PDF 原檔:報告_Daiwa_南電8046_20260714_original.pdf

報告內文日期為 2026-07-13(Nan Ya Printed Circuit Board Corp (8046 TT): 13 July 2026),檔名依收檔日 20260714。

圖片清單(已驗證 2026-07-14)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

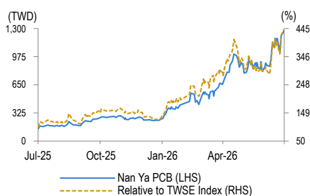

260714_daiwa_nypcb_001.png |

23KB | 真資料圖 | 股價走勢圖:Nan Ya PCB 股價(左軸 TWD)與相對 TWSE 指數(右軸 %),Jul-25 至 Jul-26 尾端急漲 |

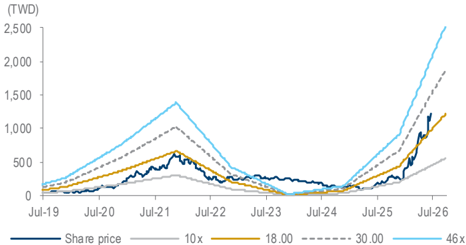

260714_daiwa_nypcb_002.png |

38KB | 真資料圖 | 1 年 forward PER band 圖(10x/18/30/46x)與股價 Jul-19 至 Jul-26;2021 高峰後回落,2025 下半年起沿 band 上緣急漲至約 1,200+ |

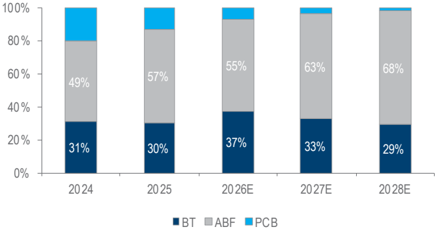

260714_daiwa_nypcb_003.png |

20KB | 真資料圖 | 營收結構堆疊柱狀圖 2024–2028E(BT/ABF/PCB):ABF 49%→57%→55%→63%→68%,BT 31%→30%→37%→33%→29%,PCB 其餘收斂 |

原始內容

Taiwan

Nan Ya Printed Circuit Board Corp (8046 TT)

Nan Ya Printed Circuit Board Corp

Target price:

TWD2,444.00 (from TWD1,444.00)

Share price (13 Jul):

TWD1,270.00 | Up/downside: +92.4%

Escalating price hikes in substrates

- Improving competitive landscape in BT substrate sector

- NYPCB is our top pick in substrate sector on fast-improving financials

- Reaffirming our Buy (1) rating; raising 12-month TP to TWD2,444

What's new: We believe that price hikes will be higher than our previous estimates, given current industry dynamics.

What's the impact: Key competitors in Asia have started to gradually exit the BT market. Due to stronger-than-expected ABF substrate demand on resilient AI server demand and rising regular server demand, we believe 2 global substrate vendors in Asia have stopped accepting BT substrate orders, as they tend to shift their capacity in co-sharing manufacturing processes from BT to ABF, given the supply-demand imbalance. We believe this would be a key positive trend for those substrate vendors that are willing to operate within the BT market; we also observe in the current cost inflation environment that low-end to mid-range materials would enjoy better pricing hikes given the capacity shift. As such, we expect price hike magnitudes of more than 20-30% QoQ for BT substrates in 3Q-4Q26E.

Financial updates. Given the improving pricing environment, we lift our gross margin forecasts for 2Q26/3Q26 to 24.3%/30.6% (from 21.3% /26.6%), factoring in higher-than-expected price hikes. We also lift our 2027-28E gross margins by c.8pp to 44.9%/53.2% (from 37.1%/46.4%). Mainly due to the current supply shortage, we believe NYPCB can achieve prior record-high gross margins from 2027E and set a new bar in 2028E (vs. our previous estimate for it to reach prior record-high levels in 2028E).

Investment ideas. We expect substrates to be the 2nd component, after memory, to have the highest price hikes (>70%/>50% price hike for BT/ABF substrates in 2026E) in the current cost inflation environment, and price hikes are just escalating. Including our updates on 17 May and 22 June, we have now lifted our 2027-28E EPS by 77-111% in just 2 months, but the share price has only risen by c.50% over the same period; hence, we see more upside from here. While we remain positive on all substrate vendors, we believe those with higher bargaining power will enjoy faster margin expansion in the short term, which makes NYPCB our top pick in the substrate sector.

What we recommend: We raise our 2026-28E EPS by 20-42% to factor in higher-than-expected price hikes from raw materials and substrates. We reaffirm our Buy (1) call and raise our 12-month TP to TWD2,444 (from TWD1,444), based on an unchanged target PER of 49x applied to our 4Q26-3Q27E EPS (vs. 3Q26-2Q27E). Downside risk: weaker-thanexpected demand for switches/PCs/smartphones.

