PDF 原檔:260701_3711_日月光_ubs_ASE_original.pdf

圖片清單(已驗證 2026-07-02)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

| _001.png | 32KB | 裝飾·valuation | Upside/Downside spectrum 目標價區間圖(835 base / 1,100 upside / 470 downside) |

| _002.png | 67KB | 裝飾·valuation | Figure 3 毛利率趨勢折線圖(margins more resilient) |

| _003.png | 59KB | 裝飾·valuation | Figure 4 capex 趨勢柱狀圖(capex rebounded from trough) |

| _004.png | 29KB | 裝飾·valuation | Figure 8 P/BV band before SPIL consolidation |

| _005.png | 22KB | 裝飾·valuation | Figure 10 P/BV band after SPIL consolidation |

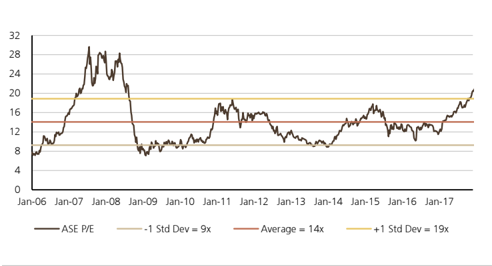

| _006.png | 28KB | 裝飾·valuation | Figure 9 PE band before SPIL consolidation |

| _007.png | 24KB | 裝飾·valuation | Figure 11 PE band after SPIL consolidation |

| _008.png | 96KB | 裝飾·文字卡 | Thesis map / 封面文字卡 |

全數為財務/估值圖表,無技術結構或供應鏈資料圖 → lib 頁不嵌入。

原始內容

ASE Industrial

Higher capex to power larger advanced packaging opportunity

Higher capex suggests stronger advanced packaging sales

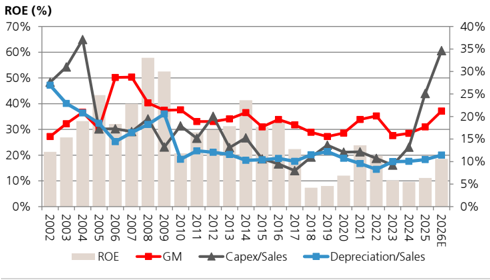

ASE has rallied 171% YTD, outperforming the 59% increase in Taiex, and we expect its strength to continue. We believe ASE is in the early stage of a multi-year fundamental transformation due to Cloud AI and the fast growing advanced packaging opportunity, and that ASE's industry position is strengthening. At its recent AGM, management flagged upside potential for its already elevated 2026 capex of US$8.5bn vs. TSMC's back-end capex of cUS$8.3bn in 2026. We raise our ASE 2026/27 capex forecasts to US $9.0bn/10.0bn from US$8.5bn/9.0bn.

LEAP sales to rise to US$3.6bn/6.7bn in 2026/27E

Our recent industry analysis indicates that ASE has been further accelerating full process CoWoS expansion. We forecast ASE's CoWoS capacity to increase from c20kwpm at end-2026 to c50kwpm at end-2027 vs. our prior estimate of 35-40kwpm. We think the significant expansion is to support stronger demand for AMD's new Venice server CPUs and possible upside for AI accelerators. We forecast ASE's full process CoWoS sales to rise from US$0.3bn in 2026 to US$2.0bn in 2027 with upside risk. The outlook for TSMC's on-substrate outsourcing, probing and final test has been strengthening as well. For final test, we expect ASE to grow sales in 2027E via Amazon's Trainium 3 and MediaTek's TPU v8t, both of which are set to ramp meaningfully next year. We forecast ASE's LEAP platform sales to rise from US$3.6bn in 2026 to US$6.7bn in 2027 vs. our prior estimate of US$5.8bn (see Figure 1 S A ' s E l e a d i n - v g c p k b u , for our detailed LEAP sales forecasts). We raise our IC ATM GM to 27.9%/32.8%/33.7% in 2026/27/28E.

Healthy outlook for mainstream packaging & testing

The traditional back-end outlook appears better than expected in coming quarters. We expect mature foundry utilisation to further improve in H226-2027E with stable consumer restocking, growing demand for servers, and an improving auto and industrial cycle. This should support ASE's mainstream semis sales growth to the guided 13-14% in 2026 and sustain growth in 2027E.

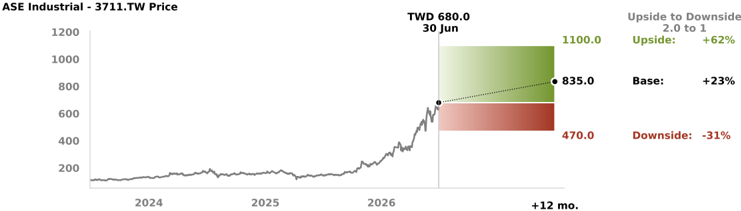

Valuation: raise price target to NT$835.00 from NT$660.00; reiterate Buy

We fine tune 2026E EPS and raise 2027/28E EPS by 11%/10% to factor in our more optimistic LEAP outlook. Our new PT is based on 25x 2027-28E PE vs. 25x 2027E PE previously, justified by 26% long-term earnings CAGR forecast. Key catalyst could be its upcoming earnings conference in late July, as we anticipate another solid set of earnings and guidance, and a potential capex upgrade.

| Equities | Equities | Equities | Equities |

|---|---|---|---|

| Taiwan | Taiwan | Taiwan | Taiwan |

| Semiconductors | Semiconductors | Semiconductors | Semiconductors |

| 12-month rating | 12-month rating | 12-month rating | Buy |

| 12m price target | 12m price target | 12m price target | NT$835.00 Prior : NT$660.00 |

| Price (30 Jun 2026) | Price (30 Jun 2026) | Price (30 Jun 2026) | NT$680.00 |

| RIC: 3711.TW BBG: 3711 TT | RIC: 3711.TW BBG: 3711 TT | RIC: 3711.TW BBG: 3711 TT | RIC: 3711.TW BBG: 3711 TT |

| Trading data and key metrics 52-wk | range | Trading data and key metrics 52-wk | NT$680.00-141.50 |

| Market cap. | Market cap. | Market cap. | NT$3,025b/US$95.0b |

| Shares o/s | Shares o/s | Shares o/s | 4,448m (ORD) |

| Free float | Free float | Free float | 73% |

| Avg. daily volume ('000) | Avg. daily volume ('000) | Avg. daily volume ('000) | 26,238 |

| Avg. daily value (m) | Avg. daily value (m) | Avg. daily value (m) | NT$14,215.1 |

| Common s/h equity (12/26E) | Common s/h equity (12/26E) | Common s/h equity (12/26E) | NT$387b |

| P/BV (12/26E) | P/BV (12/26E) | P/BV (12/26E) | 7.7x |

| Net debt to EBITDA (12/26E) | Net debt to EBITDA (12/26E) | Net debt to EBITDA (12/26E) | 1.4x |

