PDF 原檔:報告_JPM_Ibiden4062_20260715_original.pdf

圖片清單(已驗證 2026-07-17)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

JPM_Ibiden__4062__Revisi_2026-07-15_5357892_008.png |

72KB | 真資料圖 | 股價與歷次目標價沿革圖:藍線為股價(Y軸 Price(Y),2023/9-2026 中),標註歷次評等與目標價(OW ¥5,350/OW ¥4,500/OW ¥4,200/N ¥3,250/OW ¥6,450/OW ¥7,000/OW ¥10,200/OW ¥18,400),股價 2025 下半年後急拉升至約 2萬多 |

JPM_Ibiden__4062__Revisi_2026-07-15_5357892_002.png |

55KB | 真資料圖 | Figure 1:12個月 forward 一致預期 P/E(Ibiden Consensus P/E T+1 Forward,深灰線,左軸 0-60x)與相對族群 P/E(藍線,右軸 0-3.0x)走勢圖,橫軸 2016/08-2026/07,2025 年後兩線皆明顯上揚至近期高點 |

JPM_Ibiden__4062__Revisi_2026-07-15_5357892_003.png |

52KB | 真資料圖 | Figure 2:12個月 forward 一致預期 P/B(深灰線,左軸 0-10.0x)與相對族群 P/B(藍線,右軸 0-4.0x)走勢圖,橫軸 2016/08-2026/07,同樣近期急升至近8x |

JPM_Ibiden__4062__Revisi_2026-07-15_5357892_004.png |

52KB | 真資料圖 | Figure 3:24個月 forward 一致預期 P/E(深灰線,左軸 0-40.0x)與相對族群 P/E(藍線,右軸 0-2.5x)走勢圖,橫軸同上,近期同步上揚 |

JPM_Ibiden__4062__Revisi_2026-07-15_5357892_005.png |

52KB | 真資料圖 | Figure 4:24個月 forward 一致預期 P/B(深灰線,左軸 0-7.0x)與相對族群 P/B(藍線,右軸 0-3.5x)走勢圖,橫軸同上,近期同步上揚 |

JPM_Ibiden__4062__Revisi_2026-07-15_5357892_006.png |

446KB | 文字卡 | Excel 財務模型截圖(Figure 5 損益/部門拆分表格畫面截圖,非圖表視覺化,數字已列於原始內容表格中) |

JPM_Ibiden__4062__Revisi_2026-07-15_5357892_007.png |

481KB | 文字卡 | Excel 財務模型截圖(Figure 8 損益表細項畫面截圖,非圖表視覺化,數字已列於原始內容表格中) |

JPM_Ibiden__4062__Revisi_2026-07-15_5357892_001.png |

37KB | 裝飾·banner | J.P. Morgan Quant style/performance driver 版面裝飾圖(未 Read,<40KB 預設) |

原始內容

Quant

Factors

Value

Growth

Momentum

Quality

Low Vol

Current

29

5

Hist %Rank (1=Top)

47

29

5

14

25

34

72

98

72

27

72

63

72

Ibiden (4062) 89

Revising up our earnings forecasts, maintaining our bullish stance; Ibiden benefiting from higher demand for ABF substrates for GPU, EMIB-T, and ASIC

We change the time horizon of our price target from December 2026 to December 2027. We raise our December 2027 price target from ¥18,400 to ¥28,500 and reiterate our Overweight rating. Although the company raised its medium-term management plan (MTP; FY2023-27) targets at FY2025 results, its top-line assumptions for substrates for GPUs and EMIB-Ts seem cautious. At present, our assumption is that capacity will be tight from 2H FY2029, and if the company announces the construction of new facilities at the Gama and Ono Plants or the acquisition of external fabs, we think earnings will rise even higher above the MTP targets in FY2029-30. We believe the company will fully benefit from growing demand for AI servers, not only with substrates for GPUs and EMIB-T but also with the expansion of its standard ABF substrates for ASIC applications (we expect this from FY2028 onward). Furthermore, we still anticipate growth in the number of substrates for servers for Agentic AI. While Ibiden's share price has fallen sharply from its recent peak due to the recent risk-off sentiment toward AI-related stocks, we maintain a bullish stance since the company is in a solid position with regard to fundamentals, amid ongoing advancements in its substrate technology.

- Earnings forecasts: We revise up our earnings forecasts in light of FY2025 results and current demand trends (we change our forex assumption from ¥152/ US$ to ¥155/US$). We revise up our operating profit forecasts from ¥81.0 billion to ¥115.6 billion for FY2026 (guidance: ¥90.0 billion; Bloomberg consensus estimate: ¥100.8 billion), from ¥97.5 billion to ¥156.9 billion for FY2027 (Bloomberg consensus estimate: ¥154.9 billion), from ¥172.1 billion to ¥209.4 billion for FY2028 (¥224.7 billion), and from ¥224.4 billion to ¥319.9 billion for FY2029, and we newly add a forecast of ¥392.6 billion for FY2030. The MTP targets sales of ¥650 billion and operating profit of ¥150 billion in FY2027 and sales of over ¥1 trillion and operating profit of over ¥300 billion in FY2030. However, guidance strikes us as cautious, particularly for substrates for EMIB-T and GPU applications. If there are additional investments to increase capacity, we think there will be room for significant upside over the FY2030 MTP targets.

Overweight

4062.T, 4062 JP Price (15 Jul 26):¥19,340

▲Price Target (Dec-27):¥28,500 Prior (Dec-26):¥18,400

Japan Equity Research

Technology - Electronic Components

Akinori Kanemoto AC

(81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

Ikki Shibata

(81-3) 6736 8641 ikki.shibata@jpmorgan.com JPMorgan Securities Japan Co., Ltd.

| Key Changes (FYE Mar) | Key Changes (FYE Mar) | Key Changes (FYE Mar) | Key Changes (FYE Mar) |

|---|---|---|---|

| Prev | Cur | Δ | |

| Adj. EPS - 27E (¥) | 190.00 | 271.71 | 43.0% |

| Adj. EPS - 28E (¥) | 229.08 | 369.74 | 61.4% |

Style Exposure

Frice Ferrormance

Ferormance Univers

30k

J.P. Morgan

Market

20k

*

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

10k

0

Factors

Market: MSCI Japan

Macro:

Quant Styles:

LowVol

Value

DivYld

Oct 25

Jan 26

Apr 26

6M Corr

0.52

0.59

41%

1Y Corr

0.47

Jul 26

0.64

— TOPIX (rebased)

YTD

187.3%

167.4%

Abs

Rel

1m

-15.0%

-17.2%

3m

106.2%

97.8%

12m

501.2%

456.5%

| Company Data | |

|---|---|

| Shares O/S (mn) | 279 |

| 52-week range (¥) | 27,500-3,029 |

| Market cap ($ bn) | 33.3 |

| Exchange rate | 162.25 |

| Free float (%) | 88.6% |

| 3M ADV (mn) | 8.58 |

| 3M ADV ($ mn) | 1,005.5 |

| Volatility (90 Day) | 105 |

| Index | TOPIX |

| BBG ANR (Buy | Hold | Sell) | 13|3|1 |

Key Metrics (FYE Mar)

| ¥ in millions | 2026/3A | 2027/3E | 2028/3E | 2029/3E |

|---|---|---|---|---|

| Financial Estimates | ||||

| Revenue | 416,201.0 | 534,406.0 | 645,931.0 | 750,071.0 |

| EBITDA | 128,263 | 196,422 | 254,317 | 316,441 |

| EBIT | 62,027.0 | 115,621.8 | 156,916.8 | 209,440.8 |

| Net income | 63,713 | 80,312 | 109,289 | 146,056 |

| Reported EPS | 215.6 | 271.7 | 369.7 | 494.1 |

| BBG EPS | 192.61 | 248.24 | 369.09 | - |

| Cashflow from operations | 77,016 | 232,667 | 388,993 | 408,566 |

| FCFF | 11,047 | 20,980 | 87,306 | 136,879 |

| Margins and Growth | ||||

| Revenue Growth Y/Y (%) | 12.7% | 28.4% | 20.9% | 16.1% |

| EBIT margin | 14.9% | 21.6% | 24.3% | 27.9% |

| EBIT Growth | 30.3% | 86.4% | 35.7% | 33.5% |

| EBITDA margin | 30.8% | 36.8% | 39.4% | 42.2% |

| EBITDA Growth Y/Y (%) | 26.0% | 53.1% | 29.5% | 24.4% |

| Net margin | 15.3% | 15.0% | 16.9% | 19.5% |

| Fully Diluted EPS growth | 89.0% | 26.1% | 36.1% | 33.6% |

| Ratios | ||||

| Effective Tax Rate | 29.6% | 30.0% | 30.0% | 30.0% |

| Interest cover | NM | NM | NM | NM |

| Net debt/Equity | NM | NM | NM | NM |

| Net debt/EBITDA | NM | NM | NM | NM |

| ROE | 12.2% | 13.7% | 16.4% | 18.8% |

| Valuation | ||||

| FCFF yield | 0.2% | 0.4% | 1.5% | 2.4% |

| Dividend yield | 0.1% | 0.2% | 0.3% | 0.3% |

| EV/Revenue | 2.0 | 1.7 | 1.7 | 1.5 |

| EV/EBITDA | 6.6 | 4.7 | 4.2 | 3.6 |

| P/E | 89.7 | 71.2 | 52.3 | 39.1 |

Summary Investment Thesis and Valuation

Investment Thesis

In addition to the company's dominant market share in substrates for GPUs for AI servers, we also expect the company to see major earnings growth in EMIB substrates for ASICs and in standard ABF substrates from growing demand for AI servers. We believe Ibiden is well-positioned to maximize benefits from the shift to larger and higher multi-layered FCBGA substrates for AI server-use GPUs because of its strong technological abilities.

Valuation

Our December 2027 price target of ¥28,500 is based on (1) the ¥16,300 value derived from a zero-growth ROIC model (EV/IC = ROIC/WACC) using our FY2030 estimates (Rf = 2.57%, Rp = 5.15%, beta = 1.30, WACC = 5.9%) plus (2) Ibiden's 75% premium to the sector-average P/E (from August 2025 to July 2026, 12-month forward Bloomberg consensus basis), reflecting the rise in Ibiden's share price since August 2025 on expectations for earnings growth for AI server applications. Our price target is equivalent to a P/E of 31x our FY2030 EPS estimate.

We calculated our previous December 2026 price target of ¥18,400 based on (1) the ¥10,200 value derived from a zerogrowth ROIC model (EV/IC = ROIC/WACC) using our FY2029 estimates (Rf = 2.2%, Rp = 5.15%, beta = 1.30, WACC = 6.45%) plus (2) Ibiden's 80% premium to the sector-average P/E (from August 2025 to May 2026, 12-month forward Bloomberg consensus basis), reflecting the rise in Ibiden's share price since August 2025 on expectations for earnings growth for AI server applications.

| Performance Drivers | Performance Drivers | Performance Drivers | Performance Drivers |

|---|---|---|---|

Source: J.P. Morgan Global Markets Strategy for Performance Drivers; company data, Bloomberg Finance L.P. and J.P. Morgan estimates for all other tables. Note: Price history may not be complete or exact.

22%

32%

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

Asia Pacific Equity Research 15 July 2026

J P M O R G A N

- Changes: We revise up our earnings forecasts mainly for the electronics business, and we lower them slightly for the ceramics business. In the electronics business, in addition to a slower rise in depreciation than we previously forecast, we also revise up our sales forecasts for GPUs for AI servers. We previously anticipated that EMIB substrates for ASICs used as accelerators for AI servers would start up from FY2028, but now we expect them to start up from FY2027 with the previous generation product (which we assume is a product with built-in silicon capacitors). As a result, we revise up our earnings forecasts for FY2026-27. In addition, we anticipate the launch of standard ABF substrates for ASICs from FY2028, and newly factor this into our earnings forecasts. We formulate our earnings forecasts for FY2029-30 on the assumption that capacity constraints can be eliminated through additional capacity expansion.

- Our earnings forecasts call for earnings growth to significantly overshoot the company's forecasts from a medium- to long-term perspective, although this will depend on factors such as fluctuations in fixed costs associated with the start-up of plants as well as capex/depreciation schedules and the timing of the start-up of logic semiconductors. Looking ahead, the stock market's expectations for FY2029-30 earnings will likely rise, if Ibiden constructs new facilities in vacant spaces at the Gama and Ono Plants, and moreover, acquires external fabs. On the other hand, hiring human resources should also become important, given the prospect of significant capacity expansion.

