PDF 原檔:報告_MorganStanley_記憶體Chipflation_20260602_original.pdf

原始內容

M June 2, 2026 08:00 PM GMT

Global Technology

Chipflation - Navigating A Memory Crisis

Surging memory prices and supply scarcity are becoming a cross-sector risk as AI reprices a critical input across the digital economy. What began as an AI infrastructure bottleneck is now spreading into hardware margins, device affordability, cloud costs, inflation and policy.

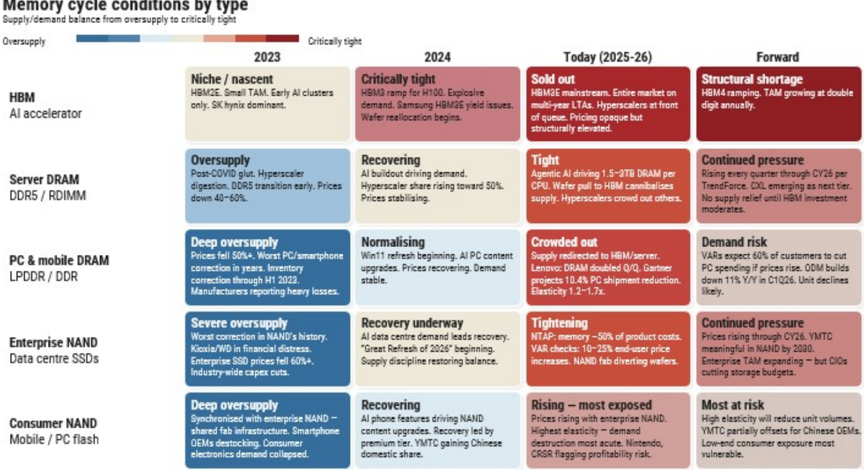

AI is turning memory into a structural bottleneck. AI demand is rising across HBM, DRAM and enterprise SSDs, pushing memory prices up six-fold in the past year. New supply takes years to build, qualify and ramp. That makes this cycle look less like a normal semiconductor upturn and more like a durable supply-demand reset.

Allocation is replacing commodity-market pricing. Hyperscalers and AI buyers are increasingly using long-term agreements (LTAs), prepayments and strategic commitments to secure capacity. That leaves a smaller, tighter and more volatile supply pool for traditional buyers.

HBM is crowding out conventional memory. HBM is essential for AI accelerators but consumes disproportionate advanced DRAM capacity. As suppliers prioritize HBM, server DRAM and enterprise SSDs, less supply remains for smartphones, PCs, autos, networking & industrial markets. Even as total DRAM wafer capacity expands ~30% by 2027, we see memory supply for smartphones/PCs falling 12-15% short.

Chipflation is spreading beyond Big Tech ... Large cloud buyers can secure supply and capitalize higher costs, while non-AI buyers face higher COGS and weaker allocation, price increases, spec cuts and delayed launches.

… and creates a clear divide between suppliers and OEMs. Memory producers benefit from stronger pricing, margins and visibility. Downstream hardware companies must absorb costs, pass them through, redesign products or risk demand destruction, especially in price-sensitive consumer markets.

The macro impact is bigger than CPI alone. Headline CPI effects may be modest given small basket weights, but pressure is visible in PPI, corporate margins, cloud bills, capex budgets and delayed technology deployment.

Policy policy could ease pressure, but would take years. Even if the US and China deploy tools such as subsidies, tax credits or permitting reform, supply responses will take years and near-term China capacity growth is insufficient. We assume US policy stays restrictive and is unlikely to ease pressures in the near or long term.

Stock implications. Pricing power sits with DRAM suppliers (Samsung, SK hynix, Micron), NAND (SanDisk, KIOXIA), HDD (Seagate, Western Digital) infrastructure (ASML, AMAT, KLA). OEMs over-indexed to the consumer, with less pricing power and elevated memory cost exposure face the sharpest margin headwinds.

| Morgan Stanley & Co. International plc+ | |

|---|---|

| Shawn Kim Equity Analyst Shawn.Kim@morganstanley.com | +44 20 7677-1018 |

| Morgan Stanley & Co. LLC Joseph Moore Equity Analyst Joseph.Moore@morganstanley.com | +1 212 761-7516 |

| Senior Global Economist Rajeev.Sibal@morganstanley.com Morgan Stanley & Co. LLC Ariana Salvatore Equity Strategist Morgan Stanley & Co. | |

| Erik.Woodring@morganstanley.com Diego Anzoategui Economist Diego.Anzoategui@morganstanley.com Morgan Stanley & Co. Lee Simpson Equity Analyst Lee.Simpson@morganstanley.com Cindy Huang Equity Analyst | +1 212 296-8083 +1 212 761-8573 International plc (DIFC Branch)+ |

| Rajeev Sibal | |

| Ariana.Salvatore@morganstanley.com International | +971 4 709-7201 |

| plc+ | +44 20 7425-3378 |

| +44 20 7425-2915 | |

| Cindy.Huang@morganstanley.com Morgan Stanley Asia Limited+ Duan Liu | |

| Equity Analyst Duan.Liu@morganstanley.com Morgan Stanley & Co. LLC | +852 2239-7357 |

| Mason Wayne Research Associate Mason.Wayne@morganstanley.com | +1 212 761-6012 |

| Shane.Brett@morganstanley.com Maya C Neuman Research Associate | +1 212 761-1022 |

| +1 212 761-1946 | |

| Dylan Liu Research Associate | |

| +1 212 761-4519 | |

| Dylan.Liu@morganstanley.com | |

| Maya.Neuman@morganstanley.com |

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

+= Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to FINRA restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

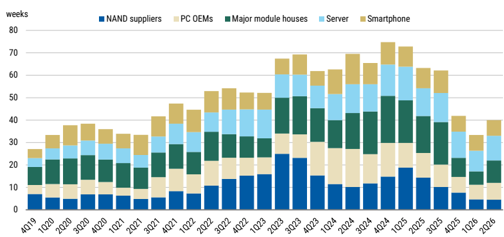

SURGING MEMORY TAM

DRAM DEMAND

M

$220bn

$890bn

37%

ENTERPRISE SSDS

RAPIDLY GAIN SHARE

Enterprise SSDs Jump from

18%

65%

Chipflation - The Story in Numbers

000s

in 20288

SUPPLY IS CONCENTRATED AND SHIFTING

3 firms control ~90% of DRAM output worldwide

SAMSUNG

sk'hynix micron

35%

Al Chip

7x Surge in HBM usage

30%

HBM USAGE SURGES ACROSS HIERARCHY LEVELS

Al System

65X Surge

in HBM usage

Al Cluster 1800x Surge in HBM usage

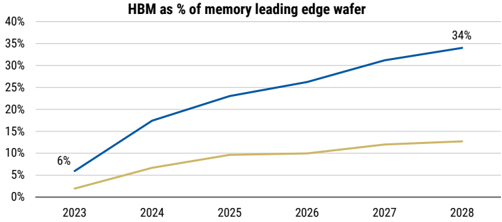

HBM & AI CROWD OUT CONVENTIONAL MEMORY

HBM SHARE OF

LEADING-EDGE WAFERS

HBM rises from ~6% of leading-edge memory wafers

INCREASING AI PRIORITIZATION

leads to ~15% PC DRAM shortfall

and ~12% smartphone DRAN

shortfall in 2027, equivalent to ~58mn in 2023 to ~34% by 2028E

PCs and ~134mn smartphones

PRICING IMPACT

Direct

US CPI

exposure <1%

Incremental global memory

market equivalent to ~45%

of traditional hardware revenue

Source: Trendforce projections (TAM and capacity), Morgan Stanley Research estimates

| ss |

Electronics component

PPI +30% y/y

18% to > 23% by 2028E, representing ~30% of net wafer additions - second only to South Korea

M

What is "Chipflation"?

The shift from historical, deflationary pricing for commoditized microelectronics toward sustained, structural price increases poses a continuous upside risk to overall consumer goods pricing. For memory, inflation is no longer just a component-price issue.

AI infrastructure is absorbing a growing share of memory (DRAM, HBM and enterprise SSD) supply, while suppliers prioritize higher-margin AI/server products over mainstream consumer and industrial demand. The potential impacts of higher memory prices include:

- constrained supply and increases in consumer hardware prices

- a squeeze in corporate profit margins

- a division in the hardware industry between the 'have' and 'have not'

- persistent upside risks to core inflation

Chipflation is demand-driven by the rapid rollout of AI infrastructure and datacenters, where tighter memory availability is feeding into higher device ASPs, higher cloud and enterprise IT costs, lower product specifications, delayed refresh cycles and margin pressure.

Memory shortages have become a macroeconomic concern. The direct CPI impact may be limited, but the effects are increasingly showing up in corporate COGS, cloud bills, capex budgets and delayed technology deployment - making this cycle broader than a traditional semiconductor upcycle. Insufficient chip supply can delay data center projects, slow cloud development and increase costs for businesses, ultimately affecting productivity growth.

Differentiated datasets

This report updates a range of proprietary Morgan Stanley models and introduces several new datasets.

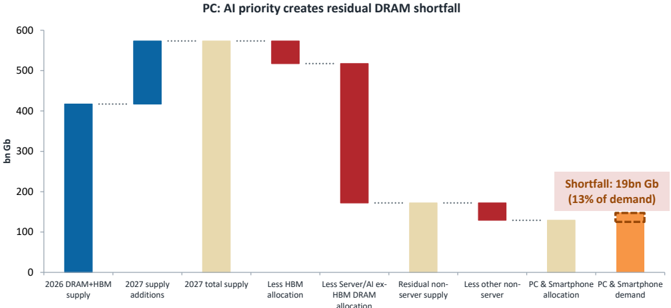

- Two-tier DRAM supply waterfall ( Exhibit 7 ). Our framework decomposes total DRAM supply down to the residual pool available to non-Al buyers. We estimate PCs could face a 15% memory shortfall (~58mn units) and smartphones a 12% gap (~134mn units) as AI crowds out non-server allocation.

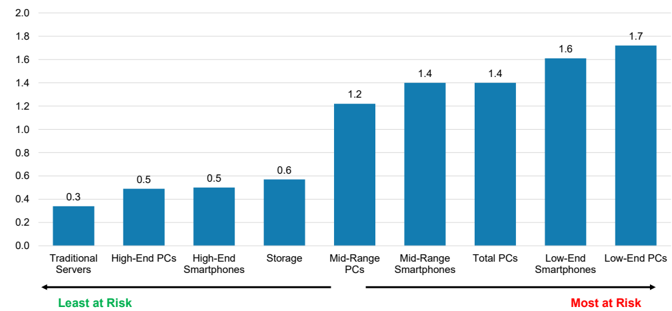

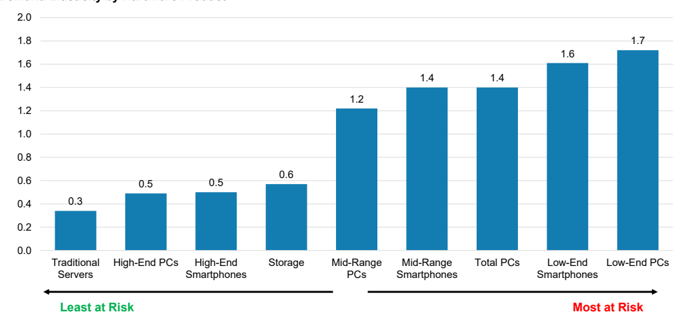

- Demand elasticity by hardware product ( Exhibit 8 ). We rank which end markets are most exposed to demand destruction from higher memory prices, from traditional servers (least elastic) to low-end PCs (most elastic).

- CPI impact of higher memory costs ( Exhibit 11 ). Higher memory costs carry a measurable CPI pass-through: PCs and smartphones add 0.08pp to headline CPI, with total consumer electronics impact reaching 0.10pp.

