PDF 原檔:報告_GF_ASML_20260715_original.pdf

報告日期:內文未列明確發布日期,依 PDF 檔案 metadata CreationDate(2026-07-15T15:10 UTC)認定;內容數字(2Q26營收€9.3bn、EPS €7.58)與 CTBC 2026-07-16 報告一致,應屬 ASML 2Q26 法說當週同批報告。

圖片清單(已驗證 2026-07-17)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

GF - ASML 2Q26 Review_002.png |

52.6KB | 真資料圖 | Forward P/E 歷史區間圖:橫軸 2025-01 至 2026-06,股價/倍數曲線從約 23 上升至 2026 年中約 40-45,圖上有多條不同色階水平帶線(表示不同 P/E 倍數區間) |

GF - ASML 2Q26 Review_001.png |

23.8KB | 未 Read(<40KB,預設 logo/版面裝飾) | — |

原始內容

ASML Holding (ASML US)

2Q26 Review: WFE strength continues

Guidance raised; TP $2,571: ASML reported 2Q26 revenue of €9.3bn with a gross margin of 54%. Management raised its 2026 full-year revenue guidance to €43-45bn (from €3640bn) with a gross margin outlook of 54-56%, supported by stronger demand from both logic and memory. We believe the earnings and margin upside is driven not only by robust endmarket demand but also by pin-to-pin price increases and old model upgrade. We remain bullish on ASML's demand outlook and continue to see capacity upside as the company works to diversify its supply chain beyond Zeiss. Accordingly, we raise our 2026/2027 EPS forecasts to €38.88/54.46, and our target price of $2,571 is based on 40x 2027E P/E unchanged.

Likely a 300bn WFE in 2028: We forecast global WFE to reach $163bn in 2026, accelerating to $236bn in 2027 and $295bn in 2028, representing the strongest WFE upcycle on record. We believe the current cycle is supported by: 1) Stronger visibility into memory capex: Samsung/SK's capex is projected to reach ₩100tn/70tn by 2028, followed by an estimated ~20% CAGR through 2033; 2) incremental demand from Terafab; 3) A more constructive outlook for TSMC's capex, for which we forecast $57bn/75bn in 2026/2027; 4) Intel's capacity expansion, including ~35kpm for Intel 3 and ~ 40kpm for 18A between late 2026 and 2028, alongside an accelerated 14A ramp; and 5) continued strength in China's demand.

Capacity expansion becoming increasingly visible: Management indicated that both EUV and immersion DUV production capacity are expected to expand by ~30% annually in both 2027 and 2028, implying annual output of ~85/110 EUV systems and ~169/220 immersion DUV systems, respectively. Our checks indicate customer demand has already exceeded 110 EUV systems for 2028, while ASML continues to explore alternative lens suppliers beyond Zeiss to alleviate supply constraints. Although achieving 120 EUV systems in 2028 remains challenging, we still see upside potential to management's existing guidance.

Risks: 1) AI demand deceleration; 2) Geo-political uncertainties; 3) Competition.

| Profit forecast (EUR to USD 1.18) | FY2023 | FY2024 | FY2025 | FY2026E | FY2027E |

|---|---|---|---|---|---|

| Revenue (m) | 27,559 | 28,263 | 32,667 | 44,074 | 57,325 |

| Revenue YoY ( % ) | 30.2% | 2.6% | 15.6% | 34.9% | 30.1% |

| Net profit (m) | 7,839 | 7,572 | 9,609 | 14,936 | 20,838 |

| Net profit YoY ( % ) | 39.4% | -3.4% | 26.9% | 55.4% | 39.5% |

| EPS ($) | 19.89 | 19.24 | 24.72 | 38.88 | 54.46 |

| P/E | 75.7 | 78.2 | 60.90 | 38.71 | 27.6 |

| ROE ( % ) | 114.6% | 35.9% | 48.8% | 65.3% | 56.0% |

Source: Company data, GF Securities (Hong Kong) Brokerage.

Please be sure to read the disclosures at the end of this report carefully .

