PDF 原檔:260610_6274_台耀_daiwa_tuc_original.pdf

原始內容

Taiwan

Taiwan Union Technology Corp (6274 TT)

Target price:

TWD2,122.00 (from TWD1,680.00)

Share price (10 Jun): TWD1,500.00 | Up/downside: +41.5%

Favourable revenue momentum ahead

- We expect TUC to benefit from the favourable market environment…

- … with the improving product mix being a key alpha

- Reaffirming our Buy (1) rating; lifting 12M TP to TWD2,122

What's new: We provide our latest view on TUC after it joined our Taiwan Corporate day. Overall, we believe the pricing environment remains favourable towards the CCL/PCB industry given the more conservative capacity expansion from 2025/2026 (vs. a 40-50% CAGR for AI server shipments). TUC plans to increase its capacity by 0.3m/0.3m/ 1.2m to reach 2.3m/2.6m (+13%)/3.8m (+46%) from 2025 to 2027 (year end). On top of this, we believe AMZN's Trainium 3 has ramped up from 2Q26, while TUC will start benefiting more from this project from 2H26 once the key PCB vendor leverages its Taiwan/Thailand plants to manufacture, which should act as key share-price catalyst, in our view.

What's the impact: Favourable pricing environment. As we highlighted in our previous note , glass fibre and copper prices from 2H25 to 1Q26 have increased more than 20% and 40%, respectively, which has triggered TUC to increase its ASPs by 20% and 40% (above M6/below M4) to reflect the cost material increase. The last key material (ie, resin) price also increased by c.3040% after the war began in February. We believe this would also lead another c.10% price hike from 2H26, which we didn't factor in our previous note. On top of it, we also underestimated TUC's capabilities to optimise its product mix given its current supply demand situation. While the low-end product (non-low loss) only accounted for 18% of total sales in 1Q26, we expect it consumed c.50% of product capacity (eg, square feet of CCL). By relocating its capacity from low-end product (eg, M2) to high-end product (M7-8), revenue per square feet could increase by 6-8x (based on our assumptions), which we underestimated earlier. As such, we further lift our 2026 revenue growth rate to 98% YoY (from 76% YoY last time), and believe half of the upward revision is driven by the 10% ASP hike assumption from resin and the other driven by product optimisation. Also, given the CCL capacity constraint, we believe TUC also doesn't prefer to manufacture low-end products for its clients considering the return difference. As such, we also expect that gross margin from low-end product would have more meaningful increase (than high-end product) for following quarters. Along with the product mix shift, this is the key reason why we lift our gross margin assumptions by 1.3-2pp over our forecast period.

What we recommend: We lift our 2026-28E EPS by 19-39% to reflect higher ASP hikes and improving product mix. We reaffirm our Buy (1) rating and raise our 12-month TP to TWD2,122 (from TWD1,680), based on an unchanged target PER of 48x, applied to our 2H26-1H27E EPS. Downside risks: 1) weaker-than-expected demand for switches/AI servers; 2) market share loss to CCL peers; and 3) raw material shortages.

How we differ: Our 2026-27E EPS are 1-2% above the Bloomberg consensus, mainly due to our higher confidence on revenue growth .

10 June 2026

Daiwa

5

3

→

2

1

Buy

Sheng Cheng

(886) 2 8758 6253

sheng.cheng@daiwacm-cathay.com.tw

Stacy Lin (886) 2 8758 6252 stacy.lin@daiwacm-cathay.com.tw

Forecast revisions (%)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue change | 12.2 | 23.5 | 29.5 |

| Net profit change | 19 | 32.5 | 38.9 |

| Core EPS (FD) change | 19 | 32.5 | 38.9 |

Source: Daiwa forecasts

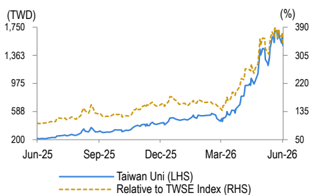

Share price performance

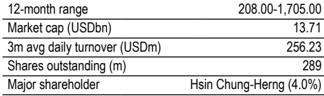

| 12-month range | 208.00-1,705.00 |

|---|---|

| Market cap (USDbn) | 13.71 |

| 3m avg daily turnover (USDm) | 256.23 |

| Shares outstanding (m) | 289 |

| Major shareholder | Hsin Chung-Herng (4.0%) |

Financial summary (TWD)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue (m) | 60,034 | 99,614 | 147,736 |