| EPS (UBS, diluted) (NT$) | EPS (UBS, diluted) (NT$) | EPS (UBS, diluted) (NT$) | EPS (UBS, diluted) (NT$) |

| From | To | %ch Cons. | |

| 12/26E | 16.99 | 17.13 | 1 16.85 |

| 12/27E | 25.67 | 28.53 | 11 24.32 |

| 12/28E | 33.21 | 36.64 | 10 31.80 |

Sunny Lin

Analyst sunny.lin@ubs.com +886-2-8722 7346

Ryan Sun

Associate Analyst ryan-za.sun@ubs.com +886-2-8722 7267

Christine Chen

Associate Analyst christine.chen@ubs.com

+886-2-8722 7352

| Highlights (NT$m) | 12/23 | 12/24 | 12/25 | 12/26E | 12/27E | 12/28E | 12/29E | 12/30E |

|---|---|---|---|---|---|---|---|---|

| Revenues | 581,914 | 595,410 | 645,388 | 782,430 | 964,726 | 1,156,462 | 1,344,635 | 1,563,003 |

| EBIT (UBS) | 40,328 | 39,166 | 50,756 | 96,304 | 163,669 | 213,394 | 262,147 | 325,363 |

| Net earnings (UBS) | 31,725 | 32,482 | 40,658 | 76,835 | 127,952 | 164,342 | 203,520 | 253,759 |

| EPS (UBS, diluted) (NT$) | 7.30 | 7.41 | 9.20 | 17.13 | 28.53 | 36.64 | 45.38 | 56.58 |

| DPS (net) (NT$) | 5.23 | 5.33 | 6.09 | 11.42 | 19.02 | 24.43 | 30.25 | 37.72 |

| Net (debt) / cash | (68,222) | (89,834) | (145,683) | (267,602) | (387,295) | (468,674) | (500,904) | (477,538) |

| Profitability/valuation | 12/23 | 12/24 | 12/25 | 12/26E | 12/27E | 12/28E | 12/29E | 12/30E |

| EBIT (UBS) margin% | 6.9 | 6.6 | 7.9 | 12.3 | 17.0 | 18.5 | 19.5 | 20.8 |

| ROIC (EBIT)% | 11.1 | 10.9 | 12.1 | 17.8 | 22.6 | 23.6 | 24.9 | 27.9 |

| EV/EBITDA (UBS core) x | 5.7 | 7.2 | 6.7 | 17.2 | 10.8 | 8.4 | 6.9 | 5.6 |

| P/E (UBS, diluted) x | 15.5 | 20.7 | 18.5 | 39.7 | 23.8 | 18.6 | 15.0 | 12.0 |

| Equity FCF (UBS) yield% | 12.6 | 2.0 | (2.5) | (3.8) | (3.1) | (0.6) | 1.6 | 4.3 |

| Dividend yield (net)% | 4.6 | 3.5 | 3.6 | 1.7 | 2.8 | 3.6 | 4.4 | 5.5 |

Source: Company accounts, LSEG Eikon, UBS estimates. Metrics marked as (UBS) have had analyst adjustments applied. Valuations: based on an average share price that year, (E): based on a share price of NT$ 680.00 on 30-Jun-2026

Thesis Map UBS Research THESIS MAP a guide to our thinking and what´s where in this report

Pivotal Questions

UBS VIEW

EVIDENCE

WHAT´S PRICED IN?

Upside/Downside Spectrum

Company Description

Q: Can ASE's IC ATM GM continue to improve and be in line with its structural GM target?

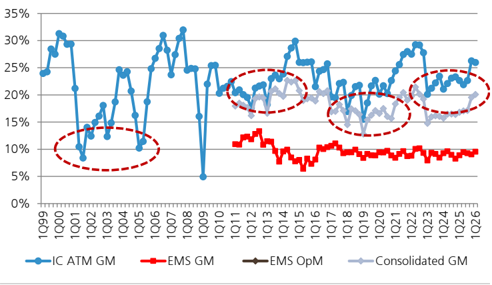

Likely. ASE's IC ATM GM reached 26.0% in Q126, and management expects a high 20-30% range by H226. We are optimistic about ASE's GM outlook in the next two to three years with strong expansion of LEAP , increasing turnkey testing and a rebound in non-AI demand. We forecast ASE's IC ATM GM to improve to 27.9% in 2026 and 32.8% in 2027 vs. 22.6% in 2023-25.

Q: Could ASE benefit from structural growth in advanced packaging and testing?

Yes. We expect ASE to grow LEAP and testing segment sales to US$3.6bn in 2026E and US$6.7bn in 2027E. We are positive about ASE's opportunity as: 1) it is the largest back-end supplier globally and has the largest scale to invest in R&D and capex; 2) its close collaboration with TSMC; and 3) upside potential in testing via the full turnkey service.

We are constructive about ASE's fundamental business transformation due to the LEAP platform and testing, and we expect meaningful upside for profitability and earnings for 2026E and beyond. We think ASE's strong earnings beat in Q1 was further evidence that its investment is starting to pay off and we expect further upside. We believe GM is on track to continue to strengthen based on the rising contribution from LEAP and testing, ASE's expanding scale and value add, and tighter traditional packaging supply/demand. ASE's ramp of full-process CoWoS could accelerate, given its improving technology maturity and customer diversification along with TSMC being more focused on higher-end solutions.

In April ASE raised its total capex target to US$8.5bn for 2026, a significant step up from US$5.5bn in 2025. At ASE's AGM in June 2026 , the CEO flagged the possibility of a further increase in capex. The increased investment is for 2027-28 and also for longer term plans, which could include developing new manufacturing sites as well as expanding existing sites. This reflects the robust future demand profile for Cloud AI in the upcoming years.

ASE has rallied 171% YTD, outperforming the 59% increase in Taiex. We believe the stock has room to continue to re-rate, driven by the increasing advanced packaging TAM and ASE's improving position in full-process CoWoS, probing and final test.

| Value drivers (2027/28E) | IC ATM revenue growth | EMS revenue growth | Gross margin |

|---|---|---|---|

| NT$1,100 upside | 33%/24% | 13%/17% | 25.5%/26.7% |

| NT$835 base | 30%/+22% | 12%/+16% | 25.0%/26.0% |

| NT$470 downside | 27%/19% | 10%/+14% | 24.9%/25.2% |

Source: UBS estimates

ASE Industrial is the holding company that controls ASE and Siliconware, and was the world's largest and assembly and testing service provider in 2024 in terms of revenue. In addition to semiconductor back-end services, ASE provides electronic manufacturing services (EMS).

