PDF 原檔:報告_MS_NVL72機櫃6月_20260708_original.pdf

圖片清單(已驗證 2026-07-09)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_MS_NVL72機櫃6月_20260708_004.png |

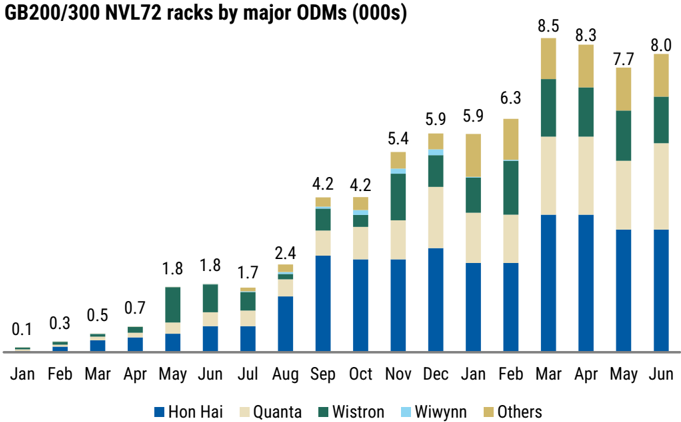

44KB | 真資料圖 | Exhibit 3:「GB200/300 NVL72 racks by major ODMs (000s)」月度堆疊長條圖,2025/1 至 2026/6,數值 0.1→8.0,圖例 Hon Hai/Quanta/Wistron/Wiwynn/Others |

報告_MS_NVL72機櫃6月_20260708_007.png |

60KB | 真資料圖 | 鴻海精密(2317.TW) 股價(藍線)與目標價調整沿革(紅色階梯線)圖,2023/07-2026/07,目標價區間 115→310 |

報告_MS_NVL72機櫃6月_20260708_008.png |

77KB | 真資料圖 | 廣達(2382.TW) 股價與目標價調整沿革圖,2023/07-2026/07,目標價區間 110→400 |

報告_MS_NVL72機櫃6月_20260708_009.png |

69KB | 真資料圖 | 緯創(3231.TW) 股價與目標價調整沿革圖,2023/07-2026/07,目標價區間 47→210 |

報告_MS_NVL72機櫃6月_20260708_001.png |

65KB | 裝飾·banner | 「Asia Summer School 2026」廣告 banner,泳池圖片+信封圖示 |

<40KB 未逐張列出者(002/003/005/006)為 Exhibit 1/2/4/5 的月度/份額圖,內容與已驗證的 Exhibit 3 及正文文字重複,未 Read。

原始內容

M July 8, 2026 01:07 PM GMT

Greater China Technology Hardware | Asia Pacific

GB200 and GB300 NVL72 Racks in June 2026

We provide monthly/quarterly rack shipment forecasts for ODMs. Within the major Server ODMs, our order of preference is Wistron > Hon Hai > Quanta, based on upside to PT.

Key Takeaways

- We estimate GB200/300 rack output in June at ~8.0K (+5% m/m), within which:

- Quanta shipped 2.3-2.4K GB200/GB300 racks.

- Wistron shipped 1.2-1.3K GB200/GB300 racks.

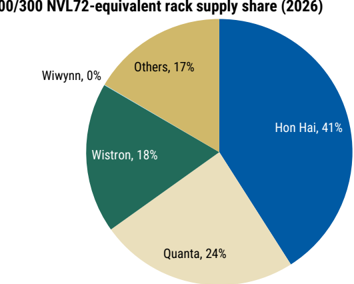

- Hon Hai shipped ~3.3K GB200/300 racks.

We continue to forecast 70-80K racks in CY26: This year should remain a strong one for downstream rack assembly. We expect over 100% y/y growth in rack shipments, vs. ~29k last year.

Quanta (2382.TW, OW): June revenue was NT$385.2B (+24% m/m, +103% y/y). We attribute the m/m growth primarily to higher GB200/300 rack shipments in the month, while NB shipments were also higher m/m at 4.5M units. But for GB200/300 rack shipments in the month, we estimate Quanta shipped 2.3-2.4K, higher than the 1.8-1.9K racks shipped in May. This brings overall 2Q GB200/300 rack shipments to approximately 6.2-6.3K (+32% q/q), slightly below our prior forecast of ~6.7K units, with the lowered rack shipments likely just pushed out into 2H. Our full-year assumption is unchanged at ~18.7K racks.

