PDF 原檔:報告_BofA_記憶體週報_20260711_original.pdf

原始內容

Global Memory Tech

Global Memory Tech

Weekly theme: Samsung correction, strong indicator, CXMT IPO, Nanya Tech upturn

Industry Overview

Samsung share-price correction vs strong fundamentals

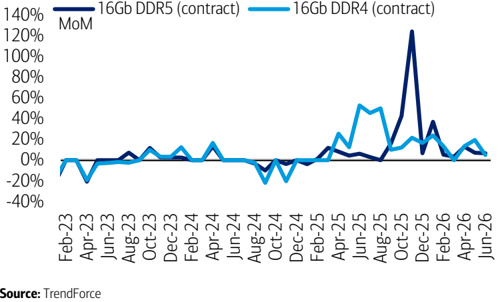

Many investors have asked why Samsung Electronics ' share price corrected despite reporting (7 July) strong 2Q OP of W89.4tn. In our view, the bearish sentiment stemmed from following concerns: (1) Meta US -chip order cut; (2) CXMT China -large capacity; and (3) QoQ growth -no longer strong after 2Q peak. That said, we don ' t see any downturn signals -our weekly channel check still indicates strong memory chip demand (from US Big Tech), low impact of CXMT (no severe competition), and more favorable 3Q ASP (many new quarterly contracts already reveal 20%+ price hike, in our view). In fact, we have slightly raised 3Q DRAM ASP assumptions in our global memory industry model (new: +21% QoQ vs old +17%); see Exhibit 15 for our new forecast summary.

Super-cycle reconfirmed by BofA memory indicator

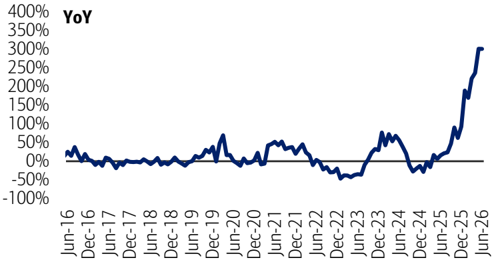

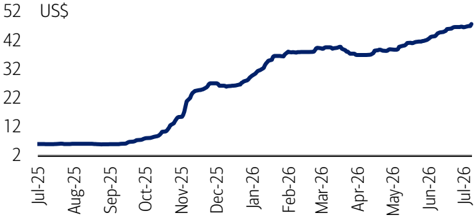

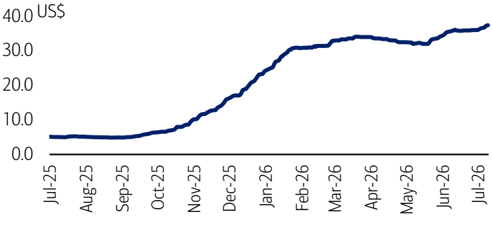

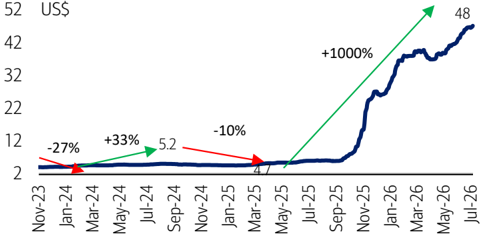

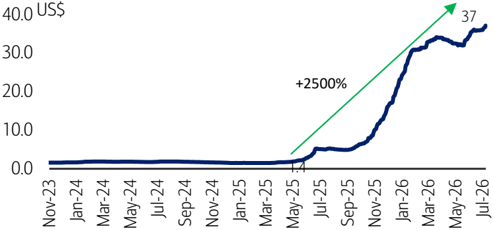

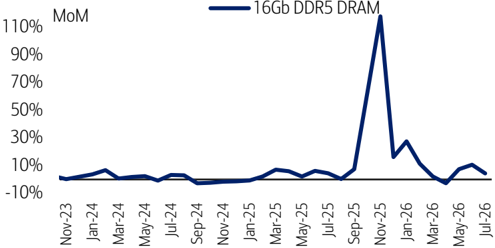

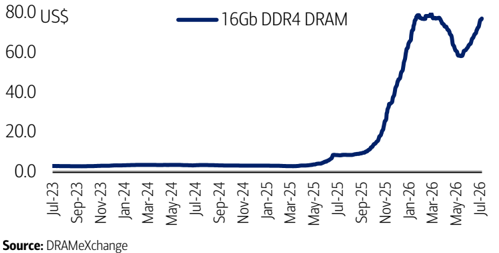

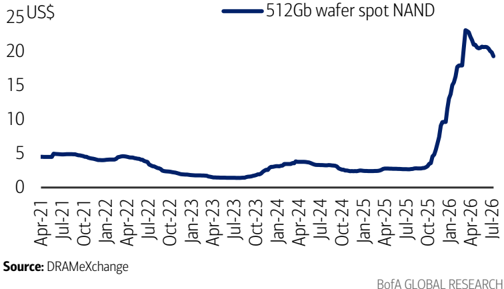

Our memory indicator, which is based on YoY changes in spot price, global billings, Korea exports, etc., remained at a record-high level, with May results at 183 -far above 2017/ 2024 peaks (120-130; mid-cycle: 100; downturn: 80). DRAM/NAND global billings grew more than 300% YoY in May, according to our analysis using WSTS ' s data. We also note solid June sales (Nanya Tech: +621% YoY; Phison +301% YoY), exports (Korea semis: +199%) and DRAM spot (+700%; even NAND shows +600% despite MoM drop). One of the most interesting point in Jun results was resumption of DRAM spot rally MoM (+11% on average vs -4%/+3% in Apr/May) but this is weaker than Korea ' s semis exports (+21% MoM) that include more high-end memory (HBM4, SOCAMM, etc.) vs May level.

CXMT's IPO share subscription date announced - 16 July

CXMT, China-based DRAM manufacturer, stated the firm ' s IPO share subscription date will be 16 July. Thus, actual listing can happen in late-July if the government regulations are properly followed. CXMT has disclosed its 2Q26 sales guidance (CNY59-69bn; ~US$9.5bn). This is 7x YoY growth but still only high-single-digit% of global DRAM market share despite large wafer capacity (high-200k wpm or 300k, according to media reports; this accounts for mid-teen% of global total DRAM capacity). We still assume high-end DRAM (10Ghz+ LPDDR5, HBM, SOCAMM, GDDR7, etc.) will be supplied mostly by ex-China memory chipmakers due to quality and US ' s strict control (on China semis).

Nanya Tech's legacy DRAM more profitable vs HBM

Nanya Tech reported very strong 2Q results (sales up 684% YoY; OP margin 74% vs large loss or -43% a year ago). The key contributor was DRAM ASP rise (up 60%+ QoQ; 500%+ YoY). Management ' s guidance was also bullish for 3Q and even for the long term (shortage of legacy DRAM such as DDR3 & 4 continues, low impact of China memory players ' capacity expansion, etc). We also learned that Nanya Tech ' s DRAM business is more profitable than HBM. Since 2Q results were broadly in line with our already bullish forecasts, our EPS estimate changes (2026-28) are almost nil and, as such, PO (NT$660; 9x 2027-28E P/E) is unchanged; maintain Buy on solid earnings and low multiples.

>> Employed by a non-US affiliate of BofAS and is not registered/qualified as a research analyst under the FINRA rules.

Refer to "Other Important Disclosures" for information on certain BofA Securities entities that take responsibility for the information herein in particular jurisdictions.

BofA Securities does and seeks to do business with issuers covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Refer to important disclosures on page 32 to 35. Analyst Certification on page 30. Price Objective Basis/Risk on page 29. 12992970

Timestamp: 10 July 2026 07:52PM EDT

11 July 2026

Equity Global Technology

Simon Woo, CFA >> Research Analyst Merrill Lynch (Seoul) +82 2 3707 0554

simon.woo@bofa.com

Dai Shen >> Research Analyst Merrill Lynch (Hong Kong) dai.shen@bofa.com

Vivek Arya Research Analyst BofAS vivek.arya@bofa.com

Mikio Hirakawa >> Research Analyst BofAS Japan mikio.hirakawa@bofa.com

Matt Shin >> Research Analyst Merrill Lynch (Seoul) matt.shin2@bofa.com

Exhibit 1: Global memory outlook supercycle likely to continue through 2027 despite 2026 quadrupling

BofA global memory forecasts

| YoY | 24 | 25 | 26E | 27E |

|---|---|---|---|---|

| DRAM sales | 86% | 52% | 325% | 45% |

| NAND sales | 84% | 4% | 299% | 30% |

| DRAM ASP | 62% | 29% | 249% | 25% |

| NAND ASP | 65% | -8% | 238% | 9% |

| DRAM bit | 15% | 18% | 22% | 17% |

| NAND bit | 11% | 13% | 18% | 20% |

| DRAM capex | 49% | 43% | 65% | 27% |

| NAND capex | 4% | -5% | 55% | 18% |

| DRAM capa | 7% | 8% | 11% | 9% |

| NAND capa | -2% | -7% | 5% | 4% |

Source:

BofA Global Research estimates

BofA GLOBAL RESEARCH

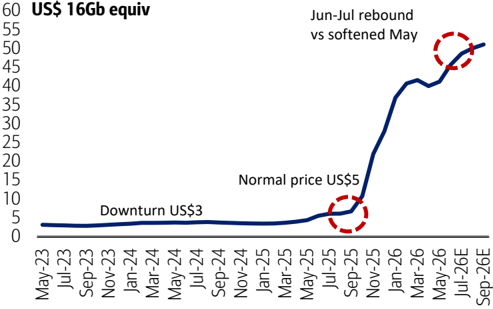

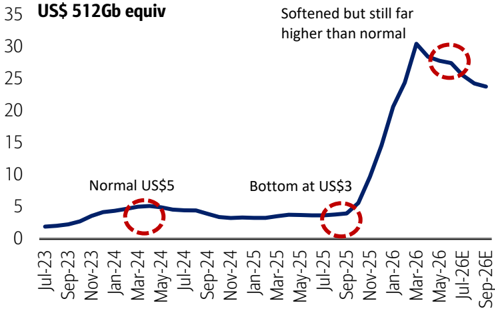

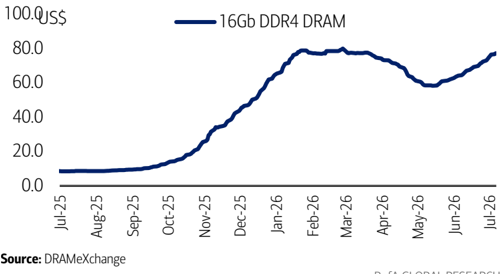

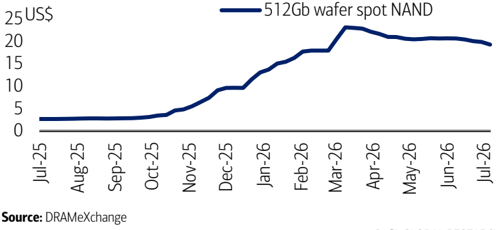

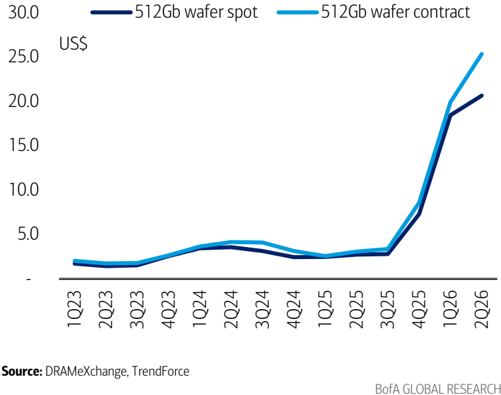

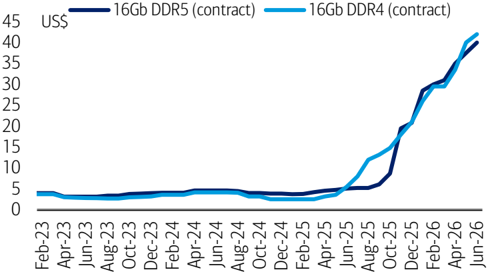

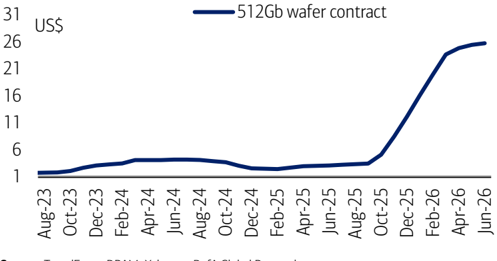

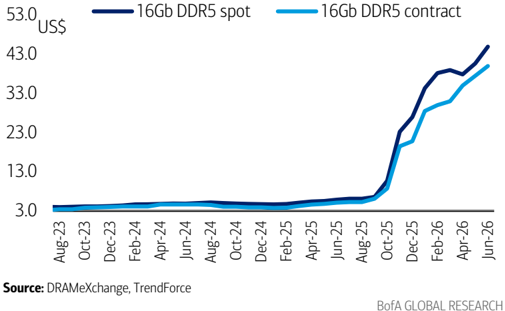

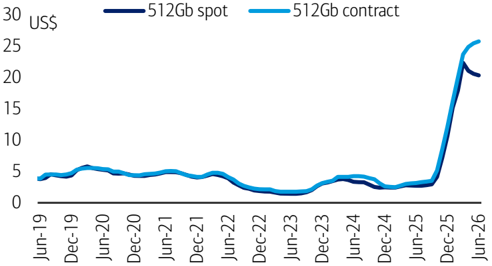

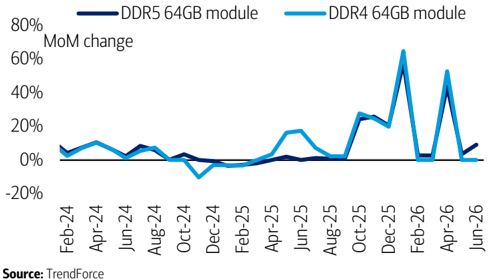

Exhibit 2: DDR5 and DDR4 price up in Jun/early-Jul, while NAND prices softened

Spot-market prices among DRAM and NAND

| US$ | Current | WoW | QoQ | YoY |

|---|---|---|---|---|

| DRAM spot | ||||

| 16Gb DDR5 | 47.8 | 2% | 29% | 688% |

| 16Gb DDR4 | 77.6 | 2% | 9% | 825% |

| 8Gb DDR4 | 37.8 | 3% | 13% | 661% |

| NAND spot | ||||

| 1Tb wafer | 24.2 | -1% | -9% | 377% |

| 512Gb wafer | 19.3 | -3% | -11% | 621% |

| 256Gb wafer | 10.2 | 0% | -7% | 578% |

Source:

DRAMeXchange

BofA GLOBAL RESEARCH

ASP-driven memory super-cycle to continue

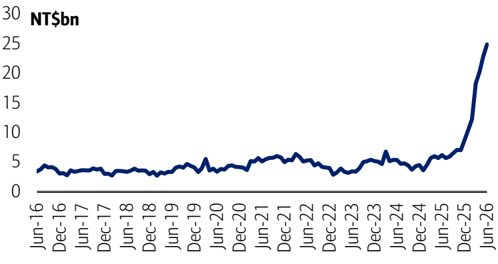

Exhibit 3: New record-high in Jun (NT$29.4bn; +6% MoM); more than 5x higher than 2025-avg (NT$5.5bn)

Nanya Tech - Monthly sales (Jun 2026)

Source: Company

BofA GLOBAL RESEARCH

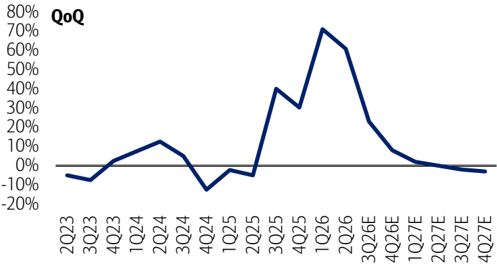

Exhibit 5: Exceptionally strong ASP hike in 2Q (up >60% QoQ) even after robust 1Q (up >70%); we assume decelerating growth in 2H, but still strong at 23%/8% in 3Q/4Q, respectively; no downturn in 2027 - just softening ASP QoQ (still super-cycle)

Nanya Tech DRAM ASP trend - quarterly; 8Gb equiv.