Forecast changes and key financials

Figure 1: ASE's leading-edge advanced packaging business

| 2023 | 2024 | 2025 | 2026E | 2027E | |

|---|---|---|---|---|---|

| Leading edge adv packaging | 250 | 550 | 1,200 | 2,720 | 5,218 |

| Non CoWoS | 250 | 250 | 275 | 303 | 333 |

| CoWoS | 350 | 925 | 2,417 | 4,885 | |

| - TSMC's outsourced WoS | 311 | 886 | 2,098 | 2,935 | |

| Units (k per month) | 432 | 923 | 1,165 | 1,439 | |

| Unit service revenue (US$) | 60 | 80 | 150 | 170 | |

| - CoWoS S outsourcing (kwpm) | 14 | 15 | 10 | 10 | |

| - Units per interposer | 30 | 30 | 30 | 30 | |

| - CoWoS L outsourcing (kwpm) | 32 | 87 | 127 | ||

| - Units per interposer | 15 | 10 | 9 | ||

| - ASE's own CoWoS | 39 | 39 | 320 | 1,950 | |

| Units (kwpm) | 0.5 | 0.5 | 4.1 | 25 | |

| Unit revenue (US$) | 6,500 | 6,500 | 6,500 | 6,500 | |

| Testing | 50 | 400 | 875 | 1,500 | |

| LEAP & testing revenue (US$mn) | 250 | 600 | 1,600 | 3,595 | 6,718 |

| YoY | 140% | 167% | 125% | 87% | |

| %of IC ATM sales | 2% | 6% | 13% | 23% | 33% |

| %of whole company's sales | 1% | 3% | 8% | 15% | 22% |

Source: Company data, UBS estimates

Figure 2: ASE's operating metrics

| ASE Consolidated metrics | Q126 | Q226E | Q326E | Q426E | Q127E | Q227E | Q327E | Q427E | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue (NT$m) Sequential Change Gross Profit (NT$m) | 173,662 -2% 34,850 | 191,123 10% 39,304 | 207,151 8% 44,642 | 210,494 2% 47,436 | 210,600 0% 51,384 | 233,512 11% 58,338 | 257,622 10% 65,294 | 262,992 2% 66,154 | 670,873 18% 134,930 | 581,914 -13% 91,757 | 595,410 2% 96,932 | 645,388 8% 114,193 | 782,430 21% 166,232 | 964,726 23% 241,170 |

| Gross Margin | 20.1% | 20.6% | 21.6% | 22.5% | 24.4% | 25.0% | 25.3% | 25.2% | 20.1% | 15.8% | 16.3% | 17.7% | 21.2% | 25.0% |

| Operating Margin | 10.1% | 11.9% | 13.1% | 13.8% | 15.7% | 17.0% | 17.6% | 17.2% | 12.0% | 6.9% | 6.6% | 7.9% | 12.3% | 17.0% |

| Capex (NT$m) | 44,092 25.4% | 44,092 23.1% | 44,092 21.3% | 153,317 72.8% | 79,966 | 79,966 | 79,966 | 79,966 | 71,890 10.7% | 53,683 9.2% | 78,614 | 162,149 | 285,593 | 319,864 |

| Capex/revenue | 38.0% | 34.2% | 31.0% | 30.4% | 13.2% | 25.1% | 36.5% | 33.2% | ||||||

| Equipment capex (US$m) | 1,499 | 1,499 | 1,499 | 1,499 | 1,750 | 1,750 | 1,750 | 1,750 | 1,697 | 913 | 1,877 | 3,396 | 5,996 | 7,000 |

| Depreciation (NT$m) EPS (NT$) | 18,648 3.24 | 20,669 4.15 | 22,079 4.95 | 28,390 5.24 | 31,392 5.96 | 34,391 7.16 | 37,387 8.15 | 40,380 7.99 | 55,452 14.53 | 58,102 7.39 | 59,815 7.52 | 67,440 9.37 | 89,786 17.57 | 143,550 29.26 |

| ASE ATM metrics | Q126 | Q226E | Q326E | Q426E | Q127E | Q227E | Q327E | Q427E | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E |

| Revenue (NT$m) Sequential Change Gross Profit (NT$m) | 112,434 2% 29,198 | 123,264 10% | 130,239 6% | 135,791 4% | 143,207 5% | 159,122 11% | 171,467 8% | 177,067 3% | 372,176 11% | 315,115 -15% | 325,874 3% | 389,229 19% | 501,728 29% 140,105 | 650,863 30% 213,383 |

| 32,957 | 37,194 | 40,756 | 45,073 | 52,101 | 57,541 | 58,668 | 105,894 | 68,718 | 73,168 | 91,380 | ||||

| Gross Margin | 26.0% | 26.7% | 28.6% | 30.0% | 31.5% | 32.7% | 33.6% | 33.1% | 28.5% | 21.8% | 22.5% | 23.5% | 27.9% | 32.8% |

| ASE EMS metrics | Q126 | Q226E | Q326E | Q426E | Q127E | Q227E | Q327E | Q427E | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E |

| Revenue (NT$m) Sequential Change | 61,875 -10% | 67,858 10% | 76,912 13% | 74,703 -3% | 67,393 -10% | 74,389 10% | 86,155 16% | 85,925 0% | 301,982 26% | 268,309 -11% | 272,551 2% | 259,078 -5% | 281,349 9% | 313,863 12% |

| Gross Profit (NT$m) | 5,894 | 6,347 | 7,448 | 6,680 | 6,311 | 6,237 | 7,754 | 7,486 | 29,031 | 23,362 | 24,475 | 23,695 | 26,369 | 27,787 |

| Gross Margin | 9.4% | 9.7% | 8.9% | 9.4% | 8.4% | 8.7% | 8.7% | 9.1% | 8.9% | |||||

| 9.5% | 9.0% | 9.6% | 9.0% | 9.4% |

Source: Company data, UBS estimates Note: Our EPS estimates are based on basic EPS, and may differ from the table on the cover page

Figure 3: Margins more resilient in this cycle

Source: Company data, UBS estimates

Figure 4: Capex rebounded from a trough in 2024

Source: Company data, UBS estimates

Figure 5: Revisions to UBS earnings estimates

| New | New | New | Old | Old | Old | Change | Change | Change | |

|---|---|---|---|---|---|---|---|---|---|

| (NT$m) | 2026E | 2027E | 2028E | 2026E | 2027E | 2028E | 2026E | 2027E | 2028E |

| Revenue | 782,430 | 964,726 | 1,156,462 | 779,187 | 931,176 | 1,108,055 | 0% | 4% | 4% |

| - YoY chg | 21% | 23% | 20% | 21% | 20% | 19% | |||

| Revenue (US$m) | 24,657 | 30,337 | 36,367 | 24,555 | 29,282 | 34,845 | 0% | 4% | 4% |

| - YoY chg | 19% | 23% | 20% | 19% | 19% | 19% | |||

| Gross profit | 166,232 | 241,170 | 300,407 | 165,299 | 222,938 | 277,808 | 1% | 8% | 8% |

