PDF 原檔:260601_2308_台達電_daiwa_Delta_original.pdf

原始內容

Delta Electronics (2308 TT)

Target price:

TWD2,922.00 (from TWD2,440.00)

Share price (1 Jun):

TWD2,420.00

|

Up/downside:

+20.7%

2026 Taiwan corporate day conference note

- Positive AI server power development with faster HVDC adoption

- New growth drivers from fuel cell, SST, ESS and micro grid

- Reaffirming our Buy (1) rating; lifting 12-month TP to TWD2,922

What's new: We provide an update on Delta after our 2026 Taiwan Corporate Day. We reaffirm our positive view on Delta and view it as one of our top ideas within the AI trend.

What's the impact: Position in the power segment remains resilient.

Based on our understanding, we believe there are four potential power architecture solutions to be applied in the Vera Rubin generation, with two from a high-voltage environment and the other two from a low-voltage environment. The high-voltage environment could be divided into 800VDC or +-400VDC, while the total voltage from rack could range from 600kW to 1.5MW, depending on client requirements. As for low-voltage options, these can either be 72kW powershelf (bundled with 6x of 12kW PSUs) or 110kW powershelf (bundled with 6x of Nvidia's standard 18.3kW solution), but width of 18.3kW power supply will be 3x bigger than Delta's 12kW solution. We assume Nvidia's strategy to use HVDC has sped up by c.1 year, and it would have 20-30% of HVDC adoption from this generation and 50% from 2027. This is the key driver of our higher AI server revenue assumption. New growth drivers anticipated by investors. During Taiwan Corporate Day, we believe investor interest has gradually shifted to fuel cells (ie, SOFC or SOEC). Due to the technology licenses from Ceres Power (CWR L), Delta plans to build up trial fuel cell-capacity from 4Q26 and start mass production in 2027. We believe investors are keen to know the competition between Ceres and Bloom Energy in terms of tech spec and Delta's competitors (Weichai [2338 HK, HKD40.14, Outperform (2); covered by Kelvin Lau] and Doosan Enerbility [034020 KS, KRW106,900, Buy (1); covered by Mike Oh]), which are also licensed from Ceres Power. We believe it will become the next growth driver for Delta after HVDC plays out. The micro grid (vs. utility grid) concept with rising new-type energy generation method (eg, fuel cells), solid-state transformers (SSTs), Energy Storage System (ESS) could enable Delta to further transform itself from a power systems company into an infrastructure provider.

What we recommend: We raise our 2026-28E EPS by 8-9% to reflect better-than-expected gross margin performance and AI server contributions on rapid adoption of HVDC from Nvidia. We raise our 12M TP to TWD2,922 (from TWD2,440), based on a higher target PER of 55x (from 50x; above its past-3-year range of 11-50x) applied to our 1-year-forward EPS, due to new growth drivers from the micro grid. We believe a higher target PER is justified as the PEG ratio stands at 0.90x (vs. our 2025-28E earnings CAGR of 61%). Downside risk: weaker-than-expected demand.

How we differ: Our 2026-28E EPS are 4-36% above Bloomberg consensus, likely due to our more bullish HVDC adoption rate.

Sheng Cheng

(886) 2 8758 6253

sheng.cheng@daiwacm-cathay.com.tw

Allan Wang (886) 2 8758 6249 allan.wang@daiwacm-cathay.com.tw

Forecast revisions (%)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue change | 1.7 | 1.1 | 1.1 |

| Net profit change | 8.8 | 7.7 | 8.8 |

| Core EPS (FD) change | 8.8 | 7.7 | 8.8 |

Source: Daiwa forecasts

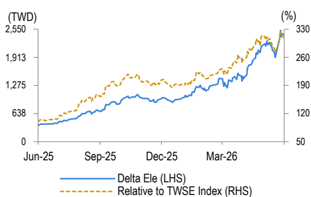

Share price performance

| 12-month range | 367.50-2,520.00 |

|---|---|

| Market cap (USDbn) | 200.67 |

| 3m avg daily turnover (USDm) | 687.49 |

| Shares outstanding (m) | 2,598 |

| Major shareholder | Hsiang Ta International (10.3%) |

Financial summary (TWD)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue (m) | 720,711 | 1,002,184 | 1,466,796 |