Source: Company, BofA Global Research estimates

BofA GLOBAL RESEARCH

Exhibit 7: Also at all-time high in Jun (NT$24.9bn; +9% MoM); more than 4x higher than 2025-avg (NT$6.1bn)

Phison Electronics - Monthly sales (Jun 2026)

Source: Company

BofA GLOBAL RESEARCH

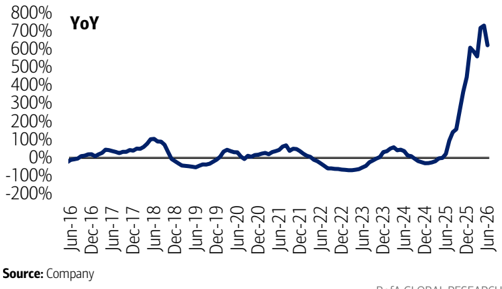

Exhibit 4: Robust YoY growth continued in Jun (+621%); already 11 consecutive months of triple-digit rebound

Nanya Tech - YoY monthly sales (Jun 2026)

BofA GLOBAL RESEARCH

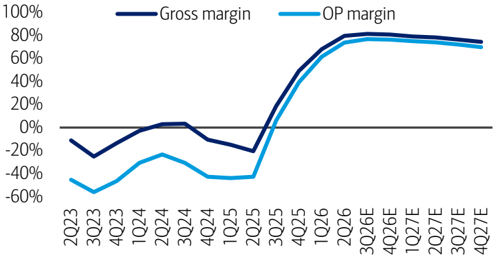

Exhibit 6: We expect robust margins to continue in 2H26-27 (GM/OPM 70%+); record-high margins well-proved in 2Q (GM 79%, OPM 74%)

Nanya Tech - Gross and OP margin trend

Source: Company, BofA Global Research estimates

BofA GLOBAL RESEARCH

Exhibit 8: Strong YoY growth continued in Jun (+621%); already six consecutive months of triple-digit rebound

Phison Electronics - YoY monthly sales (Jun 2026)

Source: Company

BofA GLOBAL RESEARCH

Exhibit 9: Given 2Q results were broadly in-line with our already bullish forecasts, our EPS estimate changes (2026-28) are almost nil and consequently PO (NT$660; 9x 2027-28E P/E) is unchanged; reiterate Buy on strong earnings and low multiples

Nanya Tech - Earnings revisions (2026-28E)

| (NT$bn, NT$) | 1Q26 | 2Q26 | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| New | 8.3 | 14.6 | 18.7 | 20.2 | 20.8 | 21.3 | 21.9 | 20.7 | 4.7 | -2.4 | -1.6 | 2.1 | 62.6 | 84.6 | 68.3 |

| Old | 8.3 | 14.7 | 19.0 | 20.5 | 20.9 | 21.3 | 21.8 | 20.6 | 4.7 | -2.4 | -1.6 | 2.1 | 62.6 | 84.7 | 68.0 |

| Diff | n/a | -1% | -2% | -1% | -1% | 0% | 0% | 0% | n/a | n/a | n/a | n/a | 0% | 0% | 0% |

| Dividend/share | |||||||||||||||

| New | 0.0 | 1.4 | 0.0 | 0.0 | 0.0 | 20.0 | 0.0 | 0.0 | 2.1 | 0.0 | 0.0 | 1.4 | 20.0 | 25.0 | 25.0 |

| Old | 0.0 | 1.4 | 0.0 | 0.0 | 0.0 | 20.0 | 0.0 | 0.0 | 2.1 | 0.0 | 0.0 | 1.4 | 20.0 | 25.0 | 25.0 |

| Difference | n/a | nm | nm | nm | nm | nm | nm | nm | n/a | n/a | n/a | n/a | 0% | 0% | 0% |

| Sales total | |||||||||||||||

| New | 49.1 | 82.5 | 110.7 | 120.5 | 126.2 | 130.9 | 138.1 | 134.8 | 57.0 | 29.9 | 34.1 | 66.6 | 362.9 | 530.0 | 519.2 |

| Old | 49.1 | 82.2 | 102.6 | 111.6 | 116.8 | 121.1 | 127.8 | 124.8 | 57.0 | 29.9 | 34.1 | 66.6 | 345.5 | 490.5 | 480.5 |

| Diff | n/a | 0% | 8% | 8% | 8% | 8% | 8% | 8% | n/a | n/a | n/a | n/a | 5% | 8% | 8% |

| OP margin | |||||||||||||||

| New | 61.3% | 73.7% | 76.7% | 76.2% | 74.9% | 73.8% | 72.0% | 69.7% | 19.3% | -48.4% | -30.9% | 7.9% | 73.8% | 72.5% | 59.8% |

| Old | 61.3% | 72.5% | 75.6% | 75.1% | 73.2% | 71.8% | 69.8% | 67.3% | 19.3% | -48.4% | -30.9% | 7.9% | 72.7% | 70.5% | 57.8% |

| Diff | n/a | 1.1% | 1.1% | 1.1% | 1.7% | 2.0% | 2.2% | 2.3% | n/a | n/a | n/a | n/a | 1.1% | 2.1% | 2.0% |

| EBITDA | |||||||||||||||

| New | 33.0 | 63.8 | 87.8 | 94.9 | 97.5 | 99.8 | 102.7 | 97.4 | 26.2 | 0.9 | 5.6 | 19.5 | 279.5 | 397.4 | 326.3 |

| Old | 33.0 | 62.6 | 80.5 | 86.8 | 88.5 | 90.2 | 92.5 | 87.5 | 26.2 | 0.9 | 5.6 | 19.5 | 262.9 | 358.7 | 293.5 |

| Diff | n/a | 2% | 9% | 9% | 10% | 11% | 11% | 11% | n/a | n/a | n/a | n/a | 6% | 11% | 11% |

| Capex | |||||||||||||||

| New | 2.8 | 4.0 | 15.0 | 28.1 | 18.0 | 16.0 | 17.0 | 19.0 | 20.7 | 13.2 | 16.1 | 13.4 | 50.0 | 70.0 | 70.0 |

| Old | 2.8 | 10.0 | 15.0 | 27.2 | 18.0 | 16.0 | 17.0 | 19.0 | 20.7 | 13.2 | 16.1 | 13.4 | 55.0 | 70.0 | 70.0 |

| Diff | n/a | -60% | 0% | 4% | 0% | 0% | 0% | 0% | n/a | n/a | n/a | n/a | -9% | 0% | 0% |

| DRAM sales (US$mn) | |||||||||||||||

| New | 1,551 | 2,612 | 3,325 | 3,645 | 3,840 | 4,002 | 4,248 | 4,160 | 1,935 | 958 | 1,062 | 2,156 | 11,133 | 16,249 | 16,082 |

| Old | 1,551 | 2,411 | 3,060 | 3,356 | 3,537 | 3,687 | 3,915 | 3,833 | 1,935 | 958 | 1,062 | 2,156 | 10,378 | 14,972 | 14,820 |

| Diff | n/a | 8% | 9% | 9% | 9% | 9% | 9% | 9% | n/a | n/a | n/a | n/a | 7% | 9% | 9% |

| Shipments (8Gb, mn) | |||||||||||||||

| New | 220 | 220 | 224 | 226 | 233 | 243 | 262 | 265 | 447 | 429 | 450 | 705 | 890 | 1,002 | 1,154 |

| Old | 220 | 212 | 216 | 219 | 225 | 234 | 253 | 255 | 447 | 429 | 450 | 705 | 867 | 967 | 1,114 |

| Diff | n/a | 4% | 4% | 4% | 4% | 4% | 4% | 4% | n/a | n/a | n/a | n/a | 3% | 4% | 4% |

| ASP US$/8b equiv | |||||||||||||||

| New | 7.90 | 12.70 | 15.62 | 16.87 | 17.21 | 17.21 | 16.86 | 16.36 | 4.49 | 2.52 | 2.86 | 3.54 | 13.31 | 16.89 | 14.50 |

| Old | 7.90 | 12.23 | 14.98 | 16.18 | 16.50 | 16.50 | 16.17 | 15.69 | 4.49 | 2.52 | 2.86 | 3.54 | 12.81 | 16.20 | 13.91 |

| Diff | n/a | 4% | 4% | 4% | 4% | 4% | 4% | 4% | n/a | n/a | n/a | n/a | 4% | 4% | 4% |

| ASP chg (QoQ/YoY) | |||||||||||||||

| New | 71% | 61% | 23% | 8% | 2% | 0% | -2% | -3% | -10% | -44% | 13% | 24% | 276% | 27% | -14% |

| Old | 71% | 55% | 23% | 8% | 2% | 0% | -2% | -3% | -10% | -44% | 13% | 24% | 262% | 26% | -14% |

| Diff | n/a | 6% | 1% | 0% | 0% | 0% | 0% | 0% | n/a | n/a | n/a | n/a | 14% | 0% | 0% |

| Cost US$/8Gb equiv | |||||||||||||||

| New | 3.05 | 3.34 | 3.64 | 4.01 | 4.33 | 4.50 | 4.73 | 4.96 | 3.61 | 3.75 | 3.74 | 3.30 | 3.52 | 4.64 | 5.83 |

| Old | 3.05 | 3.36 | 3.66 | 4.03 | 4.43 | 4.65 | 4.88 | 5.13 | 3.61 | 3.75 | 3.74 | 3.30 | 3.53 | 4.79 | 5.88 |

| Diff | n/a | -2% | -2% | -2% | -10% | -15% | -16% | -17% | n/a | n/a | n/a | n/a | -1% | -14% | -4% |

| Bit growth (QoQ/YoY) | |||||||||||||||

| New | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 0% | -27% | -4% | 5% | 57% | 26% | 13% | 15% |

| Old | 0% | 0% | 0% | 0% | 0% | 0% | 0% | 0% | -27% | -4% | 5% | 57% | 23% | 12% | 15% |

| Diff | n/a | 0% | 0% | 0% | 0% | 0% | 0% | 0% | n/a | n/a | n/a | n/a | 3% | 1% | 0% |

Source:

Company, BofA Global Research estimates

BofA GLOBAL RESEARCH

BofA Memory Indicator

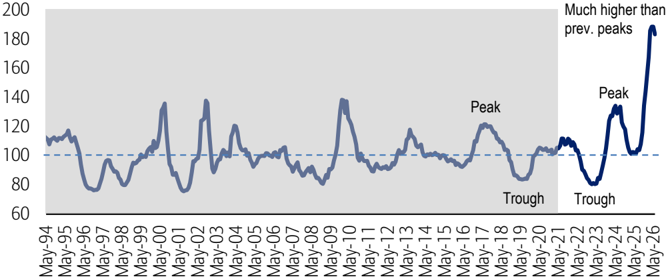

Exhibit 10: Our memory indicator still near all-time high level in May (183) vs 186/189/189 in Feb/Mar/Apr-26, driven by exceptionally strong DRAM/NAND spot pricing, rising ASPs and billings, along with Korea's 150%+ export growth.

BofA Memory Indicator - back to upturn level since Oct-2025 and hit highest peak in Mar/Apr-26 (back-tested)

Note: Our indicator had previously been capped at ~140, but the recent unprecedented surge-driven by memory spot prices, ASPs, and billings-has led us to raise the ceiling (up to 240 levels) to reflect a more accurate relative comparison. This exceptional strength is further validated by strong earnings from memory chipmakers.

Source: DRAMeXchange, WSTS, MoTIR Korea, BofA Global Research

*The shaded area represents back-tested results from January 1991 to March 2021. The unshaded area represents actual performance since April 2021. This performance is back-tested up to March-2021, and does not represent the actual performance of any account or fund. Back-tested performance depicts the theoretical (not actual) performance of a particular strategy over the time period indicated. No representation is being made that any actual portfolio is likely to have achieved returns similar to those shown herein.

Disclaimer: The BofA Memory Indicator is intended to be an indicative metric only and may not be used for reference purposes or as a measure of performance for any financial instrument or contract, or otherwise relied upon by third parties for any other purpose, without the prior written consent of BofA Global Research. This indicator was not created to act as a benchmark. For methodology, see the 5 Aug 2024 Global Memory Tech report.

BofA GLOBAL RESEARCH

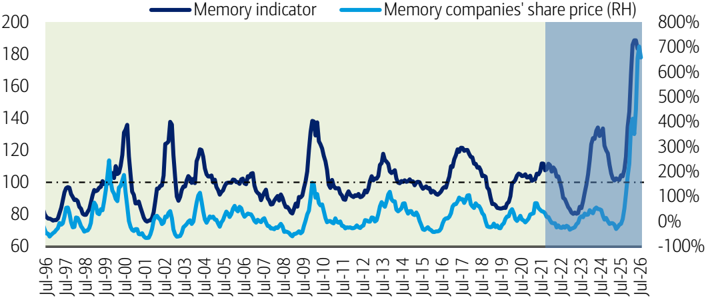

Exhibit 11: Mild setback in memory companies' stock prices in early-July, but still near record highs, supported by Samsung (strong 2Q prelim, optimism around HBM4 upside, and higher exposure to conventional DRAM), Micron (solid May-Q results and strong Aug-Q guidance), and Nanya Tech (record Jan-Jun monthly sales, up ~500-700% YoY).

BofA Memory Indicator is highly correlated with stock performance (back-tested)

Note: Memory companies share price is average of Samsung, Micron, and Nanya share price YoY changes

Source: Bloomberg, BofA Global Research

The light green shaded area represents back-tested results from January 1991 to March 2021. The blue shaded area represents actual data since April 2021. This performance is back-tested and does not represent the actual performance of any account or fund. Back-tested performance depicts the theoretical (not actual) performance of a particular strategy over the time period indicated. No representation is being made that any actual portfolio is likely to have achieved returns similar to those shown herein. For methodology, see the 5 Aug 2024 Global Memory Tech report.

