PDF 原檔:260701_2454_聯發科_gs_MTK_original.pdf

圖片清單(已驗證 2026-07-02)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

| _001.png | 21KB | 裝飾·valuation | 季度 EPS 摘要小圖 |

| _002.png | 29KB | 裝飾·valuation | 股價表現圖 |

| _003.png | 36KB | 裝飾·valuation | Exhibit 1 營收成長趨勢圖 |

| _004.png | 24KB | 裝飾·valuation | Exhibit 2 毛利率趨勢圖 |

| _005.png | 37KB | 裝飾·valuation | Exhibit 3 依部門營收組合圖 |

| _006.png | 25KB | 裝飾·valuation | Exhibit 4 AI ASIC 營收與貢獻佔比圖 |

| _007.png | 41KB | 裝飾·valuation | Exhibit 7 Taiex vs MediaTek |

| _008.png | 44KB | 裝飾·valuation | Exhibit 9 Forward P/B |

| _009.png | 43KB | 裝飾·valuation | Exhibit 8 Forward P/E |

| _010.png | 33KB | 裝飾·valuation | Exhibit 10 P/B vs ROE |

| _011.png | 86KB | 裝飾·文字卡 | Thesis map / 封面文字卡 |

全數為財務/估值圖表 → lib 頁不嵌入。

原始內容

MediaTek (2454.TW)

Stronger AI ASIC momentum to reshape earnings growth trajectory; reiterate Buy with TP up to NT$6,800

2454.TW

12m Pri c e Target:

NT$6,800.00

Pri c e:

NT$4,335.00

Upside:

56.9%

Stronger AI ASIC ramp unlocks signi fi cant earnings upside

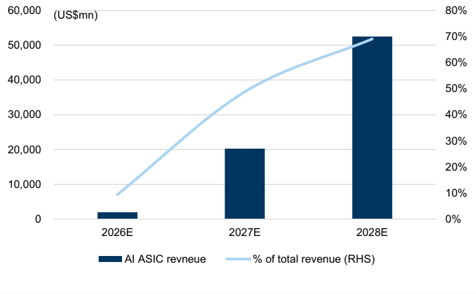

We are now seeing stronger AI ASIC momentum at MediaTek beginning in 2027, and we are raising our AI ASIC revenue to US$20.3bn (vs. US$12.3bn previously), accounting for 49% of its total revenue in 2027E. We note that our forecast is signi fi cantly higher than the company's high end guidance of US$12bn (AI ASIC TAM of US$70-80bn in 2027 with 10-15% of market share), as we see a stronger demand upward revision from key customers over the past 2 months. For 2028, we also tweak up our AI ASIC revenue to US$52.5bn (from US$48bn previously), accounting for 69% of total revenue , as we expect to see incremental shipment units from the current project, on top of the next-gen project.

Price hike to re fl ect elevated cost

We are also factoring in a 5% price hike for MediaTek starting 3Q26. The increase mainly re fl ects the rising cost along the supply chain, including higher wafer pricing, packaging and testing, and component costs, underscored by the recent step-up in memory and substrate pricing. As the adjustment is intended to cover cost in fl ation, we expect MediaTek's GM to remain largely steady at the current level post the price hike.

Raising TP to NT$6,800 from NT$5,000

In light of the stronger AI ASIC outlook and higher pricing, we revise up 2027-28E EPS by 38%/4%. Net net, we are now modeling MediaTek's 2027-28E revenue to grow by 95%/83% YoY (vs. 61%/111% previously) with OpM expanding to 25%/33% (vs. 15% in 2026E), and EPS of NT$181.92/NT$422.17 in 2027/28E . We raise our 12m TP to NT$6,800 from NT$5,000 (still based on 25x 2H27-1H28E EPS). With 57% implied upside, we reiterate our Buy rating on MediaTek.

BUY

Evelyn Yu

+886(2)2730-4187 | evelyn.yu@gs.com Goldman Sachs (Asia) L.L.C., Taipei Branch

James Schneider, Ph.D.

