PDF 原檔:報告_MS_能源算力Supercycle_20260521_original.pdf

原始內容

M May 21, 2026 09:00 PM GMT

Asia Energy Security and AI

Energy Meets Compute: Supercycle Recharges

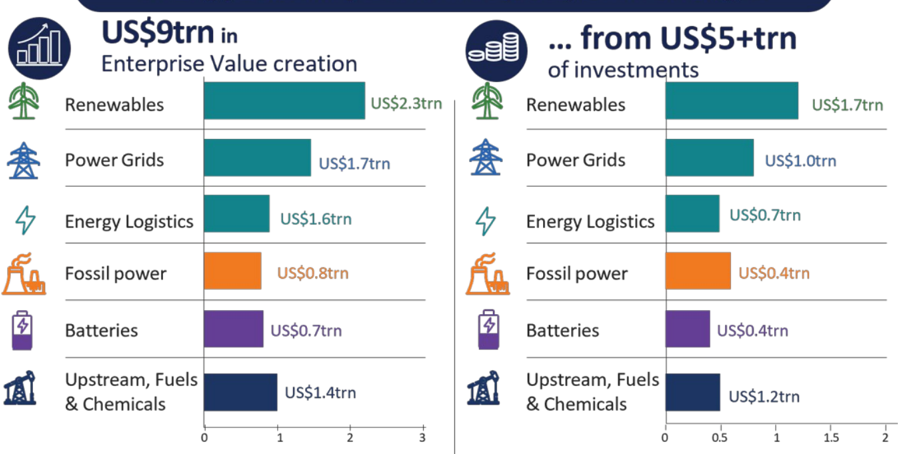

Energy shocks have become more frequent making energy and economic security critical in an AI world. US$5 trillion-plus investment needs should kick-start a golden age in dependable energy investments to secure AI, food and tech supply chains after a decade of underinvestment. An investment supercycle unlocking US$9 trillion in value beckons.

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

- = Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to NASD/NYSE restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

M

Contributors

Morgan Stanley Asia (Singapore) Pte.+ Mayank Maheshwari Equity Analyst +65 6834-6719

Mayank.Maheshwari@morganstanley.com

Morgan Stanley & Co. International plc+ Martijn Rats, CFA Equity Analyst and Commodities Strategist +44 20 7425-6618 Martijn.Rats@morganstanley.com

Morgan Stanley Asia Limited+

Eva Hou Equity Analyst +852 2848-6964 Eva.Hou@morganstanley.com

Morgan Stanley India Company Private Limited+ Pranitha Shetty Research Associate +91 22 6118-3022 Pranitha.Shetty@morganstanley.com

Morgan Stanley & Co. International plc, Seoul Branch+ Young Suk Shin Equity Analyst +82 2 399-4994 Young.Shin@morganstanley.com

Morgan Stanley India Company Private Limited+ Girish Achhipalia Equity Analyst +91 22 6118-1124 Girish.Achhipalia@morganstanley.com

Morgan Stanley & Co. LLC Joe Laetsch, CFA Equity Analyst +1 212 761-8804 Joe.Laetsch@morganstanley.com

Morgan Stanley MUFG Securities Co., Ltd.+ Takeshi Kitaura Equity Analyst +81 3 6836-5427

Takeshi.Kitaura@morganstanleymufg.com

Morgan Stanley Asia (Singapore) Pte.+

Derrick Y Kam

Asia Economist

+65 6834-8272

Derrick.Kam@morganstanley.com

Morgan Stanley & Co. International plc+ Amy Gower (Amy Sergeant), CFA Commodities Strategist +44 20 7677-6937 Amy.Gower1@morganstanley.com

Morgan Stanley Asia Limited+ Jack Lu Equity Analyst +852 2848-5044 Jack.Lu@morganstanley.com

Morgan Stanley & Co. LLC Devin McDermott Equity Analyst and Commodities Strategist +1 212 761-1125 Devin.McDermott@morganstanley.com

Morgan Stanley Asia (Singapore) Pte.+ Vivek Rajamani Equity Analyst +65 6834-6740 Vivek.Rajamani@morganstanley.com

Morgan Stanley India Company Private Limited+ Hinal Choudhary Research Associate +91 22 6118-2044 Hinal.Choudhary@morganstanley.com

Morgan Stanley MUFG Securities Co., Ltd.+ Reiji Ogino Equity Analyst +81 3 6836-8930

Reiji.Ogino@morganstanleymufg.com

Morgan Stanley Asia Limited+

Sheng Zhong

Equity Analyst

+852 2239-7821

Sheng.Zhong@morganstanley.com

Morgan Stanley & Co. LLC Angel Castillo Equity Analyst +1 212 761-1931 Angel.Castillo@morganstanley.com

Morgan Stanley & Co. International plc, Seoul Branch+ Joon Seok Equity Analyst +82 2 399-4934

Joon.Seok@morganstanley.com

Morgan Stanley India Company Private Limited+

Binay Singh

Equity Analyst

+91 22 6118-1158

Binay.Singh@morganstanley.com

Morgan Stanley & Co. International plc+ Alain Gabriel, CFA Equity Analyst +44 20 7425-8959

Alain.Gabriel@MorganStanley.com

Morgan Stanley & Co. LLC Stephen C Byrd Equity Analyst +1 212 761-3865 Stephen.Byrd@morganstanley.com

Morgan Stanley Asia Limited+ Chetan Ahya Chief Asia Economist +852 2239-7812 Chetan.Ahya@morganstanley.com

Morgan Stanley Asia (Singapore) Pte.+ Ryan M Heng Research Associate +65 6834-6465 Ryan.Heng@morganstanley.com

Morgan Stanley Australia Limited+ Rob Koh Equity Analyst +61 3 9256-8932 Rob.Koh@morganstanley.com

Morgan Stanley Australia Limited+

Samantha R Edie

Equity Analyst

+61 2 9770-1671

Samantha.Edie@morganstanley.com

Morgan Stanley Asia Limited+ Qianlei Fan, CFA Equity Analyst +852 2239-1875 Qianlei.Fan@morganstanley.com

Morgan Stanley MUFG Securities Co., Ltd.+ Yu Shirakawa Equity Analyst +81 3 6836-5432

Yu.Shirakawa@morganstanleymufg.com

Morgan Stanley Asia (Singapore) Pte.+ Daniel K Blake Equity Strategist +65 6834-6597

Daniel.Blake@morganstanley.com

Morgan Stanley & Co. International plc+ Guilherme Levy Equity Analyst +44 20 7425-6616

Guilherme.Levy@morganstanley.com

Morgan Stanley & Co. International plc+

Charlotte Firkins

Commodities Strategist

+44 20 7425-3866

Charlotte.Firkins@morganstanley.com

M

Morgan Stanley Asia Limited+ Tim Hsiao Equity Analyst +852 2848-1982 Tim.Hsiao@morganstanley.com

Morgan Stanley Asia Limited+ Yiyi Wang Research Associate +852 3963-4169 Yiyi.Wang@morganstanley.com

Morgan Stanley Australia Limited+ Rahul Anand, CFA Equity Analyst +61 2 9770-1136 R.Anand@morganstanley.com

Morgan Stanley & Co. LLC Stefan Diaz, CFA Equity Analyst +1 212 761-1834 Stefan.Diaz@morganstanley.com

Morgan Stanley & Co. International plc, Seoul Branch+ Chan Park Research Associate +82 2 399-9920 Chan.Park1@morganstanley.com

Morgan Stanley & Co. LLC Jacqueline M Kenny Research Associate +1 212 761-2253 Jacqueline.Kenny@morganstanley.com

Morgan Stanley India Company Private Limited+ Rahul Gupta Equity Analyst +91 22 6118-2233 Rahul.Gupta1@morganstanley.com

Morgan Stanley Asia Limited+ Kaylee Xu Equity Analyst +852 2239-1506

Morgan Stanley Asia Limited+ Chelsea Wang Equity Analyst +852 2239-1118 Jinlin.Wang@morganstanley.com

Kaylee.Xu@morganstanley.com

Morgan Stanley Asia Limited+ Rachel L Zhang Equity Analyst +852 2239-1520 Rachel.Zhang@morganstanley.com

Morgan Stanley Asia (Singapore) Pte.+ Kristal Ji Equity Strategist +65 6834-6949 Kristal.Ji@morganstanley.com

Morgan Stanley Asia Limited+ Lisa Jiang Equity Analyst +852 2239-1282 Lisa.Jiang1@morganstanley.com

M

Contents

- 7 Energy Supercycle in Numbers

- 8 US$9trn Energy Value Creation: Who Benefits?

- 11 Calculating the Investment and Value Creation

- 13 Investment Case

- 19 Securing Energy: The Nuts, Bolts and Challenges

- 24 The Supply Chain Paradox: A Solution to Energy Independence

- 28 Energy Security Beneficiaries in Multipolar World

- 32 US$9 trillion of Value Creation: Learnings from Power's Re-rating

- 36 Asia's Competitive Reinvention of Energy Security - A Strategy Perspective

- 40 US Energy = Asia's Supply Chain Diversification

- 45 China: Fortifying Defences, Supporting Asia's Energy Security

- 49 Energy Security - A Key Pillar to Capex and Industrial Supercycle

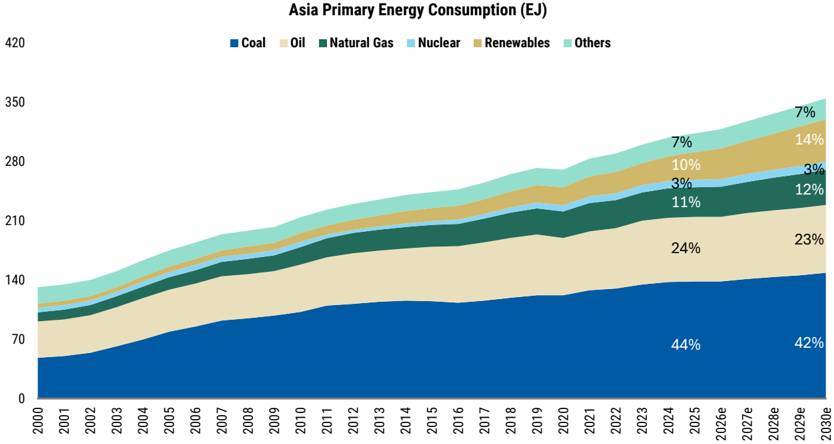

- 51 Energy: Consumption Keeps Growing

- 53 Power Consumption: The Supercycle Accelerates policy maker

- 62 Power: Security in Diversity

- 68 Power: Key Beneficiaries

- 69 Coal Returns: A Key Pillar of Security and Growth

- 76 Coal: Key Beneficiaries across the value chain

- 77 Power Grids: Unlocking the Gridlock

- 85 Power Grids: Key Beneficiaries of Asia's US$1trn Investment

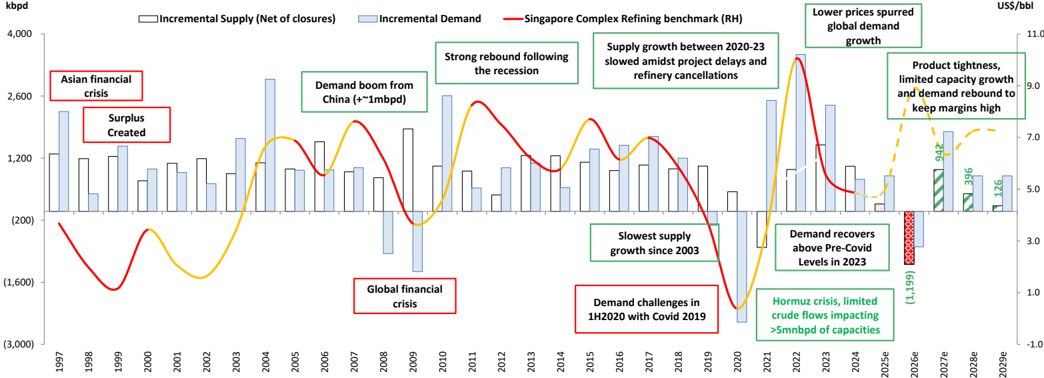

- 86 Renewables: Pacing the Growth

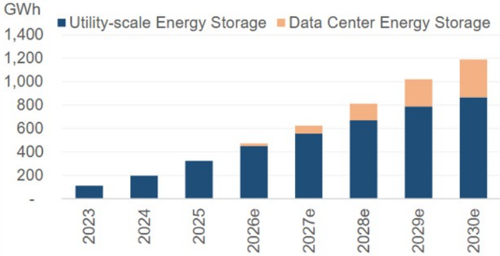

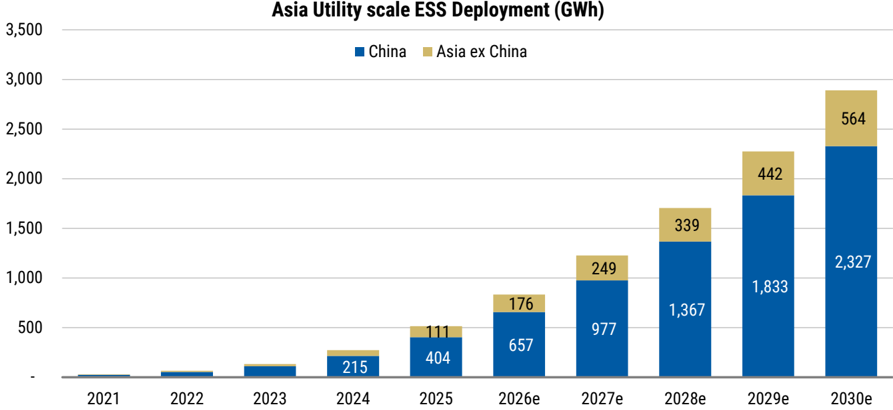

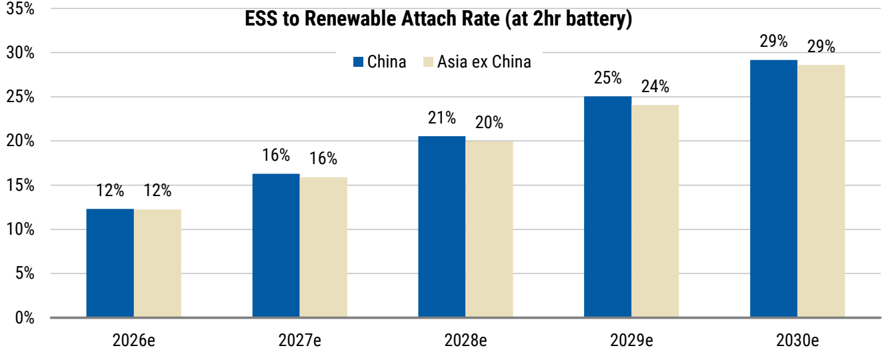

- 90 Energy Storage: Enabling Security

- 96 Renewables and Batteries: Key Potential Beneficiaries of the US$2trn Investment

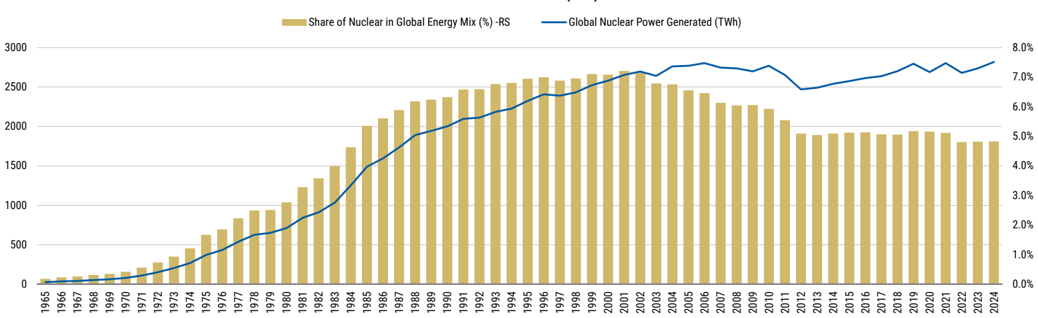

- 97 Nuclear: The Long-Term Solution

- 100 Nuclear: Key Beneficiaries

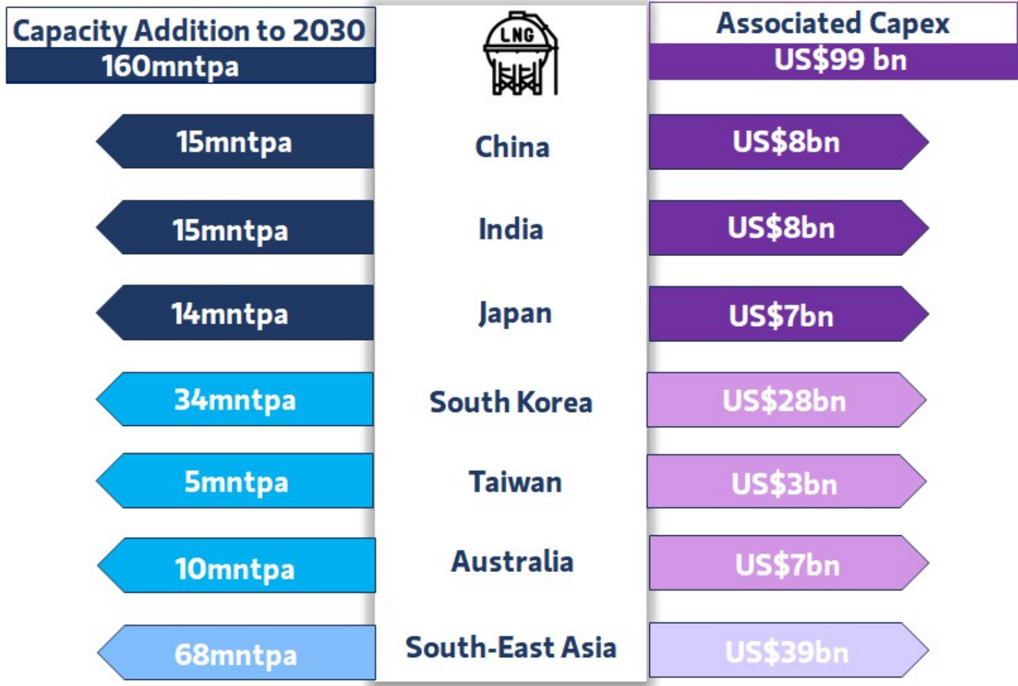

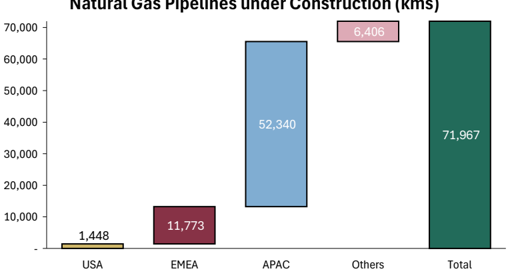

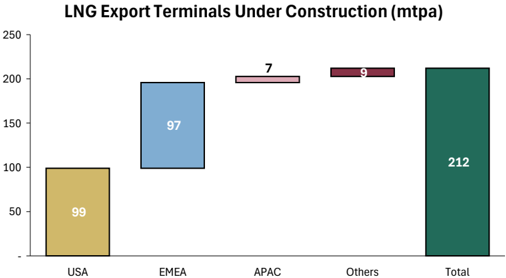

- 101 Natural Gas: The Next Dependable Fuel Supporting Coal and Renewables

- 105 Natural Gas: Key Beneficiaries

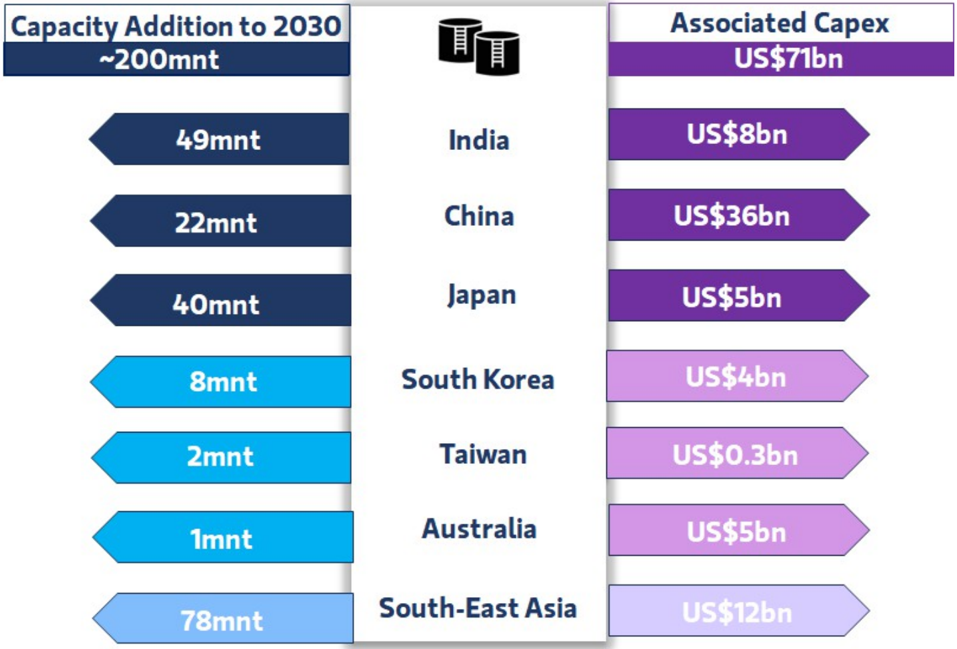

- 106 Fuel: A New Refinery Needed Every Year

- 112 Fuels: Key Beneficiaries

- 113 Strategic Reserves: A Multi-Year Capex Cycle

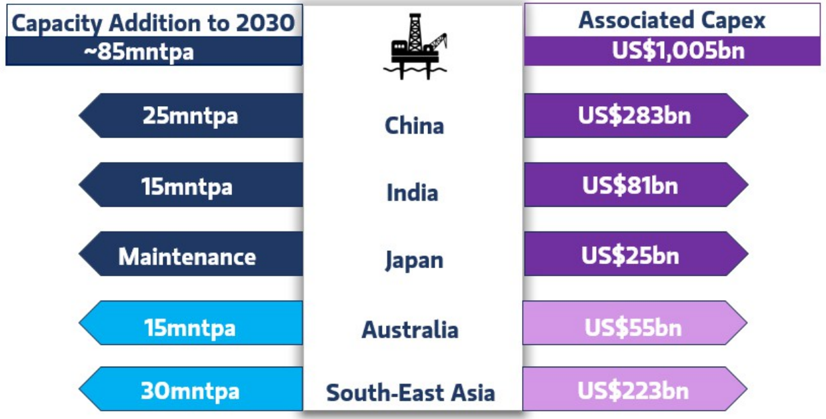

- 116 Upstream: Back in Vogue

- 124 Upstream Energy: Beneficiaries of Higher Oil and Natural Gas Production

- 125 Energy Services and Logistics

- 130 Oil Services, Equipment & Logistics: Key Beneficiaries

- 131 Chemicals: Security Needs Underappreciated

- 137 Fertilizers - Food Security in Focus

- 141 Chemicals and Fertilizers: Key Beneficiaries

- 142 Appendix: Equities to Play Powering AI & The Changing Face of Power Markets

M

Energy Meets Compute: Supercycle Recharges

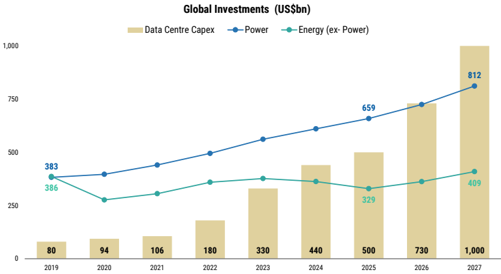

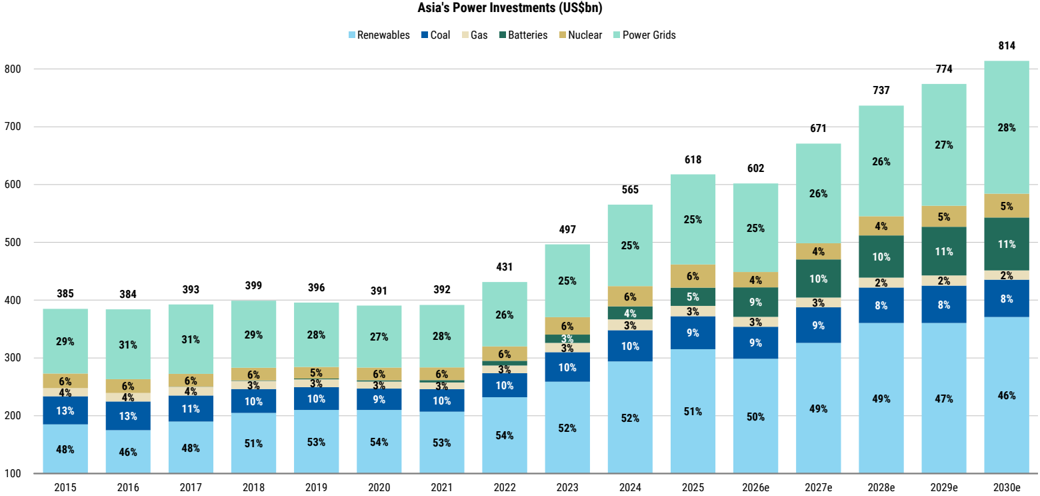

Asia's energy capex will nearly double through the end of the decade.

