PDF 原檔:260618_6831_邁科_daiwa_Taiwan Microloops _original.pdf

原始內容

Taiwan

Taiwan Microloops (6831 TT)

Taiwan Microloops

Target price:

TWD1,150.00

Share price (18 Jun): TWD773.00 | Up/downside: +48.8%

Initiation: ASIC thermal solutions share heating up

- Strong earnings visibility over 2026-28E

- Key supplier to one US ASIC client; another likely to be added in 2027

- Initiating with a Buy (1) rating and 12-month TP of TWD1,150

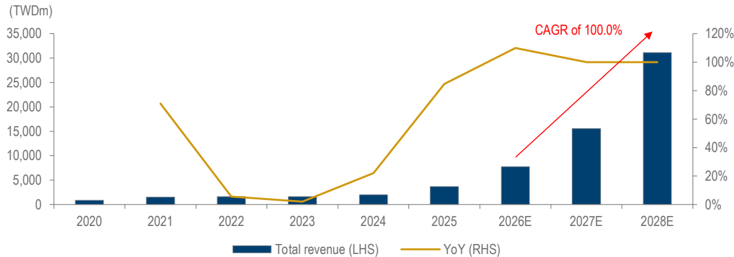

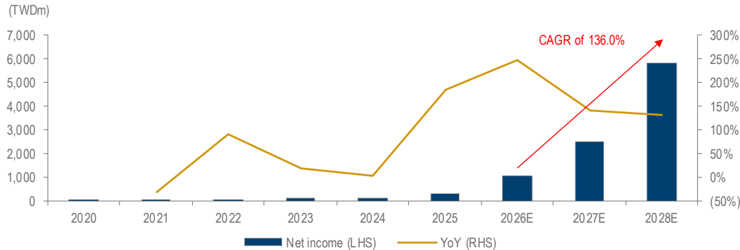

Investment case: We initiate coverage of Taiwan Microloops Corp. (Microloops), an emerging thermal module provider in Taiwan, with a Buy (1) rating. Microloops operates a vertically integrated model for its cooling products, incorporating know-how in areas such as design capability, automated vapour chamber (VC) module production and micron-level channel manufacturing. We forecast the company's revenue to rise at a CAGR of 100.0% and net profit at a CAGR of 136.0% over 2026-28E.

Riding the ASIC AI server expansion. Over the past 2 years, CSPs have been developing ASIC AI servers, designed exclusively for AI training and inference. This trend brings massive demand for air-cooling modules, where Microloops has an advantage due to its competitive 2.5DVC and 3DVC solutions. Fortune Business Insights and Precedence Research projects the thermal systems market and the global liquid cooling market to reach USD169bn and USD22bn by 2034E, respectively. Given Microloops' favourable position, broad product coverage and vertical capabilities, we expect it to significantly outgrow the market as customers migrate to higher -ASP solutions (from air cooling to liquid cooling modules from 2026).

Potential to grow market share with operating margin expansion. We forecast Microloops' revenue to rise at a 100.0% CAGR over 2026-28E, with margin expansion driven by: 1) rising operating leverage - Microloops' opex ratio has been falling as revenue scales, a trend we expect will continue given strong order visibility and growing demand for thermal efficiency AI servers; 2) improving product mix - a move to higher -margin segments; and 3) spec upgrades - rising thermal performance requirements in upcoming ASIC generations to lift Microloops' ASPs.

Catalysts: We believe near-term catalysts include mass shipment of nextgeneration ASIC AI servers, continued monthly revenue momentum; midto long-term catalysts include qualification from new CSP customers, mass shipment of CSP self-developed CPU racks and even GPU share gains.

Valuation: We initiate coverage with Buy (1) rating and TP of TWD1,150, based on a target PER of 40x (0.29x PEG over 2026-28E) applied to our one-year forward EPS. We are the first foreign broker to cover the name. We view our target valuation as undemanding, given its strong earnings visibility over our forecast horizon and favourable position in ASIC AI server thermal modules, hence, we believe the company deserves a re-rating in the next 12 months. Our DCF model yields a valuation of TWD1,213/share.

Risks: 1) weaker-than-expected global AI server demand, 2) slower-thanexpected progress in ASIC AI server development.

18 June 2026

4

Daiwa

5

3

2

1

Buy

Helen Chien

Helen Chien (886) 2 8758 6254

helen.chien@daiwacm-cathay.com.tw

Neil Teng (886) 2 8758 6256 neil.teng@daiwacm-cathay.com.tw

Share price performance

| 12-month range | 99.20-820.00 |

|---|---|

| Market cap (USDbn) | 1.65 |

| 3m avg daily turnover (USDm) | 27.56 |

| Shares outstanding (m) | 68 |

| Major shareholder | Chao family (20.0%) |

Financial summary (TWD)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue (m) | 7,777 | 15,554 | 31,108 |

| Operating profit (m) | 1,414 | 3,375 | 7,777 |

| Net profit (m) | 1,047 | 2,531 | 5,833 |

| Core EPS (fully-diluted) | 15.514 | 37.502 | 86.411 |

| EPS change (%) | 214.2 | 141.7 | 130.4 |

| Daiwa vs Cons. EPS (%) | 9.8 | 69.7 | n.a. |

| PER (x) | 49.8 | 20.6 | 8.9 |

| Dividend yield (%) | 1.2 | 2.9 | 6.7 |

| DPS | 9.3 | 22.5 | 51.8 |

| PBR (x) | 14.8 | 9.7 | 5.4 |

| EV/EBITDA (x) | 31.8 | 14.4 | 6.7 |

| ROE (%) | 33.0 | 56.9 | 77.4 |

Source: FactSet, Daiwa forecasts

Table of contents

| Rising star of ASIC thermal solutions......................................................................6 |

|---|

| Starting from air cooling… ...................................................................................................6 |

| …to liquid cooling.................................................................................................................7 |

| Competitive advantages..........................................................................................10 |

| High entry barriers to the segment.....................................................................................10 |

| Financial analysis.....................................................................................................13 |

| Strong order visibility, with growing revenue contribution from ASIC AI server thermal modules over 2026-28E.....................................................................................................13 |

| Gross- and operating-margin expansion trend ..................................................................13 |

| Net margin likely to rise over 2026-28E.............................................................................13 |

| Quarterly P&L ....................................................................................................................14 |

| Valuation and risks ..................................................................................................16 |

| Undemanding valuation on its global leading position and optimistic industry outlook......16 |

| Risks to our call..................................................................................................................18 |

| Appendix...................................................................................................................20 |

| Company background........................................................................................................20 |

| ESG analysis.............................................................................................................22 |

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

valuation carnings revisions

5

Daiwa

4

Growth outlook

We forecast Microloops to record a 136.0% net profit CAGR over 2026-28E, on the back of a 100% revenue CAGR over the same period, driven by: 1) spec upgrades, as higher thermal functionality requirements in the next generation of thermal solutions products for ASIC AI servers will likely support an upward ASP trend for Microloops, in our view; and 2) an improving product mix, with a more favourable product mix to thermal modules. We look for operating margin to expand by 3.5pp in 2027E and 3.3pp in 2028E, driven by operating leverage and economies of scale, and a better profit profile from liquid cooling modules.

Valuation

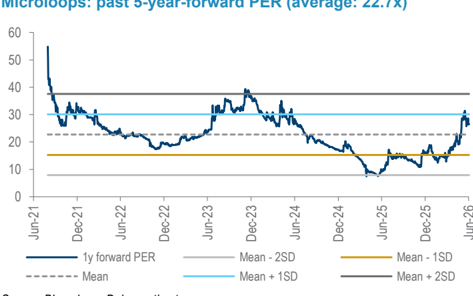

Our 12-month TP of TWD1,150 is based on a target PER of 40x applied to our 1-year forward EPS forecast (ie, 3Q26-2Q27E). Our target multiple of 40x is higher than the stock's past-3-year forward PER (21.5x) and past-5-year forward PER (22.7x), and implies a PEG of 0.29x on our 136.0% net profit CAGR forecast over 2026-28E.

Our TP is also supported by an alternative DCF valuation of TWD1,213/share.

Earnings revisions

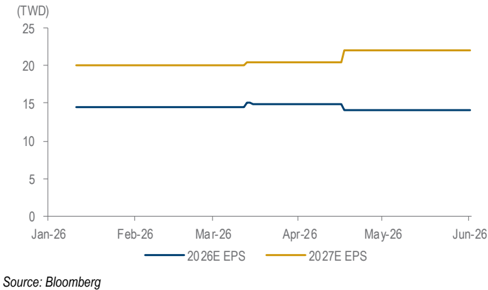

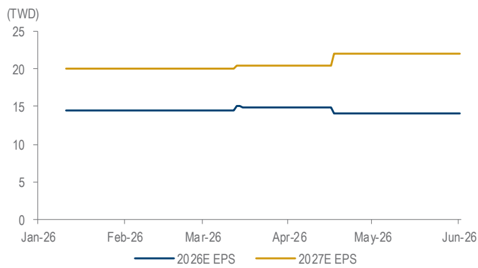

Since the first initiation of coverage by a local brokerage house on 23 January 2026, the Bloomberg consensus 2026E EPS estimate has been slightly lowered by 2.6%, but that for 2027E has risen by 10.5%. This is likely due to the better-than-expected 2027 guidance and the ongoing thermal solution upgrade trend. We are the first foreign broker to cover Microloops.

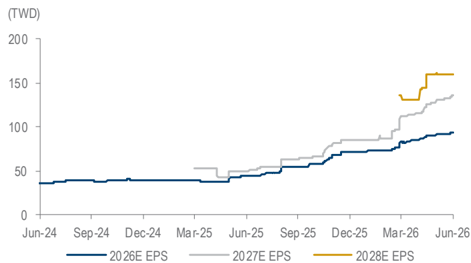

Microloops: net profit and net-profit growth

Source: Company, Daiwa forecasts

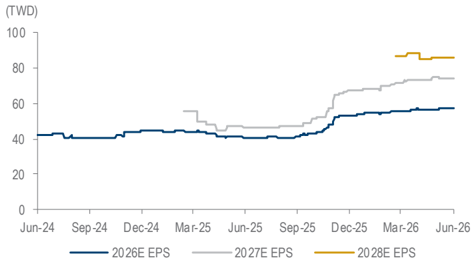

Microloops: 1-year-forward PER bands

Source: Bloomberg, Daiwa forecasts

Microloops: Bloomberg consensus EPS forecast revisions

Source: Bloomberg

3

2

1

Taiwan Microloops (6831 TT): 18 June 2026

Financial summary

Key assumptions

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Thermal module revenue growth (%) | 74.4 | 7.6 | 2.1 | 22.1 | 84.7 | 110.0 | 100.0 | 100.0 |

| Others revenue growth (%) | 111.1 | 81.5 | (51.9) | (9.7) | 289.9 | 110.0 | 100.0 | 100.0 |

| Key ASIC client revenue (TWDm) | 0 | 0 | 0.0 | 0.0 | 0 | 2,520.0 | 6,804.0 | 15,750.0 |