| Operating profit (m) | 12,709 | 23,468 | 36,576 |

| Net profit (m) | 9,337 | 17,388 | 27,090 |

| Core EPS (fully-diluted) | 32.308 | 60.165 | 93.735 |

| EPS change (%) | 163.7 | 86.2 | 55.8 |

| Daiwa vs Cons. EPS (%) | 1.1 | 1.5 | (9.6) |

| PER (x) | 46.4 | 24.9 | 16.0 |

| Dividend yield (%) | 1.5 | 2.8 | 4.4 |

| DPS | 22.6 | 42.1 | 65.6 |

| PBR (x) | 17.9 | 12.2 | 8.5 |

| EV/EBITDA (x) | 32.8 | 18.3 | 11.7 |

| ROE (%) | 43.6 | 58.2 | 62.8 |

Source: FactSet, Daiwa forecasts

TUC: Daiwa's revenue and earnings forecast revisions

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | Previous | New | Consensus | Previous | New | Consensus | Previous | New | Consensus |

| Revenue | 53,488 | 60,034 | 57,224 | 80,668 | 99,614 | 88,157 | 114,086 | 147,736 | 142,938 |

| Diff (%) | 12.2% | 4.9% | 23.5% | 13.0% | 29.5% | 3.4% | |||

| Gross margin (%) | 26.8% | 28.1% | 28.1% | 28.6% | 30.5% | 30.5% | 29.7% | 31.7% | 31.4% |

| Operating profit | 10,579 | 12,709 | 12,236 | 17,470 | 23,468 | 21,483 | 25,967 | 36,576 | 38,842 |

| Operating margin (%) | 19.8% | 21.2% | 21.4% | 21.7% | 23.6% | 24.4% | 22.8% | 24.8% | 27.2% |

| Net profit | 7,849 | 9,337 | 9,433 | 13,125 | 17,388 | 16,378 | 19,499 | 27,090 | 29,887 |

| EPS (TWD) | 27.16 | 32.31 | 31.97 | 45.41 | 60.17 | 59.25 | 67.47 | 93.74 | 103.68 |

| Diff (%) | 19.0% | 1.1% | 32.5% | 1.5% | 38.9% | -9.6% |

Source: Daiwa forecasts, Bloomberg

TUC: quarterly and annual P&L statement

| 2026E | 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2027E | 2025 | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | 1Q | 2QE | 3QE | 4QE | 1QE | 2QE | 3QE | 4QE | ||||

| Net revenue | 10,054 | 13,925 | 16,898 | 19,157 | 19,381 | 21,325 | 27,041 | 31,867 | 30,340 | 60,034 | 99,614 | 147,736 |

| COGS | -7,525 | -10,071 | -12,006 | -13,537 | -13,663 | -14,955 | -18,633 | -21,949 | -23,442 | -43,139 | -69,200 | -100,859 |

| Gross profit | 2,529 | 3,854 | 4,892 | 5,620 | 5,719 | 6,369 | 8,407 | 9,918 | 6,898 | 16,895 | 30,413 | 46,877 |

| Operating expenses | -701 | -971 | -1,178 | -1,336 | -1,351 | -1,487 | -1,885 | -2,222 | -2,554 | -4,186 | -6,946 | -10,301 |

| Operating profit | 1,828 | 2,883 | 3,714 | 4,284 | 4,367 | 4,883 | 6,522 | 7,696 | 4,344 | 12,709 | 23,468 | 36,576 |

| Non-operating profit | 46 | 13 | 11 | 10 | 9 | 8 | 6 | 7 | 175 | 80 | 30 | 32 |

| Pre-tax profit | 1,874 | 2,896 | 3,725 | 4,294 | 4,376 | 4,890 | 6,528 | 7,703 | 4,519 | 12,789 | 23,497 | 36,608 |

| Net profit | 1,260 | 2,143 | 2,757 | 3,177 | 3,238 | 3,619 | 4,831 | 5,700 | 3,409 | 9,337 | 17,388 | 27,090 |

| Net EPS (TWD) | 4.36 | 7.42 | 9.54 | 10.99 | 11.20 | 12.52 | 16.72 | 19.72 | 12.1 | 32.3 | 60.2 | 93.7 |

