PDF 原檔:260528_6285_起碁_gs_WNC_original.pdf

原始內容

WNC (6285.TW): 800G switch in expansion; Buy with TP up to NT$364

WNC is bene fi ting from networking technology migrations. As a major ODM supplier of network communications solutions with long-term experience, WNC enables rapid shipment of new designs for its customers. We remain positive on WNC, riding on the networking switch product expansion, including the Enterprise 800G switch (contributing revenues in 2H26) and OCS switch (long-term opportunities) , the accelerating adoption of LEO satellite networks (Read more), and the WiFi-7 adoption cycle that is driving up replacement demand. We raise our 12-month target price by 14.5% to NT$364.0 and maintain our Buy rating.

800G switch in expansion. As a leading ODM for networking equipment, WNC will start mass shipment of 800G switch in 2H26. The 800G switch will be an ODM product for branded customers, targeting enterprise clients as the major end users. This supports our positive view on rising networking demand along with AI computing, where 800G high-speed products have already expanded applications from CSPs to enterprises. With ongoing networking technology migrations, we expect 800G switch demand to continue into 2027 and may expand to 1.6T in the future. Apart from the 800G switch, OCS switches are also a long term opportunity (link), as they are also innovative networking products that will greatly increase data transmission e ffi ciency and in our view have the potential to become a mainstream form factor in the future. We are positive that the continuous development of advanced networking solutions will support WNC's growth along with the ramping trend of networking advancements in AI data centers.

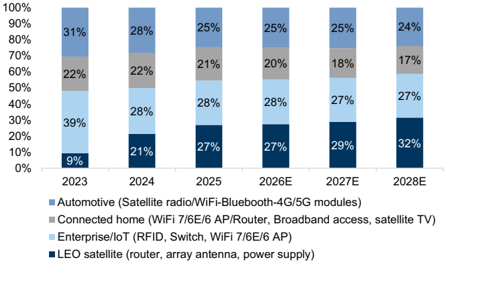

Exhibit 1: WNC's revenue mix

Source: Company data, Goldman Sachs Global Investment Research

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to ed as research www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi analysts with FINRA in the U.S.

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Verena Jeng +852-2978-1681 | verena.jeng@gs.com

Goldman Sachs (Asia) L.L.C.

Xuan Zhang +852-2978-1478 | xuan.zhang@gs.com

Goldman Sachs (Asia) L.L.C.

e92c7a75ab8b4efbba794e6b187208c8

Earnings revision: we raise WNC revenues by 1%/ 2%/ 2% for 2026-28E, based on a more positive outlook on the high speed switch business. While we raise revenues by 1%/ 2%/ 2%, we make no changes to our GM and OPM estimates as we already factored in the higher margin expectations of WNC as new products ramp up, with 2026-28E GM at 13.5%+ (vs. 2025A GM of 12.5%).

Exhibit 2: Earnings revisions

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| NT$m | Old | New | Diff% | Old | New | Diff% | Old | New | Diff% |

| Revenues | 132,190 | 132,995 | 1% | 151,365 | 154,417 | 2% | 169,085 | 172,508 | 2% |

| GP | 18,355 | 18,468 | 1% | 20,617 | 21,044 | 2% | 23,081 | 23,560 | 2% |

| OP | 6,509 | 6,551 | 1% | 7,600 | 7,764 | 2% | 9,560 | 9,768 | 2% |

| Net income | 5,224 | 5,259 | 1% | 6,080 | 6,212 | 2% | 7,666 | 7,830 | 2% |

| Margins | |||||||||

| GM | 13.9% | 13.9% | 13.6% | 13.6% | 13.7% | 13.7% | |||

| OPM | 4.9% | 4.9% | 5.0% | 5.0% | 5.7% | 5.7% | |||

| NM | 4.0% | 4.0% | 4.0% | 4.0% | 4.5% | 4.5% |

Source: Company data, Goldman Sachs Global Investment Research

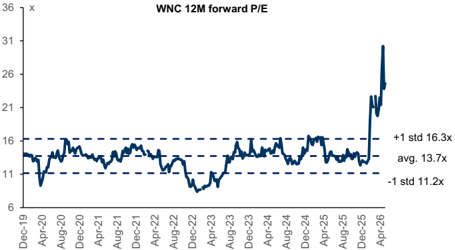

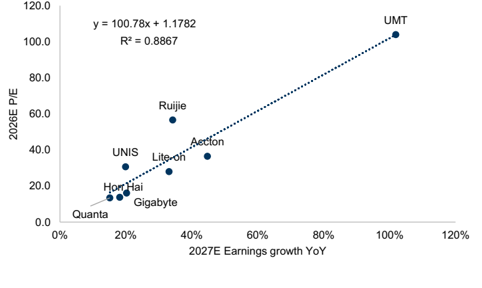

Valuation: With the earning estimate changes and a refreshed target P/E ratio, we raise our 12M TP by 14.5% to NT$364.0 (based on 28.0x 2027E P/E , vs. 25.0x previously). We continue to base our TP on 2027E P/E, and the target multiple is still derived from the correlation between P/E and EPS growth of its peers (Exhibit 5), which is higher as we mark to market. Our target P/E of 28.0x is higher than company's avg. +1 std P/E (16.3x), which we believe is not stretched considering the sustainable growth of WNC driven by long-term satellite and high speed networking demand. Maintain Buy.