Profit and loss (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Thermal module | 1,493 | 1,607 | 1,641 | 2,005 | 3,702 | 7,773 | 15,546 | 31,093 |

| Others | 1 | 1 | 1 | 0 | 2 | 4 | 8 | 15 |

| Other Revenue | 30 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Total Revenue | 1,524 | 1,608 | 1,642 | 2,005 | 3,703 | 7,777 | 15,554 | 31,108 |

| Other income | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| COGS | (1,245) | (1,245) | (1,258) | (1,542) | (2,835) | (5,755) | (11,354) | (22,087) |

| SG&A | (141) | (169) | (184) | (205) | (268) | (373) | (513) | (778) |

| Other op.expenses | (100) | (85) | (91) | (130) | (174) | (234) | (311) | (467) |

| Operating profit | 38 | 108 | 109 | 127 | 426 | 1,414 | 3,375 | 7,777 |

| Net-interest inc./(exp.) | (6) | (7) | 8 | 8 | (9) | 3 | 0 | 0 |

| Assoc/forex/extraord./others | (5) | 9 | 17 | 6 | (69) | (21) | 0 | 0 |

| Pre-tax profit | 28 | 111 | 134 | 141 | 348 | 1,396 | 3,375 | 7,777 |

| Tax | 18 | (23) | (31) | (35) | (48) | (349) | (844) | (1,944) |

| Min. int./pref. div./others | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Net profit (reported) | 46 | 87 | 103 | 106 | 301 | 1,047 | 2,531 | 5,833 |

| Net profit (adjusted) | 46 | 87 | 103 | 106 | 301 | 1,047 | 2,531 | 5,833 |

| EPS (reported)(TWD) | 1.215 | 2.223 | 2.033 | 1.800 | 4.943 | 15.514 | 37.502 | 86.411 |

| EPS (adjusted)(TWD) | 1.215 | 2.223 | 2.033 | 1.800 | 4.943 | 15.514 | 37.502 | 86.411 |

| EPS (adjusted fully-diluted)(TWD) | 1.214 | 2.214 | 2.024 | 1.794 | 4.938 | 15.514 | 37.502 | 86.411 |

| DPS (TWD) | 0.000 | 0.190 | 0.780 | 1.250 | 3.000 | 9.308 | 22.501 | 51.846 |

| EBIT | 38 | 108 | 109 | 127 | 426 | 1,414 | 3,375 | 7,777 |

| EBITDA | 112 | 185 | 204 | 246 | 493 | 1,643 | 3,740 | 8,311 |

Cash flow (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Profit before tax | 28 | 111 | 134 | 141 | 348 | 1,396 | 3,375 | 7,777 |

| Depreciation and amortisation | 79 | 67 | 78 | 113 | 136 | 249 | 364 | 534 |

| Tax paid | (3) | (7) | (9) | (3) | (53) | (349) | (844) | (1,944) |

| Change in working capital | (141) | 29 | (12) | (114) | (679) | (1,231) | (2,995) | (5,236) |

| Other operational CF items | 53 | 74 | (12) | (0) | 6 | (3) | (0) | 0 |

| Cash flow from operations | 16 | 274 | 180 | 137 | (240) | 63 | (99) | 1,131 |

| Capex | (393) | (85) | (167) | (511) | (325) | (520) | (900) | (1,200) |

| Net (acquisitions)/disposals | 19 | (17) | 325 | 10 | (105) | (105) | (105) | (105) |

| Other investing CF items | (13) | (17) | (18) | (17) | (12) | 0 | 0 | 0 |

| Cash flow from investing | (387) | (119) | 140 | (518) | (442) | (625) | (1,005) | (1,305) |

| Change in debt | 274 | (95) | (248) | 20 | 363 | 617 | 2,500 | 2,500 |

| Net share issues/(repurchases) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Dividends paid | 0 | 0 | (23) | (44) | (75) | (203) | (628) | (1,519) |

| Other financing CF items | (12) | 268 | (42) | 320 | 956 | 0 | 0 | 0 |

| Cash flow from financing | 262 | 172 | (313) | 296 | 1,245 | 414 | 1,872 | 981 |

| Forex effect/others | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Change in cash | (109) | 327 | 7 | (85) | 563 | (148) | 768 | 807 |

| Free cash flow | (377) | 121 | 16 | (382) | (563) | (457) | (999) | (69) |

Source: FactSet, Daiwa forecasts

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

Financial summary continued …

Balance sheet (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Cash & short-term investment | 277 | 603 | 609 | 528 | 1,106 | 958 | 1,727 | 2,534 |

| Inventory | 226 | 207 | 194 | 207 | 439 | 824 | 1,477 | 2,813 |

| Accounts receivable | 546 | 442 | 657 | 869 | 1,932 | 3,573 | 7,478 | 14,624 |

| Other current assets | 37 | 23 | 25 | 69 | 188 | 188 | 188 | 188 |

| Total current assets | 1,086 | 1,275 | 1,485 | 1,673 | 3,665 | 5,544 | 10,869 | 20,159 |

| Fixed assets | 498 | 534 | 329 | 809 | 1,017 | 1,422 | 2,153 | 3,104 |

| Goodwill & intangibles | 12 | 8 | 10 | 36 | 24 | 24 | 24 | 24 |

| Other non-current assets | 96 | 138 | 93 | 312 | 312 | 312 | 312 | 312 |

| Total assets | 1,692 | 1,956 | 1,917 | 2,830 | 5,018 | 7,301 | 13,358 | 23,599 |

| Short-term debt | 126 | 38 | 0 | 20 | 383 | 500 | 1,500 | 2,500 |

| Accounts payable | 587 | 535 | 697 | 888 | 1,379 | 2,333 | 4,053 | 7,458 |

| Other current liabilities | 29 | 41 | 67 | 91 | 217 | 217 | 217 | 217 |

| Total current liabilities | 743 | 613 | 764 | 999 | 1,980 | 3,050 | 5,770 | 10,175 |

| Long-term debt | 218 | 210 | 0 | 0 | 0 | 500 | 2,000 | 3,500 |

| Other non-current liabilities | 44 | 54 | 18 | 257 | 220 | 220 | 220 | 220 |

| Total liabilities | 1,004 | 877 | 781 | 1,257 | 2,200 | 3,770 | 7,990 | 13,895 |

| Share capital | 374 | 434 | 509 | 600 | 675 | 675 | 675 | 675 |

| Reserves/R.E./others | 313 | 644 | 626 | 973 | 2,143 | 2,856 | 4,692 | 9,029 |

| Shareholders' equity | 688 | 1,079 | 1,135 | 1,573 | 2,818 | 3,531 | 5,367 | 9,704 |

| Minority interests | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Total equity & liabilities | 1,692 | 1,956 | 1,917 | 2,830 | 5,018 | 7,301 | 13,358 | 23,599 |

| EV | 52,245 | 51,823 | 51,569 | 51,670 | 51,455 | 52,219 | 53,951 | 55,644 |

| Net debt/(cash) | 67 | (355) | (609) | (508) | (723) | 42 | 1,773 | 3,466 |

| BVPS (TWD) | 18.370 | 27.413 | 22.313 | 26.725 | 46.337 | 52.318 | 79.517 | 143.761 |

Key ratios (%)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Sales (YoY) | 70.8 | 5.5 | 2.1 | 22.1 | 84.7 | 110.0 | 100.0 | 100.0 |

| EBITDA (YoY) | 3.7 | 64.5 | 10.6 | 20.5 | 100.7 | 232.9 | 127.7 | 122.2 |

| Operating profit (YoY) | (51.7) | 181.1 | 0.9 | 16.9 | 234.4 | 231.9 | 138.6 | 130.4 |

| Net profit (YoY) | (32.0) | 92.2 | 18.2 | 2.4 | 183.8 | 248.3 | 141.7 | 130.4 |

| Core EPS (fully-diluted) (YoY) | (40.3) | 82.3 | (8.6) | (11.4) | 175.3 | 214.2 | 141.7 | 130.4 |

| Gross-profit margin | 18.3 | 22.6 | 23.4 | 23.1 | 23.4 | 26.0 | 27.0 | 29.0 |

| EBITDA margin | 7.4 | 11.5 | 12.4 | 12.3 | 13.3 | 21.1 | 24.0 | 26.7 |

| Operating-profit margin | 2.5 | 6.7 | 6.6 | 6.4 | 11.5 | 18.2 | 21.7 | 25.0 |

| Net profit margin | 3.0 | 5.4 | 6.3 | 5.3 | 8.1 | 13.5 | 16.3 | 18.8 |

| ROAE | 6.8 | 9.9 | 9.3 | 7.8 | 13.7 | 33.0 | 56.9 | 77.4 |

| ROAA | 3.2 | 4.8 | 5.3 | 4.5 | 7.7 | 17.0 | 24.5 | 31.6 |

| ROCE | 4.4 | 9.2 | 8.9 | 9.3 | 17.8 | 36.6 | 50.4 | 63.3 |

| ROIC | 11.7 | 11.6 | 13.4 | 12.0 | 23.3 | 37.4 | 47.3 | 57.4 |

| Net debt to equity | 9.8 | n.a. | n.a. | n.a. | n.a. | 1.2 | 33.0 | 35.7 |

| Effective tax rate | (64.9) | 20.9 | 22.9 | 25.1 | 13.7 | 25.0 | 25.0 | 25.0 |

| Accounts receivable (days) | 102.2 | 112.2 | 122.2 | 138.9 | 138.0 | 129.2 | 129.7 | 129.7 |

| Current ratio (x) | 1.5 | 2.1 | 1.9 | 1.7 | 1.9 | 1.8 | 1.9 | 2.0 |

| Net interest cover (x) | 6.7 | 16.4 | n.a. | n.a. | 48.1 | n.a. | n.a. | n.a. |

| Net dividend payout | 0.0 | 8.5 | 38.4 | 69.4 | 60.7 | 60.0 | 60.0 | 60.0 |

| Free cash flow yield | n.a. | 0.2 | 0.0 | n.a. | n.a. | n.a. | n.a. | n.a. |

Source: FactSet, Daiwa forecasts

Company profile

Founded in 2002, Taiwan Microloops Corp. (Microloops) is a leading global provider of system-level thermal modules for AI data centres, including ASICs, network interface cards (NICs) and switches, as well as notebooks and graphics cards (VGAs). Headquartered in New Taipei City, Taiwan, the company operates manufacturing facilities in China and Vietnam. Its core product offerings currently focus on aircooling solutions, including 2.5DVC and 3DVC modules, while it is also expanding into liquid cooling, and developing immersion cooling technologies for next-generation servers in collaboration with Intel.