How we differ: Our 2026-28E EPS are 28-66% above the Bloomberg consensus, likely due to our more bullish view on ABF/BT ASP hikes.

Daiwa

5

3

2

1

Buy

Sheng Cheng

Sheng Cheng (886) 2 8758 6253 sheng.cheng@daiwacm-cathay.com.tw

Allan Wang (886) 2 8758 6249

allan.wang@daiwacm-cathay.com.tw

Forecast revisions (%)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue change | 2.7 | 10.1 | 24.9 |

| Net profit change | 20 | 33.5 | 41.8 |

| Core EPS (FD) change | 20 | 33.5 | 41.8 |

Source: Daiwa forecasts

Share price performance

| 12-month range | 143.50-1,270.00 |

|---|---|

| Market cap (USDbn) | 25.48 |

| 3m avg daily turnover (USDm) | 541.04 |

| Shares outstanding (m) | 646 |

| Major shareholder | Nan Ya Plastics Corp (67.0%) |

Financial summary (TWD)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue (m) | 60,064 | 112,828 | 172,751 |

| Operating profit (m) | 14,962 | 48,457 | 88,579 |

| Net profit (m) | 12,725 | 40,031 | 72,783 |

| Core EPS (fully-diluted) | 19.693 | 61.951 | 112.638 |

| EPS change (%) | 553.6 | 214.6 | 81.8 |

| Daiwa vs Cons. EPS (%) | 28.2 | 66.2 | 55.6 |

| PER (x) | 64.5 | 20.5 | 11.3 |

| Dividend yield (%) | 0.8 | 2.4 | 4.4 |

| DPS | 9.8 | 31.0 | 56.3 |

| PBR (x) | 14.2 | 9.0 | 5.7 |

| EV/EBITDA (x) | 36.4 | 14.2 | 7.8 |

| ROE (%) | 24.5 | 53.7 | 61.9 |

Source: FactSet, Daiwa forecasts

Financial summary

Key assumptions

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Global PC shipment (m) | 361 | 301 | 260 | 263 | 287 | 244 | 244 | 244 |

| Regular server shipment (m) | 14 | 15 | 12 | 14 | 16 | 18 | 22 | 26 |

| Global smartphone shipment (m) | 1,655 | 1,437 | 1,380 | 1,437 | 1,429 | 1,249 | 1,255 | 1,300 |

Profit and loss (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| ABF | 25,805 | 38,250 | 25,758 | 15,797 | 22,701 | 33,333 | 71,547 | 117,990 |

| BT | 15,987 | 16,905 | 9,393 | 9,880 | 12,153 | 22,301 | 36,940 | 50,507 |

| Other Revenue | 10,437 | 9,492 | 7,101 | 6,606 | 5,320 | 4,429 | 4,341 | 4,254 |

| Total Revenue | 52,228 | 64,647 | 42,253 | 32,283 | 40,173 | 60,064 | 112,828 | 172,751 |

| Other income | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| COGS | (37,346) | (38,779) | (34,075) | (31,926) | (36,526) | (43,348) | (62,161) | (80,853) |

| SG&A | (2,012) | (2,293) | (1,847) | (1,624) | (1,665) | (1,754) | (2,210) | (3,320) |

| Other op.expenses | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Operating profit | 12,871 | 23,575 | 6,330 | (1,267) | 1,982 | 14,962 | 48,457 | 88,579 |

| Net-interest inc./(exp.) | (32) | (22) | (19) | (18) | (14) | (15) | (15) | (15) |

| Assoc/forex/extraord./others | 257 | 1,809 | 796 | 1,447 | 377 | 594 | 446 | 324 |

| Pre-tax profit | 13,095 | 25,362 | 7,107 | 163 | 2,346 | 15,541 | 48,889 | 88,888 |

| Tax | (2,514) | (5,946) | (1,290) | 41 | (399) | (2,816) | (8,858) | (16,105) |

| Min. int./pref. div./others | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Net profit (reported) | 10,582 | 19,416 | 5,817 | 204 | 1,947 | 12,725 | 40,031 | 72,783 |

| Net profit (adjusted) | 10,582 | 19,416 | 5,817 | 204 | 1,947 | 12,725 | 40,031 | 72,783 |

| EPS (reported)(TWD) | 16.376 | 30.047 | 9.002 | 0.315 | 3.013 | 19.693 | 61.951 | 112.638 |

| EPS (adjusted)(TWD) | 16.376 | 30.047 | 9.002 | 0.315 | 3.013 | 19.693 | 61.951 | 112.638 |

| EPS (adjusted fully-diluted)(TWD) | 16.376 | 30.047 | 9.002 | 0.315 | 3.013 | 19.693 | 61.951 | 112.638 |

