同一份 CLSA 報告的完整版

本份為螢幕截圖版 報告_CLSA-SinoPac_聯發科2454_20260522 的完整 PDF 版本——同一份 CLSA/SinoPac「No turning back」報告(報告日 2026-05-22;檔名 0523 為下載日)。完整財務(P&L/資產負債/現金流)、TPU 路線圖(Figure 1)、銷售結構(Figure 4)、估值橋(Figure 5)以本份為準。

PDF 原檔:報告_CLSA_聯發科2454_20260523_original.pdf

原始內容

22 May 2026

Taiwan

Technology

Reuters

2454.TW

Bloomberg

2454 TT

Priced on 22 May 2026

Taiwan Wtd @ 42,268.0

12M hi/lo

NT$3,880.00/1,145.00

12M price target

NT$5,922.00

±% potential

+53%

Shares in issue

1,589.7m

Free float (est.)

87.1%

Market cap

US$180.9bn

3M ADV

US$821.0m

Foreign s'holding

56.1%

Major shareholders

Vanguard Group 4.3% BlackRock Inc 3.9%

SinoPac analysts:

Astoria Chen, SinoPac astoria.chen@cl-sec.com

+886 223 268162

Stock performance (%)

Source: Bloomberg

MediaTek

NT$3,860.00 - HIGH CONVICTION OUTPERFORM

No turning back

Now at the centre of Google's TPU strategy

Recent TPU roadmap changes suggest Google is no longer treating MediaTek as merely an alternative supplier. Instead, it appears to be increasingly positioned at the centre of Google's next-generation TPU strategy, while Broadcom's role becomes more complementary. We believe the market is not yet fully reflecting this strategic shift, and after raising our 2028 EPS forecast by 38%, we are now 68% above consensus. We lift our TP from NT$4,500 to NT$5,922 and reiterate High Conviction Outperform.

Critical strategy changes in TPU v9 supply chains

Google recently cancelled Pumafish (Broadcom's original TPU v9) after the project had kicked off only around a month, and replaced it with a new one, Whalefish. Whalefish, is more like a version of 'Sunfish Ultra', which puts two Sunfish (TPU 8i) together. This implies Broadcom's v9 is likely to stay at 3nm with HBM3e, while MediaTek's v9 (Humufish, aka A5922) will migrate to 2nm with HBM4e.

No longer merely an alternative solution for Google

We believe Google's latest TPU strategy marks a meaningful shift in positioning between MediaTek and Broadcom. While MediaTek's project was previously viewed by the market as a secondary program with uncertain volume, we now see it increasingly becoming the core platform within Google's roadmap, with Broadcom's solution taking on a more backup or less strategic role. Reflecting this shift and our supply chain checks, we raise our 2028 Humufish shipment forecast to 2.4m units (from 1.6m) and increase our previously conservative ASP assumption to US$15k, leading to US$36bn revenue contribution, or 63% of total sales in 2028SP.

Potential inflection points in smartphone

Our checks suggest MediaTek is working on supplying modified D9500 for Samsung's Galaxy S27 FE. However, the project is still being verified by Samsung with fairly demanding requirements, and final market share will depend on the results. We currently do not factor in any Samsung contribution but see potential upside if the project enters mass production.

Earnings revisions and valuations

We raise our 2028 EPS forecast by 38% to reflect the higher TPU contribution, bringing our TP to a Street high of NT$5,922 (up from NT$4,500), still based on 30x 2H27-1H28SP PE. Reiterate High Conviction Outperform.

| Financials | |||||

|---|---|---|---|---|---|

| Year to 31 December Revenue (NT$m) | 24A 530,586 | 25A 595,966 | 26SP 637,567 | 27SP 1,057,400 | 28SP 1,850,099 |

| Rev forecast change (%) | - | - | (0.3) | (0.4) | 35.0 |

| Net profit (NT$m) | 106,387 | 105,319 | 102,356 | 213,139 | 444,796 |

| NP forecast change (%) | - | - | (0.3) | (0.3) | 38.0 |

| EPS (NT$) | 66.92 | 66.16 | 64.30 | 133.89 | 279.40 |

| SP/consensus (27) (EPS%) | - | - | 100 | 120 | 168 |

| EPS growth (% YoY) | 38.0 | (1.1) | (2.8) | 108.2 | 108.7 |

| PE (x) | 57.7 | 58.3 | 60.0 | 28.8 | 13.8 |

| Dividend yield (%) | 1.4 | 1.4 | 1.0 | 2.1 | 4.3 |

| ROE (%) | 31.3 | 29.3 | 27.0 | 45.9 | 63.6 |

| Net cash per share (NT$) | 120.84 | 140.72 | 131.66 | 204.46 | 351.40 |

Source: SinoPac

Financials at a glance

| Year to 31 December | 2024A | 2025A | 2026SP | (% YoY) | 2027SP | 2028SP |

|---|---|---|---|---|---|---|

| Profit & Loss (NT$m) | ||||||

| Revenue | 530,586 | 595,966 | 637,567 | 7 | 1,057,400 | 1,850,099 |

| Cogs (ex-D&A) | (246,264) | (289,911) | (320,110) | (564,002) | (1,034,498) | |

| Gross Profit (ex-D&A) | 284,322 | 306,054 | 317,458 | 3.7 | 493,399 | 815,600 |

| SG&A and other expenses | (160,974) | (179,610) | (190,707) | (229,429) | (260,490) | |

| Op Ebitda | 123,348 | 126,444 | 126,751 | 0.2 | 263,969 | 555,110 |

| Depreciation/amortisation | (20,936) | (22,974) | (25,701) | (34,603) | (50,280) | |