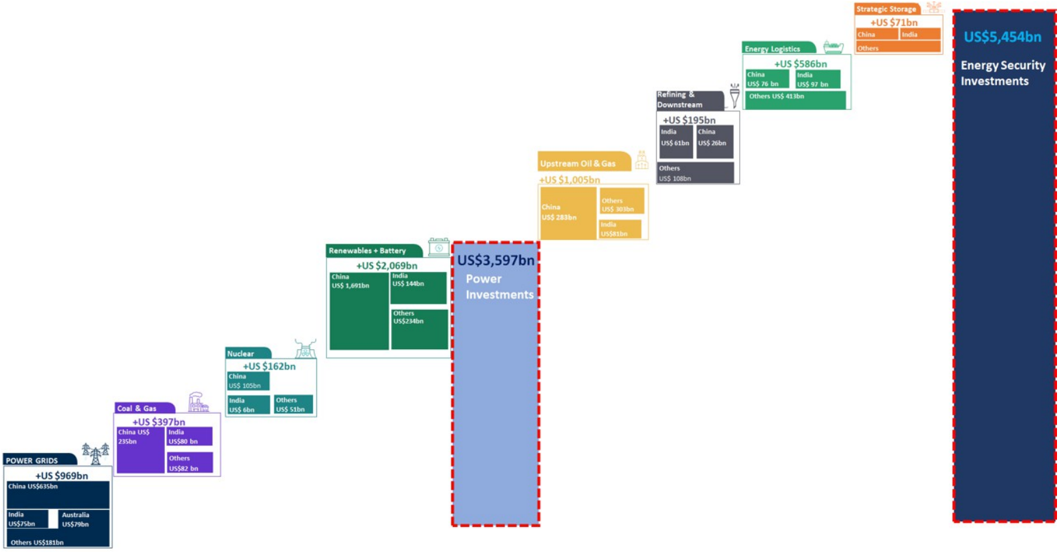

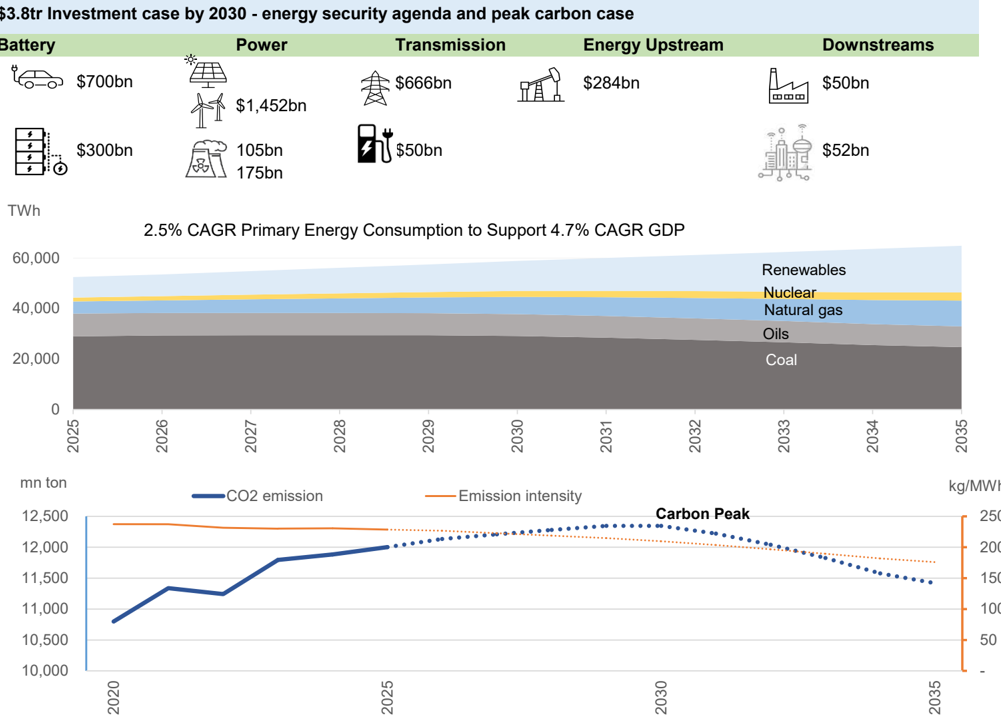

By 2030, over US$1.2 trillion in new investments will be needed to reduce Asia's import dependence by 100bps based on expected consumption growth. This is in addition to US$4.3trn of investments currently in progress and implies annual capital deployment growth of 11% through 2030 vs. 2% in the past decade. Many themes will provide durable alpha, in our view: powering AI, coal's comeback, a biofuel inflection, a golden age of fuel refining and shipbuilding, heavy equipment capacity expansion, organic chemicals and fertilizer investments, and energy storage deployment. We estimate US$9trn of value creation potential as energy consumption grows faster than expected on rising AI adoption, making multiples re-rate with tighter energy markets and given the need for higher returns to attract investments.

Industry View

India Oil & Gas | Asia Pacific In-Line

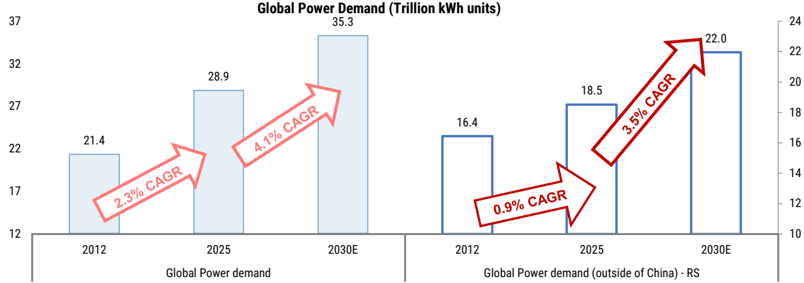

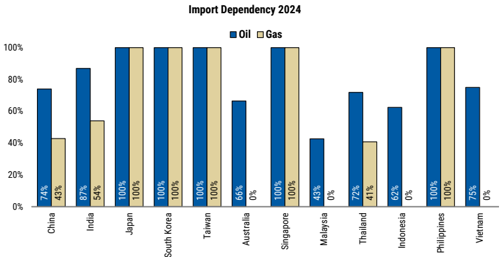

Energy security a must-have for all. Energy is the lifeblood of modern economies and security is critical to the future of energy, as there is no energy transition or AI without security. Asia consumes as much energy as rest of the world combined but only produces a third of it at home, making dependable energy investments essential as cross-border energy flows become more fragile and less reliable. Asia's energy investments have been stagnant, but consumption has risen 50% in the past decade, even as investments in traditional energy supply chains fell to their lowest levels ever and are now below data center investments, which need energy to power them. The lopsided investment profile should rebalance in the coming years as energy access and affordability become increasingly critical to the security of power, compute, food, technology, and metal supply chains in Asia.

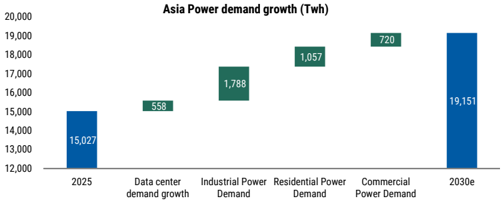

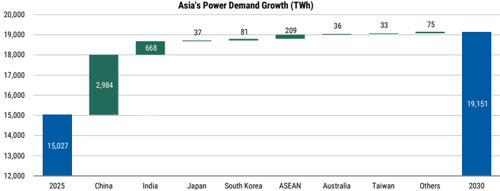

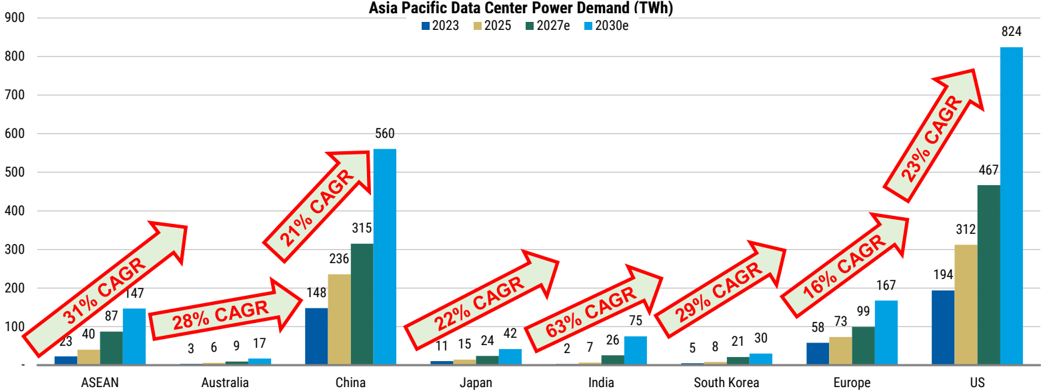

Asia's energy demand for compute and AI is accelerating at a pace comparable with the United States, with projections indicating that by 2030 data centers will consume roughly one-sixth of all new power units in the region. This surge will not be limited to electricity; it will also drive up requirements for essential fuels and raw materials, such as coal, copper, aluminium, diesel, and other commodities across Asia. As policy makers work to overhaul and strengthen supply chains to safeguard and support AI development, reliable energy investments are receiving a critical boost, positioning the region to meet the challenges of an increasingly digital and interconnected future.

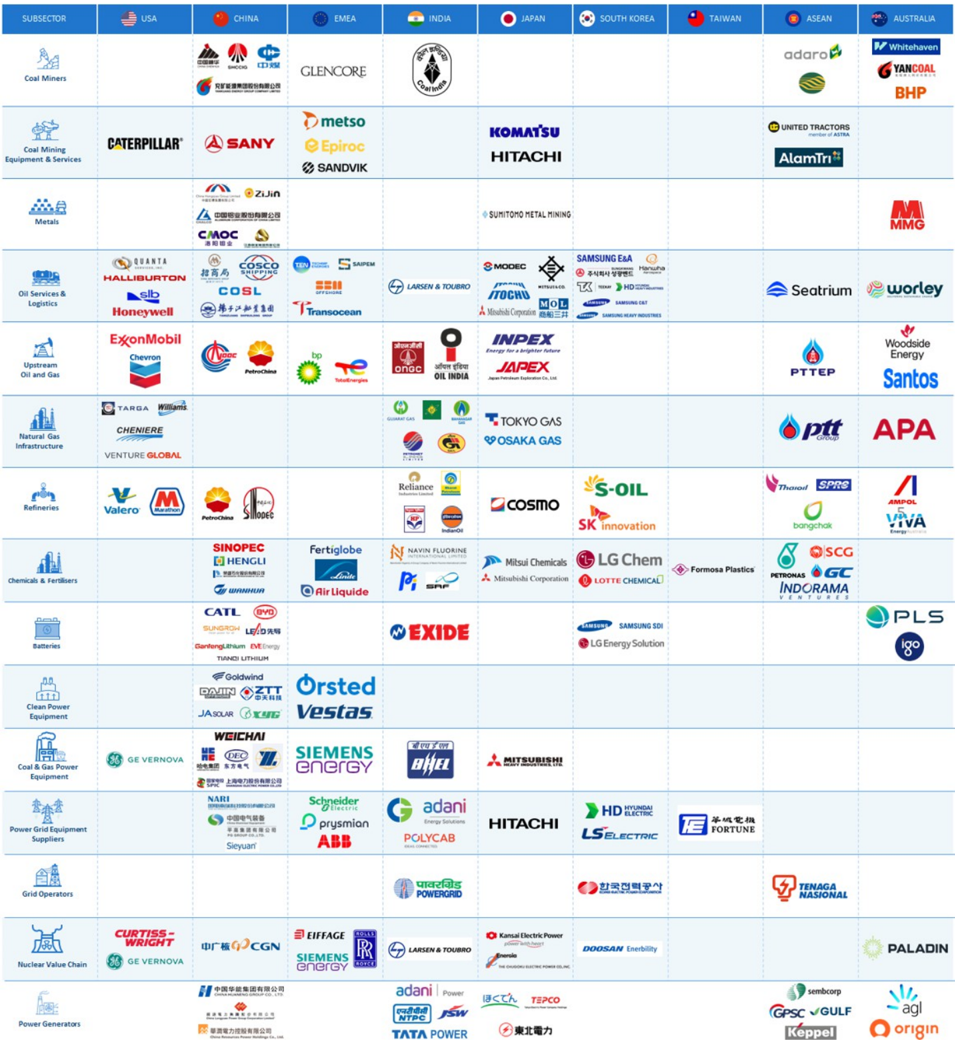

Energy spans sectors, and securing energy for Asia has global implications for equities from copper to commodity traders, fuel refiners, fertilizers, and even shipyards ( Exhibit 23 ). Recent events show that while energy markets may be global, oil insecurity is always local.This makes energy security the top priority in a world where energy demand will only rise. Below we present our key forecasts for 2030 that are not currently expected by the market:

- Asia's average annual energy investments to double by 2030 ( Exhibit 11 ) and become the second-largest area of spending after AI. We expect power, including coal, to take up more than two-thirds of the investment share, followed by fuel, energy storage and natural gas. The 'Powering AI' theme will drive a new investment cycle in energy systems, particularly storage, coal plants and grid flexibility, as exponential AI infrastructure growth collides with physical-world limitations.

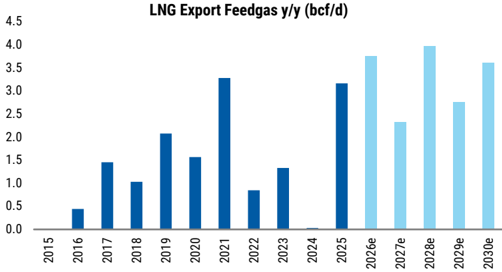

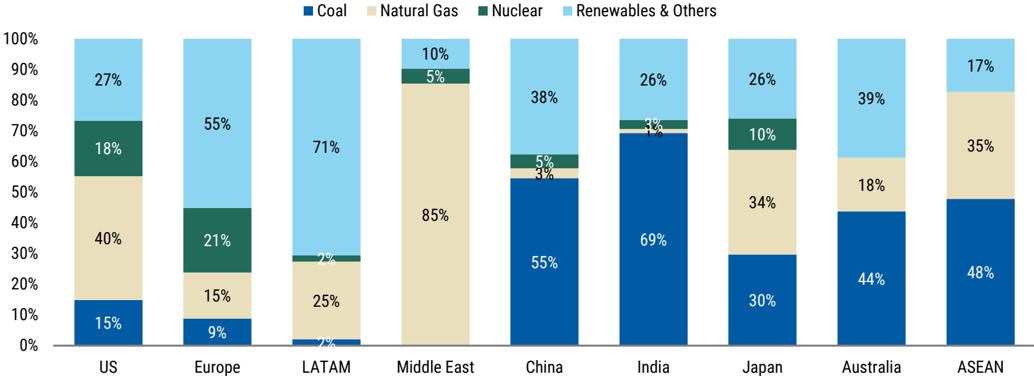

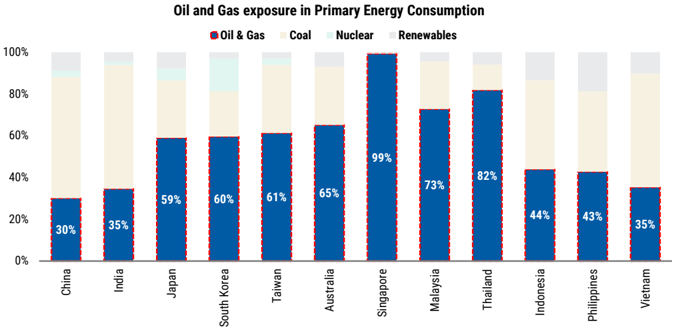

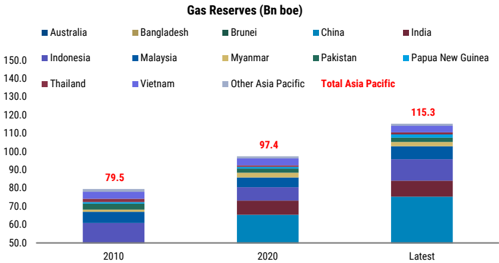

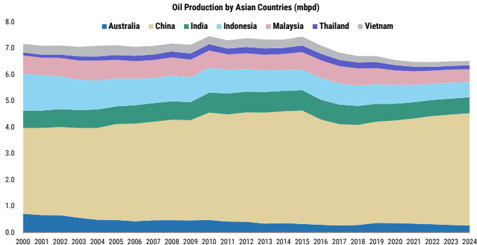

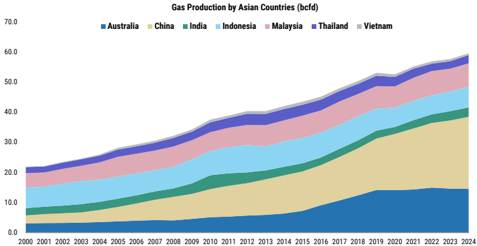

- The return of coal to secure AI's need for energy , and an inflection in natural gas adoption with new infrastructure investments and fuel refinery investments making a comeback. Asia holds massive coal reserves, estimated at nearly three-fifths of the world's total, which should help slow LNG import needs ( Exhibit 19 ).

- Diversification of energy sourcing to the US, LatAm and internally within Asia for natural gas and coal; shipbuilding and investments in new tankers rise to cycle highs after a decade of underinvestment.

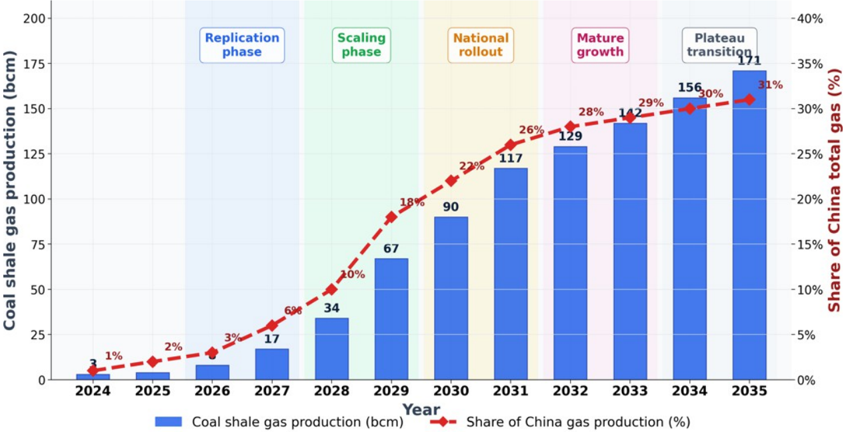

- Oil and gas exploration picking up steam, and coal gasification capacity builds double: Shale mining in China, deepwater finds in India/Southeast Asia, and new coal gasification projectsto leverage Asia's vast coal resource base reduce Asia's import dependence on natural gas and fertilizers.

- Energy storage expands rapidly, even in markets outside of China; Rise of biofuels to double in Asia's energy mix: Energy storage becomes a necessity in grid-level renewable

M

deployment with innovative technologies like sodium ion in energy storage gaining traction.

- Accelerated nuclear power, fertilizer and power grid deployment as combating power shortages becomes even more critical. Data centers cross-subsidise households, with tiered power pricing keeping prices affordable.

- Corporate balance sheets can support about 75% of the investments , as many are net cash and can increasingly focus on domestic allocation of growth capital. Governments may chip in more aggressively for the remaining 25% of capital needs with policies that kick-start and accelerate investments, and keep energy prices affordable.

Buy dependable energy security beneficiaries as AI pushes Asia into a US$5.5trn capex cycle: We recommend owning energy security assets, as the thematic is inextricably tied to AI, and highlight 70 global equities across the coal equipment supply chain, fuel refiners, petrochemical producers, and natural gas exporters that we expect to benefit the most globally.Areas where we think earnings and dividends could surprise the most in Asia ( Exhibit 24 ) are: 1) fossil- and nuclear-based power generators; 2) the energy storage supply chain, including power grids; and 3) fertilizers. Our shortlist of 7 global equities that should benefit the most: Mitsui & Co, Venture Global, CATL, Keppel Corp, Kansai Electric, Cummins, and Doosan Enerbility.

Exmoll. chergy securly allu rowelly al. A oupelcycle neullalyes A ollapollut by <uou

M

... from US$5+trn

Energy Supercycle in Numbers

Exhibit 1: Energy Security and Powering AI: A Supercycle Recharges - A Snapshot by 2030

Energy Logistics

US$1.7trn

US$1.0trn

US$1.6trn Energy Logistics US$0.7trn

4

China

US$3,089bn

US$552bn US$116bn US$128bn

Benefiting these subsectors

Equipment

Suppliers

(Coal Mining, Power Generation

Equipment, Grid

Equipment, Refining

Equipment)

Source: Morgan Stanley Research estimates

Oil Services &

logistics (Rig operators,

offshore energy, tankers)

Power

(Thermal

power generators,

Grid

Operators)

Downstream

Infrastructure

energy (refiners,

chemicals, fertilizers)

Operators (LNG terminals,

Gas pipeline

Operators)

ullallylly race ul rowel Mainels

M

T TOKYO GAS

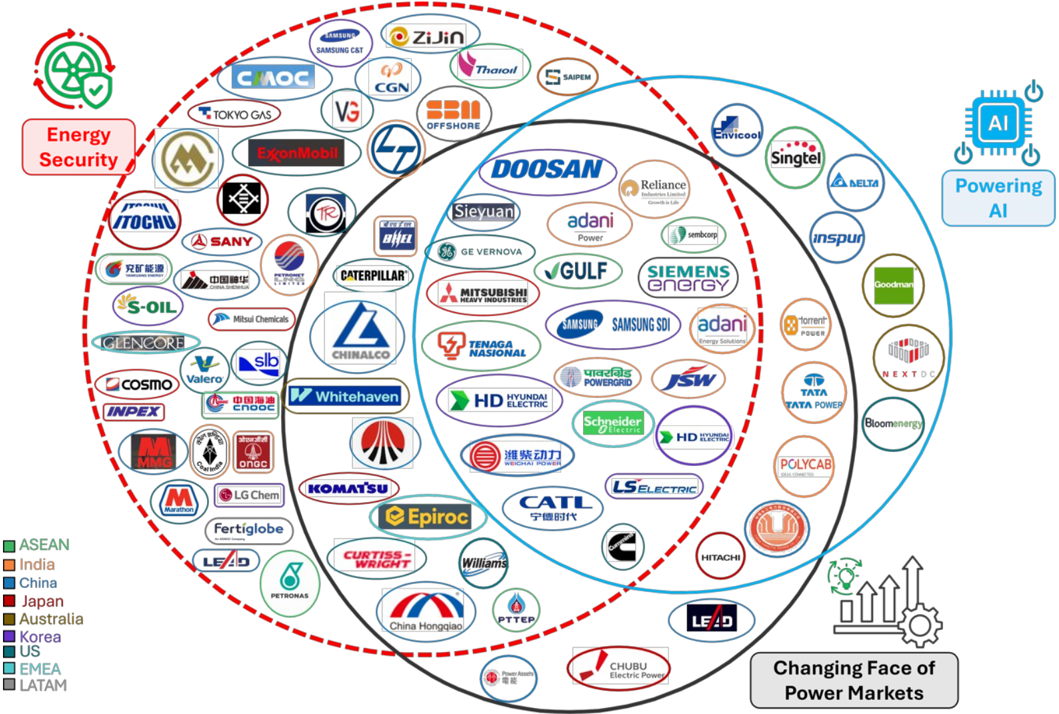

US$9trn Energy Value Creation: Who Benefits?