| DPS (TWD) | 10.000 | 18.000 | 5.500 | 1.000 | 1.000 | 9.847 | 30.976 | 56.319 |

| EBIT | 12,871 | 23,575 | 6,330 | (1,267) | 1,982 | 14,962 | 48,457 | 88,579 |

| EBITDA | 16,505 | 27,919 | 12,226 | 5,193 | 8,876 | 22,062 | 54,847 | 94,330 |

Cash flow (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Profit before tax | 13,095 | 25,362 | 7,107 | 163 | 2,346 | 15,541 | 48,889 | 88,888 |

| Depreciation and amortisation | 3,634 | 4,344 | 5,896 | 6,460 | 6,894 | 7,101 | 6,391 | 5,752 |

| Tax paid | (2,514) | (5,946) | (1,290) | 41 | (399) | (2,816) | (8,858) | (16,105) |

| Change in working capital | (2,337) | (2,805) | 7,510 | (1,779) | (3,218) | (6,559) | (13,394) | (14,066) |

| Other operational CF items | 4,050 | 11,352 | (2,709) | (2,725) | (2,596) | 0 | 0 | 0 |

| Cash flow from operations | 15,929 | 32,307 | 16,513 | 2,160 | 3,027 | 13,266 | 33,027 | 64,469 |

| Capex | (8,451) | (16,922) | (11,779) | (2,379) | (2,422) | (2,543) | (2,416) | (2,295) |

| Net (acquisitions)/disposals | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other investing CF items | 3,061 | 53 | (471) | (223) | 700 | 7 | 24 | 15 |

| Cash flow from investing | (5,391) | (16,869) | (12,251) | (2,602) | (1,723) | (2,537) | (2,393) | (2,280) |

| Change in debt | 983 | (1,981) | 0 | 0 | 0 | 0 | 0 | 0 |

| Net share issues/(repurchases) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Dividends paid | (2,197) | (6,462) | (11,631) | (3,554) | (646) | (646) | (6,363) | (20,015) |

| Other financing CF items | (1,678) | (222) | (180) | (289) | (241) | (413) | 0 | 0 |

| Cash flow from financing | (2,892) | (8,665) | (11,811) | (3,843) | (887) | (1,059) | (6,363) | (20,015) |

| Forex effect/others | (25) | 76 | (166) | 436 | (309) | (72) | (76) | (85) |

| Change in cash | 7,621 | 6,850 | (7,714) | (3,849) | 109 | 9,599 | 24,196 | 42,089 |

| Free cash flow | 7,478 | 15,386 | 4,734 | (219) | 605 | 10,723 | 30,611 | 62,174 |

Source: FactSet, Daiwa forecasts

Nan Ya Printed Circuit Board Corp (8046 TT): 13 July 2026

Daiwa

Financial summary continued …

Balance sheet (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Cash & short-term investment | 13,194 | 20,044 | 12,567 | 8,587 | 8,706 | 18,305 | 42,501 | 84,590 |

| Inventory | 5,348 | 5,803 | 3,896 | 4,101 | 5,068 | 6,255 | 8,868 | 11,655 |

| Accounts receivable | 11,062 | 14,893 | 6,898 | 6,996 | 9,552 | 16,203 | 28,935 | 42,640 |

| Other current assets | 572 | 570 | 1,113 | 991 | 296 | 296 | 296 | 296 |

| Total current assets | 30,176 | 41,310 | 24,474 | 20,675 | 23,623 | 41,059 | 80,600 | 139,181 |

| Fixed assets | 25,668 | 39,926 | 45,476 | 41,804 | 37,085 | 32,527 | 28,553 | 25,097 |

| Goodwill & intangibles | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other non-current assets | 502 | 514 | 487 | 460 | 500 | 494 | 470 | 455 |

| Total assets | 56,345 | 81,750 | 70,437 | 62,938 | 61,207 | 74,080 | 109,623 | 164,733 |

| Short-term debt | 1,669 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Accounts payable | 6,710 | 8,895 | 5,808 | 3,672 | 3,979 | 5,257 | 7,208 | 9,634 |

| Other current liabilities | 2,137 | 4,794 | 3,292 | 2,992 | 3,210 | 3,210 | 3,210 | 3,210 |

| Total current liabilities | 10,516 | 13,689 | 9,100 | 6,664 | 7,189 | 8,467 | 10,418 | 12,845 |

| Long-term debt | 227 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other non-current liabilities | 5,123 | 14,339 | 13,429 | 10,824 | 7,896 | 7,896 | 7,896 | 7,896 |

| Total liabilities | 15,866 | 28,028 | 22,530 | 17,488 | 15,085 | 16,363 | 18,314 | 20,740 |

| Share capital | 6,462 | 6,462 | 6,462 | 6,462 | 6,462 | 6,462 | 6,462 | 6,462 |

| Reserves/R.E./others | 34,017 | 47,261 | 41,446 | 38,989 | 39,661 | 51,256 | 84,848 | 137,531 |

| Shareholders' equity | 40,479 | 53,723 | 47,908 | 45,450 | 46,123 | 57,717 | 91,309 | 143,992 |