| Op Ebit | 102,412 | 103,470 | 101,050 | (2.3) | 229,366 | 504,830 |

| Net interest inc/(exp) | 10,696 | 10,167 | 10,561 | 3.9 | 11,000 | 11,000 |

| Other non-Op items | 6,410 | 11,251 | 8,118 | (27.8) | 8,400 | 8,400 |

| Profit before tax | 119,519 | 124,888 | 119,728 | (4.1) | 248,766 | 524,230 |

| Taxation | (12,378) | (18,770) | (16,549) | (34,827) | (78,635) | |

| Profit after tax | 107,141 | 106,118 | 103,179 | (2.8) | 213,939 | 445,596 |

| Minority interest | (754) | (798) | (822) | (800) | (800) | |

| Net profit | 106,387 | 105,319 | 102,356 | (2.8) | 213,139 | 444,796 |

| Adjusted profit | 106,387 | 105,319 | 102,356 | (2.8) | 213,139 | 444,796 |

| Cashflow (NT$m) | 2024A | 2025A | 2026SP | (% YoY) | 2027SP | 2028SP |

| Operating profit | 102,412 | 103,470 | 101,050 | (2.3) | 229,366 | 504,830 |

| Depreciation/amortisation | 20,936 | 22,974 | 25,701 | 11.9 | 34,603 | 50,280 |

| Working capital changes | 12,624 | 22,540 | (39,115) | (54,371) | (115,180) | |

| Other items | 20,082 | 13,808 | 370 | (97.3) | (17,427) | (61,235) |

| Net operating cashflow | 156,055 | 162,793 | 88,006 | (45.9) | 192,171 | 378,696 |

| Capital expenditure | (13,787) | (15,059) | (16,745) | (17,582) | (18,461) | |

| Free cashflow M&A/Others | 142,268 (22,141) | 147,734 (22,695) | 71,261 (1,000) | (51.8) | 174,589 (1,000) | 360,234 (1,000) |

| Net investing | (35,928) | (37,754) | (17,745) | (18,582) | ||

| cashflow Increase in loans | (1,260) | 60 | 4,000 | 6,566.7 | 4,000 | (19,461) 4,000 |

| Dividends | (87,551) | (86,070) | (85,169) | (61,414) | (127,883) | |

| Net equity raised/other | (1,309) | (1,665) | 350 | 350 | 350 | |

| Net financing cashflow | (90,119) | (87,675) | (80,819) | (57,064) | (123,533) | |

| Incr/(decr) in net cash | 30,008 | 37,364 | (10,558) | 116,525 | 235,701 | |

| Exch rate movements | 8,292 | (5,770) | 2,315 | 3,397 | 1,470 | |

| Balance sheet (NT$m) | 2024A | 2025A | 2026SP | (% YoY) | 2027SP | 2028SP |

| Cash & equivalents | 203,696 | 235,290 | 227,047 | (3.5) | 346,969 | 584,141 |

| Accounts receivable | 51,770 | 68,597 | 73,385 | 7 | 121,709 | 212,950 |

| Other current assets | 79,693 | 82,746 | 89,821 | 8.6 | 144,143 | 248,614 |

| Fixed assets | 56,917 | 60,427 | 60,159 | (0.4) | 62,660 | 64,146 |

| Investments | 186,915 | 191,058 | 198,284 | 3.8 | 198,798 | 199,573 |

| Intangible assets Other non-current assets | 82,257 | 80,262 25,404 | 80,262 | 0 | 80,262 32,890 | 80,262 31,647 |

| Total assets | 36,619 697,868 | 743,785 | 36,646 765,606 | 44.3 2.9 | 10,685 | 1,421,333 |

| Short-term debt | 8,919 | 4,481 | 8,655 | 93.2 | 987,430 | 11,940 |

| Accounts payable | 40,777 | 48,710 | 53,836 | 10.5 | 93,191 | 168,878 |

| Other current liabs | 217,207 | 250,159 | 217,587 | (13) | 228,317 | 232,021 |

| Long-term debt/CBs | 2,681 | 6,795 | 8,795 | 29.4 | 10,795 | 12,795 |

| Provisions/other LT liabs | 23,228 | 24,444 | 49,730 | 103.4 | 64,994 | 98,618 |

| Shareholder funds | 347,560 | 370,178 | 387,986 | 4.8 | 540,430 | 858,063 |

| Minorities/other equity | 57,495 | 39,017 | 39,017 | 0 | 39,017 | 39,017 |

| Total liabs & equity | 697,868 | 743,785 | 765,606 | 2.9 | 987,430 | 1,421,333 |

| Ratio analysis | 2024A | 2025A | 2026SP | (% YoY) | 2027SP | 2028SP |

| Revenue growth (% YoY) | 22.4 | 12.3 | 7.0 | 65.8 | 75.0 | |

| Ebitda margin (%) | 23.2 | 21.2 | 19.9 | 25.0 | 30.0 | |

| 19.3 | 17.4 | 15.8 | 21.7 | 27.3 | ||

| Ebit margin (%) Net profit growth (%) | 38.2 | (1.0) | (2.8) | 108.2 | 108.7 | |