数据来源:公司财务报表,广发证券发展研究中心

Yang Zhou

SFC CE No. BSF949 zhouyang@gfgroup.com.hk

Jeff Pu, CFA SFC CE No. BNO719 jeffpu@gfgroup.com.hk

Michelle Jing SFC CE No. BUK594 michellejing@gfgroup.com.hk

Earnings Review

2Q26 results review

ASML reported 2Q26 revenue of €9.3bn EUR, +6.4% QoQ and +21.3% YoY. By segment, net system sales reached €6.6bn EUR, +4.5% QoQ and +17.3% YoY; net service & field option sales reached €2.8bn EUR, +11.0% QoQ and +31.8% YoY. 2Q26 gross profit margin was 54.0%, up 1ppt QoQ, up 0.3ppt YoY; and operating profit margin was 37.0%, up 1.1ppt QoQ, up 2.4ppt YoY. Diluted EPS was €7.58.

We forecast revenue of €44/57bn EUR in 2026/2027

We revise ASML's earnings forecast for 2026/2027 to €44.1/57.3bn EUR, with net profit of €14.9/20.8bn EUR and EPS of €38.88/54.46 EUR, respectively.

Figure 1: Earnings revision (mn EUR)

| FY2025 | FY2026E | FY2026E | FY2027E | FY2027E | Change (%) | Change (%) | |

|---|---|---|---|---|---|---|---|

| Old | New | Old | New | FY2026E | FY2027E | ||

| Net sales | 32,667 | 40,555 | 44,074 | 50,922 | 57,325 | 8.7% | 12.6% |

| Gross profit | 17,258 | 21,250 | 24,273 | 27,300 | 32,648 | 14.2% | 19.6% |

| Op. profit | 11,302 | 14,971 | 17,612 | 20,164 | 24,799 | 17.6% | 23.0% |

| Pre-tax Income | 11,406 | 15,214 | 17,761 | 20,478 | 24,958 | 16.7% | 21.9% |

| Net profit | 9,609 | 12,909 | 14,936 | 17,239 | 20,838 | 15.7% | 20.9% |

| Key ratios (%) | |||||||

| Gross margin | 52.8% | 52.4% | 55.1% | 53.6% | 57.0% | ||

| Operating margin | 34.6% | 36.9% | 40.0% | 39.6% | 43.3% | ||

| Net profit margin | 29.4% | 31.8% | 33.9% | 33.9% | 36.4% |

Sources: Company data, GF Securities (Hong Kong) Brokerage

Figure 2: ASML's P&L Forecast

| (EUR m) | FY25 | 1Q26 | 2Q26 | 3Q26E | 4Q26E | FY26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | FY27E |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 32,667 | 8,767 | 9,327 | 11,906 | 14,074 | 44,074 | 11,559 | 13,214 | 15,370 | 17,181 | 57,325 |

| COGS | -15,409 | -4,122 | -4,291 | -5,214 | -6,174 | -19,800 | -5,078 | -5,706 | -6,585 | -7,308 | -24,677 |

| Gross profit | 17,258 | 4,645 | 5,035 | 6,692 | 7,901 | 24,273 | 6,482 | 7,508 | 8,786 | 9,873 | 32,648 |

| Opex | -5,957 | -1,487 | -1,579 | -1,667 | -1,928 | -6,662 | -1,711 | -1,943 | -2,014 | -2,182 | -7,849 |

| Operating profit | 11,302 | 3,158 | 3,456 | 5,025 | 5,972 | 17,612 | 4,771 | 5,566 | 6,772 | 7,691 | 24,799 |

| Non-op profit | 105 | 41 | 30 | 45 | 34 | 150 | 28 | 45 | 43 | 43 | 159 |

| Pre-tax profit | 11,406 | 3,199 | 3,486 | 5,070 | 6,007 | 17,761 | 4,799 | 5,610 | 6,815 | 7,734 | 24,958 |

| Income tax | -2,013 | -547 | -610 | -887 | -1,050 | -3,093 | -839 | -981 | -1,192 | -1,352 | -4,364 |

| Non-GAAP Net Income | 9,609 | 2,757 | 2,918 | 4,245 | 5,016 | 14,936 | 4,020 | 4,693 | 5,684 | 6,440 | 20,838 |

| Diluted EPS (€) | 25 | 7.15 | 7.58 | 11.04 | 13.06 | 39 | 10.48 | 12.24 | 14.84 | 16.83 | 54 |