| Minority interests | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Total equity & liabilities | 56,345 | 81,750 | 70,437 | 62,938 | 61,207 | 74,080 | 109,623 | 164,733 |

| EV | 809,333 | 800,587 | 808,064 | 812,044 | 811,924 | 802,326 | 778,130 | 736,041 |

| Net debt/(cash) | (11,298) | (20,044) | (12,567) | (8,587) | (8,706) | (18,305) | (42,501) | (84,590) |

| BVPS (TWD) | 62.645 | 83.141 | 74.142 | 70.339 | 71.379 | 89.323 | 141.309 | 222.841 |

Key ratios (%)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Sales (YoY) | 35.6 | 23.8 | (34.6) | (23.6) | 24.4 | 49.5 | 87.8 | 53.1 |

| EBITDA (YoY) | 134.4 | 69.2 | (56.2) | (57.5) | 70.9 | 148.6 | 148.6 | 72.0 |

| Operating profit (YoY) | 213.3 | 83.2 | (73.1) | n.a. | n.a. | 654.7 | 223.9 | 82.8 |

| Net profit (YoY) | 188.6 | 83.5 | (70.0) | (96.5) | 855.6 | 553.6 | 214.6 | 81.8 |

| Core EPS (fully-diluted) (YoY) | 188.6 | 83.5 | (70.0) | (96.5) | 855.6 | 553.6 | 214.6 | 81.8 |

| Gross-profit margin | 28.5 | 40.0 | 19.4 | 1.1 | 9.1 | 27.8 | 44.9 | 53.2 |

| EBITDA margin | 31.6 | 43.2 | 28.9 | 16.1 | 22.1 | 36.7 | 48.6 | 54.6 |

| Operating-profit margin | 24.6 | 36.5 | 15.0 | n.a. | 4.9 | 24.9 | 42.9 | 51.3 |

| Net profit margin | 20.3 | 30.0 | 13.8 | 0.6 | 4.8 | 21.2 | 35.5 | 42.1 |

| ROAE | 29.1 | 41.2 | 11.4 | 0.4 | 4.3 | 24.5 | 53.7 | 61.9 |

| ROAA | 21.0 | 28.1 | 7.6 | 0.3 | 3.1 | 18.8 | 43.6 | 53.1 |

| ROCE | 34.0 | 49.1 | 12.5 | n.a. | 4.3 | 28.8 | 65.0 | 75.3 |

| ROIC | 36.6 | 57.4 | 15.0 | n.a. | 4.4 | 31.9 | 89.9 | n.a |

| Net debt to equity | net cash | net cash | net cash | net cash | net cash | net cash | net cash | net cash |

| Effective tax rate | 19.2 | 23.4 | 18.2 | 0.0 | 17.0 | 18.1 | 18.1 | 18.1 |

| Accounts receivable (days) | 70.7 | 73.3 | 94.1 | 78.5 | 75.2 | 78.3 | 73.0 | 75.6 |

| Current ratio (x) | 2.9 | 3.0 | 2.7 | 3.1 | 3.3 | 4.8 | 7.7 | 10.8 |

| Net interest cover (x) | 406.2 | 1,128.2 | 367.9 | 10.3 | 170.8 | 1,022.9 | 3,367.8 | 6,031.3 |

| Net dividend payout | 61.1 | 59.9 | 61.2 | n.a. | 33.2 | 50.0 | 50.0 | 50.0 |

| Free cash flow yield | 0.9 | 1.9 | 0.6 | n.a. | 0.1 | 1.3 | 3.7 | 7.6 |

Source: FactSet, Daiwa forecasts

Company profile

Nan Ya PCB originated as one of the business divisions of Nan Ya Plastics Corporation before transforming into a subsidiary in 1997, specialising in the manufacturing of printed circuit boards (PCBs) and integrated circuit (IC) substrates. The company's primary end applications include networking (c.50%), PCs (c.20%), consumer electronics (c.10%), automotive (c.10%) and other sectors. Its manufacturing facilities are located in Taiwan and China.

Nan Ya Printed Circuit Board Corp (8046 TT): 13 July 2026

Daiwa

NYPCB: revenue and earnings forecast revisions

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | Previous | New | Consensus | Previous | New | Consensus | Previous | New | Consensus |

| Revenue | 58,494 | 60,064 | 58,391 | 102,461 | 112,828 | 93,657 | 138,301 | 172,751 | 139,037 |

| Diff (%) | 2.7% | 2.9% | 10.1% | 20.5% | 24.9% | 24.2% | |||

| Gross Margin (%) | 24.0% | 27.8% | 22.1% | 37.1% | 44.9% | 33.5% | 46.4% | 53.2% | 47.8% |

| Operating profit | 12,367 | 14,962 | 11,885 | 36,180 | 48,457 | 30,009 | 62,239 | 88,579 | 57,628 |