BofA GLOBAL RESEARCH

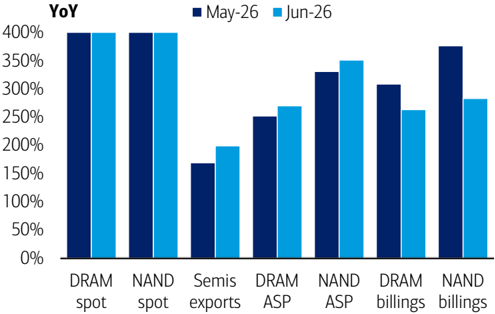

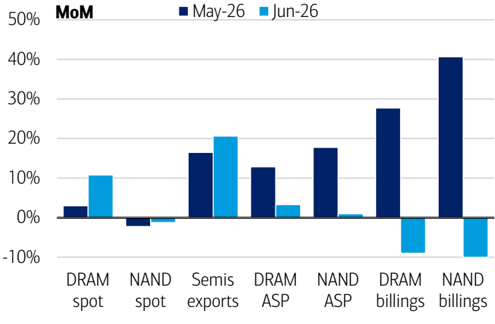

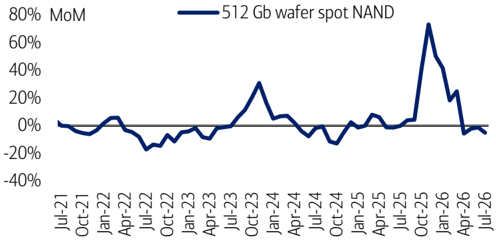

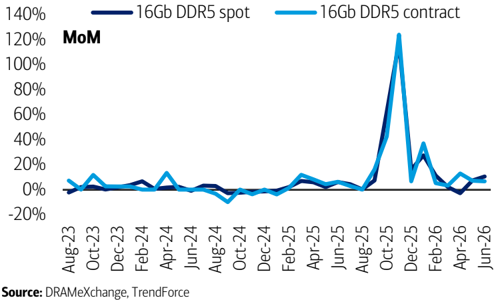

Exhibit 12: HBM, DDR5, and legacy DRAM drove a strong YoY rebound in May, with DRAM ASP/billings up +252%/+309% and NAND +331%/+377%; momentum carried into Jun with sharp YoY gains in spot pricing (DRAM +723%, NAND +647%) and Korea semiconductor exports rising near-3x Seven components of BofA Memory Indicator - MoM and YoY trends (back-tested)

| Jun-25 | Jul-25 | Aug-25 | Sep-25 | Oct-25 | Nov-25 | Dec-25 | Jan-26 | Feb-26 | Mar-26 | Apr-26 | May-26 | Jun-26 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| MoM | |||||||||||||

| DRAM spot price | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Down | Up | Up |

| NAND spot price | Down | Down | Up | Up | Up | Up | Up | Up | Up | Up | Down | Down | Down |

| Korea semis exports | Up | Down | Up | Up | Down | Up | Up | Up | Up | Up | Down | Up | Up |

| DRAM ASP | Down | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | na |

| NAND ASP | Down | Up | Down | Down | Up | Up | Up | Up | Up | Up | Up | Up | na |

| DRAM billings | Up | Up | Up | Up | Down | Up | Up | Down | Up | Up | Down | Up | na |

| NAND billings | Up | Down | Up | Up | Down | Up | Up | Up | Up | Up | Down | Up | na |

| Avg of MoMtrend | Up | Down | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | na |

| YoY | |||||||||||||

| DRAM spot price | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up |

| NAND spot price | Down | Down | Down | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up |

| Korea semis exports | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up |

| DRAM ASP | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | na |

| NAND ASP | Down | Down | Down | Down | Down | Up | Up | Up | Up | Up | Up | Up | na |

| DRAM billings | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | na |

| NAND billings | Down | Down | Down | Up | Up | Up | Up | Up | Up | Up | Up | Up | na |

| Avg of YoY trend | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | Up | na |

| Memory indicator | 102 | 105 | 104 | 108 | 116 | 135 | 144 | 168 | 186 | 189 | 189 | 183 | na |

Source: DRAMeXchange, WSTS, MoTIE Korea, BofA Global Research estimates. This performance is back-tested and does not represent the actual performance of any account or fund. Back-tested performance depicts the theoretical (not actual) performance of a particular strategy over the time period indicated. No representation is being made that any actual portfolio is likely to have achieved returns similar to those shown herein. Notes: *May-26 results recovered in all aspects in terms of YoY growth, but softened in terms of MoM change for DRAM/NAND billings and NAND spot price due to high base level in Apr-26

**For Jun-26, only spot prices and exports are reported so far

***DRAM spot price is based on weighted average MoM change of16Gb DDR5, 16Gb DDR4 and 8Gb DDR4; NAND spot price is based on MoM change in 512Gb wafer spot price

Exhibit 13: Exceptionally strong DRAM/NAND spot pricing persisted through May-Jun, with DRAM ASPs and billings also rising sharply in May, while semiconductor exports remained robust, reaching record highs in Jun

Seven components of BofA Memory Indicator - YoY

All May data and Jun spot/exports are actual, but Jun billings are our estimates *DRAM spot up +839%/723% YoY and NAND spot up +646%/647% YoY in May/Jun

Source: DRAMeXchange, WSTS, MoTIR Korea, BofA Global Research estimates

BofA GLOBAL RESEARCH

BofA GLOBAL RESEARCH

Exhibit 14: Solid price hike in DRAM spot seen in Jun vs NAND spot slightly down following a sharp rally in 4Q25/1Q26; semis exports rebounded strongly MoM in May-Jun, while DRAM/NAND ASP and billingss remained elevated in May

Seven components of BofA Memory Indicator - MoM

*All May data and Jun spot/exports are actual, but Jun billings are our estimates

Source:

DRAMeXchange, WSTS, MoTIR Korea, BofA Global Research estimates

BofA GLOBAL RESEARCH

Global memory forecasts

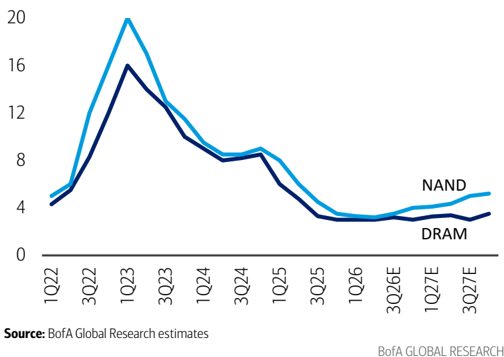

Exhibit 15: We expect global DRAM revenue to nearly quadruple (+325% YoY) in 2026E, building on the strong growth trajectory of 86%/52% in 2024/25, primarily driven by a sharp ~3x rebound in ASPs (+249% YoY). NAND revenue is similarly forecast to increase nearly fourfold (+299% YoY) in 2026E, following modest low-single-digit growth in 2025, supported by a robust ~2.3x expansion in ASPs (+238% YoY).

Global memory forecast summary - top-down approach

| 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue US$bn DRAM | 83.9 | 134.6 | 167.7 | 182.6 | 191.8 | 200.1 | 213.3 | 221.2 | 92.1 | 77.7 | 47.3 | 87.9 | 133.8 | 568.8 | 826.4 | 900.7 |

| NAND | 45.3 | 78.9 | 96.4 | 102.4 | 101.7 | 103.1 | 106.8 | 108.8 | 73.3 | 67.3 | 42.4 | 78.1 | 81.0 | 323.1 | 420.4 | 421.5 |

| DRAM+NAND total | 129.2 | 213.6 | 264.1 | 285.0 | 293.5 | 303.2 | 320.1 | 329.9 | 165.4 | 144.9 | 89.7 | 166.0 | 214.8 | 891.8 | 1,246.8 | 1,322.2 |

| %QoQ | ||||||||||||||||

| DRAM | 78% | 60% | 25% | 9% | 5% | 4% | 7% | 4% | ||||||||

| NAND | 71% | 74% | 22% | 6% | -1% | 1% | 4% | 2% | ||||||||

| DRAM/NAND total | 75% | 65% | 24% | 8% | 3% | 3% | 6% | 3% | ||||||||

| %YoY | ||||||||||||||||

| DRAM | 258% | 378% | 378% | 287% | 129% | 49% | 27% | 21% | 41% | -16% | -39% | 86% | 52% | 325% | 45% | 9% |

| NAND | 196% | 332% | 360% | 287% | 125% | 31% | 11% | 6% | 25% | -8% | -37% | 84% | 4% | 299% | 30% | 0% |

| DRAM/NAND total | 234% | 360% | 371% | 287% | 127% | 42% | 21% | 16% | 34% | -12% | -38% | 85% | 29% | 315% | 40% | 6% |

| Blended ASP US$/unit | ||||||||||||||||

| DRAM 8Gb equiv | 8.1 | 12.4 | 14.9 | 16.0 | 16.3 | 16.3 | 16.1 | 15.8 | 3.8 | 3.2 | 1.8 | 2.9 | 3.7 | 13.0 | 16.1 | 14.9 |

| NAND 256Gb equiv | 5.0 | 8.3 | 9.5 | 9.6 | 9.5 | 9.2 | 8.7 | 8.5 | 3.4 | 3.0 | 1.6 | 2.6 | 2.4 | 8.2 | 8.9 | 7.8 |

| %QoQ | ||||||||||||||||

| DRAM ASP | 73% | 53% | 21% | 7% | 2% | 0% | -2% | -2% | ||||||||

| NAND ASP | 75% | 65% | 15% | 1% | -2% | -3% | -5% | -3% | ||||||||

| %YoY | ||||||||||||||||

| DRAM ASP | 155% | 283% | 318% | 242% | 102% | 32% | 8% | -1% | 14% | -16% | -45% | 62% | 29% | 249% | 25% | -8% |

| NAND ASP | 115% | 281% | 313% | 236% | 89% | 11% | -9% | -12% | -9% | -13% | -46% | 65% | -8% | 238% | 9% | -13% |

| Shipments bn units | ||||||||||||||||

| DRAM 8Gb equiv | 10.4 | 10.9 | 11.2 | 11.4 | 11.8 | 12.2 | 13.3 | 14.0 | 24.1 | 24.2 | 26.7 | 30.6 | 36.0 | 43.9 | 51.2 | 60.5 |

| NAND 256Gb equiv | 9.0 | 9.5 | 10.1 | 10.6 | 10.7 | 11.2 | 12.2 | 12.8 | 21.3 | 22.6 | 26.6 | 29.5 | 33.2 | 39.3 | 47.0 | 54.3 |

| %QoQ | ||||||||||||||||

| DRAM bit growth | 3% | 5% | 3% | 2% | 3% | 4% | 8% | 5% | ||||||||

| NAND bit growth | -2% | 5% | 6% | 5% | 1% | 5% | 9% | 5% | ||||||||

| %YoY DRAM bit growth | 41% | 25% | 14% | 13% | 13% | 12% | 18% | 22% | 23% | 0% | 10% | 15% | 18% | 22% | 17% | 18% |

| NAND bit growth | 38% | 13% | 11% | 15% | 19% | 18% | 21% | 21% | 38% | 6% | 18% | 11% | 13% | 18% | 20% | 16% |

| Capacity300mmkwpm | ||||||||||||||||

| DRAM wafer capacity | 1,988 | 2,036 | 2,091 | 2,150 | 2,182 | 2,224 | 2,264 | 2,299 | 1,481 | 1,561 | 1,628 | 1,734 | 1,867 | 2,066 | 2,242 | 2,379 |

| NAND wafer capacity | 1,695 | 1,722 | 1,736 | 1,750 | 1,767 | 1,784 | 1,801 | 1,834 | 1,681 | 1,783 | 1,820 | 1,781 | 1,651 | 1,726 | 1,797 | 1,878 |

| DRAM+NAND total | 3,683 | 3,758 | 3,827 | 3,900 | 3,949 | 4,008 | 4,065 | 4,133 | 3,162 | 3,344 | 3,447 | 3,515 | 3,517 | 3,792 | 4,039 | 4,256 |

| %QoQ | ||||||||||||||||

| DRAM capacity total | 3% | 2% | 3% | 3% | 1% | 2% | 2% | 2% | ||||||||

| NAND capacity total | 1% | 2% | 1% | 1% | 1% | 1% | 1% | 2% | ||||||||

| 2% | 1% | |||||||||||||||

| DRAM/NAND total | 2% | 2% | 2% | 1% | 1% | 2% | ||||||||||

| %YoY | ||||||||||||||||

| DRAM capacity | 9% | 11% | 12% | 11% | 10% | 9% | 8% | 7% | 8% | 5% | 4% | 7% | 8% | 11% | 9% | 6% |

| NAND capacity | 2% | 6% | 6% | 4% | 4% | 4% | 4% | 5% | 1% | 6% | 2% | -2% | -7% | 5% | 4% | 5% |

| DRAM+NAND total | 5% | 9% | 9% | 8% | 7% | 7% | 6% | 6% | 4% | 6% | 3% | 2% | 0% | 8% | 7% | 5% |

| Capex spending | ||||||||||||||||

| DRAM | 23.0 | 22.2 | 21.3 | 22.2 | 26.0 | 27.1 | 29.4 | 30.5 | 27.1 | 31.0 | 25.2 | 37.7 | 53.9 | 88.6 | 112.9 | 119.5 |

| NAND | 6.9 | 7.2 | 7.5 | 8.4 | 9.2 | 8.8 | 8.5 | 8.8 | 27.9 | 29.0 | 19.7 | 20.4 | 19.3 | 30.1 | 35.4 | 37.2 |

| Total (DRAM+NAND) | 30.0 | 29.4 | 28.8 | 30.6 | 35.2 | 35.9 | 37.8 | 39.3 | 55.0 | 60.0 | 45.0 | 58.2 | 73.2 | 118.7 | 148.3 | 156.7 |

| QoQ/YoY in capex | ||||||||||||||||

| DRAM | 58% | -4% | -4% | 4% | 17% | 4% | 8% | 4% | 27% | 14% | -19% | 49% | 43% | 65% | 27% | 6% |

| NAND | 28% | 4% | 4% | 12% | 9% | -4% | -4% | 4% | -32% | 4% | 5% | |||||

| 6% | 2% | 5% | 4% | 24% | 4% | -5% | 55% | 18% | 6% | |||||||

| Total (DRAM+NAND) | 50% | -2% | -2% | 15% | 25% | 9% | -25% | 29% | 26% | 62% | 25% |

Source:

Companies' reports, BofA Global Research estimates

BofA GLOBAL RESEARCH

Exhibit 16: We slightly raise our 2026-28 DRAM revenue forecasts by 2-3%, primarily reflecting higher ASP assumptions (at ~$13/$16/$15 per 8Gb equivalent in 2026/27/28). NAND revenue estimates are also increased by 1-2% for 2026-28, driven by stronger ASP expectations (~$8-9 per 256Gb equivalent) amid the recent pricing upcycle.

