PDF 原檔:報告_Daiwa_富世達6805_20260707_original.pdf

圖片清單(已驗證 2026-07-08)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源。<40KB 未 Read(預設 logo/裝飾)。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Daiwa_富世達6805_20260707_001.png |

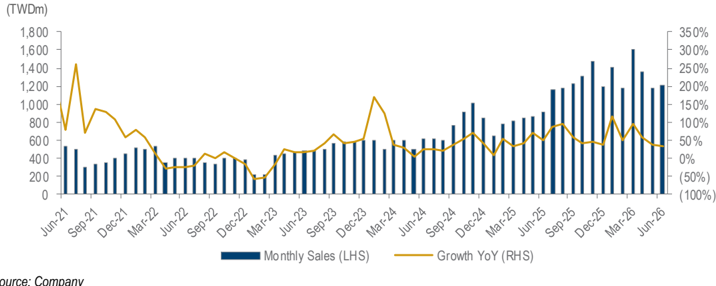

65KB | 真資料圖 | 富世達月營收長條圖(TWD mn)及 YoY 折線(%)——Jun-21 至 Jun-26,顯示 Jun-26 月營收 TWD1,206mn,YoY +32.7% |

原始內容

Fositek Corp (6805 TT)

Share price (7 Jul): TWD1,490.00

12-mth rating: Buy (1)

7 July 2026

Information Technology: Taiwan

2Q26 revenue missed due to weaker-than-expected foldable phone shipments

Helen Chien

(886) 2 8758 6254 helen.chien@daiwacm-cathay.com.tw

Neil Teng

(886) 2 8758 6256 neil.teng@daiwacm-cathay.com.tw

Summary: Fositek reported its monthly revenue in June 2026 of TWD1,206m (+2.2% MoM and +32.7% YoY; +62.6% YoY for 6M26) after market hours on 7 July 2026. Its 2Q26 revenue accounts for 87.9% and 88.1% of our and the consensus forecasts, respectively. We attribute the miss to weaker-than-expected foldable phone shipments.

We have a Buy (1) rating and 12-month TP of TWD2,600, based on a target PER of 33x applied to our one-year-forward EPS forecast. For more information on the company, please refer to our latest flash, Positive tone on the 2026-27 outlook , published on 1 June 2026.

What's the impact

- 2Q26 revenue missed due to weaker-than-expected foldable phone shipments. On 7 July, Fositek reported its monthly revenue in June 2026, which was TWD1,206m (+2.2% MoM and +32.7% YoY; +62.6% YoY for 6M26). Its 2Q26 revenue of TWD3,740m (-10.6% QoQ and +42.7% YoY) accounted for 87.9% and 88.1%, respectively, of our (TWD4,253m, +1.7% QoQ and +62.3% YoY) and the Bloomberg consensus forecasts for 2Q26 revenue. We attribute the miss to weaker-than-expected foldable phone shipments.

Fositek: consolidated monthly sales

Source: Company

- Positive tone from the company. For 3Q26 and 4Q26, Fositek guided for revenue to grow by double digits QoQ. We believe 2H26 revenue should be stronger than for 1H26, supported by more ASIC, VR, LPX and Vera CPU projects. For CPO, Fositek is sampling QDs for CSP and GPU clients, which is likely to contribute revenue in 2027, according to management. Apart from AVC, Fositek is also testing with other thermal solution vendors, as well as new segments such as the power rack.

What we recommend

We have a Buy (1) rating and 12-month TP of TWD2,600, based on a target PER of 33x applied to our one-year-forward EPS forecast. Based on our 2026/27E EPS, the stock is currently trading at PERs of 22.4x/15.2x, vs. its past-3-year trading range of 9-43x. Key downside risks: lower-than-expected market share for key clients, slower-than-expected penetration rate of foldable phones, and geopolitical risks.

In the interests of timeliness, this document has not been edited.