- Price target: Our December 2027 price target of ¥28,500 is based on (1) the ¥16,300 value derived from a zero-growth ROIC model (EV/IC = ROIC/WACC) using our FY2030 estimates (Rf = 2.57%, Rp = 5.15%, beta = 1.30, WACC = 5.9%) plus (2) Ibiden's 75% premium to the sector-average P/E (from August 2025 to July 2026, 12-month forward Bloomberg consensus basis), reflecting the rise in Ibiden's share price since August 2025 on expectations for earnings growth for AI server applications. Our price target is equivalent to a P/E of 31x our FY2030 EPS estimate. We change the base year for our price target from FY2029 to FY2030 due to factoring in our medium- to long-term earnings outlook, based on the company's medium-term outlook.

Figure 1: 12-Month Forward Consensus P/E, Sector Relative P/E

Source: Bloomberg Finance L.P. consensus estimates, J.P. Morgan. Note: Share price and consensus as of July 13

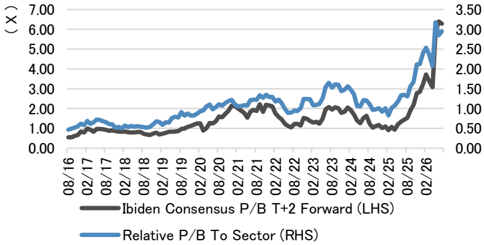

Figure 2: 12-Month Forward Consensus P/B, Sector Relative P/B

Source: Bloomberg Finance L.P. consensus estimates, J.P. Morgan. Note: Share price and consensus as of July 13

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

Asia Pacific Equity Research 15 July 2026

Figure 3: 24-Month Forward Consensus P/E, Sector Relative P/E

Source: Bloomberg Finance L.P. consensus estimates, J.P. Morgan. Note: Share price and consensus as of Jul 13

Figure 4: 24-Month Forward Consensus P/B, Sector Relative P/B

Source: Bloomberg Finance L.P. consensus estimates, J.P. Morgan. Note: Share price and consensus as of Jul 13

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

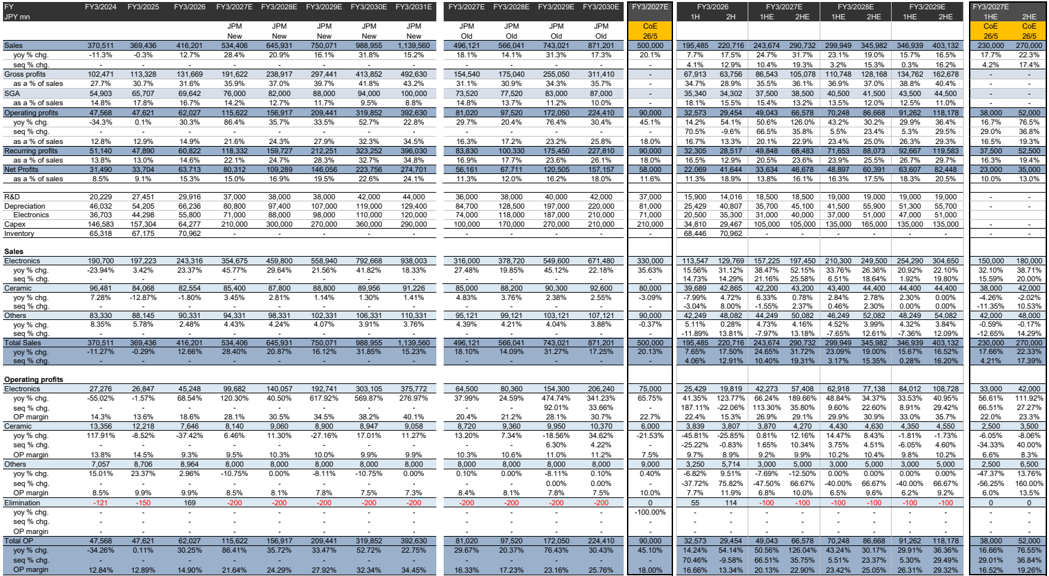

Figure 5: Earnings Forecast Summary

| Ibiden 4062 | Ibiden 4062 | Ibiden 4062 | JPY mn Sales | YoY | JPY mn | YoY Operating Pofits | OPM | JPY mn Recurring | YoY profits | JPY mn Net | YoY Profits | EPS JPY | BPS JPY | DPS JPY | Capex JPY mn | Dep. JPY mn | R&D JPY mn | R&D JPY mn | R&D JPY mn | R&D JPY mn | R&D JPY mn | R&D JPY mn |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FY3/24 | 370,511 | -11.27% | 47,568 | -34.26% | 12.84% | 51,140 | -32.87% | 31,490 | -39.66% | 213.0 | 3,543 | 40 | 146,583 | 46,032 | 20,229 | 20,229 | 20,229 | 20,229 | 20,229 | 20,229 | ||

| FY3/25 | 369,436 | -0.29% | 47,621 | 0.11% | 12.89% | 47,890 | -6.36% | 33,704 | 7.03% | 228.1 | 3,513 | 40 | 157,304 | 54,205 | 27,451 | 27,451 | 27,451 | 27,451 | 27,451 | 27,451 | ||

| FY3/26 | 416,201 | 12.66% | 62,027 | 30.25% | 14.90% | 60,822 | 27.00% | 63,713 | 89.04% | 215.6 | 1,970 | 25 | 64,277 | 66,236 | 29,916 | 29,916 | 29,916 | 29,916 | 29,916 | 29,916 | ||

| FY3/27E | JPM | 534,406 | 28.40% | 115,622 | 86.41% | 21.64% | 118,332 | 94.55% | 80,312 | 26.05% | 271.7 | 2,223 | 35 | 210,000 | 80,800 | 37,000 | 37,000 | 37,000 | 37,000 | 37,000 | 37,000 | |

| FY3/28E | JPM | 645,931 | 20.87% | 156,917 | 35.72% | 24.29% | 159,727 | 34.98% | 109,289 | 36.08% | 369.7 | 2,559 | 55 | 300,000 | 97,400 | 38,000 | 38,000 | 38,000 | 38,000 | 38,000 | 38,000 | |

| FY3/29E | JPM | 750,071 | 16.12% | 209,441 | 33.47% | 27.92% | 212,251 | 32.88% | 146,056 | 33.64% | 494.1 | 3,017 | 65 | 270,000 | 107,000 | 38,000 | 38,000 | 38,000 | 38,000 | 38,000 | 38,000 | |

| FY3/30E | JPM | 988,955 | 31.85% | 319,852 | 52.72% | 32.34% | 323,252 | 52.30% | 223,756 | 53.20% | 757.0 | 3,719 | 100 | 360,000 | 119,000 | 42,000 | 42,000 | 42,000 | 42,000 | 42,000 | 42,000 | |

| FY3/31E | JPM | 1,139,560 | 15.23% | 392,630 | 22.75% | 34.45% | 396,030 | 22.51% | 274,701 | 22.77% | 929.4 | 4,582 | 120 | 290,000 | 129,400 | 44,000 | 44,000 | 44,000 | 44,000 | 44,000 | 44,000 | |

| FY3/27E | JPM Old | 496,121 | 18.10% | 81,020 | 29.67% | 16.33% | 83,830 | 35.33% | 56,161 | -26.12% | 190.0 | 2,250 | 21 | 100,000 | 84,700 | 36,000 | 36,000 | 36,000 | 36,000 | 36,000 | 36,000 | |

| FY3/28E | JPM Old | 566,041 | 14.09% | 97,520 | 20.37% | 17.23% | 100,330 | 19.68% | 67,711 | 20.57% | 229.1 | 2,471 | 22 | 170,000 | 128,500 | 38,000 | 38,000 | 38,000 | 38,000 | 38,000 | 38,000 | |

| FY3/29E | JPM Old | 743,021 | 31.27% | 172,050 | 76.43% | 23.16% | 175,450 | 74.87% | 120,505 | 77.97% | 407.7 | 2,879 | 23 | 270,000 | 197,000 | 40,000 | 40,000 | 40,000 | 40,000 | 40,000 | 40,000 | |

| FY3/30E | JPM Old | 871,201 | 17.25% | 224,410 | 30.43% | 25.76% | 227,810 | 29.84% | 157,157 | 30.42% | 531.7 | 3,417 | 25 | 210,000 | 220,000 | 42,000 | 42,000 | 42,000 | 42,000 | 42,000 | 42,000 | |

| FY3/27E | 26/5 | |||||||||||||||||||||

| CoE | 500,000 | 35.34% | 90,000 | 88.99% | 18.00% | 90,000 | 87.93% | 58,000 | 72.09% | 196.2 | - | 35 | 210,000 | 81,000 | 37,000 | 37,000 | 37,000 | 37,000 | 37,000 | 37,000 | ||

| FY3/26E | BBG | 516,998 | 39.94% | 100,828 | 111.73% | 19.50% | 101,265 | 111.45% | 70,747 | 109.91% | 248.2 | 2,182 | 37 | 210,000 | 81,203 | - | - | - | - | - | - | |

| FY3/27E | BBG | 646,742 | 25.10% | 154,902 | 53.63% | 23.95% | 155,662 | 53.72% | 109,165 | 54.30% | 369.1 | 2,516 | 49 | 257,500 | 98,748 | |||||||

| FY3/28E | BBG | 796,470 | 23.15% | 224,706 | 45.06% | 28.21% | 215,769 | 38.61% | 154,225 | 41.28% | 527.7 | 2,976 | 59 | 152,500 | 116,706 | - | - | - | - | - | - | |

| FY3/25 | 1H 2H | 181,585 187,851 | -3.23% 2.72% | 28,512 19,109 | 18.44% -18.67% | 15.70% 10.17% | 29,531 18,359 | 10.09% -24.50% | 20,527 13,177 | 14.73% -3.10% | 69.4 44.6 | 1,659 1,757 | 20 20 | 83,532 73,772 | 22,900 31,305 | 15,491 | 15,491 | 15,491 | 15,491 | 15,491 | 15,491 | |

| FY3/26 | 1H | 195,485 | 7.65% | 32,573 | 14.24% | 16.66% | 32,305 | 9.39% | 22,069 | 7.51% | 74.7 | 1,881 | 30 | 34,810 | 25,429 | 15,900 | 15,900 | 15,900 | 15,900 | 15,900 | 15,900 | |

| FY3/27 | 2H 1HE | JPM | 220,716 243,674 | 17.50% 24.65% | 29,454 49,043 | 54.14% 50.56% | 13.34% 20.13% | 28,517 49,848 | 55.33% 54.31% | 41,644 33,634 | 216.04% 52.40% | 140.9 113.8 | 1,970 - | 15 - | 29,467 105,000 | 40,807 35,700 | 14,016 18,500 | 14,016 18,500 | 14,016 18,500 | 14,016 18,500 | 14,016 18,500 | 14,016 18,500 |

| 2HE 1HE | JPM | 290,732 | 31.72% | 66,578 | 126.04% | 22.90% | 68,483 | 140.15% | 46,678 | 12.09% | 157.9 | - | - | 105,000 | 45,100 | 18,500 | 18,500 | 18,500 | 18,500 | 18,500 | 18,500 | |

| FY3/28 | JPM | 300,569 | 23.35% | 70,620 | 44.00% | 23.50% | 72,025 | 44.49% | 49,158 | 46.16% | 166.3 | - | - | 135,000 | 41,500 | 19,000 | 19,000 | 19,000 | 19,000 | 19,000 | 19,000 | |

| 2HE | JPM | 341,332 | 17.40% 16.00% | 83,878 | 25.98% | 24.57% | 85,283 | 24.53% | 58,438 | 25.19% | 197.7 | - | - | 165,000 | 55,900 51,300 | 19,000 19,000 | 19,000 19,000 | 19,000 19,000 | 19,000 19,000 | 19,000 19,000 | 19,000 19,000 | |

| FY3/29 | 1HE 2HE | JPM JPM | 348,675 398,017 | 16.61% | 92,304 | 30.70% 37.23% | 26.47% 28.92% | 93,709 116,514 | 30.11% 36.62% | 64,336 80,300 | 30.88% | 217.7 | - - | 135,000 | 135,000 | 55,700 | 19,000 | 19,000 | 19,000 | 19,000 | 19,000 | 19,000 |

| FY3/27E | 1HE | CoE 26/5 | 230,000 17.66% | 115,109 | 16.66% | 16.52% | 37,500 | 16.08% | 37.41% | 271.7 | 15 | - | - | - | - | - | - | - | - | |||

| 2HE | CoE 26/5 | 270,000 22.33% | 38,000 52,000 | 76.55% | 19.26% | 52,500 | 84.10% | 23,000 35,000 | 4.22% -15.95% | 77.8 118.4 | - - | 20 | - | - | - | - | - | - | - | - | ||