| Op cashflow growth (% YoY) | (6.0) | 4.3 | (45.9) | 118.4 | 97.1 | |

| Capex/sales (%) | 2.6 | 2.5 | 2.6 (49.1) | 1.7 | 1.0 (62.4) | |

| Net debt/equity (%) (x) | (47.4) - | (54.7) - | - | (56.2) - | - | |

| Net debt/Ebitda ROE (%) | 31.3 | 29.3 | 27.0 | 45.9 | 63.6 | |

| ROIC (%) | 143.6 | 259.2 | 199.2 | 208.7 | 240.5 |

Source: SinoPac

Figure 1

| TPU roadmap | TPU roadmap | TPU roadmap | TPU roadmap | TPU roadmap | TPU roadmap |

|---|---|---|---|---|---|

| TPU | TPU 8t | TPU 8i | TPU 9t? | TPU 9i? | TPU 9i? |

| Code name | Zebrafish (A5921) | Sunfish | Humufish (A5922) | Pumafish (Cancelled) | Whalefish (Sunfish Ultra?) |

| Design Service | Google + MediaTek | Broadcom | Google + MediaTek | Broadcom | Broadcom |

| Compute die | N3*1 | N3*2 | N2*4 | N2? | N3*4 |

| Other logic die | na | na | N3*4 | TBD | na |

| I/O die | N4*1 | N4*1 | N3*4 | N3? | N4*2? |

| HBM | HBM3e *6 | HBM3e *8 | HBM4e *12 | HBM4/4e | HBM3e *16 |

| Packaging | CoWoS-S | CoWoS-L | EMIB-T | CoWoS-L | CoWoS-L |

| MP schedule | 4Q26 | 2H26 | 4Q27/1Q28 | Cancelled | 2027? |

Source: SinoPac

Figure 2

| Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L | Quarterly P&L |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (NT$m) | 1Q26 | 2Q26SP | 3Q26SP | 4Q26SP | 1Q27SP | 2Q27SP | 3Q27SP | 4Q27SP | 2025 | 2026SP | 2027SP | 2028SP |

| Sales | 149,151 | 145,022 | 136,826 | 206,569 | 238,457 | 278,966 | 283,626 | 256,351 | 595,966 | 637,567 | 1,057,400 | 1,850,099 |

| Gross profit | 69,055 | 66,737 | 63,008 | 92,956 | 106,369 | 119,733 | 121,746 | 110,946 | 283,080 | 291,757 | 458,795 | 765,321 |

| Opex | 46,165 | 45,682 | 45,153 | 53,708 | 52,461 | 58,583 | 58,143 | 60,242 | 179,610 | 190,707 | 229,429 | 260,490 |

| Operating profit | 22,891 | 21,056 | 17,855 | 39,248 | 53,909 | 61,150 | 63,603 | 50,704 | 103,470 | 101,050 | 229,366 | 504,830 |

| Non-OP | 4,129 | 4,850 | 4,850 | 4,850 | 4,850 | 4,850 | 4,850 | 4,850 | 21,418 | 18,679 | 19,400 | 19,400 |

| Pretax profit | 27,019 | 25,906 | 22,705 | 44,098 | 58,759 | 66,000 | 68,453 | 55,554 | 124,888 | 119,728 | 248,766 | 524,230 |

| Net profit | 24,154 | 21,820 | 19,099 | 37,283 | 50,333 | 56,560 | 58,670 | 47,576 | 105,319 | 102,356 | 213,139 | 444,796 |

| EPS (NT$) | 15.17 | 13.71 | 12.00 | 23.42 | 31.62 | 35.53 | 36.85 | 29.89 | 66.16 | 64.30 | 133.89 | 279.40 |

| Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth | Growth |

| Sales QoQ | (1%) | (3%) | (6%) | 51% | 15% | 17% | 2% | (10%) | ||||

| Sales YoY | (3%) | (4%) | (4%) | 38% | 60% | 92% | 107% | 24% | 12% | 7% | 66% | 75% |

| EPS QoQ | 5% | (10%) | (12%) | 95% | 35% | 12% | 4% | (19%) | ||||

| EPS YoY | (18%) | (22%) | (24%) | 63% | 108% | 159% | 207% | 28% | (1%) | (3%) | 108% | 109% |

| Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin |

| Gross margin | 46.3% | 46.0% | 46.0% | 45.0% | 44.6% | 42.9% | 42.9% | 43.3% | 47.5% | 45.8% | 43.4% | 41.4% |

| Opex | 31.0% | 31.5% | 33.0% | 26.0% | 22.0% | 21.0% | 20.5% | 23.5% | 30.1% | 29.9% | 21.7% | 14.1% |

| OP margin | 15.3% | 14.5% | 13.0% | 19.0% | 22.6% | 21.9% | 22.4% | 19.8% | 17.4% | 15.8% | 21.7% | 27.3% |

| Non-OP | 2.8% | 3.3% | 3.5% | 2.3% | 2.0% | 1.7% | 1.7% | 1.9% | 3.6% | 2.9% | 1.8% | 1.0% |

| Net margin | 16.2% | 15.0% | 14.0% | 18.0% | 21.1% | 20.3% | 20.7% | 18.6% | 17.7% | 16.1% | 20.2% | 24.0% |

