PDF 原檔:報告_GS_萬潤6187_20260709_original.pdf

圖片清單(已驗證 2026-07-09)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_GS_萬潤6187_20260709_003.png |

42KB | 真資料圖 | Exhibit 1:「All Ring's revenue growth outlook」長條+曲線圖,NT$mn,2024-2028E,分 Others/Passive component equipment/Semi equipment-others/Semi equipment-CoWoS/Semi equipment-CPO,另疊 YoY% 曲線 |

報告_GS_萬潤6187_20260709_004.png |

29KB | 真資料圖 | Exhibit 2:「All Ring's margin trend」GM/OpM 曲線圖,2022-2028E |

報告_GS_萬潤6187_20260709_005.png |

47KB | 真資料圖 | Exhibit 5:「Taiex vs. All Ring」雙軸股價比較圖,2014/07-2026/07 |

報告_GS_萬潤6187_20260709_006.png |

41KB | 真資料圖 | Exhibit 6:「Forward P/E」股價圖疊 20x-40x 本益比帶狀線,2014/07-2026/07 |

報告_GS_萬潤6187_20260709_007.png |

42KB | 真資料圖 | Exhibit 7:「Forward P/B」股價圖疊 8x-14x 淨值比帶狀線,2014/07-2026/07 |

報告_GS_萬潤6187_20260709_008.png |

38KB | 真資料圖 | Exhibit 8:「P/B vs ROE」ROE 長條圖+Fwd P/B 曲線,2014/07-2026/07 |

報告_GS_萬潤6187_20260709_009.png |

76KB | 真資料圖 | 萬潤(6187.TWO) 評等與目標價沿革圖,股價曲線疊評等變化(2026/3/10 由 NA 升至 Buy)與多次目標價調整標記(550/475/320/365/800 等),Covered by Evelyn Yu as of Jun 25, 2025 |

報告_GS_萬潤6187_20260709_001.png |

22KB | 真資料圖 | 「GS Factor Profile」橫向長條圖,Growth/Financial Returns/Multiple/Integrated 四維度百分位,對比 6187.TWO vs Asia ex-Japan Coverage 與 vs Taiwan Semiconductor |

報告_GS_萬潤6187_20260709_002.png |

29KB | 真資料圖 | 「Price Performance」股價曲線圖,6187.TWO(NT$) vs Taiwan SE Weighted Index,2025/10-2026/07 |

原始內容

For the exclusive use of KEVINLU@LENOVO.COM

All Ring Tech Co. (6187.TWO)

CPO concern likely largely priced in; building in stronger CoWoS into 2027E; reiterate Buy

6187.TWO

12m Pri c e Target:

NT$1,550.00

2Q26 tracking ahead of expectations

All Ring reported its June 2026 revenue on July 8, 2026, with June revenue of NT$1,012mn, bringing total 2Q26 revenue to NT$2,355mn, coming in 12.8% ahead of GSe. We attribute the strong 2Q26 momentum primarily to the stronger ramp of CoWoS demand from customers. With this, we raise our 2Q26 GM as we anticipate All Ring to exceed our prior expectation (52.3% previously), supported by a higher advanced packaging mix, though we now expect a modest sequential decline in 4Q26 GM as All Ring begins shipping new products including new panel-level equipment, which we believe will weigh on margins during the initial ramp-up phase. Overall, we now forecast 2Q26/3Q26/4Q26E GM to be 54.0%/54.5%/52.7%.

Stronger advanced packaging expansion supporting 2027 outlook

In our recent TSMC report (see: TSMC (2330.TW) Accelerating capacity build to secure a stronger growth trajectory, 3 Jul 2026) , we raised our end-2027E CoWoS (include WMCM) capacity to 280kwpm (vs. 250kwpm previously), fueled by stronger AI accelerator and server-CPU demand. As a key back-end equipment supplier for CoWoS, we expect All Ring to bene fi t directly from such accelerating capacity expansion. We now model All Ring's CoWoS-related revenue to grow 27% YoY in 2027E (vs. 16% YoY previously) and account for 77% of total revenue (vs. 60% previously).