| FY3/25 | 1Q | 88,220 | -6.75% | 11,295 | 38.06% | 12.80% | 12,868 | 26.19% | 8,816 | 20.97% | 29.8 | 1,717 | - | 40,321 | 10,198 | 5,500 | 5,500 | 5,500 | 5,500 | 5,500 | 5,500 | |

| 2Q 3Q | 93,365 88,752 | 0.35% | 17,217 | 8.34% | 18.44% | 16,663 6,376 | 0.22% -53.06% | 11,711 | 10.44% | 39.6 | 1,659 | - | 43,211 | 12,702 | 6,460 | 6,460 | 6,460 | 8,300 | 6,460 | 6,460 | ||

| FY3/26 | 4Q | -4.08% 99,099 9.69% | 12,764 | 6,345 | -50.72% 20.18% | 7.15% 12.88% | 11,983 17,407 | 11.65% | 4,274 8,903 | -55.02% 117.41% | 14.5 30.1 | 1,724 1,757 | - - | 26,971 46,801 | 15,278 16,027 | 7,191 | 7,191 | 7,191 | 7,191 | 7,191 | 7,191 | |

| 1Q 2Q | 97,464 10.48% | 17,636 | 56.14% | 18.09% 15.24% | 14,898 | 35.27% -10.59% | 12,728 | 44.37% | 43.1 | 1,822 | - | 20,436 | 11,667 | 7,800 | 7,800 | 7,800 | 7,800 | 7,800 | 7,800 | |||

| 4.99% | 14,937 | -13.24% | 9,341 | -20.24% | 31.6 | 1,881 | - | 14,374 | 13,762 | 8,100 | 8,100 | 8,100 | 8,100 | 8,100 | 8,100 | |||||||

| 98,021 | 30.2 | 6,700 | 6,700 | 6,700 | 6,700 | 6,700 | 6,700 | |||||||||||||||

| 3Q | 103,136 | 16.21% 117,580 | 11,954 18.65% | 17,500 | 88.40% 37.10% | 11.59% 14.88% | 11,328 17,189 | 77.67% 43.44% | 8,931 32,713 | 108.96% 267.44% | 110.7 | 1,943 1,970 | - | 12,536 16,931 | 19,065 21,742 | 7,316 | 7,316 | 7,316 | 7,316 | 7,316 | 7,316 | |

| FY3/27 | 4Q 1QE | JPM | 117,554 20.61% | 22,179 | 25.76% | 18.87% | 22,129 | 27.13% | 14,860 | 16.75% | 50.3 | - | - | 52,500 | 17,300 | 9,000 9,500 | 9,000 9,500 | 9,000 9,500 | 9,000 9,500 | 9,000 9,500 | 9,000 9,500 | |

| 2QE | JPM | 28.67% | 26,864 | 79.85% | 21.30% | 27,719 | 86.06% | 18,773 | 100.98% | 63.5 | - | - | 52,500 | 18,400 | ||||||||

| 3QE | 126,120 142,872 147,860 | 38.53% | 32,394 | 170.99% | 22.67% | 33,444 | 195.23% | 22,781 | 77.1 | - | 52,500 | 21,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | ||||

| 4QE | JPM JPM | 25.75% | 34,184 | 95.34% | 23.12% | 35,039 | 103.85% | 23,897 | 155.08% -26.95% | 80.8 | - | - - | 52,500 | 23,600 9,000 | 23,600 9,000 | 23,600 9,000 | 23,600 9,000 | 23,600 9,000 | 23,600 9,000 | 23,600 9,000 | ||

| FY3/28 | 1QE | JPM JPM | 150,429 27.97% 18.55% | 36,224 34,024 | 63.33% 26.65% | 24.08% | 37,274 | 68.44% | 25,462 23,435 | 71.34% 24.83% | 86.1 | - | - | 67,500 | 67,500 | 20,200 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | |

| 2QE | 149,520 | 22.76% | 34,379 | 24.03% | 79.3 | - | - | 21,300 | ||||||||||||||

| 3QE 4QE | JPM JPM | 20.96% 17.11% | 43,334 | 33.77% | 25.07% | 44,384 | 32.71% | 30,439 | 33.62% | 103.0 | - | - | 82,500 82,500 | 27,400 | 28,500 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | ||

| 172,822 173,160 173,924 | 43,334 | 26.77% | 25.03% | 43,689 | 24.69% | 29,952 | 25.34% | 101.3 | - | - | ||||||||||||

| FY3/29 | 1QE | JPM | 15.62% | 46,131 | 27.35% | 26.52% | 47,181 | 26.58% | 32,397 | 27.24% | 109.6 | - | - | 67,500 | 25,100 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | 9,500 9,500 | |

| 2QE | JPM | 173,015 | 15.71% | 45,131 | 32.64% | 26.09% | 45,486 | 32.31% | 31,210 | 33.18% | 105.6 | - | 67,500 | 26,200 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | |

| 3QE 4QE | JPM | 16.53% | 59,089 | 36.36% | 29.34% | 60,139 | 35.50% | 41,467 | 36.23% | 140.3 | - | - - | 67,500 | 27,300 28,400 | 9,500 | |||||||

| JPM | 201,397 201,735 | 16.50% | 59,089 | 36.36% | 29.29% | 59,444 | 36.06% | 40,981 | 36.82% | 138.6 | - | - | 67,500 |

Source: Company data, Bloomberg Finance L.P. consensus estimates, J.P. Morgan estimates.

Note: Share price and consensus as of July 13

Asia Pacific Equity Research 15 July 2026

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

Asia Pacific Equity Research 15 July 2026

Figure 6: Sales and OP Forecasts by Segment (Half Year, Full Year)

| FY JPY mn | FY3/2024 FY3/2025 | FY3/2026 | FY3/2027E | FY3/2028E JPM | FY3/2029E JPM | FY3/2030E JPM | FY3/2031E | FY3/2027E | FY3/2028E | FY3/2029E | FY3/2030E | FY3/2027E | 1H | 2H FY3/2026 | 1HE 2HE FY3/2027E | 1HE 2HE FY3/2028E | 1HE | 2HE FY3/2029E | FY3/2027E 1HE 2HE CoE CoE 26/5 26/5 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| JPM New | New | New | New | JPM New | JPM Old | JPM Old | JPM Old | JPM | Old | CoE 26/5 | |||||||||||||||||

| Sales | 370,511 369,436 | 416,201 | 534,406 | 645,931 | 750,071 | 988,955 | 1,139,560 | 496,121 | 566,041 | 743,021 | 871,201 | 500,000 | 195,485 220,716 | 243,674 290,732 | 299,949 345,982 | 346,939 | 403,132 | 230,000 270,000 | |||||||||

| yoy %chg. | -11.3% -0.3% - | 12.7% - | 28.4% - | 20.9% - | 16.1% - | 31.8% - | 15.2% - | 18.1% - | 14.1% | 31.3% | 17.3% | 20.1% - | 7.7% 17.5% 4.1% 12.9% | 24.7% 31.7% 10.4% 19.3% | 23.1% 19.0% 15.3% | 15.7% 0.3% | 16.5% 16.2% | 17.7% 22.3% 4.2% 17.4% | |||||||||

| seq %chg. | - 113,328 | 131,669 | 191,622 | 238,917 | 297,441 | 413,852 | 492,630 | 154,540 | - 175,040 | - 255,050 | - 311,410 | - | 67,913 105,078 | 63,756 86,543 | 3.2% 110,748 | 134,762 | 162,678 | - - | |||||||||

| Gross profits as a %of sales | 102,471 27.7% 30.7% | 31.6% | 35.9% | 37.0% | 39.7% | 41.8% | 43.2% | 31.1% | 30.9% | 34.3% | 35.7% | - | 34.7% 28.9% 36.1% | 35.5% | 128,168 36.9% 37.0% | 38.8% | 40.4% | - | - | ||||||||

| SGA | 65,707 | 69,642 | 76,000 | 82,000 | 88,000 | 94,000 | 100,000 | 73,520 | 77,520 | 83,000 | 87,000 | - | 35,340 34,302 38,500 | 37,500 | 40,500 41,500 | 43,500 | 44,500 | - - | |||||||||

| as a %of sales | 54,903 14.8% 17.8% | 16.7% | 14.2% | 12.7% | 11.7% | 9.5% | 8.8% | 14.8% | 13.7% | 11.2% | 10.0% | - | 18.1% | 15.5% 13.2% | 15.4% | 13.5% 12.0% | 12.5% | 11.0% | - - | ||||||||

| Operating profits | 47,568 47,621 | 62,027 | 115,622 | 156,917 | 209,441 | 319,852 | 392,630 | 81,020 | 97,520 | 172,050 | 224,410 | 90,000 | 32,573 | 29,454 66,578 | 49,043 | 70,248 86,668 | 91,262 | 118,178 | 38,000 52,000 | ||||||||

| yoy %chg. | -34.3% 0.1% | 30.3% | 86.4% | 35.7% | 33.5% | 52.7% | 22.8% | 29.7% | 20.4% | 76.4% | 30.4% | 45.1% | 14.2% 54.1% 126.0% | 50.6% | 43.2% 30.2% | 29.9% | 36.4% | 16.7% 76.5% | |||||||||

| seq %chg. as a %of sales | - - | - 14.9% | - 21.6% | - | - | - | - | - | - | - | - | 18.0% | - | 70.5% -9.6% 35.8% 16.7% 13.3% | 66.5% | 5.5% 23.4% | 5.3% | 29.5% | 29.0% 36.8% | ||||||||

| Recurring profits | 12.8% 12.9% | 24.3% | 27.9% | 32.3% | 34.5% | 16.3% | 17.2% | 23.2% | 25.8% | 22.9% | 20.1% | 23.4% | 26.3% | 29.3% | 16.5% 19.3% | ||||||||||||

| as a %of sales | 51,140 47,890 | 60,822 | 118,332 | 159,727 | 212,251 | 323,252 | 396,030 | 83,830 | 100,330 | 175,450 | 227,810 | 90,000 | 32,305 28,517 68,483 | 49,848 | 71,653 | 25.0% 88,073 | 92,667 119,583 | 37,500 52,500 | |||||||||

| Net Profits | 13.8% 13.0% | 14.6% | 22.1% | 24.7% | 28.3% | 32.7% | 34.8% | 16.9% | 17.7% | 23.6% | 26.1% | 18.0% | 16.5% | 12.9% 23.6% | 20.5% | 23.9% 48,897 | 25.5% 26.7% | 29.7% | 16.3% 19.4% | ||||||||

| as a %of sales | 31,490 33,704 8.5% | 63,713 | 80,312 | 109,289 | 146,056 | 223,756 | 274,701 | 56,161 | 67,711 | 120,505 | 157,157 | 58,000 | 22,069 41,644 46,678 13.8% 16.1% | 33,634 | 60,391 17.5% | 63,607 | 82,448 | 23,000 35,000 | |||||||||

| 9.1% 20,229 27,451 | 15.3% 29,916 | 15.0% 37,000 | 16.9% 38,000 | 19.5% 38,000 | 22.6% 42,000 | 24.1% 44,000 | 11.3% | 12.0% | 16.2% | 18.0% | 11.6% | 11.3% 18.9% 18,500 18,500 | 16.3% 19,000 | 18.3% | 20.5% | 10.0% 13.0% | |||||||||||

| R&D Depreciation | 46,032 54,205 44,298 | 66,236 55,800 | 80,800 71,000 | 97,400 88,000 | 107,000 | 119,000 | 129,400 | 36,000 84,700 | 38,000 128,500 | 40,000 197,000 | 42,000 220,000 210,000 | 81,000 | 37,000 71,000 | 15,900 14,016 25,429 40,807 35,700 45,100 20,500 | 19,000 41,500 37,000 | 19,000 51,300 | 19,000 55,700 | - - - - | |||||||||

| Electronics Capex | 36,703 | 98,000 | 110,000 360,000 | 120,000 | 74,000 100,000 | 118,000 170,000 | 187,000 270,000 | 210,000 | 35,300 31,000 29,467 | 55,900 51,000 165,000 | 47,000 135,000 | 51,000 | - - | ||||||||||||||

| 146,583 157,304 | 64,277 | 210,000 | 300,000 | 270,000 | 290,000 | 210,000 | 34,810 | 105,000 | 40,000 | 105,000 | 135,000 | 135,000 | |||||||||||||||

| Inventory | 67,175 | 70,962 | - | - | - | - | - | - | - | - | - | - | 68,446 | 70,962 | - - | - - | - | - | - | - | - | - | - | - | - | - | - |