Global memory forecast revisions - top-down analysis

| 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DRAM (8Gb equiv) Sales (US$bn) | ||||||||||||||||

| New | 83.9 | 134.6 | 167.7 | 182.6 | 191.8 | 200.1 | 213.3 | 221.2 | 92.1 | 77.7 | 47.3 | 87.9 | 133.8 | 568.8 | 826.4 | 900.7 |

| Old | 83.9 | 134.6 | 162.1 | 176.6 | 185.5 | 193.5 | 206.3 | 213.9 | 92.1 | 77.7 | 47.3 | 87.9 | 133.8 | 557.2 | 799.1 | 870.9 |

| Diff | nm | 0.0% | 3.4% | 3.4% | 3.4% | 3.4% | 3.4% | 3.4% | nm | nm | nm | nm | nm | 2.1% | 3.4% | 3.4% |

| Shipments (bn units) | ||||||||||||||||

| New | 10.4 | 10.9 | 11.2 | 11.4 | 11.8 | 12.2 | 13.3 | 14.0 | 24.1 | 24.2 | 26.7 | 30.6 | 36.0 | 43.9 | 51.2 | 60.5 |

| Old | 10.4 | 10.9 | 11.2 | 11.4 | 11.8 | 12.2 | 13.3 | 14.0 | 24.1 | 24.2 | 26.7 | 30.6 | 36.0 | 43.9 | 51.2 | 60.5 |

| Diff | nm | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | nm | nm | nm | nm | nm | 0.0% | 0.0% | 0.0% |

| Bit growth - sequential | ||||||||||||||||

| New | 2.8% | 5.0% | 3.0% | 1.8% | 3.0% | 4.1% | 8.3% | 5.3% | 23.3% | 0.3% | 10.3% | 14.8% | 17.6% | 21.9% | 16.7% | 18.1% |

| Old | 2.8% | 5.0% | 3.0% | 1.8% | 3.0% | 4.1% | 8.3% | 5.3% | 23.3% | 0.3% | 10.3% | 14.8% | 17.6% | 21.9% | 16.7% | 18.1% |

| Diff | nm | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | nm | nm | nm | nm | nm | 0.0% | 0.0% | 0.0% |

| ASP chg - sequential | ||||||||||||||||

| New | 73.2% | 52.9% | 20.9% | 7.0% | 2.0% | 0.2% | -1.6% | -1.5% | 14.2% | -16.0% | -44.8% | 61.8% | 29.4% | 248.7% | 24.5% | -7.7% |

| Old | 73.2% | 52.9% | 16.9% | 7.0% | 2.0% | 0.2% | -1.6% | -1.6% | 14.2% | -16.0% | -44.8% | 61.8% | 29.4% | 241.6% | 22.9% | -7.7% |

| Diff | nm | 0.0% | 4.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | nm | nm | nm | nm | nm | 7.1% | 1.6% | 0.0% |

| Blended ASP (US$) | ||||||||||||||||

| New | 8.1 | 12.4 | 14.9 | 16.0 | 16.3 | 16.3 | 16.1 | 15.8 | 3.8 | 3.2 | 1.8 | 2.9 | 3.7 | 13.0 | 16.1 | 14.9 |

| Old | 8.1 | 12.4 | 14.4 | 15.5 | 15.8 | 15.8 | 15.6 | 15.3 | 3.8 | 3.2 | 1.8 | 2.9 | 3.7 | 12.7 | 15.6 | 14.4 |

| Diff | nm | 0.0% | 3.4% | 3.4% | 3.4% | 3.4% | 3.4% | 3.4% | nm | nm | nm | nm | nm | 2.1% | 3.4% | 3.4% |

| NAND (256Gb equiv) | ||||||||||||||||

| Sales (US$bn) | ||||||||||||||||

| New | 45.3 | 78.9 | 96.4 | 102.4 | 101.7 | 103.1 | 106.8 | 108.8 | 73.3 | 67.3 | 42.4 | 78.1 | 81.0 | 323.1 | 420.4 | 421.5 |

| Old | 45.3 | 78.9 | 94.7 | 100.6 | 99.9 | 101.3 | 104.9 | 106.9 | 73.3 | 67.3 | 42.4 | 78.1 | 81.0 | 319.6 | 413.0 | 414.1 |

| Diff | nm | 0.0% | 1.8% | 1.8% | 1.8% | 1.8% | 1.8% | 1.8% | nm | nm | nm | nm | nm | 1.1% | 1.8% | 1.8% |

| Shipments (bn units) | ||||||||||||||||

| New | 9.0 | 9.5 | 10.1 | 10.6 | 10.7 | 11.2 | 12.2 | 12.8 | 21.3 | 22.6 | 26.6 | 29.5 | 33.2 | 39.3 | 47.0 | 54.3 |

| Old | 9.0 | 9.5 | 10.1 | 10.6 | 10.7 | 11.2 | 12.2 | 12.8 | 21.3 | 22.6 | 26.6 | 29.5 | 33.2 | 39.3 | 47.0 | 54.3 |

| Diff | nm | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | nm | nm | nm | nm | nm | 0.0% | 0.0% | 0.0% |

| Bit growth - sequential | ||||||||||||||||

| New | -2.2% | 5.4% | 6.2% | 5.2% | 0.9% | 4.6% | 9.0% | 5.0% | 37.8% | 6.1% | 17.6% | 11.2% | 12.5% | 18.2% | 19.7% | 15.6% |

| Old | -2.2% | 5.4% | 6.2% | 5.2% | 0.9% | 4.6% | 9.0% | 5.0% | 37.8% | 6.1% | 17.6% | 11.2% | 12.5% | 18.2% | 19.7% | 15.6% |

| Diff | nm | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | nm | nm | nm | nm | nm | 0.0% | 0.0% | 0.0% |

| ASP chg - sequential | ||||||||||||||||

| New | 74.7% | 65.4% | 15.0% | 1.0% | -1.6% | -3.1% | -5.0% | -3.0% | -9.1% | -13.5% | -46.4% | 65.5% | -7.8% | 237.6% | 8.7% | -13.3% |

| Old | 74.7% | 65.4% | 13.0% | 1.0% | -1.6% | -3.1% | -5.0% | -3.0% | -9.1% | -13.5% | -46.4% | 65.5% | -7.8% | 234.0% | 7.9% | -13.3% |

| Diff | nm | 0.0% | 2.0% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% | nm | nm | nm | nm | nm | 3.6% | 0.7% | 0.0% |

| Blended ASP (US$) | ||||||||||||||||

| New | 5.0 | 8.3 | 9.5 | 9.6 | 9.5 | 9.2 | 8.7 | 8.5 | 3.4 | 3.0 | 1.6 | 2.6 | 2.4 | 8.2 | 8.9 | 7.8 |

| Old | 5.0 | 8.3 | 9.4 | 9.5 | 9.3 | 9.0 | 8.6 | 8.3 | 3.4 | 3.0 | 1.6 | 2.6 | 2.4 | 8.1 | 8.8 | 7.6 |

| Diff | nm | 0.0% | 1.8% | 1.8% | 1.8% | 1.8% | 1.8% 1.8% | nm | nm | nm | nm | nm | 1.1% | 1.8% | 1.8% |

Source: BofA Global Research estimates, industry data. Chg = change. Equiv = equivalent

BofA GLOBAL RESEARCH

Exhibit 17: Servers-especially AI systems using HBM-now make up over half of total DRAM demand, mainly due to higher memory per system Global DRAM demand mix by application

| (8Gb equiv, mnunits) | 1Q262Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2022 | 2023 | 2024 | 2025E | 2026E | 2027E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Supply-to-demand | ||||||||||||||||

| Sufficiency (supply-to-demand) | 64.1% | 75.0% | 88.0% | 96.0% | 101.0% | 100.0% | 101.0% | 101.8% | 108.5% | 100.6% | 94.3% | 92.1% | 79.3% | 101.0% | 101.8% | 101.8% |

| Supply | 10,375 | 10,894 | 11,220 | 11,422 | 11,765 | 12,247 | 13,264 | 13,968 | 24,171 | 26,670 | 30,628 | 36,023 | 43,912 | 51,245 | 60,514 | 60,514 |

| Demand | 16,196 | 14,525 | 12,751 | 11,898 | 11,649 | 12,247 | 13,133 | 13,728 | 22,270 | 26,514 | 32,491 | 39,106 | 55,370 | 50,757 | 59,462 | 59,462 |

| Wafer capacity (12" equiv k wpm) | 1,988 | 2,036 | 2,091 | 2,150 | 2,182 | 2,224 | 2,264 | 2,299 | 1,561 | 1,628 | 1,734 | 1,867 | 2,066 | 2,242 | 2,379 | 2,379 |

| Revenue (US$bn) | 83.9 | 134.6 | 167.7 | 182.6 | 191.8 | 200.1 | 213.3 | 221.2 | 77.7 | 47.3 | 87.9 | 133.8 | 568.8 | 826.4 | 900.7 | 900.7 |

| ASP (US$) | 8.1 | 12.4 | 14.9 | 16.0 | 16.3 | 16.3 | 16.1 | 15.8 | 3.2 | 1.8 | 2.9 | 3.7 | 13.0 | 16.1 | 14.9 | 14.9 |

| Demand by application (mn units) | ||||||||||||||||

| Server | 5,468 | 5,583 | 6,094 | 6,585 | 6,452 | 6,646 | 7,599 | 7,596 | 9,731 | 9,022 | 13,217 | 18,459 | 23,730 | 28,293 | 34,504 | 34,504 |

| PC | 1,028 | 869 | 864 | 803 | 707 | 747 | 838 | 913 | 3,574 | 3,418 | 3,922 | 4,713 | 3,564 | 3,205 | 3,694 | 3,694 |

| Smartphone | 2,844 | 2,481 | 2,430 | 2,526 | 2,296 | 2,366 | 2,558 | 2,794 | 7,388 | 8,045 | 10,255 | 12,149 | 10,281 | 10,014 | 11,586 | 11,586 |

| Tablet | 233 | 194 | 183 | 196 | 184 | 188 | 187 | 221 | 846 | 786 | 929 | 1,052 | 805 | 781 | 908 | 908 |

| TV - DRAM embedded | 221 | 206 | 238 | 297 | 251 | 237 | 273 | 341 | 586 | 635 | 728 | 839 | 962 | 1,102 | 1,262 | 1,262 |

| Game - DRAM embedded | 125 | 114 | 136 | 206 | 135 | 124 | 156 | 221 | 454 | 459 | 499 | 535 | 581 | 636 | 680 | 680 |

| Auto - DRAM embedded | 105 | 113 | 125 | 132 | 135 | 145 | 161 | 170 | 168 | 219 | 288 | 370 | 475 | 611 | 785 | 785 |

| Total demand | 16,196 | 14,525 | 12,751 | 11,898 | 11,649 | 12,247 | 13,133 | 13,728 | 22,270 | 26,514 | 32,491 | 39,106 | 55,370 | 50,757 | 59,462 | 59,462 |

| Demand mix (% to total bits) | ||||||||||||||||

| Server | 34% | 38% | 48% | 55% | 55% | 54% | 58% | 55% | 44% | 34% | 41% | 47% | 43% | 56% | 58% | 58% |

| PC | 6% | 6% | 7% | 7% | 6% | 6% | 6% | 7% | 16% | 13% | 12% | 12% | 6% | 6% | 6% | 6% |

| Smartphone | 18% | 17% | 19% | 21% | 20% | 19% | 19% | 20% | 33% | 30% | 32% | 31% | 19% | 20% | 19% | 19% |

| Tablet | 1% | 1% | 1% | 2% | 2% | 2% | 1% | 2% | 4% | 3% | 3% | 3% | 1% | 2% | 2% | 2% |

| TV - DRAM embedded | 1% | 1% | 2% | 2% | 2% | 2% | 2% | 2% | 3% | 2% | 2% | 2% | 2% | 2% | 2% | 2% |

| Game - DRAM embedded | 1% | 1% | 1% | 2% | 1% | 1% | 1% | 2% | 2% | 2% | 2% | 1% | 1% | 1% | 1% | 1% |

| Auto - DRAM embedded | 0.6% | 0.8% | 1.0% | 1.1% | 1.2% | 1.2% | 1.2% | 1.2% | 0.8% | 0.8% | 0.9% | 0.9% | 0.9% | 1.2% | 1.3% | 1.3% |

| Total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% |

| DRAM content per product (GB) | ||||||||||||||||

| Server | 1,148 | 1,159 | 1,182 | 1,194 | 1,206 | 1,230 | 1,267 | 1,293 | 655 | 736 | 914 | 1,066 | 1,172 | 1,251 | 1,383 | 1,383 |

| PC | 16.9 | 15.7 | 15.4 | 14.2 | 14.3 | 14.6 | 14.9 | 15.1 | 12.2 | 13.5 | 15.3 | 17.1 | 15.6 | 14.8 | 16.2 | 16.2 |

| Smartphone | 10.4 | 10.2 | 9.8 | 9.7 | 9.8 | 10.0 | 10.3 | 10.8 | 6.2 | 7.0 | 8.4 | 9.8 | 10.0 | 10.3 | 11.3 | 11.3 |

| Tablet | 6.8 | 6.4 | 6.2 | 6.3 | 6.4 | 6.4 | 6.6 | 7.0 | 5.2 | 5.7 | 6.3 | 7.0 | 6.5 | 6.6 | 7.3 | 7.3 |

| TV - DRAM embedded | 4.5 | 4.6 | 4.7 | 4.8 | 5.1 | 5.2 | 5.3 | 5.4 | 2.9 | 3.2 | 3.6 | 4.1 | 4.7 | 5.3 | 5.9 | 5.9 |

| Game - DRAM embedded | 13.1 | 13.3 | 13.5 | 13.6 | 13.9 | 14.2 | 14.3 | 14.4 | 10.6 | 11.2 | 11.9 | 12.6 | 13.4 | 14.2 | 15.1 | 15.1 |

| Auto - DRAM embedded | 5.2 | 5.5 | 5.8 | 5.9 | 6.3 | 6.7 | 6.9 | 7.1 | 2.4 | 3.0 | 3.9 | 4.7 | 5.6 | 6.8 | 8.1 | 8.1 |

| DRAM-based products (mn units) | ||||||||||||||||

| Server | 5 | 5 | 5 | 6 | 5 | 5 | 6 | 6 | 15 | 12 | 14 | 17 | 20 | 23 | 25 | 25 |

| PC | 61 | 55 | 56 | 57 | 49 | 51 | 56 | 61 | 294 | 253 | 256 | 275 | 228 | 217 | 228 | 228 |

| Smartphone | 275 | 244 | 247 | 259 | 233 | 236 | 247 | 260 | 1,198 | 1,152 | 1,218 | 1,237 | 1,025 | 976 | 1,028 | 1,028 |

| Tablet | 34 | 31 | 29 | 31 | 29 | 29 | 28 | 32 | 163 | 138 | 147 | 151 | 125 | 118 | 124 | 124 |

| TV - DRAM embedded | 49 | 45 | 50 | 61 | 50 | 46 | 51 | 63 | 203 | 199 | 201 | 203 | 206 | 209 | 213 | 213 |

| Game - DRAM embedded | 10 | 9 | 10 | 15 | 10 | 9 | 11 | 15 | 43 | 41 | 42 | 42 | 43 | 45 | 45 | 45 |

| Auto - DRAM embedded | 20 | 20 | 22 | 22 | 21 | 22 | 23 | 24 | 69 | 72 | 75 | 79 | 85 | 90 | 96 | 96 |

| %QoQin DRAM-based products | ||||||||||||||||

| Server | 0% | 1% | 7% | 7% | -3% | 1% | 11% | -2% | 10% | -17% | 18% | 20% | 17% | 12% | 10% | 10% |

| PC | -17% | -9% | 1% | 1% | -13% | 3% | 10% | 8% | -16% | -14% | 1% | 8% | -17% | -5% | 5% | 5% |

| Smartphone | -15% | -11% | 1% | 5% | -10% | 1% | 5% | 5% | -12% | -4% | 6% | 2% | -17% | -5% | 5% | 5% |

| Tablet | -20% | -10% | -4% | 6% | -7% | 1% | -4% | 13% | -12% | -16% | 7% | 3% | -17% | -5% | 5% | |

| TV - DRAM embedded | -19% | -9% | 12% | 22% | -19% | -8% | 12% | 22% | -5% | -2% | 1% | 1% | 1% | 2% | 2% | |

| Game - DRAM embedded | -35% | -11% | 19% | 50% | -36% | -10% | 25% | 40% | -10% | -5% | 3% | 1% | 2% 3% | 1% | 1% | 1% |

| Auto - DRAM embedded | -4% | 2% | 7% | 3% | -4% | 2% | 7% | 3% | 0% | 5% | 3% | 6% | 7% | 7% | 7% |

Source: BofA Global Research estimates, industry data. Chg = change. Equiv = equivalent

BofA GLOBAL RESEARCH

Exhibit 18: SSD-especially in data center and AI applications-now accounts for over half of total NAND demand, driven by higher storage capacity per system; SSD including enterprise solutions already account for 50%+ of total NAND sales (price premium seen vs IT applications)