| Operating Ratios | ||||||||||||

| Gross margin | 25.1% | 27.7% | 29.0% | 29.3% | 29.5% | 29.9% | 31.1% | 31.1% | 22.7% | 28.1% | 30.5% | 31.7% |

| Operating margin | 18.2% | 20.7% | 22.0% | 22.4% | 22.5% | 22.9% | 24.1% | 24.2% | 14.3% | 21.2% | 23.6% | 24.8% |

| Pre-tax margin | 18.6% | 20.8% | 22.0% | 22.4% | 22.6% | 22.9% | 24.1% | 24.2% | 14.9% | 21.3% | 23.6% | 24.8% |

| Net margin | 12.5% | 15.4% | 16.3% | 16.6% | 16.7% | 17.0% | 17.9% | 17.9% | 11.2% | 15.6% | 17.5% | 18.3% |

| YoY (%) | ||||||||||||

| Net revenue | 58% | 105% | 110% | 110% | 93% | 53% | 60% | 66% | 32% | 98% | 66% | 48% |

| Gross profit | 65% | 169% | 155% | 179% | 126% | 65% | 72% | 76% | 29% | 145% | 80% | 54% |

| Operating profit | 95% | 238% | 193% | 232% | 139% | 69% | 76% | 80% | 30% | 193% | 85% | 56% |

| Pre-tax profit | 100% | 245% | 183% | 201% | 134% | 69% | 75% | 79% | 34% | 183% | 84% | 56% |

| Net profit | 88% | 229% | 175% | 193% | 157% | 69% | 75% | 79% | 31% | 174% | 86% | 56% |

| QoQ (%) | ||||||||||||

| Net revenue | 10% | 39% | 21% | 13% | 1% | 10% | 27% | 18% | ||||

| Gross profit | 26% | 52% | 27% | 15% | 2% | 11% | 32% | 18% | ||||

| Operating profit | 42% | 58% | 29% | 15% | 2% | 12% | 34% | 18% | ||||

| Pre-tax profit | 31% | 55% | 29% | 15% | 2% | 12% | 34% | 18% | ||||

| Net profit | 16% | 70% | 29% | 15% | 2% | 12% | 34% | 18% |

Source: Company, Daiwa forecasts

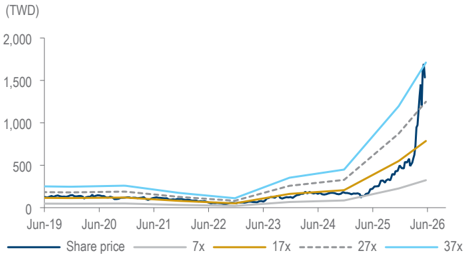

TUC: 1-year forward PER bands

Source: TEJ, Daiwa forecasts

Taiwan Union Technology Corp (6274 TT): 10 June 2026

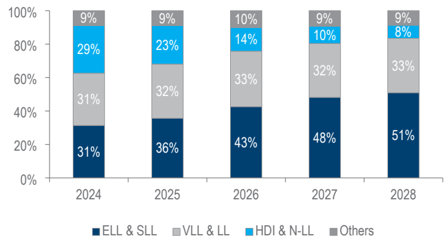

TUC: revenue breakdown by product

Source: Company, Daiwa forecasts

Daiwa

Financial summary

Key assumptions

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Global PC shipment (mn) | 361 | 301 | 260 | 263 | 287 | 244 | 244 | 244 |

| Regular server shipment (mn) | 14 | 15 | 12 | 14 | 16 | 18 | 22 | 26 |

| Global smartphone shipment (mn) | 1,655 | 1,437 | 1,380 | 1,437 | 1,429 | 1,249 | 1,255 | 1,300 |