| Diluted shares | 387 | 386 | 385 | 385 | 384 | 384 | 384 | 383 | 383 | 383 | 383 |

| Margin analysis | |||||||||||

| Gross margin | 52.8% | 53.0% | 54.0% | 56.2% | 56.1% | 55.1% | 56.1% | 56.8% | 57.2% | 57.5% | 57.0% |

| Operating margin | 34.6% | 36.0% | 37.1% | 42.2% | 42.4% | 40.0% | 41.3% | 42.1% | 44.1% | 44.8% | 43.3% |

| Pre-tax margin | 34.9% | 36.5% | 37.4% | 42.6% | 42.7% | 40.3% | 41.5% | 42.5% | 44.3% | 45.0% | 43.5% |

| Effective tax rate | 17.7% | 17.1% | 17.5% | 17.5% | 17.5% | 17.4% | 17.5% | 17.5% | 17.5% | 17.5% | 17.5% |

| Growth (YoY%) | |||||||||||

| Sales | 15.6% | 13.2% | 21.3% | 58.4% | 44.8% | 34.9% | 31.9% | 41.7% | 29.1% | 22.1% | 30.1% |

| Operating profit | 25.3% | 15.3% | 29.7% | 103.6% | 74.1% | 55.8% | 51.1% | 61.0% | 34.8% | 28.8% | 40.8% |

| Net income | 26.9% | 17.1% | 27.4% | 99.8% | 76.7% | 55.4% | 45.8% | 60.9% | 33.9% | 28.4% | 39.5% |

| EPS | 28.5% | 19.1% | 28.5% | 101.4% | 78.0% | 57.3% | 46.6% | 61.5% | 34.4% | 28.9% | 40.1% |

Sources: Company data, GF Securities (Hong Kong) Brokerage

Valuation and Recommendation

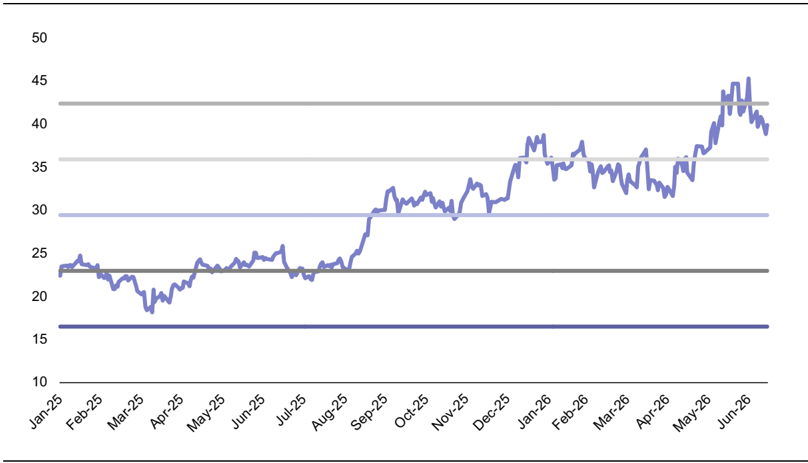

Maintain Buy with TP of $2,571

We remain bullish on ASML's demand outlook and continue to see capacity upside as the company works to diversify its supply chain beyond Zeiss. Accordingly, we raise our 2026/2027 EPS forecasts to €38.88/54.46, and our target price of $2,571 is based on 40x 2027E P/E unchanged.

Figure 3: ASML's Historical Forward P/E

Sources: Company data, GF Securities (Hong Kong) Brokerage

Risks

- 1) AI demand deceleration; 2) Geo-political uncertainties; 3) Competition.