Global NAND demand mix by application

| (256Gb equiv, mnunits) | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2022 | 2023 | 2024 | 2025E | 2026E | 2027E | 2028E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Supply-to-demand Sufficiency (supply-to-demand) | 65.1% | 69.2% | 92.4% | 99.9% | 101.0% | 103.0% | 104.0% | 102.7% | 108.0% | 101.8% | 94.9% | 97.7% | 79.8% | 102.7% | 102.2% | 102.2% |

| Supply | 9,022 | 9,510 | 10,099 | 10,624 | 10,720 | 11,217 | 12,227 | 12,838 | 22,576 | 26,558 | 29,528 | 33,222 | 39,256 | 47,003 | 54,350 | 54,350 |

| Demand | 13,853 | 13,742 | 10,930 | 10,639 | 10,614 | 10,891 | 11,757 | 12,498 | 20,910 | 26,097 | 31,128 | 34,004 | 49,164 | 45,759 | 53,172 | 53,172 |

| Wafer capacity (12" | 1,695 | 1,722 | 1,736 | 1,750 | 1,767 | 1,784 | 1,801 | 1,834 | 1,783 | 1,820 | 1,781 | 1,651 | 1,726 | 1,797 | 1,878 | 1,878 |

| equiv k wpm) Revenue (US$bn) | 45.3 | 78.9 | 96.4 | 102.4 | 101.7 | 103.1 | 106.8 | 108.8 | 67.3 | 42.4 | 78.1 | 81.0 | 323.1 | 420.4 | 421.5 | 421.5 |

| ASP (US$) | 5.0 | 8.3 | 9.5 | 9.6 | 9.5 | 9.2 | 8.7 | 8.5 | 3.0 | 1.6 | 2.6 | 2.4 | 8.2 | 8.9 | 7.8 | 7.8 |

| Demand by application (mn units) Smartphones | 2,808 | 2,474 | 2,449 | 2,623 | 2,408 | 2,481 | 2,683 | 2,902 | 6,821 | 7,724 | 9,792 | 11,965 | 10,355 | 10,473 | 12,467 | 12,467 |

| SSDs | 3,932 | 4,033 | 4,511 | 4,928 | 4,392 | 4,651 | 5,379 | 5,860 | 9,520 | 9,715 | 12,587 | 15,738 | 17,405 | 20,282 | 23,880 | 23,880 |

| Notebook | 1,129 | 1,013 | 1,061 | 1,072 | 961 | 1,036 | 1,178 | 1,316 | 3,172 | 3,275 | 3,991 | 4,934 | 4,275 | 4,491 | 5,325 | 5,325 |

| Desktop | 431 | 437 | 482 | 502 | 445 | 455 | 502 | 523 | 990 | 1,031 | 1,271 | 1,708 | 1,853 | 1,925 | 2,004 | 2,004 |

| Server | 1,929 | 2,105 | 2,428 | 2,749 | 2,467 | 2,617 | 3,085 | 3,333 | 4,256 | 4,432 | 6,057 | 7,335 | 9,211 | 11,502 | 13,866 | 13,866 |

| Spot &inventories | 443 | 477 | 540 | 606 | 519 | 542 | 614 | 689 | 1,101 | 978 | 1,268 | 1,760 | 2,066 | 2,363 | 2,686 | 2,686 |

| Tablets | 393 | 335 | 312 | 335 | 311 | 321 | 316 | 370 | 1,134 | 1,155 | 1,483 | 1,812 | 1,374 | 1,319 | 1,509 | 1,509 |

| Game - NAND embedded | 216 | 196 | 235 | 357 | 235 | 216 | 273 | 386 | 736 | 760 | 843 | 913 | 1,004 | 330 | 1,202 | 1,202 |

| Autos - NAND embedded | 55 | 58 | 72 | 77 | 87 | 94 | 80 | 107 | 147 | 191 | 251 | 1,111 | 434 | 434 | ||

| Others &spot adj | 6,449 | 6,645 | 66 3,356 | 72 2,324 | 3,195 | 3,145 | 3,019 | 2,885 | 2,620 | 6,636 | 6,277 | 3,385 | 18,775 | 12,245 | 13,679 | 13,679 |

| 20,910 | 34,004 | |||||||||||||||

| NAND demand total | 13,853 | 13,742 | 10,930 | 10,639 | 10,614 | 10,891 | 11,757 | 12,498 | 26,097 | 31,128 | 49,164 | 45,759 | 53,172 | 53,172 | ||

| Demand mix (% to total bits) | ||||||||||||||||

| Smartphones | 20% | 18% | 22% | 25% | 23% | 23% | 23% | 23% | 33% | 30% | 31% | 35% | 21% | 23% | 23% | 23% |

| SSDs | 28% | 29% | 41% | 46% | 41% | 43% | 46% | 47% | 46% | 37% | 40% | 46% | 35% | 44% | 45% | 45% |

| Notebook | 8% | 7% | 10% | 10% | 9% | 10% | 10% | 11% | 15% | 13% | 13% | 15% | 9% | 10% 4% | 10% | 10% |

| Desktop | 3% | 3% | 4% | 5% | 4% | 4% | 4% | 4% | 5% | 4% | 4% | 5% | 4% | 4% | 4% | |

| Server | 14% | 15% | 22% | 26% | 23% | 24% | 26% | 27% | 20% | 17% | 19% | 22% | 19% | 25% | 26% | 26% |

| Spot &inventories | 3% | 3% | 5% | 6% | 5% | 5% | 5% | 6% | 5% | 4% | 4% | 5% | 4% | 5% | 5% | 5% |

| Tablets | 3% | 2% | 3% | 3% | 3% | 3% | 3% | 3% | 5% | 4% | 5% | 5% | 3% | 3% | 3% | 3% |

| Game - NAND embedded | 2% | 1% | 2% | 3% | 2% | 2% | 2% | 3% | 4% | 3% | 3% | 3% | 2% | 2% | 2% | 2% |

| Autos - NAND embedded | 0% | 0% | 1% | 1% | 1% | 1% | 1% | 1% | 0% | 0% | 0% | 1% | 1% | 1% | 1% | 1% |

| Total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% |

| NAND content per product (GB) | ||||||||||||||||

| Smartphones | 327 | 324 | 318 | 324 | 330 | 337 | 347 | 357 | 182 | 215 | 257 | 310 | 323 | 343 | 388 | 388 |

| SSDs | 1,293 | 1,371 | 1,449 | 1,503 | 1,558 | 1,594 | 1,652 | 1,662 | 763 | 885 | 1,065 | 1,185 | 1,406 | 1,620 | 1,796 | 1,796 |

| Notebook | 846 | 867 | 910 | 919 | 938 | 956 | 975 | 985 | 525 | 600 | 700 | 801 | 884 | 965 | 1,035 | 1,035 |

| Desktop | 892 | 914 | 960 | 970 | 989 | 1,009 | 1,029 | 1,039 | 555 | 632 | 739 | 845 | 935 | 1,017 | 1,091 | 1,091 |

| Server | 3,822 | 3,899 | 3,996 | 4,076 | 4,158 | 4,241 | 4,347 | 4,434 | 2,348 | 2,676 | 3,215 | 3,640 | 3,959 | 4,305 | 4,683 | 4,683 |

| Spot &inventories | 617 | 632 | 645 | 658 | 691 | 708 | 722 | 736 | 388 | 438 | 505 | 572 | 639 | 716 | 801 | 801 |

| Tablets | 370 | 351 | 341 | 344 | 344 | 351 | 358 | 373 | 223 | 269 | 324 | 383 | 352 | 357 | 390 | 390 |

| Game - NAND embedded | 960 | 1,049 | 779 | |||||||||||||

| Autos - NAND embedded | 941 | 95 | 970 | 979 | 1,009 | 1,029 | 1,039 | 719 | 48 | 841 | 900 | 965 | 1,034 | 1,108 152 | 1,108 152 | |

| NAND-based products (mn units) | 91 | 101 | 107 | 112 | 118 | 125 | 133 | 38 | 65 | 80 | 99 | 122 | 122 | |||

| Smartphones | 275 | 244 | 247 | 259 | 233 | 236 | 247 | 260 | 1,198 | 1,152 | 1,218 | 1,237 | 1,025 | 976 | 1,028 | 1,028 |

| SSDs | 97 | 94 | 100 | 105 | 90 | 93 | 104 | 113 | 399 | 351 | 378 | 425 | 396 | 401 | 426 | 426 |

| Notebook | 43 | 37 | 37 | 37 | 33 | 35 | 39 | 43 | 193 | 175 | 182 | 197 | 155 | 149 | 165 | 165 |

| Desktop | 15 | 15 | 16 | 17 | 14 | 14 | 16 | 16 | 57 | 52 | 55 | 65 | 63 | 61 | 59 | 59 |

| Server | 16 | 17 | 19 | 22 | 19 | 20 | 23 | 24 | 58 | 53 | 60 | 64 | 74 | 86 | 95 | 95 |

| 27 | 29 | 107 | 107 | |||||||||||||

| Spot &inventories | 23 | 24 | 24 | 25 | 27 | 30 | 91 | 71 | 80 | 98 | 103 | 106 | ||||

| Tablets | 34 | 31 | 29 | 31 | 29 | 29 | 28 | 32 | 163 | 138 | 147 | 151 | 125 | 124 | 124 | 124 |

| Game - NAND embedded | 7 | 7 | 8 | 12 | 7 | 8 | 12 | 33 | 31 | 32 | 32 | 33 | 34 | 35 | ||

| Auto | 19 | 20 | 21 | 21 | 21 | 7 21 | 22 | 23 | 68 | 71 | 73 | 77 | 81 | 86 | 92 | |

| %QoQ/YoY in NAND-based products | ||||||||||||||||

| Smartphones | -15% | -11% | 1% | 5% | -10% | 1% | 5% | 5% | -12% | -4% | 6% | 2% | -17% | -5% | 5% | 5% |

| SSDs Notebook | -18% -18% | -3% -12% | 6% 0% | 5% 0% | -14% -12% | 3% 6% | 12% 11% | 8% 11% | -7% -12% | -12% -10% | 8% 4% | 12% 8% | -7% -22% | 1% -4% | 6% 11% | 6% 11% |

| -1% | 5% | -13% | 0% | 8% | 3% | 10% | -9% | 5% | -2% | -3% | -3% | -3% | ||||

| Desktop | -13% | 13% | 3% | -12% | 17% 7% | 15% | 15% | |||||||||

| Server | -14% | 7% | 11% | 4% | 15% | 6% -9% | 8% | 14% 13% | 5% | 11% 2% | 11% 2% | 11% 2% | ||||

| Spot &inventories | -25% | 5% | 11% | 10% | -19% | 2% | 11% -4% | 10% | -15% | -22% | 23% | 2% -5% | 5% | 5% | 5% | 5% |

| Tablets | -20% | -10% | -4% | 6% | -7% | 1% | 13% -16% | -12% | 7% | 3% 1% | -17% 1% | -17% 1% | -17% 1% | -17% 1% | -17% 1% | |

| Game - NAND embedded | -35% | -11% | 19% | 50% | -36% | -10% | 25% | 40% | -10% | -5% | 3% | 3% | 6% | 6% | 6% |

Source: BofA Global Research estimates, industry data. Chg = change. Equiv = equivalent

BofA GLOBAL RESEARCH

Exhibit 19: Company-specific DRAM sales/ASP/shipment/margin comparison - high margin due to HBM

Bottom-up approach analysis based on top-4 DRAM companies' quarterly earnings results

| (8Gb equiv) | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Units (bn) | |||||||||||||||||

| Samsung | 4.3 | 4.6 | 4.7 | 4.8 | 4.9 | 5.1 | 5.6 | 5.9 | 10.9 | 10.8 | 11.8 | 13.4 | 15.0 | 18.4 | 21.5 | 24.9 | 24.9 |

| SK Hynix | 3.1 | - | - | - | - | - | - | - | 6.8 | 6.8 | 7.6 | 9.0 | 11.0 | - | - | - | - |

| Micron | 2.5 | 2.6 | 2.7 | 2.9 | 3.0 | 3.2 | 3.4 | 3.5 | 5.2 | 5.2 | 5.8 | 7.2 | 8.6 | 10.7 | 13.1 | 15.4 | 15.4 |

| Nanya | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.2 | 0.3 | 0.3 | 0.6 | 0.4 | 0.4 | 0.4 | 0.7 | 0.9 | 1.0 | 1.2 | 1.2 |

| Top 4 total | 10.1 | 23.5 | 23.3 | 25.7 | 30.1 | 35.3 | |||||||||||

| ASP (US$) | |||||||||||||||||

| Samsung | 9.0 | 13.1 | 15.8 | 17.0 | 17.4 | 17.4 | 17.2 | 16.7 | 3.9 | 3.3 | 1.8 | 2.9 | 3.5 | 13.9 | 17.2 | 15.5 | 15.5 |

| SK Hynix | 9.4 | - | - | - | - | - | - | - | 4.1 | 3.3 | 2.1 | 3.6 | 4.8 | - | - | - | - |

| Micron | 7.5 | 12.2 | 14.2 | 14.6 | 14.6 | 14.6 | 14.2 | 13.7 | 4.1 | 3.8 | 2.0 | 2.9 | 3.9 | 12.2 | 14.3 | 13.0 | 13.0 |

| Nanya | 7.9 | 12.7 | 15.6 | 16.9 | 17.2 | 17.2 | 16.9 | 16.4 | 5.0 | 4.5 | 2.5 | 2.9 | 3.5 | 13.3 | 16.9 | 14.5 | 14.5 |

| Top 4 total | 8.7 | 4.0 | 3.4 | 2.0 | 3.1 | 4.0 | |||||||||||

| OP margin (%) | |||||||||||||||||

| Samsung | 79% | 80% | 81% | 81% | 80% | 80% | 80% | 79% | 50% | 41% | -4% | 30% | 40% | 80% | 80% | 76% | 76% |

| SK Hynix | 77% | - | - | - | - | - | - | - | 39% | 31% | 0% | 47% | 61% | - | - | - | - |

| Micron | 70% | 81% | 83% | 83% | 82% | 82% | 81% | 80% | 39% | 35% | -31% | 19% | 40% | 81% | 81% | 76% | 76% |

| Nanya | 61% | 74% | 77% | 76% | 75% | 74% | 72% | 70% | 32% | 20% | -48% | -31% | 7% | 74% | 73% | 60% | 60% |

| Top 4 total | 76% | 44% | 36% | -10% | 32% | 47% | |||||||||||

| Sales (US$bn) | |||||||||||||||||

| Samsung | 39.2 | 59.7 | 73.9 | 81.4 | 85.7 | 89.1 | 96.2 | 98.0 | 42.0 | 35.3 | 21.8 | 39.2 | 53.2 | 254.2 | 369.1 | 385.9 | 385.9 |

| SK Hynix | 28.7 | - | - | - | - | - | - | - | 27.7 | 22.8 | 15.7 | 32.6 | 52.4 | - | - | - | - |

| Micron | 18.8 | 31.3 | 38.9 | 41.6 | 43.7 | 46.3 | 47.9 | 48.5 | 21.6 | 19.6 | 11.6 | 20.6 | 33.0 | 130.6 | 186.5 | 200.7 | 200.7 |

| Nanya | 1.7 | 2.8 | 3.5 | 3.8 | 4.0 | 4.2 | 4.4 | 4.3 | 3.1 | 2.0 | 1.1 | 1.3 | 2.5 | 11.9 | 16.9 | 16.7 | 16.7 |