Exhibit 3: WNC P&L summary

| NT$ mn | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 | 2Q26E | 3Q26E | 4Q26E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Income statement | |||||||||||||||

| Revenue | 95,257 | 110,788 | 110,213 | 110,251 | 132,995 | 154,417 | 172,508 | 28,366 | 27,491 | 27,378 | 27,015 | 29,156 | 31,021 | 36,718 | 36,100 |

| Gross profit | 11,595 | 13,594 | 13,381 | 13,762 | 18,468 | 21,044 | 23,560 | 3,462 | 3,176 | 3,319 | 3,805 | 4,011 | 4,307 | 5,122 | 5,027 |

| Selling expense | 2,994 | 3,277 | 3,264 | 3,219 | 3,788 | 4,169 | 4,218 | 758 | 730 | 824 | 907 | 850 | 900 | 1,028 | 1,011 |

| G&A expense | 1,489 | 1,636 | 2,069 | 2,263 | 2,679 | 3,088 | 3,019 | 576 | 540 | 547 | 601 | 593 | 630 | 734 | 722 |

| R&D expense | 3,584 | 4,007 | 4,427 | 4,511 | 5,449 | 6,022 | 6,555 | 1,084 | 1,027 | 1,199 | 1,201 | 1,207 | 1,365 | 1,469 | 1,408 |

| OP income | 3,527 | 4,674 | 3,622 | 3,768 | 6,551 | 7,764 | 9,768 | 1,045 | 879 | 749 | 1,096 | 1,362 | 1,412 | 1,891 | 1,886 |

| Pretax income | 3,760 | 4,801 | 4,242 | 3,854 | 6,493 | 7,716 | 9,726 | 1,099 | 626 | 880 | 1,248 | 1,427 | 1,372 | 1,851 | 1,844 |

| Net income | 3,122 | 3,803 | 3,451 | 3,063 | 5,259 | 6,212 | 7,830 | 918 | 493 | 665 | 987 | 1,132 | 1,097 | 1,518 | 1,512 |

| EBITDA | 5,317 | 6,759 | 6,263 | 6,773 | 8,953 | 9,949 | 11,894 | 1,774 | 1,592 | 1,531 | 1,876 | 1,962 | 2,013 | 2,492 | 2,487 |

| EPS (NT$) | 7.41 | 8.58 | 7.10 | 6.41 | 11.01 | 13.00 | 16.39 | 1.92 | 1.03 | 1.39 | 2.07 | 2.37 | 2.30 | 3.18 | 3.16 |

| DPS (NT$) | 4.84 | 6.00 | 4.80 | 4.30 | 7.38 | 8.72 | 10.99 | ||||||||

| Dividend payout | 65.4% | 69.9% | 67.6% | 67.1% | 67.1% | 67.1% | 67.1% | ||||||||

| Dividend yield | 4% | 5% | 4% | 4% | 6% | 7% | 9% | ||||||||

| Ratios | |||||||||||||||

| R&D to rev | 3.8% | 3.6% | 4.0% | 4.1% | 4.1% | 3.9% | 3.8% | 3.8% | 3.7% | 4.4% | 4.4% | 4.1% | 4.4% | 4.0% | 3.9% |

| Opex ratio | 8.5% | 8.1% | 8.9% | 9.1% | 9.0% | 8.6% | 8.0% | 8.5% | 8.4% | 9.4% | 10.0% | 9.1% | 9.3% | 8.8% | 8.7% |

| Tax rate | 17.0% | 20.8% | 18.6% | 20.5% | 19.0% | 19.5% | 19.5% | 16.5% | 21.2% | 24.4% | 20.9% | 20.6% | 20.0% | 18.0% | 18.0% |

| Margins | |||||||||||||||

| Gross margin | 12.2% | 12.3% | 12.1% | 12.5% | 13.9% | 13.6% | 13.7% | 12.2% | 11.6% | 12.1% | 14.1% | 13.8% | 13.9% | 14.0% | 13.9% |

| Operating margin | 3.7% | 4.2% | 3.3% | 3.4% | 4.9% | 5.0% | 5.7% | 3.7% | 3.2% | 2.7% | 4.1% | 4.7% | 4.6% | 5.2% | 5.2% |

| Pretax margin | 3.9% | 4.3% | 3.8% | 3.5% | 4.9% | 5.0% | 5.6% | 3.9% | 2.3% | 3.2% | 4.6% | 4.9% | 4.4% | 5.0% | 5.1% |