Reliance

Powering

Exhibit 2: Our preferred 70 equities that should benefit as Energy Security intersects with our global thematics of Powering AI and the Changing Face of Power Markets BHEL Power sembcorp GE VERNOVA inspur)

• ASEAN

India

China

Japan

Australia

Korea

US

EMEA

LATAM

Source: Morgan Stanley Research

The ouvelcycles value uleatlull. A vogyull value ulcatull rulellulal

M

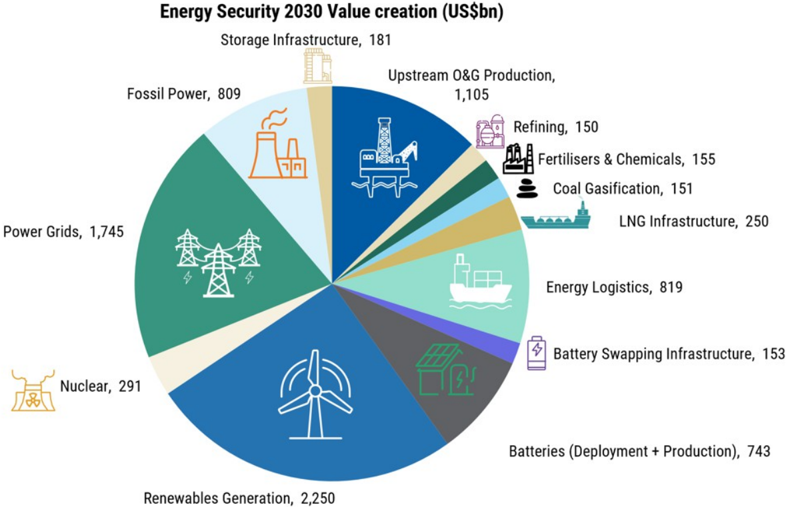

Upstream 0&G Production,

1,105

Exhibit 3: The Supercycle's Value Creation: A US$9trn Value Creation Potential

Power Grids, 1,745

Сашал лемАЙ САпІЛ ПАЛАЛРАЙ САРІМА-АА

Refining, 150

Source: Morgan Stanley Research Estimates

CAIIDIL 4.

SUBSECTOR

CHINA

I EMEA

INDIA

JAPAN

M

ASEAN

adarod

Exhibit 4: Global Exposure to Asia's Energy Security as Compute's Need for Energy Inflects

Coal Mining

Equipment & Services

Metals

Oil Services &

Logistics

Upstream

Oil and Gas

Natural Gas

Infrastructure

Refineries

Chemicals & Fertilisers

Waltere

Clean Power

Equipment

Coal & Gas Power

Equipment

Power Grid Equipment

Suppliers

Grid Operators

Nuclear Value Chain

Power Generatorsl

Source: Company data, Morgan Stanley Research

SOUTH KOREA

TAIWAN

AUSTRALIA

W Whitehaven

YANCOAL

BHP

POWER GRIDS

+US $969bn

China US$635bn

India

USS75bn

Others US$181bn

Strategic Storage

+US $71bn

M Calculating the Investment and Value Creation

US$ 61bn

US$ 26bn

Exhibit 5: The US$5tn+ investment supercycle: Dependable energy investments will nearly double vs. the last decade while renewables should plateau after five years of significant growth Others China

US$ 283bnl

Source: Company data, Morgan Stanley Research (e) estimates

Exhibit 6: What's driving the US$5+ trillion supercycle?

Source: Morgan Stanley Research estimates; We include capital work in progress investments in our estimates above for all countries vullals univinly thie

Enersy Logistics

+US $586bn

China

India

US$5,454bn

Energy Security

Investments

M

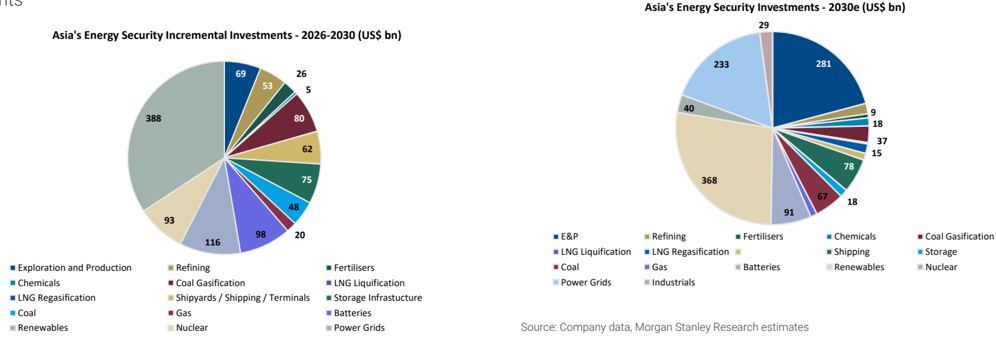

Exhibit 7: How the US$5trn+ investment unlocks a US$9trn value creation potential

| Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Value Creation (US$ bn) | Value Creation (US$ bn) | Value Creation (US$ bn) | Value Creation (US$ bn) |

|---|---|---|---|---|---|---|

| Category | Sub-Category | Total | Return on Capital employed | EBITDA | EV/EBITDA Multiple | Enterprise Value |

| Upstream | Exploration and Production | 1,005 | 17% | 221 | 5.0 | 1,105 |

| Refining | 94 | 15% | 19 | 8.0 | 150 | |

| Fertilisers | 37 | 12% | 6 | 8.0 | 51 | |

| Chemicals | 64 | 13% | 12 | 9.0 | 104 | |

| Coal Gasification | 98 | 17% | 22 | 7.0 | 151 | |

| Mid Stream | LNG Liquification | 12 | 16% | 3 | 12.0 | 31 |

| LNG Regasification | 87 | 16% | 18 | 12.0 | 219 | |

| Energy Logistics | 310 | 20% | 78 | 10.0 | 775 | |

| Pipelines | 17 | 12% | 3 | 15.0 | 44 | |

| Battery Swapping Infrastructure | 61 | 20% | 15 | 10.0 | 153 | |

| STORAGE | Storage Infrastucture | 71 | 12% | 12 | 15.0 | 181 |

| Oil/Fuels | 61 | |||||

| INFRASTRUCTURE | Natural Gas | 8.1 | ||||

| Fertilizers | 1.8 | |||||

| Power | Coal | 318 | 12% | 54 | 12.0 | 649 |

| Gas | 79 | 12% | 13 | 12.0 | 160 | |

| Batteries (Deployment + Production) | 364 | 12% | 62 | 12.0 | 743 | |

| Renewables Generation | 1,705 | 7% | 205 | 11.0 | 2,250 | |

| Nuclear | 162 | 10% | 24 | 12.0 | 291 | |

| Power Grids | 969 | 10% | 145 | 12.0 | 1,745 | |

| Total | 5,454 | 911 | 8,803 |

Source: Morgan Stanley Research

M

Investment Case

A US$5trn+ Supercycle

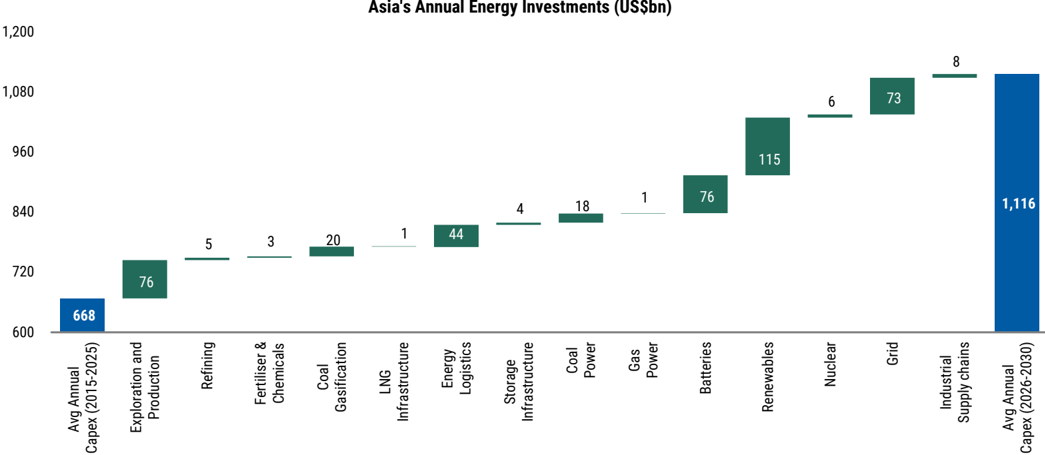

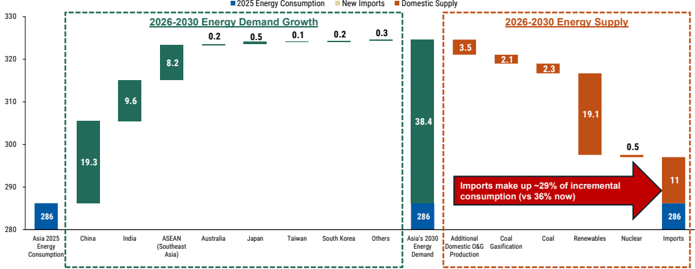

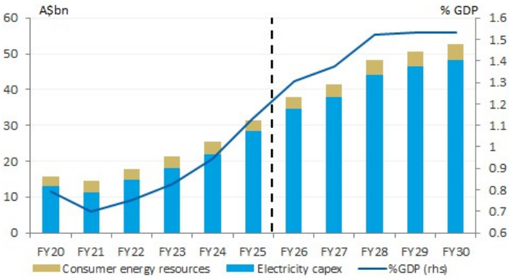

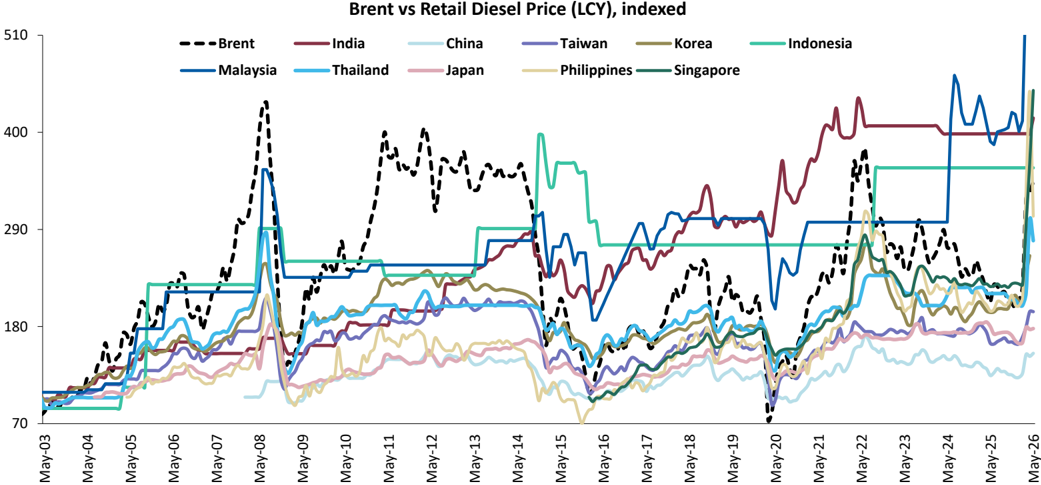

Energy markets may be global but energy insecurity is always local, with all major economies now focused on the same issue (see Exhibit 10 ). Given that Asia imports roughly 36% of its energy, we see the need for US$5.5 trillion of energy investments over the next five years, which would cut import dependence by nearly a fifth ( Exhibit 12 ). This would also need US$1.2 trillion of new investments to help increase Asia's energy self dependence 100bps on average in Asia by 2030. While we believe Asia will never be fully energy independent, it can reduce its dependence on single-supply sources and diversify its energy needs, both in terms of importing nations and fuel type. We believe spending growth will focus on fossil fuels and dependable energy sources - attracting 2x more annual spend than in the recent past. Renewables may see a plateau in spending after more than doubling over the past decade, as power grids will need to improve with ~US$1 trillion of new investments before the adoption curve for renewables inflects further.

Powering AI is increasingly grabbing policy attention as bottlenecks of energy supply to data centers become more critical and accelerate the need for coal, diesel and natural gas across economies. In an increasingly power-constrained world, AI workloads are structurally changing the shape of electricity demand across Asia. Hence, AI is forcing a greater need for dependable energy, and we believe domestic power and fuel production, and diversification of energy sourcing is becoming more critical for policy makers as AI adoption picks up. Natural gas and coal will help meet Asia's need for dependable power, and as the US shale revolution expands to Asia, it should reshape Asia's energy consumption landscape, solving grid bottlenecks and shortages in energy systems by 2030.

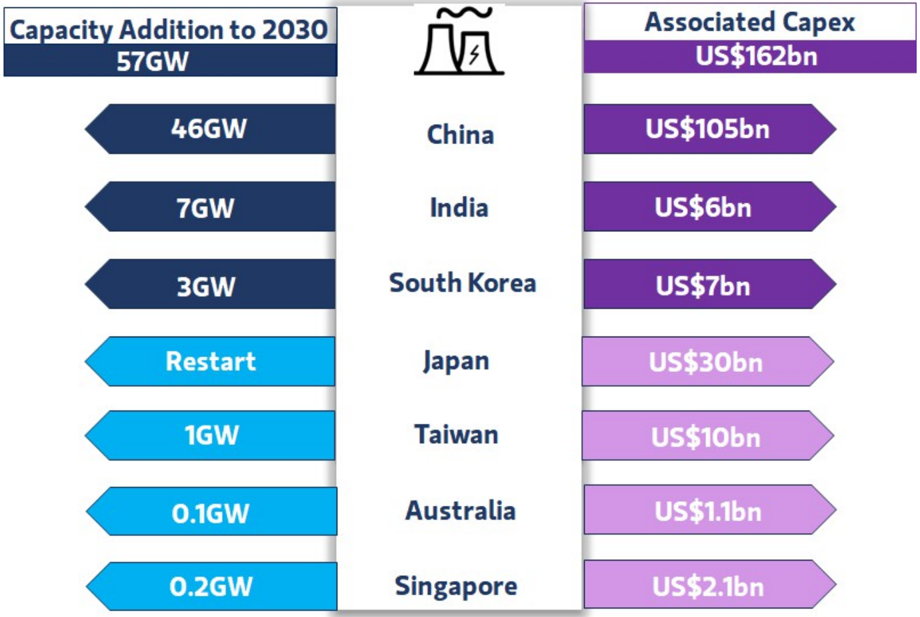

We estimate that Asia's energy consumption will rise by 38 exajoules (EJ) by 2030 ( Exhibit 12 ) - as much as the whole of the Middle East currently consumes, and that about two-thirds of this will be met with domestic sources - renewables, coal, and domestic natural gas; the rest will need to be imported. Import dependence varies greatly by economy, but even excluding China we estimate Asia will consume roughly 20EJ more energy by 2030, with domestic production satisfying about half of this. Energy security is no longer just a talking point for policy makers: Japan has highlighted the need to secure domestic energy supplies and is making strategic investments in shipbuilding and fusion energy; Southeast Asian nations have highlighted energy security as critical; China is focusing on improving "energy resource security guarantee levels"; and India is increasingly looking to diversify its sources of energy imports, and use technologies such as coal gasification and biofuels to reduce import dependence.

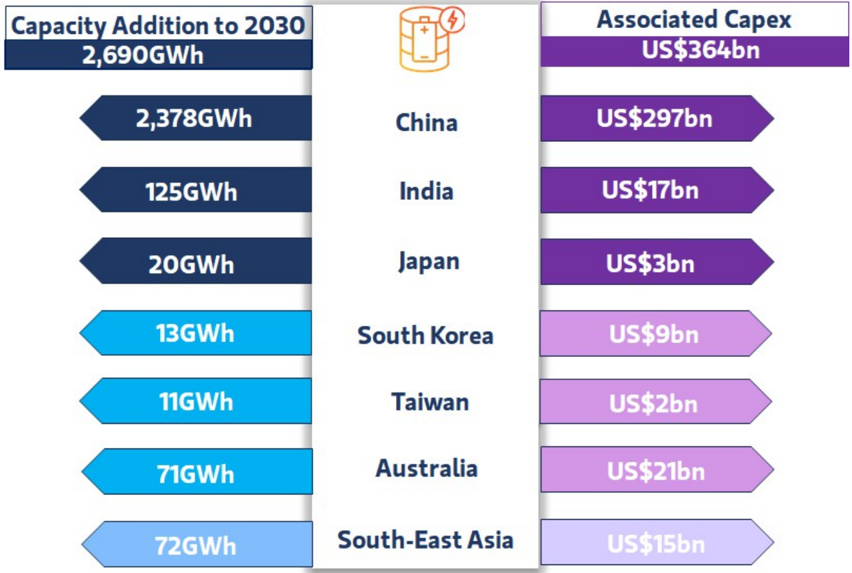

Exhibit 8: Energy Security: Investments to translate into a significant uplift in manufacturing capacity across power generation, storage infrastructure and downstream chemicals

| Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e | Additional Capacity over 2026-2030e |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Category | Sub-Category | China | India | Japan | South Korea | Taiwan | Australia | Singapore | Malaysia | Thailand | Indonesia | Philippines | Vietnam | Total |

| UPSTREAM | Exploration and Production (mntpa) | 25 | 15 | - | - | - | 15 | - | 10 | 5 | 13 | - | 2 | 85 |

| Refining (mntpa) | 10 | 40 | - | - | - | - | - | - | 10 | 22 | 17 | 17 | 117 | |

| Fertilisers (mntpa) | 4 | 7 | - | - | - | 2 | - | 2 | - | 4 | 2 | 2 | 23 | |

| Chemicals (mntpa) | 5 | 15 | - | 2 | - | - | - | - | - | 5 | - | 5 | 32 | |

| Coal Gasification (mnt) | 20 | 100 | 10 | 130 | ||||||||||

| MID STREAM | LNG Liquification (mntpa) | - | - | - | - | - | 5 | - | 3 | 5 | - | - | 12 | |

| MID STREAM | LNG Regasification (mntpa) | 15 | 15 | 14 | 34 | 5 | 5 | 10 | 10 | 10 | 15 | 15 | 148 | |

| MID STREAM | Energy Logistics | - | - | - | - | - | - | - | - | - | - | - | - | 502 |

| Pipelines (kms) | 2,500 | 4,000 | 300 | 638 | 300 | 335 | - | 1,000 | 2,000 | 2,000 | 1,000 | 2,000 | 16,073 | |

| Battery Swapping Infrastructure | - | |||||||||||||

| Storage Infrastucture | 22 | 49 | 40 | 8 | 2 | 1 | 6 | 8 | 17 | 21 | 5 | 22 | 200 | |

| STORAGE | Oil/Fuels (mn bbl) | 164 | 337 | 291 | 40 | 16 | 6 | 45 | 56 | 113 | 147 | 34 | 145 | 1,395 |

| INFRASTRUCTURE | Natural Gas (mtoe) | - | 1.0 | - | 2.3 | - | - | - | - | 1.4 | - | - | 1.7 | 6.3 |

| Fertilizers (mnt) | - | 1.8 | - | - | - | 0.5 | - | - | - | 0.7 | - | - | 3.1 | |

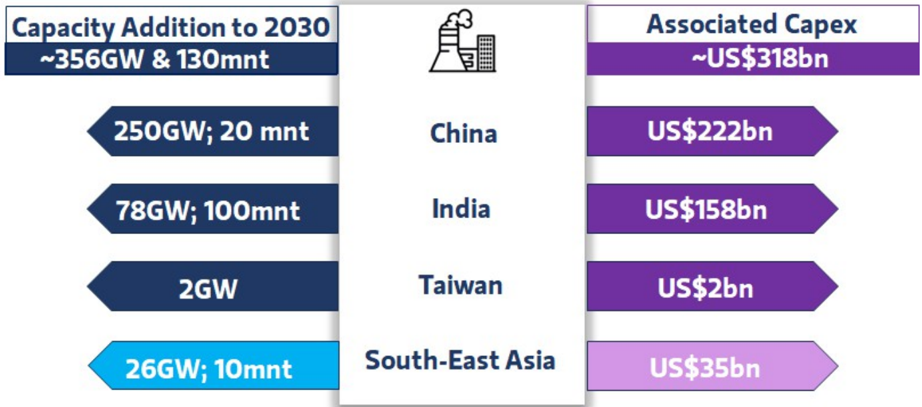

| Coal (GW) | 250 | 78 | - | - | 2 | - | - | 3 | 4 | 13 | 4 | 3 | 356 | |

| Gas (GW) | 50 | - | 5 | 12 | 4 | 2 | 4 | 2 | 2 | 1 | 2 | 3 | 86 | |

| POWER | Batteries (GWh) | 2,378 | 125 | 20 | 13 | 11 | 71 | 2 | 10 | 15 | 15 | 7 | 23 | 2,690 |

| Renewables (GW) | 1,675 | 183 | 25 | 39 | 14 | 45 | 1 | 5 | 10 | 17 | 7 | 6 | 2,026 | |

| Nuclear (GW) | 46 | 7 | - | 3 | 1 | 0.1 | 0.2 | - | - | - | - | - | 57 |

Source: Morgan Stanley Research estimates

M

Exhibit 9: Energy Security: What we think Asia's economies will spend

| Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) | Associated Investments (US$ bn) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Category | Sub-Category | China | India | Japan | South Korea | Taiwan | Australia | Singapore | Malaysia | Thailand | Indonesia | Philippines | Vietnam | Total |

| Upstream | Exploration and Production | 283 | 81 | 25 | 55 | 71 | 40 | 86 | 6 | 20 | 1,005 | |||

| Refining | 8 | 32 | - | - | - | - | - | - | 8 | 18 | 14 | 14 | 94 | |

| Fertilisers | 5 | 11 | - | - | - | 5 | - | 3 | - | 6 | 5 | 3 | 37 | |

| Chemicals | 13 | 18 | - | 7 | - | - | - | - | - | 13 | - | 13 | 64 | |

| Coal Gasification | 14 | 78 | - | 7 | 98 | |||||||||

| Mid Stream | LNG Liquification | - | - | - | - | - | 5 | - | 3 | - | 5 | - | - | 12 |

| LNG Regasification | 8 | 8 | 7 | 28 | 3 | 2 | 5 | - | 5 | 5 | 8 | 8 | 87 | |

| Energy Logistics | 4 | 2 | 4 | 2 | 4 | 310 | ||||||||

| Pipelines | 3 | 4 | 0 | 1 | 0 | 1 | - | 1 | 2 | 2 | 1 | 2 | 17 | |

| Battery Swapping Infrastructure | 52 | 3 | 1 | 0 | 2 | 1 | 0 | 2 | 61 | |||||

| STORAGE INFRASTRUCTURE | Storage Infrastucture | 36 | 8 | 5 | 4 | 0.3 | 5 | 1 | 1 | 2 | 2 | 2 | 4 | 71 |

| Oil/Fuels | 36 | 5 | 5 | 0.6 | 0.3 | 5 | 1 | 1 | 2 | 2 | 1 | 2 | 61 | |

| Natural Gas | 2.0 | 3.8 | 0.0 | 0.02 | 0.3 | 1.0 | 1.0 | 8.1 | ||||||

| Fertilizers | 0.5 | 0.01 | 0.2 | 0.03 | 0.01 | 0.08 | 0.5 | 0.5 | 1.8 | |||||

| Coal | 208 | 80 | - | - | 2 | - | - | 3 | 3 | 16 | 3 | 3 | 318 | |

| Gas | 27 | - | 8 | 11 | 7 | 4 | 6 | 3 | 3 | 2 | 3 | 5 | 79 | |

| Batteries (Deployment + Production) | 297 | 17 | 3 | 9 | 2 | 21 | 0 | 2 | 2 | 5 | 1 | 5 | 364 | |

| Power | Renewables Generation | 1,395 | 127 | 27 | 28 | 17 | 65 | 1 | 4 | 8 | 20 | 6 | 7 | 1,705 |

| Nuclear | 105 | 6 | 30 | 7 | 10 | 1.1 | 2.1 | - | - | - | - | - | 162 | |

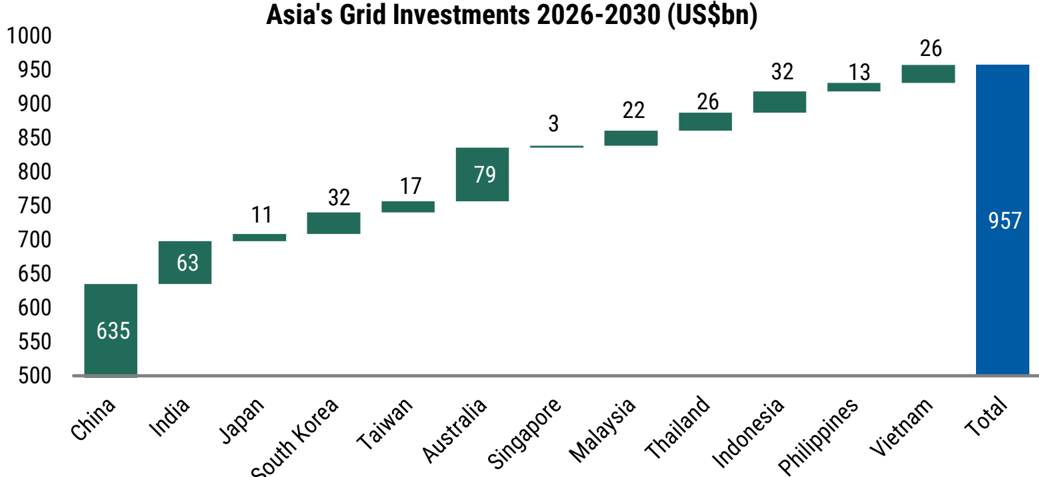

| Power Grids | 635 | 75 | 11 | 32 | 17 | 78.6 | 3.2 | 22 | 26 | 32 | 13 | 26 | 969 | |

| Total | 3,089 | 552 | 116 | 128 | 59 | 242 | 19 | 115 | 103 | 223 | 63 | 115 | 5,454 |