CPO trending towards fewer shipment but higher-value tools

On the CPO side, we revise down our revenue forecast as we factor in lower equipment shipment as we believe All Ring is working to increase the throughput to meet customer requests. While we believe this could translate into fewer equipment shipments given higher productivity, we expect the content value per equipment to increase. On pricing, we now see upside to ASP and are now

BUY

Evelyn Yu

+886(2)2730-4187 | evelyn.yu@gs.com Goldman Sachs (Asia) L.L.C., Taipei Branch

Ryan Huang, CFA

+886(2)2730-4084 | ryan.huang@gs.com Goldman Sachs (Asia) L.L.C., Taipei Branch

Key Data _____________________________________

Market cap: NT$91.7bn / $2.9bn

Enterprise value: NT$88.6bn / $2.8bn

3m ADTV: NT$3.7bn / $117.0mn

Taiwan

Taiwan Semiconductor

M&A Rank: 3

Leases incl. in net debt & EV?: Yes

| GS Forecast | 12/25 | __________ 12/26E | 12/27E | 12/28E |

|---|---|---|---|---|

| Revenue(NT$mn) New | 5,366.2 | 9,276.9 | 13,477.6 | 17,193.8 |

| Revenue (NT$ mn) Old | 5,366. 2 | 8,865.3 | 14,693.0 | 19,889.0 |

| EBITDA (NT$ mn) | 1,679.3 | 3, 2 65.4 | 5,316.0 | 7,197.3 |

| EPS(NT$) New | 15.47 | 28.23 | 44.30 | 59.13 |

| EPS (NT$) Old | 15.47 | 2 6.33 | 47.13 | 66.88 |

| P/E (X) | 22 .7 | 33.8 | 2 1.6 | 16. 2 |

| P/B (X) | 4.5 | 11. 2 | 8.8 | 7.1 |

| Dividend yield (%) | 3.3 | 2 . 2 | 3.5 | 4.6 |

| CROCI (%) | 44. 2 | 36.5 | 66.9 | 71. 2 |

| 3/26 | 6/26E | 9/26E | 12/26E | |

| EPS (NT$) | 3.37 | 6. 2 5 | 10.8 2 | 7.79 |

Source: Company data, Goldman Sachs Research estimates. See disclosures for details.

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi ed as research analysts with FINRA in the U.S.

Pri c e:

NT$955.00

Upside:

62.3%

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

BUY

All Ring Tech Co. (6187.TWO)

Rating since Mar 11, 2026

Ratios & Valuation __________________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| P/E (X) | 22.7 | 33.8 | 21.6 | 16.2 |

| P/B (X) | 4.5 | 11.2 | 8.8 | 7.1 |

| FCF yield (%) | 4.3 | 0.2 | 2.6 | 4.9 |

| EV/EBITD A R(X) | 17.8 | 27.2 | 16.6 | 12.1 |

| EV/EBITD A (excl. leases) (X) | 17.8 | 27.2 | 16.6 | 12.1 |

| CROCI (%) | 44.2 | 36.5 | 66.9 | 71.2 |

| ROE (%) | 21.5 | 35.3 | 46.2 | 49.1 |

| Net debt/equity (%) | (51.3) | (37.1) | (32.9) | (36.8) |

| Net debt/equity (excl. leases) (%) | (51.3) | (37.1) | (32.9) | (36.8) |

| Inte r est c ov e r (X) | 172.6 | 459.1 | 824.4 | 1 , 113.7 |

| Days in v ent or y o utst , sales | 70.2 | 72.4 | 83.7 | 73.2 |

| Recei v able days | 82.1 | 46.5 | 56.4 | 56.4 |

| Days p ayable o utstandin g | 210.6 | 173.0 | 206.7 | 191.5 |

| DuP o nt ROE (%) | 19.8 | 32.8 | 40.5 | 43.7 |

| Tu r n ov e r (X) | 0.6 | 0.8 | 0.9 | 1.0 |

| L e v e r a g e (X) | 1.3 | 1.4 | 1.5 | 1.4 |

| Gro ss cas h in v ested (ex cas h ) (NT $ ) | 3 , 924.6 | 5 , 543.8 | 7 , 534.1 | 8 , 891.0 |