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

Microloops benefits from fast-growing thermal solution demand for ASIC servers, most of which adopt air cooling solutions

Taiwan Microloops (6831 TT): 18 June 2026

Rising star of ASIC thermal solutions

Starting from air cooling…

Air cooling usage booms as low-TDP ASIC servers expand faster than expected

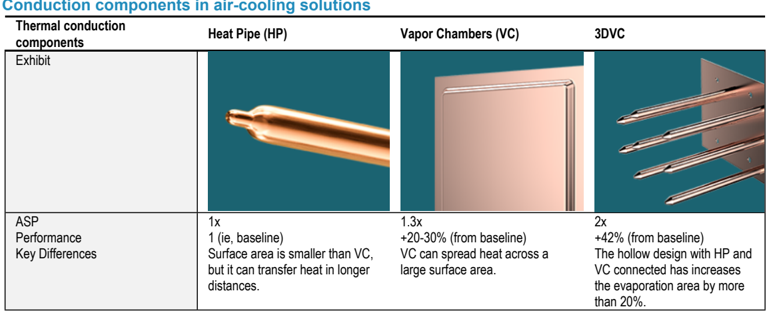

We believe air-cooling solutions, which comprise fins, heat pipes (HPs), vapour chambers (VCs) and cooling fans, remain the mainstream choice across most infrastructure segments, given their cost-performance value. To tackle rising power consumption, one primary method is to introduce more complicated convection components in air-cooling solutions, in our view. This is demonstrated by Amazon's Trainium 2 (T2) and Trainium 3 (T3) platforms, which use 2.5DVC to expand the conduction area instead of relying solely on heat pipes. Through these increasingly complicated designs, advanced air-cooling solutions can currently support thermal design power (TDP) of up to 1,000W.

We believe this sustained demand for high-efficiency air cooling is further driven by a structural market movement towards ASIC servers among major cloud providers such as AWS, Meta, Microsoft and Google. These custom ASICs are expanding faster than general-purpose GPUs-though both are growing very fast-because they are structurally optimised for specific AI training and inference workloads, in our view. For hyperscaler applications, we believe air cooling is selected because it optimally balances necessary heat dissipation with lower operational complexity and a reduced total cost of ownership (TCO). This structural preference is clearly reflected in AWS's T3 platform, where supply chain data indicates that only 20-30% of T3 racks will adopt liquid cooling, leaving a dominant 70-80% of the base relying entirely on air-cooled infrastructure, according to our supply chain checks.

Microloops is set to benefit from the trend

Microloops is successfully capturing the volume expansion in custom AI ASICs. While the market narrative heavily emphasises liquid cooling adoption, the company is well positioned to capitalise on the high-volume air-cooled baseline, supported by a tier-one CSP validation and highly automated manufacturing capabilities. This growth thesis is firmly anchored by the sustained use of advanced air cooling, including 2.5DVC and 3DVC modules, in custom ASIC deployments, which provides a solid volume foundation for Microloops' advanced air thermal solutions.

The company is well positioned to capture this massive scaling trend. According to our supply chain checks, total volume of AWS ASIC chips alone is projected to reach c.2.0m units in 2026E. Specialising in high-performance VC technology rather than commoditised cooling products, Microloops is a qualified Approved Vendor List (AVL) supplier for one major CSP client, providing 2.5D/3DVC air-cooling modules that power both the secondand third-generation ASIC platforms. The company also expects to be approved by at least another CSP by 2027. Furthermore, as next-generation ASIC chips increase in thermal density, the technical complexity of these air-cooling modules has increased the value per unit; for example, the ASP of thermal modules for network interface cards (NICs) is expected to increase by 10% as the architecture transitions from T2 to T3.

Daiwa

Heat Pipe (HP)

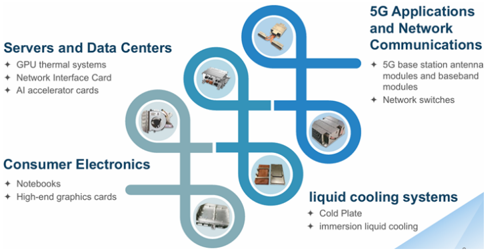

Microloops: main products and applications

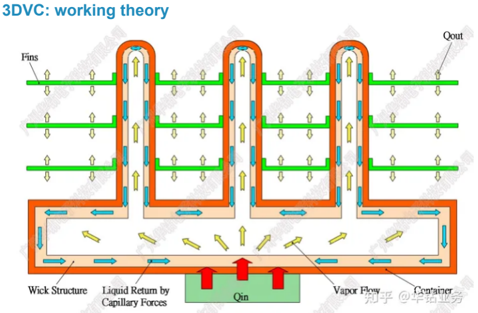

3DVC: working theory

Fins

1x

Wick Structure

Liquid Return by

Capillary Forces

Source• Guanazhou Huazuan Flect Techl

Vapor Chambers (VC)

Vapor Chambers (VC)

1.3x

3DVe

5G Applications and Network

Qout

Communications

- 5G base station antenna modules and baseband

modules

• Network switches

Source: Cooler Master, Auras, AVC, Celsia

Microloops: main products and applications

Source: Company

ASIC servers are transitioning from air cooling to liquid cooling

…to liquid cooling

In the long term, liquid cooling is inevitable

The adoption of liquid cooling in ASIC servers has become an inevitable trend across the industry. As performance demands for AI computing escalate, chip TDP continues to rise; once TDP approaches or exceeds 1,000W, traditional air-cooling solutions can no longer adequately meet dissipation requirements. This generational transition is directly driving liquid cooling penetration. Within the AWS ASIC platform, for instance, the T2 generation relied primarily on air cooling, but we project liquid cooling penetration to reach 20-30% in the T3 generation, particularly commencing in 2H26.

Furthermore, thermal requirements are extending beyond main processors to peripheral components within the data centre. Next-generation AI NICs and 1.6T switches are increasingly moving towards liquid-cooled designs to handle heightened thermal loads. Consequently, large CSPs are actively transitioning their physical infrastructure towards liquid cooling technologies, including cold plates, to improve power usage effectiveness (PUE) and support high-density data centres.

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

Source: Guangzhou Huazuan Elect.Tech

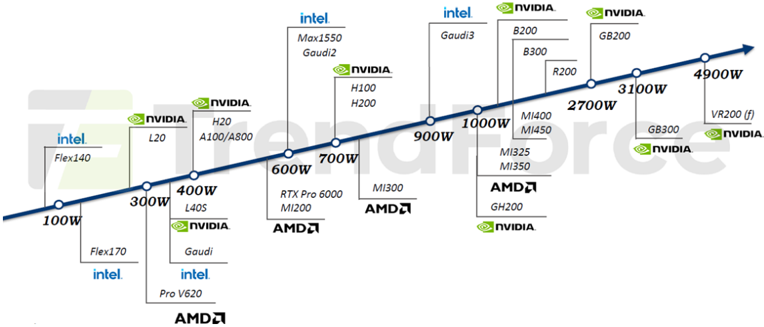

Thermal design power demand as Al server generation evolves intel.

Max1550

Gaudi2

@. NVIDIA

H100

H200

intel.

nVIDIA

Gaudi3

B200

B300

R200

3100W

2700W

intel.

Flex140

100W

Flex170

intel.

Source: Trendforce. Daiwa

@ NVIDIA.

L20

300W

nVIDIA.

H20

A100/A800

400W

L40S

• NVIDIA

Gaudi intel.

Pro V620

AMDA

1000W

MI400

4900W

VR200 (f)

Thermal design power demand as AI server generation evolves

600W

700W

RTX Pro 6000

MI200

AMDA

Source: Trendforce, Daiwa

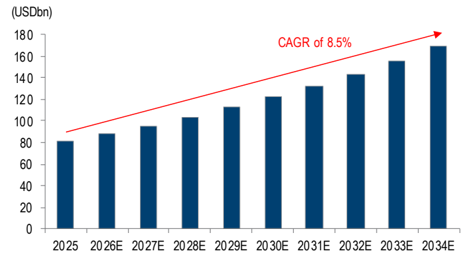

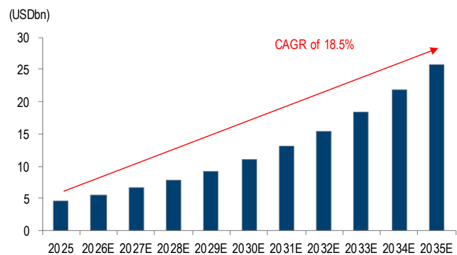

The ongoing CPU, GPU, and ASIC spec upgrade trend will likely lead to an expansion in the size of the thermal solutions market under the AI theme, in our view. Fortune Business Insights projects the global thermal systems market size to expand at a CAGR of 8.5% over 2025-34E and Precedence Research projects the global liquid cooling market size to expand at a CAGR of 18.5% over 2025-35E. We believe spec upgrades have become a structural and favourable trend for Taiwan's thermal makers, offering additional potential for order-share gains.

Global: thermal system market size and growth

Source: Fortune Business Insights, Daiwa

Microloops provides liquid cooling solutions for ASICs, GPUs, CPUs, NICs and switches

Global: data centre liquid cooling market size and growth

Source: Precedence Research, Daiwa

Microloops is set to benefit from the upgrade to liquid cooling

Importantly, backing Microloops' air-cooling business line does not conflict with the structural upside seen in high-end liquid cooling or advanced materials providers; instead, it highlights a complementary ecosystem in which different players capture distinct pools of value, in our view. Within this framework, Microloops provides mature and highly recognised 2.5DVC air-cooling solutions, while still a share gainer in the liquid cooling field, offering clients advanced liquid cooling modules with its in-house-developed cold plates.

Meanwhile, other Taiwanese competitors represent the premium liquid cooling standard, capturing the top-tier, highest-wattage training nodes. For the 20-30% of liquid-cooled T3 racks and premium Nvidia Blackwell/Rubin clusters, these competitors secure allocation and value via system-level liquid cold plates and coolant distribution units (CDUs), in our view. Whether a chip transfers heat into a 2.5DVC or a liquid cold plate, it requires a precise heat spreader at the silicon interface, suggesting chip-level protection and heat dissipation remain a must across the whole thermal solution chain.