M

Table of Contents

| Section | Page Number |

|---|---|

| Executive Summary | 5 |

| Memory - A Multi-Year Bottleneck | 14 |

| HBM Cannibalization and the Two-Tier Market | 20 |

| Chipflation Passthrough and Sector Impact | 26 |

| Chips, Growth and Inflation - A Macro Perspective | 37 |

| US/China Policy Options Don't Offer Near-term Relief | 40 |

| Primer: Memory 101 - Types, Market Structure and the Cycle | 47 |

| Appendix: Memory Demand per Gigawatt of AI Data Center Deployment | 53 |

(US$)

100.0

10.0

1.0

0.1

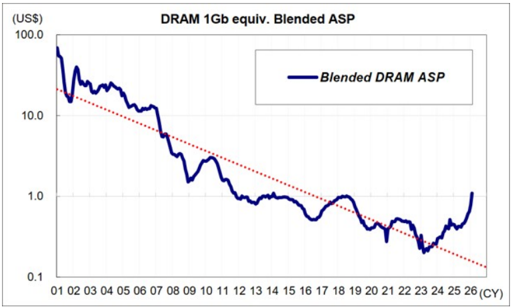

DRAM 1Gb equiv. Blended ASP

M

Executive Summary

Key Theme of 2026

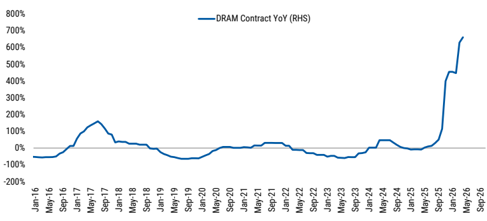

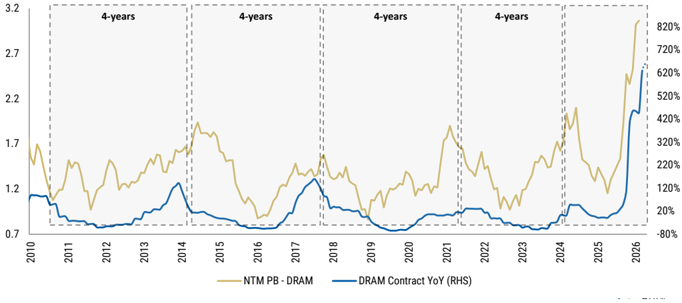

Exhibit 1: DRAM prices YoY

Source: TrendForce, Morgan Stanley Research

A multi-year memory bottleneck

Memory chips are emerging as a critical input in the global AI ecosystem, underpinning the expansion of today's agentic AI architectures ( Technology: Rise of the AI Agent - Global Implications, 19 Apr 2026) . We believe that rising memory prices are rationally anticipating an AI-led price-inelastic leap in memory demand. This pricing strength is less a function of conventional supply discipline by producers, and more a reflection of the exponential growth in end-demand evidenced in the annual capital expenditure commitments from hyperscalers eager not to be left behind in the race for superintelligence.

Rising memory prices create an increasingly challenging cost-push dynamic, where server build costs rise, cloud capex increases and hardware prices inflate. For nonhyperscaler corporates, this inflationary pressure could require choices on whether to pass on price increases, reduce device specifications, or accept reduced profits.

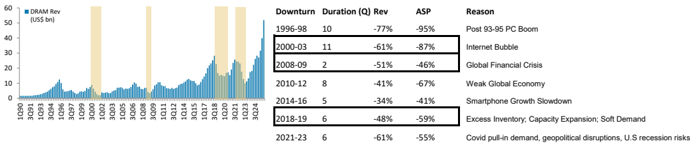

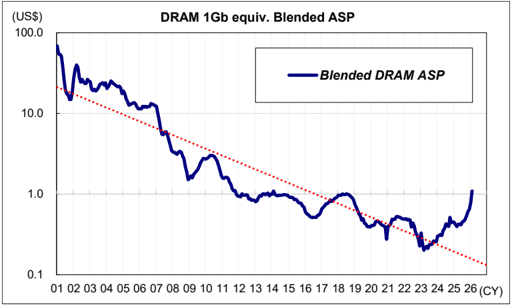

Structural bottleneck

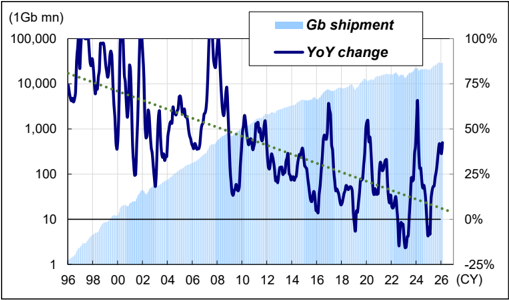

Prices for memory have risen more than 6-fold over the last year ( Exhibit 1 ) - a sharp discontinuity from the multi-decade price declines. The price of a gigabyte of DRAM fell by around a factor of ten every 5 years from 1957 to 2020. Since 2010, the price has fallen more slowly as Moore's Law drove sustained price declines. However, this trend no longer applies in the AI economy, which has driven DRAM ASPs sharply higher ( Exhibit 2 ). Building memory fabrication (fabs) plants takes years, so there is no quick response to address demand. This means sustained upside risks to consumer goods prices in the coming years.

Exhibit 2: Long-term DRAM price/Gb

Source: WSTS

curl allu all ayyreyale?

Memuly supply telet depenus ont molail, yuamuation, yelu lamp allu prouuul allocatlun

• AMZN = MSFT = GOOGL = META

lutoo ft rustlesullo monoto previously

Top 4 Cloud Providers: Cloud Capex Y/Y Growth

→-Current Cloud Capex Forecast

From Tool Capacity to Qualified Memory Output

80%

yeal viuueos

Prior Cloud Capex Forecast

ASML capacity is expanding; memory relief depends on install, qualification, yield ramp and product allocation

M

30%

24%

Exhibit 3: Memory supply relief depends on install, qualification, yield ramp and product allocation - a ~2 year process

$413

$72

$91

$118

Orders placed → tools delivered → qualified → production: 1-2-year lag $276 10% 0%

-10%

What's different this time? Previous chip shortages during COVID demonstrated how even minor supply disruptions can halt entire industries. However, this memory chip shortage looks more structural, and AI-related demand could amplify such effects on a much larger scale.

- Mobile AI agents and physical AI agents - another very large additional surge in demand for memory chips is likely as these are rolled out. As AI increasingly moves beyond data centers into edge devices and the physical world, the computational requirement for AI is set to grow exponentially. These components would no longer be seen as commodity memory chips but as critical pillars of the global digital infrastructure.

- Long-Term Agreements (LTAs) are now absolute necessities to secure capacity given long lead times and the persistence of the supply-demand mismatch. Memory producers are establishing strategic supply chain partnerships with all hyperscale customers via L TAs, through which memory producers are able to lock in long-term orders and prices, establish a stable high-margin model, and mitigate the industry's cyclical volatility.

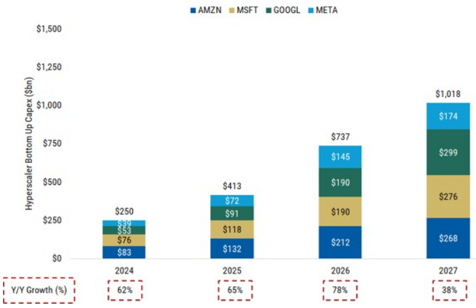

Exhibit 4: We expect hyperscaler capex to surpass US$1tr in 2027 and an aggregate ~US$2tr invested since 2024

Exhibit 5: The 2026 consensus cloud capex forecast increased to +75% Y/Y post results from 64% previously

Source: Company data, Morgan Stanley Research estimates

Source: Company data, Factset consensus estimates, Morgan Stanley Research estimates

$1,500

$1,250

$1,000

$750

$500

Hyperscaler Bottom Up Capex (Sbn)

$250

$250

Chuan. Marnon Canla, Donnerol

SO

/ V/Y Growth (%)

$190

$190

Source: Morgan Stanley Research

59%

Tools ship;

customers install,

38%

291

qualify and ramp

29%

34%

75%

65%

55%

available

DRAM output

Duyer Theraruly. Who yelo memory supply mol!

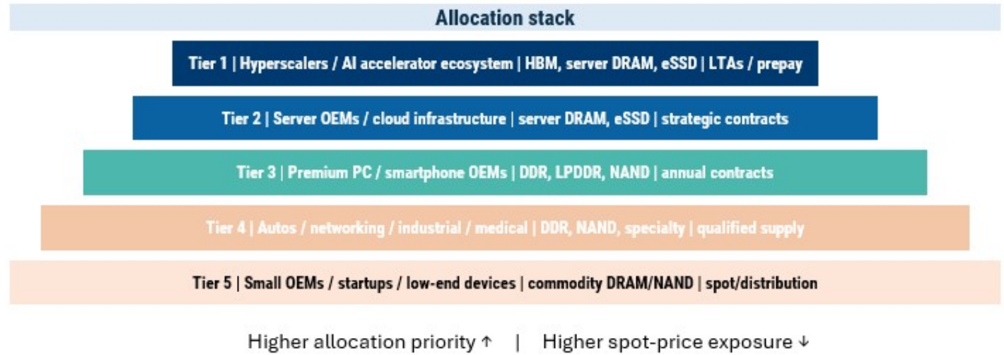

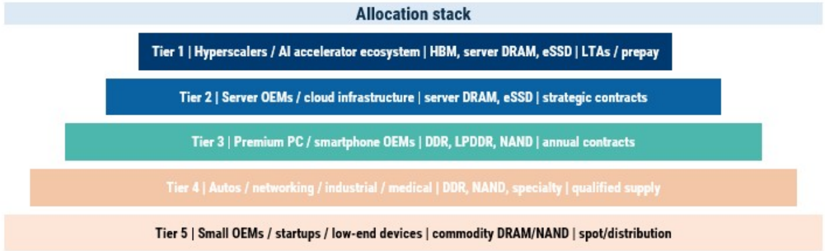

Allocation stack

M

Exhibit 6:

Buyer Hierarchy: Who gets memory supply first?

Margin risk for the broader hardware sector

Memory inflation is turning into a broad hardware-sector margin risk , extending beyond PCs and smartphones into gaming consoles, servers, cloud, networking, autos, medical devices, broadband equipment, industrial systems and low-cost education/ embedded devices. The impact is not only higher DRAM/NAND pricing, but also allocation priority:

- Suppliers are prioritizing HBM, server DRAM and enterprise SSD demand tied to AI infrastructure, while traditional consumer and industrial memory users are increasingly coping with significantly higher prices, longer lead times and weaker bargaining power.

- The more impacted group are companies that are not directly monetizing Al but still have to pay Al-driven memory prices. There is accounting asymmetry, where hyperscalers can capitalize memory-heavy AI servers and depreciate them over time, while consumer hardware and industrial OEMs see memory inflation flow more directly through inventory and COGS. This will require choices on whether to pass on price increases to consumers, reduce device specifications, or accept reduced profits.

- Memory inflation is not just a financial transfer from non-Al sectors to memory producers. It is increasingly a constraint on what gets built and when for many nontech industries.

Applying our memory sufficiency framework separately to PC and smartphones, we

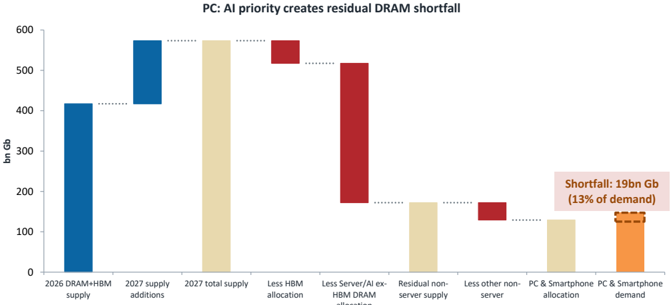

find both segments face supply shortfalls in 2027. On our assumptions (PCs absorbing 17% of non-server DRAM and smartphones 58%) total addressable memory falls ~15% and -12% short of demand, respectively. This implies unit downside of - 58mn PCs (-15% vs MS shipment forecast) and ~134mn smartphones (-12% vs MS forecast). These numbers are sensitive to assumptions on memory content per device, but our analysis indicates demand rationing risk if the supply build does not accelerate.

Source: Morgan Stanley Research

M

Exhibit 7: AI prioritization turns 2027 supply growth into a consumer memory shortfall

Source: Morgan Stanley Research estimates

Exhibit 8: Our quant analysis implies low-end smartphones and PCs are the most demand elastic, while servers, storage and high-end smartphones are least at risk of demand destruction from higher prices

Demand Elasticity by Hardware Product

Source: IDC, Company data, AlphaWise, Morgan Stanley Research. Demand elasticity takes the absolute value. PC data goes back to 1995, for storage it starts in 2008, servers in 2003 and smartphones in 2007.