+1(212)357-2929 | jim.schneider@gs.com Goldman Sachs & Co. LLC

Ryan Huang, CFA

+886(2)2730-4084 | ryan.huang@gs.com Goldman Sachs (Asia) L.L.C., Taipei Branch

Key Data _____________________________________

Market cap: NT$6.9tr / $216.4bn

Enterprise value: NT$6.7tr / $208.8bn

3m ADTV: NT$47.0bn / $1.5bn

Taiwan

Taiwan Semiconductor

M&A Rank: 3

Leases incl. in net debt & EV?: No

| GS Forecast | 12/25 | __________ 12/26E | 12/27E | 12/28E |

|---|---|---|---|---|

| Revenue(NT$mn) New | 595,965.7 | 670,819.0 | 1,306,508.8 | 2,394,232.4 |

| Revenue (NT$ mn) Old | 595,965.7 | 673,339.8 | 1,084,001.9 | 2,288,915.5 |

| EBITDA (NT$ mn) | 126,444.1 | 124,348.0 | 352,371.5 | 805,993.7 |

| EPS(NT$) New | 66.17 | 62.24 | 181.92 | 422.17 |

| EPS (NT$) Old | 66.17 | 63.29 | 132.18 | 406.51 |

| P/E (X) | 20.7 | 69.7 | 23.8 | 10.3 |

| P/B (X) | 5.5 | 17.2 | 11.7 | 6.3 |

| Dividend yield (%) | 5.5 | 1.2 | 3.5 | 8.2 |

| CROCI (%) | 54.0 | 37.0 | 90.1 | 192.3 |

| 3/26 | 6/26E | 9/26E | 12/26E | |

| EPS (NT$) | 15.17 | 12.74 | 12.46 | 21.87 |

Source: Company data, Goldman Sachs Research estimates. See disclosures for details.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi ed as research analysts with FINRA in the U.S.

BUY

MediaTek (2454.TW)

Rating since Feb 5, 2026

Ratios & Valuation __________________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| P/E (X) | 20.7 | 69.7 | 23.8 | 10.3 |

| P/B (X) | 5.5 | 17.2 | 11.7 | 6.3 |

| FCF yield (%) | 6.7 | 1.8 | 4.4 | 9.6 |

| EV/EBITDAR (X) | 15.5 | 53.6 | 18.3 | 7.4 |

| EV/EBITDA (excl. leases) (X) | 15.5 | 53.6 | 18.3 | 7.4 |

| CROCI (%) | 54.0 | 37.0 | 90.1 | 192.3 |

| ROE (%) | 26.4 | 24.6 | 58.1 | 79.5 |

| Net debt/equity (%) | (57.3) | (60.8) | (75.3) | (86.0) |

| Net debt/equity (excl. leases) (%) | (57.3) | (60.8) | (75.3) | (86.0) |

| Interest c ov er (X) | 173.3 | 287.1 | 778.4 | 1 , 946.4 |

| Days in v ent o ry o utst , sales | 38.5 | 47.5 | 39.7 | 41.3 |

| Recei v able days | 36.9 | 54.8 | 48.6 | 49.4 |

| Days p ayable o utstandin g | 179.5 | 209.2 | 168.0 | 167.7 |

| DuP o nt ROE (%) | 25.7 | 24.0 | 48.1 | 60.6 |

| Turn ov er (X) | 0.8 | 0.8 | 1.1 | 1.1 |

| L e v era g e (X) | 1.8 | 2.1 | 2.0 | 1.9 |

| G r o ss cas h in v ested (ex cas h ) (NT $ ) | 324 , 106.7 | 333 , 811.3 | 342 , 884.7 | 370 , 832.3 |

| A v era g e ca p ital e mp l o yed (NT $ ) | 188 , 602.2 | 168 , 578.0 | 155 , 488.8 | 152 , 101.9 |

| BVP S (NT $ ) | 249.76 | 252.55 | 369.40 | 685.58 |

Growth & Margins (%) ______________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Total revenue growth | 12.3 | 12.6 | 94.8 | 83.3 |