| Op Margin (%) | 21.1% | 24.9% | 20.4% | 35.3% | 42.9% | 32.0% | 45.0% | 51.3% | 41.4% |

| Net profit | 10,600 | 12,725 | 9,926 | 2,979 | 40,031 | 24,091 | 51,319 | 72,783 | 46,765 |

| EPS (TWD) | 16.41 | 19.69 | 15.36 | 46.39 | 61.95 | 37.28 | 79.42 | 112.64 | 72.37 |

| Diff (%) | 20.0% | 28.2% | 33.5% | 66.2% | 41.8% | 55.6% |

Source: Daiwa forecasts

NYPCB: quarterly and annual P&L statement

| 2026E | 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2027E | 2025 | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | 1Q | 2QE | 3QE | 4QE | 1QE | 2QE | 3QE | 4QE | ||||

| Net revenue | 11,177 | 13,575 | 16,735 | 18,576 | 20,821 | 26,123 | 32,391 | 33,492 | 40,173 | 60,064 | 112,828 | 172,751 |

| COGS | (9,406) | (10,282) | (11,644) | (12,016) | (12,738) | (15,098) | (17,261) | (17,063) | (36,526) | (43,348) | (62,161) | (80,853) |

| Gross profit | 1,771 | 3,293 | 5,092 | 6,560 | 8,083 | 11,025 | 15,129 | 16,429 | 3,647 | 16,716 | 50,667 | 91,899 |

| Operating expenses | (419) | (425) | (450) | (460) | (490) | (520) | (580) | (620) | 1,665 | 1,754 | 2,210 | 3,320 |

| Operating profit | 1,352 | 2,868 | 4,642 | 6,100 | 7,593 | 10,505 | 14,549 | 15,809 | 1,982 | 14,962 | 48,457 | 88,579 |

| Non-operating profit | 246 | 112 | 110 | 111 | 106 | 106 | 108 | 111 | 363 | 579 | 432 | 309 |

| Pre-tax profit | 1,598 | 2,981 | 4,752 | 6,210 | 7,699 | 10,611 | 14,657 | 15,920 | 2,346 | 15,541 | 48,889 | 88,888 |

| Net profit | 1,309 | 2,441 | 3,891 | 5,085 | 6,304 | 8,689 | 12,002 | 13,036 | 1,947 | 12,725 | 40,031 | 72,783 |

| Net EPS (TWD) | 2.03 | 3.78 | 6.02 | 7.87 | 9.76 | 13.45 | 18.57 | 20.17 | 3.0 | 19.7 | 62.0 | 112.6 |

| Operating Ratios | ||||||||||||

| Gross margin | 15.8% | 24.3% | 30.4% | 35.3% | 38.8% | 42.2% | 46.7% | 49.1% | 9.1% | 27.8% | 44.9% | 53.2% |

| Operating margin | 12.1% | 21.1% | 27.7% | 32.8% | 36.5% | 40.2% | 44.9% | 47.2% | 4.9% | 24.9% | 42.9% | 51.3% |

| Pre-tax margin | 14.3% | 22.0% | 28.4% | 33.4% | 37.0% | 40.6% | 45.3% | 47.5% | 5.8% | 25.9% | 43.3% | 51.5% |

| Net margin | 11.7% | 18.0% | 23.2% | 27.4% | 30.3% | 33.3% | 37.1% | 38.9% | 4.8% | 21.2% | 35.5% | 42.1% |

| YoY (%) | ||||||||||||

| Net revenue | 32% | 42% | 53% | 66% | 86% | 92% | 94% | 80% | 24% | 50% | 88% | 53% |

| Gross profit | 312% | 328% | 385% | 369% | 356% | 235% | 197% | 150% | 920% | 358% | 203% | 81% |

| Operating profit | 3986% | 684% | 648% | 533% | 462% | 266% | 213% | 159% | -257% | 655% | 224% | 83% |

| Pre-tax profit | 524% | n.m. | 424% | 341% | 382% | 256% | 208% | 156% | 1338% | 563% | 215% | 82% |

| Net profit | 531% | n.m. | 437% | 323% | 382% | 256% | 208% | 156% | 856% | 554% | 215% | 82% |