Product-wise, Microloops is deeply integrated into the CSP client's ecosystem, supplying thermal modules for self-developed CPUs and maintaining a dominant market share in NIC

MI350

• nVIDIA

Taiwan Microloops (6831 TT): 18 June 2026

GB200

Daiwa

Microloops: immersion cooling applications

Microloops: liquid cooling applications

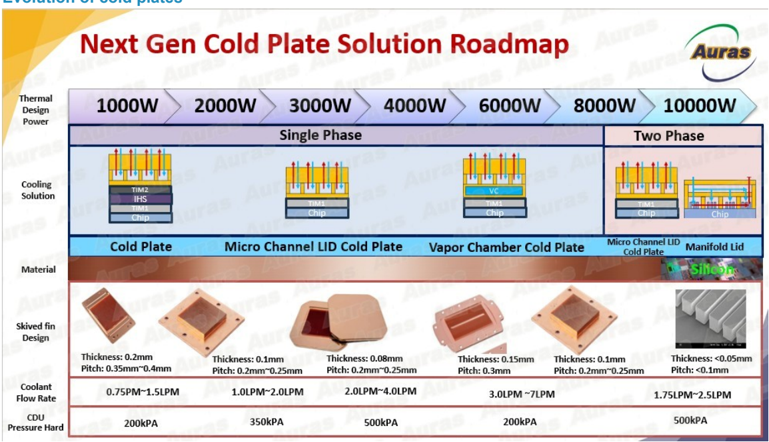

Evolution of cold plates

Primary water inlet pipe

3/4 inch Dunlop EPDM

Thermal

Design

Power

1000W

2000W

1 vs 38 flow distributor

38*38mm 316 SUS

G1/4 Connector

Quick Disconnector

Cooling

Solution

Coolan

PG25

IHS

Microloops & Intel Advanced Thermal

Technology Joint Laboratory

Product Advantages

Chip

Product Advantages

- The only cooling solution certified by global tier 1 clients

Cold Plate

Material

Skived fin

Design

Coolant

Flow Rate

CDU

Pressure Hard

ВИІДА

Coolant distribution unit

4U 80KW L2L CDU|

Redundancy Design

3000W

4000W

Single Phase

B. E

Cold plate quick connector

Cold plate with QD

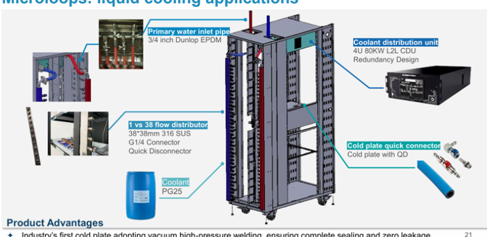

cooling. As the deployment ratio of NICs to ASICs increases to 4:1 - 8:1 within the next-gen architecture, Microloops stands to benefit from volume expansion and technical upgrades. Also, in GPU servers, the CSP client deploys 4-8 NICs per GPU, further increasing demand for Microloops, as it is the leading thermal solutions provider for NICs. Given that the ASP of liquid cooling solutions is estimated to be >3x that of air cooling, the volume ramp of liquid cooling shipments starting in 2H26 is expected to meaningfully transform Microloops' revenue mix and elevate total output value.

Microloops: liquid cooling applications

Source: Company

Several growth drivers present near-term share price catalysts

Thickness: 0.15mm

Evolution of cold plates

Microloops: immersion cooling applications

Source: Company

Source: Auras, Daiwa

Additional upside from several growth drivers

Except for the abovementioned revenue growth expectations and drivers, there are a few additional growth engines that might propel the next wave of revenue growth, including: (1) CSP self-designed CPU. The major CSP client is now self-developing its in-house CPU for AI servers, which is even expected to receive orders from other CSPs. Microloops is expected to be the main supplier of thermal modules for this CPU. (2) Next-gen GPU server. Microloops now certifies its cold plate products (at the request of an existing ASIC client) for the next-gen GPU server's recommended vendor list (RVL). This could be another revenue driver, according to management. (3) New ASIC customer(s). There is a high chance that Microloops will onboard a new ASIC customer in 2027, and the company is looking for a third one, aiming to onboard it in 2027 or 2028. (4) Probe card thermal modules. Probe card vendors are now discussing with Microloops to explore the possibility to cooperate on probe card thermal modules. Should this happen, it will be a recurring income stream, in our view, given the probe cards' consumable nature.

6000W

Taiwan Microloops (6831 TT): 18 June 2026

8000W

10000W

Two Phase

Daiwa

Microloops has higher operating efficiency than its global competitors

Taiwan Microloops (6831 TT): 18 June 2026

Competitive advantages

High entry barriers to the segment

Microloops maintains its strong competitive position and moat through solid execution, technical barriers, and higher efficiency. Technically, Microloops has invested in liquid cooling research and development for over 6 years, successfully engineering cooling systems and cold plates. This expertise is complemented by a collaboration with Intel to co-develop immersion cooling technologies and establish joint thermal laboratories. Given the highly customised nature of ASIC hardware, its qualified AVL supplier status creates a barrier to entry, making it highly difficult for competitors to bypass.

The company's competitive moat is further strengthened by its engineering proficiency, procurement efficiencies, rigorous quality control, and strong supply chain relationships. Microloops' Huizhou facility operates at a 70% automation rate, ensuring the quality control, product consistency, and yield stability required by global CSPs. To support the multi-million-unit ASIC ramp and mitigate ongoing geopolitical risks, Microloops is actively expanding its manufacturing footprint with new facilities in Vietnam.

Focus on core thermal manufacturing technologies

Microloops adopts a manufacturing strategy characterised by the in-house production of core thermal components, combined with some external sourcing of non-core electronic and dynamic parts. Positioned as a thermal module provider rather than a component supplier, the company maintains control over key manufacturing steps for its air-cooling solutions. We believe in-house capabilities encompass the fabrication of VCs, heat pipes, and welding assembly, allowing Microloops to deliver integrated thermal modules for AI servers and VGAs. For its liquid cooling systems, Microloops similarly focuses its R&D and production resources on the core heat-exchange interface, making cold plates the primary in-house manufactured product within this segment. This focus on core design and precision machining, such as proprietary etching and micro-channel technologies for VCs and cold plates, is supported by automated operations and an agile outsourcing framework, per management. To optimise capacity allocation, when the capacity is fully occupied, Microloops uses an outsourcing model, matching the operational strategies of peers. This suggests that labour shortage remains a potential bottleneck of the thermal solution industry, in our view. Overall, Microloops drives capital efficiency by leveraging its internal hardware manufacturing strengths while relying on external procurement for motor, electronic control, and fan sub-assemblies.

Microloops faces different rivals across its main product line: in the AI server thermal module and consumer (notebooks, VGAs) segments, key competitors include AVC (3017 TT, TWD2,400, Buy [1]), Auras (3324 TT, TWD1,070, Buy [1]) and Cooler Master (not listed); in the fan and CDU area, where Microloops does not focus, the main competitors are Sunonwealth (2421 TT, TWD145, Buy [1]) and Delta (2308 TT, TWD2,150, Buy [1]; covered by Sheng Cheng). Even under these headwinds, Microloops maintains a very strong competitive moat built on several key advantages. We attribute this to the fact that Microloops has been in the industry for more than 20 years, enabling it to develop an expertise that is hard for competitors to replicate.

Daiwa

Microloops: peer comparison

Daiwa

| Company | Ticker | Market Cap (USDm) | Market | Main thermal product | Solution Types 2025 Product mix | Solution Types 2025 Product mix | 2025 Segment breakdown | 2025 Market breakdown |

|---|---|---|---|---|---|---|---|---|

| Microloops | 6831 TT | 1,652 | Taiwan | Thermal module (heat pipe, VC, 2.5DVC, 3DVC) | Air, liquid | Thermal module (100%) | AI server (60%), consumer (40%) | Taiwan (65%), China (33%), others (2%) |

| AVC | 3017 TT | 29,828 | Taiwan | Thermal module (heat pipe, VC, 3DVC), chassis, fans, cold plate, CDU | Air, liquid | Thermal & chassis (75%), system integration (16%), Fositek (9%) | 3C (14%), server (52%), communication (7%), PC/AIO (16%), Fositek (9%), others (2%) | Asia (72%), America (19%), Europe (2%) |

| Auras | 3324 TT | 3,153 | Taiwan | Thermal module (heat pipe, VC, 3DVC), cold plate, CDU | Air, liquid | Cooling module (100%) | PC (27%), VGA (13%), server (57%), others (2%) | China (27%), Taiwan (33%), U.S. (21%), Ireland (8%), Thailand (1%), others (11%) |

| Delta | 2308 TT | 176,816 | Taiwan | Fan, CDU, side car | Air, liquid | Power electronics (51%), infrastructure (30%), mobility (7%), automation (8%), others (4%) | Power electronics (51%), infrastructure (30%), mobility (7%), automation (8%), others (4%) | China (15%), U.S. (36%), Taiwan (12%), Thailand (1%), others (36%) |

| Sunonwealth | 2421 TT | 1,317 | Taiwan | Fan | Air | DC cooling (75%), AC cooling (3%), material and components (22%) | IT&OE (16%), telecom & server (58%), industrial medical equipment (9%), home application (3%), distribution (5%), automobile (9%), LED lighting (1%) | Asia (75%), Europe (19%), America (6%) |

| Jentech | 3653 TT | 18,420 | Taiwan | Heat spreader | Air, liquid | Thermal heat spreader (73%), lead frame (9%), electronic components 7%), communication connectors (1%), others (10%) | Server, auto, NB, DT, gaming | Taiwan (95%), China (5%) |

| Kaori | 8996 TT | 4,701 | Taiwan | Tank, CDU | Liquid, immersion | Plate heat exchanger (26%), thermal products (74%) | Server, data centre, industrial | Asia (21%), Europe (12%), America (68%) |

| Taisol | 3338 TT | 209 | Taiwan | Heat sink, heat pipe, VC, cold plate | Air, liquid | Radiator products (85%), connector products (15%) | NB (41%), server (22%), DT&AIO (10%), auto (12%), communication (5%), others (10%) | Asia (97%), Europe (1%), America (2%) |

| NCCI | 6230 TT | 362 | Taiwan | Heat sink, heat pipe, VC | Air, liquid | Heat dissipation module (76%), heat sink (17%), others (7%) | NB & DT (41%), server & network (29%), game console (25%), smart phone (1%), others (4%) | China (57%), Singapore (12%), Taiwan (9%), others (22%) |

| Yen Sun | 6275 TT | 120 | Taiwan | Fans | Air | Cooling fan and module (84%), air series (9%), water series (5%), others (2%) | Auto (48%), HPC (28%), consumer technology (16%), industrial & others (8%) | Taiwan (43%), Germany (35%), China (15%), U.S. (3%), Korea (1%), others (2%) |

| Forcecon | 3483 TT | 294 | Taiwan | Fans, thermal module, CDU, Cold Plate | Air, liquid, immersion | Thermal module and fan (100%) | NB/gaming (90%), telecom (5%), auto (5%) | Taiwan (59%), China (41%) |

Source: Companies, Bloomberg, Daiwa

Note: market cap as of 18 June 2026

Reliable execution of manufacturing, procurement efficiency, quality control, and positive supply chain feedback are key to winning market share

Taiwan Microloops (6831 TT): 18 June 2026

Core hardware competency drives market share gains

Engineering proficiency ensures reliable execution of manufacturing

From an engineering standpoint, the company expands its market share through forwardlooking R&D capabilities, manufacturing execution that aligns with client expectations, and robust debugging proficiency. These technical strengths ensure that hardware designs can transition smoothly into mass production. By keeping key components in-house, the engineering team maintains the agility required to solve bottlenecks.

Procurement efficiencies deliver commercial advantages

On the procurement front, Microloops remains competitive by offering attractive pricing and reliable lead times. This advantage is supported by the cost efficiencies and supply visibility gained from its vertically integrated in-house production of key thermal components. By minimising reliance on external manufacturing for core hardware, the company optimises its cost structure and ensures predictable delivery schedules for clients. This is especially crucial for ASIC and GPU AI servers, as their iteration cycles have shortened dramatically.

Rigorous quality control mitigates operational risks

The company's quality control provides rigorous validation and consistent product quality, which are crucial for high-tier CSPs. This is backed by a strong capacity for emergency response to mitigate unexpected operational disruptions. The tightly controlled internal manufacturing environment allows the quality team to implement rapid corrections and maintain high yield stability.