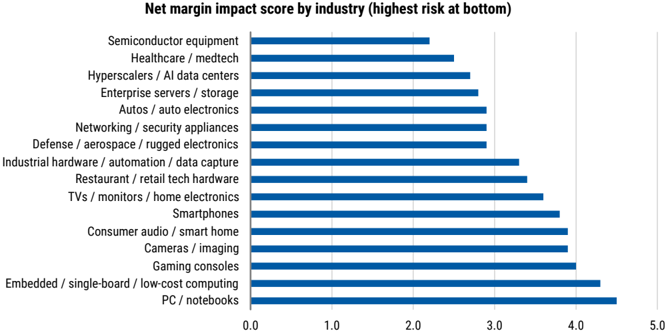

Exhibit 9: The Chipflation impact by industry (illustrative)

Note: Ranking reflects net margin pressure after passthrough, assuming: 45% gross cost impact + 25% demand/volume risk + 20% allocation risk + 10% passthrough burden. Score scale: 1 = low risk, 5 = highest risk. Source: Morgan Stanley Research estimates allocation

M

Macro implications

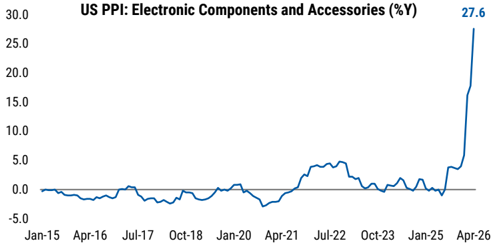

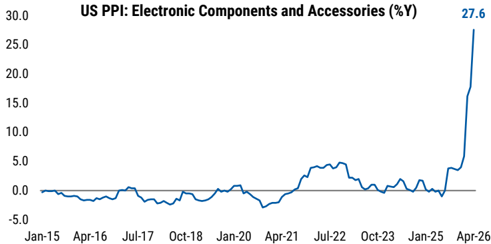

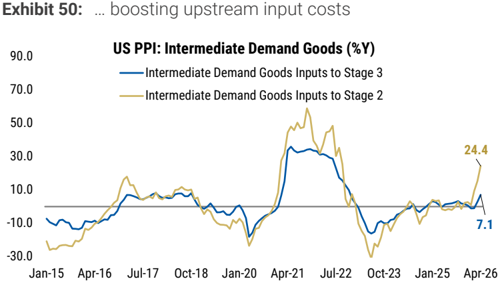

Chipflation is translating into higher producer price inflation , notably in measures of computer and electronics linked equipment. How this translates into consumer inflation in these segments will define margin pressures - for now the effect is strong in US PPI and softer in CPI. The effect on headline CPI inflation is likely less because of the small weight of memory-sensitive goods in the basket, but the longer chip prices stay elevated, the more macro consequences we can expect.

Exhibit 10: The effect of rising costs is visible in exposed PPI, with some sub-components rising to all time highs

Source: BLS, Morgan Stanley Research

Exhibit 11: Higher memory costs could drive 15pp CPI for PCs and smartphones in the US this year - even if the headline CPI effect is more muted because of basket weights

| CPI component | Memory costs effect on CPI in 2026 (pp) | CPI weight |

|---|---|---|

| PCs | 15 | 0.30% |

| Smartphones | 15 | 0.20% |

| TVs | 10 | 0.10% |

| Cars | 0 | 3.80% |

| Major household appliances | 5 | 0.06% |

| Game consoles | 125 | 0.01% |

| Impact on headline CPI: PCs and smartphones only | 0.08 | |

| Total impact on headline CPI | 0.1 |

Note: Smartphones and game consoles weights are estimates. Source: BLS, Morgan Stanley Research forecasts

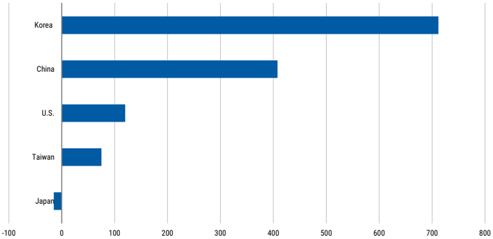

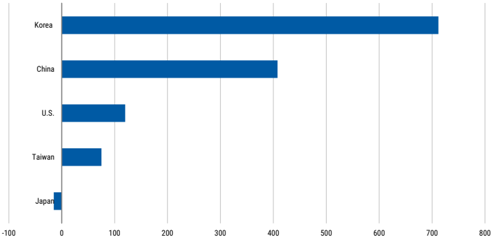

Concentration strengthens the position of memory producers and boosts regional

markets. For export-oriented economies dominated by semiconductor chip manufacturing (especially South Korea and Taiwan for logic chips), the surge in memory revenues and market demand has substantially bolstered national GDP and local stock indices. Samsung, SK hynix and Micron Technology together control roughly 90% of the global DRAM market and 100% of the HBM market, giving them significant pricing power. South Korea alone produces nearly 75% of the global DRAM chips.

M

Policy options

Memory chips are increasingly being viewed as a strategic resource , in particular where HBM and advanced DRAM directly enable AI end uses (and consequently, US policy options to support this end are likely to persist following the midterm elections). We therefore expect policy efforts in this area to focus less on near-term cost relief and more on protecting AI-strategic memory through supply-chain resilience, trusted capacity, and geopolitical de-risking. For less sophisticated (non-frontier) memory end uses (automotive, consumer, etc.) policymakers may seek to distinguish commodity or legacy memory from AI-strategic memory through differentiated licensing and targeted supply-side support for trusted capacity in the former category. Importantly, political obstacles, timing lags, and associated supply chain constraints still likely dilute these efforts' effectiveness. Forced allocation would likely be a last resort, in our view. It might protect favored sectors in the short term, but would risk turning memory into a rationed geopolitical commodity.

Across the board, the policy options may mitigate, but ultimately not solve, the problem.

- Direct subsidies can support new fabs, packaging and test capacity, but may not lower prices quickly.

- Tax credits can encourage investment but are less targeted. Procurement guarantees can de-risk capacity additions, but may distort allocation.

- Expedited permitting can improve time-to-capacity, but execution is difficult.

- Equipment-access coordination can support allied capacity expansion, but must be balanced against export-control objectives.

- Strategic stockpiles may help critical sectors, but are hard to manage in fastmoving technology markets.

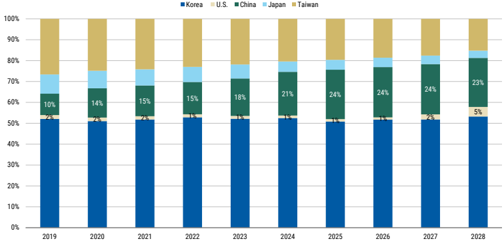

China fabs are the largest swing factor for global memory supply, but the upside is policy-gated

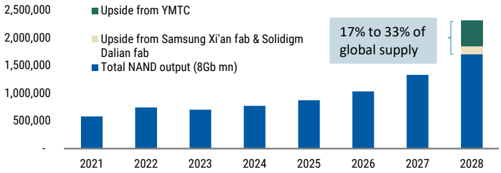

Mainland China accounts for ~30% of net wafer additions over 2023-28E, second only to South Korea ( Exhibit 12 ). However, not all capacity is equally advanced, accessible, or trusted. On NAND, the potential uplift is considerable: combining YMTC capacity and yield expansion with node migration at Samsung's Xi'an and Solidigm's Dalian facilities, Chinabased incremental output could reach 17-33% of 2028E global NAND supply ( Exhibit 13 ). This acceleration scenario assumes a meaningful relaxation of US export controls and is not our base case, as we do not assume the EUV ban on exports to China is lifted. The key gating factor is not Chinese ambition or investment appetite, but access to leading-edge equipment.

M

Exhibit 12: Mainland China accounts for 30% share of 202328E net DRAM wafer additions, behind South Korea

Source: TrendForce estimates, Morgan Stanley Research

Exhibit 13: China NAND acceleration scenario - YMTC and Koran suppliers' China fabs could add up to 17%-33% of 2028 global NAND supply

Source: Morgan Stanley Research estimates

Stock exposure

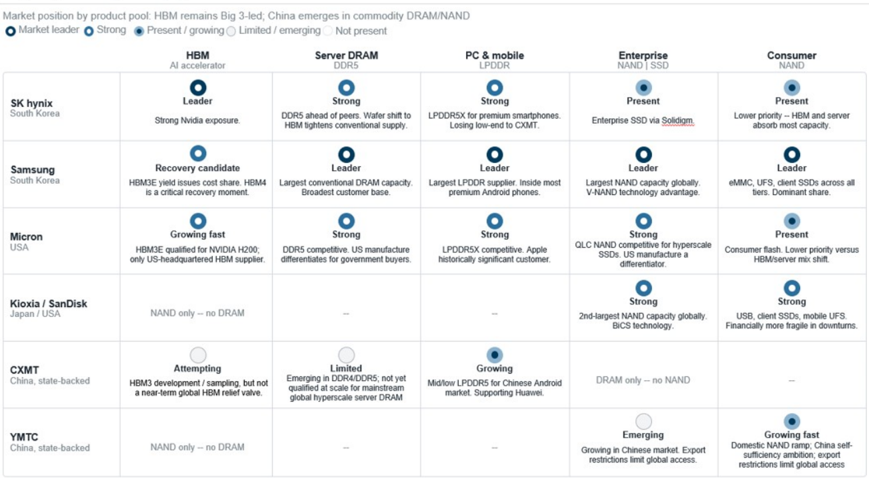

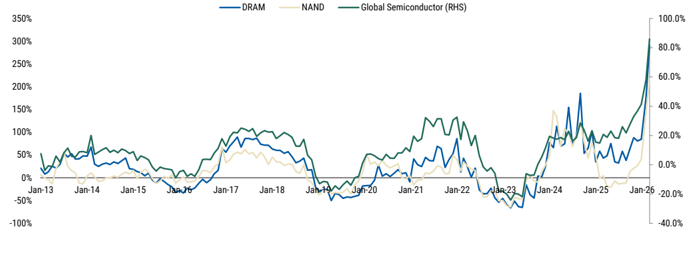

Companies selling into AI enjoy pricing power, while the buyers face margin pressure. In an agentic AI world, demand and pricing power gravitates towards memory and CPU plus the associated supply chains. This is evident in year-to-date stock performance: global consumer electronics stocks have fallen 1% on average, while a memory makers have risen by almost 300%, alongside unprecedented EPS revisions of 333% YTD. We continue to like DRAM suppliers (Samsung, SK hynix, Micron), NAND (SanDisk, KIOXIA), and HDD (Seagate, Western Digital).

The opportunity extends beyond individual memory chips to the full AI system. The beneficiaries of this shift are global and full-stack. The surge in memory is mainly driven by the recent agentic AI shift broadening well beyond headline AI chips - we lay out in Exhibit 14 which stocks offer exposure. Beneficiaries include CPU vendors, memory suppliers, storage companies, and advanced packaging and substrate providers, alongside foundries, equipment makers and server manufacturers. In short, agentic AI widens the AI investment landscape, shifting focus from owning the best accelerator to enabling the full system that makes intelligent agents work.

Exmble 19. Tow lu viay the thielle!

Global Exposure Across the Stack? Names by exposure

CPU

M

• Micron

PCB/Substrate/CCL & Materials

• SEMCO • Unimicron • NYPCB

• Ibiden • Nittobo • MEC

MLCC & CPU socket

• Murata • TDK • Yageo

• FIT Hon Teng • Lotes

ODM

• Wiwynn

• Hon Hai

• TDK

IC-design

• GUC

• Egis

Exhibit 14: How to play the theme?

BMC, CPU & Memory interface

• Aspeed • Renesas • Montage

• WPG • AP Memory

SPE

• ASML • ASMi • AMAT • Besi • KLAC

• Tokyo Electron • Ulvac • Wonik

Source: Morgan Stanley Research

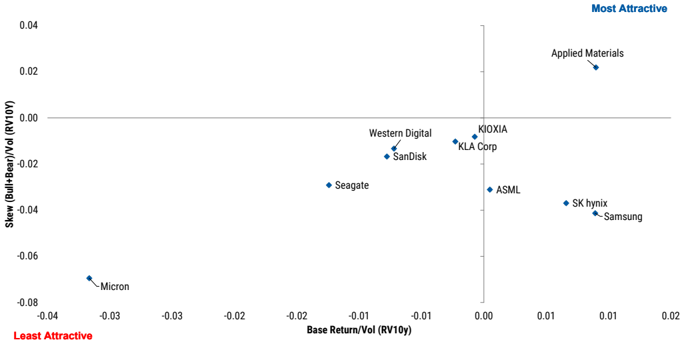

Exhibit 15: Risk/return positioning for key memory and SPE stocks

Source: Factset (historical share price data), Morgan Stanley Research estimates. Note: Methodology: X-axis (Base Return/Vol) represents our base case price target return divided by 10-year realized volatility (RV10y). Y-axis (Skew) represents the sum of our bull and bear case returns divided by RV10y, capturing payoff asymmetry.