Source: Morgan Stanley Research estimates

Increasing energy security is a critical goal

Asia will leverage its coal, palm oil, solar radiation availability, and agriculture feedstock to become more self reliant on energy needs. It will also more aggressively seek energy self dependence in an increasingly multipolar and AI-driven world. Boosting energy security could include the following:

-

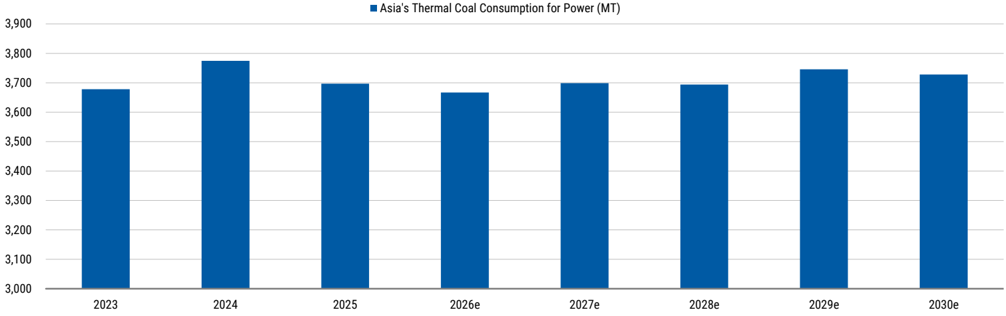

- Asia and Australia are home to 60%+ of global coal reserves with a diverse geographical spread. We see coal consumption for power rising to 4,000mntpa, the fastest growth by 2030 seen in this decade.

-

- Palm oil, sugar and agri waste will be increasingly leveraged by India and Southeast Asia to diversify their fuel mix, with Asia accounting for ~80% of global palm oil production, 40-45% of global sugar, and home to about half the world's agricultural production.

-

- Upstream oil and natural gas production has been restricted due to unfavourable pricing and government policies. A material shift which is in the works here could raise output in Asia by 1.7mnbpd, i.e., 5-7% of import dependence.

-

- Asia is the hub for shipbuilding and accounts for 85% of global capacity. This accelerates Asia's ability to source energy from countries outside of the Middle East a lot quicker.

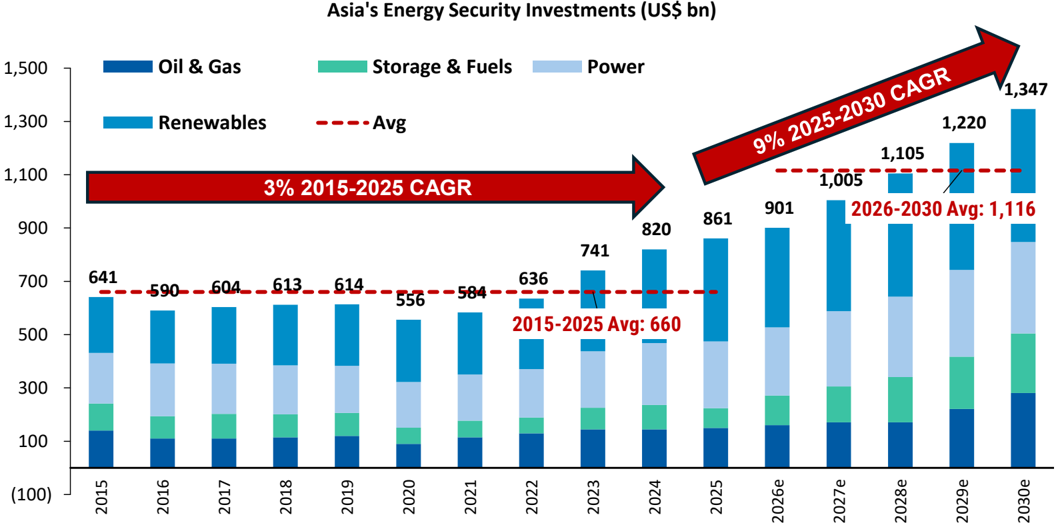

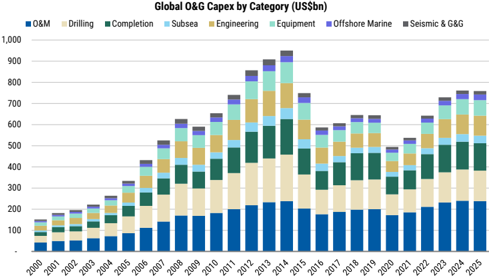

Energy insecurity has manifested in the form of plastics shortages, curtailment of air travel, lower steel and nickel production, and tiered power pricing for data centers. The tightness in energy markets will keep margins structurally high for the coming decade, incentivizing new investments, while policy makers underwrite some critical components of energy security. Energy investments in Asia have averaged US$660bn ( Exhibit 5 ) annually over the past decade. We expect them to double on average annually until 2030, with evidence of increased spending since 2024 after the Russia-Ukraine conflict.

M

Exhibit 10: Asia: What policy makers are saying about energy security

| Country | Key Quotes | Type | Notes |

|---|---|---|---|

| India | India should be "self-reliant' in energy sector | Fuel Coal Gasification Coal Fertilisers Renewables | Higher ethanol blending in vehicles (including E85 fuel and E100) First ever tranche of four commercial coal mines for underground coal gasification. Coal ministry launches 15th auction, offers 17 blocks to boost output Discussion on fresh investment policy for ~10mntpa of Urea State level policy push on Renewables and Storage |

| China | 'Wemust systematically respond to external shocks and challenges, improve energy resource security guarantee levels and counter various uncertainties with the certainty of high-quality development." | Nuclear Power Energy Efficiency Coal Renewables | China to triple Nuclear Energy capacity between 2020-50 Three-year action plan to accelerate the high-quality development of energy-saving equipment in six major categories China revives Coal-to-Gas Projects Building new energy systems including geothermal energy |

| Singapore | "In Singapore, weare geographically disadvantaged. Weare a very small country. Wediversify our energy portfolio and wepursueall feasible options to strengthen our energy reliability, security and our ownresilience ." | Power Nuclear Energy Co-odination with ASEAN countries | 1.8GW of Newgasfired power capacity to be built by 2032 Capability building in Small Modular Reactors (SMRs) MoUwith South Korea ASEAN Ministers committed to focus on advancing energy resilience through diversification of energy sources, accelerating renewable energy deployment, and exploring emerging technologies Co-operation with Japan in LNGupstream and storage infrastructure. Increase biodiesel blend from 5%to7%. Authorities probe to expand biodiesel blends (B10 and B20) |

| Thailand | "Strengthen energy security, including diversification of oil and gas imports and energy saving" | Gas Fuel Renewables | Approval of solar rooftop installation plan with ability for households to sell electricity back to the grid |

| Malaysia | "Energy security is no longer optional, but it has become a strategic national priority " | Coal | Tenaga is looking to sign 10 contracts of affreightment (COAs) to import the coal for the next 15 years |

| Japan | " Diversify both energy suppliers and sources to mitigate market volatility" | Nuclear Coal | Japan restarted existing reactors; plans to maximize nuclear energy Govt decided not to apply curbs on inefficient coal power plants in 2026, usage of coal plants to increase |

| South Korea | "We encourage economies to diversify their power sources and technologies while... enabling efficient market operation to enhance power system flexibility, resilience and stability." | Coal Nuclear | Lifted limits on coal- fired power generation capacity Korea will raise nuclear power plant utilisation to as high as80% |

| Australia | "Ensuring long-term energy security for Australia is a priority of our Government" | Fuel and Fertiliser Coal Natural Gas Critical Mineral Value | Export Finance and Insurance Corporation Amendment (Strategic Reserve) Bill 2026 to secure fuel and other strategic materials including fertiliser NewSouth Wales coal mines given two-year extension as well as the first new area for gas exploration after a decade NSWopenedits first new areas for gas exploration in a decade after gas for power generation fell to two -decade low Diversification in Critical Mineral Strategic Reserve |

| " Increased investment in comprehensive energy infrastructure across the entire energy supply chain, from upstream development facilities to downstream equipment, in order to support affordable, reliable and secure | chain Fuel Natural Gas | B50 biodiesel implementation testing for automotive, mining and railway sectors Government study on national CNGuseasLPGsubstitute | |

| Indonesia | energy supply, including baseload electricity." | Renewables Natural Gas | The government has begun drafting the 2026-2035 National Energy Plan (RUEN) focusing on energy security Indonesia and Japan accelerated the US$20.9 bn Abadi LNGProject in the Masela Block |

Source: Reuters, Bloomberg, Morgan Stanley Research

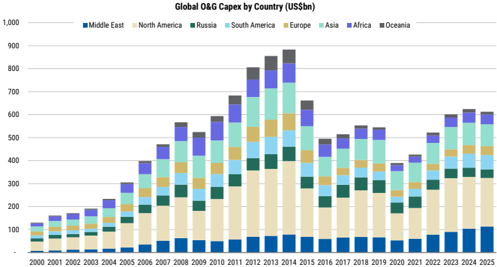

China is facing an energy chokepoint : China, the world's largest manufacturing hub and second-largest economy, is increasingly confronting a structural challenge of energy security within a more fragmented, multipolar global landscape. With rising geopolitical uncertainties, supply chain realignment, growing domestic demand, and ensuring reliable and affordable energy have become central strategic priorities. Against this backdrop, China's 15th Five-Year Plan featured an unprecedented US$3-3.8trn investment across energy production, power systems, and downstream infrastructure.

A local focus - grids and fossil-based power drive spending the most

Recent access to energy in Asia is now coming from local markets, despite energy being a global supply chain, as multiple countries ceased fuel and chemical exports, thereby exposing vulnerabilities in

other economies' supply chains. We expect energy capex outside of renewables to nearly double to US$640bn with new projects to secure energy rising to US$1.2 trillion over the next five years, as Asia's energy needs rise 15% by 2030. The key area of growth will likely be power, which will attract about two-thirds of new investment spend, followed by energy storage, oil, natural gas exploration and midstream ( Exhibit 32 ). We see an inflection in spending on natural gas pipelines, coal gasification, biofuels, new fuel refineries, and storage ( Exhibit 32 ). For power, grids will attract the largest part of the spending, then fossil-based power generation, while renewables may see stable capacity additions. Tertiary benefits will flow into commodity trading houses in Japan and shipping corporates, as energy diversification drivers longer supply chains, and also benefits steel, uranium, aluminium and copper consumption supported by over three trillion dollars of power grid and power investments.

M

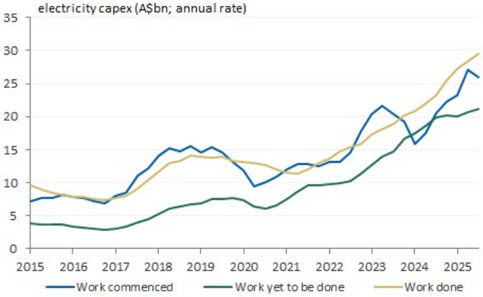

Exhibit 11: Asia's annual energy investment is set to nearly double for the rest of the decade

Source: Morgan Stanley Research estimates

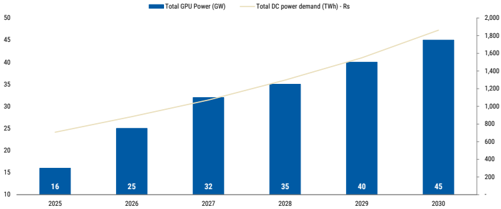

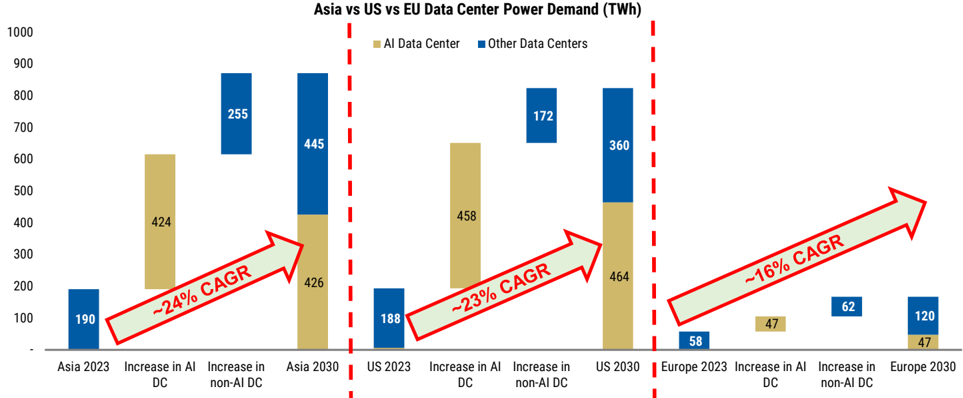

From 'powering AI' to 'securing power' for AI: There is no AI without energy. AI investments have now risen above energy investments in Asia, and we believe power supply tightness in multiple markets will accelerate new dependable energy investments as AI adoption picks up, with 75GW of data center capacity by 2030. While China is well positioned to power its AI needs with renewables, we estimate the rest of Asia will need to invest US$235bn to set up 100GW of coaland gas-based power generation, while supplementing it with batteries and renewable investments of US$1.3tn. We believe India, Thailand and Singapore will see upside surprises to data center capacity growth in the coming years.

Balancing Consumption Growth and Self Reliance

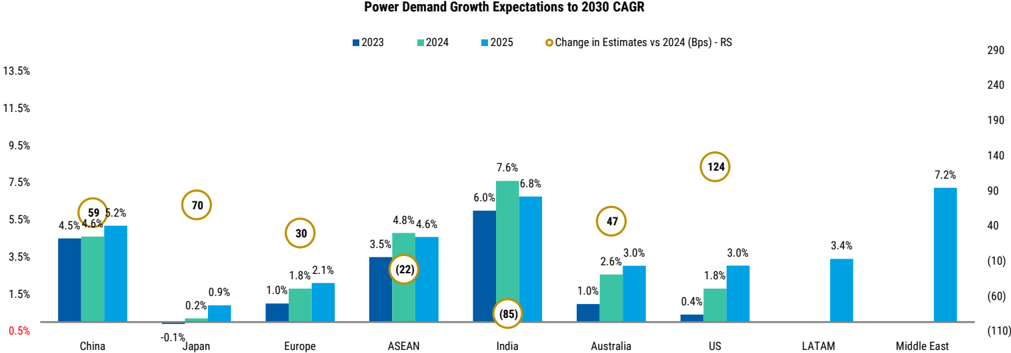

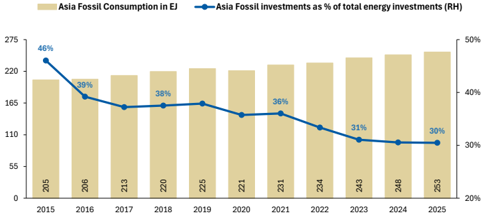

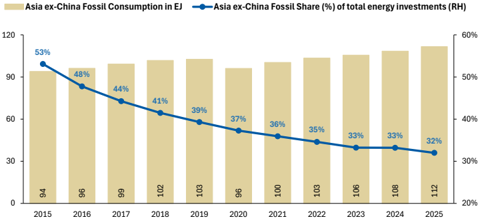

Energy consumption has grown 50% in Asia over the past decade but energy investments have been stagnant at around US$0.7trn ( Exhibit 5 ), leading to rising stresses in energy systems, which now have reached a critical stage as global energy supply chains readjust and AI adoption accelerates energy intensity for economies a lot faster than most policy makers were ready for. Energy consumption in Asia will rise 300bps faster than in the past decade, we estimate, with power consumption growing at twice the pace. Energy investments will accelerate across Asia at its fastest pace for the rest of decade, with every single economy now pledging to improve energy security issues quickly.

Exhibit 12: Asia: US$5.5trn investment = Import reliance on new energy consumption reduces to less than 30%

Reducing Asia's Incremental Energy Import Reliance by 7% (EJ)

Source: Morgan Stanley Research estimates

M

Funding the US$5trn investment supercycle

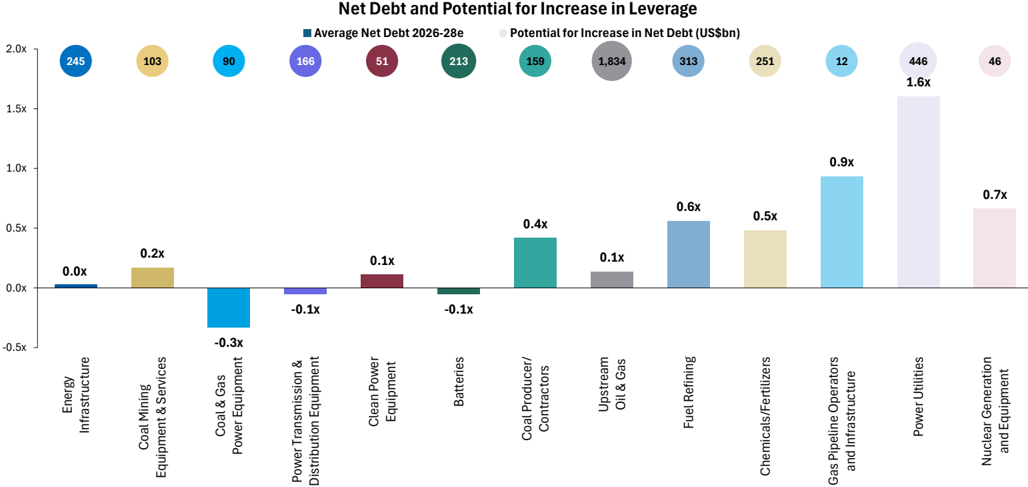

Energy corporates, especially fossil fuel-based power generation companies, upstream oil and gas producers, integrated oils and downstream fuel refiners companies, have under invested over the past decade and generally have very strong balance sheets. Even equipment producers in upstream turbine/transformer and wires supply chain have been cautiously putting capex to work in Asia due to changing fuel mix that favoured green technologies in the primary energy mix over fossil fuels and power grids. With a more balanced outlook ahead and policies presenting less of a challenge for fossilbased operators, we believe corporates with strong balance sheets, especially integrated oils which could also be among the largest power supply chain players, will benefit the most.

As both governments and hyperscalers are underwriting the cash flows for power and energy storage producers, we estimate 75% of investments will be funded by balance sheets of energy companies with a combination of OCF and debt. The remaining funding, we believe, should be a combination of government support and global sovereign support.

Exhibit 13: Funding energy security: Corporate balance sheets are strong with limited debt as the companies have been behind the curve on growing investments vs. consumption growth. Collectively we see US$4trn potential for funding by debt on 2028 multiples

Source: Refinitiv, Morgan Stanley Research estimates

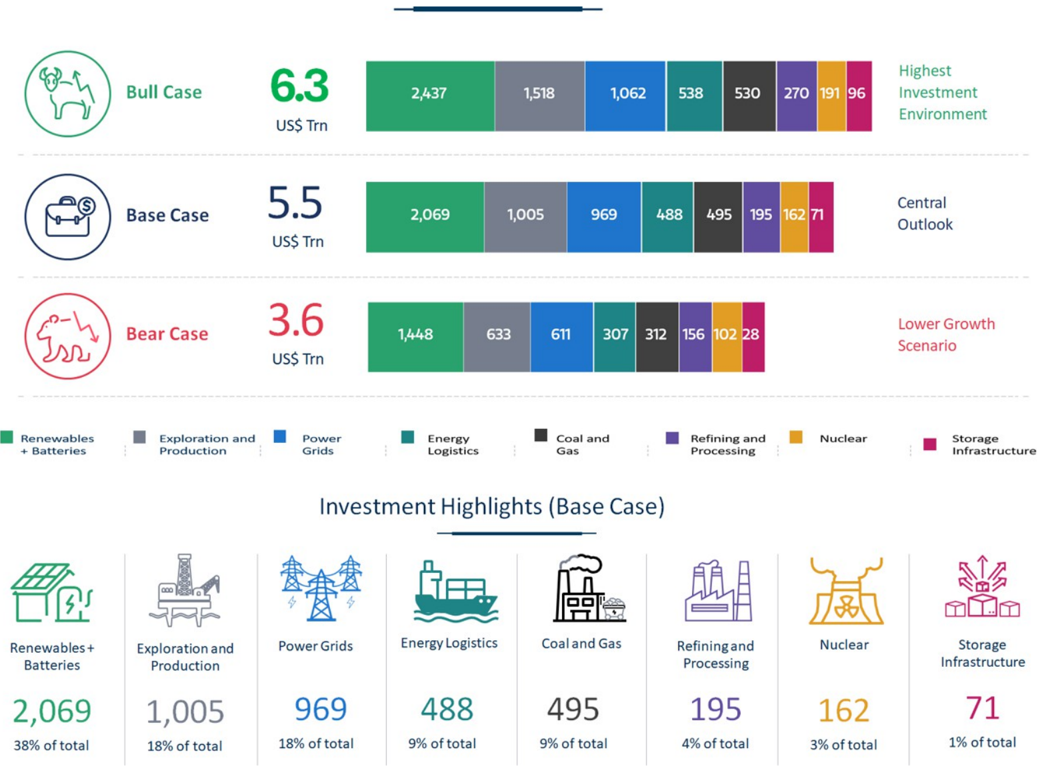

camble 14. The chelyy secury mivesthell oupel cycle. The bull, base allu Deal vases

M

Understanding our Bull-Bear framework in the context of a supercycle

Our US$5 trillion-plus investment calculation from a bottom-up country level basis includes each country's needs needs for power, oil, storage and chemical capacities, while triangulating it with government policy, powering AI needs and execution time frames. Our

Issi

US$ Trn

Exhibit 14: The Energy Security Investment Supercycle: The Bull, Base and Bear Cases

Renewables

- Batteries

Renewables +

Batteries

2,069

38% of totall

Source: Morgan Stanley Research estimates

Bear Case

1,448

633

611

Highest

Investment

Environment bear case assumes challenges around availability of manpower, equipment supply chain bottlenecks and delays in execution, especially in India and ASEAN, around projects involving coal plants, new fuel refineries, and upstream oil and gas production. For our bull case, we assume accelerated policy support helping the execution of powergrids, energy storage, storage of fuel and LNG, as well as renewables in China.