Source: SinoPac

Figure 3

Forecast revisions

| 2026SP | 2026SP | 2027SP | 2027SP | 2027SP | 2028SP | 2028SP | 2028SP | ||

|---|---|---|---|---|---|---|---|---|---|

| (NT$m) | old | new | % ch | old | new | % ch | old | new | % ch |

| Revenue | 639,783 | 637,567 | 0% | 1,061,356 | 1,057,400 | 0% | 1,370,919 | 1,850,099 | 35% |

| Gross profit | 292,753 | 291,757 | 0% | 460,717 | 458,795 | 0% | 606,122 | 765,321 | 26% |

| Opex | 191,283 | 190,707 | 0% | 230,618 | 229,429 | (1%) | 249,891 | 260,490 | 4% |

| Operating profit | 101,470 | 101,050 | 0% | 230,100 | 229,366 | 0% | 356,231 | 504,830 | 42% |

| Pretax profit | 120,149 | 119,728 | 0% | 249,500 | 248,766 | 0% | 375,631 | 524,230 | 40% |

| Tax expense | 16,612 | 16,549 | 0% | 34,930 | 34,827 | 0% | 52,588 | 78,635 | 50% |

| Net profit | 102,714 | 102,356 | 0% | 213,770 | 213,139 | 0% | 322,243 | 444,796 | 38% |

| EPS (NT$) | 64.52 | 64.30 | 0% | 134.28 | 133.89 | 0% | 202.42 | 279.40 | 38% |

| Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin | Margin |

| Gross margin | 45.8% | 45.8% | 43.4% | 43.4% | 44.2% | 41.4% | |||

| Operating margin | 15.9% | 15.8% | 21.7% | 21.7% | 26.0% | 27.3% | |||

| Tax rate | 13.8% | 13.8% | 14.0% | 14.0% | 14.0% | 15.0% | |||

| Net margin | 16.1% | 16.1% | 20.1% | 20.2% | 23.5% | 24.0% |

Source: SinoPac

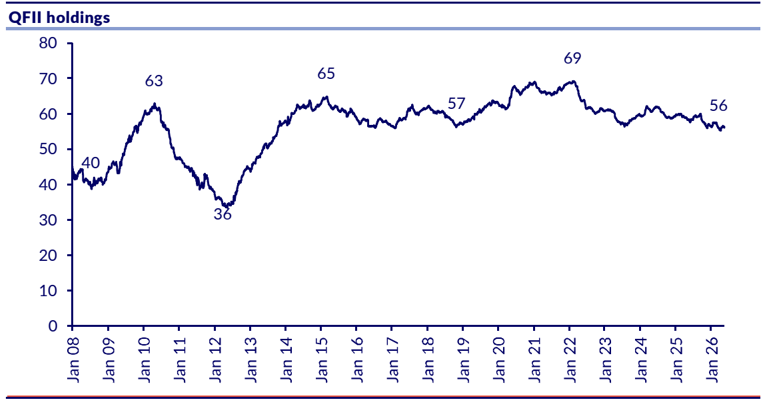

Foreign investors hold 56%

Figure 4

| Sales mix assumptions | ||||

|---|---|---|---|---|

| Sales (NT$m) | 2025 | 2026SP | 2027SP | 2028SP |

| Mobile phone | 328,429 | 265,168 | 268,267 | 300,670 |

| Smart edge platforms | 238,642 | 345,136 | 766,170 | 1,525,504 |

| Power IC & Others | 28,895 | 27,263 | 22,964 | 23,925 |

| Total | 595,966 | 637,567 | 1,057,400 | 1,850,099 |

| YoY | 2025 | 2026SP | 2027SP | 2028SP |

| Mobile phone | 8% | (19%) | 1% | 12% |

| Smart edge platforms | 21% | 45% | 122% | 99% |

| Power IC & Others | (5%) | (6%) | (16%) | 4% |

| Total | 12% | 7% | 66% | 75% |

| Sales mix | 2025 | 2026SP | 2027SP | 2028SP |

| Mobile phone | 55% | 42% | 25% | 16% |

| Smart edge platforms | 40% | 54% | 72% | 82% |

| Power IC & Others | 5% | 4% | 2% | 1% |

| Total | 100% | 100% | 100% | 100% |

Source: SinoPac

Figure 5

| Target price change | (x) | Valuation period | EPS (NT$) | Target Price (NT$) |

|---|---|---|---|---|

| Old | 30 | 2H27-1H28SP | 151.46 | 4,500 |

| New | 30 | 2H27-1H28SP | 197.06 | 5,922 |

Source: SinoPac

Figure 6

Source: SinoPac

Source: SinoPac

Investment thesis

We are seeing greater visibility into MediaTek's TPU business, with Google asking it to pull forward the schedule. Lukewarm smartphone demand and sustained margin pressure are likely to remain key near-term drags, and we believe the market could react negatively if China's weekly sell-out data shows a disappointing trend at the beginning of 2026, which is likely to create an entry point. However, we expect investor focus to increasingly shift towards the company's long-term opportunity in AI semiconductors, and we view the current valuation as undemanding compared with ASIC peers (trading at 30-55x).

Catalysts

1) Higher-than-expected GPM, 2) market share gain in the high-end smartphone segment, 3) smoother verification process for TPUs.

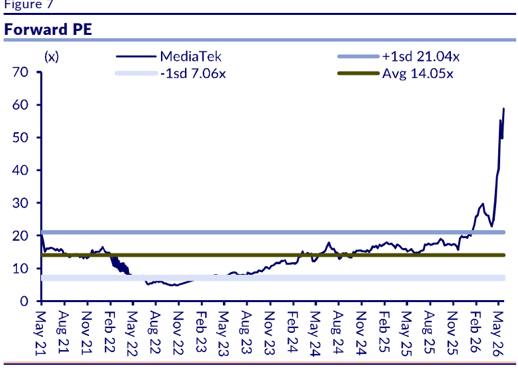

Valuation details

We use PE as our valuation methodology as IC design fabless companies typically deliver higher growth, and we believe the market will focus primarily on its earnings outlook. We have previously used a historical PE range to value MediaTek based on our evaluation of the company's product cycle at the time. Our valuation is about +2sd of its five-year average to reflect robust EPS growth driven by better smart edge business and higher TPU forecasts.