| QoQ (%) | ||||||||||||

| Net revenue | 0% | 21% | 23% | 11% | 12% | 25% | 24% | 3% | ||||

| Gross profit | 27% | 86% | 55% | 29% | 23% | 36% | 37% | 9% | ||||

| Operating profit | 40% | 112% | 62% | 31% | 24% | 38% | 38% | 9% | ||||

| Pre-tax profit | 13% | 86% | 59% | 31% | 24% | 38% | 38% | 9% | ||||

| Net profit | 9% | 86% | 59% | 31% | 24% | 38% | 38% | 9% |

Source: Company, Daiwa forecasts

NYPCB: 1-year forward PER bands

Source: TEJ, Daiwa forecasts

Nan Ya Printed Circuit Board Corp (8046 TT): 13 July 2026

NYPCB: revenue breakdown by product

Source: Company, Daiwa forecasts

Daiwa

Nan Ya Printed Circuit Board Corp (8046 TT): 13 July 2026

ESG analysis

ESG risks

| Risks | Risks | Management | Analyst comments |

|---|---|---|---|

| Executive/board quality | 2 | Nan Ya PCB's board of directors (BoD) is responsible for overseeing the company's operations and ensuring adherence to corporate governance principles. The board comprises individuals with diverse expertise, contributing to effective decision-making and strategic planning. The company emphasizes the importance of corporate governance as a set of processes, customs, policies, laws, and institutions affecting the way the corporation is directed, administered, or controlled. Principal stakeholders include stockholders, management, and the board of directors, among others. | |

| G | Capital management | 2 | Nan Ya PCB maintains a prudent approach to capital management, ensuring financial stability and the availability of resources necessary for operational and strategic initiatives. The company's financial statements reflect a solid capital structure, supporting its growth and sustainability objectives. |

| Related party & transaction | 1 | The company adheres to strict policies regarding related party transactions to maintain transparency and fairness. Such transactions are conducted under terms comparable to those with independent third parties and are disclosed in financial reports to ensure compliance with regulatory standards and corporate governance best practices. For example, the company's consolidated financial statements provide details on transactions with related parties, ensuring transparency and accountability. | |

| S Supply management | chain | 1 | Nan Ya PCB is committed to sustainable supply chain management, emphasizing environmental protection, procurement policies, and social responsibility. The company has established a comprehensive procurement policy that integrates sustainability considerations, ensuring that suppliers adhere to ethical standards and environmental regulations. This commitment is part of the company's broader sustainable responsibility policy, which includes areas such as corporate governance, environmental protection, and social welfare. |

| E | Data security | 1 | While specific details on Nan Ya PCB's data security measures are not extensively disclosed in the available sources, the company recognizes the importance of information security in its operations. As part of its corporate governance framework, Nan Ya PCB is likely to implement standard data protection practices to safeguard sensitive information and ensure compliance with relevant regulations. Stakeholders are encouraged to consult the company's official communications or contact the company directly for detailed information on data security policies. |

Note: Management score represents a company's ability to manage/benefit from certain ESG topics. The scores range from 1 to 3, with 1 being the strongest.

Update Date: 7 May 2026

Source: Daiwa, Company

Daiwa

Nan Ya Printed Circuit Board Corp (8046 TT): 13 July 2026

Daiwa's Asia Pacific Research Directory

| HONG KONG | ||

|---|---|---|

| Hiroyuki GOTO | (852) 2773 8870 | hiroyuki.goto@hk.daiwacm.com |

| John HETHERINGTON (852) 8787 | 2773 Research and Head | john.hetherington@hk.daiwacm.com of Research Publications |

| Co-Head of Asia Pacific | ||

| Li XIONG | (852) 2773 8878 | li.xiong@hk.daiwacm.com |

| Strategy (Hong Kong/China) | ||

| Yue TAN | (852) 2848 4947 | yue.tan@hk.daiwacm.com |

| Strategy (Greater China) and Macro Economics (China) | ||

| Kelvin LAU | (852) 2848 4467 | kelvin.lau@hk.daiwacm.com |

| Regional Head of Automobiles, Industrials and Transportation | ||

| Evelyn ZHANG | (852) 2848 4970 | evelyn.zhang@hk.daiwacm.com |

| Frank YIP | (852) 2773 8842 | frank.yip@hk.daiwacm.com |

| Industrials and Transportation (Hong Kong/China) | ||

| Carol XIA | (852) 2532 4349 | carol.xia@hk.daiwacm.com |

| Head of China Consumer; Consumer (Hong Kong/China) | ||

| Steven NIE | (852) 2848 4464 | steven.nie@hk.daiwacm.com |

| Consumer (Hong Kong/China); Global Cryptocurrency | ||

| Siman CHEN | (852) 2532 4350 | siman.chen@hk.daiwacm.com |

| (Hong Kong/China) | ||

| Consumer Jing YANG | (852) 2532 4308 | jing.yang@hk.daiwacm.com |

| Head of China Healthcare | ||

| John CHOI | (852) 2773 8730 | john.choi@hk.daiwacm.com |

| Head of China Internet; Regional Head of Emerging Opportunities | ||

| Dennis IP 4068 Head of Asia US Power Equipment Wind, | (852) 2848 ex-Japan Power, Utilities, (Gas, Nuclear, Solar, | dennis.ip@hk.daiwacm.com Renewables & ESG (PURE) Research Grid, ESS & Battery Materials) |

| Derek ZHANG | (852) 2532 4341 | derek.zhang@hk.daiwacm.com |

| Power, Utilities, Renewables and ESS (PURE) - Gas, Wind and Grid (China), Utilities | ||