| Balance Sheet | [Table_FinanceDetail] | EUR m | |||

|---|---|---|---|---|---|

| FY23 | FY24 | FY25 | FY26E | FY27E | |

| Current assets | 24,394 | 30,357 | 30,241 | 35,377 | 49,116 |

| Cash and cash equivalents | 7,010 | 12,741 | 13,322 | 4,281 | 12,315 |

| Inventory | 8,851 | 10,892 | 11,429 | 16,890 | 19,993 |

| Accounts Receivable | 5,713 | 4,560 | 3,637 | 11,790 | 14,392 |

| Other current assets | 2,820 | 2,164 | 1,853 | 2,416 | 2,416 |

| Non-current assets | 15,564 | 22,209 | 25,336 | 20,999 | 21,776 |

| Long-term equity investment | - | - | - | - | - |

| Fixed assets | 5,493 | 6,847 | 7,894 | 8,149 | 8,925 |

| Other long-term assets | 10,070 | 15,363 | 17,443 | 12,850 | 12,850 |

| Total assets | 39,958 | 52,567 | 55,577 | 56,376 | 70,892 |

| Current liabilities | 16,275 | 20,050 | 24,439 | 23,687 | 24,589 |

| Accounts Payable | 2,347 | 3,499 | 3,522 | 4,598 | 5,443 |

| Short-term borrowings | 0 | 1,010 | 990 | 879 | 937 |

| Other current liabilities | 13,927 | 15,541 | 19,927 | 18,209 | 18,209 |

| Non-current liabilities | 10,230 | 10,495 | 6,952 | 5,318 | 4,559 |

| Long-term Debt | 4,632 | 3,677 | 2,709 | 1,067 | 309 |

| Other non-current liabilities | 5,599 | 6,818 | 4,243 | 4,250 | 4,250 |

| Total liabilities | 26,505 | 30,545 | 31,392 | 29,005 | 29,149 |

| Total Equity | 13,453 | 22,022 | 24,185 | 27,371 | 41,742 |

| Share Capital | 4,034 | 4,554 | 4,626 | 4,626 | 4,626 |

| Treasury stock | (3,306) | (476) | (2,253) | (2,253) | (2,253) |

| Retained earnings | 12,380 | 13,516 | 16,535 | 23,917 | 37,733 |

| Capital adjustment | (6,267) | 3,476 | 772 | (3,424) | (2,869) |

| Total Liabilities & Equity | 39,958 | 52,567 | 55,577 | 56,376 | 70,892 |

| Income Statement | EUR m | ||||

|---|---|---|---|---|---|

| FY23 | FY24 | FY25 | FY26E | FY27E | |

| Revenue | 27,559 | 28,263 | 32,667 | 44,074 | 57,325 |

| Cost of sales | (13,422) | (13,771) | (15,409) | (19,800) | (24,677) |

| Gross profit | 14,136 | 14,492 | 17,258 | 24,273 | 32,648 |

| Operating Expense | (5,094) | (5,469) | (5,957) | (6,662) | (7,849) |

| Operating profit | 9,042 | 9,023 | 11,302 | 17,612 | 24,799 |

| Interest Income | - | - | - | - | - |

| Interest Expense | (41) | (20) | (105) | (150) | (159) |

| Net other Non-op. Income/(Loss) | - | - | - | - | - |

| Pre-tax profit | 9,084 | 9,042 | 11,406 | 17,761 | 24,958 |

| Income tax & Income from Affiliates | 1,245 | 1,471 | 1,797 | 2,826 | 4,120 |

| Profit for the year | 7,839 | 7,572 | 9,609 | 14,936 | 20,838 |

| Minority interest | - | - | - | - | - |

| Net profit to ord. equity | 7,839 | 7,572 | 9,609 | 14,936 | 20,838 |

| EPS (€) | 19.89 | 19.24 | 24.72 | 38.88 | 54.46 |

| Cash Flow Statement | EUR m | ||||

|---|---|---|---|---|---|

| FY23 | FY24 | FY25 | FY26E | FY27E | |

| Operating cash flow | 5,443 | 11,166 | 12,659 | 1,861 | 17,654 |

| Profit for the year | 7,839 | 7,571 | 9,609 | 14,936 | 20,838 |

| Depreciation & amortization | 740 | 919 | 1,026 | 1,007 | 1,064 |

| Change in working capital | (3,664) | 2,053 | 1,027 | (14,498) | (4,861) |

| Others | 528 | 623 | 997 | 416 | 613 |

| Investing cash flow | (2,136) | (2,304) | (3,377) | (2,211) | (1,840) |

| Capex | (2,170) | (2,067) | (1,574) | (1,536) | (1,840) |

| Change in investment | (553) | (305) | (401) | (37) | 0 |

| Others | 586 | 68 | (1,402) | (638) | 0 |

| Free cash flow | 3,274 | 9,099 | 11,085 | 325 | 15,814 |

| Financing cash flow | (3,004) | (2,832) | (8,671) | (9,164) | (7,780) |

