PDF 原檔:260601_4958_甄鼎_gs_ZDT_original.pdf

原始內容

Zhen Ding Technology Holding (4958.TW): Taiwan Computex & Corporate Day: Multi-year expansion to support strong AI

We hosted meetings with Zhen Ding at our Taiwan Computex & Corporate Day (June 1st). Key takeaways include:

- (1) Upward revision on IC substrate/AI server/optical business: Management has revised up its guidance on IC substrate/AI server/optical business to reach 40-45% of total revenue by 2030 (previous guidance was 20-25%), and expects these businesses to reach 25% in 2026 (was ~12% in 2025).

- (2) IC substrate business with strong momentum: Management has revised up its IC substrate business YoY growth from 60% to 80% in 2026 with strong visibility extended into 2027. ABF substrate business has turned pro fi table in 1Q26, while ABF plant 2 in ShenZhen will begin contributing from 2H26 and the company will continue to expand non-China ABF substrate capacity.

- (3) Ongoing progress with mSAP solutions for 1.6T optical: The company is currently sampling mSAP solutions for 1.6T optical and expects to reach MP starting from 3Q26. Optical revenue is expected to account for 4% of total revenue in 2026 (vs. 0.4% in 2025). Management mentioned that yield is currently at 80%+, and is improving toward 90%, and believes the leading yield vs. peers is the key reason that the company can capture leading market share in optical mSAP solutions amid supply shortage.

(4) Massive multi-year CAPEX cycles supported by customer demand:

Management reiterated its 2026 CAPEX guidance of NT$80bn, driven by customer orders and long-term agreements. This year's CAPEX is primarily for expanding HDI and higher layer count PCBs (>65% of CAPEX), with the remainder allocated between IC substrates (15-20%) and FPC (~15%). The company also mentioned CAPEX spending is expected to remain high at similar levels throughout 2028-30.

- (5) Consumer business remains stable while mSAP shifts toward AI: The consumer business remains core, but as IC substrate/AI server/optical scale up, overall seasonality in GM is expected to fl atten in 2026 (was seeing 80ppts quarterly GM variation in 2025). mSAP was previously mainly used in smartphones, but is expected to shift toward a 50:50 split between smartphone and optical/AI server in next 3 years driven by the strong demand.

- (6) IC substrate subsidiary going public: Zhen Ding's IPO plan for its IC substrate subsidiary, Leading Tech, has passed board approval, with documentation to be delivered in 2H26, followed by a planned IPO in Hong Kong in 2027.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi ed as research

Chao Wang

+886(2)2730-4195 | kuanchao.wang@gs.com Goldman Sachs (Asia) L.L.C., Taipei Branch

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Al Wang

+886(2)2730-4081 | al.wang@gs.com Goldman Sachs (Asia) L.L.C., Taipei Branch e92c7a75ab8b4efbba794e6b187208c8

Outlook

We are positive on ZDT's IC substrate/AI server/optical business outlook as management guided for these businesses to contribute 25% of total revenue in 2026. We expect AI server demand to accelerate in 2H26, supported by the company's successful PCB veri fi cation for Vera Rubin's compute tray, and we expect the contribution to become more meaningful in 2H26-1H27, with better pro fi tability (average OPM of 20-30% for AI computing tray vs. company overall OPM of 10-15%), assuming the company continues to deliver good yield. Furthermore, we expect to see increasing contribution from both ASIC-related projects (from AWS and Google) and optical solutions (with PCB for 1.6T optical module to see small volume starting in 2Q26) in 2026. We expect to see more ABF substrate contribution upon the completion of ShenZhen Plant 2 and the company continues to expand non-China capacity.

The company reiterated its 2026 CAPEX guidance of NT$80bn+ (implying 150%+ YoY), as the company expects to complete 10 factories this year as part of its long-term strategy to build 15 factories. The company guided that 65% of 2026 CAPEX will be allocated for the server and optical business, 15% to the IC substrate business, and 10% to the PFC business. The proactive investment plan is in line with our positive view that AI PCB will see 140% 2025-27E CAGR (see here), and we believe ZDT is well-positioned to be one of the winners in the AI era considering its strong execution track record and proactive capacity expansion plan relative to peers.

Valuation : Our 12-month TP of NT$388 is based on a SOTP valuation methodology, including (1) 2.6x blended 4Q26-3Q27E P/B for ABF & BT substrate, (2) 20x 4Q26-3Q27E P/E for high-growth AI server/switch related PCB (in line with industry average), and (3) 8x 4Q26-3Q27E P/E for low-growth consumer electronics PCB (in-line with industry downcycle average valuation).

Key downside risks include : (1) weaker-than-expected iPhone demand or slower content upgrade, (2) delay in new substrate capacity or slower-than-expected yield rate ramp up progress, and (3) fi ercer competition in China ABF market.

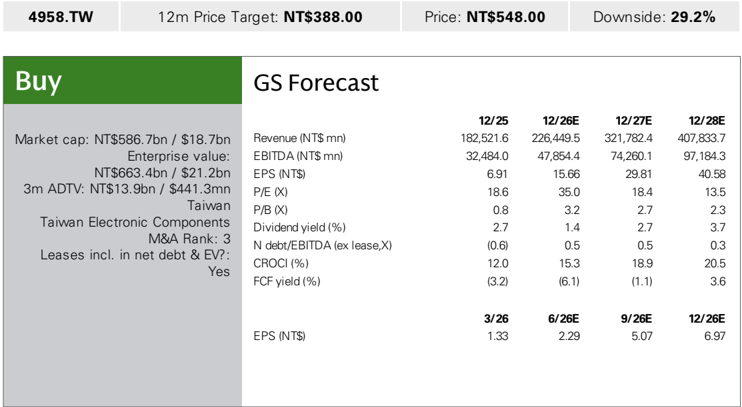

| 4958.TW | 12m Price Target: NT$388.00 | Price: NT$548.00 | Downside: 29.2% | Downside: 29.2% |

|---|---|---|---|---|

| Buy | Buy | |||

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | Revenue (NT$ mn) EBITDA (NT$ mn) EPS (NT$) P/E (X) P/B (X) Dividend yield (%) N debt/EBITDA (ex CROCI (%) F C F yield (%) | 12/25 12/26E 182,521.6 226,449.5 32,484.0 6.91 18.6 0.8 2.7 (0.6) 12.0 (3.2) 3/26 1.33 | 12/27E 321,782.4 74,260.1 29.81 18.4 2.7 2.7 0.5 18.9 (1.1) | 12/28E 407,833.7 |

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | 47,854.4 | 97,184.3 | ||

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | 15.66 | 40.58 | ||

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | 35.0 | 13.5 | ||

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | 3.2 | 2.3 | ||

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | 1.4 | 3.7 | ||

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | lease,X) | 0.5 | 0.3 | |

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | 15.3 | 20.5 | ||

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | (6.1) | 3.6 | ||

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | 6/26E | 9/26E | 12/26E | |

| Market c ap: NT$586.7bn / $ 1 8.7bn E nterpr is e v a lu e: NT$66 3 . 4 bn / $ 21 . 2 bn 3m AD T V : NT$ 13 . 9 bn / $ 441 . 3m n Ta iw an Ta iw an El e c tr o n ic Com p o nent s M &A R ank: 3 L ea s e s i n cl . i n net d ebt & EV? : Y e s | EPS (NT$) | 2.29 | 5.07 | 6.97 |

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 1 Jun 2026 close.

e92c7a75ab8b4efbba794e6b187208c8