 2) increasing instability from global trade restrictions causing tech supply chains to suffer production issues; and 3) potential contraction in major economies leading to a slowdown in global consumer and enterprise IT demand.

Downside risks: 1) Higher US interest rates as neo-CSPs and Open AI implement investment through financing; 2) more aggressive capacity expansion at memory makers, 3) KRW appreciation, leading to weaker earnings and margin pressure.

Downside risks: (1) Downside revisions to semiconductor manufacturing capex, (2) continued geopolitical and macroeconomic factors that can impact end-demand of IT consumer applications, leading to earnings cuts and capex cuts for memory and foundry players, (3) delays in customer equipment installation due to changes in customer investment schedules, and (4) increased competition leading to margin declines due to competitive pricing.

Downside risks: (1) Sudden reduction in global semiconductor wafer equipment capex due to a change in market dynamics; (2) decline in market share due to potential entrance of a new competitor for its key product; (3) slower front-end node expansion at key customers, resulting in product shipment delays; and (4) ongoing court case with domestic equipment maker on patent infringement claims.

| Valuation | Risks | ||

|---|---|---|---|

| Park Systems 140860 KQ Buy | Current price: KRW278,000 Target price: KRW360,000 Up/downside: +29.5% | We have a Buy rating with a TP of KRW360k : We apply our unchanged target PE multiple of 36.3x (5y average 12m fwd PE during 2020-24) to our 2026/27e average EPS of KRW9,810 to derive our TP of KRW360k. Our TP implies 29.5% upside; we therefore reiterate our Buy rating. | Downside risks: (1) Sudden reduction in global semiconductor wafer equipment capex due to a change in market dynamics; (2) a decline in market share due to the potential entry of new competitors for key products; and (3) slower front-end node expansion at key customers, resulting in product shipment delays. |

| Hansol Chemical 014680 KP Buy | Current price: KRW260,500 Target price: KRW400,000 Up/downside: +53.6% | We have a Buy rating with a TP of KRW400k. We use our unchanged target PE multiple of 19.8x, which is the upper-end PE multiple of the upcycle valuation in 2021, with an EPSG of 20%, reflecting faster growth. We apply this to our 2026-27 EPS estimate of KRW20,369 to derive our TP. Our target price implies upside of 54% to the current share price and we therefore have a Buy rating on the stock. Hankil Chang* | han.kil.chang@kr.hsbc.com | +822 3706 8750 | Downside risks: (1) Weaker demand for quantum dot TVs; (2) slower-than-expected 3D NAND capacity ramp-up; (3) delayed market share gains for new products, such as lithium-ion battery (LIB) materials and precursors; and (4) potential raw material cost increases due to an increase in oil prices. |

Priced at 1 June 2026

Source: HSBC estimates

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260602_hsbc_korea-ai-supply-chain_013.png |

35908 bytes | 真資料圖 | 折線圖,Y軸「(GB) HBM per GPU(GB)」,X軸依序為DGX H100(80)/GB200 NVL72(192,+50%)/GB300 NVL72(288)/Rubin NVL72(Vera Rubin,288)/Rubin Ultra NVL576(1,024,+256%) |

260602_hsbc_korea-ai-supply-chain_023.png |

40186 bytes | 真資料圖 | 柱狀圖,Y軸-50.0%~30.0%百分比,X軸年度2020~2028e,數值如2023年20.0%、2024年17.2%,2026e/2027e/2028e為紅色負值(-7.5%/-27.2%/-35.1%);圖上無可見標題或軸名稱 |