| 65,318 | - | ||||||||||||||||||||||||||

| Sales Electronics yoy %chg. seq %chg. Ceramic | 190,700 197,223 -23.94% 3.42% - - 96,481 84,068 -12.87% - | 243,316 23.37% - 82,554 -1.80% | 354,675 45.77% - | 459,800 29.64% - | 558,940 21.56% - 88,800 | 792,668 41.82% - 89,956 1.30% | 938,003 18.33% - 91,226 1.41% - | 316,000 27.48% - 85,000 4.83% - | 378,720 19.85% - 88,200 3.76% - 99,121 | - 90,300 2.38% - | - 92,600 2.55% | 549,600 671,480 330,000 45.12% 22.18% 35.63% - 80,000 -3.09% | 113,547 15.56% 14.73% 39,689 -7.99% - -3.04% | 129,769 157,225 197,450 31.12% 38.47% 52.15% 14.29% 21.16% 25.58% 42,865 4.72% 8.00% 42,249 48,082 | 42,200 43,200 6.33% -1.55% | 210,300 249,500 33.76% 26.36% 6.51% 18.64% 44,400 2.78% 2.30% | 44,400 2.30% 0.00% | 254,290 20.92% 1.92% 44,400 0.00% 0.00% 54,082 | 15.59% 20.00% 38,000 42,000 -4.26% -2.02% -11.35% 10.53% 42,000 48,000 | 304,650 22.10% 19.80% | 150,000 32.10% | 180,000 38.71% | |||||

| yoy %chg. seq %chg. Others yoy %chg. | 7.28% 88,145 | - | 85,400 3.45% - | 87,800 2.81% - | 1.14% - 102,331 | - 106,331 3.91% | 110,331 3.76% | 95,121 4.39% | 4.21% | 103,121 4.04% | - 107,121 | 90,000 | 5.11% | 0.28% | 0.78% 2.37% 44,249 50,082 4.73% 4.16% | 43,400 2.84% 0.46% 46,249 | 52,082 3.99% | 48,249 4.32% | 3.84% | ||||||||

| - 83,330 8.35% 5.78% - | 90,331 2.48% | 94,331 4.43% | 98,331 4.24% | 4.07% | 3.88% | -0.37% | 13.81% | 4.52% | -0.59% -12.65% | ||||||||||||||||||

| seq %chg. Total Sales | - | - | - | - 645,931 | - 750,071 | - 988,955 | - 1,139,560 | - | - | - | - | - | -11.89% | 13.18% | -7.65% | 12.09% | -0.17% 14.29% | -0.17% 14.29% | -0.17% 14.29% | -0.17% 14.29% | -0.17% 14.29% | -0.17% 14.29% | -0.17% 14.29% | ||||

| yoy %chg. | 370,511 369,436 -11.27% -0.29% | 416,201 12.66% | 534,406 28.40% | 20.87% | 16.12% | 31.85% | 15.23% | 496,121 18.10% | 566,041 14.09% | 743,021 | 871,201 | 500,000 | 195,485 220,716 | -7.97% 243,674 | 12.61% 299,949 | -7.36% 346,939 | 230,000 270,000 | 230,000 270,000 | 230,000 270,000 | 230,000 270,000 | 230,000 270,000 | 230,000 270,000 | 230,000 270,000 | ||||

| seq %chg. | 31.27% | 17.25% | 20.13% | 7.65% | 17.50% | 290,732 24.65% 31.72% | 23.09% | 345,982 19.00% | 15.67% | 17.66% 22.33% | 17.66% 22.33% | 17.66% 22.33% | 17.66% 22.33% | 17.66% 22.33% | 17.66% 22.33% | 17.66% 22.33% | 17.66% 22.33% | 17.66% 22.33% | |||||||||

| - - | - | - | - | - | - | - | 10.40% | 3.17% | 15.35% 0.28% | 403,132 16.52% 16.20% | 17.39% | 17.39% | 17.39% | 17.39% | 17.39% | 17.39% | 17.39% | ||||||||||

| Operating profits Electronics yoy %chg. | 27,276 26,847 -55.02% -1.57% - 13.6% | 45,248 68.54% | 99,682 120.30% | - 140,057 40.50% | - 192,741 617.92% | - 303,105 569.87% | 375,772 276.97% - | 64,500 37.99% - 20.4% | 80,360 24.59% - | 154,300 474.74% 92.01% | - | - 206,240 75,000 341.23% 65.75% | 25,429 41.35% | 4.06% 12.91% 19,819 42,273 57,408 123.77% 66.24% 189.66% | 19.31% | 62,918 77,138 48.84% 34.37% | 4.21% | 84,012 108,728 33,000 33.53% 40.95% 56.61% | 42,000 111.92% 27.27% | 42,000 111.92% 27.27% | 42,000 111.92% 27.27% | 42,000 111.92% 27.27% | 42,000 111.92% 27.27% | 42,000 111.92% 27.27% | 42,000 111.92% 27.27% | 42,000 111.92% 27.27% | 42,000 111.92% 27.27% |

| seq %chg. OP margin Ceramic yoy %chg. | - 14.3% 12,218 | - 18.6% | - 28.1% | - 30.5% | - 34.5% 8,900 | - 38.2% | 40.1% | 21.2% | 28.1% | 33.66% 30.7% | - 22.7% | 187.11% -22.06% 22.4% 15.3% | 113.30% 35.80% 26.9% | 9.60% 29.9% | 22.60% 30.9% | 8.91% 29.42% 35.7% | 66.51% 22.0% 23.3% 2,500 | ||||||||||

| -8.52% | 7,646 -37.42% | 8,140 6.46% | 9,060 11.30% | -27.16% | 8,947 17.01% | 9,058 11.27% | 8,720 13.20% | 9,360 7.34% | 9,950 -18.56% | 10,370 34.62% | 6,000 -21.53% | 3,839 -45.81% | 3,807 -25.85% | 3,870 0.81% | 29.1% 4,270 4,430 14.47% | 33.0% | -6.05% | 3,500 | 3,500 | 3,500 | 3,500 | 3,500 | 3,500 | 3,500 | |||

| seq %chg. | - | - | - | - | 6.30% | 4.22% | - | -25.22% | -0.83% | 1.65% | 3.75% | 4,630 | 4,550 -1.73% 4.60% | -8.06% | |||||||||||||

| 13,356 117.91% - - | - | - | -34.33% | 4,350 -1.81% -6.05% | |||||||||||||||||||||||

| OP margin | 14.5% | - 9.3% | 9.5% 8,000 | - 10.3% | 10.0% | 9.9% 8,000 | 9.9% | 10.3% | 10.6% | 11.0% | 11.2% | 9.7% 8.9% | 9.2% | 12.16% 10.34% 9.9% | 6.6% | 8.43% 4.51% 10.4% 5,000 | 40.00% | ||||||||||

| Others | 13.8% 7,057 8,706 | 8,964 | 8,000 | 8,000 | 8,000 | 8,000 0.10% | 8,000 0.00% | 8,000 -8.11% | 8,000 0.10% | 7.5% 9,000 0.40% | 3,250 5,714 -6.82% 9.51% | 10.2% 3,000 0.00% | 9.8% 3,000 | 2,500 | 8.3% 6,500 | 10.2% 5,000 0.00% | |||||||||||

| yoy %chg. seq %chg. | 15.01% 23.37% - - | 2.96% - | -10.75% - | 0.00% - | -8.11% - | -10.75% - | 0.00% - | - | - | 0.00% | 0.00% | - | 75.82% | 3,000 5,000 -7.69% -12.50% -47.50% 66.67% | 0.00% -40.00% | -47.37% -56.25% | 13.76% 160.00% | ||||||||||

| OP margin | 8.5% | 8.1% | 7.5% | 7.3% | 8.4% | 8.1% | 7.8% | 7.5% | 10.0% | -37.72% 7.7% 11.9% | 6.8% | 0.00% 66.67% | -40.00% 6.5% | 9.6% | 6.0% | 0 - - | 6.2% -100 - | 66.67% 9.2% | 13.5% | ||||||||

| Elimination | 8.5% 9.9% -121 -150 - | 9.9% 169 | -200 | -200 | 7.8% -200 | -200 | -200 | -200 | -200 | -200 | -200 | 0 | -100.00% | 55 114 | 10.0% -100 | -100 | -100 | 0 | |||||||||

| yoy %chg. Total OP yoy %chg. | - - - 47,568 47,621 -34.26% 0.11% | - 62,027 30.25% | 115,622 86.41% | - 156,917 35.72% | - 209,441 33.47% | - - - 319,852 52.72% | - 392,630 22.75% | - - 81,020 29.67% | - 97,520 20.37% | - | - - - - - 172,050 224,410 76.43% 30.43% | - - 49,043 50.56% 126.04% | -100 - - | 86,668 43.24% 30.17% | - | - - - 91,262 29.91% | -100 - - - 118,178 36.36% | - - - 66,578 70,248 | - - | - | - 38,000 16.66% | - - 52,000 76.55% | |||||

| seq %chg. OP margin | - - | - - | - - | - - | - - | - | - | - | - | - - - | - | - 90,000 32,573 45.10% 14.24% 70.46% | - - - 29,454 54.14% -9.58% | - - - |

Source: Company data, J.P. Morgan estimates.

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

Asia Pacific Equity Research 15 July 2026

Figure 7: Sales and OP Forecasts by Segment (Quarterly)

| FY JPY mn | FY3/2025 1Q | 2Q | 3Q | 4Q | FY3/2026 1Q | 2Q | 3Q | 4Q | FY3/2027E 1QE JPM | 2QE JPM | 3QE JPM | 4QE JPM | JPM | FY3/2028E 1QE JPM | 2QE JPM | 3QE JPM | 4QE JPM | FY3/2029E 1QE | 3QE | 2QE 4QE JPM | 2QE 4QE JPM | JPM | 2QE 4QE JPM | JPM |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 88,220 | 93,365 | 88,752 | 99,099 | 97,464 | 98,021 | 103,136 | 117,580 | 117,554 | 126,120 | 142,872 | 147,860 | 150,429 | 149,520 | 172,822 | 173,160 | 173,924 | 173,015 | 201,397 | 201,735 | 201,735 | 201,735 | 201,735 | 201,735 |

| yoy %chg. | -6.7% | 0.4% | -4.1% | 9.7% | 10.5% | 5.0% | 16.2% | 18.6% | 20.6% | 28.7% | 38.5% | 25.8% | 28.0% | 18.6% | 21.0% | 17.1% | 15.7% | 16.5% | 16.5% | 16.5% | 16.5% | 16.5% | 16.5% | |

| -2.4% | 5.8% | -1.6% | 14.0% | 0.0% | 13.3% | 3.5% | 1.7% | -0.6% | 15.6% | 0.2% | 15.6% | 16.4% | 0.2% | 0.2% | 0.2% | 0.2% | 0.2% | |||||||

| qoq %chg. | 25,614 | 32,755 | -4.9% 23,602 | 11.7% 31,357 | 35,072 | 0.6% 32,841 | 5.2% 28,070 | 35,686 | 40,679 | 7.3% 45,864 | 51,394 | 53,684 | 56,224 | 54,524 | 63,834 | 64,334 | 0.4% 67,631 | -0.5% 67,131 | 81,089 | 81,589 | 81,589 | 81,589 | 81,589 | 81,589 |

| Gross profits as a %of | 29.0% | 33.5% | 36.9% | 37.2% | ||||||||||||||||||||

| sales SGA | 14,319 | 35.1% 15,538 | 26.6% 17,257 | 31.6% 18,593 | 36.0% 17,436 | 17,904 | 27.2% 16,116 | 30.4% 18,186 | 34.6% 18,500 | 36.4% 19,000 | 36.0% 19,000 | 36.3% 19,500 | 37.4% 20,000 | 36.5% 20,500 | 20,500 | 21,000 | 38.9% 21,500 22,000 | 38.8% | 40.3% | 40.4% 22,500 | 40.4% 22,500 | 22,000 | 40.4% 22,500 | 40.4% 22,500 |

| as a %of sales | 16.2% | 16.6% | 19.4% | 18.8% | 17.9% | 18.3% | 15.6% | 15.5% | 15.7% | 15.1% | 13.3% | 13.2% | 13.3% | 13.7% | 11.9% | 12.1% | 12.4% | 12.7% | 10.9% | 11.2% | 11.2% | 11.2% | 11.2% | 11.2% |

| Operating profits | 11,295 | 17,217 | 6,345 | 12,764 | 17,636 | 14,937 | 11,954 | 17,500 | 22,179 | 26,864 | 32,394 | 34,184 | 36,224 | 34,024 | 43,334 | 43,334 | 46,131 | 45,131 | 59,089 | 59,089 | 59,089 | 59,089 | 59,089 | 59,089 |