Wistron (3231.TW, OW): June revenue was NT$321.8B (+11% m/m, +54% y/y). We attribute the m/m growth to 1) higher revenue from Wiwynn (revenue grew 33% m/ m, to NT$111.4B), 2) higher monitor shipments at 1,000K units (+5% m/m), 3) higher DT shipments at 800K units (+33% m/m), and 4) higher NB shipments at 2M units (+18% m/m), offset slightly by lower GB200/300 server computing tray shipments (1,200-1,300 rack equivalents, by our estimates, down 5-10% m/m). This brings overall 2Q rack shipments to 3.9-4.0K units (flattish q/q), slightly below our prior forecast of ~4.2K, with the lowered rack shipments likely just pushed out into 2H. Our full-year assumption is unchanged at ~14.1K racks.

Hon Hai (2317.TW, OW): June revenue was NT$821.8B (-4% m/m, +52% y/y), with 1) the consumer segment, which mainly includes iPhone assembly, seeing slowing pullins and declining slightly m/m, 2) server-related revenue seeing sustained momentum for AI products, coming in flattish m/m, and 3) the computing segment falling slightly m/m. We model HH's GB rack shipments as flattish m/m at ~3.3K units, resulting in overall 2Q rack shipments of ~10.3K units (+21% q/q), slightly above our prior forecast of ~10K. For 3Q, it expects AI-related rack shipments to maintain growth, implying upside to our previous forecast of ~7.5K racks.

Update

Morgan Stanley Taiwan Limited+

Howard Kao

Equity Analyst Howard.Kao@morganstanley.com

+886 2 2730-2989

Irene Yen

Research Associate

Irene.Yen@morganstanley.com

+886 2 2730-2869

Morgan Stanley Asia Limited+

Andy Meng, CFA

Equity Analyst

Andy.Meng@morganstanley.com

+852 2239-7689

Greater China Technology Hardware

Asia Pacific Industry View

In-Line

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

+= Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to FINRA restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

M

GB200/300 Exhibits

We believe actual rack deliveries to end-customers are likely lower than these numbers because we include Wistron's computing tray (L10) rack equivalent (without accounting for rack assembly and test times for L11).

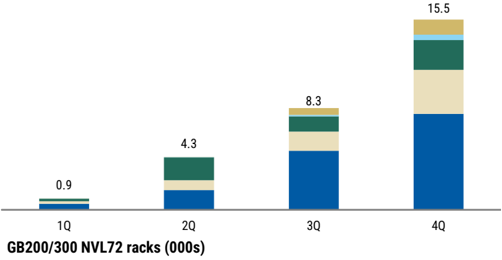

Exhibit 1: Industry-wide GB200/300 NVL72-equivalent monthly rack output, by major ODMs (2025)

GB200/300 NVL72 racks by major ODMs (000s)

Source: Morgan Stanley Research estimates.

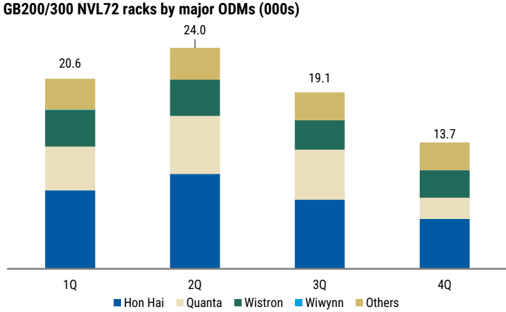

Exhibit 2: Industry-wide GB200/300 NVL72-equivalent monthly rack output, by major ODMs (2026)

Source: Morgan Stanley Research estimates.

Hon Hai

Quanta

Wistron

Exhibit 3:

Industry-wide GB200/300 NVL72-equivalent monthly rack output, by major ODMs (2025-2026)

Source: Morgan Stanley Research estimates.

Wiwynn

Others

M

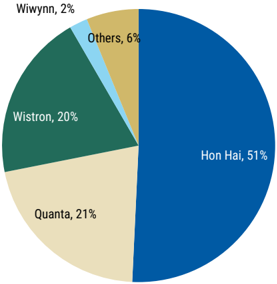

Exhibit 4: GB200/300 rack supply share, by major ODMs (2025)

GB200/300 NVL72-equivalent rack supply share (2025)

Source: Morgan Stanley Research estimates.

Exhibit 5: GB200/300 rack supply share, by major ODMs (2026)

Source: Morgan Stanley Research estimates.

M

Valuation Methodology and Risks

Hon Hai Precision (2317.TW)

Base case scenario value, derived from a residual income valuation model. Our key assumptions include a cost of equity of 8.5%, a medium-term growth rate of 13%, and a terminal growth rate of 3%.