Guidance calls for capex to increase to more than TWD500m in 2026E and TWD800-1,000m in 2027E, from c.TWD325m in 2025

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

Strategic supply chain relationships accelerate market traction

Beyond internal execution, Microloops drives market share gains by leveraging strong supply chain feedback and deeply anchored industry relationships. The company's ecosystem integration has earned high satisfaction from major customers, who are displaying increased preference for Microloops. This commercial traction is significantly reinforced by the company's close relationships with key industry players.

Expanding capacity meets fast-growing demand

Microloops is taking an aggressive pace to expand its capacity in China and Vietnam. This is to ensure it can always have sufficient capacity to meet the ever-growing client requests. In May, the company purchased equipment worth tens of millions of TWD, which is expected to expand its VC capacity by 40%, per management. The company has also secured a new plant (to rent) in Vietnam as the next step after the current plant becomes completely occupied with production lines. Management guidance calls for capex of more than TWD500m in 2026 and TWD800-1,000m in 2027, up from c.TWD325m in 2025.

We forecast Microloops' revenue to record a CAGR of 100% over 2026-28E

We forecast an upward operating-margin trend over 2026-28E

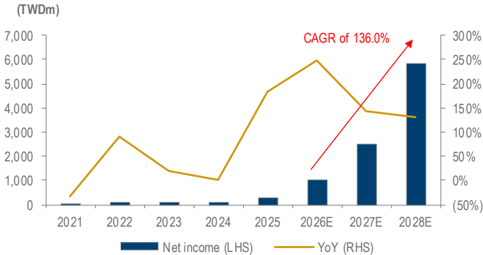

We forecast Microloops' net profit to record a CAGR of 136.0% over 2026-28E

Financial analysis

We forecast the company's net profit to rise at a CAGR of 136.0% over 2026-28E, driven by a revenue CAGR of 100.0% due to Microloops' capacity expansion plan (an increase in VC capacity of c.40% in May 2026) and 6.8pp expansion in operating margin over 202628E based on higher operating leverage, economies of scale and a better product mix.

Strong order visibility, with growing revenue contribution from ASIC AI server thermal modules over 2026-28E

We forecast Microloops' revenue to increase at a CAGR of 100% over 2026-28E, driven by capacity expansion and a growing revenue contribution from ASIC AI servers (to reach 80% in 2026E vs. 60% in 2025).

Microloops: revenue growth trend

Source: Company, Daiwa forecasts

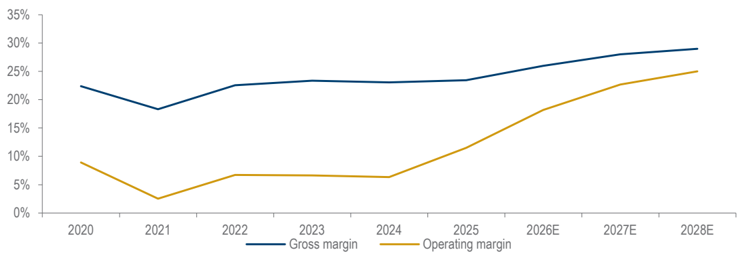

Gross- and operating-margin expansion trend

Over 2026-28E, we forecast Microloops' gross and operating margins to expand on rising revenue scale and an increasing revenue contribution from ASIC AI server thermal modules . We note that the gross margin from ASIC AI server thermal modules is higher than that from consumer products, such as notebooks and VGAs. Thus, we estimate the company's gross margin to reach 29.0% in 2028E from 23.4% in 2025 and its operating margin to reach 25.0% in 2028E from 11.5% in 2025.

Microloops: gross- and operating-margin trend

Source: Company, Daiwa forecasts

Net margin likely to rise over 2026-28E

We forecast Microloops' net income to rise to TWD2,531m in 2027E and TWD5,833m in 2028E (from TWD1,047m in 2026E). We expect its net margin to come in at 16.3% in 2027E and 18.8% in 2028E (vs. 13.5% in 2026E) and for its net profit to post a CAGR of 136.0% over 2026-28E.

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

Microloops: quarterly P&L

Microloops: net profit trend

Source: Company, Daiwa forecasts

Quarterly P&L

| (TWDm) | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E |

|---|---|---|---|---|---|---|---|---|

| Revenue | 854 | 993 | 2,900 | 3,029 | 3,000 | 3,300 | 4,500 | 4,754 |

| Gross profit | 156 | 228 | 783 | 855 | 780 | 875 | 1,215 | 1,330 |

| Operating profit | 56 | 116 | 609 | 633 | 630 | 710 | 1,013 | 1,023 |

| Profit before tax | 56 | 97 | 610 | 634 | 630 | 710 | 1,013 | 1,023 |

| Net profit | 45 | 73 | 457 | 473 | 473 | 532 | 759 | 767 |

| Basic EPS (TWD) | 0.66 | 1.08 | 6.77 | 7.00 | 7.00 | 7.88 | 11.25 | 11.37 |

| Margin | ||||||||

| Gross margin | 18.2% | 23.0% | 27.0% | 28.2% | 26.0% | 26.5% | 27.0% | 28.0% |

| Operating margin | 6.5% | 11.7% | 21.0% | 20.9% | 21.0% | 21.5% | 22.5% | 21.5% |

| Pre-tax margin | 6.5% | 9.8% | 21.0% | 20.9% | 21.0% | 21.5% | 22.5% | 21.5% |

| Net margin | 5.2% | 7.3% | 15.8% | 15.6% | 15.8% | 16.1% | 16.9% | 16.1% |

| YoY | ||||||||

| Revenue | 50.7% | -4.6% | 151.2% | 222.0% | 251.1% | 232.2% | 55.2% | 56.9% |

| Gross profit | 30.7% | 9.1% | 144.2% | 289.8% | 401.6% | 282.7% | 55.2% | 55.6% |

| Operating profit | 150.6% | 5.3% | 186.5% | 682.4% | 1025.9% | 510.4% | 66.3% | 61.6% |

| Profit before tax | 232.5% | 136.5% | 198.8% | 631.6% | 1030.3% | 632.2% | 66.1% | 61.4% |

| Net profit | 232.5% | 186.3% | 206.3% | 319.9% | 959.7% | 632.2% | 66.1% | 62.4% |

| QoQ | ||||||||

| Revenue | -9.2% | 16.3% | 191.9% | 4.5% | -1.0% | 10.0% | 36.4% | 5.6% |

| Gross profit | -29.1% | 46.9% | 242.7% | 9.2% | -8.8% | 12.1% | 38.9% | 9.5% |

| Operating profit | -30.9% | 107.7% | 424.0% | 4.0% | -0.5% | 12.6% | 42.7% | 1.1% |

| Profit before tax | -35.7% | 73.9% | 529.2% | 4.0% | -0.6% | 12.6% | 42.7% | 1.1% |

| Net profit | -60.4% | 63.0% | 529.2% | 3.4% | 0.0% | 12.6% | 42.7% | 1.1% |

Source: Company, Daiwa forecasts

We expect stronger cash balances and CFFO over 2026-28E due to better profitability

Strong ROE outlook over 2026-28E

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

Intact demand to support revenue growth in upcoming years; ROE expansion underway

We forecast Microloops' total cash and equivalents to reach TWD958m (13.1% of its total assets) in 2026E and increase to TWD2,534m in 2028E (10.7% of total assets) with net debt likely to come in at TWD42m in 2026E, vs. TWD3,466m in 2028E.

After factoring in our 2027E capex assumptions of TWD900m and TWD1,200m for 2028E (supporting Vietnam capacity expansion), we expect Microloops' free cash flow (FCF) burn to improve to TWD69m in 2028E, from TWD457m in 2026E. We believe the capacity expansion will cost some cash at the beginning, but the company will start to benefit from the investment, with FCF turning positive from 2029E.

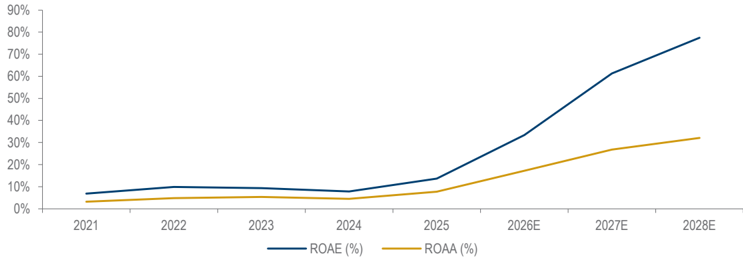

We expect Microloops' ROAE to improve to a record-high of 77.4% in 2028E from 13.7% in 2025 (following steady annual increases to 33.0% in 2026E and 56.9% in 2027E), which we attribute to margin expansion from the revenue size increase and gross margin expansion led by spec upgrades.

Microloops: ROAE and ROAA trend

Source: Company, Daiwa forecasts

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

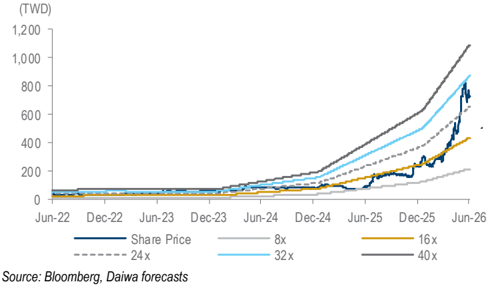

12-month target price of TWD1,150, based on a target PER of 40x

Taiwan Microloops (6831 TT): 18 June 2026

Valuation and risks

Undemanding valuation on its global leading position and optimistic industry outlook

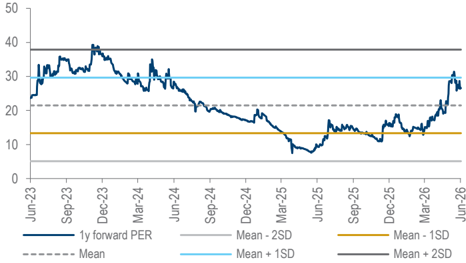

We initiate coverage of Microloops with a Buy (1) rating and 12-month TP of TWD1,150, based on a target PER of 40x applied to our one-year-forward EPS forecast (ie, 3Q262Q27E). This target multiple is higher than the average of its past-3-year 1-year-forward PER of 21.5x and the average of its past-5-year 1-year-forward PER of 22.7x, which we view as undemanding as we forecast a 136.0% EPS CAGR over 2026-28E, and implying a 0.29x PEG. This is supported by business expansion in the next 2-3 years. We expect a potential rerating for the stock given Microloops' global leading position in thermal modules, especially for ASIC AI servers.

The stock is trading currently at a 27.9x 1-year-forward PER vs. its earnings CAGR of 136.0% over 2026-28E, translating into a 0.21x PEG ratio.

Microloops: past 3-year-forward PER (average: 21.5x)

Source: Bloomberg, Daiwa estimates

Stronger earnings growth outlook and more room to grow vs. global peers

The stronger earnings visibility deserves a valuation premium, in our view

Microloops: past 5-year-forward PER (average: 22.7x)

Source: Bloomberg, Daiwa estimates

We compare Microloops with other leading thermal solution companies like AVC (3017 TT, TWD2,400, Buy [1]), Auras (3324 TT, TWD1,070, Buy [1]) and Cooler Master (not listed). AVC and Auras are trading at a PER of 22.6x and 16.4x on their 1-year-forward EPS, implying 1-year-forward PEG ratios of 0.76x and 0.53x, respectively, on our estimates.