| Operating profit (m) | 135,098 | 215,592 | 342,138 |

| Net profit (m) | 101,656 | 158,647 | 251,013 |

| Core EPS (fully-diluted) | 39.136 | 61.076 | 96.635 |

| EPS change (%) | 69.1 | 56.1 | 58.2 |

| Daiwa vs Cons. EPS (%) | 4.3 | 11.0 | 36.2 |

| PER (x) | 61.8 | 39.6 | 25.0 |

| Dividend yield (%) | 0.5 | 0.7 | 1.2 |

| DPS | 11.6 | 18.0 | 28.5 |

| PBR (x) | 17.2 | 12.8 | 9.1 |

| EV/EBITDA (x) | 38.0 | 25.0 | 16.1 |

| ROE (%) | 32.1 | 36.9 | 42.4 |

Source: FactSet, Daiwa forecasts

Delta Electronics: revenue and earnings forecasts - Daiwa vs. consensus

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | Previous | New | Consensus | Previous | New | Consensus | Previous | New | Consensus |

| Revenue | 708,431 | 720,711 | 738,386 | 991,348 | 1,002,184 | 925,551 | 1,451,122 | 1,466,796 | 1,330,714 |

| Diff (%) | 1.7% | -2.4% | 1.1% | 8.3% | 1.1% | 10.2% | |||

| Gross Margin (%) | 35.1% | 36.7% | 35.4% | 35.5% | 36.7% | 36.2% | 35.8% | 37.4% | 33.6% |

| Operating profit | 123,261 | 135,098 | 132,517 | 200,985 | 215,592 | 194,537 | 315,952 | 342,138 | 252,415 |

| Op Margin (%) | 17.4% | 18.7% | 17.9% | 20.3% | 21.5% | 21.0% | 21.8% | 23.3% | 19.0% |

| Net profit | 93,451 | 101,656 | 97,464 | 147,275 | 158,647 | 142,878 | 230,626 | 251,013 | 184,336 |

| EPS (TWD) | 35.98 | 39.14 | 37.52 | 56.70 | 61.08 | 55.01 | 88.79 | 96.63 | 70.97 |

| Diff (%) | 8.8% | 4.3% | 7.7% | 11.0% | 8.8% | 36.2% |

Source: Bloomberg, Daiwa forecasts

Delta: quarterly and annual P&L statement

| 2026E | 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2027E | 2025 | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | 1Q | 2QE | 3QE | 4QE | 1QE | 2QE | 3QE | 4QE | ||||

| Net revenue | 159,353 | 174,456 | 185,997 | 200,905 | 203,352 | 232,380 | 266,734 | 299,718 | 554,885 | 720,711 | 1,002,184 | 1,466,796 |

| COGS | -100,392 | -110,643 | -117,658 | -127,869 | -128,957 | -146,464 | -167,943 | -191,041 | -364,729 | -456,562 | -634,405 | -918,356 |

| Gross profit | 58,961 | 63,813 | 68,339 | 73,037 | 74,395 | 85,917 | 98,791 | 108,677 | 190,157 | 264,149 | 367,779 | 548,439 |

| Operating expenses | -30,544 | -31,402 | -32,549 | -34,556 | -34,570 | -37,646 | -39,210 | -40,762 | -106,224 | -129,051 | -152,187 | -206,302 |

| Operating profit | 28,417 | 32,411 | 35,789 | 38,481 | 39,825 | 48,271 | 59,581 | 67,916 | 83,932 | 135,098 | 215,592 | 342,138 |

| Non-operating profit | 2,676 | 1,824 | 2,037 | 1,811 | 1,320 | 1,313 | 1,310 | 1,713 | 3,934 | 8,347 | 5,656 | 5,652 |

| Pretax profit | 31,093 | 34,235 | 37,826 | 40,292 | 41,145 | 49,584 | 60,891 | 69,629 | 87,866 | 143,445 | 221,249 | 347,790 |

| Income taxes | -7,258 | -7,018 | -7,754 | -8,260 | -8,846 | -10,661 | -13,092 | -14,970 | -19,930 | -30,291 | -47,568 | -74,775 |

| Net profit | 20,556 | 24,600 | 27,282 | 29,219 | 29,248 | 35,438 | 43,798 | 50,163 | 60,108 | 101,656 | 158,647 | 251,013 |

| Net EPS (TWD) | 7.91 | 9.47 | 10.50 | 11.25 | 11.26 | 13.64 | 16.86 | 19.31 | 23.14 | 39.14 | 61.08 | 96.63 |