| yoy %chg. | 38.1% | 8.3% | -50.7% | 20.2% | 56.1% | -13.2% | 88.4% | 37.1% | 25.8% | 79.9% | 171.0% | 95.3% | 63.3% | 26.7% | 33.8% | 26.8% | 27.3% | 32.6% | 36.4% | 36.4% | 36.4% | 36.4% | 36.4% | 36.4% |

| qoq %chg. | 6.3% | 52.4% | -63.1% | 101.2% | 38.2% | -15.3% | -20.0% | 46.4% | 26.7% | 21.1% | 20.6% | 5.5% | 6.0% | -6.1% | 27.4% | 0.0% | 6.5% | -2.2% | 30.9% | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

| as a %of sales | 12.8% | 18.4% | 7.1% | 12.9% | 18.1% | 15.2% | 11.6% | 14.9% | 18.9% | 21.3% | 22.7% | 23.1% | 24.1% | 22.8% | 25.1% | 25.0% | 26.5% | 26.1% | 29.3% | 29.3% | 29.3% | 29.3% | 29.3% | 29.3% |

| Pretax profits | 12,868 | 16,663 | 6,376 | 11,983 | 17,407 | 14,898 | 11,328 | 17,189 | 22,129 | 27,719 | 33,444 | 35,039 | 37,274 | 34,379 | 44,384 | 43,689 | 47,181 | 45,486 | 60,139 | 59,444 | 59,444 | 59,444 | 59,444 | 59,444 |

| as a %of sales | 14.6% | 17.8% | 7.2% | 12.1% | 17.9% | 15.2% | 11.0% | 14.6% | 18.8% | 22.0% | 23.4% | 23.7% | 24.8% | 23.0% | 25.7% | 25.2% | 27.1% | 26.3% | 29.9% | 29.5% | 29.5% | 29.5% | 29.5% | 29.5% |

| Net Profits | 9,341 | 8,931 | 32,713 | 14,860 | 25,462 | 23,435 | 30,439 | 29,952 | 41,467 | 40,981 | 40,981 | 40,981 | 40,981 | 40,981 | ||||||||||

| as a %of sales | 8,816 | 11,711 | 4,274 | 8,903 | 12,728 | 9.5% | 8.7% | 27.8% | 12.6% | 18,773 | 22,781 | 23,897 | 16.9% | 15.7% | 17.6% | 17.3% | 32,397 | 31,210 | ||||||

| 10.0% | 12.5% | 4.8% | 9.0% | 13.1% | 14.9% | 15.9% | 16.2% | 18.6% | 18.0% | 20.6% | 20.3% | 20.3% | 20.3% | 20.3% | 20.3% | |||||||||

| R&D Depreciation | 5,500 | 6,460 | 8,300 | 7,191 | 7,800 | 8,100 | 6,700 | 7,316 | 9,000 | 9,500 18,400 | 9,500 | 9,000 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 | 9,500 |

| 10,198 8,100 | 12,702 | 15,278 | 16,027 | 11,667 | 13,762 | 19,065 | 21,742 | 17,300 | 21,500 | 23,600 | 20,200 | 21,300 | 27,400 | 28,500 | 25,100 | 26,200 | 27,300 | 28,400 | 28,400 | 28,400 | 28,400 | 28,400 | ||

| Electronics Capex | 40,321 | 10,200 43,211 | 12,000 | 13,998 | 9,300 | 11,200 | 16,400 | 18,900 | 15,000 | 16,000 | 19,000 | 21,000 | 18,000 67,500 | 19,000 | 25,000 26,000 | 23,000 | 24,000 | 25,000 | 26,000 67,500 | 26,000 67,500 | 26,000 67,500 | 26,000 67,500 | 26,000 67,500 | |

| Inventory | 26,971 | 46,801 | 20,436 | 14,374 | 12,536 | 16,931 | 52,500 | 52,500 | 52,500 | 52,500 | 67,500 | 82,500 | 82,500 | 67,500 | 67,500 | 67,500 | ||||||||

| 68,054 | 69,201 | 67,175 | 67,552 | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | ||||||

| 73,136 | 68,446 | 73,426 | 70,962 | 101,050 | 105,150 26.15% | 124,750 29.41% | 124,750 23.45% | - 127,145 | 127,145 | 152,325 22.10% | 152,325 22.10% | 152,325 22.10% | 152,325 22.10% | 152,325 22.10% | ||||||||||

| Electronics yoy %chg. qoq %chg. | 44,949 -10.99% | 53,305 2.35% 18.59% | 47,163 3.41% -11.52% | 51,806 21.85% 9.84% | 56,285 25.22% | 57,262 7.42% 1.74% | 58,366 23.75% 1.93% | 71,403 37.83% 22.34% | 73,875 31.25% 3.46% | 83,350 45.56% 12.83% | 96,400 65.16% 15.66% | 41.52% 4.82% | 42.34% 4.06% | 105,150 | 18.64% | 0.00% 22,200 | 20.92% 1.92% 22,200 | 20.92% 0.00% | 19.80% 22,200 0.00% | 0.00% 22,200 | 0.00% 22,200 | 0.00% 22,200 | 0.00% 22,200 | 0.00% 22,200 |

| Ceramic | 5.73% 23,571 -3.40% | 19,564 | 18,921 -23.61% | 22,012 -6.74% | 8.65% 19,600 -16.85% | 20,089 2.68% | 20,898 10.45% | 21,967 -0.20% 5.12% | 21,100 7.65% | 21,100 5.03% | 21,600 3.36% | 21,600 -1.67% | 21,700 2.84% | 0.00% 21,700 2.84% | 22,200 2.78% | 2.78% | 22,200 2.30% 2.30% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | ||

| yoy %chg. qoq %chg. | -0.13% 19,700 | -17.49% -17.00% | -3.29% | 16.34% 25,281 | -10.96% 21,579 | 2.49% 20,670 | 4.03% 23,872 | 24,210 | -3.95% | 0.00% 21,670 | 2.37% | 0.00% | 0.46% 23,579 | 0.00% 22,670 | 2.30% 25,872 | 0.00% 26,210 | 0.00% 24,579 | 0.00% 23,670 | 0.00% 26,872 | 0.00% 27,210 | 0.00% 27,210 | 0.00% 27,210 | 0.00% 27,210 | 0.00% 27,210 |

| Others yoy %chg. | 20,496 | 22,668 2.33% | 4.35% | 9.54% | 0.85% | 5.31% | -4.24% | 22,579 4.63% | 24,872 | 25,210 | 4.61% | 4.02% | 3.97% | 4.24% | 4.41% | 3.87% | 3.82% | 3.82% | 3.82% | 3.82% | 3.82% | |||

| -0.01% -18.69% | 18.82% 4.04% | 10.60% | 11.53% | -14.64% | -4.21% | 15.49% | 1.42% | -6.74% | 4.84% | 4.19% | 4.13% | 4.43% -6.47% | -3.86% | 14.12% | 1.31% | 13.53% | 1.26% | 1.26% | 1.26% | 1.26% | 1.26% | |||

| qoq %chg. | 88,220 -6.75% | 93,365 | 88,752 | 99,099 | 97,464 | 98,021 4.99% | 103,136 16.21% | 117,580 18.65% | 117,554 | -4.03% 126,120 | 14.78% | 1.36% 147,860 | 150,429 | 149,520 18.55% | 172,822 | 173,160 | -6.22% 173,924 | -3.70% 173,015 | 201,397 | |||||

| Total Sales yoy %chg. | -2.35% | 0.35% 5.83% | 9.69% | 10.48% -1.65% | 0.57% | 5.22% | 14.00% | 20.61% -0.02% | 28.67% | 142,872 38.53% | 25.75% | 27.97% 1.74% | -0.60% | 20.96% 15.58% | 17.11% | 15.62% | 15.71% | 16.53% | 201,735 16.50% | 201,735 16.50% | 201,735 16.50% | 201,735 16.50% | 201,735 16.50% | |

| qoq %chg. | -4.08% -4.94% | 11.66% | 7.29% | 13.28% | 3.49% | 0.20% | -0.52% | 16.40% | 0.17% | 0.17% | 0.17% | 0.17% | 0.17% | 0.17% | ||||||||||

| Operating profits | 0.44% | |||||||||||||||||||||||

| Electronics yoy %chg. | 5,314 19.39% | 12,676 9.84% | 1,920 -74.98% | 6,937 92.11% | 14,028 163.98% | 11,401 -10.06% | 7,608 296.25% -33.27% | 12,211 76.03% 60.50% 17.1% | 18,794 33.98% 53.91% 25.4% | 23,479 105.94% | 28,309 20.57% 29.4% | 29,099 272.10% 138.30% | 32,559 73.24% 11.89% | 30,359 29.30% -6.76% 28.9% | 39,069 38.01% 28.69% 31.3% | 38,069 30.83% -2.56% 30.5% | 42,506 30.55% 11.66% 33.4% | -2.35% 32.6% | 41,506 36.72% 32.18% 36.0% | 41.49% -1.82% 35.4% | 41.49% -1.82% 35.4% | 41.49% -1.82% 35.4% | 41.49% -1.82% 35.4% | |

| qoq %chg. OP margin Ceramic | 47.16% 11.8% 4,282 | 138.54% 23.8% 2,802 | -84.85% 4.1% | 261.30% 13.4% 2,881 | 102.22% 24.9% 2,096 | -18.73% 19.9% 1,743 | 13.0% 2,064 | 1,743 | 1,935 | 24.93% 28.2% | 2.79% 28.8% | 31.0% 2,215 | 2,215 | 2,315 | 2,315 | 2,175 | 2,175 | 2,275 | ||||||

| 50.88% | -4.01% -34.56% | 2,253 | -31.13% | -51.05% | -37.79% | -8.39% | -39.50% | -7.68% | 1,935 11.02% | 2,135 | 2,135 | 14.47% | 14.47% 0.00% | 8.43% | -1.81% | -1.73% | 2,275 -1.73% | 2,275 -1.73% | 2,275 -1.73% | 2,275 -1.73% | 2,275 -1.73% | 2,275 -1.73% | 2,275 -1.73% | |

| yoy %chg. qoq %chg. | 2.37% | -34.05% | 18.42% | -15.55% | 11.02% | 3.44% | 22.49% | 3.75% | 4.51% | 4.60% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | ||||||||

| OP margin | 18.2% | 14.3% | -19.59% 11.9% | 27.87% 13.1% | -27.25% | -16.84% 8.7% | 9.9% | 7.9% | 9.2% | 0.00% | 10.34% | 0.00% 9.9% | 10.2% | 10.2% | 10.4% | 8.43% 0.00% 10.4% | -1.81% 0.00% 9.8% | 10.2% | 10.2% | 10.2% | 10.2% | 10.2% | ||

| Others | 1,769 | 1,719 | 2,404 | 2,814 | 10.7% 1,503 | 1,747 | 2,242 | 3,472 | 1,500 | 9.2% | 3,000 | 1,500 | 1,500 | 3,000 | 9.8% 1,500 | -6.05% | 1,500 | 2,000 | 3,000 | 3,000 | 3,000 | 3,000 | 3,000 | |

| 9.9% 2,000 | 2,000 | 0.00% 0.00% 50.00% 11.4% -50 | 0.00% | |||||||||||||||||||||

| yoy %chg. qoq %chg. | 91.45% -37.73% | 11.84% | 36.98% | -0.95% 17.05% | -15.04% | 1.63% | -6.74% 28.33% | 23.38% 54.86% | -0.20% -56.80% | 1,500 -14.14% 0.00% | -10.79% | -13.59% 50.00% | 0.00% -50.00% | 0.00% 0.00% | 6.3% | 33.33% | 0.00% 50.00% | 0.00% 50.00% | ||||||

| -2.83% | 16.23% | 33.33% | 0.00% 33.33% | 0.00% 0.00% | ||||||||||||||||||||

| OP margin Elimination | 9.0% | 8.4% | 39.85% 10.6% | 11.1% | -46.59% 7.0% | 8.5% | 9.4% 40 | 14.3% 74 | 6.6% -50 | 8.0% | 11.9% | 6.4% | 6.6% -50 | 7.7% -50 | -50.00% 6.1% | 7.4% -50 | 11.0% -50 | 11.0% -50 | ||||||

| -232 | 132 | 9 | 46 | - | 6.9% -50 | -50 | -50 - | |||||||||||||||||

| -70 - | 20 | - | - | - | - - | -50 | - | -50 | - | - | - - | -50 | - | - | - | - | - | - | - | |||||

| yoy %chg. qoq %chg. OP margin Total OP yoy %chg. | - - 11,295 38.06% | - - - 17,217 8.34% | - - - 6,345 -50.72% | - - - 12,764 20.18% | - - 17,636 56.14% | - - 14,937 -13.24% | - - 11,954 88.40% | - 17,500 37.10% | - - 22,179 25.76% | - - - 26,864 79.85% | - - - 32,394 170.99% | - - - - 34,184 95.34% | - 36,224 63.33% | - - 34,024 26.65% | - - 43,334 33.77% | - 43,334 26.77% | - 27.35% | - | 59,089 36.36% 36.36% | - - - - 46,131 45,131 32.64% | - | - | - | - 59,089 |

Source: Company data, J.P. Morgan estimates.