- US Semiconductors: Agentic AI-driven CPU demand structurally favors AMD in cloud share gains, but we prefer exposure via AI enablers in NVIDIA and Micron where token growth and capex translate more directly into earnings upside.

- US Semiconductor Equipment: Rising compute and CPU TAM drive incremental WFE demand, with DRAM and leading-edge logic (<5nm/2nm) capacity expansion supporting upside for equipment names such as AMAT and KLA.

- US Hardware: AI agent proliferation is a structural tailwind for HDD demand, as persistent storage is required to capture growing volumes of context, history, and system-level data, with ~80% of cloud data still residing on disks. We expect HDD demand to remain strong (Demand growing at 50% EB vs. 30%+ supply CAGR), with supply tightness supporting a 'stronger for longer' pricing backdrop, benefiting Seagate and Western Digital. On the flip side, we see US Hardware OEMs and hyperscalers as most exposed to memory inflation/shortages. Among the US Hardware OEMs, vendors with (1) more consumer exposure, (2) smaller scale/TAMs, and (3) less pricing power/differentiation face the most significant

M

margin risk. While Server and Storage OEMs have greater exposure to memory inflation than this cohort, structural demand for AI supports greater pricing power/ ability to pass through costs to the end customer (DELL, HPE). This puts small cap consumer electronics and PC vendors most at risk of seeing margin pressure. AAPL is our only Overweight-rated OEM in US Technology Hardware.

- European Semiconductors: ASML's EUV tools are a critical enabler of future DRAM supply expansion, and the company benefits from rising compute intensity and design complexity.

- Korea Technology: We continue to see Samsung Electronics and SK hynix as key beneficiaries of memory content growth from AI CPU penetration.

- Greater China Semiconductors: Montage is leveraged to the structural increase in memory content per server, with higher CPU and DRAM intensity driving demand for memory interconnect solutions.

- Japan Semiconductors: Increasing CPU complexity and memory scaling drive demand for advanced semi-cap (Tokyo Electron, Ulvac) and memory interface solutions, positioning Renesas as a beneficiary of higher DRAM bandwidth/capacity requirements. Agentic AI also supports NAND demand (KIOXIA) and broader data center exposure across Japan semi names.

What could challenge the chipflation theme

AI spend slows down. Reduced competition among frontier LLMs could result in lower AI capex spend and a shift back to ample memory supply. Alternatively, dramatic improvements in AI model architectures and KV cache/tokenization could shrink the amount of memory needed by data centers per token generation. The high costs of funding AI infrastructure could also lead major cloud service providers to scale back buildouts.

Electricity and power supply. The availability of reliable, large -scale electricity could be an obstacle, as scaling advanced AI models and running agentic ecosystems requires unprecedented electrical loads. A new phase of agentic systems designed to reason, plan and operate over extended periods with continuous, high-intensity computing is pushing data centers into sustained peak power usage, far beyond the short bursts typical of earlier chatbot-style AI. This poses a significant challenge to global grid infrastructures.

Demand destruction . Memory demand destruction is already here for traditional technology products and could take the form of a hardware margin squeeze, higher retail prices, and a structural market shift where smaller vendors and mid-tier OEMs are disproportionately affected. A material slowdown in demand would ease supply tightness and hence reduce prices.

Geopolitics and trade policy. Memory and advanced packaging sit in a global supply chain. Any new restriction or disruption could alter patterns of supply and demand.

M

Memory - A Multi-Year Bottleneck

Shawn Kim, Joseph Moore

The explosive demand for AI infrastructure has caused supply constraints in all types of memory (DRAM, HBM, NAND, HDD). As AI increasingly moves beyond data centers into edge devices and the physical world, it could trigger a further surge in demand for memory chips. In that scenario, these components would no longer be seen as commodity chips but as critical pillars of the global digital infrastructure.

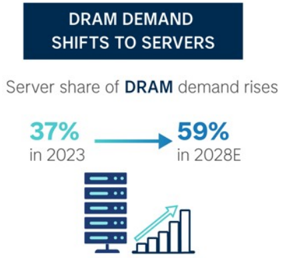

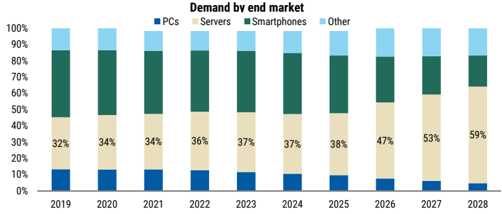

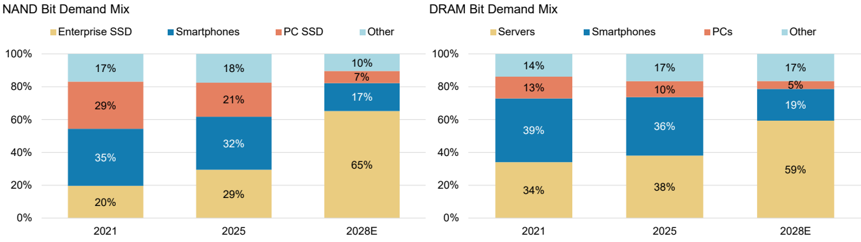

AI and data centers are becoming the dominant buyers of memory - we expect the server share of DRAM demand to rise from 37% in 2023 to 59% in 2028e, while enterprise SSDs jump from 18% to 65% of NAND demand. The result is a structurally tighter market where non-AI buyers may face weaker access to supply for an extended period.

A quick primer - what is memory?

Memory is the working space a computer uses to hold data it is actively processing - the digital equivalent of the desk you are working on right now, as opposed to the filing cabinet behind you. Three types of memory matter for the AI economy:

- DRAM (Dynamic Random Access Memory) is the fast but expensive working memory used by every server, PC and smartphone. It is what the CPU uses to hold and fetch the data it is computing.

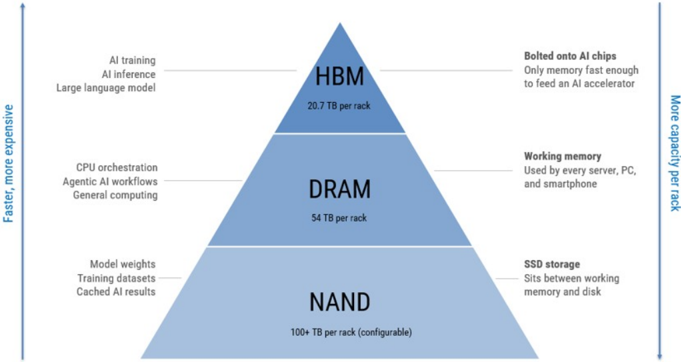

- HBM (High Bandwidth Memory) is a premium type of DRAM focused on providing maximum data bandwidth. HBM is DRAM stacked vertically and bolted directly onto AI chips - it is the memory layer that makes large AI models possible, feeding data fast enough to limit an AI accelerator downtime. Think of DRAM as a single lane road and HBM as a 12-lane highway for data transmission.

- NAND is the storage memory used in solid-state drives (SSDs), which sit between working memory and slower HDD disk storage. NAND holds the trained model weights, the training datasets, and the cached results that AI systems retrieve from. It is also used for picture, video and data storage.

All three types of memory matter as Al workloads use all three at once and in massive quantities. Next-generation rack-scale AI systems such as NVIDIA's Vera Rubin NVL72 contain 20.7TB of HBM attached to GPUs and 54TB of LPDDR5X serving the CPUs, before considering local or external SSD storage.

AI demand is scaling across three layers at once - more memory per chip, more chips per system, and more systems per cluster. Agentic AI adds another layer of pressure through longer context windows, larger conversation memory and repeated inference across multiple agents. The result is a structural increase in memory intensity across all aspects of the AI stack

Cxnnolt 10.

Faster, more expensive cAmbre 17. Tomoor capacily lo yuameu memory vulput leau times die multiple yual tels

From Tool Capacity to Qualified Memory Output

ASML capacity is expanding; memory relief depends on install, qualification, yield ramp and product allocation

M

QO

CPU orchestration

Agentic Al workflows

General computing

Model weights

Training datasets

Cached Al results aee. AllInIAAAenel

Q1

DRAM

Tools ship;

customers install, qualify and ramp

Exhibit 16: AI servers are becoming memory systems

and smartphone

Orders placed → tools delivered → qualified → production: 1-2-year lag

54 TB per rack

NAND

100+ TB per rack (configurable)

Atata. Oohis tilt 70 moaeaet

DRAM output available

Q7/8

Source: NVIDIA, Morgan Stanley Research. Note: Rubin NVL72 memory capacity based on platform disclosures. NAND/eSSD capacity varies by OEM and storage architecture.

For readers less familiar with the memory market structure, a full primer is included in Primer: Memory 101 - Types, Market Structure and the Cycle

The AI Memory Wall

The bottleneck in AI is increasingly memory, not just compute. As inference shifts from single-turn chat to agentic workflows, memory intensity rises sharply: large models need weights resident in memory, while longer context windows and KV caches increase memory usage per user, per session and per agent. Agent swarms multiply this effect because many agents maintain or reload context simultaneously, turning inference into a much larger memory-capacity and memory-bandwidth problem. Hyperscalers therefore need more HBM, server DRAM and enterprise SSD capacity to meet this surge in memory use now, not when new fabs ramp in a few years' time.

That urgency is pushing Big Tech toward multi-year LTAs , to secure future capacity via prepayments. The challenge for producers is that supply is unable to respond immediately: EUV tool availability, fab construction, process qualification, HBM stacking, packaging, testing and yield ramp are multi-year, multi-billion-dollar projects. This is why visible demand today can still translate into shortages through 2027 and beyond.

Exhibit 17: From tool capacity to qualified memory output - lead times are multiple quarters

Source: Morgan Stanley Research

SAmble 17. homil uruel boun allu baunluy

Order book (€mn) (LHS)

14,000

12,000

10,000

8,000

6,000

4,000

- Backlog (Emn) (RHS)

46,000

M

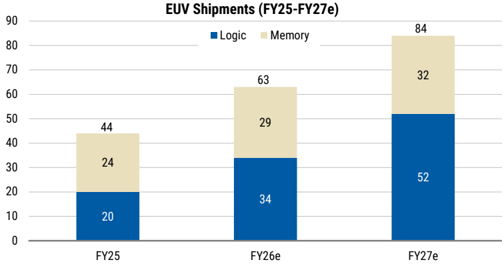

Supply response requires demand visibility. The supply response is coming, but it requires demand visibility and commercial commitment. Our Europe semis team expects ASML to expand capacity in line with sustained EUV demand, with shipments guided from 44 systems last year to 60+ systems this year and potential capacity moving higher as demand visibility improves. The issue is therefore not simply ASML lead time. The constraint is the full conversion chain: memory customers need to commit, tools need to ship, fabs need to be ready, processes need to qualify, yields need to ramp, and HBM packaging/test capacity needs to scale.

The post-Covid cycle was a lesson here. Intel and Samsung both deferred EUV orders after demand weakened and execution challenges delayed ramps, creating order volatility for the equipment supply chain. This cycle, memory makers and hyperscalers may need to provide firmer LTAs, prepayments and allocation commitments before capacity is built. That supports our view that supply relief is real, but phased - and that memory tightness could persist into 2027 even as EUV capacity expands.

Exhibit 18: ASML EUV shipments FY25-FY27e

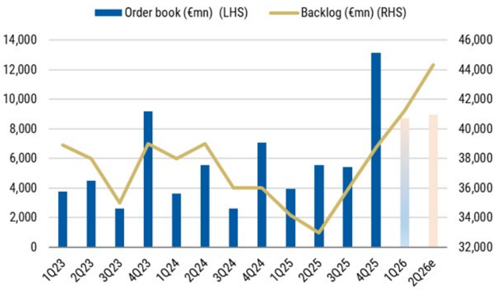

Exhibit 19: ASML order book and backlog

Source: Company data, Morgan Stanley Research estimates

Source: Company data, Morgan Stanley Research estimates

Demand is shifting from consumer electronics to AI/server infrastructure

DRAM server share of bit demand rises from 37% in 2023 to 59% in 2028e , while the share of shipments for PCs and smartphones declines sharply. This matters because the dominant buyer increasingly has stronger purchasing power, longer-duration demand visibility and greater willingness to sign L TAs or prepay for supply. As a result, pricing and shipment allocation continue to gravitate toward AI/server infrastructure requirements at the expense of traditional consumer end markets.