Microloops' global thermal solution peers are trading at 43.1x for 2026E and 25.0x for 2027E. We forecast Microloops to deliver an EPS CAGR of 136.0% over 2026-28E vs. 50.2% CAGR for the segment over the same period.

We believe our target 2026E PER of 40x (equivalent to a 0.29x PEG using 2026-28E EPS CAGR) is undemanding as: 1) Microloops is ramping up to meet growing demand from CSPs and is in a margin-expansion cycle; and 2) its leading global position warrants a valuation premium, as seen among global peers .

Daiwa

Microloops: 1-year-forward PER bands

Source: Bloomberg, Daiwa forecasts

AVC: 1-year-forward PER bands

Source: Bloomberg, Daiwa forecasts

Auras: 1-year-forward PER bands

Source: Bloomberg, Daiwa forecasts

Microloops: peers valuation comparison

| Bloomberg | Price (lc) | Daiwa | Market cap | D. turnover | PER (x) | PER (x) | PER (x) | EPS CAGR | ROE (%) | ROE (%) | ROE (%) | PBR (x) | PBR (x) | PBR (x) | EV/EBITDA (x) | EV/EBITDA (x) | EV/EBITDA (x) | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Companies | code | 18/06/25 | rating | (USDm) | (USDm) | 2026E | 2027E | 2028E | 2026-28E | 2026E | 2027E | 2028E | 2026E | 2027E | 2028E | 2026E | 2027E | 2028E |

| Microloops* | 6831 TT | 773.0 | Buy (1) | 1,652 | 27.4 | 49.8 | 20.6 | 8.9 | 136.0 | 33.0 | 56.9 | 77.4 | 14.8 | 9.7 | 5.4 | 31.8 | 14.4 | 6.7 |

| AVC* | 3017 TT | 2,400.0 | Buy (1) | 29,828 | 409.5 | 25.8 | 19.9 | 15.3 | 29.6 | 59.2 | 49.6 | 46.2 | 11.6 | 8.3 | 6.0 | 0.9 | 1.6 | 2.1 |

| Auras* | 3324 TT | 1,070.0 | Buy (1) | 3,153 | 155.8 | 19.2 | 14.1 | 11.2 | 30.9 | 41.1 | 43.6 | 43.5 | 6.7 | 5.4 | 4.3 | 1.1 | 2.4 | 3.3 |

| Delta* | 2308 TT | 2,150.0 | Buy (1) | 176,816 | 785.3 | 54.9 | 35.2 | 22.2 | 57.1 | 32.1 | 36.9 | 42.4 | 15.3 | 11.3 | 8.1 | 0.3 | 0.5 | 0.8 |

| Sunonwealth* | 2421 TT | 145.0 | Buy (1) | 1,317 | 30.4 | 14.5 | 12.1 | 10.4 | 18.1 | 28.9 | 30.5 | 31.3 | 4.0 | 3.5 | 3.1 | 3.8 | 4.8 | 5.7 |

| Jentech* | 3653 TT | 3,965.0 | Buy (1) | 18,420 | 195.5 | 58.4 | 29.7 | 19.9 | 71.3 | 37.4 | 52.6 | 55.4 | 19.1 | 13.2 | 9.4 | 0.6 | 1.0 | 2.0 |

| Kaori | 8996 TT | 1,590.0 | Not rated | 4,701 | 117.8 | 85.7 | 39.0 | 22.8 | 94.0 | 41.7 | 57.7 | 63.2 | 25.9 | 17.9 | 11.8 | 0.7 | 1.2 | 1.9 |

| Taisol | 3338 TT | 75.2 | Not rated | 209 | 7.4 | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| NCCI | 6230 TT | 132.5 | Not rated | 362 | 0.8 | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Yen Sun | 6275 TT | 47.3 | Not rated | 120 | 1.6 | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Forcecon | 3483 TT | 93.8 | Not rated | 294 | 4.2 | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Peer average | 43.1 | 25.0 | 17.0 | 50.2 | 40.1 | 45.2 | 47.0 | 13.8 | 9.9 | 7.1 | 1.2 | 1.9 | 2.6 |

Source: Bloomberg; *Daiwa forecasts

Taiwan Microloops (6831 TT): 18 June 2026

Microloops: earnings revision trend

Source: Bloomberg, Daiwa

AVC: earnings revision trend

Source: Bloomberg, Daiwa

Auras: earnings revision trend

Source: Bloomberg, Daiwa

Daiwa

Our 12-month TP of TWD1,150 is also supported by our DCF valuation

Microloops: DCF calculation

Daiwa

We also reference a DCF methodology (see charts below), which indicates a DCF-derived fair value estimate of TWD1,213/share, which supports our 12-month TP of TWD1,150.

In our DCF calculation, we apply a WACC of 17.3% to FCF over 2026-34E and a terminal growth rate of 8.0% thereafter. We expect the company to continue to record stable FCF over 2026-35E.

| Target gearing (debt/capital) | 5.0% |

|---|---|

| Market risk premium (%) | 20.0% |

| Risk-free rate (%) | 0.0% |

| Cost of debt (%) | 5.0% |

| Cost of equity (%) | 18.0% |

| WACC (%) | 17.3% |

| Terminal growth rate | 8.0% |

| Terminal WACC | 17.3% |

| Enterprise value (TWDm) | 81,127 |

| Less: net debt (as of end-2025) (TWDm) | -723 |

| Equity value (TWDm) | 81,850 |

| No. shares (m) | 68 |

| Per share equity value (TWD) | TWD1,213 |

Source: Company, Daiwa estimates

Key downside risks: weaker-than-expected end-market demand, lower penetration of new spec and larger-thanexpected increases in labour costs

Microloops: DCF sensitivity

| WACC (%) | WACC (%) | WACC (%) | WACC (%) | WACC (%) | ||

|---|---|---|---|---|---|---|

| 16.9 | 17.1 | 17.3 | 17.5 | 17.7 | ||

| Terminal growth rate (%) | 9.0 | 1,417 | 1,372 | 1,330 | 1,290 | 1,252 |

| Terminal growth rate (%) | 8.5 | 1,346 | 1,306 | 1,268 | 1,232 | 1,197 |

| Terminal growth rate (%) | 8.0 | 1,284 | 1,247 | 1,213 | 1,180 | 1,148 |

| Terminal growth rate (%) | 7.5 | 1,228 | 1,195 | 1,163 | 1,132 | 1,104 |

| Terminal growth rate (%) | 7.0 | 1,178 | 1,147 | 1,118 | 1,090 | 1,063 |

Source: Daiwa estimates

Microloops: free cash flow forecasts

| (TWDm) | 2026E | 2027E | 2028E | 2029E | … | 2035E |

|---|---|---|---|---|---|---|

| EBITDA | 1,643 | 3,740 | 8,311 | 10,388 | … | 39,628 |

| Less: taxation (EBIT*tax rate) | -349 | -844 | -1,944 | -2,430 | … | -9,271 |

| Plus: decrease in working capital | -1,231 | -2,995 | -5,236 | -5,236 | … | -5,236 |

| Less: capital expenditure | -520 | -900 | -1,200 | -1,200 | … | -1,200 |

| Free cash flow (TWDm) | -457 | -999 | -69 | 1,522 | … | 23,921 |

| Discount rate | 17.3% | 17.3% | 17.3% | 17.3% | … | 17.3% |

| Discount factor | 0.91 | 0.78 | 0.66 | 0.57 | … | 0.22 |

| NPV of free cash flow | -418 | -779 | -46 | 862 | … | 5,203 |

Source: Daiwa estimates and forecasts

Risks to our call

Primary risk: weaker-than-expected end-market demand

In our view, the biggest downside risk to our call for Microloops is weaker-than-expected end-market demand, which could be driven by: 1) a longer-than-expected macro-driven slowdown that would drag down global demand for AI services and therefore negatively affect the capex from CSPs/datacentre operators, and 2) lower-than-expected server shipments, likely due to overbooking of AI servers, delay of new server ASIC AI platforms and replacement between regular and AI servers caused by limited budgets, which would impact revenue from the server segment.

Secondary risk: lower penetration of new spec

As we expect spec upgrades (from air cooling modules to liquid cooling modules) to be the key revenue and gross-profit drivers for Microloops, any slower-than-expected penetration, especially in the next-generation ASIC platforms, could drag down the company's ASP and gross-margin performance. We think this could come in the form of a slow pace of chip upgrade or cost concerns in the server segment. This is a secondary downside risk.

Secondary risk: labour issues or larger-than-expected increases in labour costs

Our earnings forecasts would likely be at risk if basic labour costs at the company's production sites increase more than our expectations and labour disputes materialise. Despite a >70% adoption rate across Microloops' production lines, the lack of labour could still cause the utilisation rate to drop and thus negatively affect revenue growth and margin expansion. This is a secondary downside risk to our call.

Taiwan Microloops (6831 TT): 18 June 2026

Taiwan Microloops (6831 TT): 18 June 2026

Secondary risk: unfavourable currency movement

For FX risk, the company employs a natural hedging strategy, enhances the operational capabilities of its finance team, and negotiates floating price contracts tied to international rates to share risk with customers. Any dramatic appreciation in USD/TWD would lead to worse-than-expected revenue growth and profitability.

Secondary risk: failure to optimise manufacturing and operational processes

To counter operational challenges, Microloops is committed to improving automation to boost efficiency and capacity, while simultaneously seeking alternative materials and technology upgrades to lower costs and strengthening its manufacturing systems to meet market demand. Lower-than-expected operating efficiency or slower-than-expected automation would jeopardise the profitability of the company.

Daiwa

With business started from consumer segments, Microloops entered the ASIC AI server space in 2024

Taiwan Microloops (6831 TT): 18 June 2026

Appendix

Company background

History

Taiwan Microloops Corp. (Microloops) was established in November 2002 as a technical spin-off from the specialised teams of Taiwan's Industrial Technology Research Institute (ITRI). Headquartered in the Zhonghe District of New Taipei City, the company initially established its business as a manufacturer focused on the development and the production of thermal module, including self-made components such as heat pipes and vapour chambers (VCs). A crucial moment in the company's history occurred in 2006 when it successfully developed and mass-produced VCs, making Microloops the first VC manufacturer in Taiwan. After that, the company's operations were mainly focused on providing cooling solutions for consumer applications as a critical supplier of thermal modules for notebooks, desktop computers and high-end graphics cards.

Microloops has transformed over the years, shifting its core business from traditional consumer electronics (notebooks, VGAs) to the high-growth AI ASIC server sector. In 2024, it successfully secured itself as a verified partner for a major global CSP, particularly in the supply chain for its ASIC accelerators, NIC cards and top-of-rack (TOR) switches. Its current product mix is heavily weighted on high-performance air-cooling modules, including 2.5D and 3DVCs designed to support heat dissipation requirements of high-wattage AI chips. Microloops is also expanding its liquid-cooling portfolio, producing a full suite of thermal modules, with self-made cold plates. To support this growth, Microloops is diversifying its geographic manufacturing footprint by expanding capacity in Vietnam to complement its facilities in Huizhou, China. Microloops has automated over 70% of its capacity, which was critical to the company securing its position as a late-entering supplier for the CSP client. This high level of automation also mitigates reliance on labour recruitment, accelerating capacity expansion to meet the surging demand.