| Av e r a g e ca p ital e mp l o yed (NT $ ) | 3 , 457.9 | 4 , 430.7 | 6 , 140.3 | 7 , 651.2 |

| BVP S (NT $ ) | 77.10 | 85.60 | 108.51 | 134.16 |

Growth & Margins (%) ______________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| Total revenue growth | (3.0) | 7 2 .9 | 45.3 | 2 7.6 |

| EBITDA growth | 13. 2 | 94.4 | 6 2 .8 | 35.4 |

| EPS growth | 0.7 | 8 2 .5 | 56.9 | 33.5 |

| DPS growth | 0.7 | 8 2 .5 | 56.9 | 33.5 |

| EBIT margin | 30.0 | 34.1 | 38.4 | 40.8 |

| EBITDA margin | 31.3 | 35. 2 | 39.4 | 41.9 |

| Net income margin | 2 7.7 | 2 9.3 | 31.7 | 33.1 |

Price Performance __________________________________________

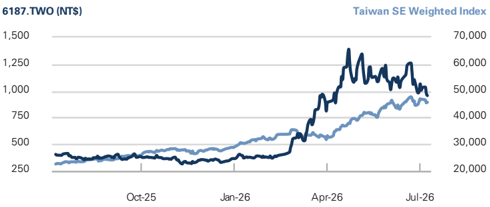

| 3m | 6m | 12m | |

|---|---|---|---|

| Absolute | (2.6)% | 1 43.0% | 1 40.9% |

| Rel. to the TaiwanSE Weighted Index | (25.9)% | 6 1 .3% | 1 7.8% |

Source: FactSet. Price as of 8 Jul 2026 close.

Income Statement (NT$ mn) ________________________________

| 12/25 | 12/26E | 12/27E | 12/28E | |

|---|---|---|---|---|

| To t a l r e v e nu e | 5,366 . 2 | 9,276 . 9 | 13,477 . 6 | 17,193 . 8 |

| Co s t of good s s old | (2,452 . 9) | (4,315 . 3) | (6,155 . 2) | (7,448 . 7) |

| SG&A | (535 . 8) | (961 . 9) | (986 . 2) | (1,271 . 3) |

| R&D | (766 . 8) | (835 . 2) | (1,161 . 9) | (1,460 . 3) |

| Other operating inc . /(exp . ) E BITDA | -- 1 , 67 9.3 | -- 3, 265 .4 | -- 5 ,3 16 .0 | -- 7 , 1 9 7 .3 |

| Depreciation& amortization | (68 . 5) | (100 . 9) | (141 . 7) | (183 . 7) |

| E BIT | 1 , 61 0. 8 | 3, 16 4. 5 | 5 , 17 4.3 | 7 ,0 1 3. 6 |

| Net intere s t inc . /(exp . ) | 40 . 0 | 37 . 2 | 39 . 7 | 39 . 6 |

| Income/(lo ss ) from a ss ociate s | (0 . 6) | -- 3, 28 3. 8 | -- 5 , 2 34.0 | -- 7 ,0 7 3. 2 |

| Pre-tax pro fi t Provi s ion for taxe s | 1 , 812 . 8 (316 . 4) | (570 . 0) | (968 . 3) | (1,379 . 3) |