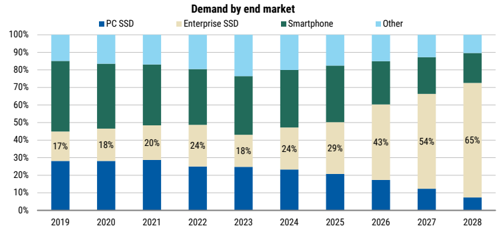

NAND is undergoing a rapid mix shift in enterprise SSDs. Enterprise SSD share of NAND bit demand rises from 18% in 2023 to 65% in 2028e, making AI/server storage the key swing factor for NAND. This reflects the storage intensity of AI workloads, including training data, model checkpoints, retrieval-augmented generation, inference infrastructure and enterprise data lakes.

M

Exhibit 20: DRAM - AI server demand becomes dominant …

Source: TrendForce estimates, Morgan Stanley Research

Exhibit 21: … as well as NAND enterprise SSDs as key growth drivers

Source: TrendForce estimates, Morgan Stanley Research

Supply slow to respond

New memory capacity will come online from late 2027 but is still unable to meet

demand for all markets. Strategically, most of the valuable capacity is likely to be dedicated to where pricing, margins and customer commitments are strongest - namely to HBM customers, server DRAM and enterprise SSDs. While AI semiconductors are forecast to grow at a ~50% CAGR by 2030 (as per TSMC forecasts at its annual technology symposium on May 14, 2026), we expect DRAM production to grow at a pace that will meet only about 60% of demand, given annual bit shipments are unlikely to rise much above the 30% level due to EUV constraints.

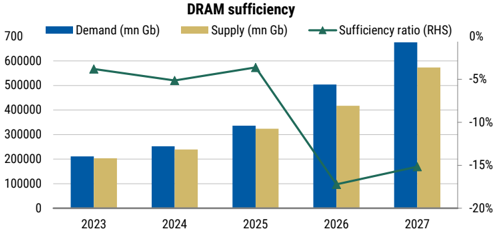

We model DRAM supply remaining tight even as capacity additions accelerate. DRAM undersupply widens from ~4-5% in 2023-24 to ~17% in 2025-26, before easing but still remaining tight at ~15% in 2027e. The key issue is timing.

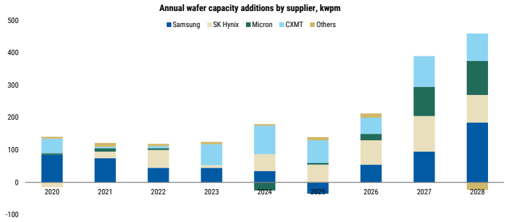

- Annual DRAM wafer capacity additions rise from ~105kwpm in 2025e to ~390kwpm in 2027e and ~460kwpm in 2028e, led by Samsung, SK hynix, Micron and CXMT. This represents meaningful supply growth by historical standards, but arrives after the period of maximum tightness.

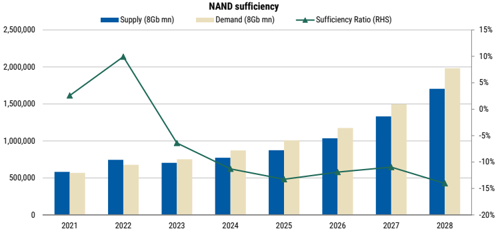

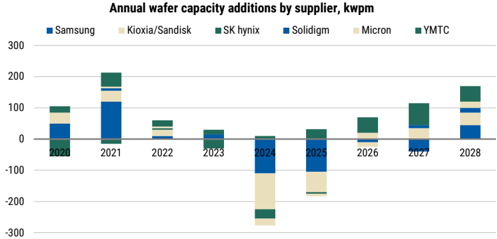

- NAND remains under-supplied through 2028e, with the sufficiency ratio deteriorating to roughly ~14% undersupply in 2028e. Capacity additions recover only after net cuts in 2024-25, rising to roughly ~170kwpm in 2028e, led by Samsung, KIOXIA/SanDisk, SK hynix/Solidigm, Micron and YMTC.

- Of these, CXMT and YMTC are Chinese memory producers whose recent acceleration represents a meaningful shift in the supply-side landscape. From 2023 to 2028e, we expect Mainland China to account for ~31% of net global DRAM capacity additions, behind South Korea but ahead of the US, Taiwan and Japan. We discuss China's role in the global memory landscape and the geopolitical questions it raises here.

The timing issue in bringing on new capacity is compounded by execution risk. New memory capacity requires fab construction, tool delivery, process qualification, customer validation and yield ramp. Even when capacity is announced, usable output can lag by several quarters or years.

M

Exhibit 22: DRAM supply sufficiency ratio

Source: TrendForce estimates, Morgan Stanley Research

Exhibit 24: DRAM annual wafer capacity additions are moving to all-time high

Source: TrendForce estimates, Morgan Stanley Research

Exhibit 23: NAND supply sufficiency ratio

Source: TrendForce estimates, Morgan Stanley Research

Exhibit 25: NAND annual wafer capacity additions are held back by DRAM producers

Source: TrendForce estimates, Morgan Stanley Research

LTAs: strategies to guarantee supply allocation and priority

Shifting from price-driven cycles to supply-security focused LTAs. The memory industry is undergoing a structural transformation in how supply is contracted. Historically, memory customers often procured opportunistically, with pricing largely linked to shortterm supply-demand conditions. During upcycles, customers sometimes signed LTAs to secure allocation, but these agreements often had limited enforceability and could be renegotiated when the market softened.

This cycle looks different as memory availability is now tied directly to AI deployment roadmaps. Leading Cloud Service Providers (CSPs) are no longer managing just price risk; they are managing supply risk as well. As a result, multi-year agreements, production capacity guarantees and prepayments are becoming more important.

- Samsung has discussed moving quarterly and annual contracts into 3-5 year agreements.

- SK hynix has highlighted increasing customer requests for medium- to long-term supply commitments.

- Micron has announced a 5-year Strategic Customer Agreement.

- SanDisk has described multi-year partnerships backed by firm financial guarantees.

- KIOXIA has indicated that long-term supply agreements with hyperscale customers are extending into FY28-29.

M

This is where we see a two-tier market starting to emerge. AI/cloud buyers lock in supply first, while non-L TA buyers compete for a smaller and more volatile residual pool.

Canon co. Mimenory menolly cumboullus auloss ullu, sel vel, laun allu uluotel

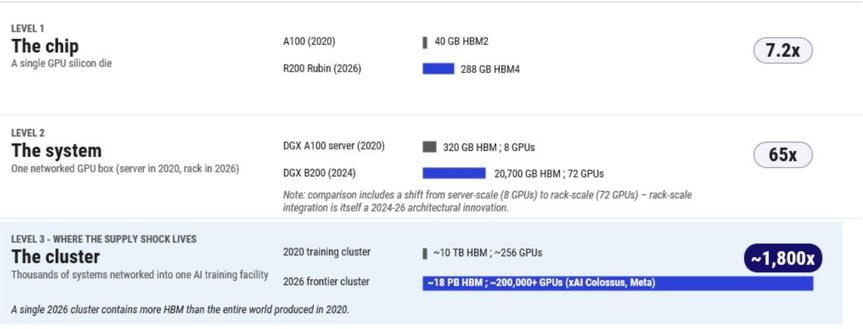

LEVEL 1

LEVEL 2

A100 (2020)

• 40 GB HBM2

M

DGX A100 server (2020)

320 GB HBM; 8 GPUs

HBM Cannibalization and the Two-Tier Market

LEVEL 3 - WHERE THE SUPPLY SHOCK LIVES

The cluster

Thousands of systems networked into one Al training facility

2020 training cluster

2026 frontier cluster

A single 2026 cluster contains more HBM than the entire world produced in 2020.

Shawn Kim, Joseph Moore

-18 PB HBM; -200,000+ GPUs (xAI Colossus, Meta)

HBM is increasingly becoming the mechanism through which AI demand crowds out conventional memory supply, by consuming advanced DRAM wafer capacity and locking in future supply through L TAs. This is sharply reducing available DRAM supply - our analysis implies a ~15% PC DRAM shortfall and ~12% smartphone DRAM shortfall, equivalent to ~58mn PCs and ~134mn smartphones. This could drive a two-tier market, where large AI buyers secure supply first, while non-AI buyers face higher prices, weaker allocation and higher volatility. CALCAA NIVNA dicalauras Marcan Canla Dacaral natimatas NatA. IDM canaditine arilletrativa natiam laval damnericano: altatar natimata acclimas frantiar canla trainine

HBM demand is scaling non-linearly

The HBM demand curve is compounding at every layer of the AI stack. With growing complexity in AI models and larger systems architectures, memory requires higher capacity, lower latency, higher bandwidth, and improved energy efficiency. All leading AI chips deployed for AI training and inference use HBM to scale memory capacity and bandwidth per chip by adding more stacks, higher layer counts, with faster generations of HBM. HBM's critical role in AI chip architecture is scaling across three layers at once:

- HBM content rises 7.2x at the chip level, from 40GB per A100 GPU to 288GB per Rubin GPU.

- At the system level, memory content rises even faster: an 8-GPU A100 server had roughly 320GB of HBM, while a Rubin NVL72 rack-scale system carries 20.7TB, or around 65x more.

- At cluster scale, the memory consumption becomes exponential. A 2020 training cluster with ~256 A100 GPUs contained roughly ~10TB of HBM. A 2026 frontier cluster with ~200,000+ GPUs could contain roughly ~18PB of HBM, or around ~1,800x more.

Exhibit 26: AI memory intensity compounds across chip, server, rack and cluster

Source: NVIDIA disclosures, Morgan Stanley Research estimates. Note: HBM capacities are illustrative platform-level comparisons; cluster estimate assumes frontier-scale training clusters.

7.2x

~1,800x

M

HBM consumes disproportionate DRAM capacity

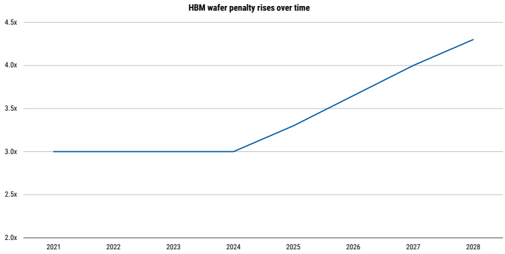

HBM is not just incremental DRAM demand. It causes a meaningful throughput penalty due to significantly larger die sizes and yield challenges from 3D stacking, TSVs, advanced packaging, intensive testing and customer qualification. These steps significantly reduce effective bit output versus conventional DRAM and increase the burden on wafer, packaging and test capacity.

Our model shows the HBM bit-output penalty rising from roughly 3.0x conventional DRAM wafers in 2021-24 to ~4.3x by 2028e. In other words, each unit of HBM output consumes materially more wafer capacity than conventional DRAM output.

At the same time, HBM is absorbing a growing share of the most constrained wafer pool. HBM rises from ~6% of leading-edge memory wafers in 2023 to ~34% by 2028e. AI customers are not only adding new demand; they are taking a larger share of leading-edge capacity that might otherwise support DDR, LPDDR and conventional server DRAM.

Exhibit 27: HBM die penalty - bit-output is reduced due to much larger DRAM dies

Exhibit 28: HBM cannibalization: share of advanced DRAM wafer is rising sharply

Source: Morgan Stanley Research estimates

Source: Morgan Stanley Research estimates

HBM supply is ramping, but remains concentrated

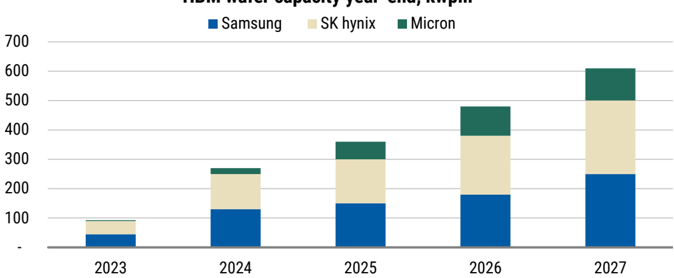

Significant growth in HBM bit demand is driven by AI chip demand. HBM capacity is ramping quickly, but the market remains concentrated across Samsung, SK hynix and Micron. We forecast year-end HBM capacity to rise from ~480kwpm in 2026e to ~610kwpm in 2027e.

Even with this ramp, supply remains constrained because HBM capacity is not just a waferstart question. It also depends on yield, utilization, TSV capability, advanced packaging, test capacity and customer qualification. Qualification is especially important: not all HBM capacity is immediately usable by all accelerator customers.