307

312

156

102 28

Lower Growth

Scenario

1,062

538

530

270

191

96

Speed of Implementation

1-2 years

3-4 years

5+ years

Aolas Shelyy secury mplem ellatlon vo. Urgency Maulix

M

Australia

Securing Energy: The Nuts, Bolts and Challenges

Korea

Japan

China

India

China

ASEAN

China

Feedstock Diversification

'Safety and certainty in oil lie in variety and variety alone.' First Lord of the Admiralty Winston Churchill gave the defining quote on oil diversification in 1913 while addressing the British Parliament after the US navy made the switch from coal to oil. China

Australia

Japan

ASEAN

Securing Asia's Energy

Taiwan

South

Australia

Korea

We expect the ongoing energy shock to trigger more than US$1trn of annual spending ( Exhibit 5 ) on fuel refining, storage, gas pipelines, power grids, and coal and gas power generation through 2030, as well as boosting capex in renewables and nuclear supply chains. We believe the strong balance sheets of energy corporates can fund these new investments ( Exhibit 13 ), especially in the context of tight energy markets.

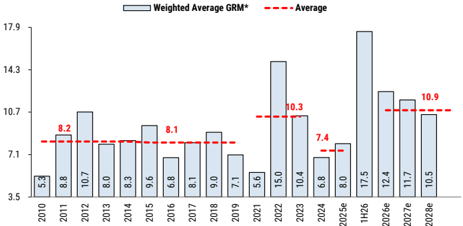

Tight energy markets also provide upside risks for: 1) fuel margins, as new capacity adds still lag consumption by about half, driving higher

Australia

China fuel refining investments; 2) government support and funding leads to 1bn+ barrels of new fuel storage build in Asia; 3) coal generation rises by more than 350GW, the fastest in a decade, and energy storage rises 6x to ~3,000GwH as power consumption grows 3x faster outside of China; China uses coal-based power generation for intermittent supply to balance renewable loads; 4) gas pipeline infrastructure helps accelerate natural gas adoption with diversification of feedstock supplies to the US; US ethane and propane for plastic manufacturing also makes Asian chemical and fertilizer players more competitive; and 5) organic chemicals such as sulphur that are essential in metal processing, pharma and tech supply chains go from being byproducts to being more valued commodities.

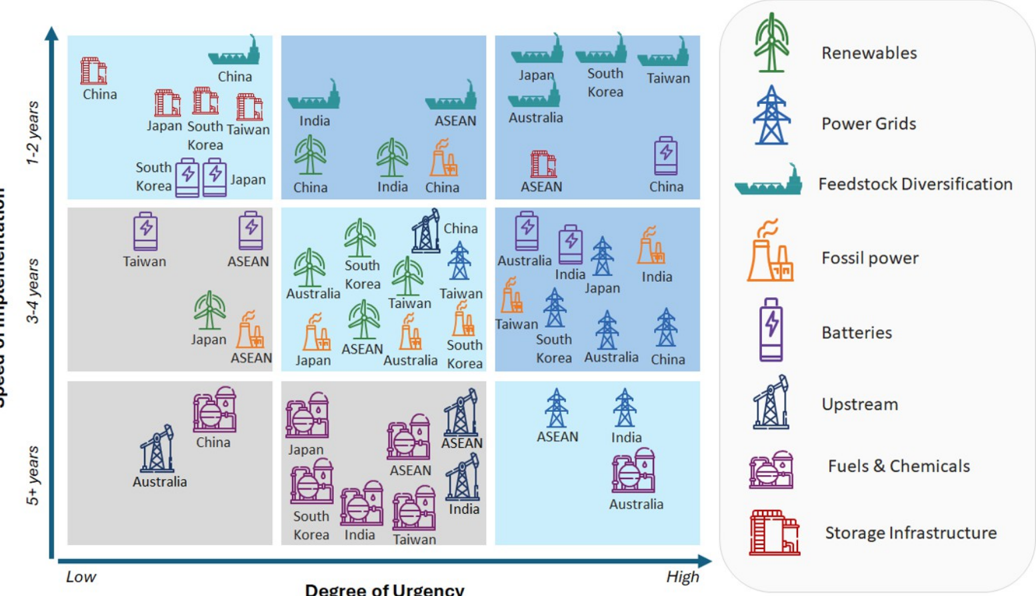

Exhibit 15: Asia's Energy Security Implementation vs. Urgency Matrix

Source: Morgan Stanley Research estimates; not drawn to scale

Taiwan

Taiwan

South

Korea

South

Korea

Taiwan

Renewables

Batteries

M

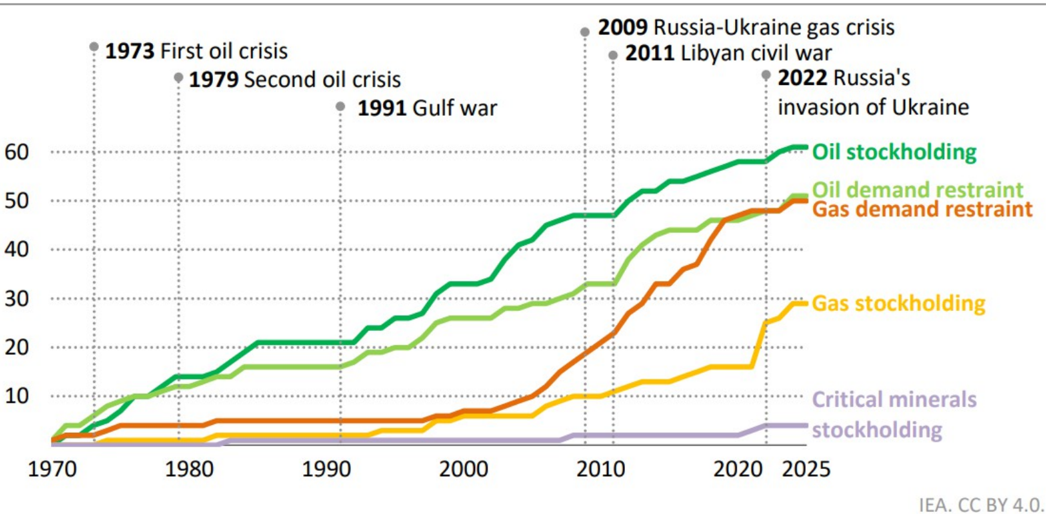

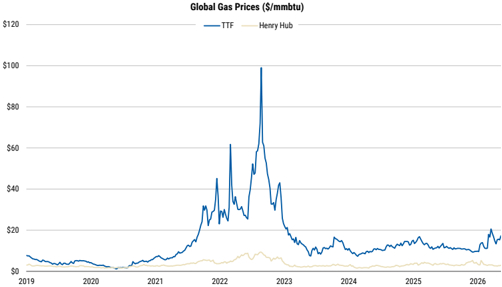

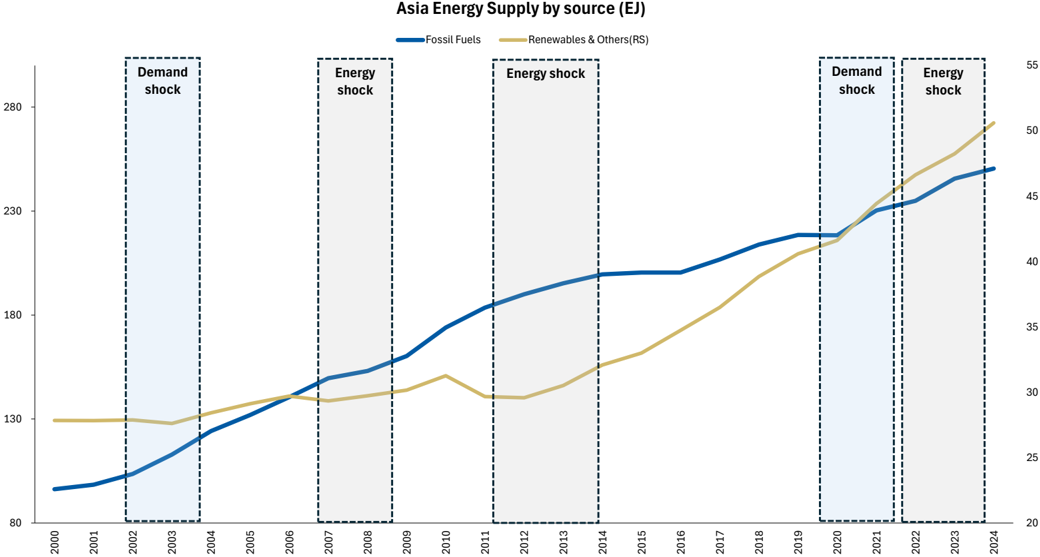

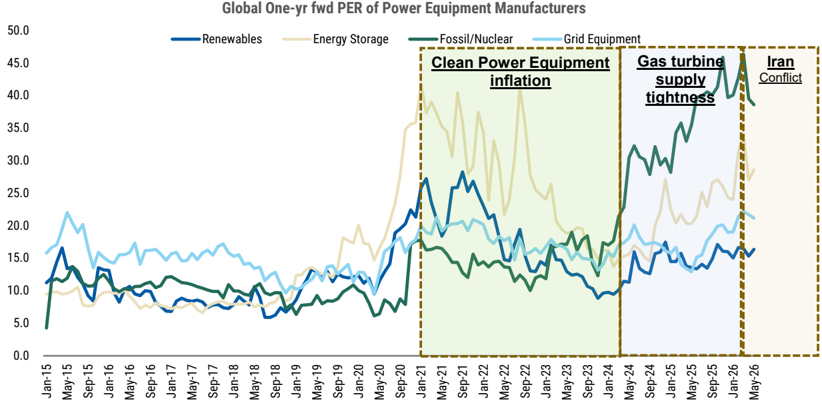

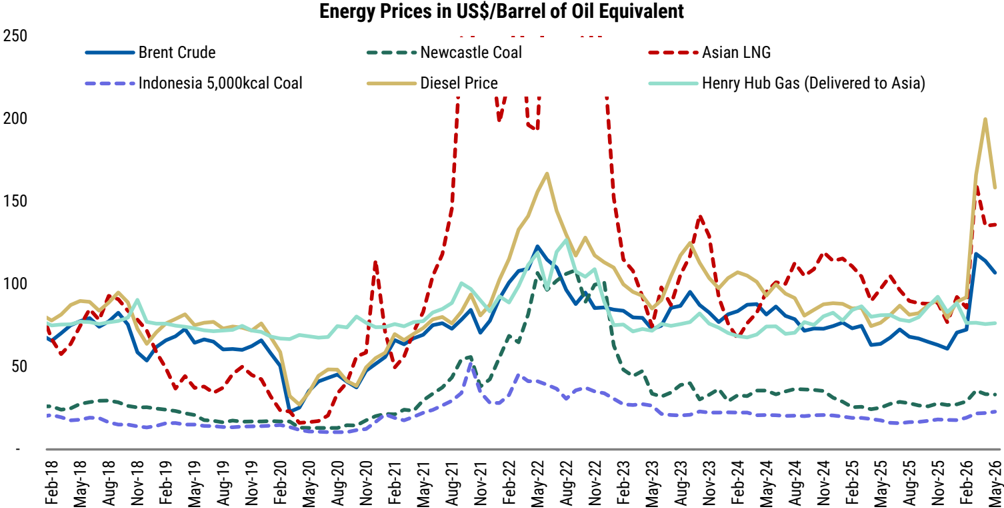

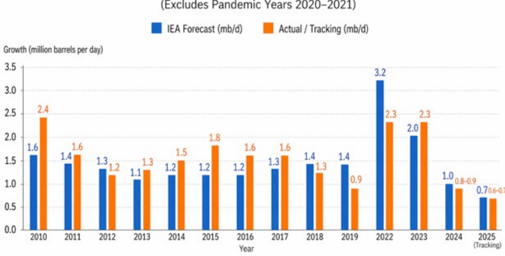

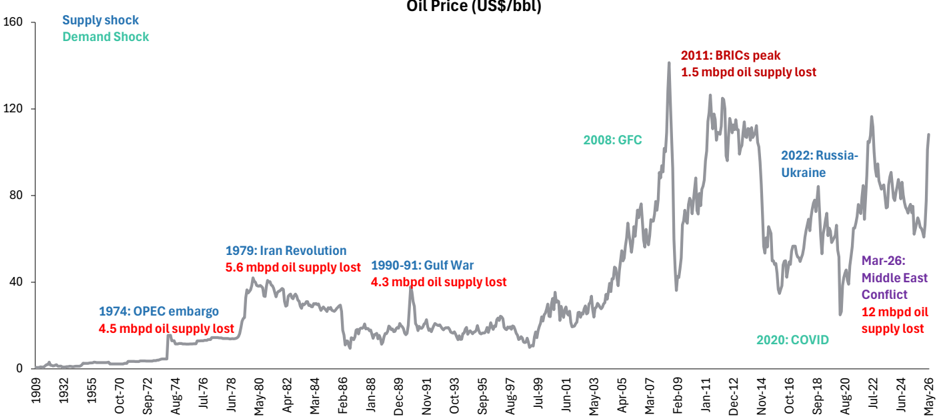

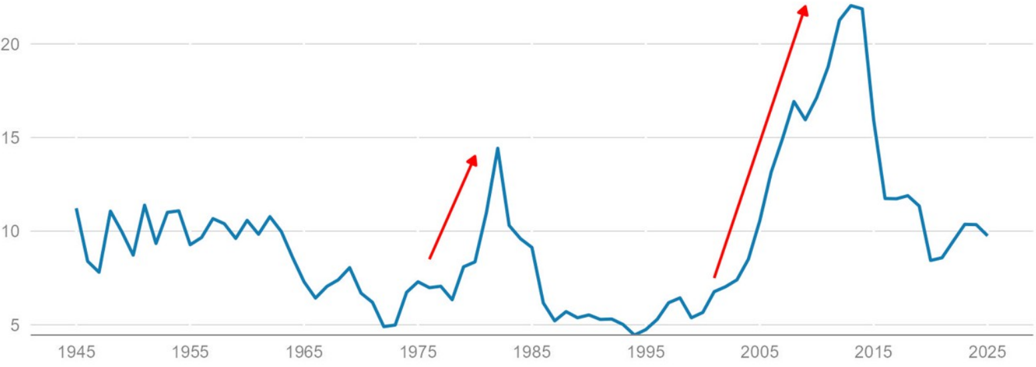

Policy makers began to pay more attention to energy security following the 2022 oil price shock ( Exhibit 18 ). In its wake, we saw a pickup in fossil and nuclear fuel supply chain investments, which were then boosted by AI's power needs. Now, the 2026 supply shock puts the focus more structurally on energy security and not just the energy transition, as Asia goes through its worst access-to-energy challenge in at least 50 years.

Energy supply chains will realign as countries avoid the current chokepoints: Energy supply chain realignment is shifting from "justin-time" cost efficiency to "just-in-case" resilience, driven by geopolitical tensions, trade tariffs (e.g., US tariffs, FEOC restrictions), and the need to decouple from dominant suppliers like the Middle East. This restructuring prioritizes friend-shoring, regionalization, and closer to home. We believe Asia will import a lot more natural gas from the US and Russia incrementally, considering it is essential for power and transport systems, while also seeing higher oil imports from LatAm, Canada and Africa. Fuel systems in Asia will also likely realign as exports were curbed for the first time by China and Thailand. We have already seen signs of this change with the Australia-Singapore energy co-operation and expect other economies such as Japan, Taiwan and Korea to re-look at fuel sourcing options. Coal, which is ample in Indonesia, India and China, will also be key for 'just in case' resilience for power systems. Power grid connectivity in Southeast Asia between countries, such as India-Bangladesh, will get more traction after two decades of limited progress.

While supply chains alone will not help in addressing the energy and national security concerns, economies like Japan and Australia are looking to invest directly in regions like ASEAN to expand the security of supply chains. Japan's Prime Minister highlighted ( Exhibit 10 )

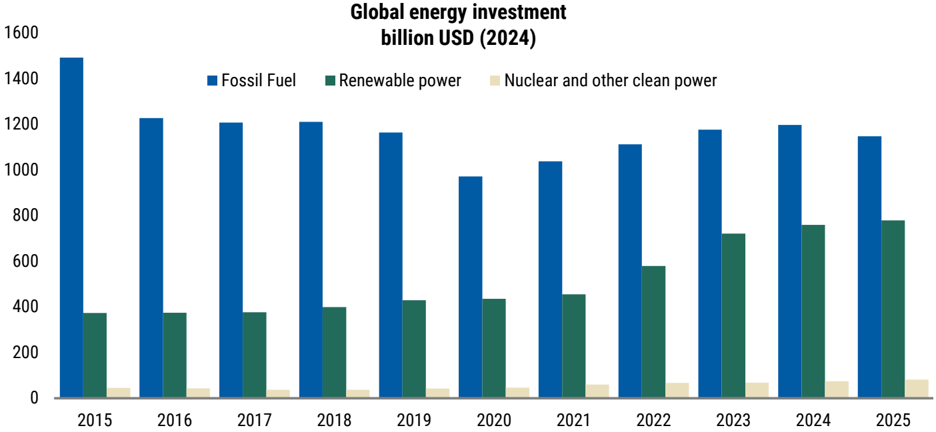

Exhibit 16: Global AI data center capex is set to surpass investment in both power and oil & gas

Source: IEA, Morgan Stanley Research estimates the country's mutual dependence on ASEAN as it channels US$10bn into ASEAN for sourcing crude oil, while Japanese energy corporates are raising their Southeast Asia footprint. In addition, UAE will invest US$5bn in India across energy and storage. Australia has also signed energy supply agreements with Singapore for fuel and LNG.

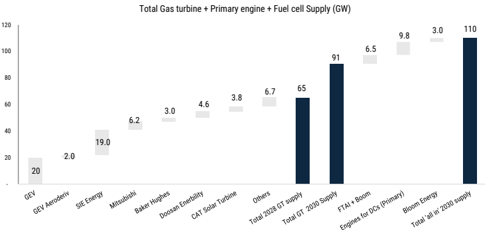

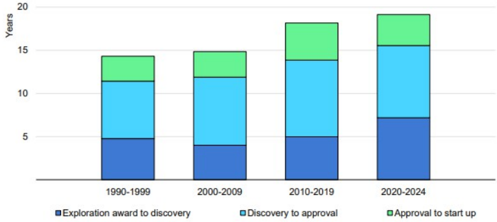

Bottlenecks to energy security - Limited investments over the past decade and the availability of labour are the key bottlenecks to achieving energy security and powering AI investments. The availability of capacity to build steam turbines, high voltage transformers, fuel refinery CDUs, FPSOs for oil extraction, FLNG infrastructure and skilled labour will drive investment over multiple years (but not the next few given long lead timelines for land sourcing, environmental approvals and construction. Corporate balance sheets are very strong but energy corporates have had high hurdle rates to grow and have normally been more reactive to consumption growth in their investment approach. We believe national oil, power and private players will invest over US$4tn+, or about 80% of the necessary infrastructure to fortify energy needs domestically, while government subsidies, and the collaboration of Global South with Global North will help address funding needs as well. Increasingly the role played by technology companies with large balance sheets to underwrite these investments will become critical.

Innovation will provide solutions where the diversification of supply chains is difficult: Examples include coal gasification in India, green hydrogen supply chains to Singapore and Korea from India, sodium ion batteries for energy storage to make China less dependent on lithium imports, and SMRs (small-module reactors) in India and Southeast Asia.

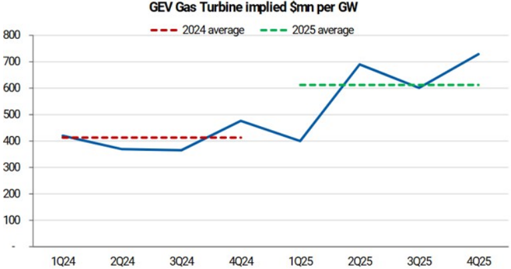

Exhibit 17: Gas turbine, engine and fuel cell capacity supply developments out to 2030. Gas turbine supply (GW) is set to double between 2025 and 2030, reducing some of the recent bottlenecks in the electrification supply chain

Source: Morgan stanley Research estimates

cambre 1o. cutulative number or countles will selecteu ellel yelley leopolise dilu ellelyy securly poncies, T9fU<ULo

M

Affordability vs. New Investments

The affordability question - Tiered energy prices to become the

norm: Asia is home to some of the most price-sensitive consumers, so affordability is key for any energy source to be adopted. Energy security is expensive and does come with infrastructure which is not always useful but needs investment to create and maintain. Hence, like in power, we believe tiered energy pricing will become even more prevalent as industrial consumers, data centers, airlines, and higher voltage users pay for energy security. In the process they subsidize the lower income consumer groups. We have seen some evidence of this in Malaysia with data centers, Thailand with high volume retail consumers, higher taxes for fuel in India, and lower power taxes for distributed power consumers in the Philippines.

2009 Russia-Ukraine gas crisis

• 2011 Libyan civil war

2022 Russia's

The Challenge: Energy security = Oversupply? - Oil stockholding

Oil demand restraint

Increased domestic capacity for everything from power to chemicals has historically led to oversupply in globally linked commodities, such as plastics and fuel. While we expect oversupply in some parts of the value chain, shipyards, power, fuel and even coal should see the least challenges in terms of domestic pricing. Although we could see a new downcycle take shape in 2029-30 with the startup of new supplies in specific value chains, it is unlikely to be as challenging as the last few years considering the higher cost of capital for economies like ASEAN and India vs. China, which should see capacity growth. Domestic coal in Asia - whether in Indonesia, India or China - should provide competition for US LNG imports, while power, being a highly domestic commodity, should not see many of the challenges of oversupply, especially against a backdrop of rising AI adoption. On equipment and battery supply chains, we see limited risk of oversupply until 2030, considering the rising orderbook.

60

50

40

30

20

10

Note: The analysis focuses on 85 countries, covering 93% of global primary energy demand, 87% of global

Exhibit 18: Cumulative number of countries with selected emergency response and energy security policies, 1970-2025

Source: IEA Energy Outlook 2025

M

The Nuts & Bolts of Securing Asia's Energy Complex

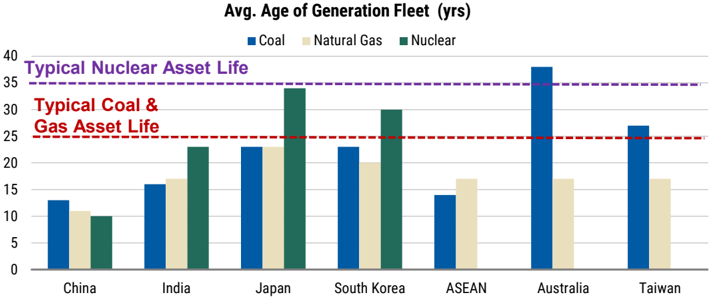

Power: We estimate 320GW of new power generation will be built in Asia by 2030, covering 40% of its new power consumption needs. While China's power generation exceeds consumption, most other economies are struggling to meet their future power needs after half a decade of underinvestment in dependable base load power systems. Renewable power and related supply chains have accounted for 67% of investment in Asia since 2020, but fossil fuelbased power consumption grew 4% and accounted for 70% of total units consumed outside of China. Even in China, fossil-based power generation grew at one of the fastest paces, despite the focus on renewable capacity. We see this adoption in fossil-based power generation accelerating with 440GW+ of new consumption coming from coal and gas, while the pace of renewable adoption slows (vs. the past five years) in Asia, partly also due to grid constraints and reallocation of capital to alternative fuels and new technologies. With with the dependable power fleet aging with an average life of 20+ years in Japan, Korea, Malaysia, Singapore, Australia and Taiwan, we see a replacement cycle in the works.