| Minority intere s t | (11 . 2) | 4 . 6 | -- | -- |

| Preferred dividend s | -- | -- | -- | -- |

| N et inc . ( pre-ex c ept i o n a ls) | 1 ,4 85 . 2 | 2 , 718 .4 | 4, 265 . 7 | 5 , 6 93.9 |

| Po s t-tax exceptional s | -- | -- | -- | -- |

| N et inc . ( po s t-ex c ept i o n a ls) | 1 ,4 85 . 2 | 2 , 718 .4 | 4, 265 . 7 | 5 , 6 93.9 |

| E P S(b a sic , pre-ex c ept ) (N T $) | 15 .4 7 | 28 . 2 3 | 44.30 | 5 9. 1 3 |

| E P S(dilu te d , pre-ex c ept ) (N T $) | 15 .4 7 | 28 . 2 3 | 44.30 | 5 9. 1 3 |

| E P S(b a sic , po s t-ex c ept ) (N T $) | 15 .4 7 | 28 . 2 3 | 44.30 | 5 9. 1 3 |

| E P S(dilu te d , po s t-ex c ept ) (N T $) | 15 .4 7 | 28 . 2 3 | 44.30 | 5 9. 1 3 |

| DPS (NT$) | 11 . 56 | 21 . 11 | 33 . 12 | 44 . 21 |

| Div . payout ratio (%) | 74 . | 74 . | 74 . | 74 . 8 |

| Balance Sheet (NT$ mn) | 8 | 8 | 8 | ______ 12/28E |

| C a sh& c a sh equiv a lents | 12/25 4,182.0 | 12/26E 3,210.1 | 12/27E 3,594.4 | 4,925.2 2,660.4 |

| Accounts receiv a ble | 858.6 | 1,505.4 2,564.9 | 2,656.4 3,616.8 | 3,279.6 |

| Inventory Other current a ssets | 1,114.0 180.4 | 294.5 | 294.5 | 294.5 |

| Total current assets | 6 ,33 5 . 2 | 7 , 57 4. 9 | 1 0, 162 . 1 | 11 , 159 . 8 |

| Net PP&E | 1,878.7 | 2,797.9 | 3,840.9 | 4,848.9 |

| Net int a ngibles | 31.8 | 47.4 | 64.2 1,111.4 | 74.0 1,111.4 |

| Tot a l investments Other long-term a ssets | 986.8 | 1,111.4 431.0 | 431.0 | 431.0 |

| Total assets | 376.9 9 , 6 0 9 .4 | 11 , 962 . 6 | 15 , 6 0 9 . 6 | 17 , 625 . 1 |

| 1,292.4 | 2,799.2 | 4,173.3 | 3,644.8 | |

| Accounts p a y a ble | -- | -- | -- | |

| Short-term debt Short-term le a se li a bilities | -- -- | -- | -- | -- |

| Other current li a bilities Total current liabilities | 348.0 | 593.9 | 633.9 8 0 7 . 2 | 673.9 18 . 7 |

| 1 , 6 40.4 | 3,3 9 3. 1 | 4, | 4,3 | |

| Long-term debt | 339.2 | 132.8 | 132.8 -- | 132.8 -- |

| Long-term le a se li a bilities | -- | -- 143.4 | 143.4 | 143.4 |

| Other long-term li a bilities liabilities | 141.6 | 276 . 2 | 276 . 2 | |

| Total long-term Total liabilities | 4 8 0. 8 2 , 121 . 2 | 276 . 2 3, 669 .3 | 5 ,0 8 3.4 | 4, 59 4. 9 |

| Preferred sh a res | -- | -- 8,108.6 | -- 10,341.5 | -- 12,845.5 |

| Tot a l commonequity Minority interest | 7,299.0 189 . 2 | 18 4. 6 | 18 4. 6 | 18 4. 6 |