| - Gross margin | 21.2% | 25.0% | 26.0% | 21.2% | 23.9% | 25.1% | |||

| Operating profit | 96,304 | 163,669 | 213,394 | 95,507 | 146,745 | 192,634 | 1% | 12% | 11% |

| - Operating margin | 12.3% | 17.0% | 18.5% | 12.3% | 15.8% | 17.4% | |||

| Pretax profit | 98,122 | 162,025 | 207,512 | 97,328 | 146,019 | 188,275 | 1% | 11% | 10% |

| Reported net profit | 76,835 | 127,952 | 164,342 | 76,200 | 115,147 | 148,952 | 1% | 11% | 10% |

| - Net margin | 9.8% | 13.3% | 14.2% | 9.8% | 12.4% | 13.4% | |||

| - YoY chg | 89% | 67% | 28% | 87% | 51% | 29% | |||

| UBS EPS (NT$) | 17.57 | 29.26 | 37.58 | 17.42 | 26.33 | 34.06 | 1% | 11% | 10% |

| - YoY chg | 88% | 67% | 28% | 86% | 51% | 29% |

Source: Company data, UBS estimates Note: Our EPS estimates are based on basic EPS, and may differ from the table on the cover page

Figure 6: UBS earnings estimates vs. consensus pre-results

| UBSe | UBSe | UBSe | Consensus | Consensus | Consensus | Difference | Difference | Difference | |

|---|---|---|---|---|---|---|---|---|---|

| (NT$m) | 2026E | 2027E | 2028E | 2026F | 2027F | 2028F | 2026E | 2027E | 2028E |

| Revenue | 782,430 | 964,726 | 1,156,462 | 793,621 | 957,350 | 1,138,406 | -1% | 1% | 2% |

| - YoY chg | 21% | 23% | 20% | 23% | 21% | 19% | |||

| Gross profit | 166,232 | 241,170 | 300,407 | 167,758 | 222,514 | 278,063 | -1% | 8% | 8% |

| - Gross margin | 21.2% | 25.0% | 26.0% | 21.1% | 23.2% | 24.4% | |||

| Operating profit | 96,304 | 163,669 | 213,394 | 94,327 | 139,435 | 183,613 | 2% | 17% | 16% |

| - Operating margin | 12.3% | 17.0% | 18.5% | 11.9% | 14.6% | 16.1% | |||

| Net profit | 76,835 | 127,952 | 164,342 | 75,467 | 110,851 | 145,618 | 2% | 15% | 13% |

| - Net margin | 9.8% | 13.3% | 14.2% | 9.5% | 11.6% | 12.8% | |||

| EPS (NT$) | 17.57 | 29.26 | 37.58 | 17.26 | 25.36 | 33.32 | 2% | 15% | 13% |

| - YoY chg | 88% | 67% | 28% | 84% | 47% | 31% |

Source: Visible Alpha, UBS estimates Note: Our EPS estimates are based on basic EPS, and may differ from the table on the cover page

Figure 7: UBS earnings forecasts

| (NT$m) Revenue | 2025 645,388 | Q126 173,662 | Q226E 191,123 | Q326E 207,151 | Q426E 210,494 | 2026E 782,430 | Q127E 210,600 | Q227E 233,512 | Q327E 257,622 | Q427E 262,992 | 2027E 964,726 | 2028E 1,156,462 | 2029E 1,344,635 | 2030E 1,563,003 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| - QoQ chg | -2% | 10% | 8% | 2% | 0% | 11% | 10% | 2% | ||||||

| - YoY chg Revenue (US$m) | 8% 20,720 | 17% 5,508 -4% | 27% 6,010 9% | 23% 6,514 8% | 18% 6,619 2% | 21% 24,657 | 21% 6,623 0% | 22% 7,343 | 24% 8,101 10% | 25% 8,270 2% | 23% 30,337 | 20% 36,367 | 16% 42,284 | 16% 49,151 |

| - QoQ chg | 11% | 22% | 24% | 15% | 15% | 19% | 11% | 25% | 23% | 20% | 16% | 16% | ||

| - YoY chg | 114,193 | 34,850 | 39,304 | 44,642 | 47,436 | 166,232 | 20% 51,384 | 22% | 24% 65,294 | 66,154 | 241,170 | 300,407 | 358,411 | 430,301 |

| Gross profit - Gross margin | 20.1% | 20.6% | 21.6% | 22.5% | 58,338 | 25.3% | 25.2% | |||||||

| Operating | 17.7% | 21.2% | 24.4% | 25.0% | 25.0% | 26.0% | 26.7% | 27.5% | ||||||

| profit - Operating margin | 50,756 7.9% | 17,532 | 22,712 | 27,051 | 29,008 13.8% | 96,304 12.3% | 33,040 15.7% | 39,810 | 45,468 | 45,351 | 163,669 17.0% | 213,394 18.5% | 262,147 19.5% | 325,363 20.8% |

| Pre-tax income | 51,301 | 10.1% 18,200 | 11.9% 23,184 | 13.1% 27,575 | 29,163 | 98,122 | 33,124 | 17.0% 39,659 | 17.6% 45,046 | 17.2% 44,196 | 162,025 | 207,512 | 256,485 | 319,284 |

| Reported net profit | 40,658 | 14,148 | 18,130 | 21,643 | 22,914 | 76,835 | 26,082 | 31,310 | 35,620 | 34,940 | 127,952 | 164,342 | 203,520 | 253,759 |

| - Net margin | 6.3% | 9.5% | 10.4% | 10.9% | 9.8% | 12.4% | 13.4% | 13.8% | 13.3% | |||||

| 8.1% | 13.3% | 14.2% | 15.1% | 16.2% | ||||||||||

| Basic EPS (NT$) | 9.37 | 3.24 | 4.15 | 4.95 | 5.24 | 17.57 | 5.96 | 7.16 | 8.15 | 7.99 | 29.26 | 37.58 | 46.54 | 58.03 |

| - QoQ chg | 25% | -2% 88% | 28% | 19% | 6% | 88% | 14% 84% | 20% | 14% | -2% | ||||

| - YoY chg | 142% | 100% | 58% | 73% | 65% | 52% | 67% | 28% | 24% | 25% |

Source: Company data, UBS estimates Note: Our EPS estimates are based on basic EPS, and may differ from the table on the cover page