The nexus between energy and AI is also catalysing policy makers' response to energy security . There are at least two broad dimensions to this relationship. In the race for AI and robotics, energy remains a key bottleneck and power grid investments are the most important part as grids serve as highways for powering AI until dependable supply catches up. Energy storage will also act as a quickto-market solution in the race for AI adoption - and until supply becomes ample, which we believe will take until at least 2030.

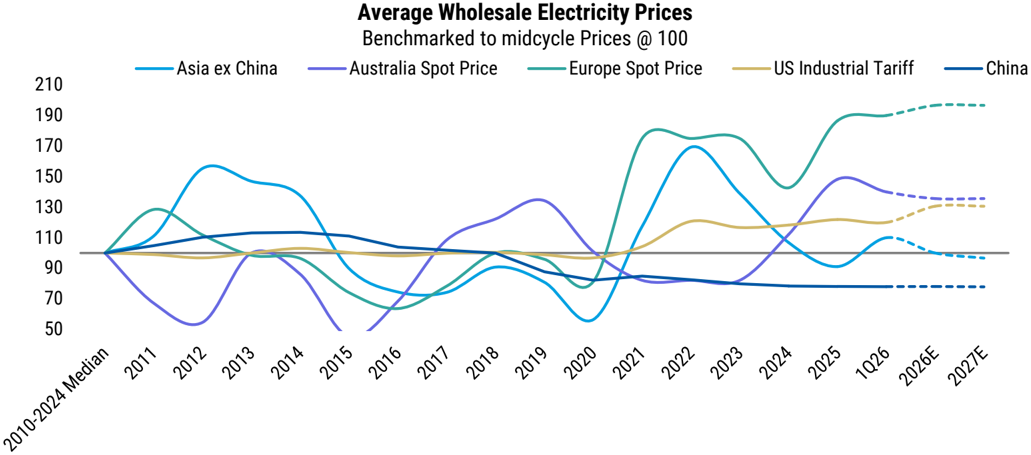

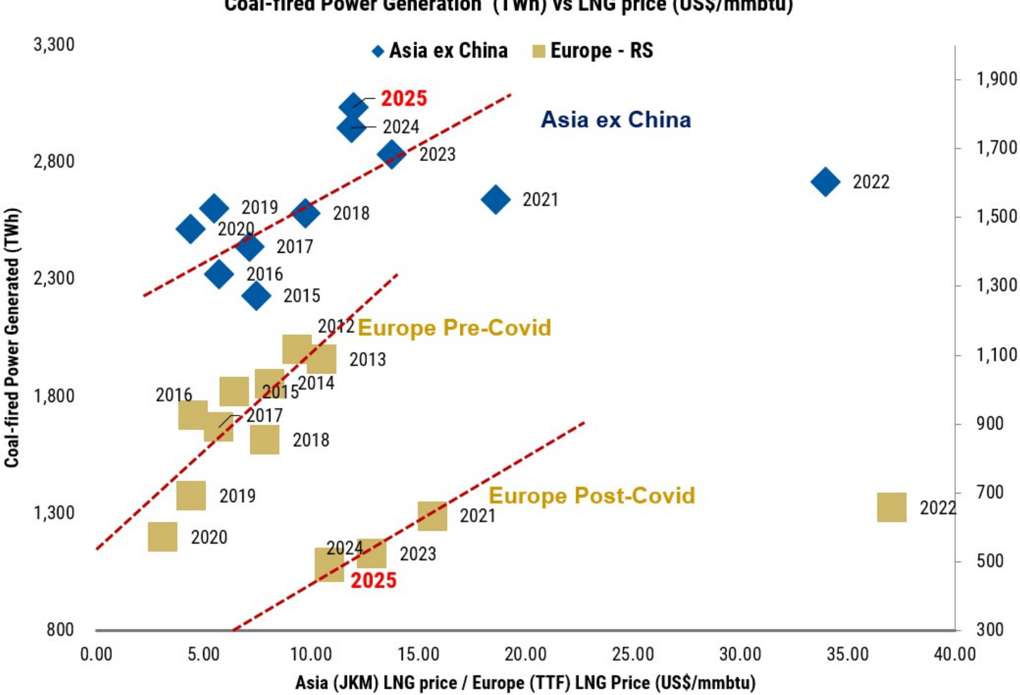

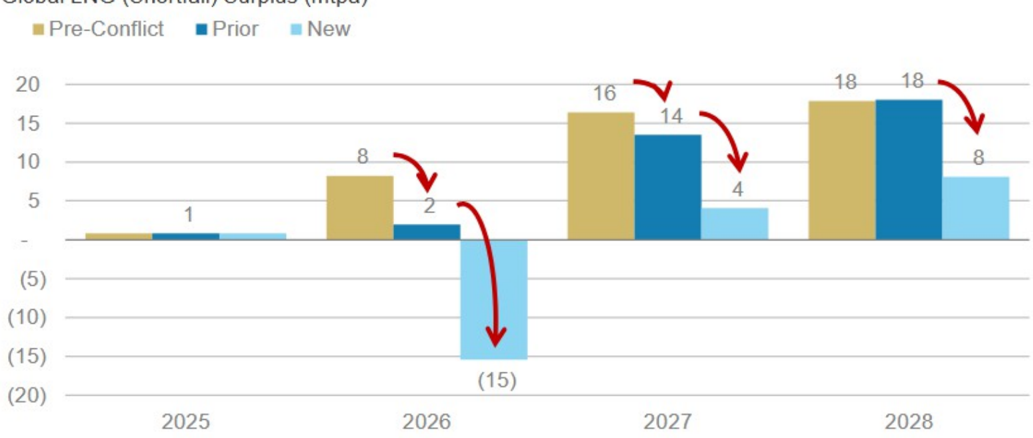

Coal and natural gas to take share in power, transport and industrials. We see coal and natural gas making a comeback in Asia's energy security story while natural gas imports become more diversified - a path Asia was already on but which will be accelerated in the coming quarters and years. Both fuels are dependable and diversified in terms of availability globally across US, LatAm, the Middle East and within Asia in countries like Australia, Indonesia and Malaysia. We estimate 500mntpa of new coal consumption needs and 100mntpa of gas consumption in Asia by 2030, driven by transport, AI and household needs for cooking and power. This should keep lower calorific value coal prices supported at higher levels with much lower discounts (at 15-20%) to natural gas vs. the past. While coal will replace 20mntpa of potential LNG imports for power, in absolute terms we do see US LNG imports making up two-thirds of incremental imports in Asia in the coming years as Asia diversifies its gas sourcing, especially in India/ASEAN and Korea/Japan. With oversup- plied global LNG markets, we also see significant pricing power for Asian consumers beyond 2027.

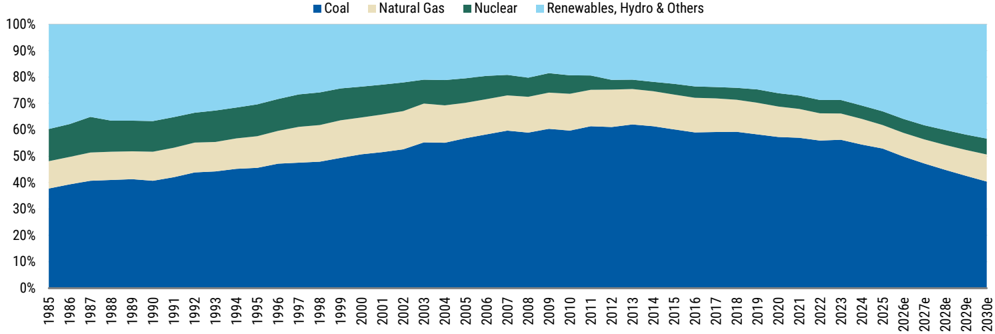

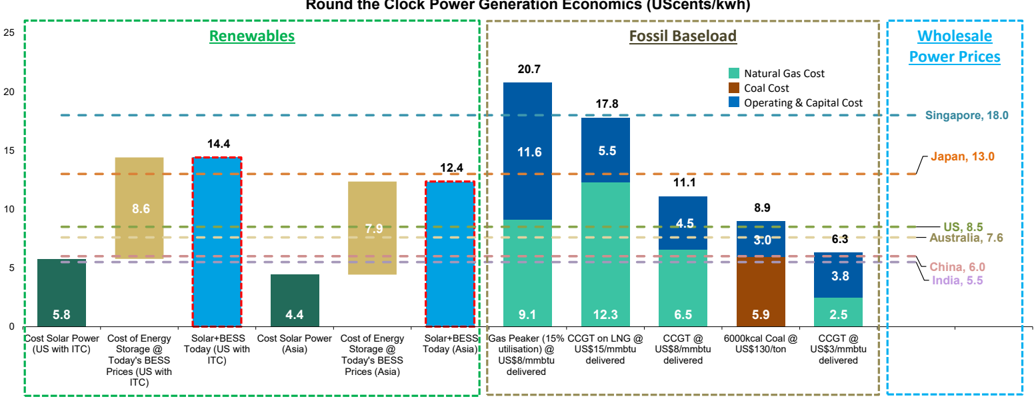

Coal and renewables to work together: Learnings from China. Over the past five years, China has added more renewables and nuclear generation capacity than the rest of the world combined, and solar PV and wind now account for 18% of generation. Despite this, coal demand for electricity rose by more than 25% from 2019 to 2024 and the country also has over 200GW of coal generation capacity under construction. The low capital cost of coal plants in China means that operating them flexibly to support renewables has much lower opportunity costs than in other markets. Even at a 30% capacity factor, its average levelized cost of coal generation at US$80/Mwh is lower than the levelized cost of gas at US$110/MWh.

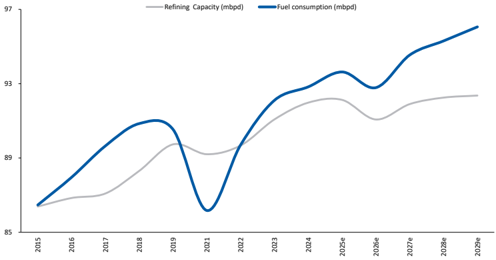

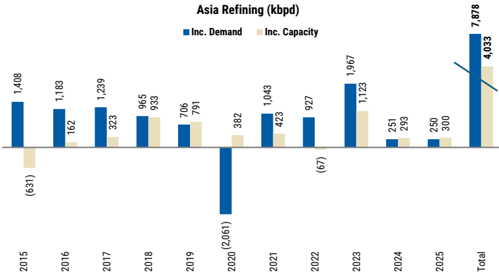

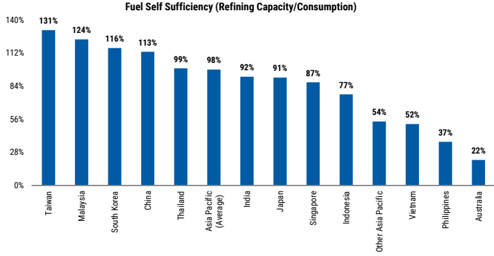

Fuels, plastics and storage: Asia's fuel consumption increased by 4mbpd from pre-Covid to 2025 and will keep rising until 2030. We estimate Asia will need at least one new fuel refinery to be built every year, i.e., US$12-15bn in annual investments to service this rising need for fuels ( Exhibit 141 ). Storage infrastructure to increase strategic reserves of oil, coal, fertilizers and even natural gas will be built to increase storage from 30-45 days in most economies to nearly 90 days, and will need US$40bn in annual infrastructure capex with implications for steel needs ( Exhibit 153 ), on our estimates. The export ban on fuel and fertiliser exporters in the past two oil shocks and the impact of this on India, Southeast Asia, Australia and Japan should drive new investments in the sector - something we last saw in 2017.

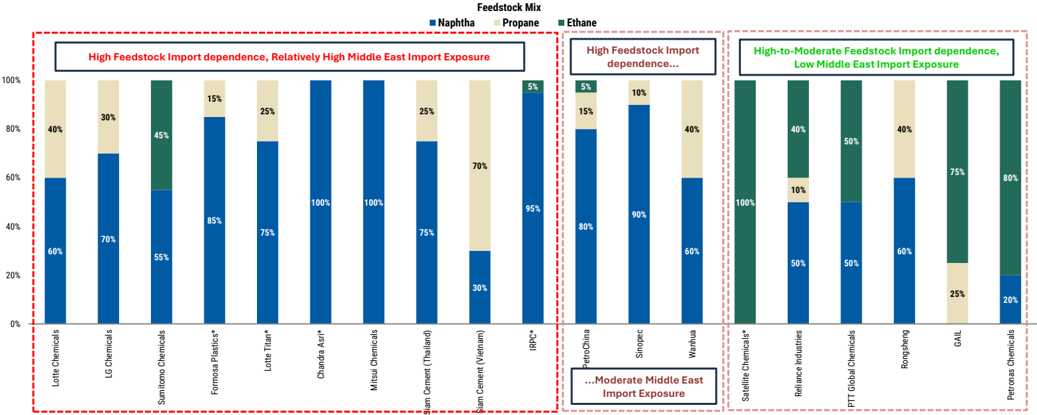

While most countries have focused on diversifying into natural gas and electric fleets for transport, it has become apparent that those efforts are only helping negate the increase in miles traveled by consumers, but not covering new consumers of oil (i.e., new car owners, air travel, etc.). Even supply chains for energy storage and batteries are being diversified away from China, with China itself increasingly focusing on sodium ion technology due to its dependence on lithium and nickel supply chains. We see new refineries being built in India, Thailand, Vietnam and possibly Australia. The shortage of fuel has led to lower petrochemical supply in multiple countries during the present oil shock. While there is excess chemical capacity in Asia and the world, naphtha access is going to be critical and will be a key consideration for new fuel refining capacity.

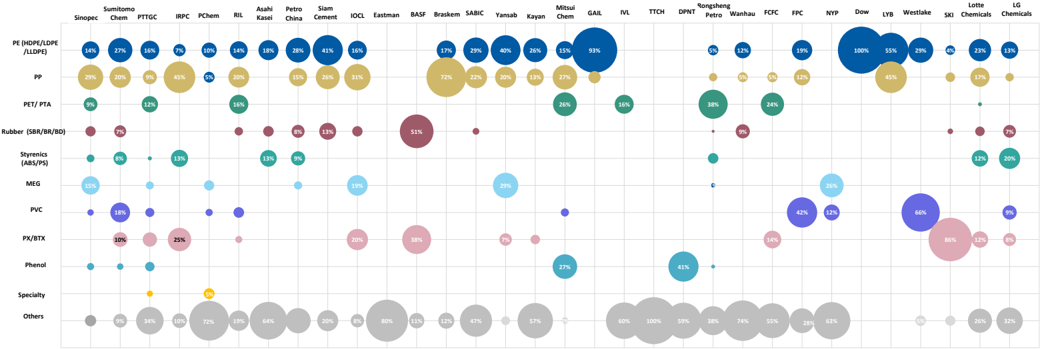

Chemicals for tech and metal processing supply chains: Metals, which are key in the age of electricity like nickel, uranium and copper, need significant amounts of sulphur to process ore, and sulphur is also used in chip-making for etching. We expect demand for sulphur,

M

a by-product of fuel refining, to rise at a 5% CAGR in Asia through 2030, despite Asia already accounting for half the world's consumption. We see new organic chemical investments in India, Thailand, Taiwan and Indonesia to secure supply chains.

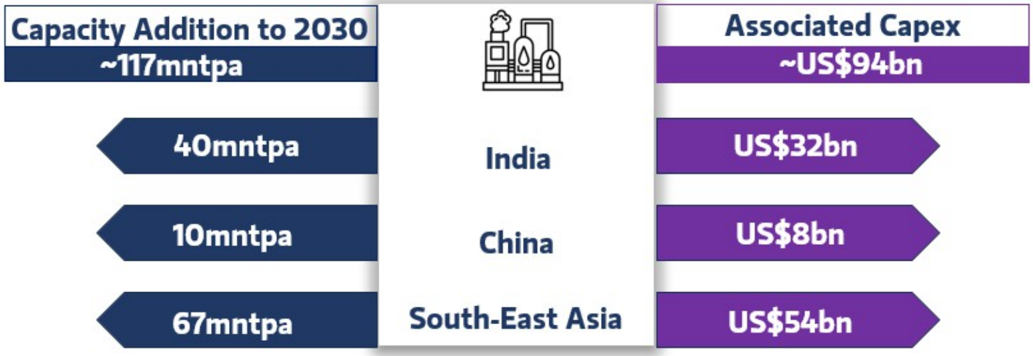

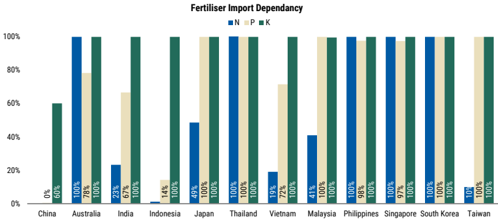

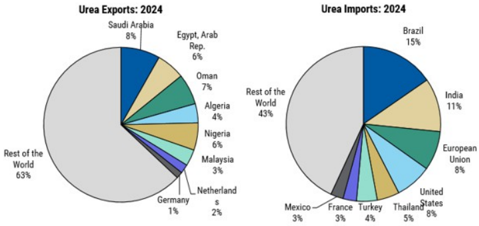

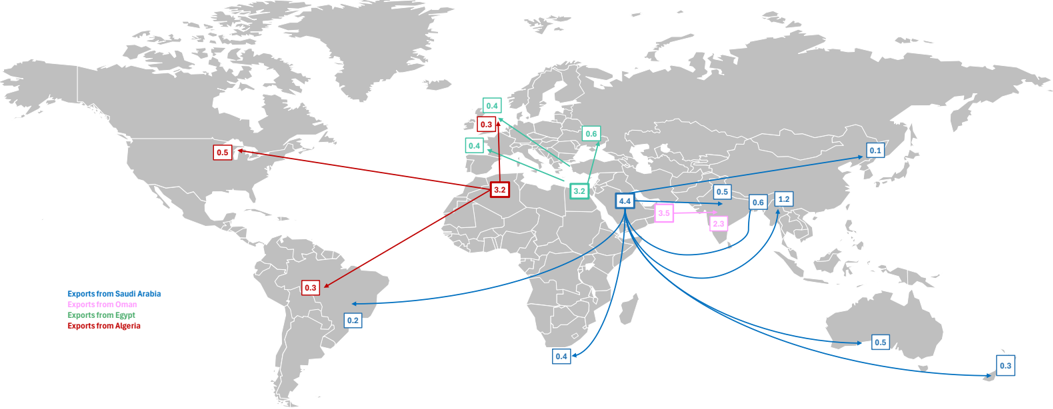

Fertilizers: Asia will build at least 20mntpa of new fertilizer capacity by 2030 as consumption rises by 3% annually through 2030. Ensuring the availability of fertilizers at stable prices is imperative for the good of humanity, since globally, in the last 50 years, fertilizers have made a 60% contribution to crop yield growth. Asia is the largest fertilizer-consuming region globally, importing a third of its requirements at US$100bn in 2025. The current shortage of fertilizer supplies is due to limited gas reserves in Asia and high import dependence on the US, Russia and Middle East. For non-nitrogen nutrients, Asia's (ex-China) dependence on countries like Morocco, Canada and Russia for potash and phosphate will likely continue. We see upside to our forecast of 12mntpa capacity additions, especially as new feasibility studies for fertilizer supply additions in India, Philippines, Vietnam and Australia have started as 'indigenous production' and security takes center stage.

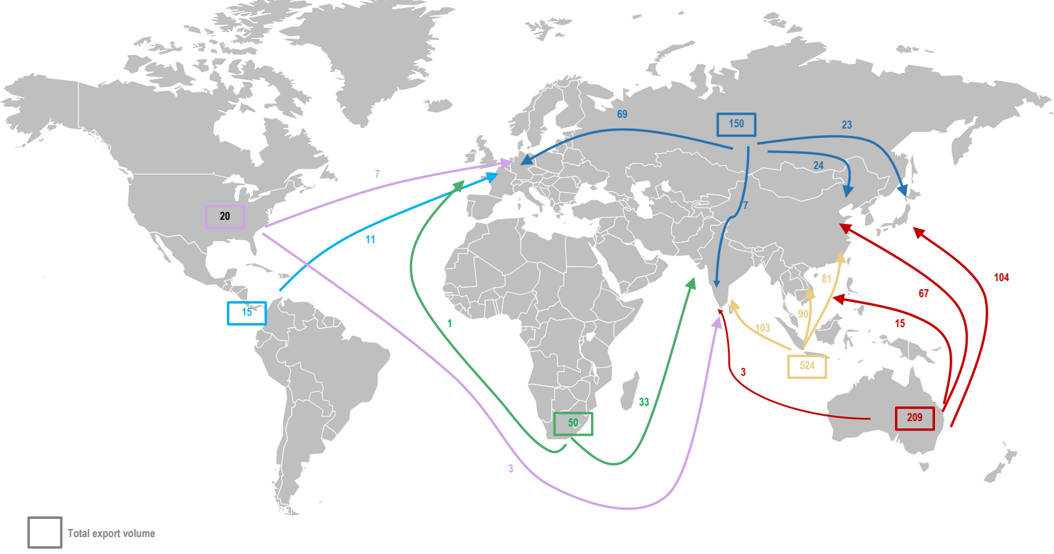

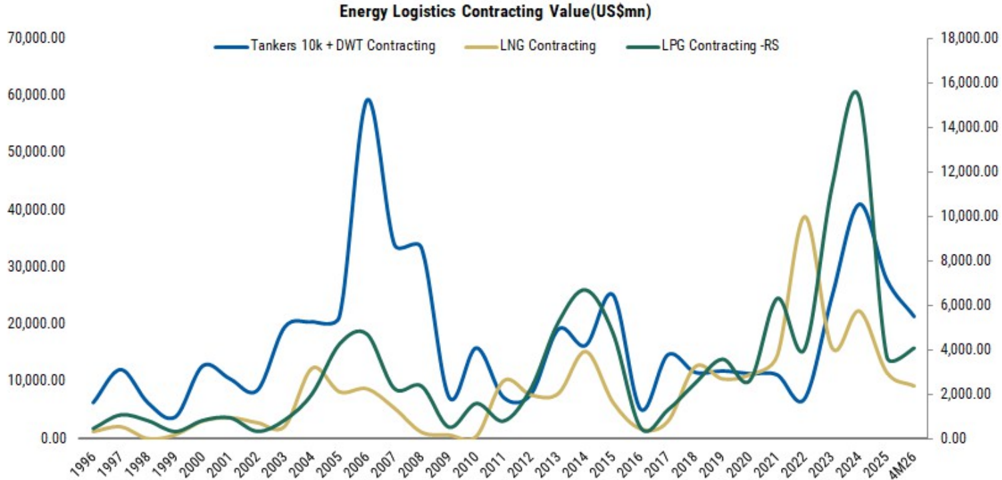

Shipping and shipyards: Global shipyard capacity has halved in more than a decade with 85% of capacity now concentrated in China, Korea and Japan . Other countries in Asia are taking note as the need to transport energy and defend supply chains rises. Another positive effect is that the industry helps raise employment locally. In the medium term, as energy supply chains rewire and diversify in Asia towards the US, LatAm and Africa for natural gas, LPG, oil and fertilizers, the miles travelled to ship energy will rise given the distance from the US to Asia, materially higher than from the Middle East to Asia. Undersupply of vessels could sustain for longer than expected, driving elevated asset returns, and an orderbook upcycle.