| Operating Ratios | ||||||||||||

| Gross margin | 37.0% | 36.6% | 36.7% | 36.4% | 36.6% | 37.0% | 37.0% | 36.3% | 34.3% | 36.7% | 36.7% | 37.4% |

| Operating margin | 17.8% | 18.6% | 19.2% | 19.2% | 19.6% | 20.8% | 22.3% | 22.7% | 15.1% | 18.7% | 21.5% | 23.3% |

| Pre-tax margin | 19.5% | 19.6% | 20.3% | 20.1% | 20.2% | 21.3% | 22.8% | 23.2% | 15.8% | 19.9% | 22.1% | 23.7% |

| Net margin | 12.9% | 14.1% | 14.7% | 14.5% | 14.4% | 15.2% | 16.4% | 16.7% | 10.8% | 14.1% | 15.8% | 17.1% |

| YoY (%) | ||||||||||||

| Net revenue | 34% | 41% | 24% | 24% | 28% | 33% | 43% | 49% | 32% | 30% | 39% | 46% |

| Gross profit | 56% | 45% | 30% | 31% | 26% | 35% | 45% | 49% | 39% | 39% | 39% | 49% |

| Operating profit | 102% | 74% | 44% | 46% | 40% | 49% | 66% | 76% | 76% | 61% | 60% | 59% |

| Pretax profit | 99% | 75% | 40% | 57% | 32% | 45% | 61% | 73% | 71% | 63% | 54% | 57% |

| Net profit | 101% | 76% | 47% | 69% | 42% | 44% | 61% | 72% | 71% | 69% | 56% | 58% |

| QoQ (%) | ||||||||||||

| Net revenue | -1% | 9% | 7% | 8% | 1% | 14% | 15% | 12% | ||||

| Gross profit | 5% | 8% | 7% | 7% | 2% | 15% | 15% | 10% | ||||

| Operating profit | 8% | 14% | 10% | 8% | 3% | 21% | 23% | 14% | ||||

| Pretax profit | 21% | 10% | 10% | 7% | 2% | 21% | 23% | 14% | ||||

| Net profit | 19% | 20% | 11% | 7% | 0% | 21% | 24% | 15% |

Source: Company, Daiwa forecasts

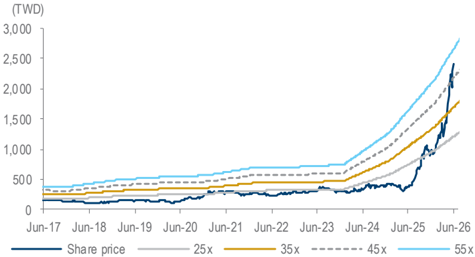

Delta: 1-year forward PER band

Source: TEJ, Daiwa forecasts

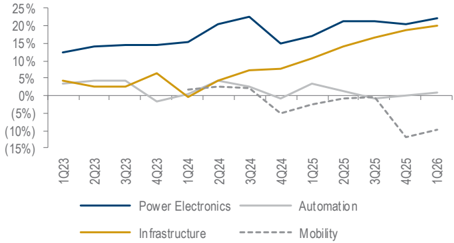

Delta: operating margin by segment (quarterly)

Source: Company

Financial summary

Key assumptions

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Automation revenue growth (YoY) | 18 | 19 | (0) | (3) | 5 | 13 | 9 | 7 |

| Infrastructure revenue growth (YoY) | (8) | 26 | (4) | 2 | 82 | 32 | 61 | 57 |

| Power Electronics sales growth (YoY) | 21 | 21 | 9 | (10) | 25 | 38 | 33 | 45 |

Profit and loss (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Power Electronics | 187,316 | 227,311 | 248,257 | 223,992 | 280,032 | 385,053 | 512,710 | 745,408 |

| Automation | 45,881 | 54,519 | 54,296 | 52,403 | 54,943 | 61,994 | 67,428 | 72,222 |

| Other Revenue | 81,474 | 102,613 | 98,674 | 144,752 | 219,911 | 273,664 | 422,046 | 649,166 |

| Total Revenue | 314,671 | 384,443 | 401,227 | 421,148 | 554,885 | 720,711 | 1,002,184 | 1,466,796 |

| Other income | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| COGS | (224,461) | (273,671) | (284,013) | (284,567) | (364,729) | (456,562) | (634,405) | (918,356) |