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

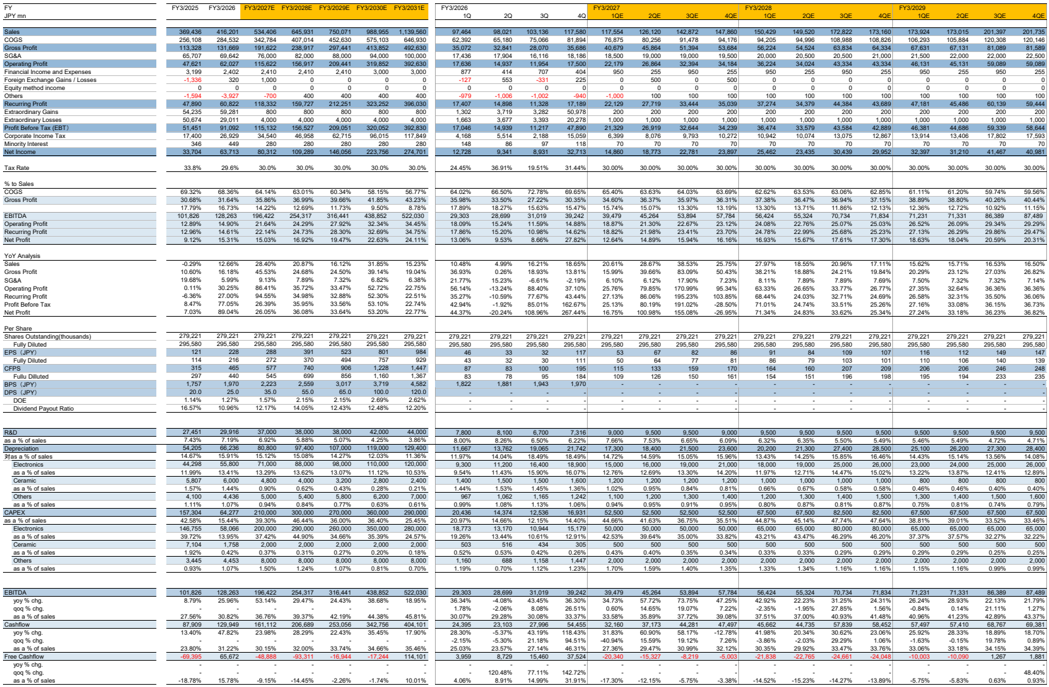

Figure 8: Profit and Loss Statement

| FY | |

|---|---|

| JPY mn Sales COGS Gross Profit SG&A Operating Profit Financial Income and Expenses Foreign Exchange Gains / Losses Equity method income Others | FY3/2025 FY3/2026 FY3/2027E FY3/2028E FY3/2029E FY3/2030E FY3/2031E FY3/2026 FY3/2027 FY3/2028 FY3/2029 1Q 2Q 3Q 4Q 1QE 2QE 3QE 4QE 1QE 2QE 3QE 4QE 1QE 2QE 3QE 4QE 369,436 416,201 534,406 645,931 750,071 988,955 1,139,560 97,464 98,021 103,136 117,580 117,554 126,120 142,872 147,860 150,429 149,520 172,822 173,160 173,924 173,015 201,397 201,735 256,108 284,532 342,784 407,014 452,630 575,103 646,930 62,392 65,180 75,066 81,894 76,875 80,256 91,478 94,176 94,205 94,996 108,988 108,826 106,293 105,884 120,308 120,146 113,328 131,669 191,622 238,917 297,441 413,852 492,630 35,072 32,841 28,070 35,686 40,679 45,864 51,394 53,684 56,224 54,524 63,834 64,334 67,631 67,131 81,089 81,589 65,707 69,642 76,000 82,000 88,000 94,000 100,000 17,436 17,904 16,116 18,186 18,500 19,000 19,000 19,500 20,000 20,500 20,500 21,000 21,500 22,000 22,000 22,500 47,621 62,027 115,622 156,917 209,441 319,852 392,630 17,636 14,937 11,954 17,500 22,179 26,864 32,394 34,184 36,224 34,024 43,334 43,334 46,131 45,131 59,089 59,089 3,199 2,402 2,410 2,410 2,410 3,000 3,000 877 414 707 404 950 255 950 255 950 255 950 255 950 255 950 255 -1,336 320 1,000 0 0 0 0 -127 553 -331 225 0 500 0 500 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 -1,594 -3,927 -700 400 400 400 400 -979 -1,006 -1,002 -940 -1,000 100 100 100 100 100 100 100 100 100 100 100 |

| Recurring Profit Extraordinary Gains Extraordinary Losses Profit Before Tax (EBT ) Corporate Income Tax Minority Interest Net Income Tax Rate %to Sales COGS Gross Profit | 47,890 60,822 118,332 159,727 212,251 323,252 396,030 17,407 14,898 11,328 17,189 22,129 27,719 33,444 35,039 37,274 34,379 44,384 43,689 47,181 45,486 60,139 59,444 54,235 59,281 800 800 800 800 800 1,302 3,719 3,282 50,978 200 200 200 200 200 200 200 200 200 200 200 200 50,674 29,011 4,000 4,000 4,000 4,000 4,000 1,663 3,677 3,393 20,278 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 1,000 51,451 91,092 115,132 156,527 209,051 320,052 392,830 17,046 14,939 11,217 47,890 21,329 26,919 32,644 34,239 36,474 33,579 43,584 42,889 46,381 44,686 59,339 58,644 17,400 26,929 34,540 46,958 62,715 96,015 117,849 4,168 5,514 2,188 15,059 6,399 8,076 9,793 10,272 10,942 10,074 13,075 12,867 13,914 13,406 17,802 17,593 346 449 280 280 280 280 280 148 86 97 118 70 70 70 70 70 70 70 70 70 70 70 70 33,704 63,713 80,312 109,289 146,056 223,756 274,701 12,728 9,341 8,931 32,713 14,860 18,773 22,781 23,897 25,462 23,435 30,439 29,952 32,397 31,210 41,467 40,981 33.8% 29.6% 30.0% 30.0% 30.0% 30.0% 30.0% 24.45% 36.91% 19.51% 31.44% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 30.00% 69.32% 68.36% 64.14% 63.01% 60.34% 58.15% 56.77% 64.02% 66.50% 72.78% 69.65% 65.40% 63.63% 64.03% 63.69% 62.62% 63.53% 63.06% 62.85% 61.11% 61.20% 59.74% 59.56% 30.68% 31.64% 35.86% 36.99% 39.66% 41.85% 43.23% 35.98% 33.50% 27.22% 30.35% 34.60% 36.37% 35.97% 36.31% 37.38% 36.47% 36.94% 37.15% 38.89% 38.80% 40.26% 40.44% 17.79% 16.73% 14.22% 12.69% 11.73% 9.50% 8.78% 17.89% 18.27% 15.63% 15.47% 15.74% 15.07% 13.30% 13.19% 13.30% 13.71% 11.86% 12.13% 12.36% 12.72% 10.92% 11.15% |

| Per Share Shares Outstanding(thousands) Fully Diluted EPS ( JPY ) Fully Diluted | 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 279,221 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 295,580 121 228 288 391 523 801 984 46 33 32 117 53 67 82 86 91 84 109 107 116 112 149 114 216 272 370 494 757 929 43 32 30 111 50 64 77 81 86 79 103 101 110 106 140 315 465 577 740 906 1,228 1,447 87 83 100 195 115 133 159 170 164 160 207 209 206 206 246 297 440 545 699 856 1,160 1,367 83 78 95 184 109 126 150 161 154 151 196 198 195 194 233 |

| CFPS Fullu Dilluted ( ) | |

| DPS ( JPY ) DOE Dividend Payout Ratio R&D as a %of sales Depreciation 対 as a %of sales | 1,757 1,970 2,223 2,559 3,017 3,719 4,582 1,822 1,881 1,943 1,970 - - - - - - - - - - - 20.0 25.0 35.0 55.0 65.0 100.0 120.0 - - - - - - - - - - - - - - - 1.14% 1.27% 1.57% 2.15% 2.15% 2.69% 2.62% - - - - - - - - - - - - - - - 16.57% 10.96% 12.17% 14.05% 12.43% 12.48% 12.20% - - - - - - - - - - - - - - - |

| 27,451 29,916 37,000 38,000 38,000 42,000 44,000 7,800 8,100 6,700 7,316 9,000 9,500 9,500 9,000 9,500 9,500 9,500 9,500 9,500 9,500 9,500 7.43% 7.19% 6.92% 5.88% 5.07% 4.25% 3.86% 8.00% 8.26% 6.50% 6.22% 7.66% 7.53% 6.65% 6.09% 6.32% 6.35% 5.50% 5.49% 5.46% 5.49% 4.72% 54,205 66,236 80,800 97,400 107,000 119,000 129,400 11,667 13,762 19,065 21,742 17,300 18,400 21,500 23,600 20,200 21,300 27,400 28,500 25,100 26,200 27,300 14.67% 15.91% 15.12% 15.08% 14.27% 12.03% 11.36% 11.97% 14.04% 18.49% 18.49% 14.72% 14.59% 15.05% 15.96% 13.43% 14.25% 15.85% 16.46% 14.43% 15.14% 13.56% 44,298 55,800 71,000 88,000 98,000 110,000 120,000 9,300 11,200 16,400 18,900 15,000 16,000 19,000 21,000 18,000 19,000 25,000 26,000 23,000 24,000 25,000 11.99% 13.41% 13.29% 13.62% 13.07% 11.12% 10.53% 9.54% 11.43% 15.90% 16.07% 12.76% 12.69% 13.30% 14.20% 11.97% 12.71% 14.47% 15.02% 13.22% 13.87% 12.41% | |

| 9,500 4.71% 28,400 14.08% 26,000 12.89% 5,807 6,000 4,800 4,000 3,200 2,800 2,400 1,400 1,500 1,500 1,600 1,200 1,200 1,200 1,200 1,000 1,000 1,000 1,000 800 800 800 800 1.57% 1.44% 0.90% 0.62% 0.43% 0.28% 0.21% 1.44% 1.53% 1.45% 1.36% 1.02% 0.95% 0.84% 0.81% 0.66% 0.67% 0.58% 0.58% 0.46% 0.46% 0.40% 0.40% | |

| Electronics as a %of sales Ceramic | 4,100 4,436 5,000 5,400 5,800 6,200 7,000 967 1,062 1,165 1,242 1,100 1,200 1,300 1,400 1,200 1,300 1,400 1,500 1,300 1,400 1,500 1.11% 1.07% 0.94% 0.84% 0.77% 0.63% 0.61% 0.99% 1.08% 1.13% 1.06% 0.94% 0.95% 0.91% 0.95% 0.80% 0.87% 0.81% 0.87% 0.75% 0.81% 0.74% 157,304 64,277 210,000 300,000 270,000 360,000 290,000 20,436 14,374 12,536 16,931 52,500 52,500 52,500 52,500 67,500 67,500 82,500 82,500 67,500 67,500 67,500 42.58% 15.44% 39.30% 46.44% 36.00% 36.40% 25.45% 20.97% 14.66% 12.15% 14.40% 44.66% 41.63% 36.75% 35.51% 44.87% 45.14% 47.74% 47.64% 38.81% 39.01% 33.52% 146,755 58,066 200,000 290,000 260,000 350,000 280,000 18,773 13,170 10,944 15,179 50,000 50,000 50,000 50,000 65,000 65,000 80,000 80,000 65,000 65,000 65,000 |

| as a %of sales Others as a %of sales CAPEX as a %of sales | 39.72% 13.95% 37.42% 44.90% 34.66% 35.39% 24.57% 19.26% 13.44% 10.61% 12.91% 42.53% 39.64% 35.00% 33.82% 43.21% 43.47% 46.29% 46.20% 37.37% 37.57% 32.27% 7,104 1,758 2,000 2,000 2,000 2,000 2,000 503 516 434 305 500 500 500 500 500 500 500 500 500 500 500 |