Profit and loss (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| HSD Low Loss | 9,509 | 8,355 | 8,570 | 14,445 | 20,651 | 45,487 | 80,087 | 123,273 |

| HSD Non Low Loss | 9,932 | 7,174 | 4,885 | 5,241 | 5,582 | 6,784 | 8,176 | 9,261 |

| Other Revenue | 1,691 | 2,944 | 2,547 | 3,385 | 4,108 | 7,763 | 11,350 | 15,202 |

| Total Revenue | 21,132 | 18,472 | 16,003 | 23,070 | 30,340 | 60,034 | 99,614 | 147,736 |

| Other income | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| COGS | (16,702) | (15,067) | (12,844) | (17,729) | (23,442) | (43,139) | (69,200) | (100,859) |

| SG&A | (1,786) | (1,597) | (1,422) | (1,668) | (2,039) | (605) | 0 | 0 |

| Other op.expenses | (264) | (311) | (313) | (342) | (515) | (3,581) | (6,946) | (10,301) |

| Operating profit | 2,380 | 1,498 | 1,424 | 3,332 | 4,344 | 12,709 | 23,468 | 36,576 |

| Net-interest inc./(exp.) | (30) | (29) | (27) | (52) | (89) | (116) | (110) | (108) |

| Assoc/forex/extraord./others | 63 | 152 | 153 | 98 | 264 | 196 | 139 | 140 |

| Pre-tax profit | 2,413 | 1,621 | 1,550 | 3,378 | 4,519 | 12,789 | 23,497 | 36,608 |

| Tax | (532) | (360) | (726) | (773) | (1,109) | (3,452) | (6,109) | (9,518) |

| Min. int./pref. div./others | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Net profit (reported) | 1,881 | 1,261 | 823 | 2,604 | 3,409 | 9,337 | 17,388 | 27,090 |

| Net profit (adjusted) | 1,881 | 1,261 | 823 | 2,604 | 3,409 | 9,337 | 17,388 | 27,090 |

| EPS (reported)(TWD) | 7.010 | 4.687 | 3.049 | 9.561 | 12.135 | 32.308 | 60.165 | 93.735 |

| EPS (adjusted)(TWD) | 7.010 | 4.687 | 3.049 | 9.561 | 12.135 | 32.308 | 60.165 | 93.735 |

| EPS (adjusted fully-diluted)(TWD) | 7.014 | 4.687 | 3.052 | 9.573 | 12.250 | 32.308 | 60.165 | 93.735 |

| DPS (TWD) | 5.005 | 4.000 | 4.008 | 6.504 | 8.491 | 22.616 | 42.116 | 65.615 |

| EBIT | 2,380 | 1,498 | 1,424 | 3,332 | 4,344 | 12,709 | 23,468 | 36,576 |

| EBITDA | 2,819 | 1,960 | 1,885 | 3,784 | 4,803 | 13,347 | 24,201 | 37,419 |

Cash flow (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Profit before tax | 2,413 | 1,621 | 1,550 | 3,378 | 4,519 | 12,789 | 23,497 | 36,608 |

| Depreciation and amortisation | 439 | 462 | 461 | 452 | 459 | 638 | 733 | 843 |

| Tax paid | (532) | (360) | (726) | (773) | (1,109) | (3,452) | (6,109) | (9,518) |

| Change in working capital | 4,224 | (3,625) | 1,136 | 5,588 | 13,451 | 25,807 | 42,895 | 32,474 |

| Other operational CF items | (5,033) | 4,227 | (1,300) | (7,967) | (16,724) | (38,453) | (56,933) | (44,470) |

| Cash flow from operations | 1,512 | 2,326 | 1,120 | 677 | 596 | (2,671) | 4,083 | 15,937 |

| Capex | (433) | (381) | (634) | (1,196) | (1,949) | (2,774) | (1,400) | (1,400) |

| Net (acquisitions)/disposals | 0 | 3 | 0 | (9) | 4 | 8 | 6 | 7 |

| Other investing CF items | 1,702 | 1,054 | 389 | 75 | (4,558) | 1,675 | 0 | 0 |

| Cash flow from investing | 1,269 | 677 | (244) | (1,130) | (6,502) | (1,091) | (1,394) | (1,393) |

| Change in debt | (9) | (583) | 531 | (372) | 4,141 | 3,209 | 4,569 | 3,977 |

| Net share issues/(repurchases) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Dividends paid | (2,574) | (2,694) | (2,153) | (2,180) | (3,594) | (2,454) | (6,536) | (12,171) |

| Other financing CF items | 1,402 | 1,333 | (19) | 3,927 | 4,341 | 375 | 0 | 0 |

| Cash flow from financing | (1,180) | (1,944) | (1,641) | 1,376 | 4,888 | 1,131 | (1,967) | (8,195) |

| Forex effect/others | (21) | 115 | (166) | 399 | (97) | 508 | 427 | 393 |

| Change in cash | 1,580 | 1,173 | (932) | 1,322 | (1,115) | (2,123) | 1,149 | 6,743 |

| Free cash flow | 1,079 | 1,945 | 486 | (519) | (1,353) | (5,445) | 2,683 | 14,537 |