| E BITDA growth | 2.5 | (1.7) | 183.4 | 128.7 |

| E PS growth | (1.2) | (5.9) | 192.3 | 132.1 |

| DPS growth | 39.7 | (30.0) | 192.3 | 132.1 |

| E BIT margin | 17.4 | 14.9 | 25.2 | 32.8 |

| E BITDA margin | 21.2 | 18.5 | 27 | 33.7 |

| Net income margin | 17.7 | 14.8 | 22.2 | 28.1 |

Price Performance __________________________________________

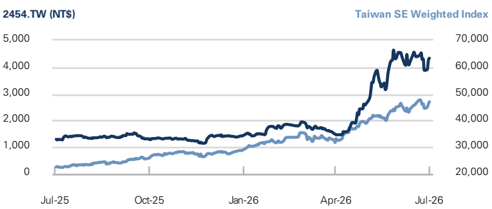

| 3m | 6m | 1 2m | |

|---|---|---|---|

| Absolute | 195.9% | 203.1% | 240.0% |

| Rel. to the TaiwanSE Weighted Index | 108.8% | 86.7% | 63.1% |

Source: FactSet. Price as of 1 Jul 2026 close.

Income Statement (NT$ mn) ________________________________

Cash Flow (NT$ mn) ________________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Tota l r e v e nu e | 595,965.7 | 670,819.0 | 1,306,508.8 | 2,394,232.4 |

| Co s t of good s s old | (312,885.7) | (363,403.5) | (723,403.4) | (1,301,908.1) |

| SG& A | (31,303.9) | (34,872.0) | (40,373.1) | (46,311.7) |

| R&D | (148,306.4) | (172,260.4) | (212,958.3) | (261,216.1) |

| Other operating inc./(exp.) | -- | -- | -- | -- |

| E BITDA | 126 ,444. 1 | 12 4,34 8 .0 | 3 52 ,3 71 . 5 | 8 0 5 ,993. 7 |

| Depreciation& amortization | (22,974.4) | (24,064.9) | (22,597.6) | (21,197.2) |

| E BIT | 1 03,4 6 9. 7 | 1 00, 28 3. 1 | 3 2 9, 77 4.0 | 78 4, 7 9 6 . 5 |

| Net intere s t inc./(exp.) | 10,222.3 | 9,719.8 | 9,784.8 | 9,795.8 |

| Income/(lo ss ) from a ss ociate s | 785.0 | 266.3 | -- | -- |

| Pre-tax pro fi t | 12 4, 887 . 8 | 116 , 2 99. 7 | 34 5 , 558 . 8 | 8 00, 5 9 2 .4 |

| Provi s ion for taxe s | (18,770.2) | (16,360.2) | (55,025.2) | (127,411.9) |

| Minority intere s t | (798.3) | (817.3) | (794.7) | (795.8) |

| Preferred dividend s | -- | -- | -- | -- |

| N et inc . ( pre-ex c ept i o n a ls) | 1 0 5 ,3 1 9.3 | 99, 122 . 2 | 28 9, 7 39.0 | 672 ,3 8 4. 7 |

| Po s t-tax exceptional s | -- | -- | -- | -- |

| N et inc . ( po s t-ex c ept i o n a ls) | 1 0 5 ,3 1 9.3 | 99, 122 . 2 | 28 9, 7 39.0 | 672 ,3 8 4. 7 |

| E P S(b a sic , pre-ex c ept ) (N T $) | 66 . 17 | 62 . 2 4 | 181 .9 2 | 4 22 . 17 |

| E P S(dilu te d , pre-ex c ept ) (N T $) | 66 . 17 | 62 . 2 4 | 181 .9 2 | 4 22 . 17 |

| E P S(b a sic , po s t-ex c ept ) (N T $) | 66 . 17 | 62 . 2 4 | 181 .9 2 | 4 22 . 17 |

| E P S(dilu te d , po s t-ex c ept ) (N T $) | 66 . 17 | 62 . 2 4 | 181 .9 2 | 4 22 . 17 |

| DPS (NT$) | 75.05 | 52.53 | 153.55 | 356.33 |

| Div. payout ratio (%) | 113.4 | 84.4 | 84.4 | 84.4 |

| Balance Sheet (NT$ mn) | ______ | |||

| 12/25 | 12/26E | 12/27E | 12/28E | |

| C a sh& c a sh equiv a lents | 235,290.1 | 268,133.2 | 469,878.3 | 971,042.3 |

| Accounts receiv a ble | 68,597.0 | 132,843.1 | 214,749.0 | 433,760.7 |

| Inventory | 67,234.6 | 107,529.4 | 176,552.2 | 365,833.8 |

| Other current a ssets | 26,334.6 | 23,001.8 | 23,001.8 | 23,001.8 |

| Total current assets | 3 97, 4 56 . 2 | 5 3 1,5 0 7 . 5 | 88 4 ,181 . 2 | 1,79 3 ,6 3 8 . 6 |