Investment risks

1) Worse-than-expected smartphone demand globally; 2) a greater-than-expected impact from share loss in the smartphone SoC market; 3) higher wafer prices.

Detailed financials

| Profit & Loss (NT$m) | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Revenue | 548,796 | 433,446 | 530,586 | 595,966 | 637,567 | 1,057,400 | 1,850,099 |

| Cogs (ex-D&A) | (262,912) | (207,879) | (246,264) | (289,911) | (320,110) | (564,002) | (1,034,498) |

| Gross Profit (ex-D&A) | 285,884 | 225,567 | 284,322 | 306,054 | 317,458 | 493,399 | 815,600 |

| Research & development costs | (116,875) | (111,385) | (131,993) | (148,306) | (158,315) | (190,426) | (216,207) |

| Selling & marketing expenses | (14,240) | (14,424) | (17,090) | (20,448) | (19,469) | (22,943) | (26,049) |

| Other SG&A | (13,002) | (9,759) | (11,891) | (10,856) | (12,923) | (16,060) | (18,234) |

| Other Op Expenses ex-D&A | - | - | 0 | 0 | - | - | - |

| Op Ebitda | 141,768 | 90,000 | 123,348 | 126,444 | 126,751 | 263,969 | 555,110 |

| Depreciation/amortisation | (14,980) | (18,200) | (20,936) | (22,974) | (25,701) | (34,603) | (50,280) |

| Op Ebit | 126,788 | 71,800 | 102,412 | 103,470 | 101,050 | 229,366 | 504,830 |

| Interest income | 3,218 | 7,308 | 11,150 | 10,819 | 11,396 | 12,000 | 12,000 |

| Interest expense | (371) | (399) | (453) | (652) | (836) | (1,000) | (1,000) |

| Net interest inc/(exp) | 2,847 | 6,908 | 10,696 | 10,167 | 10,561 | 11,000 | 11,000 |

| Associates/investments | 6,061 | 7,763 | 7,573 | 5,804 | 7,296 | 8,000 | 8,000 |

| Forex/other income | (728) | (186) | (1,551) | 664 | (84) | 0 | 0 |

| Asset sales/other cash items | - | - | - | 0 | - | 0 | 0 |

| Provisions/other non-cash items | 592 | 497 | 463 | 4,782 | 906 | 400 | 400 |

| Asset revaluation/Exceptional items | - | - | (74) | - | - | - | - |

| Profit before tax | 135,561 | 86,782 | 119,519 | 124,888 | 119,728 | 248,766 | 524,230 |

| Taxation | (16,936) | (9,591) | (12,378) | (18,770) | (16,549) | (34,827) | (78,635) |

| Profit after tax | 118,625 | 77,191 | 107,141 | 106,118 | 103,179 | 213,939 | 445,596 |

| Preference dividends | - | - | - | - | - | - | - |

| Profit for period | 118,625 | 77,191 | 107,141 | 106,118 | 103,179 | 213,939 | 445,596 |

| Minority interest | (484) | (212) | (754) | (798) | (822) | (800) | (800) |

| Net profit | 118,141 | 76,979 | 106,387 | 105,319 | 102,356 | 213,139 | 444,796 |

| Extraordinaries/others | 0 | 0 | 0 | 0 | 0 | ||

| Profit avail to ordinary shares | 118,141 | 0 | 0 | 213,139 | |||

| Dividends | (116,141) | 76,979 | 106,387 (87,551) | 105,319 (86,070) | 102,356 (85,169) | (61,414) | 444,796 |

| Retained profit | 2,000 | (120,981) (44,003) | 18,836 | 19,250 | 17,187 | 151,725 | (127,883) 316,913 |

| Adjusted profit | 118,141 | 76,979 | 106,387 | 105,319 | 102,356 | 213,139 | 444,796 |

| (NT$) | 74.6 | 66.9 | 66.2 | 64.3 | 279.4 | ||

| EPS | 48.5 | 133.9 | |||||

| Core EPS (NT$) | 74.6 | 48.5 | 66.9 | 66.2 | 279.4 | ||

| 64.3 | 133.9 | ||||||

| DPS (NT$) | 76.0 | 55.0 | 54.0 | 53.5 | 38.6 | 80.3 | 167.6 |

Profit & loss ratios

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Growth (%) | |||||||

| Revenue growth (% YoY) | 11.2 | (21.0) | 22.4 | 12.3 | 7.0 | 65.8 | 75.0 |

| Ebitda growth (% YoY) | 19.5 | (36.5) | 37.1 | 2.5 | 0.2 | 108.3 | 110.3 |

| Ebit growth (% YoY) | 17.4 | (43.4) | 42.6 | 1.0 | (2.3) | 127.0 | 120.1 |

| Net profit growth (%) | 6.0 | (34.8) | 38.2 | (1.0) | (2.8) | 108.2 | 108.7 |

| EPS growth (% YoY) | 5.7 | (35.0) | 38.0 | (1.1) | (2.8) | 108.2 | 108.7 |

| Adj EPS growth (% YoY) | 5.7 | (35.0) | 38.0 | (1.1) | (2.8) | 108.2 | 108.7 |

| DPS growth (% YoY) | 4.1 | (27.6) | (1.8) | (0.9) | (27.9) | 108.2 | 108.7 |

| Core EPS growth (% YoY) | 5.7 | (35.0) | 38.0 | (1.1) | (2.8) | 108.2 | 108.7 |