| Total liabilities &equity | 9 , 6 0 9 | , 962 . | 15 , 6 0 9 . 6 | , 625 . 1 |

| Net debt, a djusted | (3,842.8) | (3,077.2) | (3,461.6) | |

| .4 | 11 6 | 17 | ||

| (4,792.4) | ||||

| Cash Flow (NT$ mn) | 12/25 1,485.2 | 12/26E 2, 7 18.4 | 12/27E 4,265. 7 | __________ 12/28E 5,693.9 |

| Net income D&Aadd-back Minority interest | 68.5 11.2 | 100.9 (4.6) (590.9) | 141. 7 -- (828.8) | 183. 7 -- (195.3) |

| add-back Net (inc)/dec working capital | 28 7 .1 | -- | ||

| Other operating cash flow Cash flow fro m operations | 106.1 ,9 58 .0 | (1,054. 7 ) 1 , 16 9. 1 | -- 3, 578 . 6 | 5 , 682 .3 |

| 1 | ||||

| Capital expenditures | (512.9) (8 7 .8) | (1,010.0) | (1,161.5) -- | (1,161.5) -- |

| Acquisitions Divestitures | -- | -- -- | -- | -- |

| Others | (65.2) | -- | ||

| Cash flow fro m | ( 665 .9) | (45.3) ,0 55 .3) | -- , 161 . 5 ) | , 161 . 5 ) |

| investing | ( 1 | ( 1 | ( 1 | |

| Repayment of lease liabilities | -- | -- | -- | -- (3,189.9) |

| Dividends paid(common& pref) | (980.0) | (1,110.6) | (2,032.8) | -- |

| Inc/(dec) in debt flows | 142.1 | (2.0) | -- | |

| Other financing cash Cash flow fro m finan c ing | 191.3 6 4 6 . 5 ) | 26.9 | 0.0 ( 2 ,03 2 . 8 ) | 0.0 18 9.9) |

| Total c ash flow | ( 6 4 5 . 6 | ( 1 ,0 85 . 7 ) (9 72 .0) | 3 8 4.3 | (3, 1 ,330. 8 |

| Free cash flow | 1,445.2 | 159.0 | 2,41 7 .1 | 4,520.8 |

Source: Company data, Goldman Sachs Research estimates.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

expecting at least around 20% higher pricing, re fl ecting the higher complexity and performance of these next-generation systems. We continue to see CPO as the next key growth driver for All Ring, and we now model All Ring's CPO revenue to reach NT$2.1bn/NT$10.2bn, accounting for 16%/60% of revenue in 2027E/2028E (vs. 29%/69% previously).

Risk-reward now skewed to the upside

All Ring's shares have declined -31% from its recent peak in April (vs. TAIEX's +21%). We believe this weakness largely re fl ects a cluster of market concerns including potential CPO delay. However, we see All Ring's fundamental demand remaining solid across both CoWoS and CPO, and the company continues to lead peers on CPO equipment throughput. Given the improving near-term outlook, an accelerating advanced packaging build plan into 2027, and resilient long-term CPO demand, we view the risk-reward as skewed to the upside and reiterate our Buy rating. Accordingly, we adjust our 2026E-2028E earnings by +7%/-6%/-12% and revise our 12-month TP to NT$1,550 from NT$1,650 implying 62% upside.

Exhibit 1: All Ring's revenue growth outlook

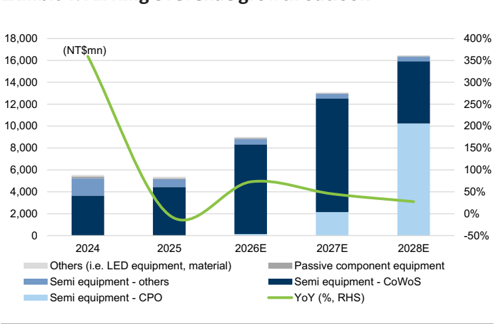

Source: Company data, Goldman Sachs Global Investment Research

Source: Company data, Goldman Sachs Global Investment Research

Earnings changes, valuation and risks

Forecast changes

We revise our 2026E-28E EPS by +7.2%/-6.0%/-11.6% mainly as we factor in 1) stronger 2Q26 revenue and GM assumptions, 2) accelerating CoWoS expansion in 2027E/2028E, but 3) lower CPO equipment units in 2027E/2028E.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 3: Earnings revisions

