PDF 原檔:報告_Daiwa_聯發科2454_20260710_original.pdf

圖片清單(已驗證 2026-07-13)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Daiwa_聯發科2454_20260710_001.png |

57KB | 真資料圖 | MTK 月營收(TWDm 長條)與 YoY 成長率(橘線,%)走勢圖,橫軸 Jan-16 至約 Jan-26 |

報告_Daiwa_聯發科2454_20260710_002.png |

65KB | 真資料圖 | MTK 股價(NT$/股,深藍線)與 5x/15x/25x/35x/45x 本益比帶狀圖,橫軸約 2001-2026 |

原始內容

MediaTek (2454 TT)

Share price (9 Jul): TWD3,925.00

12-mth rating: Hold (3)

10 July 2026

Information Technology: Taiwan

2Q26 topline beat likely on earlier-than-expected AI ASIC ramp

Rick Hsu

(886) 2 8758 6261

rick.hsu@daiwacm-cathay.com.tw

Sharon Kao

(886) 2 8758 6255

sharon.kao@daiwacm-cathay.com.tw

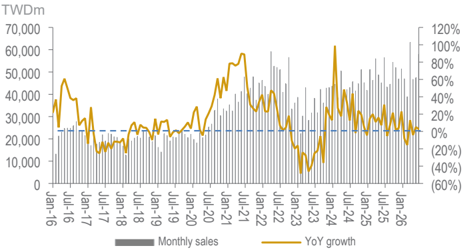

MTK: monthly revenue run rate

Source: Company

Summary: MediaTek (MTK) reported June revenue which resulted in its 2Q26 topline beating market expectations thanks to an earlier-than-expected AI ASIC ramp, in our opinion. While this means upside risk to our forecasts, we flag our Hold (3) rating on the stock as the equity market looks to have priced in its AI ASIC strength too far ahead of its fundamentals. MTK is scheduled to report 2Q26 results by end-July; we will be reviewing our model in due course.

Highlight

- Upbeat revenue run rate. MTK released June revenue of TWD58bn, up 22% MoM and 3% YoY, which closed its 2Q26 topline at TWD152bn, up 2% QoQ (+1% YoY) and beating guidance of TWD140-149bn and 5% above our/consensus estimates of TWD145bn. We attribute the beat to an earlier-than-expected AI ASIC ramp.

- Preview and outlook. We currently expect MTK to have earned TWD23bn in net profit for 2Q26, 5% above the consensus estimate; given the upbeat topline, we see upside risk to our estimate. As for 3Q26, we currently forecast MTK to grow revenue by 10% QoQ to TWD168bn, 12% above the consensus forecast; we are comfortable with our forecast given the earlier-than-expected AI ASIC ramp. MTK is scheduled to report 2Q26 results by end-July; we will be reviewing our model in due course.

Recommendation

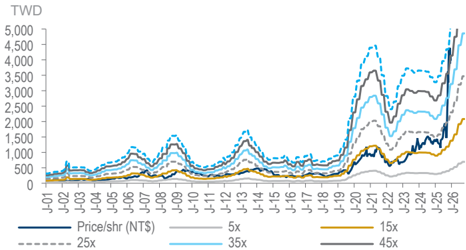

We rate MTK Hold (3). The stock has corrected 21% off its all-time high of TWD4,970 on 2 June, resetting market expectation on the AI ASIC hype back to reality and gradually justifying its fundamentals, in our opinion. Key upside/downside risk to our call would be any AI ASIC accelerator revenue ramp above/below our assumptions.

MTK: 4-quarter forward PER bands

Source: Company, TEJ, Daiwa estimates and forecasts

MTK: 2Q26 results preview and 3Q26 business outlook

| 2Q26E | 2Q26E | 2Q26E | 3Q26E | 3Q26E | 3Q26E | |

|---|---|---|---|---|---|---|

| TWDm | Daiwa | Consensus | Variance | Daiwa | Consensus | Variance |

| Revenue | 145,255 | 144,920 | 0% | 168,341 | 150,607 | 12% |

| Gross profit | 68,179 | 66,843 | 2% | 77,968 | 69,311 | 12% |

| Operating profit | 22,569 | 21,041 | 7% | 32,011 | 22,807 | 40% |

| Pretax profit | 27,469 | 36,911 | ||||

| Net profit | 23,212 | 22,207 | 5% | 31,190 | 23,588 | 32% |

| Adjusted EPS (TWD) | 14.47 | 13.85 | 5% | 19.45 | 14.71 | 32% |

| Margin | ||||||

| Gross | 46.9% | 46.1% | 46.3% | 46.0% | ||

| Operating | 15.5% | 14.5% | 19.0% | 15.1% | ||

| Net | 16.0% | 15.3% | 18.5% | 15.7% | ||

| Revenue mix* | ||||||

| Mobile phone | 48% | 42% | ||||

| Smart edge | 46% | 52% | ||||

| Power IC | 6% | 6% |

Source: Bloomberg, Daiwa estimates and forecasts

Note: * Mobile phone includes smartphones and tablets, Smart edge includes IoT, computing & ASIC, digital TV/home, monitor & optical storage

In the interests of timeliness, this document has not been edited.