| Top 4 total | 88.4 | 94.3 | 79.7 | 50.2 | 93.6 | 141.1 | |||||||||||

| Bit mkt shr | |||||||||||||||||

| Samsung | 43% | 46% | 46% | 46% | 45% | 43% | |||||||||||

| SK Hynix | 30% | 29% | 29% | 30% | 30% | 31% | |||||||||||

| Micron | 25% | 22% | 22% | 23% | 24% | 24% | |||||||||||

| Nanya | 2% | 3% | 2% | 2% | 1% | 2% | |||||||||||

| Top 4 total | 100% | 100% | 100% | 100% | 100% | 100% | |||||||||||

| Sales mkt shr | |||||||||||||||||

| Samsung | 44% | 43% | 43% | 43% | 44% | 44% | 44% | 44% | 45% | 44% | 43% | 42% | 38% | 43% | 44% | 43% | 43% |

| SK Hynix | 32% | - | - | - | - | - | - | - | 29% | 29% | 31% | 35% | 37% | - | - | - | - |

| Micron | 21% | 23% | 23% | 22% | 22% | 23% | 22% | 22% | 23% | 25% | 23% | 22% | 23% | 22% | 22% | 23% | 23% |

| Nanya | 2% | 2% | 2% | 2% | 2% | 2% | 2% | 2% | 3% | 3% | 2% | 1% | 2% | 2% | 2% | 2% | 2% |

| Top 4 total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% |

| Bit growth QoQ/YoY | |||||||||||||||||

| Samsung | 3% | 5% | 3% | 2% | 3% | 4% | 9% | 5% | 27% | -1% | 9% | 14% | 12% | 22% | 17% | 16% | 16% |

| SK Hynix | 0% | - | - | - | - | - | - | - | 19% | 0% | 12% | 17% | 23% | - | - | - | - |

| Micron | 5% | 3% | 6% | 4% | 5% | 6% | 6% | 5% | 22% | 0% | 11% | 25% | 19% | 25% | 22% | 18% | 18% |

| Nanya | -5% | 0% | 2% | 1% | 3% | 4% | 8% 1% | 0% | -27% | -4% | 5% | 57% | 26% | 13% | 15% | 15% | |

| Top 4 total | 2% | 23% | -1% | 10% | 17% | 17% | |||||||||||

| ASP chg QoQ/YoY | |||||||||||||||||

| Samsung | 91% | 45% | 20% | 8% | 2% | 0% | -1% | -3% | 13% | -15% | -43% | 58% | 21% | 291% | 24% | -10% | -10% |

| SK Hynix | 65% | - | - | - | - | - | - | - | 15% | -18% | -38% | 76% | 31% | - | - | - | |

| Micron | 65% | 62% | 17% | 3% | 0% | 0% | -3% | -4% | 17% | -9% | -47% | 43% 35% | 217% | 17% | -9% | -9% | |

| Nanya | 71% | 61% | 23% | 8% | 2% | 0% | -2% | -3% | 47% | -10% | -44% | 13% | 24% 276% | 27% | -14% | -14% | -14% |

| Top 4 total | 76% | 15% | -15% | -43% | 59% | 28% |

*Upbeat YTD data points not yet fully reflected in 2026 ASP; thus earnings upside seen

**SK Hynix information is historical data only

Source: Companies, BofA Global Research estimates, industry data. Chg = change. Equiv = equivalent

BofA GLOBAL RESEARCH

Exhibit 20: Company-specific NAND sales/ASP/shipment/margin comparison - high margin due to eSSD and 3D NAND

Bottom-up approach analysis based on top-4 NAND companies' quarterly earnings results

| (256Gb equiv) | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | 2028E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales (US$bn) | |||||||||||||||||

| Samsung | 15.4 | 26.1 | 33.4 | 36.0 | 35.0 | 33.9 | 35.1 | 36.8 | 22.2 | 14.2 | 26.1 | 25.2 | 110.9 | 140.8 | 144.4 | 144.4 | 144.4 |

| Kioxia ex-foundry | 5.8 | 10.4 | 12.5 | 12.7 | 11.7 | 11.6 | 12.1 | 12.1 | 9.4 | 5.6 | 9.5 | 9.2 | 41.4 | 47.4 | 46.7 | 46.7 | 46.7 |

| Micron | 5.0 | 9.9 | 11.4 | 12.5 | 12.9 | 12.7 | 12.2 | 12.4 | 7.0 | 4.3 | 8.2 | 9.0 | 38.9 | 50.2 | 50.3 | 50.3 | 50.3 |

| SK Hynix | 9.7 | - | - | - | - | - | - | - | 12.4 | 8.4 | 16.0 | 16.9 | - | - | - | - | - |

| Global total | 45.3 | 67.3 | 42.4 | 78.1 | 81.0 | ||||||||||||

| OP margin (%) | |||||||||||||||||

| Samsung | 60% | 65% | 65% | 62% | 59% | 58% | 56% | 54% | 13% | -68% | 13% | 4% | 63% | 57% | 52% | 52% | 52% |

| Kioxia ex-foundry | 60% | 72% | 72% | 70% | 67% | 65% | 63% | 61% | 15% | -46% | 27% | 19% | 70% | 64% | 53% | 53% | 53% |

| Micron | 58% | 78% | 78% | 79% | 78% | 77% | 75% | 74% | 0% | -71% | 8% | 5% | 76% | 76% | 71% | 71% | 71% |

| SK Hynix | 54% | - | - | - | - | - | - | - | -12% | -76% | 14% | 8% | - | - | |||

| ASP (US$) | |||||||||||||||||

| Samsung | 5.5 | 9.1 | 10.5 | 10.5 | 10.2 | 9.9 | 9.4 | 9.2 | 2.9 | 1.6 | 2.6 | 2.5 | 9.0 | 9.7 | 8.5 | 8.5 | 8.5 |

| Kioxia ex-foundry | 5.2 | 9.2 | 9.5 | 9.3 | 9.0 | 8.6 | 8.1 | 7.9 | 3.4 | 1.8 | 2.6 | 2.2 | 8.4 | 8.4 | 7.2 | 7.2 | 7.2 |

| Micron | 2.3 | 4.3 | 4.6 | 4.8 | 4.7 | 4.6 | 4.2 | 4.1 | 1.7 | 0.8 | 1.3 | 1.2 | 4.1 | 4.4 | 3.7 | 3.7 | 3.7 |

| SK Hynix | 5.5 | - | - | - | - | - | - | - | 2.4 | 1.4 | 2.6 | 2.5 | - | - | |||

| 5.0 | 3.0 | 1.6 | 2.6 | 2.4 | |||||||||||||

| Global total | |||||||||||||||||

| Samsung | 2.8 | 2.9 | 3.2 | 3.4 | 3.4 | 3.4 | 3.7 | 4.0 | 7.7 | 8.9 | 9.9 | 10.2 | 12.3 | 14.6 | 17.0 | 17.0 | 17.0 |

| Kioxia ex-foundry | 1.1 | 1.1 | 1.3 | 1.4 | 1.3 | 1.3 | 1.5 | 1.5 | 2.7 | 3.0 | 3.6 | 4.1 | 4.9 | 5.7 | 6.5 | 6.5 | 6.5 |

| Micron | 2.1 | 2.3 | 2.5 | 2.6 | 2.7 | 2.8 | 2.9 | 3.1 | 4.1 | 5.3 | 6.2 | 7.8 | 9.5 | 11.4 | 13.7 | 13.7 | 13.7 |

| SK Hynix | 1.8 | - | - | - | - | - | - | - | 5.1 | 6.1 | 6.0 | 6.7 | - | - | - | - | - |

| Global total | 9.0 | 22.6 | 26.6 | 29.5 | 33.2 | ||||||||||||

| Bit growth QoQ/YoY | |||||||||||||||||

| Samsung | 7% | 3% | 11% | 8% | -1% | 0% | 9% | 8% | 3% | 16% | 11% | 3% | 20% | 18% | 17% | 17% | 17% |

| Kioxia ex-foundry | -10% | 2% | 16% | 4% | -5% | 3% | 11% | 3% | -1% | 10% | 19% | 15% | 20% | 15% | 15% | 15% | 15% |

| Micron | 2% | 6% | 9% | 5% | 4% | 2% | 4% | 5% | 0% | 27% | 18% | 26% | 22% | 20% | 19% | 19% | 19% |

| SK Hynix | -10% | - | - | - | - | - | - | - | 42% | 21% | -2% | 12% | - | - | |||

| Global total | -2% | 6% | 18% | 11% | 13% | ||||||||||||

| ASP chg QoQ/YoY | |||||||||||||||||

| Samsung | 88% | 65% | 15% | 0% | -2% | -3% | -5% | -3% | -15% | -45% | 66% | -7% | 266% | 7% | -12% | -12% | -12% |

| Kioxia ex-foundry | 105% | 75% | 3% | -2% | -3% | -4% | -6% | -3% | -15% | -46% | 43% | -15% | 276% | 0% | -14% | -14% | -14% |

| Micron | 79% | 87% | 6% | 4% | -2% | -3% | -8% | -4% | -3% | -52% | 61% | -13% | 254% | 7% | -16% | -16% | -16% |

| SK Hynix | 75% | - | - | - | - | - | - | - | -18% | -44% | 93% | -5% | - | - | - | - | - |

| Global total | 75% | -13% | -46% | 65% | -8% | ||||||||||||

| Sales mkt shr | |||||||||||||||||

| Samsung | 34% | 33% | 34% | 33% | 31% | ||||||||||||

| Kioxia ex-foundry | 13% | 14% | 13% | 12% | 11% | ||||||||||||

| Micron | 11% | 10% | 10% | 11% | 11% | ||||||||||||

| SK Hynix | 21% | 18% | 20% | 20% | 21% | ||||||||||||

| Global total | 100% | 100% | 100% | 100% | 100% | ||||||||||||

| Bit mkt shr | |||||||||||||||||

| Samsung | 31% | 34% | 34% | 34% | 31% | ||||||||||||

| Kioxia ex-foundry | 12% | 12% | 11% | 12% | 12% | ||||||||||||

| Micron | 24% | 18% | 20% | 21% | 23% | ||||||||||||

| SK Hynix | 20% | 23% | 23% | 20% | 20% | ||||||||||||

| Global total | 100% | 100% | 100% | 100% | 100% |

*Upbeat YTD data points not yet fully reflected in 2026 ASP; thus earnings upside seen

** SK Hynix information is historical data only

***Kioxia data mostly based on JV fab NAND production/sales; thus it can be different vs the company's GAAP basis accounting results

Source: Companies, BofA Global Research estimates, industry data. Chg = change. Equiv = equivalent

BofA GLOBAL RESEARCH

Exhibit 21: Smartphone and PC production cut assumed for 2026 due to memory chip shortage and very expensive BOM - a mild recovery assumed for 2027-28 once memory supply shortage somewhat relieved; separately server shipment growth can be stronger due to AI boom

Product unit assumptions - our underlying assumptions for tech product shipments

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | CAGR 2025-28E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Units (mn) | ||||||||||||||

| 5G smartphone | 19 | 269 | 614 | 678 | 730 | 847 | 888 | 752 | 777 | 850 | -1.4% | |||

| Non-5G smartphone | 1,488 | 1,508 | 1,432 | 1,394 | 1,031 | 744 | 520 | 421 | 371 | 349 | 273 | 199 | 178 | -20.0% |

| Smartphones | 1,488 | 1,508 | 1,432 | 1,413 | 1,300 | 1,358 | 1,198 | 1,152 | 1,218 | 1,237 | 1,025 | 976 | 1,028 | -6.0% |

| Apple iPhone) | 215 | 216 | 205 | 192 | 195 | 238 | 233 | 225 | 222 | 243 | 215 | 262 | 269 | 3.4% |

| Samsung | 311 | 315 | 290 | 295 | 254 | 271 | 258 | 225 | 224 | 240 | 227 | 232 | 242 | 0.3% |

| Other OEMs | 962 | 977 | 936 | 926 | 851 | 849 | 707 | 702 | 772 | 754 | 583 | 482 | 517 | -11.8% |

| Tablet | 204 | 185 | 173 | 160 | 188 | 184 | 163 | 138 | 147 | 151 | 125 | 118 | 124 | -6.4% |

| SSD | 130 | 167 | 201 | 248 | 340 | 431 | 399 | 351 | 378 | 425 | 396 | 401 | 426 | 0.1% |

| PC | 256 | 255 | 255 | 261 | 297 | 351 | 294 | 253 | 256 | 275 | 228 | 217 | 228 | -6.0% |

| Server | 10 | 10 | 12 | 12 | 13 | 14 | 15 | 12 | 14 | 17 | 20 | 23 | 25 | 12.9% |

| Auto - DRAM embedded | 57 | 61 | 65 | 67 | 63 | 69 | 69 | 72 | 75 | 79 | 85 | 90 | 96 | 6.7% |

| TV (LCD, OLED) | 222 | 215 | 221 | 223 | 225 | 214 | 203 | 199 | 201 | 203 | 206 | 209 | 213 | 1.6% |

| Game - DRAM embedded | 44 | 50 | 52 | 51 | 42 | 48 | 43 | 41 | 42 | 42 | 43 | 45 | 45 | 2.1% |

| Growth YoY | ||||||||||||||

| 5G smartphone Non-5G smartphone | 3.3% | 1.3% | -5.1% | -2.6% | -26.1% | 128.1% -27.8% | 10.3% -30.1% | 7.8% -19.0% | 16.0% -12.0% | 4.9% -6.0% | -15.3% -21.8% | 3.3% -27.0% | 9.4% -10.4% | |

| Smartphones | 3.3% | 1.3% | -5.1% | -1.3% | -8.0% | 4.5% | -11.8% | -3.9% | 5.7% | 1.5% | -17.1% | -4.8% | 5.4% | |

| Apple iPhone) | -7.0% | 0.2% | -4.8% | -6.5% | 1.3% | 22.2% | -2.1% | -3.4% | -1.3% | 9.5% | -11.5% | 21.9% | 2.7% | |

| Samsung | -3.0% | 1.5% | -8.1% | 1.8% | -14.0% | 6.8% | -4.8% | -12.8% | -0.6% | 7.3% | -5.4% | 2.1% | 4.5% | |

| Other OEMs | 8.3% | 1.5% | -4.1% | -1.1% | -8.0% | -0.3% | -16.8% | -0.7% | 10.0% | -2.4% | -22.6% | -17.3% | 7.3% | |

| Tablet | -9.1% | -9.0% | -6.3% | -7.5% | 17.2% | -2.0% | -11.7% | -15.5% | 6.6% | 3.1% | -17.4% | -5.3% | 4.7% | |

| SSD | 36.2% | 28.4% | 20.0% | 23.7% | 36.9% | 26.7% | -7.3% | -12.0% | 7.6% | 12.4% | -6.8% | 1.1% | 6.2% | |

| PC | -5.9% | -0.3% | -0.2% | 2.6% | 13.6% | 4.0% | -16.2% | -13.8% | 1.0% | 7.6% | -17.0% | -4.9% | 5.1% | |

| Server | -1.6% | 7.2% | 15.7% | -0.4% | 7.3% | 6.9% | 9.7% | -17.5% | 18.0% | 19.8% | 16.9% | 11.7% | 10.3% | |

| Auto - DRAM embedded | 13.1% | 7.1% | 5.3% | 3.5% | -5.2% | 8.6% | 0.3% | 4.7% | 3.4% | 5.9% | 6.8% | 6.7% | 6.7% | |

| TV (LCD, OLED) | -1.2% | -3.2% | 2.9% | 0.7% | 1.0% | -5.2% | -4.8% | -2.1% | 1.0% | 1.1% | 1.2% | 1.8% | 1.8% | |

| Game - DRAM embedded | 6.9% | 12.8% | 3.0% | -1.3% | -16.8% | 12.5% | -9.7% | -4.9% | 2.5% | 1.0% | 2.4% | 3.0% | 0.8% |