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| (NT$mn) | Old | New | Diff (%) | Old | New | Diff (%) | Old | New | Diff (%) |

| Revenue | 8,865 | 9,277 | 4.6% | 14,693 | 13,478 | -8.3% | 19,889 | 17,194 | -13.6% |

| Gross profit | 4,709 | 4,962 | 5.4% | 8,046 | 7,322 | -9.0% | 11,351 | 9,745 | -14.1% |

| Op. income | 2,923 | 3,164 | 8.3% | 5,460 | 5,174 | -5.2% | 7,893 | 7,014 | -11.1% |

| Net income | 2,536 | 2,718 | 7.2% | 4,538 | 4,266 | -6.0% | 6,441 | 5,694 | -11.6% |

| EPS (NT$) | 26.33 | 28.23 | 7.2% | 47.13 | 44.30 | -6.0% | 66.88 | 59.13 | -11.6% |

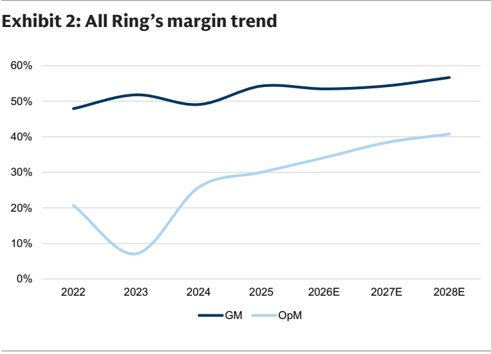

| GM | 53.1% | 53.5% | 0.4% | 54.8% | 54.3% | -0.4% | 57.1% | 56.7% | -0.4% |

| OpM | 33.0% | 34.1% | 1.1% | 37.2% | 38.4% | 1.2% | 39.7% | 40.8% | 1.1% |

| NM | 28.6% | 29.3% | 0.7% | 30.9% | 31.7% | 0.8% | 32.4% | 33.1% | 0.7% |

| 2Q26E | 2Q26E | 2Q26E | 3Q26E | 3Q26E | 3Q26E | 4Q26E | 4Q26E | 4Q26E | |

|---|---|---|---|---|---|---|---|---|---|

| (NT$mn) | Old | New | Diff (%) | Old | New | Diff (%) | Old | New | Diff (%) |

| Revenue | 2,087 | 2,355 | 12.8% | 2,799 | 3,038 | 8.6% | 2,568 | 2,472 | -3.7% |

| Gross profit | 1,092 | 1,272 | 16.5% | 1,478 | 1,655 | 12.0% | 1,408 | 1,304 | -7.4% |