| Margins (%) | |||||||

| Gross margin (%) | 52.1 | 52.0 | 53.6 | 51.4 | 49.8 | 46.7 | 44.1 |

| Ebitda margin (%) | 25.8 | 20.8 | 23.2 | 21.2 | 19.9 | 25.0 | 30.0 |

| Ebit margin (%) | 23.1 | 16.6 | 19.3 | 17.4 | 15.8 | 21.7 | 27.3 |

| Net profit margin (%) | 21.5 | 17.8 | 20.1 | 17.7 | 16.1 | 20.2 | 24.0 |

| Core profit margin | 21.5 | 17.8 | 20.1 | 17.7 | 16.1 | 20.2 | 24.0 |

| Op cashflow margin | 26.3 | 38.3 | 29.4 | 27.3 | 13.8 | 18.2 | 20.5 |

| Returns (%) | |||||||

| ROE (%) | 29.9 | 20.7 | 31.3 | 29.3 | 27.0 | 45.9 | 63.6 |

| ROA (%) | 17.5 | 10.3 | 13.8 | 12.2 | 11.5 | 22.5 | 35.6 |

| ROIC (%) | 59.7 | 47.8 | 143.6 | 259.2 | 199.2 | 208.7 | 240.5 |

| ROCE (%) | 42.0 | 27.9 | 49.6 | 55.7 | 53.0 | 102.3 | 177.8 |

| Other key ratios (%) | |||||||

| Effective tax rate (%) | 12.5 | 11.1 | 10.4 | 15.0 | 13.8 | 14.0 | 15.0 |

| Ebitda/net int exp (x) | - | - | - | - | - | - | - |

| Exceptional or extraord. inc/PBT (%) | - | - | - | - | - | - | - |

| Dividend payout (%) | 101.9 | 113.4 | 80.7 | 80.9 | 60.0 | 60.0 | 60.0 |

Source: SinoPac

Balance sheet (NT$m)

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Cash & equivalents | 147,502 | 165,396 | 203,696 | 235,290 | 227,047 | 346,969 | 584,141 |

| Accounts receivable | 56,666 | 60,641 | 51,770 | 68,597 | 73,385 | 121,709 | 212,950 |

| Inventories | 70,703 | 43,220 | 58,414 | 67,235 | 74,310 | 128,631 | 233,103 |

| Other current assets | 18,643 | 16,438 | 21,279 | 15,512 | 15,512 | 15,512 | 15,512 |

| Current assets | 293,515 | 285,695 | 335,160 | 386,633 | 390,254 | 612,821 | 1,045,705 |

| Fixed assets | 53,862 | 53,291 | 56,917 | 60,427 | 60,159 | 62,660 | 64,146 |

| Investments | 137,087 | 166,892 | 186,915 | 191,058 | 198,284 | 198,798 | 199,573 |

| Goodwill | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other intangible assets | 73,455 | 81,245 | 82,257 | 80,262 | 80,262 | 80,262 | 80,262 |

| Other non-current assets | 50,481 | 47,916 | 36,619 | 25,404 | 36,646 | 32,890 | 31,647 |

| Total assets | 608,399 | 635,038 | 697,868 | 743,785 | 765,606 | 987,430 | 1,421,333 |

| Short term loans/OD | 6,569 | 7,826 | 8,919 | 4,481 | 8,655 | 10,685 | 11,940 |

| Accounts payable | 21,518 | 38,779 | 40,777 | 48,710 | 53,836 | 93,191 | 168,878 |

| Accrued expenses | - | - | - | - | - | - | - |

| Taxes payable | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Other current liabs | 113,484 | 185,394 | 217,207 | 250,159 | 217,587 | 228,317 | 232,021 |

| Current liabilities | 141,570 | 231,999 | 266,902 | 303,350 | 280,078 | 332,193 | 412,839 |

| Long-term debt/leases/other | 863 | 4,605 | 2,681 | 6,795 | 8,795 | 10,795 | 12,795 |

| Convertible bonds | - | - | - | - | - | - | - |

| Provisions/other LT liabs | 22,907 | 24,229 | 23,228 | 24,444 | 49,730 | 64,994 | 98,618 |

| Total liabilities | 165,341 | 260,833 | 292,812 | 334,590 | 338,603 | 407,982 | 524,253 |

| Share capital | 15,994 | 15,996 | 16,017 | 16,039 | 15,919 | 15,919 | 15,919 |

| Retained earnings | 286,689 | 212,670 | 210,599 | 219,519 | 227,211 | 358,342 | 631,495 |

| Reserves/others | 109,244 | 104,133 | 120,945 | 134,620 | 144,855 | 166,169 | 210,649 |

| Shareholder funds | 411,927 | 332,800 | 347,560 | 370,178 | 387,986 | 540,430 | 858,063 |

| Minorities/other equity | 31,131 | 41,406 | 57,495 | 39,017 | 39,017 | 39,017 | 39,017 |

| Total equity | 443,058 | 374,205 | 405,055 | 409,195 | 427,003 | 579,448 | 897,080 |

| Total liabs & equity | 608,399 | 635,038 | 697,868 | 743,785 | 765,606 | 987,430 | 1,421,333 |

| Total debt | 7,432 | 12,431 | 11,600 | 11,276 | 17,451 | 21,481 | 24,736 |

| Net debt | (140,070) | (152,965) | (192,095) | (224,014) | (209,596) | (325,489) | (559,405) |

| Adjusted EV | 5,866,898 | 5,846,063 | 5,812,295 | 5,763,403 | 5,773,244 | 5,656,121 | 5,421,024 |