Beyond the current ASIC server demand, Microloops plans to supply thermal modules for the same CSP client's next-generation proprietary CPU. Management is also negotiating with other CSPs to provide thermal solutions for their ASIC servers. Furthermore, Microloops is fully prepared to expand into GPU thermal solutions should clients request it. In the long term, the next-generation potential for Microloops lies in its immersion-cooling research, where the company is collaborating with Intel to develop solutions that immerse electronic components directly into non-conductive fluids, offering better energy efficiency and heat dissipation for future AI servers.

Next frontier: immersion cooling

Beyond air cooling and legacy liquid cooling, Microloops has been co-developing immersion cooling technology with Intel for years, to tackle with the ever-growing thermal design power (TDP) levels that traditional air cooling cannot handle. Standard air cooling only works efficiently up to heat densities of about 1.6 W/cm². It fails when managing chips that draw over 700-1,000W or server racks that exceed 30-100kW. This problem is forcing the industry to switch to liquid cooling, with immersion cooling becoming the next option for higher-density setups. By submerging servers completely in non-conductive fluids, data centres can take advantage of the high heat capacity of liquids, which can hold up to 3,500 times more heat than air. This method eliminates hot spots, lowers fan noise, and cuts down total data centre power consumption.

Immersion cooling systems are divided into single-phase and two-phase types, based on how the fluid handles heat. In single-phase systems, the fluid has a high boiling point and remains liquid throughout the process. The fluid absorbs heat from the components, and pumps move it to an external heat exchanger to cool down before it flows back into the server tank. In contrast, two-phase systems use a fluid with a low boiling point, such as fluorinated ketones or hydrofluoroethers. When the components heat up, the fluid boils and

Daiwa

Immersion cooling is the next trend when the TDP goes beyond the limit of legacy liquid cooling solutions

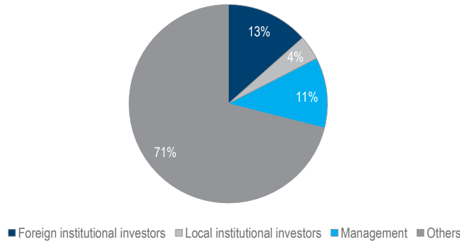

Microloops: QFII holdings

Source: TEJ

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

turns into vapour. This vapour rises to the top of the sealed tank, hits cold condenser coils, turns back into liquid, and drips back into the pool. Two-phase systems transfer heat more efficiently, but single-phase systems are more common commercially because they are simpler to build, require less maintenance, and do not lose fluid through evaporation.

However, full immersion cooling still faces material, cost, and operational hurdles. A major engineering issue Microloops and its partners (or competitors) face is how the fluid interacts with server parts over time. For example, the chemicals can draw out plasticisers from PVC cable coatings, making the wires brittle. The fluid can also cause chemical reactions that corrode solder joints, creating tiny metal whiskers (made of tin and aluminium) that cause short circuits and equipment failures. High upfront costs for specialised fluids, especially for two-phase setups, also limit. Maintenance is another issue, as technicians must pull heavy servers out of fluid baths, which causes fluid to drip out and requires tight seals to prevent environmental leaks. Because of these challenges, Microloops adopts direct-to-chip (D2C) cold plates as their liquid cooling solution, while immersion cooling remains a longer-term solution as materials and standards improve.

Microloops: management team (according to November 2025, Public Offering Prospectus)

| Management | Position | Background and experience |

|---|---|---|

| Yuan-Shan Chao | Chairperson | Elected as chairperson since 2018. Before joining Microloops, Mr. Chao has been serving in CDIB Capital Group, Walshin Lihwa Corp, Winbond Electronics and several tech companies and venture capitals. Graduated from City University of Seattle with a bachelor's degree majoring in accounting. |

| Yuan-Chi Chao | Director | Elected as director since 2021. Before joining Microloops, Mr. Chao served for Taipei Fubon Bank as independent director and First FHC as chairperson and president. Graduated from New York University with a master's degree of Finance. |

| Chun-Hung Lin | President/ Director | Former R&D Manager and Project Manager in Cooler Master Group, with decades of experience in developing thermal module. Mr. Lin has a Ph.D. degree of mechanical engineering in National Taiwan University. |

| Chien-Heng Chen | Vice President | As former Assistant Vice President of Sales in Cooler Master Group, Mr. Chen has decades of experience in thermal module related business. |

Source: Company

Microloops: major shareholders (as of April 2026)

| Holder | Share (%) |

|---|---|

| Heng Lang Co., Ltd. | 10.85% |

| Ting-Wu Hu | 7.71% |

| Yuan Ching Investment Co., Ltd. | 5.47% |

| Hermax Holdings Limited | 4.44% |

| Lien-Chun Liu | 3.15% |

| Yuan-Wen Chao | 2.47% |

| Deyin Investment Co., Ltd. | 2.02% |

| Chuen-Hua Chen | 1.37% |

| Yuan-Shan Chao | 1.37% |

Source: TEJ

Microloops: shareholding structure (as of June 2026)

Source: TEJ, Bloomberg, Company

ESG analysis

ESG risks

| Risks | Management | Analyst comments | |

|---|---|---|---|

| Executive/board quality | 1 | The positions of Chairperson and President (CEO equivalent) are held by Mr. Yuan-Shan Chao and Mr. Chun-Hung Lin, respectively. We note that Chairperson Chao has extensive senior management experience in finance, having previously served as CFO of Walsin Lihwa Corporation and Vice President of Finance at Winbond Electronics, while President Lin holds a PhD in Mechanical Engineering and brings significant R&D and project management experience from the Cooler Master Group. This separation of roles -combined with a Board consisting of 7 directors including 3 independent directors who possess diverse professional qualifications across finance, accounting, law, business management, and industrial knowledge -is a positive sign from a corporate governance perspective. | |

| G | Capital management | 1 | Over 2023-2025, Microloop recorded dividend payout ratios of 38%, 69% and 61%. Management aims to further increase the ratio to 70% over the mid-to-long-term to balance shareholder returns while meeting reinvestment needs. This approach reflects a prudent capital management policy and consistent financial discipline. |

| Related party & transaction | 1 | The company engages in transactions with subsidiaries (such as those in Samoa, Huizhou, and Vietnam) primarily for normal operational purposes, such as the procurement of equipment by Microloops Huizhou. To ensure risk control and firewall mechanisms, all interactions are governed by established internal controls, including the "Regulations Governing the Financial and Business Matters Between Related Parties" and the "Regulations Governing the Supervision and Management of Subsidiaries", ensuring that no irregular or non-transparent transactions were identified. | |

| E | Supply chain management | 1 | Microloops has a structured procurement process utilising its "Procurement Management Regulations" to select suppliers, giving preference to those with environment-related licenses who emphasise environmental protection and social responsibility. The company maintains stable, mutual-trust relationships with major raw material suppliers (including Sankou Precision and Thermal Science Technology) and promotes ethical management policies by requiring cooperating partners to sign an "Integrity Commitment Letter". This reflects strong supply chain transparency, environmental compliance regarding RoHS and lead-free regulations, and robust quality control measures. |

| S | Data security | 1 | The company has established a dedicated Information Security Department led by an Information Security Officer to oversee security management, officially obtaining the ISO 27001 Information Security Management System certificate in 2025/4. Guided by its "Computer Processing Operations Cycle" and "Information Security Management Regulations", the company conducts regular asset inventory and risk assessments while enforcing anti-virus mandates, server password updates, and strict employee access controls. Backup systems, redundancies, and regular disaster recovery drills are actively in place, allowing the company to ensure system availability and minimise operational damage during major incidents or equipment failures. |

Note: Management score represents a company's ability to manage/benefit from certain ESG topics. The scores range from 1 to 3, with 1 being the strongest.

Update Date: 18 Jun 2026

Source: Daiwa, Company

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

Daiwa's Asia Pacific Research Directory

| HONG KONG | HONG KONG | HONG KONG |

|---|---|---|

| Hiroyuki GOTO | (852) 2773 8870 | hiroyuki.goto@hk.daiwacm.com |

| Regional Head of Equity, Asia & Oceania; Regional Head of Asia Pacific Research | Regional Head of Equity, Asia & Oceania; Regional Head of Asia Pacific Research | Regional Head of Equity, Asia & Oceania; Regional Head of Asia Pacific Research |

| John HETHERINGTON | (852) 2773 8787 | john.hetherington@hk.daiwacm.com |

| Co-Head of Asia Pacific Research and Head of Research Publications | Co-Head of Asia Pacific Research and Head of Research Publications | Co-Head of Asia Pacific Research and Head of Research Publications |

| Li XIONG | (852) 2773 8878 | li.xiong@hk.daiwacm.com |

| Strategy (Hong Kong/China) | Strategy (Hong Kong/China) | Strategy (Hong Kong/China) |

| Yue TAN | (852) 2848 4947 | yue.tan@hk.daiwacm.com |

| Strategy (Greater China) and Macro Economics (China) | Strategy (Greater China) and Macro Economics (China) | Strategy (Greater China) and Macro Economics (China) |

| Kelvin LAU | (852) 2848 4467 | kelvin.lau@hk.daiwacm.com |

| Regional Head of Automobiles, Industrials and Transportation | Regional Head of Automobiles, Industrials and Transportation | Regional Head of Automobiles, Industrials and Transportation |

| Evelyn ZHANG | (852) 2848 4970 | evelyn.zhang@hk.daiwacm.com |

| Automobiles and Components (Hong Kong/China) | Automobiles and Components (Hong Kong/China) | Automobiles and Components (Hong Kong/China) |

| Frank YIP | (852) 2773 8842 | frank.yip@hk.daiwacm.com |

| Industrials and Transportation (Hong Kong/China) | Industrials and Transportation (Hong Kong/China) | Industrials and Transportation (Hong Kong/China) |

| Carol XIA | (852) 2532 4349 | carol.xia@hk.daiwacm.com |

| Head of China Consumer; Consumer (Hong Kong/China) | Head of China Consumer; Consumer (Hong Kong/China) | Head of China Consumer; Consumer (Hong Kong/China) |

| Steven NIE | (852) 2848 4464 | steven.nie@hk.daiwacm.com |

| Consumer (Hong Kong/China); Global Cryptocurrency | Consumer (Hong Kong/China); Global Cryptocurrency | Consumer (Hong Kong/China); Global Cryptocurrency |

| Siman CHEN | (852) 2532 4350 | siman.chen@hk.daiwacm.com |

| Consumer (Hong Kong/China) | Consumer (Hong Kong/China) | Consumer (Hong Kong/China) |

| Jing YANG | (852) 2532 4308 | jing.yang@hk.daiwacm.com |

| Head of China Healthcare | Head of China Healthcare | Head of China Healthcare |