| Op. income | 698 | 688 | -1.3% | 1,003 | 1,250 | 24.6% | 894 | 899 | 0.5% |

| Net income | 598 | 602 | 0.6% | 852 | 1,042 | 22.3% | 761 | 750 | -1.4% |

| EPS (NT$) | 6.21 | 6.25 | 0.6% | 8.85 | 10.82 | 22.3% | 7.90 | 7.79 | -1.4% |

| GM | 52.3% | 54.0% | 1.7% | 52.8% | 54.5% | 1.7% | 54.8% | 52.7% | -2.1% |

| OpM | 33.4% | 29.2% | -4.2% | 35.8% | 41.1% | 5.3% | 34.8% | 36.3% | 1.5% |

| NM | 28.7% | 25.6% | -3.1% | 30.4% | 34.3% | 3.8% | 29.6% | 30.3% | 0.7% |

Source: Company data, Goldman Sachs Global Investment Research

Maintain Buy with 12m TP revised to NT$1,550 from NT$1,650

Alongside our earnings revisions, we revise our 12-month TP to NT$1,550 (from NT$1,650 previously). Our 12-month TP is based on a target P/E multiple of 35x (unchanged; derived by applying the implied earnings growth uplift (per GSe) to the company's historical valuation framework) applied to our FY27E EPS. We view CPO as an even stronger structural tailwind for All Ring than CoWoS, with the potential to drive multiple-fold earnings expansion over the next several years, further supporting both earnings visibility and scope for valuation re-rating. Our new 12m TP implies 62% upside. We maintain our Buy rating on All Ring.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

Exhibit 4: All Ring's P&L overview

| 1Q26 | 2Q26E | 3Q26E | 4Q26E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| P&L | |||||||||||

| Revenue | 1,411 | 2,355 | 3,038 | 2,472 | 2,240 | 3,041 | 4,200 | 3,997 | 9,277 | 13,478 | 17,194 |

| Gross profit | 731 | 1,272 | 1,655 | 1,304 | 1,187 | 1,639 | 2,278 | 2,219 | 4,962 | 7,322 | 9,745 |

| Operating profit | 328 | 688 | 1,250 | 899 | 753 | 1,107 | 1,696 | 1,618 | 3,164 | 5,174 | 7,014 |

| Net income | 325 | 602 | 1,042 | 750 | 626 | 914 | 1,395 | 1,330 | 2,718 | 4,266 | 5,694 |

| EPS (NT$) | 3.37 | 6.25 | 10.82 | 7.79 | 6.50 | 9.50 | 14.48 | 13.82 | 28.23 | 44.30 | 59.13 |

| Margins (%) | |||||||||||

| GM | 51.8% | 54.0% | 54.5% | 52.7% | 53.0% | 53.9% | 54.3% | 55.5% | 53.5% | 54.3% | 56.7% |

| OpM | 23.2% | 29.2% | 41.1% | 36.3% | 33.6% | 36.4% | 40.4% | 40.5% | 34.1% | 38.4% | 40.8% |

| NM | 23.0% | 25.6% | 34.3% | 30.3% | 28.0% | 30.1% | 33.2% | 33.3% | 29.3% | 31.7% | 33.1% |

| YoY (%) | |||||||||||

| Revenue | 13.2% | 54.5% | 77.9% | 178.5% | 58.7% | 29.2% | 38.2% | 61.7% | 72.9% | 45.3% | 27.6% |

| Gross profit | -3.0% | 60.6% | 100.3% | 140.6% | 62.3% | 28.9% | 37.6% | 70.2% | 70.3% | 47.6% | 33.1% |

| Operating profit | -22.1% | 48.5% | 149.1% | 300.1% | 129.8% | 60.8% | 35.7% | 80.0% | 96.5% | 63.5% | 35.5% |

| Net income | -5.3% | 50.7% | 148.1% | 132.2% | 93.0% | 51.9% | 33.9% | 77.3% | 83.0% | 56.9% | 33.5% |

| EPS | -5.7% | 50.2% | 147.8% | 131.6% | 93.0% | 51.9% | 33.9% | 77.3% | 82.5% | 56.9% | 33.5% |

| QoQ (%) | |||||||||||

| Revenue | 59.0% | 66.8% | 29.0% | -18.6% | -9.4% | 35.8% | 38.1% | -4.8% | |||

| Gross profit | 34.9% | 74.0% | 30.2% | -21.2% | -9.0% | 38.1% | 39.0% | -2.6% | |||

| Operating profit | 45.9% | 110.0% | 81.5% | -28.1% | -16.2% | 46.9% | 53.2% | -4.6% | |||

| Net income | 0.4% | 85.5% | 73.1% | -28.0% | -16.5% | 46.0% | 52.5% | -4.6% | |||