What about China HBM? Current export restrictions ban all raw HBM stacks into China; however, chips with HBM can still be shipped as long as they do not exceed the FLOPS regulations. CXMT is rapidly expanding HBM capacity, targeting HBM3 this year and HBM3e in 2027 to support domestic AI chips. Other new entrants, such as XMC (Wuhan Xinxin) are producing the HBM wafers with new DRAM dies set for production by YMTC later this year. Current capacity is at R&D scale but is planned to ramp in coming years.

M

Exhibit 29: HBM wafer capacity is still highly concentrated in the Big 3 DRAM companies

HBM wafer capacity year-end, kwpm

Source: Company data, Morgan Stanley Research

HBM Model Update

We update our HBM model with the following key changes:

- Capacity : We expect all three players to continue their aggressive back-end capacity expansion. We expect total capacity to reach 610k/wpm by the end of 2027e with the potential upside if pricing negotiation goes smoothly.

- Yield and UTR : We increase the UTR and yield assumptions for Samsung Electronics, as the current qualification progress for HBM4 at key customers has been going well and company management has been confident on the market share gain moving into 2H26.

- Sufficiency : On the HBM side, we believe the supply and demand balance will be tight this year, but with Rubin Ultra ramping up in late 2027 and under current capacity expansion plans, HBM might be in shortage moving into 2027. On the overall sufficiency of the DRAM industry, we model a -7-14% decline in smartphone, PC and consumer DRAM demand in 2026 but nearly 100% growth in server DRAM demand, based on our channel checks. As a result, our 2026 forecast commodity DRAM growth increases to 48% versus supply growth at 29%, and our total DRAM & HBM sufficiency ratio decreases to -17% from -4% in 2025e. Our 2027e forecasts for YoY growth in commodity DRAM supply (37%) and demand (32%) are based on our US Semiconductor team's WFE model forecast, together with our HBM forecast. For 2027e, we model sufficiency slightly improving to -15%

Al chip vendor

NVIDIA

AMD

AWS

Microsoft

Total

CoWoS capacity allocation

(k wafers)

Chips per

CoWos wafer shipments (k)

density (GB)

M

Exhibit 30: HBM supply and demand model

12

12

36

84

HBM chip HBM chip units Total HBM siz

Total HBM size

(GB)

36

8

36

24

24

36

8

6

8

288

288

141

192

288

HBM

generation

HBM3e 12hi

HBM4

HBM3e 8hi

HBM3

HBM3e 12hil

HBM vendor

Hynix/Micron/Samsung

Hynix/Micron/Samsung?

Hynix

Samsung

Samsung/Micron

Total HBM

demand

(k GB)

599,040

285,525

6,912

24,192

| Sufficiency estimates | 2023 | 2024 | 2025 | 2026e | 2027e |

|---|---|---|---|---|---|

| HBMTSV Capacity (K wpm) | |||||

| Samsung | 45 | 130 | 150 | 180 | 250 |

| SK Hynix | 45 | 120 | 150 | 200 | 250 |

| Micron | 3 | 20 | 60 | 100 | 110 |

| Total | 93 | 270 | 360 | 480 | 610 |

| Yield rate assumptions | |||||

| Samsung | 50% | 60% | 55% | 70% | |

| SK Hynix | 60% | 75% | 65% | 70% | |

| Micron | 50% | 70% | 65% | 70% | |

| UTR assumptions | |||||

| Samsung | 80% | 60% | 70% | 100% | |

| SK Hynix | 100% | 100% | 100% | 100% | |

| Micron | 100% | 100% | 100% | 100% | |

| Implied HBMproduction (mn Gb) | |||||

| Samsung | 1,500 | 4,435 | 6,387 | 9,696 | 21,239 |

| SK Hynix | 1,500 | 6,273 | 12,830 | 17,363 | 22,226 |

| Micron | 150 | 729 | 3,548 | 7,937 | 10,372 |

| Total | 3,150 | 11,436 | 22,765 | 34,997 | 53,837 |

| Sufficiency Ratio | |||||

| HBM Demand (mn Gb) | 1,866 | 9,059 | 19,516 | 34,205 | 56,085 |

| Commodity DRAM market demand (mn Gb) | 209,527 | 243,423 | 316,640 | 469,675 | 619,970 |

| Total HBM+DRAM demand (mn Gb) | 211,393 | 252,481 | 336,156 | 503,879 | 676,055 |

| Commodity DRAM market supply (mn Gb) | 200,214 | 228,086 | 301,257 | 382,107 | 519,666 |

| Total HBM+DRAM supply (mn Gb) | 203,364 | 239,523 | 324,022 | 417,104 | 573,503 |

| Total DRAM sufficiency | -4% | -5% | -4% | -17% | -15% |

Source: Company data, Morgan Stanley Research estimates

Product name

Implied

NVIDIA accounts for the largest share of HBM demand, and we expect this to continue in 2027 driven by its Rubin Ultra roadmap, which increases per GPU capacity to 1TB. Broadcom follows as TPU and MTIA volumes surge, while other incremental projects add smaller increases. Amazon also emerges as one of the top HBM customers, with an aggressive Trainium AI chip roadmap.

Exhibit 31: HBM - AI chip consumption in 2026

Source: Company data, Morgan Stanley Research estimates. Note: Estimates are compiled using our Asian supply chain checks.

M

LTAs could create a two-tier memory market

As top-tier CSPs secure multi-year supply through LTAs, the residual memory market could become structurally tighter. Customers without LTAs may need to procure from a smaller pool of uncommitted supply, potentially at higher and more volatile prices. We view this as a potential structural cost borne by every buyer who is not at the front of the LTA queue.

Historically, weak PC or smartphone demand would help loosen DRAM markets and lower prices for everyone. In this cycle, AI demand keeps allocation tight even if consumer electronics demand softens, because HBM and server applications now set the priority order, and supplier incentives reinforce the allocation. After the last memory downcycle, suppliers have limited incentive to flood the market with commodity supply when AI customers offer stronger pricing, better margins and more durable contracts.

We run DRAM sufficiency analysis on the two largest non-server end markets: PCs and smartphones

Starting from total 2027 DRAM + HBM supply of 573,503mn Gb, we allocate 70% to servers and 30% to non-server applications. Within non-server, we assign 17% to PCs and 58% to smartphones, consistent with historical patterns. On the PC side, bottom-up demand of 34,386mn Gb implies a shortfall of 5,138mn Gb (-15%). The picture is comparably challenging for smartphones: total smartphone DRAM demand of 113,125mn Gb against an addressable supply of 99,790mn Gb produces a 13,335mn Gb gap (-12%).

The shortfall proves highly sensitive to content assumptions. On the PC side, our base case of 89Gb per device implies a -15% shortfall; holding content flat year-on-year at 83Gb narrows this to -9%, and de-speccing to 77Gb reduces it to just -2%. Smartphones follow the same pattern: against a 99Gb base case (-12%), flat content at 95Gb narrows the gap to -7%, and de-speccing to 90Gb brings it to - 2%.

The read-through is twofold. First, the unit-volume risk is a function of memory content assumptions, not an absolute supply wall - OEMs have a clear lever to protect shipment volumes. Second, that lever is not free: every gigabyte of de-speccing that protects unit volumes is a gigabyte of forgone content growth, so the adjustment ultimately resolves the unit shortfall by suppressing memory bit demand. The market clears either through fewer devices or lower memory intensity per device - and the more likely outcome is a blend of the two.

This reinforces supplier pricing power and changes the cycle. The more supply is committed to strategic AI customers, the less flexible supply remains for opportunistic or non-LTA buyers. This could support ASP resilience even if parts of consumer demand weaken.

M

Exhibit 32: Our memory sufficiency framework suggests PC and smartphone could see 12-15% memory shortfall

| PC memory sufficiency in 2027 | |

|---|---|

| Total DRAM + HBM supply (mn Gb) | 573,503 |

| Server gets 70% of allocation | 401,452 |

| Non-Server gets 30% of allocation | 172,051 |

| PC gets 17% of non-server allocation | 29,249 |

| Total PC memory demand (mn Gb) | 34,386 |

| Shortfall (mn Gb) | (5,138) |

| -15% | |

| Memory content per device (Gb) | 89 |

| Shortfall (mn units) | (58) |

| vs. MS PC shipment forecast | 388 |

| Downside vs. MSe | -15% |

Sensitivity analysis

| Smartphone memory sufficiency in 2027 | |

|---|---|

| Total DRAM + HBM supply (2027) | 573,503 |

| Server gets 70% of allocation | 401,452 |

| Non-Server gets 30% of allocation | 172,051 |

| Smartphone gets 58% of non-server allocation | 99,790 |

| Total smartphone demand (2027) | 113,125 |

| Shortfall (mn Gb) | (13,335) |

| -12% | |

| Memory content per device (Gb) | 99 |

| Shortfall (mn units) | (134) |

| vs. MS smartphone forecast | 1,137 |

| Downside vs. Mse | -12% |

Sensitivity analysis

| Memory content per device (Gb) | Shortfall | Memory content per device (Gb) | Shortfall | Shortfall | |

|---|---|---|---|---|---|

| Current assumption | 89 -15% | Current assumption | 99 | -12% | |

| Flat content YoY | 83 | -9% | Flat content YoY | 95 | -7% |

| De-specing | 77 | -2% | De-specing | 90 | -2% |

Source: Morgan Stanley Research estimates. Note: PC includes Laptops, desktops and tablets

Exhibit 33: AI prioritization turns 2027 supply growth into a consumer memory shortfall

Source: Morgan Stanley Research estimates

allocation

M

Chipflation Passthrough and Sector Impact

Erik Woodring, Shawn Kim

The current memory cycle is being driven by a structural reallocation of wafer capacity and supplier attention toward AI-related demand. This memory shortage is reshaping PC and smartphone markets as suppliers prioritize higher-value AI/ server demand over lower-margin consumer applications. This is already translating into end-demand risk.

We now expect surging memory costs to lower 2026 PC shipments by 10%+ and smartphone shipments by 13% versus 2025, with memory and SSD price inflation driving higher device prices and demand increasingly skewing toward premium devices.

There are long-term ramifications too - device redesigns, a structural shift in unit economics, industry consolidation, and a re-evaluation of the workload mix onprem versus in the cloud.

Buyer-seller matrix: who gets priority?

The buyer-seller map is shifting from a commodity market to an allocation market. On the supply side, Samsung, SK hynix and Micron dominate advanced DRAM and HBM, with CXMT increasingly relevant in DRAM capacity additions. In NAND and enterprise SSDs, the key suppliers include Samsung, KIOXIA/SanDisk, SK hynix/Solidigm, Micron and YMTC.

On the buyer side, hyperscalers, AI infrastructure providers and GPU/accelerator ecosystems are the most strategic customers for HBM, high-density server DRAM and enterprise SSDs. These buyers are more likely to receive priority allocation because they offer scale, roadmap visibility and willingness to commit through LTAs - and as a result, they sit at the front of the allocation queue. Traditional consumer and industrial buyers are more exposed: PC OEMs, smartphone OEMs, gaming console makers, networking companies, automakers, industrial firms, medical device makers and smaller hardware companies all rely on DRAM, LPDDR and NAND, but have weaker bargaining power than Al/cloud customers.

The strategic tension is that upstream supply is concentrated while downstream demand is broad. When AI customers move to the front of the allocation queue, the remaining markets face tighter access and higher price volatility.

cxlbl6or. buyer thelaruly. Vhlu yelo memory supply mol!

Allocation stack

M

Exhibit 34: Buyer Hierarchy: Who gets memory supply first?

Tier 4 | Autos / networking / industrial/ medical | DDR, NAND, specialty I qualified supply

Source: Morgan Stanley Research

Exhibit 35: Memory demand is overwhelmingly shifting towards data center technologies and away from more consumer-facing Smartphone and PC markets

Source: TrendForce estimates, Morgan Stanley Research

Sector impact and passthrough - where the pain lands

Memory inflation is becoming a broad hardware-sector margin risk , extending beyond PCs and smartphones into gaming consoles, servers, cloud, networking, autos, medical devices, broadband equipment, industrial systems and low-cost education/embedded devices. The issue is not only higher DRAM/NAND pricing, but also allocation priority: suppliers are prioritizing HBM, server DRAM and enterprise SSD demand tied to AI infrastructure, while conventional consumer and industrial memory users are increasingly exposed to higher prices, longer lead times and weaker bargaining power.