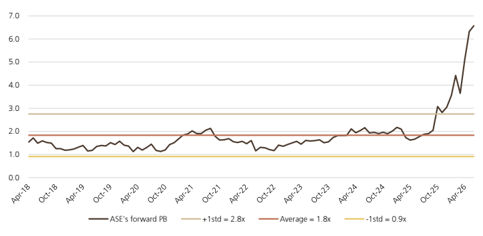

Figure 8: ASE's forward P/BV band before SPIL consolidation

Source: Company data, TEJ, UBS

Figure 10: ASE's forward P/BV band after SPIL consolidation

Source: Company data, LSEG

Figure 12: Peer valuation comparison

| Market cap | Price 30-Jun | Price target | EPS (LC$) | EPS (LC$) | EPS (LC$) | PE (x) | PE (x) | PB (x) | PB (x) | ROE (%) | ROE (%) | Div Yld (%) | Div Yld (%) | |||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Company | Ticker | (US$m) | (LC$) | (LC$) | Rating | 2025A | 2026E | 2027E | 2026E | 2027E | 2026E | 2027E | 2026E | 2027E | 2026E | 2027E |

| Semis Backend | ||||||||||||||||

| Amkor | AMKR.O | 20,224 | 82 | 80 | Neutral | 1.51 | 2.20 | 2.75 | 37.5 | 29.9 | 4.1 | 3.7 | 11.6 | 13.1 | 0.7 | 0.8 |

| ASE | 3711.TW | 94,923 | 680 | 835 | Buy | 9.37 | 17.57 | 29.26 | 38.7 | 23.2 | 7.7 | 6.4 | 20.9 | 30.0 | 1.7 | 2.8 |

| Chipbond | 6147.TWO | 4,943 | 211 | 340 | Buy | 3.76 | 5.50 | 8.22 | 38.5 | 25.7 | 3.2 | 3.0 | 8.5 | 12.1 | 1.3 | 1.8 |

| ChipMOS | 8150.TW | 2,200 | 100 | 105 | Buy | 0.69 | 3.98 | 5.43 | 25.0 | 18.3 | 2.7 | 2.5 | 11.3 | 14.1 | 1.2 | 2.0 |

| JCET | 600584.SS | 27,446 | 103 | 80 | Buy | 0.87 | 1.28 | 1.98 | 81.6 | 52.6 | 6.1 | 5.5 | 7.7 | 11.0 | 0.2 | 0.4 |

| KYEC | 2449.TW | 12,951 | 338 | 380 | Buy | 9.01 | 10.23 | 17.36 | 33.0 | 19.4 | 7.4 | 6.0 | 23.5 | 34.1 | 2.0 | 1.7 |

| Tianshui Huatian | 002185.SZ | 10,598 | 22 | 13 | Neutral | 0.22 | 0.29 | 0.37 | 77.2 | 60.7 | 3.9 | 3.6 | 5.2 | 6.2 | 0.1 | 0.2 |

| Average | 44.3 | 30.0 | 4.8 | 4.2 | 12.0 | 16.1 | 1.0 | 1.6 |

Source: LSEG, UBS estimates

Figure 9: ASE's forward PE band before SPIL consolidation

Source: Company data, TEJ, UBS

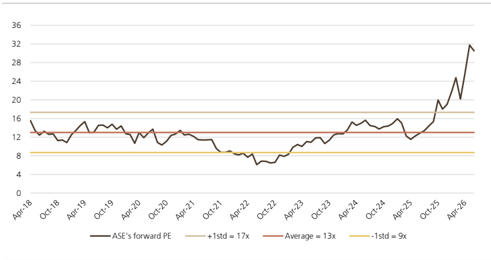

Figure 11: ASE's forward PE band after SPIL consolidation

Source: Company data, LSEG

ASE Industrial (3711.TW)

| Income Statement (NT$m) | 12/23 | 12/24 | 12/25 | 12/26E | %ch | 12/27E | %ch | 12/28E | 12/29E | 12/30E |

|---|---|---|---|---|---|---|---|---|---|---|

| Revenues | 581,914 | 595,410 | 645,388 | 782,430 | 21.2 | 964,726 | 23.3 | 1,156,462 | 1,344,635 | 1,563,003 |

| Gross profit | 91,757 | 96,932 | 114,193 | 166,232 | 45.6 | 241,170 | 45.1 | 300,407 | 358,411 | 430,301 |

| EBITDA (UBS) | 98,430 | 98,982 | 118,195 | 186,090 | 57.4 | 307,218 | 65.1 | 406,557 | 506,745 | 621,776 |

| Depreciation & amortisation | (58,102) | (59,815) | (67,440) | (89,786) | -33.1 | (143,550) | -59.9 | (193,162) | (244,598) | (296,413) |

| EBIT (UBS) | 40,328 | 39,166 | 50,756 | 96,304 | 89.7 | 163,669 | 70.0 | 213,394 | 262,147 | 325,363 |

| Associates & investment income | 1,654 | 868 | 829 | 728 | -12.2 | 0 | - | 0 | 0 | 0 |

| Other non-operating income | 5,302 | 6,614 | 5,786 | 7,516 | 29.9 | 8,578 | 14.1 | 12,000 | 14,800 | 14,800 |

| Net interest | (4,684) | (4,965) | (6,070) | (6,426) | -5.9 | (10,222) | -59.1 | (17,882) | (20,462) | (20,879) |

| Exceptionals (incl goodwill) | 0 | 0 | 0 | 0 | - | 0 | - | 0 | 0 | 0 |

| Pre-tax profit | 42,600 | 41,683 | 51,301 | 98,122 | 91.3 | 162,025 | 65.1 | 207,512 | 256,485 | 319,284 |

| Tax | (9,043) | (7,758) | (9,460) | (19,619) | -107.4 | (32,405) | -65.2 | (41,502) | (51,297) | (63,857) |

| Profit after tax | 33,557 | 33,926 | 41,841 | 78,503 | 87.6 | 129,620 | 65.1 | 166,010 | 205,188 | 255,427 |

| Preference dividends | 0 | 0 | 0 (1,182) | 0 (1,668) | - -41.1 | 0 (1,668) | - 0.0 | 0 (1,668) | 0 | 0 (1,668) |

| Minorities | (1,832) | (1,443) | 0 | - | 0 | 0 | (1,668) 0 | |||

| Extraordinary items | 0 | 0 | 0 | - | 0 | |||||

| Net earnings (local GAAP) | 31,725 | 32,482 | 40,658 | 76,835 | 89.0 | 127,952 | 66.5 | 164,342 | 203,520 | 253,759 |

| Net earnings (UBS) | 31,725 | 32,482 | 40,658 | 76,835 | 89.0 | 127,952 | 66.5 | 164,342 | 203,520 | 253,759 |

| Tax rate (%) | 21.2 | 18.6 | 18.4 | 20.0 | 8.4 | 20.0 | 0.0 | 20.0 | 20.0 | 20.0 |

| Per Share (NT$) | 12/23 | 12/24 | 12/25 | 12/26E | %ch | 12/27E | %ch | 12/28E | 12/29E | 12/30E |

| EPS (UBS, diluted) | 7.30 | 7.41 | 9.20 | 17.13 | 86.3 | 28.53 | 66.5 | 36.64 | 45.38 | 56.58 |

| EPS (local GAAP, diluted) | 7.30 | 7.41 | 9.20 | 17.13 | 86.3 | 28.53 | 66.5 | 36.64 | 45.38 | 56.58 |