| Electronics as a %of sales | 1.92% 0.42% 0.37% 0.31% 0.27% 0.20% 0.18% 0.52% 0.53% 0.42% 0.26% 0.43% 0.40% 0.35% 0.34% 0.33% 0.33% 0.29% 0.29% 0.29% 0.29% 0.25% |

| Ceramic | |

| as a %of sales | 3,445 4,453 8,000 8,000 8,000 8,000 8,000 1,160 688 1,158 1,447 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 2,000 |

| Others as a %of sales | 0.93% 1.07% 1.50% 1.24% 1.07% 0.81% 0.70% 1.19% 0.70% 1.12% 1.23% 1.70% 1.59% 1.40% 1.35% 1.33% 1.34% 1.16% 1.16% 1.15% 1.16% 0.99% |

| 101,826 128,263 196,422 254,317 316,441 438,852 522,030 29,303 28,699 31,019 39,242 39,479 45,264 53,894 57,784 56,424 55,324 70,734 71,834 71,231 71,331 86,389 | |

| 0.25% 2,000 0.99% 87,489 | |

| YoY Analysis Sales Gross Profit SG&A Operating Profit Recurring Profit Profit Before Tax | -0.29% 12.66% 28.40% 20.87% 16.12% 31.85% 15.23% 10.48% 4.99% 16.21% 18.65% 20.61% 28.67% 38.53% 25.75% 27.97% 18.55% 20.96% 17.11% 15.62% 15.71% 16.53% 16.50% 10.60% 16.18% 45.53% 24.68% 24.50% 39.14% 19.04% 36.93% 0.26% 18.93% 13.81% 15.99% 39.66% 83.09% 50.43% 38.21% 18.88% 24.21% 19.84% 20.29% 23.12% 27.03% 26.82% 19.68% 5.99% 9.13% 7.89% 7.32% 6.82% 6.38% 21.77% 15.23% -6.61% -2.19% 6.10% 6.12% 17.90% 7.23% 8.11% 7.89% 7.89% 7.69% 7.50% 7.32% 7.32% 7.14% 0.11% 30.25% 86.41% 35.72% 33.47% 52.72% 22.75% 56.14% -13.24% 88.40% 37.10% 25.76% 79.85% 170.99% 95.34% 63.33% 26.65% 33.77% 26.77% 27.35% 32.64% 36.36% 36.36% -6.36% 27.00% 94.55% 34.98% 32.88% 52.30% 22.51% 35.27% -10.59% 77.67% 43.44% 27.13% 86.06% 195.23% 103.85% 68.44% 24.03% 32.71% 24.69% 26.58% 32.31% 35.50% 36.06% 8.47% 77.05% 26.39% 35.95% 33.56% 53.10% 22.74% 42.94% -1.92% 85.01% 162.67% 25.13% 80.19% 191.02% -28.50% 71.01% 24.74% 33.51% 25.26% 27.16% 33.08% 36.15% 36.73% |

| Net Profit | 7.03% 89.04% 26.05% 36.08% 33.64% 53.20% 22.77% 44.37% -20.24% 108.96% 267.44% 16.75% 100.98% 155.08% -26.95% 71.34% 24.83% 33.62% 25.34% 27.24% 33.18% 36.23% 36.82% 279,221 295,580 |

| BPS JPY | 147 139 248 235 - |

| - - - | |

| 1,600 0.79% 67,500 | |

| 33.46% 65,000 32.22% 500 | |

| EBITDA yoy %chg. | |

| 8.79% 25.96% 53.14% 29.47% 24.43% 38.68% 18.95% 36.34% -4.08% 43.45% 36.30% 34.73% 57.72% 73.75% 47.25% 42.92% 22.23% 31.25% 24.31% 26.24% 28.93% 22.13% - - - - - - - 1.78% -2.06% 8.08% 26.51% 0.60% 14.65% 19.07% 7.22% -2.35% -1.95% 27.85% 1.56% -0.84% 0.14% 21.11% | |

| qoq %chg. | 21.79% 1.27% 27.56% 30.82% 36.76% 39.37% 42.19% 44.38% 45.81% 30.07% 29.28% 30.08% 33.37% 33.58% 35.89% 37.72% 39.08% 37.51% 37.00% 40.93% 41.48% 40.96% 41.23% 42.89% 43.37% |

| as a %of sales Cashflow | 87,909 129,949 161,112 206,689 253,056 342,756 404,101 24,395 23,103 27,996 54,455 32,160 37,173 44,281 47,497 45,662 44,735 57,839 58,452 57,497 57,410 68,767 13.40% 47.82% 23.98% 28.29% 22.43% 35.45% 17.90% 28.30% -5.37% 43.19% 118.43% 31.83% 60.90% 58.17% -12.78% 41.98% 20.34% 30.62% 23.06% 25.92% 28.33% 18.89% |

| yoy %chg. | 69,381 - - - - - - - -2.15% -5.30% 21.18% 94.51% -40.94% 15.59% 19.12% 7.26% -3.86% -2.03% 29.29% 1.06% -1.63% -0.15% 19.78% 23.80% 31.22% 30.15% 32.00% 33.74% 34.66% 35.46% 25.03% 23.57% 27.14% 46.31% 27.36% 29.47% 30.99% 32.12% 30.35% 29.92% 33.47% 33.76% 33.06% 33.18% 34.15% |

| qoq %chg. | 18.70% -69,395 65,672 -48,888 -93,311 -16,944 -17,244 114,101 3,959 8,729 15,460 37,524 -20,340 -15,327 -8,219 -5,003 -21,838 -22,765 -24,661 -24,048 -10,003 -10,090 1,267 |

| as a %of sales | 0.89% 34.39% 1,881 - - - - - - - - - - - - - - - - - - - - - - |

| Free Cashflow | |

| yoy %chg. | - - - - - - - - 120.48% 77.11% 142.72% - - - - - - - - - - - |

| qoq %chg. | |

| -18.78% 15.78% -9.15% -14.45% -2.26% -1.74% 10.01% 4.06% 8.91% 14.99% 31.91% -17.30% -12.15% -5.75% -3.38% -14.52% -15.23% -14.27% -13.89% -5.75% -5.83% 0.63% | |

| as a %of sales | |

| 48.40% 0.93% | |

| - |

Source: Company data, J.P. Morgan estimates.

Asia Pacific Equity Research 15 July 2026

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

Figure 9: Balance Sheet

| FY | FY3/2019 | FY3/2020 | FY3/2021 | FY3/2022 | FY3/2023 | FY3/2024 FY3/2025 | FY3/2026 | FY3/2027E | FY3/2028E | FY3/2029E | FY3/2030E | FY3/2031E | FY3/2025 | 3Q | FY3/2026 1Q 2Q | 3Q 4Q | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Assets | ||||||||||||||||||||||||||

| Cash and Cash Equivalents | 113,492 | 175,151 | 126,884 | 185,592 | 302,419 | 443,583 | 390,656 295,681 | 308,575 | 382,211 | 502,627 | 564,242 | 194,393 | 758,743 | 425,295 374,233 | 358,431 390,656 | 374,228 | 325,476 | 340,725 295,681 | ||||||||

| Accounts Receivable | 60,180 | 68,877 | 89,687 | 91,989 | 79,446 | 65,330 | 68,131 81,810 | 105,045 | 126,967 | 147,437 | 223,996 | 65,792 | 60,301 68,694 | 64,831 | 68,316 | 72,064 81,810 70,962 | ||||||||||

| Inventories | 48,769 | 45,279 | 57,023 | 74,566 | 79,194 | 65,318 | 67,175 70,962 | 85,490 | 101,509 | 112,886 | 143,430 | 161,344 | 68,054 | 69,201 73,136 | 68,131 67,175 | 67,552 68,446 | 73,426 | |||||||||

| Other Current Assets Total Current Assets | 6,531 | 10,937 | 11,770 | 11,123 363,270 | 15,766 476,825 | 26,579 600,810 | 23,618 17,088 465,541 | 17,088 516,198 | 17,088 627,774 | 17,088 780,038 | 17,088 919,152 | 17,088 1,161,170 | 31,038 590,179 | 35,521 22,973 539,256 523,234 | 23,618 25,767 549,580 | 25,237 487,475 | 18,509 17,088 504,724 465,541 | |||||||||

| 228,972 | 300,244 | 285,364 | 549,580 | 532,378 | ||||||||||||||||||||||

| Tangible Fixed Assets | 146,710 | 173,514 | 214,828 | 225,920 | 306,967 | 408,777 | 460,054 437,704 | 566,904 | 769,504 | 932,504 | 1,173,504 | 1,334,104 | 444,516 460,076 | 476,005 460,054 | 465,519 | 465,165 | 459,875 437,704 | |||||||||

| Investments and Other Assets | 47,374 | 44,861 | 78,326 | 75,142 | 73,716 | 120,404 | 72,050 57,180 | 57,180 | 57,180 | 57,180 | 57,180 | 57,180 | 113,014 100,671 | 106,443 | 72,050 81,782 | 85,298 | 89,519 57,180 | |||||||||

| Total Investments | 68,198 | 61,342 | 110,166 | 58,797 | 32,285 | 32,285 | 32,285 | 32,285 | 32,285 | 32,285 | 90,711 3,916 | 95,782 | 70,452 | 73,665 | 77,826 32,285 18,331 | |||||||||||

| Deferred Tax Assets | 39,142 2,915 | 34,461 4,463 | 3,488 | 64,638 3,951 | 5,533 | 4,253 | 7,159 | 18,331 | 18,331 | 18,331 | 18,331 | 18,331 | 18,331 | 102,303 4,342 | 4,125 | 58,797 7,159 5,271 | 5,240 | 5,316 | ||||||||

| Intangible Assets Other non current asset | 4,162 1,155 | 4,486 1,451 | 5,392 1,248 | 5,448 1,105 | 5,179 | 4,590 | 4,349 4,418 | 2,146 | 4,418 2,146 | 4,418 2,146 | 4,418 2,146 | 4,418 2,146 | 4,418 2,146 | 4,754 4,404 4,666 1,615 | 1,640 1,870 | 1,745 532,104 | 4,349 4,269 4,617 1,790 | 4,529 4,418 1,848 | ||||||||

| Total Non Current Assets | 194,084 | 218,375 | 293,154 | 301,062 | 1,662 380,683 | 1,395 529,181 | 1,745 532,104 | 494,884 | 624,084 | 826,684 | 989,684 | 1,230,684 | 1,391,284 | 557,530 | 560,747 582,448 | 547,301 | 1,776 550,463 | 2,146 549,394 494,884 | ||||||||

| Total Assets | 423,056 | 664,332 | 857,508 | 1,129,991 | 1,081,684 | 960,425 | 1,140,282 | 1,454,458 | 1,769,722 | 2,149,836 | 2,552,454 | 1,147,709 1,100,003 | 1,105,682 | 1,081,684 1,079,679 | 1,037,938 1,054,118 960,425 | |||||||||||

| Equity | 518,619 578,518 | |||||||||||||||||||||||||

| Liabilities and Accounts Payable | 39,562 | 45,555 | 45,717 | 51,150 | 40,431 | 43,875 | 44,143 | 53,180 63,145 | 70,222 | 89,223 | 100,366 44,223 | 42,354 | 48,936 | 36,237 | 38,761 38,442 | 45,710 44,143 | ||||||||||

| Short-term debt | 45,030 | 30,030 | 35,130 | 40,030 | 65,030 | 90,000 | 38,761 90,000 | 15,000 | 15,000 | 15,000 | 15,000 | 15,000 | 15,000 | 90,000 70,000 | 60,000 | 90,000 | 65,000 | 65,000 15,000 22,013 | ||||||||

| 2,366 | 3,016 | 5,624 | 14,909 | 14,869 | 22,013 | 22,013 | 22,013 | 22,013 | 22,013 | 4,151 | 2,286 | 90,000 14,869 | 4,601 9,839 | 2,185 | ||||||||||||

| Accrued Taxes Advanced Payment | 0 | 0 | 0 | 0 | 14,268 0 | 4,144 | 92,084 | 80,950 | 180,950 | 390,950 | 570,950 | 735,950 | 22,013 885,950 | 77,019 | 7,059 88,643 87,112 | 92,084 | 89,764 77,577 | 76,929 80,950 | ||||||||

| Other Non Current Financial Liabilities Total Current Liabilities | 31,124 118,082 | 42,135 120,736 | 45,428 131,899 | 50,071 156,160 | 103,592 223,321 | 80,098 140,245 358,362 | 92,003 327,717 | 59,539 221,645 | 59,539 330,682 | 59,539 550,647 | 59,539 737,724 | 59,539 921,725 | 59,539 1,082,868 | 150,589 365,982 | 111,070 96,065 319,126 294,399 | 92,003 327,717 | 85,294 305,896 | 70,962 69,403 59,539 261,820 259,227 221,645 | ||||||||

