PDF 原檔:報告_Daiwa_健策3653_20260707_original.pdf

圖片清單(已驗證 2026-07-08)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源;嵌入時只從這裡挑分類為「真資料圖」的,不照 trimmed 引用順序猜。建立步驟見

ingest_steps.mdStep 2.5。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Daiwa_健策3653_20260707_001.png |

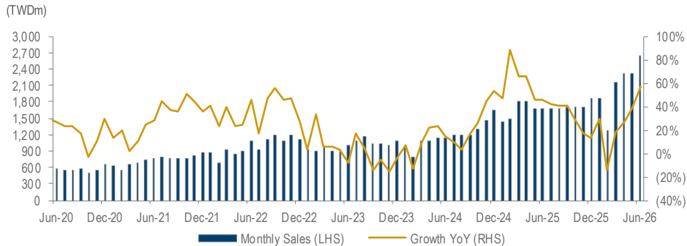

54KB | 真資料圖 | 健策月合併銷售額柱狀圖(左軸 TWDm)與 YoY 成長率折線圖(右軸 %),時間軸 Jun-20 至 Jun-26 |

原始內容

Jentech Precision Industrial (3653 TT)

Share price (7 Jul): TWD3,195.00

12-mth rating: Buy (1)

June 2026 revenue: another record high

Helen Chien

(886) 2 8758 6254 helen.chien@daiwacm-cathay.com.tw

Neil Teng

(886) 2 8758 6256 neil.teng@daiwacm-cathay.com.tw

Summary: Jentech reported June 2026 revenue of TWD2,650m (+14.5% MoM and +57.6% YoY; +26.6% YoY for 6M26), a record-high level, after market hours on 7 July 2026. Its 2Q26 revenue (+37.1% QoQ and +40.4% YoY) accounted for 102.1% and 112.4% of our and Bloomberg consensus estimates for 2Q26 revenue, respectively.

We reiterate our Buy (1) call and 12-month TP of TWD6,770, based on a PER of 73x on our 1-year-forward EPS. For more information on the company, please refer to our latest flash report, May 2026 revenue: a record high level , on 5 June 2026.

What's the impact

- Record-high monthly revenue for June. Jentech posted June 2026 revenue of TWD2,650m (+14.5% MoM and +57.6% YoY; +26.6% YoY for 6M26), setting a record high level. Its 2Q26 revenue (TWD7,275m, +37.1% QoQ and +40.4% YoY), also a record-high level, accounted for 102.1% and 112.4% of our (TWD7,123m, +34.3% QoQ and +37.5% YoY) and Bloomberg consensus estimates for 2Q26 revenue, respectively. Revenue mix in June 2026 is heat spreaders (77.0%, +57.6% YoY), lead frames (7.5%, +31.5% YoY), electronic components (5.1%, +15.5% YoY), communication (0.5%, +22.6% YoY) and others (9.9%, +106.2% YoY); revenue mix in 2Q26 is heat spreaders (74.7%, +38.8% YoY), lead frames (8.6%, +32.7% YoY), electronic components (5.7%, +17.1% YoY), communication (0.9%, +103.3% YoY) and others (10.1%, +76.6% YoY).

Jentech: consolidated monthly sales

Source: Company

- Growth to continue in 2H26. According to the company, revenue in 3Q26 and 4Q26 is likely to continue to grow by < 10% QoQ. Its removable lids are expected to start shipping from 4Q26, with ASP > USD200.

What we recommend

We reiterate our Buy (1) call and 12-month TP of TWD6,770, based on a PER of 73x on our 1-year-forward EPS. Based on our 2026/27 EPS estimates, the stock is currently trading at PERs of 47.1x/23.9x, vs. its past-3-year trading range of 17-61x. Key risks: weaker-thanexpected global AI server demand; slower-than-expected thermal spec upgrades.

In the interests of timeliness, this document has not been edited.

7 July 2026

Information Technology: Taiwan