| John CHOI | (852) 2773 8730 | john.choi@hk.daiwacm.com |

| Head of China Internet; Regional Head of Emerging Opportunities | Head of China Internet; Regional Head of Emerging Opportunities | Head of China Internet; Regional Head of Emerging Opportunities |

| Dennis IP | (852) 2848 4068 | dennis.ip@hk.daiwacm.com |

| Head of Asia ex-Japan Power, Utilities, Renewables & ESG (PURE) Research US Power Equipment (Gas, Nuclear, Solar, Wind, Grid, ESS & Battery Materials) | Head of Asia ex-Japan Power, Utilities, Renewables & ESG (PURE) Research US Power Equipment (Gas, Nuclear, Solar, Wind, Grid, ESS & Battery Materials) | Head of Asia ex-Japan Power, Utilities, Renewables & ESG (PURE) Research US Power Equipment (Gas, Nuclear, Solar, Wind, Grid, ESS & Battery Materials) |

| Derek ZHANG | (852) 2532 4341 | derek.zhang@hk.daiwacm.com |

| Power, Utilities, Renewables and ESS (PURE) - Gas, Wind and Grid (China), Utilities (Hong Kong) | Power, Utilities, Renewables and ESS (PURE) - Gas, Wind and Grid (China), Utilities (Hong Kong) | Power, Utilities, Renewables and ESS (PURE) - Gas, Wind and Grid (China), Utilities (Hong Kong) |

| Marco ZENG | (852) 2848 4430 | marco.zeng@hk.daiwacm.com |

| Power, Utilities, Renewables and ESS (PURE) - Power Equipment (US) | Power, Utilities, Renewables and ESS (PURE) - Power Equipment (US) | Power, Utilities, Renewables and ESS (PURE) - Power Equipment (US) |

| Tina YU | (852) 2532 4106 | tina.yu@hk.daiwacm.com |

| ESG (Asia ex-Japan) | ESG (Asia ex-Japan) | ESG (Asia ex-Japan) |

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa

| CHINA | CHINA | CHINA |

|---|---|---|

| Louis LUO | (86) 21 6841 3282 | louis.luo@daiwacm.cn |

| Automobiles and Components, Industrials (China) | Automobiles and Components, Industrials (China) | Automobiles and Components, Industrials (China) |

| Mavis MA | (86) 21 6841 3288 | mavis.ma@daiwacm.cn |

| Leo LU Power, Utilities, Renewables Infrastructure (China) | (86) 21 6841 3286 and ESS (PURE) | leo.lu@daiwacm.cn - Solar, ESS, Lithium, AIDC |

| Skye LIANG Power, Utilities, Renewables | (86) 21 6841 3207 and ESS (PURE) | skye.liang@daiwacm.cn Wind and Grid (China) |

| William WU Property (China/Hong | (86) 21 6841 3200 Kong) | william.wu@daiwacm.cn |

| Bintuo NI Tech Hardware and | (86) 21 6841 3228 Semiconductors (China) | bintuo.ni@daiwacm.cn |

| SOUTH KOREA | ||

|---|---|---|

| Yoonki BAE (82) 2 787 9168 yoonki.bae@kr.daiwacm.com Automobile Components, Healthcare | Yoonki BAE (82) 2 787 9168 yoonki.bae@kr.daiwacm.com Automobile Components, Healthcare | Yoonki BAE (82) 2 787 9168 yoonki.bae@kr.daiwacm.com Automobile Components, Healthcare |

| Mike OH | (82) 2 787 9179 | mike.oh@kr.daiwacm.com |

| Banking, Capital Goods - Defence, Construction and Shipbuilding, and Utilities | Banking, Capital Goods - Defence, Construction and Shipbuilding, and Utilities | Banking, Capital Goods - Defence, Construction and Shipbuilding, and Utilities |

| Youngho JANG Consumer, Healthcare | (82) 2 787 9838 | youngho.jang@kr.daiwacm.com |

| Henny JUNG EV Batteries and Battery Components | (82) 2 787 9182 Materials, IT/Electronics | henny.jung@kr.daiwacm.com (Small/Mid Cap), Automobiles |

| Daeho SON Industrials - Robotics | (82) 2 787 9176 | dh.son@kr.daiwacm.com |

| Joon LEE Media | (82) 2 787 9151 | hj.lee@kr.daiwacm.com |

| Thomas Y KWON | (82) 2 787 9181 | yskwon@kr.daiwacm.com |

| Pan-Asia Head of Internet & Telecommunications; Online Games | Pan-Asia Head of Internet & Telecommunications; Online Games | Pan-Asia Head of Internet & Telecommunications; Online Games |

| SK KIM | (82) 2 787 9173 | sk.kim@kr.daiwacm.com |

| TAIWAN | TAIWAN | TAIWAN |

|---|---|---|

| Rick HSU | (886) 2 8758 6261 | rick.hsu@daiwacm-cathay.com.tw |

| Sheng CHENG IT/Technology Hardware China) | (886) 2 8758 6253 (Automation, Datacentre | sheng.cheng@daiwacm-cathay.com.tw Components and PCB/CCL) (Greater |

| Allan WANG IT/Technology Hardware China) | (886) 2 8758 6249 (Automation, Datacentre | allan.wang@daiwacm-cathay.com.tw Components and PCB/CCL) (Greater |

| Helen CHIEN Small/Mid Cap | (886) 2 8758 6254 | helen.chien@daiwacm-cathay.com.tw |

Daiwa's Offices

| Office / Branch / Affiliate | Address | Tel | Fax |

|---|---|---|---|

| DAIWA SECURITIES GROUP INC | |||

| HEAD OFFICE | Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6753 | (81) 3 5555 3111 | (81) 3 5555 0661 |

| Daiwa Securities Trust Company | One Evertrust Plaza, Jersey City, NJ 07302, U.S.A. | (1) 201 333 7300 | (1) 201 333 7726 |

| Daiwa Securities Trust and Banking (Europe) PLC (Head Office) | 5 King William Street, London EC4N 7JB, United Kingdom | (44) 207 320 8000 | (44) 207 410 0129 |

| Daiwa Europe Trustees (Ireland) Ltd | Level 3, Block 5, Harcourt Centre, Harcourt Road, Dublin 2, Ireland | (353) 1 603 9900 | (353) 1 478 3469 |

| Daiwa Capital Markets America Inc. New York Head Office | 1251 Avenue of the Americas, 49th Floor, New York, NY 10020 | (1) 212 612 7000 | (1) 212 612 7100 |

| Daiwa Capital Markets America Inc. San Francisco Branch | 555 California Street, Suite 3360, San Francisco, CA 94104, U.S.A. | (1) 415 955 8100 | (1) 415 956 1935 |

| Daiwa Capital Markets Europe Limited, London Head Office | 5 King William Street, London EC4N 7AX, United Kingdom | (44) 20 7597 8000 | (44) 20 7597 8600 |

| Daiwa Capital Markets Deutschland GmbH | Friedrich-Ebert-Anlage 35-37, 60327 Frankfurt am Main, Germany | (49) 69 27139 8100 | (49) 69 27139 8190 |

| Daiwa Capital Markets Europe Limited, Paris Representative Office | 17, rue de Surène 75008 Paris, France | (33) 1 56 262 200 | (33) 1 47 550 808 |

| Daiwa Capital Markets Europe Limited, Moscow Representative Office | Midland Plaza 7th Floor, 10 Arbat Street, Moscow 119002, Russian Federation | (7) 495 641 3416 | (7) 495 775 6238 |

| Daiwa Capital Markets Europe Limited, Bahrain Branch | 7th Floor, The Tower, Bahrain Commercial Complex, P.O. Box 30069, Manama, Bahrain | (973) 17 534 452 | (973) 17 535 113 |

| Daiwa Capital Markets Hong Kong Limited | Level 28, One Pacific Place, 88 Queensway, Hong Kong | (852) 2525 0121 | (852) 2845 1621 |

| Daiwa Capital Markets Singapore Limited | 7 Straits View, Marina One East Tower, #16-05 & #16-06, Singapore 018936, Republic of Singapore | (65) 6387 8888 | (65) 6282 8030 |

| Daiwa Capital Markets Australia Limited | Level 34, Rialto North Tower, 525 Collins Street, Melbourne, Victoria 3000, Australia | (61) 3 9916 1300 | (61) 3 9916 1330 |

| DBP-Daiwa Capital Markets Philippines, Inc | 18th Floor, Citibank Tower, 8741 Paseo de Roxas, Salcedo Village, Makati City, Republic of the Philippines | (632) 813 7344 | (632) 848 0105 |

| Daiwa-Cathay Capital Markets Co Ltd | 14/F, 200, Keelung Road, Sec 1, Taipei, Taiwan, R.O.C. | (886) 2 2723 9698 | (886) 2 2345 3638 |

| Daiwa Securities Capital Markets Korea Co., Ltd. | 20 Fl.& 21Fl. One IFC, 10 Gukjegeumyung-Ro, Yeongdeungpo-gu, Seoul, Korea | (82) 2 787 9100 | (82) 2 787 9191 |

| Daiwa Securities Co. Ltd., Beijing Representative Office | Room 301/302 , Kerry Center , 1 Guanghua Road , Chaoyang District , Beijing 100020, People's Republic of China | (86) 10 6500 6688 | (86) 10 6500 3594 |

| Daiwa (Shanghai) Corporate Strategic Advisory Co. Ltd. | 44/F, Hang Seng Bank Tower, 1000 Lujiazui Ring Road, Pudong, Shanghai China 200120 , People's Republic of China | (86) 21 3858 2000 | (86) 21 3858 2111 |

| Daiwa Securities Co. Ltd., Bangkok Representative Office | 18 th Floor, M Thai Tower, All Seasons Place, 87 Wireless Road, Lumpini, Pathumwan, Bangkok 10330, Thailand | (66) 2 252 5650 | (66) 2 252 5665 |

| Daiwa Securities Co. Ltd., Hanoi Representative Office | Suite 405, Pacific Palace Building, 83B, Ly Thuong Kiet Street, Hoan Kiem Dist. Hanoi, Vietnam | (84) 4 3946 0460 | (84) 4 3946 0461 |

DAIWA INSTITUTE OF RESEARCH LTD

| HEAD OFFICE | 15-6, Fuyuki, Koto-ku, Tokyo, 135-8460, Japan | (81) 3 5620 5100 | (81) 3 5620 5603 |

|---|---|---|---|

| MARUNOUCHI OFFICE | Gran Tokyo North Tower, 1-9-1, Marunouchi, Chiyoda-ku, Tokyo, 100-6756 (81) | 3 5555 7011 | (81) 3 5202 2021 |

| New York Research Center | 11th Floor, Financial Square, 32 Old Slip, NY, NY 10005-3504, U.S.A. | (1) 212 612 6100 | (1) 212 612 8417 |

| London Research Centre | 3/F, 5 King William Street, London, EC4N 7AX, United Kingdom | (44) 207 597 8000 | (44) 207 597 8550 |

Taiwan Microloops (6831 TT): 18 June 2026

Daiwa