| BVPS (NT$) | 260.1 | 209.7 | 218.6 | 232.5 | 243.7 | 339.5 | 539.0 |

Balance sheet ratios

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Key ratios | |||||||

| Current ratio (x) | 2.1 | 1.2 | 1.3 | 1.3 | 1.4 | 1.8 | 2.5 |

| Growth in total assets (% YoY) | (7.9) | 4.4 | 9.9 | 6.6 | 2.9 | 29.0 | 43.9 |

| Growth in capital employed (% YoY) | (1.9) | (27.7) | (8.8) | (11.5) | 18.6 | 16.8 | 35.1 |

| Net debt to operating cashflow (x) | - | - | - | - | - | - | - |

| Gross debt to operating cashflow (x) | 0.1 | 0.1 | 0.1 | 0.1 | 0.2 | 0.1 | 0.1 |

| Gross debt to Ebitda (x) | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.1 | 0.0 |

| Net debt/Ebitda (x) | - | - | - | - | - | - | - |

| Gearing | |||||||

| Net debt/equity (%) | (31.6) | (40.9) | (47.4) | (54.7) | (49.1) | (56.2) | (62.4) |

| Gross debt/equity (%) | 1.7 | 3.3 | 2.9 | 2.8 | 4.1 | 3.7 | 2.8 |

| Interest cover (x) | 350.5 | 198.1 | 250.5 | 175.3 | 134.5 | 241.4 | 516.8 |

| Debt cover (x) | 19.5 | 13.4 | 13.5 | 14.4 | 5.0 | 8.9 | 15.3 |

| Net cash per share (NT$) | 88.4 | 96.4 | 120.8 | 140.7 | 131.7 | 204.5 | 351.4 |

| Working capital analysis | |||||||

| Inventory days | 94.6 | 92.0 | 69.4 | 73.3 | 74.7 | 61.9 | 60.9 |

| Debtor days | 40.7 | 49.4 | 38.7 | 36.9 | 40.6 | 33.7 | 33.0 |

| Creditor days | 42.7 | 48.7 | 54.3 | 52.2 | 54.1 | 44.8 | 44.1 |

| Working capital/Sales (%) | 2.0 | (24.0) | (23.8) | (24.8) | (17.0) | (5.3) | 3.3 |

| Capital employed analysis | |||||||

| Sales/Capital employed (%) | 183.6 | 200.6 | 269.2 | 341.8 | 308.3 | 437.8 | 566.9 |

| EV/Capital employed (%) | 1,963.2 | 2,705.9 | 2,949.0 | 3,305.5 | 2,792.0 | 2,341.9 | 1,661.0 |

| Working capital/Capital employed (%) | 3.7 | (48.1) | (64.2) | (84.6) | (52.3) | (23.0) | 18.6 |

| Fixed capital/Capital employed (%) | 18.0 | 24.7 | 28.9 | 34.7 | 29.1 | 25.9 | 19.7 |

| Other ratios (%) | |||||||

| PB (x) | 14.8 | 18.4 | 17.7 | 16.6 | 15.8 | 11.4 | 7.2 |

| EV/Ebitda (x) | 41.4 | 65.0 | 47.1 | 45.6 | 45.5 | 21.4 | 9.8 |

| EV/OCF (x) | 40.6 | 35.2 | 37.2 | 35.4 | 65.6 | 29.4 | 14.3 |

| EV/FCF (x) | 44.8 | 37.3 | 40.9 | 39.0 | 81.0 | 32.4 | 15.0 |

| EV/Sales (x) | 10.7 | 13.5 | 11.0 | 9.7 | 9.1 | 5.3 | 2.9 |

| Capex/depreciation (%) | 146.8 | 84.8 | 109.8 | 112.9 | 116.6 | 111.3 | 106.2 |

Source: SinoPac

Cashflow (NT$m)

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Operating profit | 126,788 | 71,800 | 102,412 | 103,470 | 101,050 | 229,366 | 504,830 |

| Operating adjustments | (8,163) | 5,391 | 4,729 | 2,648 | 2,129 | (15,427) | (59,235) |

| Depreciation/amortisation | 14,980 | 18,200 | 20,936 | 22,974 | 25,701 | 34,603 | 50,280 |

| Working capital changes | (11,886) | 111,800 | 12,624 | 22,540 | (39,115) | (54,371) | (115,180) |

| Interest paid / other financial expenses | (3,281) | (6,471) | (3,938) | (5,994) | (3,759) | (4,000) | (4,000) |

| Tax paid | - | - | - | - | - | - | - |

| Other non-cash operating items | 26,145 | (34,628) | 19,292 | 17,154 | 2,000 | 2,000 | 2,000 |

| Net operating cashflow | 144,583 | 166,091 | 156,055 | 162,793 | 88,006 | 192,171 | 378,696 |

| Capital expenditure | (13,622) | (9,325) | (13,787) | (15,059) | (16,745) | (17,582) | (18,461) |

| Free cashflow | 130,961 | 156,767 | 142,268 | 147,734 | 71,261 | 174,589 | 360,234 |

| Acq/inv/disposals | (18,783) | (35,885) | (23,387) | (23,169) | - | - | - |

| Int, invt & associate div | (5,129) | 16,464 | 1,246 | 475 | (1,000) | (1,000) | (1,000) |

| Net investing cashflow | (37,535) | (28,746) | (35,928) | (37,754) | (17,745) | (18,582) | (19,461) |

| Increase in loans | (48,575) | (2,328) | (1,260) | 60 | 4,000 | 4,000 | 4,000 |

| Dividends | (116,141) | (120,981) | (87,551) | (86,070) | (85,169) | (61,414) | (127,883) |