| Net PP&E | 60,427.4 | 56,490.5 | 49,179.1 | 43,268.0 |

| Net int a ngibles | 80,261.7 | 79,115.2 | 67,829.1 | 56,543.0 |

| Tot a l investments | 168,911.6 | 172,264.8 | 172,264.8 | 172,264.8 |

| Other long-term a ssets | 36,727.9 | 37,656.1 | 37,656.1 | 37,656.1 |

| Total assets | 7 43 ,78 4. 8 | 877, 034. 1 | 1,211,11 0.3 | 2,1 03 , 3 7 0. 5 |

| Accounts p a y a ble | 156,525.1 | 260,120.8 | 405,976.1 | 790,321.9 |

| Short-term debt | 940.0 | 16,440.0 | 16,440.0 | 16,440.0 |

| Short-term le a se li a bilities | -- | -- | -- | -- |

| Other current li a bilities | 145,884.7 | 156,127.3 | 156,127.3 | 156,127.3 |

| Total current liabilities | 303 , 34 9 . 8 | 43 2,688 . 2 | 578,5 43. 5 | 962,889 . 2 |

| Long-term debt | 60.0 | 120.0 | 120.0 | 120.0 |

| Long-term le a se li a bilities | -- | -- | -- | -- |

| Other long-term li a bilities | 31,180.0 | 30,401.8 | 30,401.8 | 30,401.8 |

| Total long-term liabilities | 3 1,2 40.0 | 30 ,521 . 8 | 30 ,521 . 8 | 30 ,521 . 8 |

| Total liabilities | 334 ,589 . 8 | 4 6 3 ,21 0.0 | 6 0 9, 0 65 .3 | 99 3 , 4 11 .0 |

| Preferred sh a res | -- | -- | -- | -- |

| Tot a l commonequity | 400,601.0 | 405,062.5 | 592,488.7 | 1,099,607.3 |

| Minority interest | 8,59 4.0 | 8,761 . 7 | 9,556 .4 | 1 0 , 3 52 . 2 |

| Total liabilities &equity | 7 43 ,78 4. 8 | 877, 034. 1 | 1,211,11 0.3 | 2,1 03 , 3 7 0. 5 |

| Net debt, a djusted | (234,290.1) | (251,573.2) | (453,318.3) | (954,482.3) |

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Net income | 105,319.3 | 99,122.2 | 289,739.0 | 672,384.7 |

| D&Aadd-back | 22,974.4 | 24,064.9 | 22,597.6 | 21,197.2 |

| Minority interest add-back | 798.3 | 817.3 | 794.7 | 795.8 |

| Net (inc)/dec working capital | (20,302.7) | (945.3) | (5,073.3) | (23,947.6) |

| Other operating cash flow | 54,003.6 | 6,088.6 | -- | -- |

| Cash flow fro m operations | 162 , 7 9 2 .9 | 12 9, 1 4 7 . 7 | 30 8 ,0 57 .9 | 67 0,430.0 |

| Capital expenditures | (15,059.1) | (7,260.2) | (4,000.0) | (4,000.0) |

| Acquisitions | (1,141.7) | (206.8) | -- | -- |

| Divestitures | -- | -- | -- | -- |

| Others | (21,553.1) | 376.3 | -- | -- |

| Cash flow fro m investing | (3 7 , 75 4.0) | ( 7 ,090. 7 ) | (4,000.0) | (4,000.0) |

| Repayment of lease liabilities | -- | -- | -- | -- |

| Dividends paid(common& pref) | (86,069.6) | (106,473.2) | (102,312.8) | (165,266.0) |

| Inc/(dec) in debt | 60.0 | 15,560.0 | -- | -- |

| Other financing cash flows | (7,435.1) | 1,699.3 | 0.0 | 0.0 |

| Cash flow fro m financing | (93,444. 7 ) | ( 8 9, 21 3.9) | ( 1 0 2 ,3 12 . 8 ) | ( 165 , 266 .0) |

| Total cash flow | 3 1 , 5 94. 2 | 3 2 , 8 43. 1 | 2 0 1 , 7 4 5 . 1 | 5 0 1 , 16 4.0 |

| Free cash flow | 147,733.8 | 121,887.5 | 304,057.9 | 666,430.0 |

Source: Company data, Goldman Sachs Research estimates.