| EPS | 0.2% | 85.5% | 73.1% | -28.0% | -16.5% | 46.0% | 52.5% | -4.6% |

Source: Company data, Goldman Sachs Global Investment Research

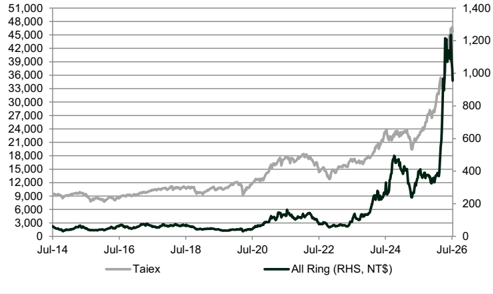

Exhibit 5: Taiex vs. All Ring

Source: TEJ

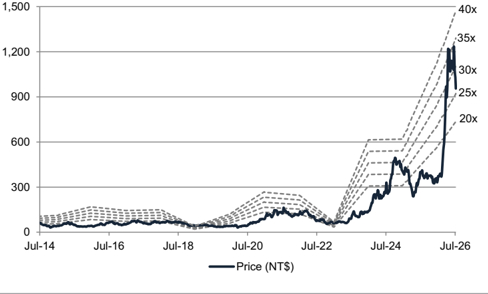

Exhibit 6: Forward P/E

Source: TEJ

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM

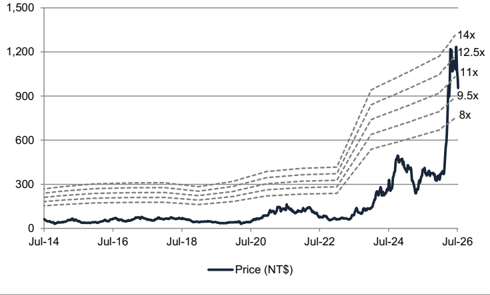

Exhibit 7: Forward P/B

Source: TEJ

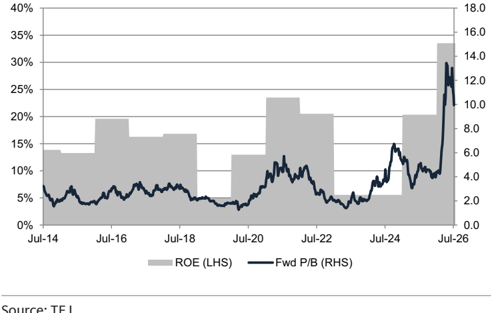

Exhibit 8: P/B vs. ROE

Source: TEJ

Investment Thesis - All Ring (6187.TWO)

All Ring is one of the key suppliers of semiconductor equipment in Taiwan, primarily utilized in back-end advanced packaging processes. The company manufactures under fi ll dispenser, TIM heat sink attach equipment, and automated optical inspection equipment which are widely adopted within the CoWoS process. All Ring currently has nearly 100% of market share in WoS under fi ll dispenser and TIM heatsink attach equipment, and its main customers include leading foundries and OSATs in Taiwan.

We like All Ring as we expect its revenue/earnings CAGR to further accelerate to 47%/56% in 2025-28E, driven by 1) continued advanced packaging capacity expansion, and 2) rapid growth of its CPO business. With All Ring's unique position in CPO coupling equipment and new packaging opportunity such as PLP, we see upside potential in its revenue and earnings growth and have a Buy rating on the name.

Price Target Risks and Methodology - All Ring (6187.TWO)

Valuation: We are Buy rated on All Ring. Our 12m TP of NT$1,550 is based on a target P/E multiple of 35x (derived from growth-adjusted historical valuation) applied to our FY27E EPS.

Key risks to our views: 1) slower advanced packaging expansion, 2) delay in adoption of new packaging technologies, and 3) intensifying competition.

e92c7a75ab8b4efbba794e6b187208c8

For the exclusive use of KEVINLU@LENOVO.COM