| EPS (UBS, basic) | 7.39 | 9.37 | 17.57 | 29.26 | 66.5 | 37.58 | 58.03 | |||

| 7.52 | 87.6 | 19.02 | 66.5 | 24.43 | 46.54 | |||||

| DPS (net) (NT$) Cash EPS (UBS, diluted) 1 | 5.23 20.66 | 5.33 21.05 | 6.09 | 11.42 37.15 | 87.6 52.0 | 60.53 | 62.9 | 79.71 | 30.25 99.91 | 37.72 122.66 |

| Book value per share | 67.91 | 73.81 | 24.45 77.99 | 88.47 | 13.4 | 106.30 | 20.2 | 124.87 | 146.98 | 174.75 |

| Average shares (diluted) | 4,348 | 4,386 | 4,422 | 4,485 | 1.4 | 4,485 | 0.0 | 4,485 | 4,485 | 4,485 |

| Balance Sheet (NT$m) | 12/23 | 12/24 | 12/25 | 12/26E | %ch | 12/27E | %ch | 12/28E | 12/29E | 12/30E |

| Cash and equivalents Other current assets | 71,369 189,978 | 84,883 190,402 | 100,223 213,572 | 55,365 256,113 | -44.8 19.9 | 25,671 316,163 | -53.6 23.4 | 34,292 365,192 | 52,063 428,993 | 125,429 495,211 |

| Total current assets | 261,348 | 275,285 | 313,795 | 311,477 | 341,834 | 9.7 | 399,485 | 481,055 | 620,640 | |

| Net tangible fixed assets | 264,812 | 312,531 | 421,115 | 630,621 | -0.7 49.8 | 807,987 | 28.1 | 951,734 | 1,060,838 | 1,135,759 |

| Net intangible fixed assets | 69,569 | 67,562 | 64,807 | 64,253 | -0.9 | 63,201 | -1.6 | 62,148 | 61,096 | 60,044 |

| Investments / other assets | 70,847 | 85,319 | 89,617 | 102,238 | 14.1 | 112,102 | 9.6 | 119,884 | 130,114 | 140,973 |

| Total assets | 666,575 | 740,698 | 889,333 | 1,108,589 | 1,325,124 | 19.5 | 1,733,103 | 1,957,416 | ||

| 24.7 | 1,533,251 | 358,061 | ||||||||

| Trade payables & other ST liabilities | 184,611 | 195,951 | 212,523 | 269,105 | 26.6 | 291,554 | 8.3 | 307,584 | 333,758 | |

| Short term debt Total current liabilities | 37,737 222,348 | 34,989 230,940 | 31,825 244,349 | 31,825 300,930 | 0.0 23.2 | 31,825 323,380 | 0.0 7.5 | 31,825 339,410 | 31,825 365,584 | 31,825 389,887 |

| Long term debt | 101,854 | 139,728 | 214,081 | 291,141 | 36.0 | 381,141 | 30.9 | 471,141 | 521,141 | 571,141 |

| Other long term | 24,263 | 122,272 | 24.9 | 141,529 | 166,841 | |||||

| liabilities | 0 | 24,243 0 | 57,536 | 97,864 | 70.1 - | 0 | - | 0 | 0 | 193,712 0 |

| Preferred shares Total liabilities (incl pref shares) | 348,466 | 394,911 | 0 515,966 | 0 689,935 | 33.7 | 826,793 | 19.8 | 952,079 | 1,053,565 | 1,154,739 |

| Minority interests | 20,284 | 22,264 | 26,468 | 31,778 | 20.1 | 33,446 | 5.2 | 35,114 | 36,782 | 764,227 |

| Common s/h equity | 297,825 | 323,523 | 346,900 | 386,876 | 11.5 | 464,885 | 20.2 | 546,058 | 642,756 | 38,450 |

| Total liabilities & equity | 666,575 | 740,698 | 889,333 | 1,108,589 | 24.7 | 1,325,124 | 19.5 | 1,533,251 | 1,733,103 | 1,957,416 |

| Cash Flow (NT$m) | 12/23 | 12/24 | 12/25 | 12/26E | %ch | 12/27E | %ch | 12/28E | 12/29E | 12/30E |

| Net income (before pref divs) | 31,725 | 32,482 | 40,658 | 76,835 | 89.0 | 127,952 | 66.5 | 164,342 | 203,520 | 253,759 |

| Depreciation & amortisation | 58,102 | 59,815 | 67,440 | 89,786 | 33.1 | 143,550 | 59.9 | 193,162 | 244,598 | 296,413 |

| Net change in working capital | 32,233 | (4,856) | (9,916) | (11,270) | -13.7 | (29,166) | -158.8 - | (23,010) | (30,246) | (32,109) |

| Other operating | (5,807) | 4,789 | 45,250 | 16,607 | -63.3 | (16,631) | (16,104) | (15,942) | (18,998) | |

| Operating cash | 116,254 | 92,231 | 143,432 | 171,959 | 19.9 | 225,705 | 31.3 | 318,390 | 401,930 | 499,065 |

| flow Tangible capital expenditure | (53,683) | (78,614) | (162,149) 0 | (285,593) | -76.1 | (319,864) | -12.0 - | (335,857) | (352,650) | (370,282) |

| Intangible capital expenditure | 0 | 0 | 0 | - | 0 | 0 | 0 | 0 | ||

| Net (acquisitions) & disposals | 0 | 0 | 0 | - | 0 0 | - - | 0 0 | 0 | 0 | |

| Other investing | (1,439) | (5,295) | 0 (3,495) | (1,653) | 52.7 | 0 | 0 | |||

| Investing cash flow | (55,122) | (83,909) | (165,644) | (287,246) | -73.4 | (319,864) | -11.4 | (335,857) | (352,650) | (370,282) |

| Equity dividends paid | (37,841) | (22,459) | (23,034) 0 | (26,428) | -14.7 | (49,942) | -89.0 - | (83,169) | (106,822) | (132,288) 0 |

| Share issues / | 0 | 0 | - | 0 | 0 | |||||

| (buybacks) Other financing | 0 (443) | (1,299) | 24,408 | 36.4 | 0 | 25,312 | 26,871 | |||

| Change in debt & pref | (13,244) | 1,260 | 17,889 90,073 | NM 43.7 | 90,000 | -0.1 | 19,257 90,000 | 50,000 | 50,000 | |

| shares Financing cash flow | (51,528) | 15,452 (8,306) | 62,666 40,892 | 81,534 | 99.4 | 64,465 | -20.9 | 26,088 | (31,510) | (55,417) |

| Cash flow inc/(dec) in cash | 9,604 | 16 | 18,680 | (33,753) | - | (29,693) 0 | 12.0 | 8,621 0 | 17,770 | 73,366 0 |

| FX / non cash items | (3,100) | 13,498 | (3,340) | (11,106) | -232.5 | (29,693) | 100.0 | 0 | ||

| Balance sheet inc/(dec) in cash | 6,504 | 13,514 | 15,340 | (44,858) | - | 33.8 | 8,621 | 17,770 | 73,366 |

Source: Company accounts, UBS estimates. (UBS) metrics use reported figures which have been adjusted by UBS analysts. 1 Cash EPS (UBS, diluted) is calculated using UBS net income adding back depreciation and amortization.