AI ASIC ramp to outweigh smartphone cyclically

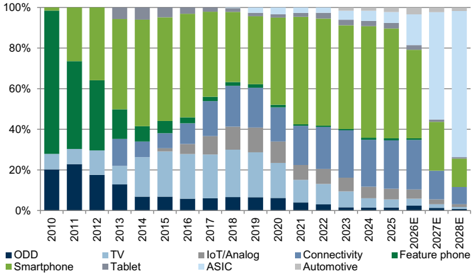

We note that there have been recent investor concerns over the smartphone business given rising memory prices that would further impact the overall shipment. However, we reiterate our thesis that MediaTek is well-positioned to transition from a traditional smartphone application provider to an AI-focused vendor. We forecast that in 2027, its smartphone business would only account for 24% of its total revenue (vs. 44% in 2026E), declining to 14% in 2028E.

We expect AI ASIC to remain the key focus of the 2Q26 analyst meeting

We expect the company to host its 2Q26 analyst meeting at the end of July. We believe investors key questions will be around MediaTek's view on: 1) latest progress on current/next generation AI ASIC and the mass production timeline, 2) next-generation AI ASIC dollar content value gain and GM upside, 3) potential updated guidance on AI ASIC TAM, and 4) any potential ASIC projects beyond the current US CSP customer.

For 3Q26E, we are now expecting revenue to grow by 6.7% QoQ, with GM/OpM at 46.1%/12.9% (vs 46.1% /13.9% in 2Q26E), and EPS of NT$12.46. We expect revenue to improve QoQ into 2H26, driven by the introduction of new N2 smartphone SoC by end of 3Q26 and strong ramp of AI ASIC in 4Q26. However, we believe the smartphone weakness is largely re fl ected in the current stock price. Overall, we remain optimistic in MediaTek's 2026 revenue growth with both ASIC and smart edge momentum o ff setting the smartphone weakness, and we now expect MediaTek's revenue to grow 13% YoY with GM/OpM reaching 45.8%/14.9%.

Exhibit 1: MediaTek's revenue growth trends

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 2: MediaTek's margin trends

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 3: MediaTek's revenue mix by segment

Source: Company data, Goldman Sachs Global Investment Research

Earnings changes, valuation and risks

Forecast changes

We have revised our 2026/27/28E earnings by -2%/+38%/+4% to re fl ect 1) much stronger TPUv8 shipment in 2027, 2) longer TPUv8 lifetime into 2028, 3) price hike among all product lines, and 4) weaker near-term smartphone demand.

Exhibit 5: Earnings revisions

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| (NT$mn) | Old | New | Diff (%) | Old | New | Diff (%) | Old | New | Diff (%) |

| Revenue | 673,340 | 670,819 | -0.4% | 1,084,002 | 1,306,509 | 20.5% | 2,288,915 | 2,394,232 | 4.6% |

| Gross profit | 308,979 | 307,416 | -0.5% | 490,358 | 583,105 | 18.9% | 1,064,726 | 1,092,324 | 2.6% |

| Op. income | 101,847 | 100,283 | -1.5% | 234,853 | 329,774 | 40.4% | 754,480 | 784,797 | 4.0% |

| Net income | 100,757 | 99,122 | -1.6% | 210,420 | 289,739 | 37.7% | 647,145 | 672,385 | 3.9% |

| EPS (NT$) | 63.29 | 62.24 | -1.7% | 132.18 | 181.92 | 37.6% | 406.51 | 422.17 | 3.9% |

| GM | 45.9% | 45.8% | -0.1% | 45.2% | 44.6% | -0.6% | 46.5% | 45.6% | -0.9% |

| OpM | 15.1% | 14.9% | -0.2% | 21.7% | 25.2% | 3.6% | 33.0% | 32.8% | -0.2% |

| NM | 15.0% | 14.8% | -0.2% | 19.4% | 22.2% | 2.8% | 28.3% | 28.1% | -0.2% |

| 3Q26E | 3Q26E | 3Q26E | 4Q26E | 4Q26E | 4Q26E | 1Q27E | 1Q27E | 1Q27E | |

|---|---|---|---|---|---|---|---|---|---|

| (NT$mn) | Old | New | Diff (%) | Old | New | Diff (%) | Old | New | Diff (%) |

| Revenue | 153,175 | 153,854 | 0.4% | 222,912 | 223,664 | 0.3% | 243,448 | 246,552 | 1.3% |