| Net margin | 3.3% | 3.4% | 3.1% | 2.8% | 4.0% | 4.0% | 4.5% | 3.2% | 1.8% | 2.4% | 3.7% | 3.9% | 3.5% | 4.1% | 4.2% |

| EBITDA margin | 5.6% | 6.1% | 5.7% | 6.1% | 6.7% | 6.4% | 6.9% | 6.3% | 5.8% | 5.6% | 6.9% | 6.7% | 6.5% | 6.8% | 6.9% |

| YoY | |||||||||||||||

| Revenue | 42% | 16% | -1% | 0% | 21% | 16% | 12% | 11% | -10% | 5% | -3% | 3% | 13% | 34% | 34% |

| Gross profit | 60% | 17% | -2% | 3% | 34% | 14% | 12% | 17% | -18% | 12% | 6% | 16% | 36% | 54% | 32% |

| OP income | 305% | 33% | -23% | 4% | 74% | 19% | 26% | 58% | -29% | 25% | -2% | 30% | 61% | 153% | 72% |

| Pretax income | 166% | 28% | -12% | -9% | 68% | 19% | 26% | 17% | -54% | 41% | -4% | 30% | 119% | 110% | 48% |

| Net income | 153% | 22% | -9% | -11% | 72% | 18% | 26% | 22% | -58% | 28% | -3% | 23% | 123% | 128% | 53% |

| EBITDA | 119% | 27% | -7% | 8% | 32% | 11% | 20% | 42% | -16% | 19% | 3% | 11% | 26% | 63% | 33% |

| QoQ | |||||||||||||||

| Revenue | 1% | -3% | 0% | -1% | 8% | 6% | 18% | -2% | |||||||

| Gross profit | -4% | -8% | 4% | 15% | 5% | 7% | 19% | -2% | |||||||

| OP income | -6% | -16% | -15% | 46% | 24% | 4% | 34% | 0% | |||||||

| Pretax income | -16% | -43% | 41% | 42% | 14% | -4% | 35% | 0% | |||||||

| Net income | -10% | -46% | 35% | 48% | 15% | -3% | 38% | 0% | |||||||

| EBITDA | -2% | -10% | -4% | 23% | 5% | 3% | 24% | 0% |

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

Exhibit 4: WNC 12M forward P/E

Source: Re fi nitiv Eikon

Exhibit 5: WNC peers' correlation of P/E and earnings growth

Source: TEJ

Price Target Risks and Methodology: WNC

Valuation: We use a near-term P/E to derive our 12m target price for WNC, consistent with our Taiwan Technology coverage. We base our TP of NT$364.0 on a target P/E multiple of 28.0x on a forward year EPS (2027E). Our target P/E is derived from the correlation between P/E and EPS growth of its peers. We are Buy rated on WNC. Key downside risks: fi ercer-than-expected competition in satellite communication, slower-than-expected Wi-Fi 7 or 5G FWA ramp-up in US and Europe markets.

| 6285.TW | 12m Price Target: NT$364.00 | 12m Price Target: NT$364.00 | Price: NT$311.50 | Price: NT$311.50 | Upside: 16.9% | Upside: 16.9% |

|---|---|---|---|---|---|---|

| Buy | Buy | GS Forecast | ||||

| Revenue ( NT$m n ) N e w Revenue (NT$ mn) Old EBITD A (NT$ mn) E PS ( NT$) N e w | 1 2 / 25 11 0,250. 8 110,250.8 6,772.9 6 .4 1 6.41 | 1 2 / 2 6E 1 32,995.5 132,190.2 8,952.8 11 .0 1 10.93 28.3 | 1 2 / 2 7E 1 54,4 17 . 1 151,364.5 | 1 2 / 2 8E 17 2,50 7 . 6 169,084.6 11,894.1 16 .39 16.04 19.0 3.7 | ||

| Market c ap: NT$148.1b n / $4. 7 b n En terpr is e v a lu e: | ||||||

| NT$14 3 .4b n / $4. 6 b n | 9,948.7 | |||||

| 3m AD T V : NT$ 7 . 0 b n / $ 22 1. 3mn n | 1 | 3.00 | ||||

| Ta iw a | EPS (NT$) Old | 12.73 | ||||

| G reater Chin a Te chnology | P/E (X) | 19.2 | 24.0 | |||

| M &A R a n k: 3 | P/B (X) | 1.7 | 4.1 | 3.9 | ||

| L ea s e s incl . in n et d ebt & EV? : | Dividend yield (%) | 3.5 | 2.4 | 2.8 | 3.5 | |

| Y e s | CROCI (%) | 13.1 | 16.9 | 17.2 | 18.9 | |

| 3 / 2 6 | 6/ 2 6E | 9 / 2 | 6E | 1 2 / 2 6E | ||

| EPS (NT$) | 2.37 | 2.30 | 3.18 | 3.16 |

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 27 May 2026 close.

e92c7a75ab8b4efbba794e6b187208c8