We have seen new tanker contracts surging in 4M26, but the orderbook/fleet ratio remains lower versus the ratio of vessels older than 20 years/total capacity, highlighting a significant capex cycle ahead for shipyards. As distances rise with Asia diversifying its energy sources, we will need more vessels (especially given the percentage of vessels older than 20 years, which may also need to be demolished). We see a mild probability that the tanker orderbook/fleet ratio could double by 2030 from the end-2025 level, as a combination of old fleet demolitions and new fleets serving longer distances comes into play. ( Exhibit 177 )

M

The Supply Chain Paradox: A Solution to Energy Independence

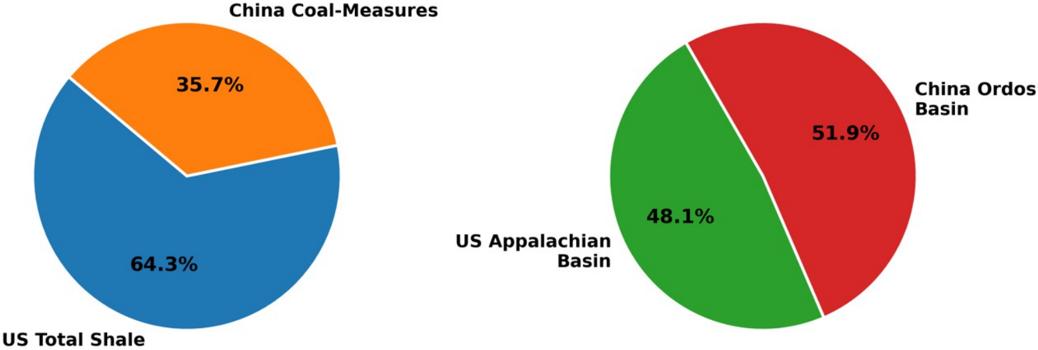

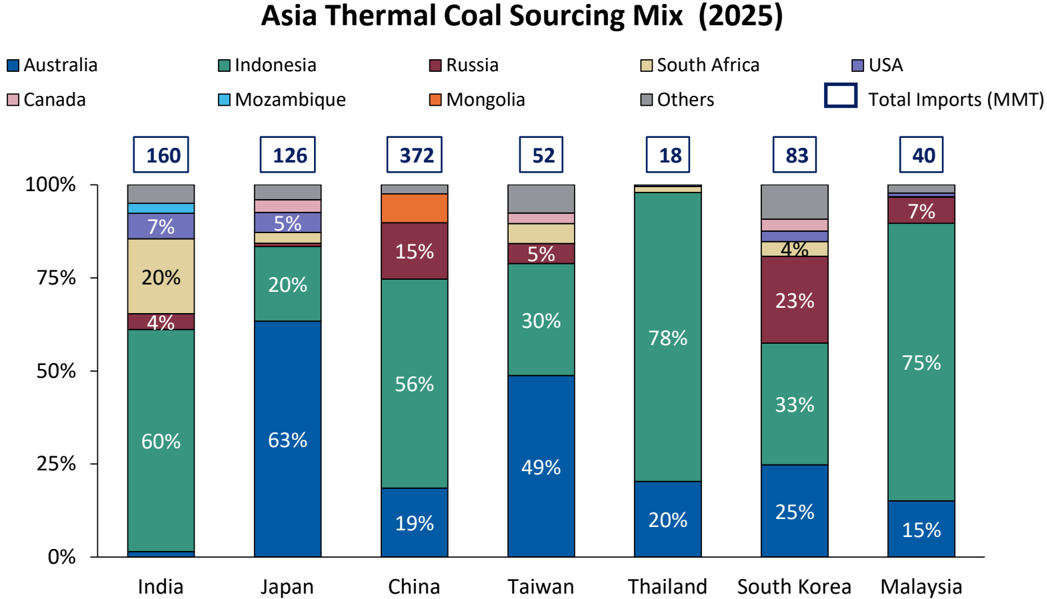

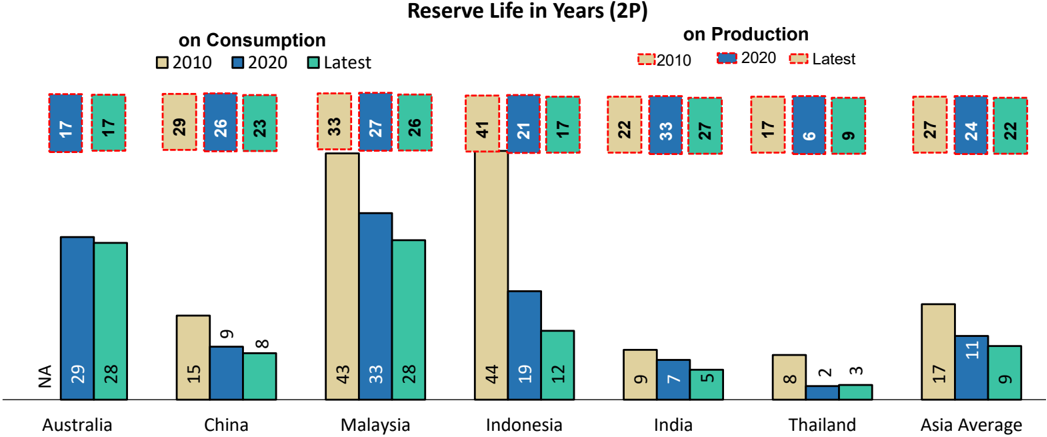

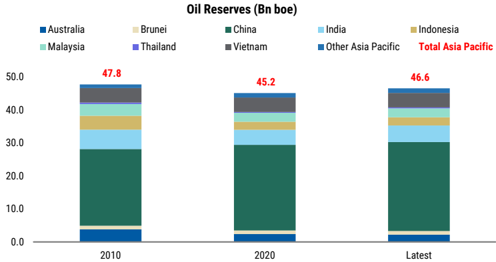

Asia consumes as much energy as the rest of the world and imports about a third of its needs ( Exhibit 10 ). While we expect the US$1tn+ of new investments and the total of US$5tn+ of investments will reduce dependence on imports, with energy imports accounting for a third of new energy consumption, not all is the same across Asia.( Exhibit 19 ). However, there are inherent geographical paradoxes in supply chains which countries have to overcome. Australia and Indonesia have significant hydrocarbon reserves but unfavourable economics have resulted in slower production and insufficient infrastructure to refine them. This is essential as they are also the largest metal ore producers and refiners. Similarly, India is the fastest-growing energy consumer globally but does not have enough oil and natural gas with limited upstream spending for the past decade due to lackluster energy pricing policies. India, Indonesia and China are also home to nearly 60% of global coal reserves ( Exhibit 19 ). Indonesia and Malaysia are the largest exporters of palm oil, which is used for gasoline/diesel fuel blending.

We see new supply chains emerging to solve for these paradoxes in each economy's energy needs, based on coal (using coal gasification), increased biofuels use and batteries, along with storage and new infrastructure development in energy.

Energy supply chains are increasingly exposed and need fortification within Asia and increasingly from the Americas. Fragmentation in the global system and rising trade uncertainty coexist with an ever -greater reliance on cross -border energy flows, as abundant supplies of oil, solar equipment, batteries and soon LNG

continue to move internationally. Yet energy dependency remains a structural weakness across much of Asia. Despite repeated energy shocks over the past two decades, investment has been fragmented, largely private -led, slow to execute, and matched by reactive - rather than forward -looking - policy responses. The current shock has laid bare the depth and diversity of these dependencies.

The imbalance is uneven. Countries such as India, Japan, South Korea and Thailand have built sufficient refining capacity but remain heavily reliant on imported upstream energy. Conversely, Australia, Indonesia and Malaysia are resource -rich upstream but poor economics caused underinvestment in production and downstream refining, with projects often delayed or scaled back. Further downstream, integration into petrochemicals and fertilizers remains patchy, leaving major economies like India and Indonesia structurally import -dependent despite capacity additions.

At the same time, baseload power investment declined across much of Asia in the past decade , following overcapacity in markets such as the Philippines, Singapore and Malaysia, excess capacity in Japan and Taiwan, and rapid renewable expansion in China and India. That backdrop has now reversed. AI, electrification and onshoring have tightened power markets sharply, prompting regulators over the past three years to recommit to baseload generation and grid capex. We see the next investment cycle driven by policy efforts to diversify generation mixes and reduce reliance on single fuels, as electricity becomes the dominant form of energy consumption across modern economies.

M

Exhibit 19: Asia: 2007 vs. 2024 - How energy dependency has evolved

| China | China | India | India | Japan | Japan | South Korea | South Korea | Taiwan | Taiwan | Australia | Singapore | Malaysia | Indonesia | Thailand | Philippines | Vietnam | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Coal | 2006 | 2024 | 2006 | 2024 | 2006 | 2024 | 2006 | 2024 | 2006 | 2024 | 2006 | 2024 | 2006 2024 | 2006 | 2024 | 2006 | 2024 | 2006 2024 | 2006 | 2024 | 2006 | 2024 | |

| %ofEnergy Basket | 76% | 58% | 55% | 59% | 21% | 28% | 25% | 22% | 35% | 33% 46% | 28% | 0% 0% | 10% | 23% | 14% | 12% | 22% | 43% 16% | 39% | 22% | 54% | ||

| Import dependancy (% of consumption) | 9% | -3% | 10% | 21% | 99% | 100% | 98% | 100% | 100% | 100% Exporter | Exporter | 100% 100% | 100% | 100% | 57% | 78% | Exporter Exporter | 100% | 100% | Exporter | 59% | ||

| Upstream Oil | |||||||||||||||||||||||

| %ofEnergy Basket | 18% | 20% | 33% | 28% | 47% | 39% | 46% | 42% | 45% 37% | 34% | 41% | 86% 87% | 42% | 38% | 52% | 47% | 47% | 29% | 44% | 38% | 49% | 31% | |

| Import dependancy (% of consumption) | 49% | 74% | 72% | 87% | 100% | 100% | 100% | 100% | 100% 100% | 41% | 66% | 100% 100% | -6% | 43% | 66% | 72% | 17% | 62% | 100% | 100% | Exporter | 75% | |

| Strategic Reserves (mn barrels of oil) | ~100 | 1,100-1,400 | Minimal | ~150 | ~500 | ~470 | 200-250 | ~400 | ~27 40-50 | 3-5 | 4-10 | 20-30 30-40 | Minimal | 20-40 | 60 days | 60-70 days | Minimal | 10-20 | Minimal | 10-30 | Minimal | 10-20 | |

| Fuel | |||||||||||||||||||||||

| Fuel Import Dependancy (Oil demand vs Fuel Refining capacity) | Exporter | Exporter | Exporter | Exporter | 14% | 9% | Exporter | Exporter | Exporter Exporter | 82% | 22% | Exporter | 13% | 80% | Exporter | Exporter | 1% | 18% | 23% | 3% | 63% | 96% | 48% |

| Refining Capacity (mbpd) | 9.2 | 18.5 | 2.9 | 5.2 | 4.6 | 3.0 | 2.6 | 3.4 | 1.1 1.1 | 0.7 | 0.2 | 1.4 | 1.3 | 0.5 | 1.2 | 1.1 | 1.2 | 1.0 | 1.3 | 0.3 | 0.2 | 0.0 | 0.4 |

| Gas | |||||||||||||||||||||||

| %ofEnergy Basket | 3% | 10% | 8% | 7% | 14% | 20% | 12% | 17% | 9% 24% | 18% | 24% | 14% | 12% | 47% | 35% | 32% | 35% | 25% | 15% | 8% | 5% | 22% | 5% |

| Gas Import dependancy (% of consumption) | 0% | 43% | 21% | 54% | 100% | 100% | 100% | 100% | 100% 100% | Exporter | Exporter | 100% | 100% | Exporter | Exporter | 24% | 41% | Exporter | Exporter | 100% | 100% | 0% | 0% |

| Chemicals | |||||||||||||||||||||||

| Ethylene Capacity | 9.0 | 59.8 | 3.0 | 8.7 | 8.0 | 6.8 | 6.1 | 12.9 | 2.7 4.0 | 0.5 | 0.0 | 1.9 | 4.1 | 1.7 | 3.1 | 2.3 | 5.4 | 0.5 1.4 | Nil | 0.5 | Nil | 1.0 | |

| Ethylene Import dependancy (% of consumption) | 48% | 42% | 42% | 44% | 47% | 31% | 50% | 28% | 59% 43% | 34% | 100% | 47% | 33% | 42% | 20% | 48% | 35% | 72% | 54% | 100% | 31% | 100% | Balanced |

| PE Capacity | 6.4 | 39.1 | 2.0 | 6.9 | 3.7 | 3.2 | 4.0 | 8.1 | 1.4 1.5 | 0.4 | 0.0 | 1.3 | 2.8 | 1.1 | 1.8 | 2.0 | 4.1 | 0.8 | 1.2 | 0.2 | 0.6 | Nil | 1.0 |

| PE Import dependancy (% of consumption) | 44% | 14% | 3% | 24% | -28% | -48% | -117% | -241% | -80% -92% | 31% | 100% | -907% -1937% | -23% | -30% | -76% | -141% | 15% | 41% | 52% | 19% | 100% | 61% | |

| Fertilisers | |||||||||||||||||||||||

| Fertiliser consumption (as %offertiliser production) | Exporter | Exporter | 153% | 139% | 121% | 144% | 238% | Increased | NA NA | 225% | 410% | NM NM | 288% | 256% | 1306% | 423% | 109% | 122% | 292% | 459% | 266% | 121% | |

| Urea Import dependancy | Exporter | Exporter | 16% | 22% | 100% | 49% | 100% | 100% | NA 100% | 80% | 100% | 100% | 100% | 36% 41% | 100% | 100% | 0% | 1% 83% | 100% | 82% | 19% | ||

| Power Grid Equipment Manufacturing | Exporter | Exporter | Importer | Exporter | Importer | Exporter | Importer | Exporter | Importer Importer | Importer | Importer | Importer | Importer | Importer | Importer | Exporter | Importer | Importer | Importer | Importer | Importer | Importer | Importer |

| Solar Module Manufacturing (Module) | Exporter | Exporter | Importer | Exporter | Exporter | Importer | Importer | Importer | Importer Importer | Importer | Importer | Importer Importer | Importer Importer | Importer | Exporter Importer | Importer | Importer | Importer | Exporter | Exporter |

Source: FOA, UN Trade, BP Statistics, World Trade, Morgan Stanley Research

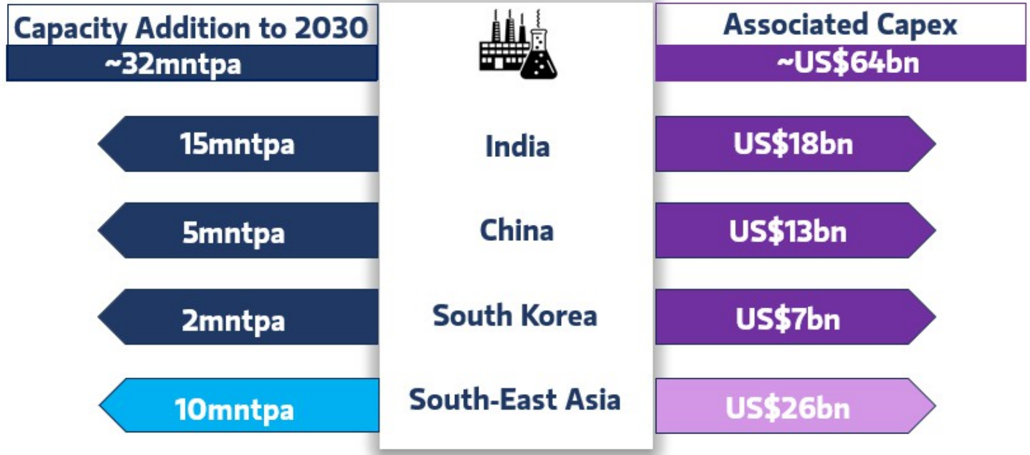

Exhibit 20: India's solar manufacturing buildout is accelerating rapidly with major players building integrated facilities

| Capacity | F27 | F27 | F27 | F27 | F28 | F28 | F28 | F28 | F28 | F28 | F28 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Company | Polysilicon (Mtpa) | Ingot | Solar cell Module | Integrated | Polysilicon | (Mtpa) | Ingot Wafer | Solar cell | Module | Integrated | Level of integration | |

| Reliance | 40,000 | 20.0 | 20.0 | 20.0 | 40,000 | 20.0 | 20.0 | 20.0 | Polysilicon to module | |||

| Shri Sai Electricals | 5 | 5 | 5 | 10 | 10 | 10 | 10 | Polysilicon to module | ||||

| Premier Energies | 8 | 11 | 11 | 8 | 10 | 10 | 11 | 8 | Ingot to module | |||

| Mundra Solar | 30,000 | 10 | 10 | 10 | 30,000 | 10 | 10 | 10 | Polysilicon to module | |||

| Waaree Energies | 10 | 5 26 | 10 | 10 | 10 | 15 | 28 | 10 | wafer/ingot to module | |||

| Renew Power | 7 | 7 | 7 | 7 | 7 | 7 | wafer to module | |||||

| Tata Power Solar | 4 | 4 | 4 | 4 | Cell & Module | |||||||

| Renew-sys | 3 | 6 | 3 | 6 | Cell & Module | |||||||

| Vikram Solar | 12 | 21 | 12 | 12 | 21 | 6 (F29) | Module | |||||

| Saatvik Solar | 4 | 5 | 9 | |||||||||

| Goldi Solar | 4 | 14 | 4 | 14 | Cell & Module | |||||||

| Jupiter Solar | 6 | 2 | 6 | 2 | Cell & Module | |||||||

| Emmvee | 3 | 7 | 3 | 7 | Cell & Module | |||||||

| Websol | 2 | 1 | 2 | 1 | Cell & Module | |||||||

| Rayzon Solar | 12 | 12 | Module | |||||||||

| First Solar | 3 | 3 | Module - vertically integrated | |||||||||

| Others | 20 | 40 | ||||||||||

| Total | 70,000.0 | 15 | 87 171 | 58 | 70,000 | 28 | 42 | 108 | 203 | 55 |

Source: Company, Morgan Stanley Research estimates

cambil 41. vo nola laue do ellel yy securly allu leeustock alvel shicatul lake bellel slaye

M

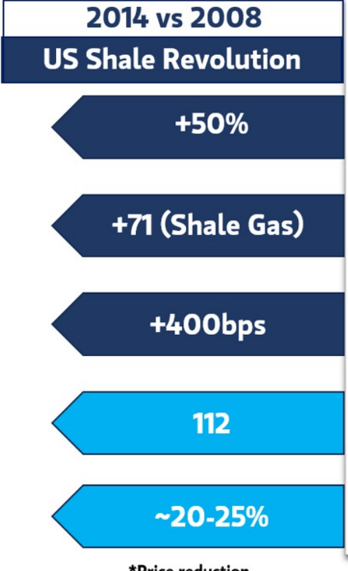

How the US can support Asia's energy diversification

US Shale Revolution

2030 vs 2025

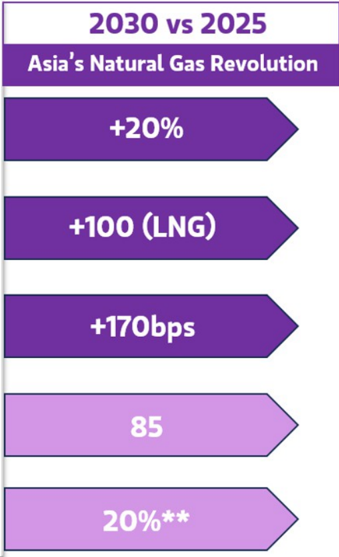

Asia's Natural Gas Revolution

Exhibit 21: US-Asia trade as energy security and feedstock diversification take center stage

+50%

Source: Morgan Stanley Research

+20% Natural Gas affordability*

Gas consumption

Growth (MTPA)

Natural Gas share in Total Energy Mix

Annual Energy Cost Savings (US$bn)

Equity Returns

Exmbles. ullculailly m supoly Chlalls lellans unuel dupleulaleu

M

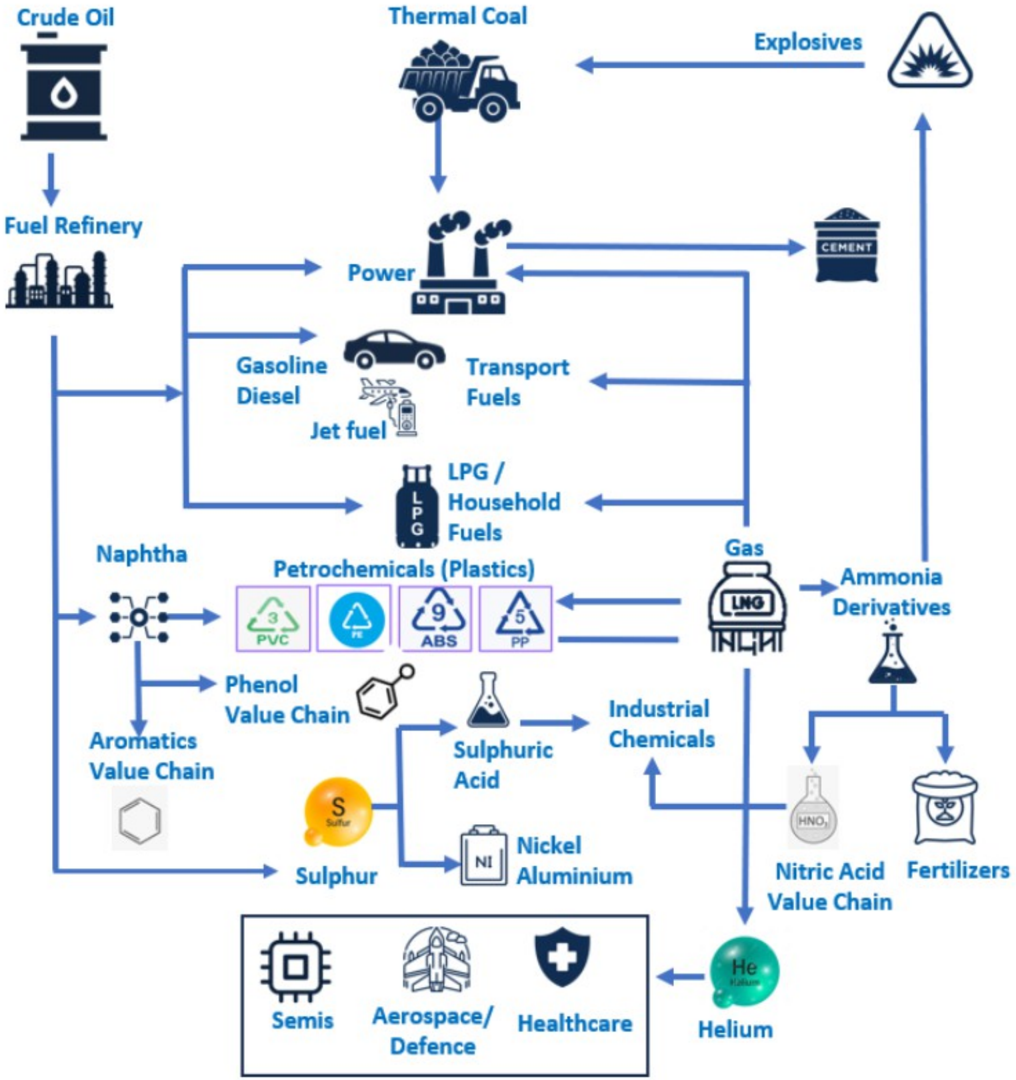

The Circularity in Energy Supply Chains

Exhibit 22: Circularity in supply chains remains underappreciated

Fuel Refinery lal

Source: Morgan Stanley Research

Explosives

M

Energy Security Beneficiaries in Multipolar World

Energy spans sectors, and securing energy for Asia has global implications, impacting equities from copper to commodity traders, to fuel refiners to fertilizers and even shipyards. We suggest owning key energy security assets - this concept is inextricably tied to AI. These include assets that give nations the ability to further energy self-sufficiency, such as nuclear, energy storage, greater local oil and natural gas production, and refining.