| Gross profit | 70,822 | 70,990 | 0.2% | 100,729 | 100,914 | 0.2% | 109,701 | 110,717 | 0.9% |

| Op. income | 19,637 | 19,804 | 0.9% | 37,341 | 37,526 | 0.5% | 47,546 | 48,910 | 2.9% |

| Net income | 19,803 | 19,847 | 0.2% | 34,806 | 34,833 | 0.1% | 43,406 | 44,459 | 2.4% |

| EPS (NT$) | 12.44 | 12.46 | 0.2% | 21.86 | 21.87 | 0.0% | 27.27 | 27.91 | 2.4% |

| GM | 46.2% | 46.1% | -0.1% | 45.2% | 45.1% | -0.1% | 45.1% | 44.9% | -0.2% |

| OpM | 12.8% | 12.9% | 0.1% | 16.8% | 16.8% | 0.0% | 19.5% | 19.8% | 0.3% |

| NM | 12.9% | 12.9% | 0.0% | 15.6% | 15.6% | 0.0% | 17.8% | 18.0% | 0.2% |

Source: Company data, Goldman Sachs Global Investment Research

Reiterate Buy, raise TP to NT$6,800 from NT$5,000

We increase our 12m TP to NT$6,800 from NT$5,000 previously, following our upward earnings revisions. Our TP is based on a target P/E multiple of 25x (unchanged; +1.8 stdv above 5 yr avg. fwd P/E) applied to our FY2H27E-1H28E EPS (unchanged). Overall, our 12m TP implies 57% upside; we reiterate our Buy rating on MediaTek.

Exhibit 4: MediaTek's AI ASIC business revenue and revenue contribution

Source: Goldman Sachs Global Investment Research

Exhibit 6: MediaTek P&L summary

| 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| P&L (NT$mn) | |||||||||||

| Revenue | 149,151 | 144,150 | 153,854 | 223,664 | 246,552 | 315,137 | 366,338 | 378,483 | 670,819 | 1,306,509 | 2,394,232 |

| Gross profit | 69,055 | 66,456 | 70,990 | 100,914 | 110,717 | 140,422 | 163,091 | 168,875 | 307,416 | 583,105 | 1,092,324 |

| Operating profit | 22,891 | 20,061 | 19,804 | 37,526 | 48,910 | 77,311 | 99,159 | 104,394 | 100,283 | 329,774 | 784,797 |

| Net income | 24,154 | 20,288 | 19,847 | 34,833 | 44,459 | 68,060 | 86,399 | 90,821 | 99,122 | 289,739 | 672,385 |

| EPS (NT$) | 15.17 | 12.74 | 12.46 | 21.87 | 27.91 | 42.73 | 54.25 | 57.02 | 62.24 | 181.92 | 422.17 |

| Margins (%) | |||||||||||

| Gross margin | 46.3% | 46.1% | 46.1% | 45.1% | 44.9% | 44.6% | 44.5% | 44.6% | 45.8% | 44.6% | 45.6% |

| Operating profit margin | 15.3% | 13.9% | 12.9% | 16.8% | 19.8% | 24.5% | 27.1% | 27.6% | 14.9% | 25.2% | 32.8% |

| Net margin | 16.2% | 14.1% | 12.9% | 15.6% | 18.0% | 21.6% | 23.6% | 24.0% | 14.8% | 22.2% | 28.1% |

| YoY (%) | |||||||||||

| Revenue | -2.7% | -4.1% | 8.3% | 48.9% | 65.3% | 118.6% | 138.1% | 69.2% | 12.6% | 94.8% | 83.3% |

| Gross profit | -6.4% | -10.0% | 7.4% | 45.7% | 60.3% | 111.3% | 129.7% | 67.3% | 8.6% | 89.7% | 87.3% |