Note: Sell-in based thus actual sell-through can be higher/lower than our assumptions; we still assume minimal impact of Huawei given other OEMs' market share increase, etc; memory content increase (auto, server,

SSD) likely stronger than unit growth; smartphone shipment estimate is slightly lowered due to Samsung Electronics' weak shipment for mid to low end phones vs upbeat AI smartphone GS24

Source: SA, IDC, IHS, BofA Global Research estimates

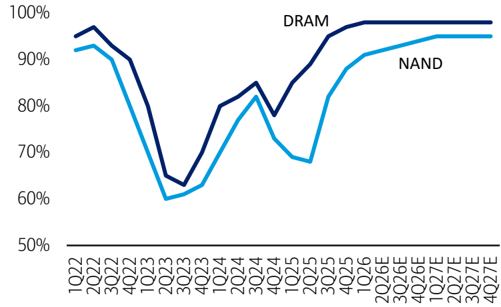

Exhibit 22: NAND inventories likely up through 2027 but still normal level or slightly higher; DRAM continuously tight

Memory chipmakers' inventories - finished chips in weeks

Source: BofA Global Research estimates

BofA GLOBAL RESEARCH

BofA GLOBAL RESEARCH

Exhibit 23: DRAM mostly full utilization; NAND also more than 90% - different vs 2H24-1H25 production cut

Memory chipmakers' fab utilization

Source: BofA Global Research estimates

BofA GLOBAL RESEARCH

Exhibit 24: Mostly server (including HBM) and smartphone-driven sales seen

Implied DRAM sales mix based on bit shipments x ASP by application

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DRAM sales mix | |||||||||||||

| Servers | 25% | 26% | 35% | 24% | 30% | 31% | 41% | 33% | 48% | 55% | 58% | 61% | 65% |

| PCs | 10% | 14% | 14% | 13% | 14% | 15% | 14% | 11% | 11% | 12% | 6% | 5% | 5% |

| Smartphones | 26% | 31% | 29% | 45% | 38% | 36% | 34% | 33% | 34% | 30% | 21% | 18% | 17% |

| Spot, others, adjustments* | 39% | 29% | 22% | 18% | 18% | 18% | 12% | 22% | 7% | 2% | 14% | 16% | 13% |

| Demand mix total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% |

| DRAM sales, US$bn | |||||||||||||

| Servers | 10.2 | 18.9 | 34.4 | 14.9 | 19.4 | 28.5 | 31.6 | 15.8 | 42.3 | 73.4 | 331.9 | 501.9 | 585.5 |

| PCs | 4.1 | 10.0 | 13.9 | 8.4 | 8.9 | 14.2 | 10.6 | 5.3 | 9.6 | 16.6 | 36.9 | 41.9 | 41.2 |

| Smartphones | 10.6 | 22.9 | 29.0 | 27.9 | 25.0 | 32.9 | 26.1 | 15.7 | 29.6 | 40.6 | 119.8 | 148.7 | 155.2 |

| Spot, others, adjustments* | 16.3 | 21.0 | 22.0 | 11.3 | 12.0 | 16.6 | 9.4 | 10.5 | 6.5 | 3.2 | 80.0 | 133.9 | 118.8 |

| Total sales US$bn | 41.2 | 72.8 | 99.3 | 62.5 | 65.4 | 92.1 | 77.7 | 47.3 | 87.9 | 133.8 | 568.8 | 826.4 | 900.7 |

| DRAM ASP, US$/8Gb | |||||||||||||

| Servers | 5.9 | 7.7 | 9.9 | 3.3 | 3.1 | 3.6 | 3.2 | 1.8 | 3.2 | 4.0 | 14.0 | 17.7 | 17.0 |

| PCs | 2.6 | 5.8 | 7.2 | 3.7 | 3.0 | 3.6 | 3.0 | 1.5 | 2.4 | 3.5 | 10.4 | 13.1 | 11.2 |

| Smartphones | 4.1 | 6.6 | 6.9 | 5.1 | 4.1 | 4.4 | 3.5 | 2.0 | 2.9 | 3.3 | 11.7 | 14.9 | 13.4 |

| Spot, others, adjustments* | 4.5 | 5.7 | 6.6 | 3.0 | 2.9 | 3.4 | 2.7 | 1.7 | 2.0 | 4.6 | 12.6 | 13.8 | 11.1 |

| DRAM ind avg price | 4.3 | 6.4 | 7.7 | 3.9 | 3.3 | 3.8 | 3.2 | 1.8 | 2.9 | 3.7 | 13.0 | 16.1 | 14.9 |

| ASP change YoY | |||||||||||||

| Servers | -20% | 31% | 29% | -66% | -7% | 17% | -11% | -46% | 82% | 24% | 252% | 27% | -4% |

| PCs | -48% | 122% | 26% | -49% | -18% | 21% | -19% | -48% | 58% | 45% | 194% | 26% | -15% |

| Smartphones | -42% | 60% | 5% | -26% | -20% | 8% | -20% | -45% | 48% | 16% | 249% | 27% | -10% |

| Spot, others, adjustments* | -35% | 25% | 17% | -54% | -6% | 19% | -21% | -37% | 18% | 128% | 177% | 9% | -20% |

| DRAM ind avg price | -34% | 48% | 20% | -49% | -15% | 14% | -16% | -45% | 62% | 29% | 249% | 25% | -8% |

*Implied amount after server/PC/smartphone demand, thus negative figures possible due to channel inventories (not consumed)

Source: Company data, BofA Global Research estimates, industry data

Exhibit 25: Mostly for SSD (including enterprise solutions) and smartphone applications

Implied NAND sales mix based on bit shipments x ASP by application

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| NAND sales mix | |||||||||||||

| SSD | 30% | 33% | 34% | 36% | 45% | 47% | 48% | 40% | 49% | 52% | 60% | 61% | 64% |

| Smartphone | 36% | 38% | 33% | 34% | 33% | 34% | 33% | 31% | 35% | 33% | 25% | 23% | 23% |

| Spot, others, adjustments* | 34% | 29% | 33% | 30% | 22% | 19% | 18% | 29% | 16% | 14% | 15% | 17% | 14% |

| Demand mix total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% |

| NAND sales, US$bn | |||||||||||||

| SSD | 11.1 | 19.8 | 22.9 | 16.7 | 26.5 | 34.3 | 32.6 | 16.9 | 38.6 | 42.2 | 193.4 | 255.7 | 268.5 |

| Smartphone | 13.7 | 22.3 | 22.0 | 15.5 | 19.2 | 24.9 | 22.4 | 13.1 | 27.2 | 27.1 | 81.8 | 94.6 | 95.7 |

| Spot, others, adjustments* | 12.8 | 17.2 | 22.6 | 14.1 | 12.7 | 14.1 | 12.3 | 12.4 | 12.3 | 11.7 | 47.9 | 70.0 | 57.2 |

| Total sales US$bn | 37.6 | 59.2 | 67.4 | 46.3 | 58.5 | 73.3 | 67.3 | 42.4 | 78.1 | 81.0 | 323.1 | 420.4 | 421.5 |

| NAND ASP, US$/8Gb | |||||||||||||

| SSD | 8.5 | 10.6 | 8.8 | 4.5 | 4.4 | 4.0 | 3.4 | 1.7 | 3.1 | 2.7 | 11.1 | 12.6 | 11.2 |

| Smartphone | 8.7 | 10.5 | 8.6 | 4.4 | 4.3 | 4.1 | 3.3 | 1.7 | 2.8 | 2.3 | 7.9 | 9.0 | 7.7 |

| Spot, others, adjustments* | 7.7 | 9.2 | 6.9 | 3.0 | 2.6 | 2.1 | 2.0 | 1.4 | 1.7 | 2.1 | 4.2 | 4.3 | 3.2 |

| NAND ind avg price | 8.3 | 10.1 | 8.0 | 3.9 | 3.8 | 3.4 | 3.0 | 1.6 | 2.6 | 2.4 | 8.2 | 8.9 | 7.8 |

| ASP change YoY | |||||||||||||

| SSD | -29% | 25% | -17% | -49% | -1% | -10% | -13% | -49% | 76% | -13% | 314% | 14% | -11% |

| Smartphone | -30% | 21% | -18% | -48% | -2% | -4% | -21% | -48% | 64% | -18% | 248% | 14% | -15% |

| Spot, others, adjustments* | -27% | 19% | -24% | -57% | -14% | -17% | -8% | -31% | 26% | 23% | 97% | 3% | -26% |

| NAND ind avg price | -28% | 22% | -21% | -52% | -2% | -9% | -13% | -46% | 65% | -8% | 238% | 9% | -13% |

*Implied amount after SSD/smartphone demand, thus negative figures possible due to channel inventories (not consumed)

Source: Company data, BofA Global Research estimates, industry data

BofA GLOBAL RESEARCH

BofA GLOBAL RESEARCH

Record high capex includes heavy infrastructure spending

Exhibit 26: Big-3 DRAM makers' capex to grow in 2026, but it includes lots of non-WFE spending (shell fab, utilities, TCB/HB); overall capex growth rate likely to decelerate through 2027-28 vs 40%+ CAGR in 2023-25

DRAM capex trend

| US$bn | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Samsung | 12.5 | 8.9 | 8.2 | 11.6 | 12.2 | 13.9 | 17.0 | 19.9 | 29.0 | 38.8 | 44.3 |

| SK Hynix | 8.1 | 7.4 | 5.6 | 7.3 | 8.9 | 3.8 | 9.0 | 16.1 | - | - | - |

| Micron | 4.6 | 4.3 | 5.3 | 5.6 | 5.7 | 3.9 | 6.3 | 13.1 | 27.9 | 37.4 | 37.2 |

| Nanya | 0.7 | 0.2 | 0.3 | 0.4 | 0.7 | 0.4 | 0.5 | 0.4 | 1.7 | 2.3 | 2.3 |

| CXMT | 0.7 | 1.5 | 1.5 | 1.7 | 2.6 | 4.0 | 3.5 | 4.0 | 4.4 | 4.5 | |

| DRAM capex total | 27.1 | 21.9 | 21.4 | 27.1 | 31.0 | 25.2 | 37.7 | 53.9 | |||

| Capex change YoY | 66% | -19% | -2% | 27% | 14% | -19% | 49% | 43% | |||

| DRAM capex to sales | 27% | 35% | 33% | 29% | 40% | 53% | 43% | 40% | |||

| DRAM capex share | |||||||||||

| Samsung | 46% | 41% | 38% | 43% | 39% | 55% | 45% | 37% | |||

| SK Hynix | 30% | 34% | 26% | 27% | 29% | 15% | 24% | 30% | |||

| Micron | 17% | 19% | 25% | 21% | 19% | 16% | 17% | 24% | |||

| Nanya | 2% | 1% | 1% | 1% | 2% | 2% | 1% | 1% | |||

| CXMT | 3% | 7% | 6% | 5% | 10% | 11% | 6% | ||||

| Total | 99% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | |||

| DRAM capex YoY | |||||||||||

| Samsung | 72% | -28% | -8% | 42% | 5% | 14% | 22% | 17% | |||

| SK Hynix | 71% | -10% | -23% | 30% | 22% | -58% | 138% | 79% | |||

| Micron | 72% | -8% | 24% | 6% | 3% | -32% | 62% | 106% | |||

| Nanya | -30% | -74% | 62% | 40% | 72% | -39% | 27% | -17% | |||

| CXMT | 75% | 114% | 0% | 13% | 50% | 57% | -13% | ||||

| Total | 66% | -19% | -2% | 27% | 14% | -19% | 49% | 43% |

- SK Hynix information is historical data only

Source:

Companies' reports, BofA Global Research estimates

Exhibit 27: NAND capex also grows in 2026, but mainly due to low base in 2025

NAND capex trend

| US$bn | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 20252026E2027E2028E | |||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Samsung | 7.3 | 4.9 | 9.2 | 10.9 | 10.3 | 10.1 | 8.1 | 4.6 | 8.2 | 11.2 | 12.5 |

| Kioxia &JVs | 5.0 | 3.8 | 4.5 | 5.7 | 6.5 | 2.7 | 4.5 | 5.2 | 7.0 | 7.5 | 7.0 |

| Micron | 4.7 | 4.4 | 3.4 | 4.6 | 5.2 | 2.7 | 3.1 | 4.6 | 7.4 | 7.7 | 7.9 |

| SK Hynix | 6.3 | 4.4 | 2.7 | 3.4 | 4.1 | 1.6 | 2.3 | 2.5 | - | - | - |

| Intel China | 2.0 | 1.6 | 0.8 | 1.5 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| YMTC | 0.3 | 0.7 | 1.6 | 1.5 | 2.5 | 2.3 | 2.0 | 2.0 | 3.0 | 3.5 | 4.0 |

| NAND capex total | 26.0 | 20.1 | 22.5 | 27.9 | 29.0 | 19.7 | 20.4 | 19.3 | |||

| NAND capex chg YoY | 7% | -23% | 12% | 24% | 4% | -32% | 4% | -5% | |||

| NAND capex to sales | 38% | 43% | 38% | 38% | 43% | 46% | 26% | 24% | |||

| NAND capex share | |||||||||||

| Samsung | 28% | 25% | 41% | 39% | 36% | 51% | 39% | 24% | |||

| Kioxia &JVs | 19% | 19% | 20% | 20% | 22% | 14% | 22% | 27% | |||

| Micron | 18% | 22% | 15% | 17% | 18% | 14% | 15% | 24% | |||

| SK Hynix | 24% | 22% | 12% | 12% | 14% | 8% | 11% | 13% | |||

| Intel China | 8% | 8% | 4% | 5% | n/a | n/a | n/a | n/a | |||

| YMTC | 1% | 3% | 7% | 5% | 9% | 11% | 10% | 10% | |||

| NAND capex total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | |||

| NAND capex growth (YoY) | |||||||||||

| Samsung | -36% | -33% | 87% | 19% | -5% | -2% | -20% | -42% | 76% | 37% | 12% |

| Kioxia &JVs | 4% | -24% | 18% | 27% | 14% | -58% | 67% | 16% | 35% | 7% | -7% |

| Micron | 100% | -6% | -22% | 35% | 11% | -47% | 13% | 49% | 60% | 5% | 2% |

| SK Hynix | 97% | -29% | -38% | 26% | 19% | -60% | 42% | 5% | - | - | - |

| Intel China | 0% | -23% | -48% | 88% | na | na | na | na | na | na | na |

| YMTC | 200% | 133% | 129% | -6% | 67% | -10% | -11% | 0% | 50% | 17% | 14% |

| NAND capex total | 7% | -23% | 12% | 24% | 4% | -32% | 4% | -5% |

- SK Hynix information is historical data only

**Kioxia data mostly based on JV fab NAND production/sales; thus it can be different vs the company's GAAP basis accounting

results

Source:

Companies' reports, BofA Global Research estimates

BofA GLOBAL RESEARCH

BofA GLOBAL RESEARCH

Exhibit 28: Ex-conventional DRAM equipment capex spend likely up strongly due to HBM, but conventional DRAM and NAND spend broadly disciplined; nonequipment spend for buildings and utilities remain high