| (852) 2848 | ||

| Tina YU | (852) 2532 | tina.yu@hk.daiwacm.com |

| ESG (Asia ex-Japan) | ||

| 4106 | ||

| Power, Utilities, Renewables and ESS (PURE) - Power Equipment (US) | ||

| Marco ZENG | ||

| 4430 | ||

| marco.zeng@hk.daiwacm.com | ||

| (Hong Kong) |

Daiwa

| CHINA | CHINA | CHINA |

|---|---|---|

| Louis LUO | (86) 21 6841 3282 | louis.luo@daiwacm.cn |

| Automobiles and Components, Industrials (China) | Automobiles and Components, Industrials (China) | Automobiles and Components, Industrials (China) |

| Mavis MA | (86) 21 6841 3288 | mavis.ma@daiwacm.cn |

| Leo LU Power, Utilities, Renewables Infrastructure (China) | (86) 21 6841 3286 and ESS (PURE) | leo.lu@daiwacm.cn - Solar, ESS, Lithium, AIDC |

| Skye LIANG Power, Utilities, Renewables | (86) 21 6841 3207 and ESS (PURE) | skye.liang@daiwacm.cn Wind and Grid (China) |

| William WU Property (China/Hong | (86) 21 6841 3200 Kong) | william.wu@daiwacm.cn |

| Bintuo NI Tech Hardware and | (86) 21 6841 3228 Semiconductors (China) | bintuo.ni@daiwacm.cn |

| SOUTH KOREA | ||

|---|---|---|

| Yoonki BAE (82) 2 787 9168 yoonki.bae@kr.daiwacm.com Automobile Components, Healthcare | Yoonki BAE (82) 2 787 9168 yoonki.bae@kr.daiwacm.com Automobile Components, Healthcare | Yoonki BAE (82) 2 787 9168 yoonki.bae@kr.daiwacm.com Automobile Components, Healthcare |

| Mike OH | (82) 2 787 9179 | mike.oh@kr.daiwacm.com |

| Banking, Capital Goods - Defence, Construction and Shipbuilding, and Utilities | Banking, Capital Goods - Defence, Construction and Shipbuilding, and Utilities | Banking, Capital Goods - Defence, Construction and Shipbuilding, and Utilities |

| Youngho JANG Consumer, Healthcare | (82) 2 787 9838 | youngho.jang@kr.daiwacm.com |

| Henny JUNG EV Batteries and Battery Components | (82) 2 787 9182 Materials, IT/Electronics | henny.jung@kr.daiwacm.com (Small/Mid Cap), Automobiles and |

| Daeho SON | (82) 2 787 9176 | dh.son@kr.daiwacm.com |

| Joon LEE Media | (82) 2 787 9151 | hj.lee@kr.daiwacm.com |

| Thomas Y KWON | (82) 2 787 9181 | yskwon@kr.daiwacm.com |

| Pan-Asia Head of Internet & Telecommunications; Online Games | Pan-Asia Head of Internet & Telecommunications; Online Games | Pan-Asia Head of Internet & Telecommunications; Online Games |

| SK KIM Head of Global Memory; | (82) 2 787 9173 IT/Electronics - | sk.kim@kr.daiwacm.com Semiconductors/Displays and Tech Hardware |

| TAIWAN | |

|---|---|

| Rick HSU | (886) 2 8758 6261 rick.hsu@daiwacm-cathay.com.tw |

| Sheng CHENG | (886) 2 8758 6253 sheng.cheng@daiwacm-cathay.com.tw |

| Allan WANG | (886) 2 8758 6249 allan.wang@daiwacm-cathay.com.tw |

| Leon CHEN (886) 2 8758 6247 leon.chen@daiwacm-cathay.com.tw IT/Technology - Semiconductors Supply Chain (Taiwan) | |

| Stacy LIN | (886) 2 8758 6252 stacy.lin@daiwacm-cathay.com.tw |

| IT/Technology - Semiconductors Supply Chain (Taiwan) | |

| Helen | (886) 2 8758 6254 |

| Small/Mid Cap | |

| helen.chien@daiwacm-cathay.com.tw | |

| CHIEN |

Daiwa's Offices

| Office / Branch / Affiliate | Address | Tel | Fax |

|---|---|---|---|

| DAIWA SECURITIES GROUP INC | |||

| HEAD OFFICE | Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6753 | (81) 3 5555 3111 | (81) 3 5555 0661 |

| Daiwa Securities Trust Company | One Evertrust Plaza, Jersey City, NJ 07302, U.S.A. | (1) 201 333 7300 | (1) 201 333 7726 |

| Daiwa Securities Trust and Banking (Europe) PLC (Head Office) | 5 King William Street, London EC4N 7JB, United Kingdom | (44) 207 320 8000 | (44) 207 410 0129 |

| Daiwa Europe Trustees (Ireland) Ltd | Level 3, Block 5, Harcourt Centre, Harcourt Road, Dublin 2, Ireland | (353) 1 603 9900 | (353) 1 478 3469 |