| SG&A | (31,642) | (37,564) | (40,215) | (47,354) | (57,482) | (69,590) | (76,575) | (101,402) |

| Other op.expenses | (27,202) | (31,770) | (36,048) | (41,575) | (48,743) | (59,461) | (75,612) | (104,900) |

| Operating profit | 31,365 | 41,439 | 40,950 | 47,652 | 83,932 | 135,098 | 215,592 | 342,138 |

| Net-interest inc./(exp.) | 134 | 38 | 899 | 1,859 | 1,501 | 1,600 | 1,576 | 1,572 |

| Assoc/forex/extraord./others | 4,128 | 4,588 | 6,793 | 1,804 | 2,433 | 6,747 | 4,080 | 4,080 |

| Pre-tax profit | 35,628 | 46,065 | 48,642 | 51,316 | 87,866 | 143,445 | 221,249 | 347,790 |

| Tax | (7,128) | (9,075) | (9,762) | (10,925) | (19,930) | (30,291) | (47,568) | (74,775) |

| Min. int./pref. div./others | (1,703) | (4,325) | (5,488) | (5,163) | (7,828) | (11,498) | (15,033) | (22,002) |

| Net profit (reported) | 26,796 | 32,666 | 33,393 | 35,229 | 60,108 | 101,656 | 158,647 | 251,013 |

| Net profit (adjusted) | 26,796 | 32,666 | 33,393 | 35,229 | 60,108 | 101,656 | 158,647 | 251,013 |

| EPS (reported)(TWD) | 10.316 | 12.576 | 12.855 | 13.562 | 23.140 | 39.136 | 61.076 | 96.635 |

| EPS (adjusted)(TWD) | 10.316 | 12.576 | 12.855 | 13.562 | 23.140 | 39.136 | 61.076 | 96.635 |

| EPS (adjusted fully-diluted)(TWD) | 10.316 | 12.576 | 12.855 | 13.562 | 23.140 | 39.136 | 61.076 | 96.635 |

| DPS (TWD) | 5.500 | 5.500 | 9.840 | 6.430 | 7.000 | 11.600 | 18.000 | 28.500 |

| EBIT | 31,365 | 41,439 | 40,950 | 47,652 | 83,932 | 135,098 | 215,592 | 342,138 |

| EBITDA | 48,516 | 60,375 | 62,540 | 72,668 | 111,771 | 164,263 | 249,477 | 382,585 |

Cash flow (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Profit before tax | 35,628 | 46,065 | 48,642 | 51,316 | 87,866 | 143,445 | 221,249 | 347,790 |

| Depreciation and amortisation | 17,151 | 18,936 | 21,590 | 25,016 | 27,839 | 29,164 | 33,884 | 40,448 |

| Tax paid | (7,128) | (9,075) | (9,762) | (10,925) | (19,930) | (30,291) | (47,568) | (74,775) |

| Change in working capital | (20,506) | (20,062) | 2,466 | (2,538) | (24,348) | (64,676) | (88,045) | (89,540) |

| Other operational CF items | 3,175 | 10,665 | 8,151 | 10,025 | 27,047 | (337) | (80) | (80) |

| Cash flow from operations | 28,319 | 46,529 | 71,086 | 72,895 | 98,474 | 77,307 | 119,440 | 223,843 |

| Capex | (23,027) | (21,824) | (27,830) | (33,485) | (46,091) | (42,522) | (59,129) | (86,541) |

| Net (acquisitions)/disposals | (1,953) | (2,489) | (5,421) | (304) | (2,702) | 0 | 0 | 0 |

| Other investing CF items | (1,501) | (406) | (251) | (6,571) | (4,420) | 0 | 0 | 0 |

| Cash flow from investing | (26,481) | (24,719) | (33,502) | (40,360) | (53,214) | (42,522) | (59,129) | (86,541) |

| Change in debt | 6,993 | (1,900) | 10,327 | 7,135 | 11,729 | 0 | 0 | 0 |

| Net share issues/(repurchases) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Dividends paid | (15,751) | (15,026) | (27,455) | (18,696) | (20,313) | (30,132) | (46,756) | (74,030) |

| Other financing CF items | 421 | (2,814) | 6,651 | 444 | (817) | 0 | 0 | 0 |

| Cash flow from financing | (8,337) | (19,739) | (10,478) | (11,118) | (9,401) | (30,132) | (46,756) | (74,030) |

| Forex effect/others | (2,358) | 9,621 | (1,198) | 8,586 | (2,146) | 0 | 0 | 0 |

| Change in cash | (8,857) | 11,692 | 25,909 | 30,003 | 33,713 | 4,653 | 13,555 | 63,272 |

| Free cash flow | 5,292 | 24,705 | 43,257 | 39,410 | 52,383 | 34,785 | 60,311 | 137,302 |