Source: FactSet, Daiwa forecasts

Taiwan Union Technology Corp (6274 TT): 10 June 2026

Daiwa

Financial summary continued …

Balance sheet (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Cash & short-term investment | 6,582 | 6,814 | 5,657 | 7,037 | 10,602 | 6,786 | 7,935 | 14,678 |

| Inventory | 2,857 | 1,965 | 2,061 | 3,189 | 7,405 | 11,503 | 20,755 | 26,078 |

| Accounts receivable | 7,602 | 6,161 | 6,713 | 9,711 | 13,823 | 29,252 | 48,466 | 65,378 |

| Other current assets | 162 | 143 | 187 | 326 | 521 | 560 | 560 | 560 |

| Total current assets | 17,202 | 15,084 | 14,618 | 20,264 | 32,351 | 48,100 | 77,716 | 106,694 |

| Fixed assets | 4,743 | 4,671 | 4,793 | 5,614 | 7,386 | 9,557 | 10,224 | 10,781 |

| Goodwill & intangibles | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other non-current assets | 5 | 8 | 9 | 0 | 4 | 21 | 15 | 8 |

| Total assets | 21,951 | 19,763 | 19,420 | 25,878 | 39,741 | 57,679 | 87,955 | 117,483 |

| Short-term debt | 447 | 2,237 | 603 | 962 | 2,141 | 2,481 | 2,599 | 2,745 |

| Accounts payable | 5,741 | 4,143 | 4,581 | 6,642 | 11,871 | 20,577 | 35,005 | 45,244 |

| Other current liabilities | 252 | 174 | 364 | 269 | 608 | 886 | 886 | 886 |

| Total current liabilities | 6,440 | 6,553 | 5,548 | 7,873 | 14,621 | 23,943 | 38,490 | 48,874 |

| Long-term debt | 3,521 | 1,146 | 2,106 | 3,449 | 6,304 | 9,193 | 13,643 | 17,475 |

| Other non-current liabilities | 252 | 205 | 187 | 219 | 203 | 314 | 314 | 314 |

| Total liabilities | 10,214 | 7,904 | 7,840 | 11,541 | 21,127 | 33,450 | 52,447 | 66,663 |

| Share capital | 2,689 | 2,692 | 2,712 | 2,760 | 2,887 | 2,888 | 2,888 | 2,888 |

| Reserves/R.E./others | 9,047 | 9,167 | 8,868 | 11,577 | 15,727 | 21,341 | 32,621 | 47,932 |

| Shareholders' equity | 11,737 | 11,858 | 11,580 | 14,337 | 18,614 | 24,229 | 35,508 | 50,820 |

| Minority interests | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Total equity & liabilities | 21,951 | 19,763 | 19,420 | 25,878 | 39,741 | 57,679 | 87,955 | 117,483 |

| EV | 430,888 | 430,070 | 430,553 | 430,875 | 431,344 | 438,389 | 441,809 | 439,042 |

| Net debt/(cash) | (2,613) | (3,431) | (2,948) | (2,626) | (2,158) | 4,888 | 8,307 | 5,541 |

| BVPS (TWD) | 43.735 | 44.063 | 42.875 | 52.635 | 66.255 | 83.837 | 122.866 | 175.847 |

Key ratios (%)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Sales (YoY) | 17.1 | (12.6) | (13.4) | 44.2 | 31.5 | 97.9 | 65.9 | 48.3 |

| EBITDA (YoY) | 5.8 | (30.5) | (3.8) | 100.8 | 26.9 | 177.9 | 81.3 | 54.6 |

| Operating profit (YoY) | 4.7 | (37.1) | (4.9) | 133.9 | 30.4 | 192.6 | 84.7 | 55.9 |

| Net profit (YoY) | 6.0 | (32.9) | (34.7) | 216.3 | 30.9 | 173.9 | 86.2 | 55.8 |