On a gross cost basis, servers and cloud and PCs are among the most exposed. But on net margin impact after passthrough, the most impacted sectors are different: midrange and low-end PCs, low-end smartphones, consumer electronics, gaming consoles, embedded and education devices, and smaller industrial OEMs ( Exhibit 36 ). While it is difficult to predict whether historical demand elasticity will repeat this cycle given such significant price hikes, our quant analysis would paint a similar picture: low/mid-range PCs and smartphones face relatively elastic demand responses and thus face more significant net margin risk than enterprise infrastructure, where demand is much more inelastic with relatively more margin protection ( Exhibit 38 ). These more consumer-led end markets combine higher memory BOM exposure with weaker pricing power and higher demand elasticity.

M

Exhibit 36: Consumer electronics companies continue to call out margin pressures relating to memory cost inflation

| Consumer Electronics Commentary on Memory Cost Inflation Pressures | Consumer Electronics Commentary on Memory Cost Inflation Pressures | Consumer Electronics Commentary on Memory Cost Inflation Pressures |

|---|---|---|

| Source | Commentary | Date |

| HP Inc | " Looking ahead, we expect the memory and storage environment to remain constrained. In addition, we also anticipate broader inflationary pressures beyond memory and storage. " | 27-May-26 |

| Xiaomi | "I think given the cost increase, pressure will continue . That is an objective fact. So we need to solve this problem. We need to balance scale, profit and also gross margin... We cannot simply pass the cost increase to consumers. Given the new cost structure, we need to make sure that users are happy with the value for money." | 26-May-26 |

| ASUSTeK Computer | "Due to the AI server boom, supply for both memory and CPUs have become very tight. And furthermore, we're seeing that memory shortages, in particular, and those price hikes have been extreme for the past few quarters ... So I think that it's important to note that both memory and CPU are undergoing both supply shortages and price hikes. " | 12-May-26 |

| GoPro | "Macro challenges in the consumer electronics sector, including rising memory costs , supply chain constraints and fluctuating tariffs prompted us to take some discrete actions in the quarter that impacted gross margins and earnings per share for the period. " | 11-May-26 |

| Sony | "Of course, the memory prices going up would increase the cost of the BOM . So the cost of manufacturing will go up. And if that leads to passing on cost to prices, there would be a big impact on the gaming console prices ." | 8-May-26 |

| Fractal Gaming Group | "We are seeing a significant market decline across regions ... driven by a global imbalance in the memory market, where increased investments in AI and data centers have redirected capacity from the end consumer market and thereby driven up prices for DRAM and NAND memory. This has significantly increased the cost of building a PC with memory now accounting for a much larger share of the total system cost , at times even exceeding the CPU. As a result, we are seeing more cautious consumer behavior with many customers delaying or scaling back upgrades, which is directly impacting | 7-May-26 |

| Logitech | "We are working to make sure that we get as much memory as possible to protect our video conference portfolio. So whatever we can get, we get it, and that may impact the inventory turns. So don't expect -don't model greater than 100% [cash conversion] every quarter in fiscal year '27. " | 5-May-26 |

| Sonos | "Looking to the second half and beyond, we're managing the headwind of higher memory costs, which are putting downward pressure on our gross margin. As you know, the semiconductor industry is in the middle of a transition from DDR4 to DDR5 and high-bandwidth memory, driven by AI and data center demand. That is tightening the supply for the DDR4 chips we use and increasing costs across consumer electronics ." | 4-May-26 |

| Apple | "We said it would be a bit more in the March quarter, and we did see higher memory costs in the March quarter , and they were partially offset by benefits from carry-in inventory that we had. For the June quarter and what's embedded in the guidance that Kevan went through earlier, we expect significantly higher memory costs . They are also partly offset by the benefit of carry-in inventory. And then where we don't give color beyond June, I can tell you that beyond the June quarter, we believe memory costs will drive an increasing impact on our business ." | 30-Apr-26 |

| Samsung Electronics | "With the growing demand for AI server memory, memory supply shortages for mobile and upward trend in prices have persisted. In 1Q 2026, memory prices surged, weakening profitability year-on-year. Also in 2Q, prices are expected to rise further, adding to cost pressures. We will leverage our stable supply to expand sales of S26 and new A-Series. At the same time, across development, procurement and sales, we will enhance cost efficiency to mitigate the impact of rising memory prices on profitability." | 30-Apr-26 |

| LG Electronics | "For monitors, apart from certain smart monitor models, the impact from memory-driven price increases is minimal. For PCs, which have relatively high memory content, the industry is facing significant cost pressure. As a result, price increases of approximately 15% to 20% have already been implemented. Should the sharp rise in memory prices persist, additional price adjustments may become unavoidable. " | 29-Apr-26 |

| Best Buy | "For next year, our guide for gross profit is about 30 basis points increase year-over-year... there could be some categories, some pressure on margins because of memory costs …there could be unique areas within computing that might have some impact. " | 3-Mar-26 |

Source: Company Data, Morgan Stanley Research (emphasis added)

Exhibit 37: We estimate that memory accounts for 5-70% of tech hardware products, with servers and PCs more exposed to DRAM while storage is over-indexed to NAND

Memory as a % of BOM (Pre-Memory Inflation)

Server

Source: Company Data, Morgan Stanley Research estimates

M

Exhibit 38: Our quant analysis implies low-end smartphones and PCs are the most demand elastic, while servers, storage and high-end smartphones are least at risk of demand destruction from higher prices

Demand Elasticity by Hardware Product

Source: IDC, Company data, AlphaWise, Morgan Stanley Research. Demand elasticity takes the absolute value. PC data goes back to 1995, for storage it starts in 2008, servers in 2003 and smartphones in 2007.

Accounting asymmetry matters

A less obvious transmission mechanism for chipflation is accounting treatment, disproportionately impacting companies that are not directly monetizing Al but still have to pay Al-driven memory prices. This creates an accounting asymmetry: hyperscalers can capitalize memory-heavy AI servers and depreciate them over time, while consumer hardware and industrial OEMs see memory inflation flow more directly through inventory and COGS.

The same memory price shock can therefore look like strategic capex for one buyer and immediate gross-margin pressure for another. This is one of the most under-discussed transmission mechanisms of chipflation in the current cycle.

The capability cost: what doesn't get built

Memory inflation is not just a financial transfer from non-Al sectors to memory producers. It is increasingly a constraint on what gets built and when.

For automakers, memory costs are pushing back ADAS rollouts and compressing EV program economics. GM has raised its 2026 commodity and logistics inflation guide by $1bn-2bn, citing higher DRAM costs among the drivers.

- Magna expects more pricing tension at the vehicle level if DRAM costs remain elevated.

- Visteon's memory supply is constrained through 2027, and the company is qualifying emerging suppliers for 2026+ demand.

For healthcare and medical devices, the impact is more diffused but the challenge is real.

- GE HealthCare flagged ~$100m of a $250m inflation headwind tied to chip and cost actions.

- Siemens Healthineers said the EPS impact could reach €0.05 due to supply-chain

M

inflation including memory chips.

- Intuitive Surgical noted gross-margin pressure including roughly 100bps of impact from tariffs, freight, and semiconductor memory costs.

For the indirect channel - the largest and least visible - every enterprise running workloads on AWS, Azure or GCP is exposed to chipflation through its cloud bill. A bank running fraud detection, a logistics firm running route optimization, a retailer running inventory analytics: all are paying memory inflation indirectly without recognizing it as a memory cost. This is the channel with the broadest economic footprint, and the channel that is hardest to see in any individual company's filings.

Exhibit 39: Memory impact heat-map by end market

| End market | Memoryavailability / allocation priority | Cost impact | Pass-through ability | Demanddestruction / pull- forward risk | Majorcompany commentary / impact one-liners |

|---|---|---|---|---|---|

| Hyperscalers / AI data centers | Highest priority -suppliers are optimizing for AI/HBM, server DRAM, enterprise SSDs | Very high, but strategic | High | Low | Meta: raised 2026 capex to $125-145bn, partly due to higher component costs, especially memory. Amazon: said memory/storage component costs have 'skyrocketed,' but large cloud buyers are better positioned to secure supply. |

| Enterprise servers / storage | High priority -large server OEMs get allocation, but at sharply higher prices | Very high | High | Low-medium | HPE: DRAM/NAND are now over half of traditional server BOM, with elevated pricing expected into 2027; using shorter quote cycles, repricing rights, LTAs and alternative configs. Dell: using shorter quote validity and dynamic pricing; flagged some pull-forward risk. |

| Semiconductor equipment | Medium -supply likely manageable, but not immune to electronics BOMinflation | Medium | Medium-high | Low | KLA: e xpects elevated memory pricing through at least calendar 2026 and about 100 bps negative gross-margin impact over the next several quarters. |

| Networking / security appliances | Medium-high for large vendors; weaker for smaller appliance makers | Medium-high | Medium-high | Low-medium | Cisco: immediate price increases across memory-heavy compute/networking products. Check Point: enough inventory for H1 but H2 margin headwind. Radware: 5-8% list-price increases on memory-intensive hardware; no buying-behavior change seen yet. |

| PCs / notebooks | Medium -tier-1 OEMs have some allocation, but PC DRAMis not top priority versus AI/server | High | Medium-high | High in entry/mainstream PCs | HP: memory/storage moved to ~35% of PCBOMfrom15-18%, with LTAs, supplier diversification and price increases. Lenovo: said DRAMrose 40-50% in one quarter and almost doubled again, calling the imbalance structural. Acer/ASUS: passing higher memory costs into PCpricing; potential spec cuts such as 16GB to 8GB if pressure persists. LG PC: already seeing 15-20% price increases. |

| Smartphones | Medium -Apple/Samsung can secure supply, but low- end Android is lower priority | Medium-high | Medium at premium; low low end | High at low end; lower at premium end | Apple: memory becomes a more visible gross-margin headwind from the June quarter and increases beyond that. Xiaomi: secured 2026 memory supply but warned shortages could push smartphone prices higher. Samsung : memory division benefits from higher ASPs, while handset-side memory cost pressure is less separately quantified in official commentary. |

| Gaming consoles | Medium -large platform owners can secure supply, but consoles compete with higher-margin AI/server demand | High | Medium | Medium-high | Nintendo: built around ¥100bn of FY27 COGSimpact from rising component prices, especially memory, plus tariffs; also raised Switch 2 prices in Japan, the U.S. and Europe. Sony: secured minimum memory supply for the next holiday season, but did not fully quantify the cost impact. |

| TVs / monitors / home electronics | Medium-low -lower memory content, less priority than servers/PCs/phones | Low-medium | Medium | Low-medium | LG Electronics: TV memory content is relatively low, monitor impact is limited except smart monitors, but PCs are meaningfully exposed; mitigation includes supply MOUs, multi-sourcing, spec optimization and premium mix. Canon: mostly secured memory supply but faced an estimated ~¥50bn negative memory- |

| Cameras / imaging | Medium-low -discretionary hardware, less supplier priority than AI/server/PC/phone | Medium-high | Low-medium | Medium-high | cost impact and guidance pressure. Nikon: secured volumes, but DRAMcosts rose severalfold and could create a high-single- digit-billion-yen operating-profit hit. Fujifilm: flagged semiconductor memory and silver as cost pressures, with pricing and offsets planned. |

| Autos / auto electronics | Medium -automotive volumes are smaller, specs are specialized, and 2027 supply security is a focus | Medium | Medium, but lagged | Low near term; medium if prolonged | GM: raised commodity/logistics inflation guide, including higher DRAMcosts, to $1.5-2.0bn. Ford: expects sufficient DRAMsupply but sees pricing pressure that may affect vehicle pricing. Magna: more a price issue than availability issue; annualDRAMbuy under $100m. Visteon: memory remains constrained through 2027; qualifying emerging suppliers for ~10% of 2026 demand and negotiating customer recoveries. Renesas: automotive DRAMvolumes not large, but DDR4/DDR5 compatibility matters. |

| Healthcare / medtech | Medium -mission-critical products and largerOEM scale help, but memory is still a cost shock | Medium | Medium-high, but lagged | Low | GEHealthCare: memory chips were about $100m of a $250m inflation headwind, partly offset by price and cost actions. SiemensHealthineers: cut EPS midpoint by around €0.05 due to supply-chain inflation including memory chips. Intuitive Surgical: gross-margin guide includes about 100 bps of impact from tariffs, freight and semiconductor memory costs. |

| Defense / aerospace | Low-medium -lower- volume, long-life, rugged/legacy memory can be vulnerable | Medium-high where DDR4/legacy-heavy | Medium-high structurally, but lagged | Low | AeroVironment: disclosed lead-time and price uncertainty for memory-related microprocessors. JLT Mobile: DDR4 prices up more than 10x and lead times longer; secured 2026 supply through early purchases. Nexteq / Ependion: DDR4/memory availability is a key 2026 risk, mitigated by LTAs and price increases. |

Source: Company data, Morgan Stanley Research

M

The chipflation impact in dollars

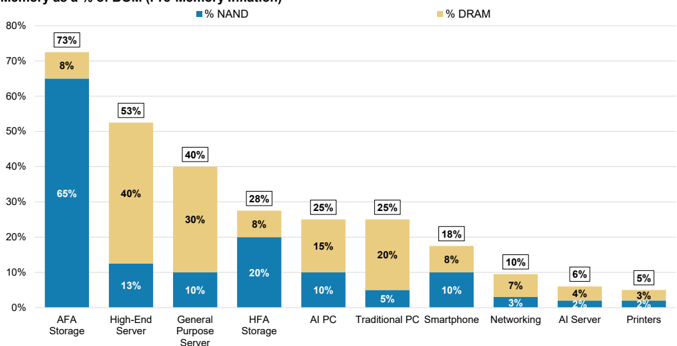

Memory cost inflation has become large enough to matter at the industry level. While it varies greatly by product, nearly every hardware product - a PC, server, storage array, smartphone, etc. - has some combination of NAND and DRAM content, which we estimate makes up anywhere between 5% of a device bill of materials (printers) to 70% (high-end servers). Simplistically, higher-end, more performance-based products such as All-Flash storage arrays, high-end & traditional servers, higher-end PCs, and AI servers all have 2570%+ NAND/DRAM mix within their product bill of materials. Conversely, products such as printers or networking hardware are generally lighter on memory content. Nevertheless, this means that most hardware OEMs and ODMs are over-exposed to memory markets, especially those with high-end device exposure ( Exhibit 37 ).