Source: FactSet, Daiwa forecasts

Financial summary continued …

Balance sheet (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Cash & short-term investment | 51,268 | 63,572 | 92,620 | 121,793 | 155,113 | 159,766 | 173,321 | 236,594 |

| Inventory | 69,697 | 83,980 | 81,756 | 89,706 | 108,208 | 137,530 | 196,594 | 265,550 |

| Accounts receivable | 72,700 | 89,676 | 81,706 | 92,180 | 125,020 | 160,634 | 220,689 | 294,307 |

| Other current assets | 3,213 | 3,222 | 3,877 | 7,246 | 7,440 | 7,440 | 7,440 | 7,440 |

| Total current assets | 196,878 | 240,450 | 259,958 | 310,925 | 395,781 | 465,370 | 598,044 | 803,890 |

| Fixed assets | 76,607 | 86,267 | 98,002 | 115,710 | 142,040 | 155,397 | 180,642 | 226,735 |

| Goodwill & intangibles | 73,610 | 77,170 | 78,544 | 78,783 | 75,326 | 75,326 | 75,326 | 75,326 |

| Other non-current assets | 18,017 | 21,987 | 21,242 | 26,480 | 26,472 | 26,808 | 26,888 | 26,968 |

| Total assets | 365,112 | 425,874 | 457,747 | 531,898 | 639,619 | 722,902 | 880,901 | 1,132,920 |

| Short-term debt | 4,442 | 2,119 | 5,875 | 8,121 | 17,325 | 2,364 | 2,364 | 2,364 |

| Accounts payable | 54,570 | 62,716 | 53,539 | 69,223 | 94,452 | 94,712 | 125,786 | 178,820 |

| Other current liabilities | 49,157 | 60,179 | 66,671 | 74,939 | 97,888 | 97,888 | 97,888 | 97,888 |

| Total current liabilities | 108,169 | 125,013 | 126,085 | 152,283 | 209,665 | 194,964 | 226,039 | 279,072 |

| Long-term debt | 43,914 | 44,337 | 51,420 | 56,309 | 56,703 | 56,703 | 56,703 | 56,703 |

| Other non-current liabilities | 26,904 | 31,156 | 37,506 | 43,740 | 47,861 | 47,861 | 47,861 | 47,861 |

| Total liabilities | 178,988 | 200,507 | 215,011 | 252,332 | 314,230 | 299,529 | 330,603 | 383,637 |

| Share capital | 25,975 | 25,975 | 25,975 | 25,975 | 25,975 | 25,975 | 25,975 | 25,975 |

| Reserves/R.E./others | 128,811 | 160,813 | 173,188 | 204,112 | 242,083 | 340,067 | 466,991 | 665,976 |

| Shareholders' equity | 154,787 | 186,789 | 199,164 | 230,087 | 268,058 | 366,042 | 492,966 | 691,952 |

| Minority interests | 31,338 | 38,578 | 43,572 | 49,478 | 57,331 | 57,331 | 57,331 | 57,331 |

| Total equity & liabilities | 365,112 | 425,874 | 457,747 | 531,898 | 639,619 | 722,902 | 880,901 | 1,132,920 |

| EV | 6,314,481 | 6,307,518 | 6,294,302 | 6,278,170 | 6,262,301 | 6,242,687 | 6,229,132 | 6,165,860 |

| Net debt/(cash) | (2,912) | (17,115) | (35,325) | (57,363) | (81,085) | (100,699) | (114,254) | (177,526) |

| BVPS (TWD) | 59.590 | 71.910 | 76.674 | 88.579 | 103.197 | 140.919 | 189.782 | 266.387 |

Key ratios (%)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Sales (YoY) | 11.3 | 22.2 | 4.4 | 5.0 | 31.8 | 29.9 | 39.1 | 46.4 |

| EBITDA (YoY) | 2.6 | 24.4 | 3.6 | 16.2 | 53.8 | 47.0 | 51.9 | 53.4 |

| Operating profit (YoY) | (0.2) | 32.1 | (1.2) | 16.4 | 76.1 | 61.0 | 59.6 | 58.7 |

