PDF 原檔:報告_MS_貿聯_20260706_original.pdf

圖片清單(已驗證 2026-07-07)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源;嵌入時只從這裡挑分類為「真資料圖」的。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260706_ms_bizlink_001.png |

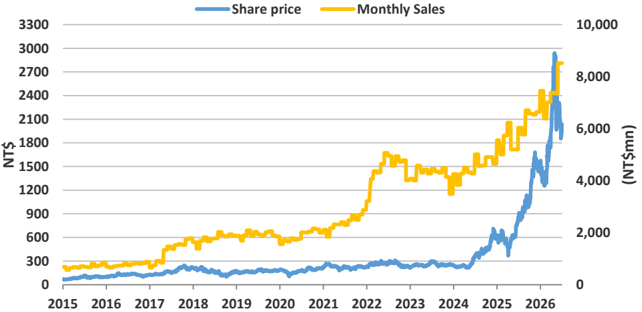

53KB | 真資料圖 | 貿聯月營收(黃線,右軸 NT$mn)vs 股價(藍線,左軸 NT$),2015 至 2026,兩者 2025-2026 急速攀升 |

260706_ms_bizlink_002.png |

66KB | 裝飾·logo·banner | "Asia Summer School 2026" 泳池背景 banner |

260706_ms_bizlink_003.png |

62KB | 真資料圖 | 貿聯股價(藍實線)與 MS 目標價歷史(紅虛線階梯),Jul-23 至 Jul-26,目標價從 336.49 步升至 3,665 |

原始內容

M July 6, 2026 02:51 PM GMT

Bizlink | Asia Pacific

June Sales +16% MoM/+64% YoY

In this report, we focus on Bizlink's monthly sales, which we believe could be a catalyst for its share price.

Details:

- June sales came in at NT$8,518mn (+16% MoM/+64% YoY).

- 2Q26 revenue reached NT$23,253mn (+11% QoQ/+40% YoY), slightly above both Mse of NT$22,836mn (+9% QoQ/+35% YoY) and consensus at NT $22,849mn (+10% QoQ/+35% YoY) by 2%.

Our view:

- We maintain our view that the lower 28.8% gross margin in 1Q26 was temporary and that the revenue mix normalized in 2Q26. As a result, we believe gross margin likely recovered to above 30% in 2Q26.

- Looking ahead, power interconnects should benefit from server rack shipment growth in 2026, while higher dollar content from next-generation GPU servers and HVDC architecture should emerge primarily from 2027.

- Meanwhile, data interconnects should continue to grow on broader AEC adoption through 2026-27, with potential incremental contributions from optical solutions (e.g., shuffle box, ALC) from 2027.

- We remain constructive on Bizlink as an AI beneficiary, driven by its data interconnect, power interconnect, and semiconductor equipment businesses. Maintain OW.

Exhibit 1 : Bizlink's monthly sales vs. its share price since 2015

Note: Past performance is no guarantee of future results. Results shown do not include transaction costs. Source: Company data, TEJ, Morgan Stanley Research.

Morgan Stanley Taiwan Limited+

Derrick Yang

Equity Analyst

Derrick.Yang@morganstanley.com

+886 2 2730-2862

Vivi Huang

Research Associate

Vivi.Huang@morganstanley.com

+886 2 2730-2860

Morgan Stanley Asia Limited+

Andy Meng, CFA

Equity Analyst

Andy.Meng@morganstanley.com

+852 2239-7689

Bizlink (3665.TW, 3665 TT)

Greater China Technology Hardware | Taiwan

| Stock Rating | Overweight |

|---|---|

| Industry View | In-Line |

| Price target | NT$3,665.00 |

| Up/downside to price target (%) | 88 |

| Shr price, close (Jul 6, 2026) | NT$1,945.00 |

| 52-Week Range | NT$3,010.00-808.00 |

| Sh out, dil, curr (mn) | 193 |

| Mkt cap, curr (mn) | NT$376,097 |

| EV, curr (mn) | NT$381,673 |

| Avg daily trading value (mn) | NT$5,805 |

| Fiscal Year Ending | 12/25 | 12/26e | 12/27e | 12/28e |

|---|---|---|---|---|

| EPS (NT$)** | 46.57 | 63.77 | 120.77 | 143.77 |

| EPS (NT$)§ | 47.71 | 67.27 | 109.42 | 144.28 |

| Revenue, net (NT$ mn) | 71,247 | 97,108 | 149,307 | 173,575 |

| EBITDA (NT$ mn) | 15,154 | 19,697 | 34,427 | 41,565 |

| ModelWare net inc (NT | 9,005 | 12,331 | 23,352 | 27,800 |

| $ mn) | ||||

| P/E | 32.6 | 30.5 | 16.1 | 13.5 |

| P/BV | 6.4 | 6.8 | 5.1 | 4.0 |

| RNOA (%) | 24.2 | 24.1 | 40.5 | 42.1 |

| ROE (%) | 24.9 | 26.4 | 41.6 | 36.8 |

| EV/EBITDA | 20.1 | 19.2 | 10.7 | 8.4 |

| Div yld (%) | 0.8 | 0.8 | 1.1 | 2.0 |

| FCF yld ratio (%)** | (0.8) | 1.9 | 3.7 | 6.4 |

| Leverage (EOP) (%) | (0.9) | (8.0) | (18.9) | (32.3) |

Unless otherwise noted, all metrics are based on Morgan Stanley ModelWare framework

** = Based on consensus methodology

§ = Consensus data is provided by Refinitiv Estimates

e = Morgan Stanley Research estimates

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.