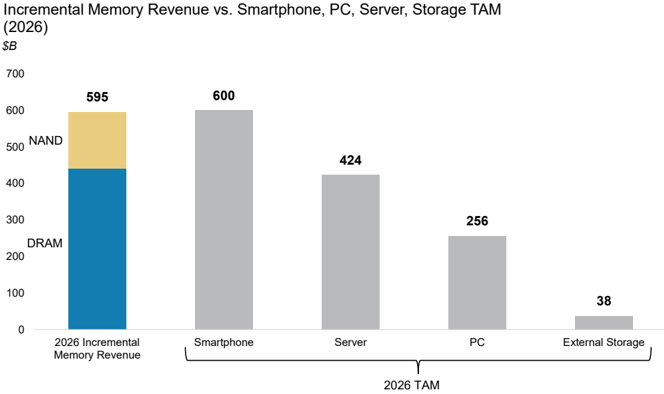

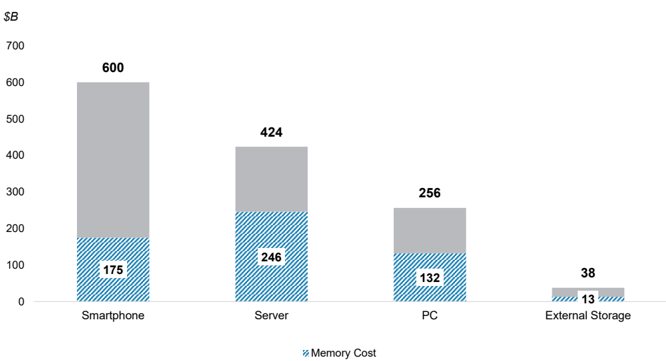

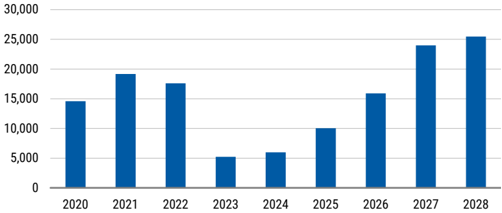

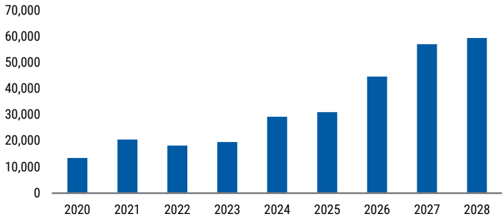

The memory market is expected to add more Y/Y revenue in 2026 (~$600B) than the entire standalone smartphone, PC, or server TAMs. To put the overall impact of memory inflation into perspective, in just the last 3 months, expectations for aggregate memory market revenue in 2026 have increased by 71%, from $520B to $890B, relative to a $220B market in 2025. Not only are memory buyers facing an incremental $300B of standalone memory costs this year - equivalent to the annual GDP of Finland or New Zealand - but the memory market is expected to add more Y/Y revenue in 2026 (~ $600B) than the entire standalone smartphone, PC, or server TAMs ( Exhibit 40 ). This will show up in 2026 as COGS or Capex for memory buyers. In aggregate, the global hardware industry must now contend with incremental memory costs that equate to over half of the $1.3T aggregate hardware TAM, with our estimation at the industry level suggesting the highest dollar burden is on Servers at $246B, followed by Smartphones at $175B, PCs at $132B, and External Storage at $13B.

Exhibit 40: Based on latest industry estimates, memory revenue will increase by $600B in 2026 ...

Source: TrendForce estimates, IDC data, Morgan Stanley Research

M

Exhibit 41: … which we estimate translates into ~$600B of incremental memory cost across Smartphone, Server, PC, and External Storage markets

Incremental Memory Cost & TAM by Market (2026)

Source: TrendForce, IDC, Morgan Stanley Research estimates

This does not mean that every hardware company faces a direct margin hit of the same magnitude. The chipflation burden will be distributed across hyperscalers, OEMs, component suppliers, distributors, enterprises and end-customers. But the order of magnitude matters: the memory supercycle is large enough to force some combination of price increases, margin pressure, specification cuts, product delays, budget reallocation and demand destruction. For hyperscalers, higher memory costs is being absorbed as strategic AI capex. For many non-AI hardware buyers, it is showing up as higher prices, COGS pressure, lower product specs, and/or delayed product launches/refresh cycles.

And in non-AI hardware markets scale matters. A vendor's ability to aggregate demand across multiple products (i.e. PC, server, storage) or come to market with exceptionally strong buying power (Apple, Samsung) makes a meaningful difference in getting memory allocations.

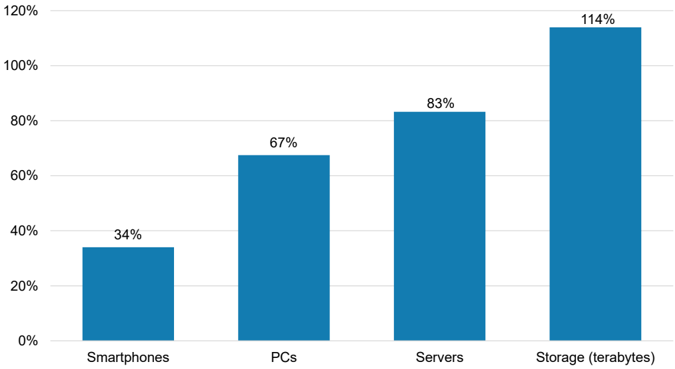

But even sufficient memory allocations come with a significant cost - higher prices across the hardware ecosystem. Using the latest TrendForce memory price forecasts, and making the assumption that hardware vendors will prioritize maintaining margin rates, we estimate like-for-like unit price hikes would have to be ~35% for Smartphones, ~70%+ for PCs, 80%+ for Servers and 110%+ for Storage arrays. This is the average though. Anecdotally, we are already hearing instances of significant price hikes - 100%+ in some cases in high-end Storage/Server markets, due to memory plus other semiconductor inflation (CPU, PCB, MLCC, etc.).

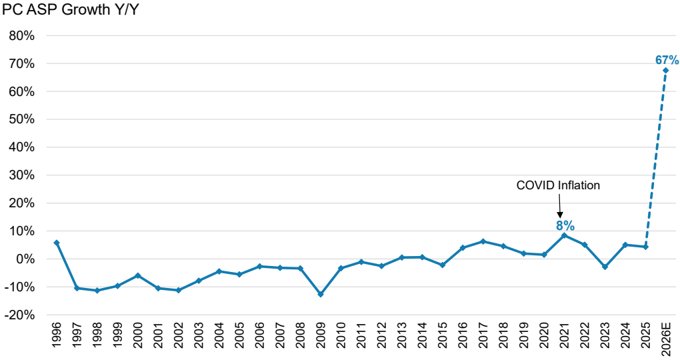

For context, these required pricing increases sit significantly above historical ASP behavior across virtually every major hardware category. PCs are the clearest example: over the past ~30 years, annual PC ASP growth has typically fluctuated within a +/-10% band, with even the strongest inflationary periods - including COVID-era supply constraints - driving aggregate pricing increases in the high-single digits Y/Y. In fact, if PC prices increase 67% Y/ Y this year, it would represent the strongest Y/Y ASP growth in PC market history by a magnitude of 8-9x ( Exhibit 43 ).

M

Exhibit 42: We estimate that in order to protect gross margins, hardware vendors would need to raise prices by 35-115% Y/Y in CY26

Y/Y ASP Growth Needed to Hold Gross Margins Steady

Source: TrendForce, IDC, Company Data, Morgan Stanley Research estimates

Exhibit 43: For context, if PC ASPs were to rise 67% Y/Y, it would mark the strongest Y/ Y ASP growth in PC market history, far surpassing COVID-era inflation

Source: IDC, Morgan Stanley Research

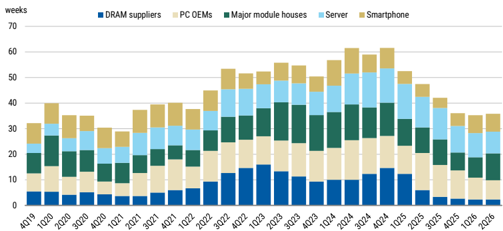

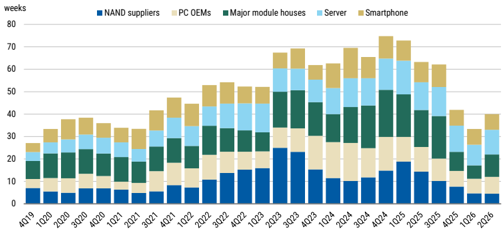

The timing of the impact is likely lagged. Many hardware companies are still working through lower-cost inventory, which can mask the near-term earnings impact. This explains why some memory-exposed companies can still beat current-quarter expectations while investors look ahead to margin risk in calendar 2H26 and beyond. However, memory inventory has depleted quickly across channels. As higher-priced memory flows through inventory and COGS, companies will need to choose whether to raise prices, cut specifications, delay launches or absorb margin pressure.

M

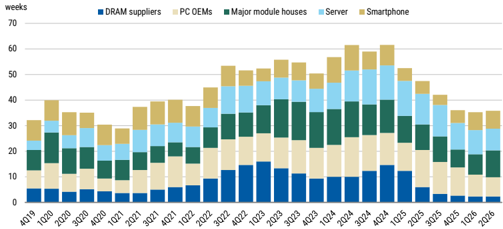

Exhibit 44: DRAM inventory

Source: TrendForce estimates, Morgan Stanley Research

Exhibit 45: NAND inventory

Source: TrendForce estimates, Morgan Stanley Research

Memory vs GPU cost convergence

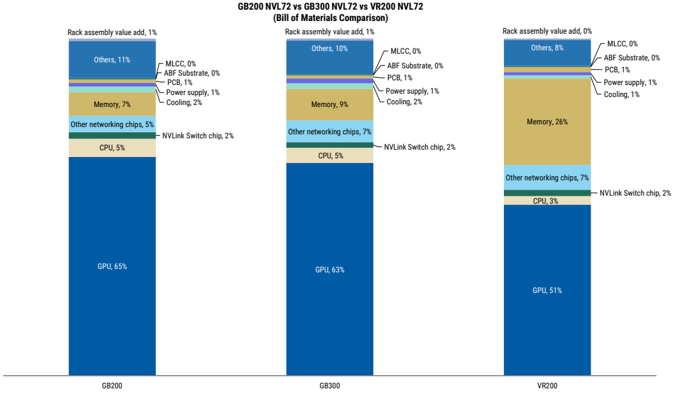

Memory is now 25%+ of a Rubin rack BOM. Our bottom-up Rubin rack BOM analysis

shows how large the memory cost has become inside AI infrastructure. Memory was only 5-10% of the GB200 NVL72 rack BOM, but with higher memory content and materially higher pricing, memory rises to roughly 25-30% of the VR200 / Rubin rack BOM. In the detailed BOM comparison, memory increases from $374k per GB300 rack to $2.0mn per VR200 rack, or +435%, making it the largest source of non-GPU cost inflation.