| Net profit (YoY) | 5.1 | 21.9 | 2.2 | 5.5 | 70.6 | 69.1 | 56.1 | 58.2 |

| Core EPS (fully-diluted) (YoY) | 5.1 | 21.9 | 2.2 | 5.5 | 70.6 | 69.1 | 56.1 | 58.2 |

| Gross-profit margin | 28.7 | 28.8 | 29.2 | 32.4 | 34.3 | 36.7 | 36.7 | 37.4 |

| EBITDA margin | 15.4 | 15.7 | 15.6 | 17.3 | 20.1 | 22.8 | 24.9 | 26.1 |

| Operating-profit margin | 10.0 | 10.8 | 10.2 | 11.3 | 15.1 | 18.7 | 21.5 | 23.3 |

| Net profit margin | 8.5 | 8.5 | 8.3 | 8.4 | 10.8 | 14.1 | 15.8 | 17.1 |

| ROAE | 17.8 | 19.1 | 17.3 | 16.4 | 24.1 | 32.1 | 36.9 | 42.4 |

| ROAA | 7.6 | 8.3 | 7.6 | 7.1 | 10.3 | 14.9 | 19.8 | 24.9 |

| ROCE | 13.8 | 16.4 | 14.3 | 14.8 | 22.6 | 30.6 | 39.5 | 48.3 |

| ROIC | 14.6 | 17.0 | 15.7 | 17.5 | 27.8 | 37.6 | 44.6 | 53.3 |

| Net debt to equity | net cash | net cash | net cash | net cash | net cash | net cash | net cash | net cash |

| Effective tax rate | 20.0 | 19.7 | 20.1 | 21.3 | 22.7 | 21.1 | 21.5 | 21.5 |

| Accounts receivable (days) | 79.7 | 77.1 | 78.0 | 75.4 | 71.4 | 72.3 | 69.4 | 64.1 |

| Current ratio (x) | 1.8 | 1.9 | 2.1 | 2.0 | 1.9 | 2.4 | 2.6 | 2.9 |

| Net interest cover (x) | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Net dividend payout | 56.1 | 53.3 | 78.2 | 50.0 | 51.6 | 50.1 | 46.0 | 46.7 |

| Free cash flow yield | 0.1 | 0.4 | 0.7 | 0.6 | 0.8 | 0.6 | 1.0 | 2.2 |

Source: FactSet, Daiwa forecasts

Company profile

Founded in 1971, Delta Electronics has been the global leader in switching power supply solutions since 2002 and DC brushless fans since 2006. Its business covers 3 key areas: power electronics (eg, power supplies, thermal management products and passive components), automation (eg, controllers, robot arms and building management systems), and infrastructure (eg, datacentre infrastructure, networking and EV charging).

ESG analysis

ESG risks

| Risks | Management | Analyst comments | |

|---|---|---|---|

| Executive/board quality | 1 | Delta's board has 7 non-independent and 5 independent directors with a term of three years. The total number of directors and ratio of independent directors appear higher than most other listed companies. Besides, according to Delta's CSR report, enhancing the board's functions is one of the key goals for the company to achieve better corporate governance; also, the board members' diversity and professionalism will be taken into consideration to ensure a good board quality. Moreover, the company evaluates all the directors in the board using internal regulations and an external independent institution each year and at least once every three years, respectively. We believe Delta has implemented relatively more enhanced measure than most listed firms to improve its board quality. | |

| G | Capital management | 2 | During 2016-19, Delta's payout ratio was stable in the range of c.70%, but fell to 56% in 2020 and 53% in 2021. For 2020, it was mainly due to a sizeable non-cash re-valuation gain after the acquisition of Delta Thailand (DET), while the company maintained more cash on hand to deal with the uncertainties caused by COVID-19. However, the DPS growth from 2016 to 2021 was limited, as Delta struggled with business diversification into new end-markets (eg, smartphone, NEV). We believe that Delta's effort started to bear fruit in recent years after its NEV business has gradually picked up. Overall, we see a stable dividend policy from Delta and expect its DPS to continue to grow YoY in the future given that they declared a TWD11.6 DPS for 2025 which |

| Related party & transaction | 1 | equals a 50% payout ratio. Revenue from related parties stood at 4% of total 2024 revenue and purchases from related parties were at 9%. We see limited risk from related party transactions. | |