ASE Industrial (3711.TW)

| Valuation (x) | 12/23 | 12/24 | 12/25 | 12/26E | 12/27E | 12/28E | 12/29E | 12/30E |

|---|---|---|---|---|---|---|---|---|

| P/E (local GAAP, diluted) | 15.5 | 20.7 | 18.5 | 39.7 | 23.8 | 18.6 | 15.0 | 12.0 |

| P/E (UBS, diluted) | 15.5 | 20.7 | 18.5 | 39.7 | 23.8 | 18.6 | 15.0 | 12.0 |

| P/CEPS | 5.4 | 7.2 | 6.8 | 17.8 | 11.0 | 8.3 | 6.6 | 5.4 |

| Equity FCF (UBS) yield% | 12.6 | 2.0 | (2.5) | (3.8) | (3.1) | (0.6) | 1.6 | 4.3 |

| Dividend yield (net)% | 4.6 | 3.5 | 3.6 | 1.7 | 2.8 | 3.6 | 4.4 | 5.5 |

| P/BV | 1.7 | 2.1 | 2.2 | 7.7 | 6.4 | 5.4 | 4.6 | 3.9 |

| EV/revenues (core) | 1.0 | 1.2 | 1.2 | 4.1 | 3.4 | 3.0 | 2.6 | 2.2 |

| EV/EBITDA (UBS core) | 5.7 | 7.2 | 6.7 | 17.2 | 10.8 | 8.4 | 6.9 | 5.6 |

| EV/EBIT (core) | 13.8 | 18.3 | 15.5 | 33.2 | 20.3 | 16.0 | 13.3 | 10.7 |

| EV/OpFCF (core) | 5.8 | 7.9 | 7.8 | 20.4 | 12.2 | 9.2 | 7.4 | 6.0 |

| EV/op. invested capital | 1.5 | 2.0 | 1.9 | 5.9 | 4.6 | 3.8 | 3.3 | 3.0 |

| Enterprise value (NT$m) | 12/23 | 12/24 | 12/25 | 12/26E | 12/27E | 12/28E | 12/29E | 12/30E |

| Market cap. | 494,905 | 672,556 | 744,420 | 3,024,624 | 3,024,624 | 3,024,624 | 3,024,624 | 3,024,624 |

| Net debt (cash) | 87,841 | 79,028 | 79,028 | 206,642 | 327,448 | 427,985 | 484,789 | 489,221 |

| Buy out of minorities | 19,462 | 21,274 | 24,366 | 29,123 | 32,612 | 34,280 | 35,948 | 37,616 |

| Pension provisions/other | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Total enterprise value | 602,208 | 772,858 | 847,814 | 3,260,390 | 3,384,685 | 3,486,889 | 3,545,361 | 3,551,461 |

| Non core assets | (44,303) | (57,173) | (60,306) | (62,687) | (62,687) | (62,687) | (62,687) | (62,687) |

| Core enterprise value | 557,905 | 715,685 | 787,508 | 3,197,703 | 3,321,998 | 3,424,202 | 3,482,675 | 3,488,775 |

| Growth (%) | 12/23 | 12/24 | 12/25 | 12/26E | 12/27E | 12/28E | 12/29E | 12/30E |

| Revenue | (13.3) | 2.3 | 8.4 | 21.2 | 23.3 | 19.9 | 16.3 | 16.2 |

| EBITDA (UBS) | (27.4) | 0.6 | 19.4 | 57.4 | 65.1 | 32.3 | 24.6 | 22.7 |

| EBIT (UBS) | (49.7) | (2.9) | 29.6 | 89.7 | 70.0 | 30.4 | 22.8 | 24.1 |

| EPS (UBS, diluted) | (49.1) | 1.5 | 24.1 | 86.3 | 66.5 | 28.4 | 23.8 | 24.7 |

| Net DPS | (40.9) | 2.0 | 14.1 | 87.6 | 66.5 | 28.4 | 23.8 | 24.7 |

| Margins & Profitability (%) | 12/23 | 12/24 | 12/25 | 12/26E | 12/27E | 12/28E | 12/29E | 12/30E |

| Gross profit margin | 15.8 | 16.3 | 17.7 | 21.2 | 25.0 | 26.0 | 26.7 | 27.5 |

| EBITDA margin | 16.9 | 16.6 | 18.3 | 23.8 | 31.8 | 35.2 | 37.7 | 39.8 |

| EBIT (UBS) margin | 6.9 | 6.6 | 7.9 | 12.3 | 17.0 | 18.5 | 19.5 | 20.8 |

| Net earnings (UBS) margin | 5.5 | 5.5 | 6.3 | 9.8 | 13.3 | 14.2 | 15.1 | 16.2 |

| ROIC (EBIT) | 11.1 | 10.9 | 12.1 | 17.8 | 22.6 | 23.6 | 24.9 | 27.9 |

| ROIC post tax | 8.6 | 8.8 | 9.9 | 14.2 | 18.1 | 18.9 | 19.9 | 22.3 |

| ROE (UBS) | 10.6 | 10.5 | 12.1 | 20.9 | 30.0 | 32.5 | 34.2 | 36.1 |

| Capital structure & Coverage (x) | 12/23 | 12/24 | 12/25 | 12/26E | 12/27E | 12/28E | 12/29E | 12/30E |

| Net debt / EBITDA | 0.7 | 0.9 | 1.2 | 1.4 | 1.3 | 1.2 | 1.0 | 0.8 |

| Net debt / total equity% | 21.4 | 26.0 | 39.0 | 63.9 | 77.7 | 80.6 | 73.7 | 59.5 |

| Net debt / (net debt + total equity)% | 17.7 | 20.6 | 28.1 | 39.0 | 43.7 | 44.6 | 42.4 | 37.3 |

| Net debt/EV% | 14.6 | 10.2 | 13.9 | 6.3 | 9.7 | 12.3 | 13.7 | 13.8 |

| Capex / depreciation% | 92.4 | 131.4 | NM | NM | NM | 173.9 | 144.2 | 124.9 |

| Capex / revenue% | 9.2 | 13.2 | 25.1 | NM | NM | 29.0 | 26.2 | 23.7 |

| EBIT / net interest | 9.0 | 8.1 | 8.5 | 15.1 | 16.0 | 11.9 | 12.8 | 15.6 |

| Dividend cover (UBS) | 1.4 | 1.4 | 1.5 | 1.5 | 1.5 | 1.5 | 1.5 | 1.5 |

| Div. payout ratio (UBS)% | 70.8 | 70.9 | 65.0 | 65.0 | 65.0 | 65.0 | 65.0 | 65.0 |