| Core EPS (fully-diluted) (YoY) | 5.1 | (33.2) | (34.9) | 213.7 | 28.0 | 163.7 | 86.2 | 55.8 |

| Gross-profit margin | 21.0 | 18.4 | 19.7 | 23.2 | 22.7 | 28.1 | 30.5 | 31.7 |

| EBITDA margin | 13.3 | 10.6 | 11.8 | 16.4 | 15.8 | 22.2 | 24.3 | 25.3 |

| Operating-profit margin | 11.3 | 8.1 | 8.9 | 14.4 | 14.3 | 21.2 | 23.6 | 24.8 |

| Net profit margin | 8.9 | 6.8 | 5.1 | 11.3 | 11.2 | 15.6 | 17.5 | 18.3 |

| ROAE | 16.5 | 10.7 | 7.0 | 20.1 | 20.7 | 43.6 | 58.2 | 62.8 |

| ROAA | 9.1 | 6.0 | 4.2 | 11.5 | 10.4 | 19.2 | 23.9 | 26.4 |

| ROCE | 15.5 | 9.7 | 9.6 | 20.2 | 19.0 | 40.4 | 53.5 | 59.6 |

| ROIC | 21.2 | 13.3 | 8.9 | 25.3 | 23.3 | 40.7 | 47.6 | 54 |

| Net debt to equity | net cash | net cash | net cash | net cash | 17.6 | 35.6 | 33.9 | 18.3 |

| Effective tax rate | 22.0 | 22.2 | 46.9 | 22.9 | 24.6 | 27.0 | 26 | 26 |

| Accounts receivable (days) | 114.3 | 136.0 | 146.8 | 129.9 | 141.6 | 130.9 | 142.4 | 140.6 |

| Current ratio (x) | 2.7 | 2.3 | 2.6 | 2.6 | 2.2 | 2.0 | 2 | 2.2 |

| Net interest cover (x) | 0.8 | 0.6 | 0.6 | 0.7 | 0.5 | 1.1 | 2.1 | 3.4 |

| Net dividend payout | 71.4 | 85.3 | 131.8 | 68.1 | 70.0 | 70.0 | 70 | 70 |

| Free cash flow yield | 0.2 | 0.4 | 0.1 | n.a. | n.a. | n.a. | 0.6 | 3.4 |

Source: FactSet, Daiwa forecasts

Company profile

Taiwan Union Technology Corporation (TUC) was established in 1974. In 2001, TUC started to provide its Mass Lamination service to customers. In Dec., 2003, TUC was officially listed in Taiwan OTC. In 2004, TUC established its Changshu plant in Jiangsu, China to satisfy customer demand in the Greater China area. TUC also provides its services globally from its network in Taiwan, China, Japan, South Korea, USA and Germany.

Taiwan Union Technology Corp (6274 TT): 10 June 2026

Daiwa

ESG analysis

ESG risks

| Risks | Risks | Management | Analyst comments |

|---|---|---|---|

| G | Executive/board quality | 2 | TUC has diverse stakeholders with varying interests. The concerns of each stakeholder category differ. TUC's departments engage with stakeholders through various channels to ensure timely communication and understanding of the Company's operations. TUC also tracks stakeholder requests and expectations and responds promptly. The Company reports to the Board of Directors annually on its communication with key stakeholders. |

| G | Capital management | 1 | TUC pays its dividend on a annual basis. In the past 5 years, it has managed its dividend payout well. We believe TUC will at least sustain its cash dividend payout in dollar terms over 2025-27E. We see its balance between investment and dividend as appropriate. |

| G | Related party & transaction | 2 | TUC's sales to related parties were insignifacnt versus its total revenue. We see limited risk for TUC. |

| S | Supply chain management | 1 | TUC audits Tier 1 suppliers for ESG compliance, requiring commitments on hazardous substance bans and human rights. Several supplier audits were completed with a 100% pass rate and no major violations. |

| S | Data security | 2 | TUC operates an Information Security Office and implements training, audits, and ISO 27001- compliant systems. No security incidents disrupted operations, and 683 employees attended security training. |

Note: Management score represents a company's ability to manage/benefit from certain ESG topics. The scores range from 1 to 3, with 1 being the strongest.

Update Date: 6 May 2026

Source: Daiwa, Company

Taiwan Union Technology Corp (6274 TT): 10 June 2026

Daiwa