| S | Supply chain management | 1 | Delta focuses on: 1) localised management, 2) supplier certification and risk management, and 3) supplier sustainability engagement as key initiatives under the scope of supply chain management. In 2019, 144 new suppliers joined Delta's supply chain system. All of them passed environmental and social evaluations, signed the declaration of "non-use of conflict materials", and complied with Responsible Business Alliance's (BRA) Code of Conduct. Also, these vendors had to implement and abide by Delta's supply chain CSR policy and code of conduct. To lower ESG risks, Delta carries out RBA audits and monitors high-risk critical suppliers each year. The suppliers that fail these audits have to provide detailed improvement plans in response to identified issues. Besides, Delta has surveyed a total of 263 suppliers with potential risk and 63 suppliers with high risk of the total 1,331 suppliers, based on its CSR policy and code of conduct. If these suppliers are flagged as high-risk and no concrete improvements are made, Delta may consider terminating cooperation and transactions with them to improve the company's engagement on supplier sustainability. Overall, we think Delta has a solid plan to improve its supply chain management with specific KPIs, including: 1) achieving supplier improvement rate of 80% in 2025, 2) reducing GHG emissions rate of critical suppliers by 10% in 2025, and 3) improving water saving rate of critical suppliers by 12% in 2025. |

| S | Data security | 2 | Delta's Information Security team created Delta's Information Security Policy in November 2013 and started providing educational training to global employees in 2014. Delta gradually introduced the Information Security Management System (ISMS) in 2016 and obtained the ISO 27001 international certification in 2018. According to ISO27001, Delta has to conduct at least one internal audit on information security and appoint an independent institution to conduct audit externally. According to Delta, no major deficiencies have been found in recent years. |

Note: Management score represents a company's ability to manage/benefit from certain ESG topics. The scores range from 1 to 3, with 1 being the strongest.

Update Date: 1 Jun 2026

Source: Daiwa, Company

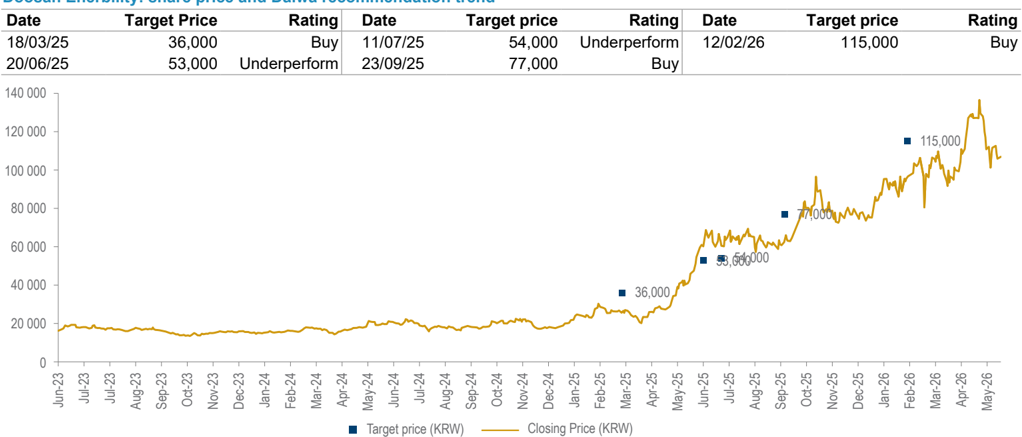

Doosan Enerbility: share price and Daiwa recommendation trend

| Date | Target Price | Rating | Date | Target price | Rating | Date | Target price | Rating |

|---|---|---|---|---|---|---|---|---|

| 18/03/25 | 36,000 | Buy | 11/07/25 | 54,000 | Underperform | 12/02/26 | 115,000 | Buy |

| 20/06/25 | 53,000 | Underperform | 23/09/25 | 77,000 | Buy |

Source: Daiwa

Note: where appropriate, historical target prices have been adjusted to reflect the current share count

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260601_2308_台達電_daiwa_Delta_003.png |

37KB | 真資料圖 | 分事業別 operating margin (quarterly) 折線圖(報告原文標題:Delta: operating margin by segment (quarterly)),橫軸 1Q23 至 1Q26,四條線分別為 Power Electronics(深藍)、Infrastructure(橘黃)、Automation(灰)、Mobility(虛線灰),Power Electronics 約 13-22%、Infrastructure 約 3-20%、Mobility 一度降至約 -10% |