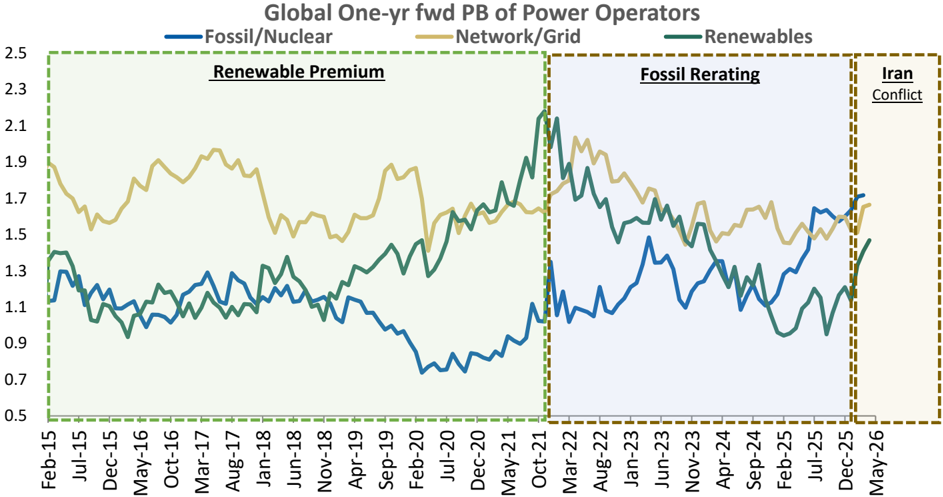

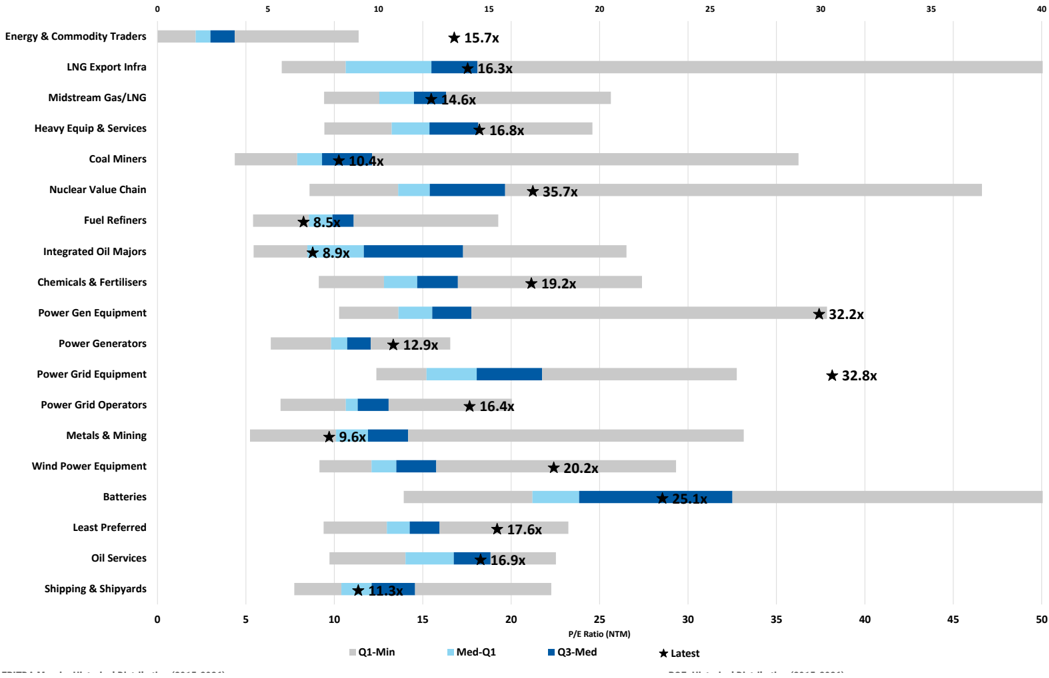

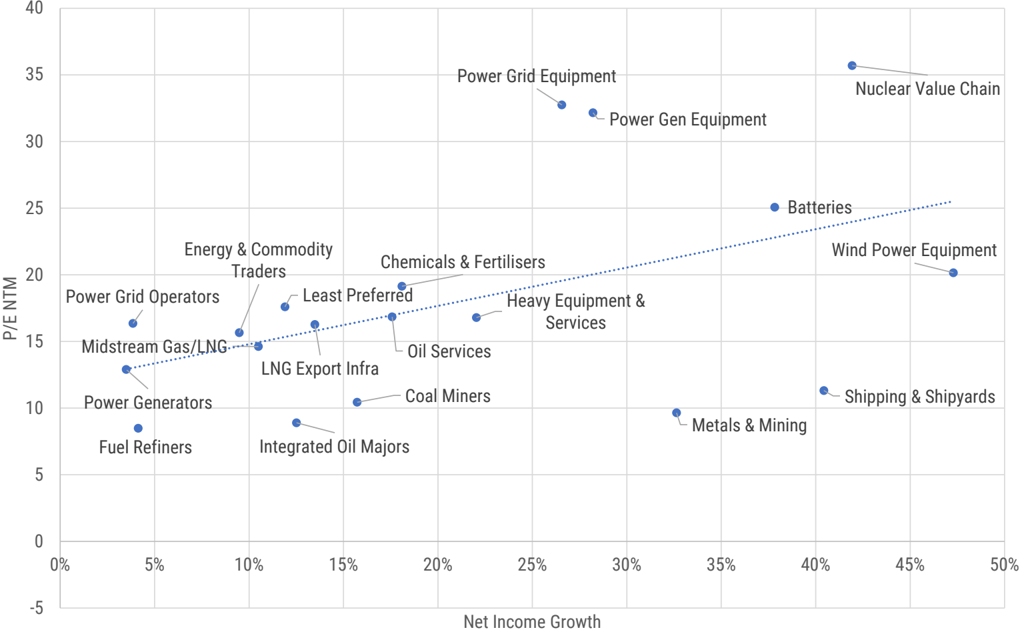

We see a nearly 1.6x torque to the value creation as US$5tn+ in investment ( Exhibit 5 ) across the Asia region ensures security of tech, AI, food and energy supply chains, unlocking US$9tn in value, we estimate. The 70+ equities we select from around the world offer US$1.5tn+ in potential enterprise value creation with 5-30% upside to Street estimates for 2028. Moreover, we believe a re-rating is in the works for energy equities in Asia as investment needs become critical, lifting returns until 2030. Historically, traditional energy corporates have been behind the curve in investing long-cycle capex, which has helped them earn 14-18% through-cycle returns as they capture multi-year margin expansion, something we believe is already being priced into equities via multiples for coal power generators, coal equipment companies, upstream oil & gas producers and fuel refiners.

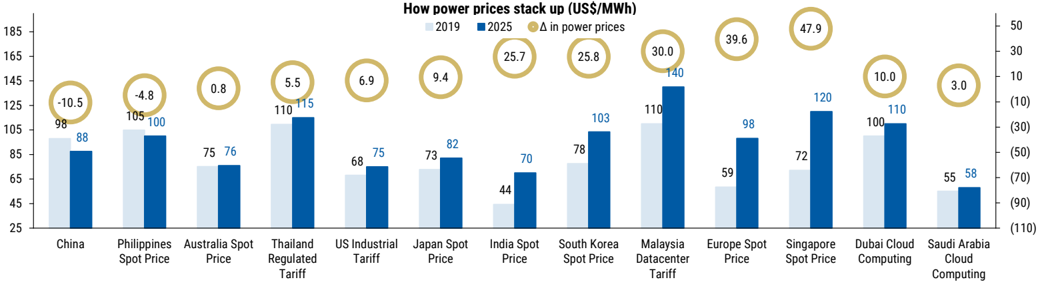

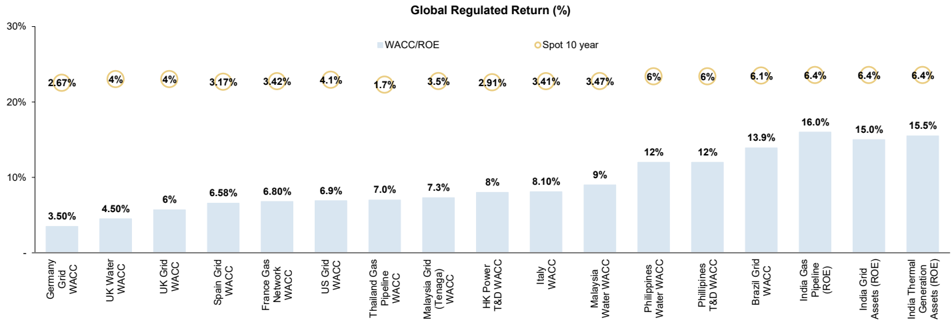

The acceleration of this investment will be catalyzed by: 1) higher fuel cracks, power prices, shipping rates, fertilizer prices and even chemical spreads, all of which we expect will remain 1.2-1.5x above midcycle levels while consumption growth stresses existing infrastructure. On average, building these projects is a 5-year cycle, and hence immediate acceleration of investment is becoming the need of the hour. With industry and transport power consumption rising nearly 80% in the past 15 years, we see pricing power for these investments, especially as AI becomes a large part of consumption growth for power. 2) Regulated returns will see a higher spread over cost of capital as the need for power grids, gas pipelines and storage terminals, along with power plants, becomes more acute. We also see governments subsidizing these investments by providing cheaper capital and also subsidies for end-consumers.

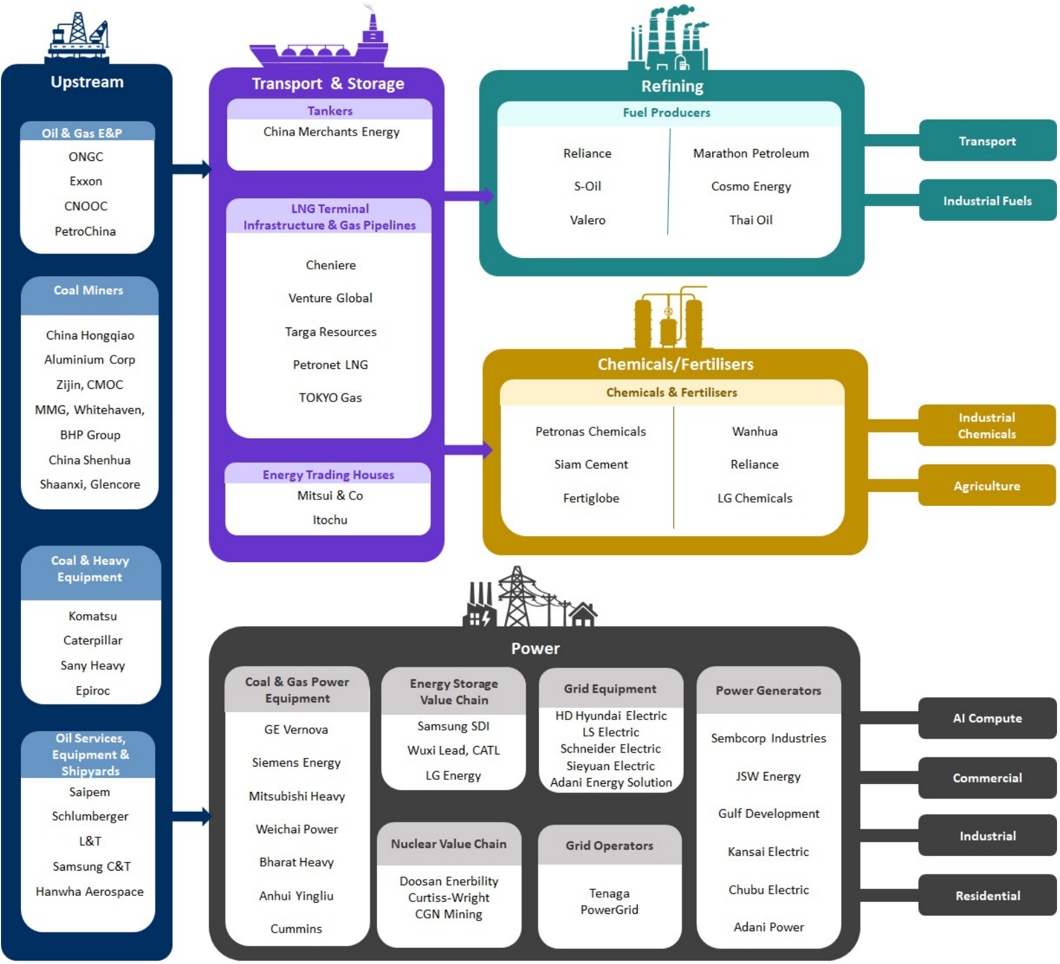

cambit do. chelyy secury. Mappily the value Chall anu wile bellello

M

Tankers

Exhibit 23: Energy security: Mapping the value chain and who benefits

China Hongqiao

Aluminium Corp

MMG, Whitehaven,

Shaanxi, Glencore

Hanwha Aerospace

Source: Morgan Stanley Research

Refining

Fuel Producers

Transport

M

Exhibit 24: Energy Security: The Beneficiaries

| Sub-Theme | Why Energy Security Benefits It | What Problem It Solves | Who Benefits Most (Public Equities) | Timing of Benefits |

|---|---|---|---|---|

| Power Infrastructure | Enhances diversification of power generation sources and improves flexibility of system | Transmission congestion, data-center interconnections, renewable curtailment, system stability. | Weichai Power, Mitsubishi Heavy GE Vernova, Siemens Energy; BHEL, Cummins, regulated utilities with transmission capex. | Near-term orders (OEMs) →long-term regulated returns (utilities). |

| Battery Storage | Energy security requires dispatchable power without fuel imports; storage turns intermittent supply into reliable capacity. | Peak demand, grid balancing, renewable intermittency, LNG volatility. | Exide, LG Energy Solution, CATL. | Near-term deployment surge →medium-term manufacturing scale. |

| Strategic Reserves (Oil, Gas, LNG) | Physical availability trumps price during crises; reserves buffer geopolitical shocks. | Supply disruptions, embargoes, price spikes. | Vopak; Indian Oil, Bharat Petroleum, Petrochina | Capacity build-out first →steady utilization over decades. |

| Coal Equipment | Domestic coal provides secure, dispatchable baseload when gas imports are volatile; acts as a bridge while grids and storage mature. | Baseload reliability, fuel import dependence. | BHEL, Doosan Enerbility; Chinese OEMs, Komatsu, Caterpillar | 2025-2030 build cycle; fades post-2030. |

| LNG Infrastructure | Diversification of supply routes and storage reduces dependence on single regions even if spot prices fall. | Import flexibility, regional gas shortages. | Cheniere Energy; Petronet LNG, Mitsui & Co, Marubeni | Near-term U.S. exports →medium-term Asian import/storage. |

| Power Generators (Utilities/IPPs) | Rising electricity demand (AI, electrification) makes reliable generation capacity strategic. | Load growth, 24/7 power for data centers and industry. | Gulf Development, Sembcorp Industries, NTPC, Hokkaido Electric | Immediate demand growth →long-duration rate-base compounding. |

| Renewable Equipment | Energy security pushes scale and domestic supply chains, even if margins fluctuate. | Fuel import reduction, long-term energy independence. | Vestas, Siemens Energy; Chinese OEMs for volume, Dajin Heavy | Medium-term volume growth; margins vary with cycle. |

| Shipping | Energy sourcing divesification leads to longer distances and ened for more crude tankers and LPG ships | Supprts Diversification of energy sourcing | Samsung C&T, COSCO Energy Shipping, Mitsui O.S.K Lines, China Merchants Shipping, Hanwha Aerospace | Starting 2026 |

| Metals | Demand for steel, copper, nickel picks up for new energy infrastructure and power | Power shortages and fuel availability | JSW Steel, BHP Group, Chalco, Jiangxi Copper | Demand pickup already starting to happen |

| Fuel Refiners | Higher fuel consumption help higher diesel, jet fuel, plastics and gasoline margins | Fuel shortages for transportation | Reliance, Thai Oil, S-Oil, PTT Global Chemicals,Valero, Marathon | Fuel Supply tightness started in 2025, gets worse in 2026-2028 |

| Chemicals | Shoratges in Sulphuric acid, urea, DAPandHelium | Crop yields, chips etching, metal ore processing | Siam Cement, PTT Global Chemicals, Mitsui Chemicals, Sinopec, Petronas Chemicals, Deepak Nitrite, Navin Fluorine | Medium term challenge |

Source: Morgan Stanley Research

While we see significant energy security tailwinds across Asia's energy value chain, our bottom-up research highlights several subsectors that look challenged:

Clean power equipment supply chain: China's solar supply chain remains significantly oversupplied with current manufacturing capacity nearly double current global demand. Although we do see a pickup in renewable deployment, the depth of the oversupply, as well as increasing competition from the onshoring of the solar value chain such as in India, will likely challenge profitability in the near to medium term.

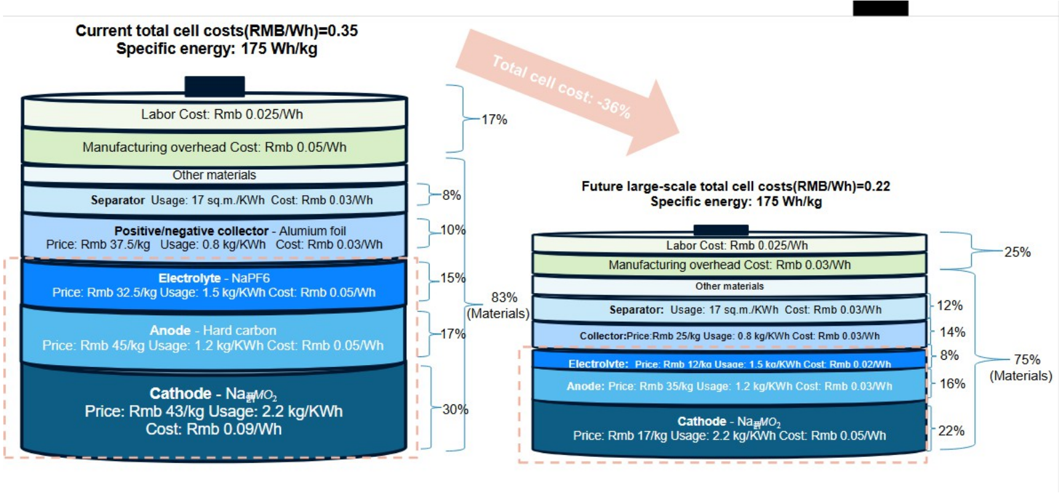

Battery components: Similar to China's solar value chain, selected battery components remain in oversupply. Based on our utilization forecasts and assessment of current valuations at a reasonable profitability level, our order of preference is LiPF6 (electrolyte) > separator > LFP cathode > anode > NCM cathode.

Power generators: While we are positive on power generation names, we see challenges in geographies where we see power spread headwinds, limited volume growth and high curtailment of renewables.

M

Exhibit 25: Asia Energy Security: Our 70 Global picks and 18 least preferred

| BBGTickers | CompanyName | Ticker | Market cap, current,USD(MM) 3MADTV, USD(MM) | Rating | Share price, last close Price Target (Local CCY) %Upside fromlast close | Country | MSAnalyst | MSAnalyst |

|---|---|---|---|---|---|---|---|---|

| MostPreferred Integrated Oil Majors | ||||||||

| 883HK 601857CG | CNOOC PetroChina | 0883.HK 601857.SS | 156,765.5 547.1 275,267.5 524.4 | Overweight Overweight | 27.56HKD 28.90HKD 4.9% 11.56 14.70 27.2% | China China | Jack Lu Jack Lu | Jack Lu Jack Lu |

| ONGCIS XOMUN | Oil &NaturalGas Corp. Exxon Mobil Corporation | ONGC.NS XOM.N | 38,715.6 68.5 673,761.2 783.2 | Overweight Overweight | 296.50 363.00 22.4% 157.92 171.00 8.3% United | India States of America | Mayank Maheshwari Devin McDermott | Mayank Maheshwari Devin McDermott |

| Fuel Refiners | ||||||||

| RIL IS | Reliance Industries | RELI.NS | 185,785.3 292.9 | Overweight | 1,322.70 1,803.00 36.3% 110,100.00 130,000.00 18.1% Korea; | India | Mayank Maheshwari | Mayank Maheshwari |

| 010950 KP TOPTB | S-Oil Thai Oil PublicCompany | 010950.KS TOP.BK | 8,323.7 80.6 3,226.5 31.3 | Overweight Overweight | 47.00 58.00 23.4% | Republic (S. Korea) Thailand | Young Suk Shin Mayank Maheshwari | Young Suk Shin Mayank Maheshwari |

| 5021 JP VLOUN | CosmoEnergyHoldings Valero Energy Corporation | 5021.T VLO.N | 3,921.6 22.7 77,980.5 235.8 | Overweight Equal-Weight | 3,774.00 5,250.00 39.1% 262.62 232.00 -11.7% United | Japan States of America | Reiji Ogino Joe Laetsch | Reiji Ogino Joe Laetsch |

| MPCUN | Marathon Petroleum Corp Chemicals& Fertilisers | MPC.N | 76,785.2 187.3 | Overweight | 263.02 233.00 -11.4% United | States of America | Joe Laetsch | Joe Laetsch |

| SCCTB | Siam Cement | SCC.BK | 8,297.5 42.8 11,353.8 26.8 | Overweight | 225.00 270.00 20.0% 5.59 6.24 11.6% | Thailand | Mayank Maheshwari | Mayank Maheshwari |

| PCHEMMK 051910 KP | Petronas Chemicals Group Berha LGChem | PCGB.KL 051910.KS | 16,615.0 93.2 | Overweight Equal-Weight | 374,000.00 430,000.00 15.0% Korea; | Malaysia Republic (S. Korea) | Mayank Maheshwari Young Suk Shin | Mayank Maheshwari Young Suk Shin |

| FERTIGLBDH | FertiglobePLC WanhuaChemical | FERTIGLB.AD 600309.SS | 7,639.7 7.8 36,598.9 473.0 | Overweight Overweight | 3.37AED 3.80AED 12.8% United 81.81 101.00 23.5% | Arab Emirates | Ricardo Rezende KayleeXu | Ricardo Rezende KayleeXu |

| 600309CG | Chemicals& Fertilisers | China | ||||||

| GEVUN ENRGY | GEVernova Siemens EnergyAG | GEV.N ENR1n.DE | 271,890.9 478.1 167,570.6 513.4 | Overweight Overweight | 1,049.23 1,250.00 19.1% United 167.70 200.00 19.3% | States of America Germany | David Arcaro Max Yates | David Arcaro Max Yates |

| 7011 JT | Mitsubishi Heavy Industries | 7011.T | 87,638.8 747.7 | Overweight | 4,126.00 5,500.00 33.3% 401.10 | Japan | Takeshi Kitaura | Takeshi Kitaura |

| BHELIS 000338CS | Bharat Heavy Electricals Ltd WeiChai Power | BHEL.NS 000338.SZ | 14,496.4 59.4 33,000.6 541.3 | Overweight | 444.00 10.7% 33.15 43.00 29.7% | India China | Girish Achhipalia Sheng Zhong | Girish Achhipalia Sheng Zhong |

| 603308CH | Anhui Yingliu Electromechanical | 603308.SS | 7,299.7 233.1 | Overweight Overweight | 73.74 101.20 37.2% | China | TomLi | TomLi |

| CMIUS | CumminsInc Power Generators | CMI.N | 90,998.3 141.5 | Overweight | 696.53 752.00 8.0% United | States of America | Angel Castillo | Angel Castillo |