| Net equity raised/others | 8,435 | 4,740 | (1,309) | (1,665) | 350 | 350 | 350 |

| Net financing cashflow | (156,280) | (118,569) | (90,119) | (87,675) | (80,819) | (57,064) | (123,533) |

| Incr/(decr) in net cash | (49,232) | 18,776 | 30,008 | 37,364 | (10,558) | 116,525 | 235,701 |

| Exch rate movements | 13,030 | (883) | 8,292 | (5,770) | 2,315 | 3,397 | 1,470 |

| Opening cash | 183,705 | 147,502 | 165,396 | 203,696 | 235,290 | 227,047 | 346,969 |

| Closing cash | 147,502 | 165,396 | 203,696 | 235,290 | 227,047 | 346,969 | 584,141 |

| OCF PS (NT$) | 91.3 | 104.7 | 98.2 | 102.3 | 55.3 | 120.7 | 237.9 |

| FCF PS (NT$) | 82.7 | 98.8 | 89.5 | 92.8 | 44.8 | 109.7 | 226.3 |

Cashflow ratio analysis

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Growth (%) | |||||||

| Op cashflow growth (% YoY) | 207.0 | 14.9 | (6.0) | 4.3 | (45.9) | 118.4 | 97.1 |

| FCF growth (% YoY) | 334.9 | 19.7 | (9.2) | 3.8 | (51.8) | 145.0 | 106.3 |

| Capex growth (%) | (19.8) | (31.5) | 47.8 | 9.2 | 11.2 | 5.0 | 5.0 |

| Other key ratios (%) | |||||||

| Capex/sales (%) | 2.5 | 2.2 | 2.6 | 2.5 | 2.6 | 1.7 | 1.0 |

| Capex/op cashflow (%) | 9.4 | 5.6 | 8.8 | 9.3 | 19.0 | 9.1 | 4.9 |

| Operating cashflow payout ratio (%) | 83.3 | 52.6 | 55.0 | 52.3 | 69.8 | 66.5 | 70.5 |

| Cashflow payout ratio (%) | 80.3 | 72.8 | 56.1 | 52.9 | 96.8 | 32.0 | 33.8 |

| Free cashflow payout ratio (%) | 88.7 | 77.2 | 61.5 | 58.3 | 119.5 | 35.2 | 35.5 |

DuPont analysis

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Ebit margin (%) | 23.1 | 16.6 | 19.3 | 17.4 | 15.8 | 21.7 | 27.3 |

| Asset turnover (x) | 0.9 | 0.7 | 0.8 | 0.8 | 0.8 | 1.2 | 1.5 |

| Interest burden (x) | 1.1 | 1.2 | 1.2 | 1.2 | 1.2 | 1.1 | 1 |

| Tax burden (x) | 0.9 | 0.9 | 0.9 | 0.8 | 0.9 | 0.9 | 0.9 |

| Return on assets (%) | 17.5 | 10.3 | 13.8 | 12.2 | 11.5 | 22.5 | 35.6 |

| Leverage (x) | 1.4 | 1.5 | 1.7 | 1.8 | 1.8 | 1.7 | 1.6 |

| ROE (%) | 29.9 | 20.7 | 31.3 | 29.3 | 27 | 45.9 | 63.6 |

EVA ® analysis

| Year to 31 December | 2022A | 2023A | 2024A | 2025A | 2026SP | 2027SP | 2028SP |

|---|---|---|---|---|---|---|---|

| Ebit adj for tax | 110,948 | 63,864 | 91,806 | 87,919 | 87,082 | 197,255 | 429,106 |

| Average invested capital | 185,847 | 133,693 | 63,926 | 33,920 | 43,710 | 94,504 | 178,438 |

| ROIC (%) | 59.7 | 47.8 | 143.6 | 259.2 | 199.2 | 208.7 | 240.5 |

| Cost of equity (%) | 9.4 | 9.4 | 9.4 | 9.4 | 9.4 | 9.4 | 9.4 |

| Cost of debt (adj for tax) | 1.4 | 1.4 | 1.4 | 1.3 | 1.4 | 1.4 | 1.3 |

| Weighted average cost of capital (%) | 9.3 | 9.3 | 9.3 | 9.3 | 9.3 | 9.3 | 9.3 |

| EVA/IC (%) | 50.4 | 38.5 | 134.3 | 249.9 | 190.0 | 199.5 | 231.2 |

| EVA (NT$m) | 93,716 | 51,467 | 85,878 | 84,774 | 83,030 | 188,493 | 412,562 |

Source: SinoPac

Research subscriptions

To change your report distribution requirements, please contact your CLSA sales representative or email us at cib@clsa.com. You can also fine-tune your Research Alert email preferences at https:/ /www.clsa.com/member/tools/email_alert/.

Companies mentioned

MediaTek (2454 TT - NT$3,860.00 - HIGH CONVICTION OUTPERFORM)¹

Alphabet (N-R)

Broadcom (AVGO US - US$414.14 - O-PF)²

Samsung Electronics (005930 KS - ₩293,000 - O-PF)³

¹ Covered by SinoPac; ² Covered by CLSA Americas; ³ Covered by CLSA

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_CLSA_聯發科2454_20260523_004.png |

49265 bytes | 真資料圖 | 標題「Figure 7 Forward PE」,折線圖MediaTek Forward PE(藍線),附+1sd 21.04x(淺藍橫線)、-1sd 7.06x(淺藍橫線)、Avg 14.05x(墨綠橫線),時間軸May-21~May-26 |