| Change in Capital | 97 | (354) | (5,808) | (3,821) | (2,868) |

| Net Change in Debt | (753) | (26) | (313) | (1,610) | (759) |

| Others | (2,348) | (2,453) | (2,550) | (3,733) | (4,154) |

| Exchange influence | (14) | 6 | (30) | 7 | 0 |

| Total cash generated | (264) | 5,731 | 180 | (9,544) | 8,033 |

| Key Financial Ratios | |||||

|---|---|---|---|---|---|

| Growth | |||||

| Revenue growth | 30.2% | 2.6% | 15.6% | 34.9% | 30.1% |

| Operating profit growth | 39.1% | -0.2% | 25.3% | 55.8% | 40.8% |

| Net profit growth | 39.4% | -3.4% | 26.9% | 55.4% | 39.5% |

| Profitability | |||||

| Gross profit margin | 51.3% | 51.3% | 52.8% | 55.1% | 57.0% |

| Operating Profit Margin | 32.8% | 31.9% | 34.6% | 40.0% | 43.3% |

| Net profit margin | 28.4% | 26.8% | 29.4% | 33.9% | 36.4% |

| Key Ratio | |||||

| ROE | 114.6% | 35.9% | 48.8% | 65.3% | 56.0% |

| ROA | 19.9% | 16.4% | 17.8% | 26.7% | 32.7% |

| Stability | |||||

| Gross debt/equity | 387.5 | 145.0 | 159.5 | 126.9 | 78.3 |

| Interest Coverage | (132.1) | (563.9) | (121.0) | (12.4) | (111.1) |

| Current Ratio | 1.5 | 1.5 | 1.2 | 1.5 | 2.0 |

| Quick Ratio | 1.0 | 1.0 | 0.8 | 0.8 | 1.2 |

| Net debt/equity | Net Cash | Net Cash | Net Cash | Net Cash | Net Cash |

Rating definitions

Benchmark: Hang Seng Index (Hong Kong)

Company ratings

Buy

Stock expected to outperform benchmark by more than 10 %

Hold

Expected stock relative performance ranges between -10 % and 10 %

Underperform

Stock expected to underperform benchmark by more than 10 %

Sector ratings

Positive

Sector expected to outperform benchmark by more than 10%

Neutral

Expected sector relative performance ranges between -10% and 10%

Cautious

Sector expected to underperform benchmark by more than 10%

Hong Kong

Company

GF Securities (Hong Kong) Brokerage Limited

Address

27/F, GF Tower, 81 Lockhart Road, Wan Chai, Hong Kong

Telephone

(852) 37191111

michellejing@gfgroup.com.hk

Disclaimer

This report has been prepared by GF Securities (Hong Kong) Brokerage Limited ('GF Securities (Hong Kong) Brokerage'). According to the laws, regulations and regulatory requirements in different countries and regions, this report is distributed by GF Securities (Hong Kong) Brokerage with relevant legal and compliant operation qualifications in these countries and regions.

GF Securities (Hong Kong) Brokerage is licensed by the Securities and Futures Commission of Hong Kong ('SFC') to conduct Type 4 Regulated Activity 'Advising on Securities'. It is regulated by the SFC, and is responsible for the distribution of this report in Hong Kong. Information about the qualifications of the research analyst(s) who is(are) the author(s) of this report as licensed by the SFC are disclosed in the section where research analyst names are shown.

The research analyst(s) primarily responsible for the content of this report, in whole or in part, certifies that with respect to the company or relevant securities that the analyst(s) covered in this report: 1) all of the views expressed accurately reflect his or her personal views on the company or relevant securities mentioned herein; and 2) no part of his or her remuneration was, is, or will be, directly or indirectly, in connection with his or her specific recommendations or views expressed in this report.

This report is published solely for information purpose and does not constitute an offer to buy or sell any securities or a solicitation of an offer to buy, or recommendation for investment in, any securities.

