PDF 原檔:報告_Citi_奇鋐3017_20260707_original.pdf

圖片清單(已驗證 2026-07-08)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源;嵌入時只從這裡挑分類為「真資料圖」的,不照 trimmed 引用順序猜。建立步驟見

ingest_steps.mdStep 2.5。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Citi_奇鋐3017_20260707_001.png |

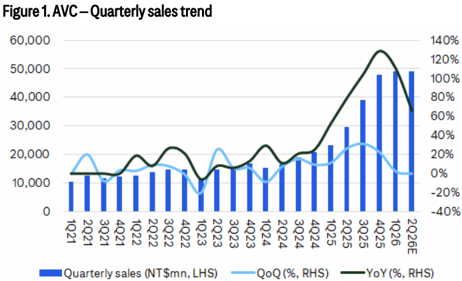

71KB | 真資料圖 | Figure 1. AVC – Quarterly sales trend:柱狀圖,橫軸 1Q21–2Q26E,左軸季營收(NT$mn),右軸 QoQ% 與 YoY% 折線 |

報告_Citi_奇鋐3017_20260707_002.png |

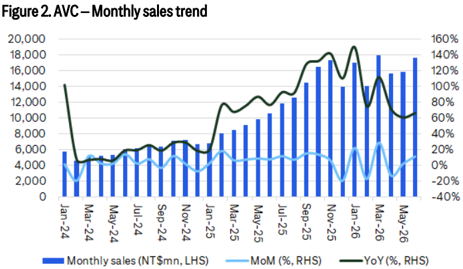

74KB | 真資料圖 | Figure 2. AVC – Monthly sales trend:柱狀圖,橫軸 Jan-24–Jun-26,左軸月營收(NT$mn),右軸 MoM% 與 YoY% 折線 |

報告_Citi_奇鋐3017_20260707_003.png |

170KB | 真資料圖 | AVC (3017.TW) 評等與目標價歷史(Fundamental Research)雙折線圖;含三個評等/目標價標記:Dec-11-25 TP NT$2,055 → Mar-11-26 TP NT$2,400 → Apr-30-26 TP NT$3,450;下半段為 Short-Term View/Catalyst Watch Research 圖 |

原始內容

citivelocity.com

07 Jul 2026 02:16:08 ET │ 11 pages

Asia Vital Components (3017.TW)

2Q26 Revenue In Line with Guidance; Transition Quarter Cleared

CITI'S TAKE

AVC reported Jun-26 revenue of NT$17.6bn (+11% MoM/+66% YoY), bringing 2Q26 revenue to NT$49.1bn (flat QoQ/+66% YoY). 2Q26 revenue was 3% below Citi/cons forecast but in line with guidance of 0-5% QoQ. The near-term shortfall reflects GPU platform transition headwinds as the cycle shifts toward Rubin generation. Looking ahead, margins upside is emerging from improving yield and the volume ramp of one of the ASIC project entering the mass production cycle. Within multiple ASIC engagements expected to accelerate in 2H26E, we expect a stronger revenue trajectory in 2H vs. 1H. Based on our supply chain checks, the recent revised up liquid cooling penetration in ASIC platforms could become the upside catalyst and further support AVC's growth into 2027E. Maintain Buy.

Prepared for Kevin Lu

Flash |

Buy

Price (06 Jul 26 13:30)

NT$2,670.00

Target price

NT$3,450.00

Expected share price return

29.2%

Expected dividend yield

0.8%

Expected total return Market Cap

30.0%

NT$1,048,090M US$32,813M

Michael Hung AC

+886-2-8726-9092 michael.hung@citi.com

Laura (Chia Yi) Chen +886-2-8726-9090 laura.cy.chen@citi.com

See Appendix A-1 for Analyst Certification, Important Disclosures and Research Analyst Affiliations

Figure 1. AVC - Quarterly sales trend

60,000

50,000

40,000

30,000

20,000

10,000

Quarterly sales (NT$mn, LHS) -

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission.

140%

120%

100%

80%

60%

40%

20%

0%

Figure 2. AVC - Monthly sales trend

20,000

18,000

16,000

14,000

12,000

10,000

8,000

6,000

4,000

- Monthly sales (NTSmn, LHS)

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission.

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission. Source: Company Reports, Citi Research

160%

140%

120%

100%

80%

60%

40%

20%

0%

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission. Source: Company Reports, Citi Research

Prepared for Kevin Lu

Prepared for Kevin Lu

Asia Vital Components

Valuation

We value AVC using a PE-based approach that factors in earnings momentum and the expansion of its addressable market. Our TP of NT$3,450 is derived from applying a 25x PE multiple on 2027E EPS, which we believe is justified given the company's entrenched positioned in the server thermal segment, rising contribution from liquid cooling, and the increasing value of thermal content per server as power density continues to climb. With these structural drivers still in place, we expect the multiple to hold at a premium relative to its historical averages.

Risks

This stock is High Risk based upon our quantitative model but assigning a High Risk rating is not supported by other qualitative factors such as cold-plate leadership and deep CSP penetration, and so a High Risk rating has not been applied. Key downside risks to our investment thesis and target price include: 1) slower adoption pace for liquid cooling adoption; 2) heightened price competition; 3) lower-than-expected share in liquid cooling components; and 4) emerging alternative cooling technologies.

Asia Vital Components (3017.TW)

Analyst: Michael Hung

TWD

2,000

If you are visually impaired and would like to speak to a Citi representative regarding the details of the graphics in this document, please call USA 1-888-500-5008 (TTY: 711), from outside the US +1-210-677-3788

Date

Appendix A-1

*Indicates Change