SPE vs non-SPE capex spend

| US$bn | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|

| SPE capex | ||||||||||

| DRAM | 12.1 | 12.7 | 16.2 | 17.3 | 14.1 | 23.8 | 34.8 | 58.9 | 74.8 | 79.9 |

| NAND | 12.1 | 14.3 | 18.2 | 18.7 | 11.9 | 12.9 | 13.5 | 21.5 | 25.6 | 26.8 |

| Total | 24.3 | 26.9 | 34.4 | 35.9 | 26.0 | 36.7 | 48.3 | 80.4 | 100.4 | 106.7 |

| SPE capex YoY | ||||||||||

| DRAM | -22% | 4% | 28% | 7% | -18% | 69% | 46% | 69% | 27% | 7% |

| NAND | -24% | 17% | 28% | 3% | -36% | 8% | 5% | 59% | 19% | 5% |

| Total | -23% | 11% | 28% | 5% | -28% | 41% | 32% | 66% | 25% | 6% |

| Non-SPE to capex | ||||||||||

| DRAM | 45% | 41% | 40% | 44% | 44% | 37% | 35% | 34% | 34% | 33% |

| NAND | 39% | 37% | 35% | 36% | 40% | 37% | 30% | 29% | 28% | 28% |

| Total | 42% | 39% | 38% | 40% | 42% | 37% | 34% | 32% | 32% | 32% |

| Total capex, US$bn | ||||||||||

| DRAM | 21.9 | 21.4 | 27.1 | 31.0 | 25.2 | 37.7 | 53.9 | 88.6 | 112.9 | 119.5 |

| NAND | 20.1 | 22.5 | 27.9 | 29.0 | 19.7 | 20.4 | 19.3 | 30.1 | 35.4 | 37.2 |

| Total | 42.0 | 43.9 | 55.0 | 60.0 | 45.0 | 58.2 | 73.2 | 118.7 | 148.3 | 156.7 |

Source: Company data, BofA Global Research estimates, industry data

BofA GLOBAL RESEARCH

Exhibit 29: DRAM capex increase likely to remain strong even in 2026 driven by big-3 chipmakers; NAND capex growth also notable (due to low base)

SPE capex spend by memory chipmakers

| US$bn | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|

| DRAM SPE | ||||||||||

| Samsung | 5.5 | 4.8 | 6.9 | 7.0 | 7.8 | 9.8 | 12.3 | 18.3 | 24.8 | 28.8 |

| SK Hynix | 2.9 | 2.5 | 3.4 | 4.3 | 1.6 | 6.1 | 9.9 | - | - | - |

| Micron | 2.9 | 3.5 | 3.7 | 3.8 | 2.1 | 3.8 | 9.0 | 18.1 | 23.2 | 23.4 |

| Nanya | 0.1 | 0.2 | 0.4 | 0.5 | 0.3 | 0.4 | 0.3 | 1.1 | 1.5 | 1.5 |

| CXMT | 0.3 | 1.2 | 1.3 | 1.2 | 2.0 | 3.2 | 2.8 | 3.2 | 3.5 | 3.6 |

| DRAM SPE total | 12.1 | 12.7 | 16.2 | 17.3 | 14.1 | 23.8 | 34.8 | |||

| YoY | ||||||||||

| Samsung | -25% | -14% | 44% | 1% | 12% | 27% | 25% | 49% | 36% | 16% |

| SK Hynix | -21% | -14% | 32% | 27% | -63% | 284% | 63% | - | - | - |

| Micron | -14% | 24% | 6% | 3% | -45% | 80% | 137% | 101% | 28% | 1% |

| DRAM SPE total | -22% | 4% | 28% | 7% | -18% | 69% | 46% | |||

| NAND SPE | ||||||||||

| Samsung | 3.4 | 5.7 | 6.7 | 6.6 | 6.2 | 5.2 | 3.2 | 6.2 | 8.4 | 9.4 |

| Kioxia &JVs | 2.1 | 2.7 | 3.4 | 4.1 | 1.4 | 2.7 | 3.7 | 5.0 | 5.3 | 4.8 |

| Micron | 3.0 | 2.3 | 3.1 | 3.5 | 1.4 | 1.9 | 3.0 | 5.2 | 5.4 | 5.5 |

| SK Hynix | 2.3 | 1.8 | 2.4 | 2.5 | 1.0 | 1.5 | 1.9 | - | - | - |

| YMTC | 0.0 | 1.0 | 1.2 | 1.8 | 1.8 | 1.3 | 1.4 | 2.0 | 2.5 | 2.8 |

| NAND SPE total | 12.1 | 14.3 | 18.2 | 18.7 | 11.9 | 12.9 | 13.5 | |||

| YoY | ||||||||||

| Samsung | -26% | 68% | 19% | -2% | -6% | -16% | -40% | 95% | 37% | 12% |

| Micron | -3% | -22% | 35% | 11% | -59% | 33% | 62% | 72% | 5% | 1% |

| SK Hynix | -38% | -24% | 36% | 2% | -61% | 57% | 27% | - | - | - |

| YMTC | 25% | 46% | 3% | -28% | 8% | 39% | 26% | 14% | ||

| NAND SPE total | -24% | 17% | 28% | 3% | -36% | 8% | 5% |

- SK Hynix information is historical data only

**Kioxia data mostly based on JV fab NAND production/sales; thus it can be different vs the company's GAAP basis accounting results

Source: Company data, BofA Global Research estimates, industry data

BofA GLOBAL RESEARCH

2026/27E HBM TAM expansion to US$77bn/135bn

Exhibit 30: We maintain our bullish view on HBM. We assume strong growth in 2026 sales (US$77bn; +122% YoY) driven by solid ASP growth (+27% YoY) and robust bit growth (+76%). Industry average OPM near 50%; no downturn in 2027 given volume growth and cost reduction fully offset price cut.

Global HBM market - record high revenue continues into 2027E (US$135bn)

| 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | 2029E | 2030E | CAGR 2025-28E | |

|---|---|---|---|---|---|---|---|---|---|---|

| HBMearnings | ||||||||||

| Sales, US$bn | 1.6 | 4.2 | 17.4 | 34.5 | 76.8 | 134.6 | 176.3 | 204.6 | 246.3 | 72% |

| Shipment units, GB bn | 0.1 | 0.5 | 1.6 | 3.1 | 5.4 | 7.7 | 10.1 | 12.9 | 16.2 | 49% |

| ASP, US$/GB | 16.7 | 8.8 | 11.0 | 11.3 | 14.3 | 17.4 | 17.5 | 15.9 | 15.2 | 16% |

| Price premium | 430% | 436% | 355% | 274% | 12% | 9% | 22% | 2% | -6% | |

| OP, US$bn | 0.4 | 1.8 | 8.3 | 14.6 | 37.6 | 72.4 | 98.2 | 111.3 | 135.7 | 89% |

| OP margin | 25% | 42% | 48% | 42% | 49% | 54% | 56% | 54% | 55% | |

| %YoY | ||||||||||

| Sales, US$bn | 55% | 155% | 316% | 98% | 122% | 75% | 31% | 16% | 20% | |

| Shipment units, GB bn | 95% | 383% | 233% | 94% | 76% | 44% | 30% | 27% | 26% | |

| ASP, US$/GB | n/a | n/a | 25% | 2% | 27% | 22% | 0% | -9% | -4% | |

| HBMshipment mix | ||||||||||

| HBM5+ | 0% | 0% | 0% | 0% | 0% | 0% | 23% | 55% | 79% | |

| HBM4e | 0% | 0% | 0% | 0% | 0% | 19% | 51% | 36% | 19% | |

| HBM4 | 0% | 0% | 0% | 0% | 32% | 64% | 24% | 9% | 3% | |

| HBM3e | 0% | 0% | 58% | 83% | 60% | 16% | 3% | 1% | 0% | |

| HBM3 | 10% | 60% | 27% | 14% | 7% | 1% | 0% | 0% | 0% | |

| HBM2e &below | 90% | 40% | 15% | 3% | 1% | 0% | 0% | 0% | 0% | |

| HBMmix total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | |

| %toDRAMshipment | 0.4% | 1.8% | 5.2% | 8.5% | 12.2% | 15.1% | 16.7% | 18.8% | 21.1% | |

| %toDRAMsales | 2.1% | 8.8% | 19.8% | 25.8% | 13.5% | 16.3% | 19.6% | 19.1% | 20.2% | |

| Wafer capacity,kwpm | 68 | 87 | 204 | 360 | 476 | 624 | 741 | 815 | 897 | 27% |

| %toDRAMwafer capacity | 4.4% | 5.4% | 11.8% | 19.3% | 23.0% | 27.8% | 31.1% | 32.6% | 34.5% | |

| Main node | 1z | 1z | 1a, 1b | 1a, 1b | 1b, 1c | 1c | 1c, 1d | 1d | 1d, 1e | |

| Implied demand, GB bn units | 0.1 | 0.5 | 1.8 | 3.3 | 6.4 | 8.7 | 10.2 | 12.1 | 15.8 | 46% |

| AI+HBM server units,mn | 0.3 | 1.0 | 1.9 | 2.8 | 4.5 | 5.9 | 6.3 | 6.8 | 7.5 | 32% |

| AI+HBM server shipment YoY | 42% | 289% | 88% | 50% | 62% | 30% | 8% | 7% | 11% | |

| GB HBMper AI+HBM server | 340 | 530 | 1,171 | 1,413 | 1,479 | 1,612 | 1,789 | 2,093 | 11% | |

| GB content growth QoQ/YoY | 13% | 56% | 954 80% | 23% | 21% | 5% | 9% | 11% | 17% | |

| AI+HBM to total server units* | 1.7% | 8.1% | 12.9% | 16.1% | 22.3% | 26.0% | 25.4% | 25.4% | 26.4% | |

| Global server units,mn | 14.9 | 12.3 | 14.5 | 17.3 | 20.2 | 22.6 | 24.9 | 26.7 | 28.6 | 13% |

| Global server units YoY | 10% | -17% | 18% | 20% | 17% | 12% | 10% | 7% | 7% | |

| Excess supply, GB bn units | 0.01 | -0.05 | -0.20 | -0.20 | -1.01 | -0.95 | -0.15 | 0.70 | 0.41 | |

| HBMsufficiency (supply to demand) | 13% | -10% | -11% | -6% | -16% | -11% | -1% | 6% | 3% |

Source: Companies' reports, BofA Global Research estimates

BofA GLOBAL RESEARCH

Exhibit 31: Our bottom-up approach based on Big-3 companies' track record and long-term plans

Global HBM market share by company

| 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | 2029E | 2030E | CAGR 2025-28E | |

|---|---|---|---|---|---|---|---|---|---|---|

| HBMunits, GB bn | ||||||||||

| SK Hynix | 0.06 | 0.27 | 0.87 | 1.78 | - | - | - | - | - | - |

| Samsung | 0.03 | 0.20 | 0.61 | 0.66 | 1.82 | 2.80 | 3.61 | 4.51 | 5.50 | 76% |

| Others | 0.00 | 0.01 | 0.10 | 0.62 | - | - | - | - | - | - |

| Global HBMtotal GB bn units | 0.10 | 0.47 | 1.58 | 3.06 | 5.38 | 7.74 | 10.08 | 12.85 | 16.19 | 49% |

| %of global DRAM volume | 0.4% | 1.8% | 5.2% | 8.5% | 12.2% | 15.1% | 16.7% | 18.8% | 21.1% | |

| HBMwafer capa, k wpm- yr avg | ||||||||||

| SK Hynix | 35 | 37 | 100 | 153 | - | - | - | - | - | - |

| Samsung | 30 | 45 | 78 | 133 | 178 | 246 | 298 | 312 | 322 | 31% |

| Others | 3 | 5 | 27 | 75 | - | - | - | - | - | - |

| GlobalHBM wafer capa total | 68 | 87 | 204 | 360 | 476 | 624 | 741 | 815 | 897 | 27% |

| %of global DRAM capacity | 4.4% | 5.4% | 11.8% | 19.3% | 23.0% | 27.8% | 31.1% | 32.6% | 34.5% | |

| Main node | 1z | 1z | 1a, 1b | 1a, 1b | 1b, 1c | 1c | 1c, 1d | 1d | 1d, 1e | |

| HBMASP, US$/GB | ||||||||||

| SK Hynix | 16.2 | 8.5 | 11.1 | 11.8 | - | - | - | - | - | - |

| Samsung | 17.8 | 9.3 | 11.0 | 9.8 | 14.8 | 17.3 | 17.4 | 16.0 | 15.2 | 21% |

| Global average - HBMASP | 16.7 | 8.8 | 11.0 | 11.3 | 14.3 | 17.4 | 17.5 | 15.9 | 15.2 | 16% |

| HBMprice premium | 430% | 436% | 355% | 274% | 12% | 9% | 22% | 2% | -6% | |

| HBMsales, US$bn | ||||||||||

| SK Hynix | 1.1 | 2.3 | 9.6 | 20.9 | - | - | - | - | - | - |

| Samsung | 0.6 | 1.8 | 6.7 | 6.5 | 26.9 | 48.5 | 62.7 | 72.1 | 83.6 | 113% |

| Others | 0.0 | 0.1 | 1.1 | 7.1 | - | - | - | - | - | - |

| GlobalHBM sales total | 1.6 | 4.2 | 17.4 | 34.5 | 76.8 | 134.6 | 176.3 | 204.6 | 246.3 | 72% |

| %of global DRAM sales | 2.1% | 8.8% | 19.8% | 25.8% | 13.5% | 16.3% | 19.6% | 19.1% | 20.2% | |

| Ex-HBM global DRAM | ||||||||||

| ex-HBM wafer capa,kwpm | 1,493 | 1,541 | 1,530 | 1,507 | 1,590 | 1,618 | 1,638 | 1,683 | 1,701 | 3% |

| ex-HBM GB bn units | 24.1 | 26.2 | 29.0 | 33.0 | 38.5 | 43.5 | 50.4 | 55.5 | 60.4 | 15% |

| ex-HBM ASP, US$/GB | 3.2 | 1.6 | 2.4 | 3.0 | 12.8 | 15.9 | 14.4 | 15.6 | 16.1 | 68% |

| ex-HBM sales, US$bn | 76.0 | 43.1 | 70.5 | 99.3 | 492.0 | 691.8 | 724.5 | 864.1 | 974.6 | 94% |

| HBMOPM | ||||||||||

| SK Hynix | 25% | 47% | 63% | 64% | - | - | - | - | - | - |

| Samsung | 27% | 38% | 33% | 20% | 53% | 58% | 62% | 62% | 63% | |

| HBMbit market share | ||||||||||

| SK Hynix | 66% | 57% | 55% | 58% | - | - | - | - | - | - |

| Samsung | 32% | 42% | 39% | 22% | 34% | 36% | 36% | 35% | 34% | |

| HBMsales market share | ||||||||||

| SK Hynix | 64% | 54% | 55% | 61% | - | - | - | - | - | - |

| Samsung | 34% | 44% | 39% | 19% | 35% | 36% | 36% | 35% | 34% | |

| HBMwafer capa mkt share | ||||||||||

| SK Hynix | 51% | 43% | 49% | 42% | - | |||||

| Samsung | 44% | 52% | 38% | 37% | ||||||

| HBMwafer capa mkt share total | 100% | 100% | 100% | 100% |

- SK Hynix information is historical data only

Source: Companies' reports, BofA Global Research estimates

BofA GLOBAL RESEARCH

Exhibit 32: Samsung's upside could come from more normalized HBM price (2026-28) vs 2025 bottom, focused on NVIDIA's Tier 2 customers (ex-US data centers) and Big Tech companies (Amazon, Google, Broadcom, AMD, etc.)

SEC - HBM earnings outlook

| 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | 2029E | 2030E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| HBM | ||||||||||||||||