| Operating profit | -23.8% | -31.7% | -10.7% | 71.7% | 113.7% | 285.4% | 400.7% | 178.2% | -3.1% | 228.8% | 138.0% |

| Net income | -17.6% | -27.1% | -21.3% | 51.9% | 84.1% | 235.5% | 335.3% | 160.7% | -5.9% | 192.3% | 132.1% |

| EPS | -17.7% | -27.2% | -21.3% | 51.9% | 84.0% | 235.5% | 335.3% | 160.7% | -5.9% | 192.3% | 132.1% |

| QoQ (%) | |||||||||||

| Revenue | -0.7% | -3.4% | 6.7% | 45.4% | 10.2% | 27.8% | 16.2% | 3.3% | |||

| Gross profit | -0.3% | -3.8% | 6.8% | 42.2% | 9.7% | 26.8% | 16.1% | 3.5% | |||

| Operating profit | 4.8% | -12.4% | -1.3% | 89.5% | 30.3% | 58.1% | 28.3% | 5.3% | |||

| Net income | 5.4% | -16.0% | -2.2% | 75.5% | 27.6% | 53.1% | 26.9% | 5.1% | |||

| EPS | 5.3% | -16.0% | -2.2% | 75.5% | 27.6% | 53.1% | 26.9% | 5.1% |

Source: Company data, Goldman Sachs Global Investment Research

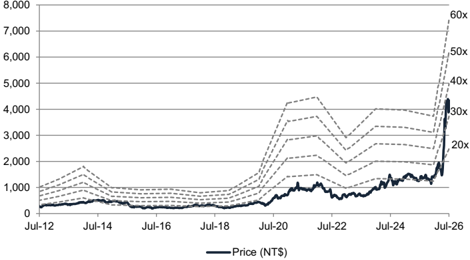

Exhibit 7: Taiex vs. MediaTek

Source: Bloomberg

Exhibit 9: MediaTek Forward P/B

Source: Bloomberg

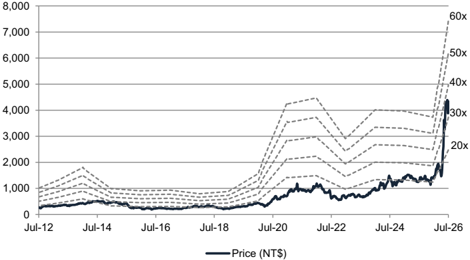

Exhibit 8: MediaTek Forward P/E

Source: Bloomberg

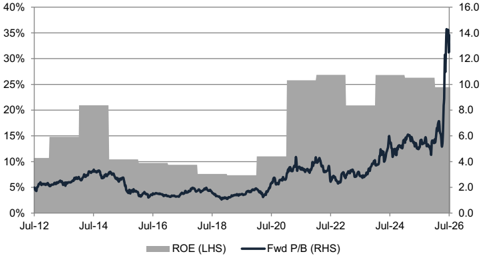

Exhibit 10: MediaTek P/B vs. ROE

Source: Bloomberg

Investment Thesis, Price Target Risks and Methodology

Investment Thesis - Mediatek

MediaTek is a leading global IC design house specializing in smartphone AP (application processor). We have a positive stance on MediaTek, viewing it as well-positioned to transition from a traditional smartphone application provider to an AI-focused vendor, beginning with AI smartphones and extending to enterprise ASICs and smart automotive solutions (in partnership with NVIDIA) in 2025 and beyond. We expect MediaTek to achieve solid multi-year growth, where we expect revenue and earnings to increase by 42%/59% CAGRs, respectively, in 2025-28E. This growth will be primarily driven by: 1) market share gains, particularly in the premium segment (speci fi cally high-end 5G fl agship SoCs), 2) strong ramp in AI ASIC business, and 3) new TAM in the automotive/computing sectors.

Price Target Risks and Methodology - MediaTek (2454.TW)

Valuation: Our 12m TP of NT$6,800 is based on a target P/E multiple of 25x (1.8 stdv above its 5-year trading average) applied to our 2H27E-1H28E EPS.

Key risks to our views: (1) Weaker-than-expected end demand especially with smartphones, (2) Higher foundry cost impacting its margin outlook, (3) Intensifying competition that would result in reduced pro fi tability, and (4) Slower ramp in ASIC would result in changes in operating leverage