| Daiwa Capital Markets America Inc. New York Head Office | 1251 Avenue of the Americas, 49th Floor, New York, NY 10020 | (1) 212 612 7000 | (1) 212 612 7100 |

| Daiwa Capital Markets America Inc. San Francisco Branch | 555 California Street, Suite 3360, San Francisco, CA 94104, U.S.A. | (1) 415 955 8100 | (1) 415 956 1935 |

| Daiwa Capital Markets Europe Limited, London Head Office | 5 King William Street, London EC4N 7AX, United Kingdom | (44) 20 7597 8000 | (44) 20 7597 8600 |

| Daiwa Capital Markets Deutschland GmbH | Friedrich-Ebert-Anlage 35-37, 60327 Frankfurt am Main, Germany | (49) 69 27139 8100 | (49) 69 27139 8190 |

| Daiwa Capital Markets Europe Limited, Paris Representative Office | 17, rue de Surène 75008 Paris, France | (33) 1 56 262 200 | (33) 1 47 550 808 |

| Daiwa Capital Markets Europe Limited, Moscow Representative Office | Midland Plaza 7th Floor, 10 Arbat Street, Moscow 119002, Russian Federation | (7) 495 641 3416 | (7) 495 775 6238 |

| Daiwa Capital Markets Europe Limited, Bahrain Branch | 7th Floor, The Tower, Bahrain Commercial Complex, P.O. Box 30069, Manama, Bahrain | (973) 17 534 452 | (973) 17 535 113 |

| Daiwa Capital Markets Hong Kong Limited | Level 28, One Pacific Place, 88 Queensway, Hong Kong | (852) 2525 0121 | (852) 2845 1621 |

| Daiwa Capital Markets Singapore Limited | 7 Straits View, Marina One East Tower, #16-05 & #16-06, Singapore 018936, Republic of Singapore | (65) 6387 8888 | (65) 6282 8030 |

| Daiwa Capital Markets Australia Limited | Level 34, Rialto North Tower, 525 Collins Street, Melbourne, Victoria 3000, Australia | (61) 3 9916 1300 | (61) 3 9916 1330 |

| DBP-Daiwa Capital Markets Philippines, Inc | 18th Floor, Citibank Tower, 8741 Paseo de Roxas, Salcedo Village, Makati City, Republic of the Philippines | (632) 813 7344 | (632) 848 0105 |

| Daiwa-Cathay Capital Markets Co Ltd | 14/F, 200, Keelung Road, Sec 1, Taipei, Taiwan, R.O.C. | (886) 2 2723 9698 | (886) 2 2345 3638 |

| Daiwa Securities Capital Markets Korea Co., Ltd. | 20 Fl.& 21Fl. One IFC, 10 Gukjegeumyung-Ro, Yeongdeungpo-gu, Seoul, Korea | (82) 2 787 9100 | (82) 2 787 9191 |

| Daiwa Securities Co. Ltd., Beijing Representative Office | Room 301/302 , Kerry Center , 1 Guanghua Road , Chaoyang District , Beijing 100020, People's Republic of China | (86) 10 6500 6688 | (86) 10 6500 3594 |

| Daiwa (Shanghai) Corporate Strategic Advisory Co. Ltd. | 44/F, Hang Seng Bank Tower, 1000 Lujiazui Ring Road, Pudong, Shanghai China 200120 , People's Republic of China | (86) 21 3858 2000 | (86) 21 3858 2111 |

| Daiwa Securities Co. Ltd., Bangkok Representative Office | 18 th Floor, M Thai Tower, All Seasons Place, 87 Wireless Road, Lumpini, Pathumwan, Bangkok 10330, Thailand | (66) 2 252 5650 | (66) 2 252 5665 |

| Daiwa Securities Co. Ltd., Hanoi Representative Office | Suite 405, Pacific Palace Building, 83B, Ly Thuong Kiet Street, Hoan Kiem Dist. Hanoi, Vietnam | (84) 4 3946 0460 | (84) 4 3946 0461 |

DAIWA INSTITUTE OF RESEARCH LTD

| HEAD OFFICE | 15-6, Fuyuki, Koto-ku, Tokyo, 135-8460, Japan | (81) 3 5620 5100 | (81) 3 5620 5603 |

|---|---|---|---|

| MARUNOUCHI OFFICE | Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6756 (81) 3 | 5555 7011 | (81) 3 5202 2021 |

| New York Research Center | 11th Floor, Financial Square, 32 Old Slip, NY, NY 10005-3504, U.S.A. | (1) 212 612 6100 | (1) 212 612 8417 |

| London Research Centre | 3/F, 5 King William Street, London, EC4N 7AX, United Kingdom | (44) 207 597 8000 | (44) 207 597 8550 |

Nan Ya Printed Circuit Board Corp (8046 TT): 13 July 2026

Daiwa