Risks to Upside

- n Better-than-expected iPhone sell-through

- n Faster progress in AI server business

- n Faster EV business development progress

- n Any new M&A activity that could improve sentiment

Risks to Downside

- n Lower iPhone sell-through

- n Smaller profit contribution from AI business

- n Slower EV business development progress

- n Geopolitical developments that could negatively affect foreign investment

Quanta Computer Inc. (2382.TW)

Base case, residual income model. Key assumptions include a cost of equity of 9.0% (beta of 1.2, equity premium of 6.0% and risk-free rate of 1.5%), an 8.5% medium-term growth rate, and a 3% terminal growth rate.

Risks to Upside

- n Stronger-than-expected NB demand

- n Stronger-than-expected Apple Watch demand

- n Stronger-than-expected server demand

- n Faster-than-expected AI server penetration

Risks to Downside

- n Weaker-than-expected NB demand

- n Softer-than-expected Apple Watch demand

- n Weak margin performance owing to rising labor costs and sales shortfalls

- n Fierce price competition in the mega data center segment

- n Slower-than-expected AI server penetration

Wistron Corporation (3231.TW)

Base case, residual income valuation. Key assumptions: 8.7% cost of equity, 7.0% mediumterm growth rate and 3% terminal growth rate.

Risks to Upside

- n Faster-than-expected divestiture of consumer electronics business

- n Stronger-than-expected NB demand

- n Margin expansion from better product mix

M

- n Faster-than-expected AI server penetration

Risks to Downside

- n Slower-than-expected divestiture of consumer electronics business

- n Weaker-than-expected NB demand

- n Margin contraction from sales shortfall and fierce competition

- n Slower-than-expected AI server penetration

M

Disclosure Section

The information and opinions in Morgan Stanley Research were prepared or are disseminated by Morgan Stanley Asia Limited (which accepts the responsibility for its contents) and/or Morgan Stanley Asia (Singapore) Pte. (Registration number 199206298Z) and/or Morgan Stanley Asia (Singapore) Securities Pte Ltd (Registration number 200008434H), regulated by the Monetary Authority of Singapore (which accepts legal responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research), and/or Morgan Stanley Taiwan Limited and/or Morgan Stanley & Co International plc, Seoul Branch, and/or Morgan Stanley Australia Limited (A.B.N. 67 003 734 576, holder of Australian financial services license No. 233742, which accepts responsibility for its contents), and/or Morgan Stanley Wealth Management Australia Pty Ltd (A.B.N. 19 009 145 555, holder of Australian financial services license No. 240813, which accepts responsibility for its contents), and/or Morgan Stanley India Company Private Limited having Corporate Identification No (CIN) U22990MH1998PTC115305, regulated by the Securities and Exchange Board of India ('SEBI') and holder of licenses as a Research Analyst (SEBI Registration No. INH000001105); Stock Broker (SEBI Stock Broker Registration No. INZ000244438), Merchant Banker (SEBI Registration No. INM000011203), and depository participant with National Securities Depository Limited (SEBI Registration No. IN-DP-NSDL-567-2021) having registered office at Altimus, Level 39 & 40, Pandurang Budhkar Marg, Worli, Mumbai 400018, India; Telephone no. +91-22-61181000; Compliance Officer Details: Mr. Tejarshi Hardas, Tel. No.: +91-22-61181000 or Email: tejarshi.hardas@morganstanley.com; Grievance officer details: Mr. Tejarshi Hardas, Tel. No.: +91-22-61181000 or Email: msic-compliance@morganstanley.com which accepts the responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research, and their affiliates (collectively, "Morgan Stanley"). Morgan Stanley India Company Private Limited (MSICPL) may use AI tools in providing research services. All recommendations contained herein are made by the duly qualified research analysts.

For important disclosures, stock price charts and equity rating histories regarding companies that are the subject of this report, please see the Morgan Stanley Research Disclosure Website at www.morganstanley.com/eqr/disclosures/webapp/generalresearch, or contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY, 10036 USA.

For valuation methodology and risks associated with any recommendation, rating or price target referenced in this research report, please contact the Client Support Team as follows: US/Canada +1 800 303-2495; Hong Kong +852 2848-5999; Latin America +1 718 754-5444 (U.S.); London +44 (0)20-7425-8169; Singapore +65 6834-6860; Sydney +61 (0)2-9770-1505; Tokyo +81 (0)3-6836-9000. Alternatively you may contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY 10036 USA.