The securities mentioned in this report may not be allowed to be sold in certain jurisdictions. No action has been taken to permit the distribution of the research report to any person in any jurisdiction that the circulation or distribution of such research report is unlawful. This report is distributed solely to clients or designated institutions authorized by GF Securities (Hong Kong) Brokerage, and is not distributed publicly. It is distributed to certain clients based on the conclusion that they are able to assess investment risks independently, execute investment decisions independently and assume corresponding risks independently.

This report has been issued and based on information obtained from sources generally available to the public and believed by the research analyst(s) to be reliable but which has not been independently verified. No representation or warranty, either express or implied, is made by GF Securities (Hong Kong) Brokerage as to their accuracy and completeness of the information contained in this report. GF Securities (Hong Kong) Brokerage accepts no liability for all loss arising from the use of the materials presented in this report, unless is excluded by applicable laws or regulations. Please be aware of the fact that investments involve risks and the price of securities may be fluctuated and therefore return may be varied, past results do not guarantee future performance. Any recommendation contained in this report does not have regard to the specific investment objectives, financial situation and the particular needs of any individuals. This report is not to be taken in substitution for the exercise of judgment by respective recipients of this report, where necessary, recipients should obtain professional advice before making investment decisions.

GF Securities (Hong Kong) Brokerage may have issued, and may in the future issue, other communications that are inconsistent with, and reach different conclusions from, the information presented in the research report. The points of view, opinions and analytical methods adopted in the research report are solely expressed by the analysts but not that of GF Securities (Hong Kong) Brokerage or its affiliates. The information, opinions and forecasts presented in the research report are the current opinions of the analysts as of the date appearing on this material only which may subject to change at any time without notice. The salesperson, dealer or other professionals of GF Securities (Hong Kong) Brokerage may deliver opposite points of view to their clients and the proprietary trading division with respect to market commentary or dealing strategy either in writing or verbally. The proprietary trading division of GF Securities (Hong Kong) Brokerage may have different investment decision which may be contrary to the opinions expressed in the research report. GF Securities (Hong Kong) Brokerage or its affiliates or respective directors, officers, analysts and employees related to research report business may have rights and interests in securities mentioned in the research report. Recipients should be aware of relevant disclosure of interest (if any) when reading this report.

GF Securities (Hong Kong) Brokerage and its affiliates may be seeking or building business relationships with company(ies) mentioned in this report. Therefore, investors should consider the impact on the independence of this report by GF Securities (Hong Kong) Brokerage and its affiliates due to potential conflicts of interests. Investors should not make any investment decisions based solely on the contents of this report. Investors should make their own investment decisions and bear their own risk. No written or verbal commitment of sharing gains or losses from securities investments in any form shall be effective.

This report may contain and/or describe/present factual historical information on prices of Futures contracts (the 'information'). Please note that this information is solely for the purpose of forming part of the argument/grounds/evidence in our research methodology/analysis to support our conclusion on our view of the relevant industry/company mentioned. It does not, by any means (express or implied) to be associated with or constituted as SFC Type 5 Regulated Activity (Advising on futures contracts).

Disclosure of Interests

- 1) The research analyst(s) and his/her associate has not served as an officer of the company(ies) mentioned in this report, and does not have any financial interests in the company(ies) mentioned in this report.

- 2) GF Securities (Hong Kong) Brokerage and/or its affiliates does not have any financial interests and has not invested in interests aggregate to an amount equal to or more than (i) 1 % of the market capitalization; or (ii) 1 % of the issued share capital, or issued units, in the company(ies) mentioned in this report.

- 3) GF Securities (Hong Kong) Brokerage and/or its affiliates does not have any market making activities, and has not employed any individual(s) serving as officer(s) of the company(ies) mentioned in this report.

- 4) GF Securities (Hong Kong) Brokerage and/or its affiliates does not have any investment banking relationship in Hong Kong with the company(ies) mentioned in this report in the past 12 months.

Copyright © GF Securities (Hong Kong) Brokerage

Without the prior written consent obtained from GF Securities (Hong Kong) Brokerage, any part of the materials contained herein should not (i) in any forms be copied or reproduced or (ii) be re-disseminated.