| Revenues by division (NT$m) | 12/23 | 12/24 | 12/25 | 12/26E | 12/27E | 12/28E | 12/29E | 12/30E |

| IC ATM | 315,115 | 325,874 | 389,229 | 501,728 | 650,863 | 793,415 | 931,463 | 1,096,688 |

| EMS | 268,309 | 272,551 | 259,078 | 281,349 | 313,863 | 363,046 | 413,173 | 466,316 |

| Others | (1,510) | (3,015) | (2,919) | (647) | 0 | 1 | (1) | (1) |

| Total | 581,914 | 595,410 | 645,388 | 782,430 | 964,726 | 1,156,462 | 1,344,635 | 1,563,003 |

| EBIT (UBS) by division (NT$m) | 12/23 | 12/24 | 12/25 | 12/26E | 12/27E | 12/28E | 12/29E | 12/30E |

| Others | 40,328 | 39,166 39,166 | 50,756 | 96,304 | 163,669 | 213,394 | 262,147 | 325,363 |

| 96,304 | 262,147 | 325,363 | ||||||

| Total | 40,328 | 50,756 | 163,669 | 213,394 |

Source: Company accounts, UBS estimates. (UBS) metrics use reported figures which have been adjusted by UBS analysts.

Forecast returns

| Forecast price appreciation | 22.8% |

|---|---|

| Forecast dividend yield | 1.7% |

| Forecast stock return | 24.5% |

| Market return assumption | 6.2% |

| Forecast excess return | 18.3% |

Company Description

ASE Industrial is the holding company that controls ASE and Siliconware, and is the world's largest and assembly and testing service providers in 2024 in terms of revenue. In addition to semiconductor back-end services, ASE provides electronic manufacturing services (EMS).

Valuation Method and Risk Statement

Our price target is based on a PE multiple relative to ASE and SPIL's previous historical valuation ranges.

We believe ASE Industrial faces a variety of upside and downside risks, including rapidlychanging technology, intense competition, high capital investment and cyclical demand.

Quantitative Research Review

UBS Global Research publishes a quantitative assessment of its analysts' responses to certain questions about the likelihood of an occurrence of a number of short term factors in a product known as the 'Quantitative Research Review'. The views for this month can be found below. Views contained in this assessment on a particular stock reflect only the views on those short term factors which are a different timeframe to the 12-month timeframe reflected in any equity rating set out in this note. For previous responses please make reference to (i) previous UBS Global Research reports; and (ii) where no applicable research report was published that month, the Quantitative Research Review which can be found at https://neo.ubs.com/quantitative, or contact your UBS sales representative for access to the report or the Quantitative Research Team on ubs-quant-answers@ubs.com. A consolidated report which contains all responses is also available and again you should contact your UBS sales representative for details and pricing or the Quantitative Research Team on the email above.

ASE Industrial

| Question | Response |

|---|---|

| 1. Is the industry structure facing the firm likely to improve or deteriorate over the next six months? Rate on a scale of 1-5 (1 = getting worse, 3 = no change, 5 = getting better, N/A = no view) | 4 |

| 2. Is the regulatory/government environment facing the firm likely to improve or deteriorate over the next six months? Rate on a scale of 1-5 (1 = getting tougher 3 = no change, 5 = getting better, N/A = no view) | 3 |

| 3. Over the last 3-6 months in broad terms have things been improving/no change/getting worse for this stock? Rate on a scale of 1-5 (1 = getting a lot worse, 3 = not much change, 5 = getting a lot better, N/A = no view) | 4 |

| 4. Relative to the current CONSENSUS EPS forecast, is the next company EPS update likely to lead to: (1 = negative surprise vs consensus, 3 = in-line with consensus, 5 = positive surprise vs consensus expectations, N/A = no view) | 3 |

| 5. What's driving the difference? | |

| 6. Relative to YOUR current earnings forecast, is there relatively greater risk at the next earnings result of:(1 = downside skew risk to earnings, 3 = equal upside or downside risk to earnings, 5 = upside skew risk to earnings, N/A = no view) | 3 |

| 7. What's driving the difference? | |

| 8. Is there an upcoming catalyst for the company over the next three months? | Positive Catalyst |

| 9. Is there an actual or approximate date for the catalyst? | |

| 10. Is the catalyst date an actual or approximate date? | |

| 11. What is the catalyst? |

Required Disclosures

This document has been prepared by UBS Securities Pte. Ltd., Taipei Branch, an affiliate of UBS AG. UBS AG, its subsidiaries, branches and affiliates, including former Credit Suisse AG and its subsidiaries, branches and affiliates are referred to herein as "UBS".

For information on the ways in which UBS manages conflicts and maintains independence of its UBS Global Research product; historical performance information; certain additional disclosures concerning UBS Global Research recommendations; and terms and conditions for certain third party data used in research report, please visit https://www.ubs.com/disclosures. Unless otherwise indicated, information and data in this report are based on company disclosures including but not limited to annual, interim, quarterly reports and other company announcements. The figures contained in performance charts refer to the past; past performance is not a reliable indicator of future results. Additional information will be made available upon request. UBS Securities Co. Limited is licensed to conduct securities investment consultancy businesses by the China Securities Regulatory Commission. UBS acts or may act as principal in the debt securities (or in related derivatives) that may be the subject of this report. This recommendation was finalized on: 01 July 2026 03:11 AM GMT. UBS has designated certain UBS Global Research department members as Derivatives Research Analysts where those department members publish research principally on the analysis of the price or market for a derivative, and provide information reasonably sufficient upon which to base a decision to enter into a derivatives transaction. Where Derivatives Research Analysts coauthor research reports with Equity Research Analysts or Economists, the Derivatives Research Analyst is responsible for the derivatives investment views, forecasts, and/or recommendations. Quantitative Research Review: UBS Global Research publishes a quantitative assessment of its analysts' responses to certain questions about the likelihood of an occurrence of a number of short term factors in a product known as the 'Quantitative Research Review'. Views contained in this assessment on a particular stock reflect only the views on those short term factors which are a different timeframe to the 12-month timeframe reflected in any equity rating set out in this note. For the latest responses, please see the Quantitative Research Review Addendum at the back of this report, where applicable. For previous responses please make reference to (i) previous UBS Global Research reports; and (ii) where no applicable research report was published that month, the Quantitative Research Review which can be found at https://neo.ubs.com/ quantitative, or contact your UBS sales representative for access to the report or the Quantitative Research Team on ubs-quantanswers@ubs.com. A consolidated report which contains all responses is also available and again you should contact your UBS sales representative for details and pricing or the Quantitative Research team on the email above.