| LT Debts | 25,000 | 120,000 - | 115,044 | 130,000 | 205,000 | 253,476 | 252,976 | 177,476 | 177,476 177,476 | 177,476 | 177,476 | 177,476 | 253,351 | 273,226 283,101 252,976 | 252,851 | 237,726 | 237,601 177,476 - | |||||||||

| Operating Lease Liabilities | 43 1,974 | - 7,117 | - 5,095 | - 825 | - 13,433 | - 1,015 | - 1,284 | - 1,284 | - 1,284 | - 1,284 | - 1,284 | - 1,284 | - | - - | - | - | 4,859 1,284 | |||||||||

| Deferred Tax Liabilities | 1,644 827 | 1,078 | 578 | 573 | 751 | 800 | 633 | 633 | 633 | 633 | 633 | 633 | 10,991 817 | 7,745 9,130 756 860 | - 1,015 | 2,749 3,621 | 633 | |||||||||

| Retirement Benefit Liabilities Other Non Current Financial Liabilities | 671 | 1,517 | 1,771 | 2,183 | 2,173 | 1,975 | 1,975 | 1,975 | 1,849 1,876 | 800 1,878 | 808 855 | 932 1,958 1,975 | ||||||||||||||

| Total Non Current Liabilities | 981 | 1,478 | 1,975 | 1,975 | 1,975 | 2,013 | 1,793 1,763 | |||||||||||||||||||

| 28,669 | 123,949 | 124,756 | 137,444 | 208,581 | 269,833 | 1,878 256,669 | 181,368 | 181,368 | 181,368 | 181,368 | 181,368 | 181,368 | 267,172 | 283,576 294,967 | 256,669 | 258,201 243,965 | 245,350 181,368 | |||||||||

| Minority Interests Capital Stock | 5,442 64,152 | 5,615 64,152 | 5,949 64,152 | 6,152 64,152 | 6,367 64,152 | 6,852 64,152 | 6,803 64,152 | 7,339 64,152 | 7,619 64,152 | 7,899 64,152 | 8,179 64,152 | 8,459 64,152 | 8,739 64,152 | 6,917 64,152 64,152 64,152 | 6,918 6,779 | 6,803 6,981 | 7,055 64,152 64,152 64,152 64,565 | 7,144 7,339 64,152 64,152 64,565 64,565 | ||||||||

| Capital Surplus Retained Earnings Treasury Shares | 64,579 122,144 | 64,579 128,578 | 64,433 149,379 | 64,494 184,612 | 64,494 229,804 | 64,494 255,698 | 64,565 283,807 | 64,565 340,525 | 64,565 411,065 | 64,565 504,996 | 64,565 632,902 | 64,565 828,736 | 64,565 1,069,931 | 64,494 64,494 261,717 | 64,600 273,428 274,904 | 64,565 283,807 | 293,738 303,078 | 64,565 307,813 340,525 | ||||||||

| Other Equity | -2,602 | -2,575 | -3,286 | -3,264 54,582 | -3,126 63,915 | -2,983 113,583 | -3,497 | -3,452 84,283 | -3,452 | -3,452 84,283 | -3,452 84,283 | -3,452 | -3,452 | -2,873 | -2,861 -3,500 91,170 | -3,497 | -3,453 -3,442 89,599 96,745 | -3,448 -3,452 109,315 84,283 | ||||||||

| Shareholder's Equity | 22,590 270,863 | 13,585 268,319 | 41,236 315,914 | 364,576 | 419,239 | 494,944 | 81,468 490,495 | 550,073 | 84,283 620,613 | 714,544 | 842,450 | 84,283 1,038,284 | 84,283 1,279,479 | 120,148 507,638 | 109,381 490,383 509,537 | 81,468 490,495 | 508,601 525,098 | 542,397 550,073 | ||||||||

| Total Liabilities and Equity | 423,056 518,619 578,518 | 664,332 | 857,508 | 1,129,991 | 1,081,684 | 960,425 | 1,140,282 | 1,454,458 | 1,769,722 | 2,149,836 | 2,552,454 | 1,147,709 1,100,003 1,105,682 | 1,081,684 1,079,679 1,037,938 | 1,054,118 960,425 | ||||||||||||

| FY | FY3/2019 | |||||||||||||||||||||||||

| FY3/2020 | FY3/2021 | FY3/2022 | FY3/2023 | FY3/2024 | FY3/2025 | FY3/2026 | FY3/2027E | FY3/2028E | FY3/2029E | FY3/2030E | FY3/2031E | FY3/2025 | FY3/2026 | 4Q | ||||||||||||

| 1Q 2Q | 3Q | 4Q 1Q | 2Q | 3Q | ||||||||||||||||||||||

| JPYmn | ||||||||||||||||||||||||||

| Debt with interest | 70,030 | 150,030 | 150,174 | 170,030 | 270,030 | 343,476 | 342,976 44,404 | 192,476 | 192,476 | 192,476 | 192,476 | 192,476 | 192,476 319,683 | 420,370 -4,925 | 431,869 430,213 57,636 | 435,060 432,615 44,404 58,387 | 380,303 | 379,530 273,426 38,805 | ||||||||

| Net Debt | -43,462 | -25,121 | 23,290 -44,908 | -15,562 -80,200 | -32,389 -93,731 | -20,009 -130,175 | -14,393 | -22,255 | 64,851 | 201,215 | 260,799 228,514 | 364,184 331,899 | 287,398 | -107,228 | 71,782 -33,075 -24,000 | -12,065 | 54,827 -18,838 | -22,255 -39,021 -54,540 | ||||||||

| Net Debt (Including Investment Securities) Consolidated Employees (Persons) Non-Consolidated Employees (Persons) | -82,604 14,718 3,525 | -59,582 13,019 3,537 | 13,161 3,504 | 12,958 3,549 | 12,744 3,669 | 11,375 3,829 | 11,168 3,920 | -54,540 11,105 4,036 | 32,566 - - | 168,930 - - | - - | - | - - | - - - - | -14,393 - - | - - - - | - - - | - - | ||||||||

| Total Asset Composition Ratio Current Assets | 54.12% | 57.89% | 49.33% | 54.68% | 55.61% | 53.17% | 50.81% | 48.47% | 45.27% | 43.16% | 44.08% | 42.75% | 45.49% 52.27% | 51.42% 49.02% 38.73% | 47.32% 41.82% 43.05% | 50.81% 49.31% 42.53% | 46.97% 44.82% | 47.88% 48.47% 43.63% 45.57% | ||||||||

| Tangible Fixed Assets Current Liabilities | 34.68% | 33.46% 23.28% | 37.13% 22.80% | 34.01% 23.51% | 35.80% 26.04% | 36.18% 31.71% | 42.53% 30.30% | 45.57% 23.08% | 49.72% | 52.91% 37.86% | 52.69% 41.69% | 54.59% 42.87% | 31.89% | 29.01% 26.63% | 43.12% 30.30% 28.33% | 25.23% | 24.59% 23.08% | |||||||||

| Shareholders' Equity | 64.03% | 51.74% 54.61% | 54.88% | 48.89% | 47.60% | 44.23% 44.58% 46.08% | 45.35% 47.11% 50.59% | |||||||||||||||||||

| Efficiency Analysis | 0.59 | 0.37 | 0.41 | 0.51 | 0.50 | 0.47 | 0.50 | 0.31 | 0.33 | 0.32 0.36 | 0.36 0.37 | 0.39 | 0.47 | 0.47 | 0.47 | 0.47 | 0.47 | 0.47 | 0.47 | 0.47 | 0.47 | |||||

| Total Asset Turnover | 27.91% | 43.80% | 45.35% | 57.27% | 29.00% 54.43% | 49.13% | 48.30% | 42.42% 50.13% | 753.07 | 1,098.40 | 1,133.88 1,007.06 | 1,011.78 | 51.46% 57.27% | 51.46% 57.27% | 51.46% 57.27% | 51.46% 57.27% | 51.46% 57.27% | 51.46% 57.27% | 51.46% 57.27% | |||||||

| 0.68 | 0.63 | 0.65 | 0.55 | 0.33 1,092.56 | 0.48 | 1,177.96 | 985.67 | 925.48 781.71 | ||||||||||||||||||

| Turnover Period (Months) Tangible Fixed Asset Turnover | 538.79 1.95 | 580.60 1.85 | 619.02 1.67 | 565.44 1.82 | 665.16 1.57 | 978.97 1.04 | 0.85 | 895.44 0.93 | 717.39 1.06 | 733.11 0.97 | 784.48 0.88 | 723.31 0.94 | 0.91 401.59 | 0.83 0.83 441.30 442.05 | 0.76 | 0.84 | 0.85 0.84 | 0.89 1.05 409.22 348.29 | ||||||||

| Turnover Period (Months) Accounts Receivable Turnover | 186.82 4.76 | 197.44 4.59 | 219.11 4.08 | 200.52 4.42 | 232.91 4.87 | 352.55 5.12 | 429.20 5.54 | 393.66 5.55 | 343.07 5.72 | 377.59 5.57 | 414.12 5.47 | 388.64 5.79 | 5.45 | 481.21 5.38 5.92 5.50 | 429.20 5.54 | 429.20 5.54 | 430.96 433.28 433.20 5.79 5.86 5.89 | 5.88 6.11 | 429.20 5.54 | 429.20 5.54 | 429.20 5.54 | 429.20 5.54 | 429.20 5.54 | 429.20 5.54 | 429.20 5.54 | 429.20 5.54 |

Source: Company data, J.P. Morgan estimates.

Asia Pacific Equity Research 15 July 2026

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

Figure 10: Cash Flow Statement

| FY | FY3/2017 FY3/2018 | FY3/2017 FY3/2018 | FY3/2019 | FY3/2020 | FY3/2021 | FY3/2022 | FY3/2023 | FY3/2024 | FY3/2025 | FY3/2026 | FY3/2027E | FY3/2028E | FY3/2029E | FY3/2030E | FY3/2031E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| JPY mn | |||||||||||||||

| Net Income | -62,848 | 11,583 | 3,306 | 11,329 | 25,698 | 41,232 | 52,187 | 31,490 | 33,704 | 63,713 | 80,312 | 109,289 | 146,056 | 223,756 | 274,701 |

| Minority Interest | 230 | 270 | 267 | 207 | 220 | 331 | 226 | 259 | 346 | 449 | 280 | 280 | 280 | 280 | 280 |

| Depreciation | 33,147 | 24,566 | 25,136 | 24,222 | 35,413 | 52,715 | 54,914 | 46,032 | 54,205 | 66,236 | 80,800 | 97,400 | 107,000 | 119,000 | 129,400 |

| Change in Working Capital | 1,123 | -4,421 | -6,366 | 786 | -32,392 | -14,412 | -2,804 | 31,436 | -9,772 | -12,084 | -28,725 | -27,976 | -24,770 | -58,500 | -36,374 |

| Change in Other Current Assets | 4,351 | 817 | -962 | 7,255 | 5,068 | 14,575 | 48,237 | 95,814 | -22,570 | -29,924 | 100,000 | 210,000 | 180,000 | 165,000 | 150,000 |

| CAPEX | -20,997 | -22,409 | -22,892 | -57,076 | -78,189 | -60,615 | -131,275 | -146,583 | -157,304 | -64,277 | -210,000 | -300,000 | -270,000 | -360,000 | -290,000 |

| Change in Investments | -5,046 | -7,848 | 12,812 | 4,681 | -33,737 | 3,560 | 3,296 | -48,824 | 51,369 | 26,512 | 0 | 0 | 0 | 0 | 0 |

| Change in Intangible assets | 955 | 524 | -473 | -324 | -906 | -56 | 269 | 589 | 241 | -69 | 0 | 0 | 0 | 0 | 0 |

| Change in Other Fixed Assets | 704 | -708 | -3,840 | -1,564 | 6,941 | -2,588 | -6,002 | 14,323 | -15,920 | -11,374 | 0 | 0 | 0 | 0 | 0 |

| FCF | -48,381 | 2,374 | 6,988 | -10,484 | -71,884 | 34,742 | 19,048 | 24,536 | -65,701 | 39,182 | 22,667 | 88,993 | 138,566 | 89,536 | 228,008 |

| Change in Interest Bearing Debt | -66 | -56 | 25 | 80,000 | 144 | 19,856 | 100,000 | 73,446 | -500 | -150,500 | 0 | 0 | 0 | 0 | 0 |

| Dividends | -4,658 | -4,890 | -4,890 | -4,891 | -4,886 | -5,584 | -6,982 | -5,588 | -5,584 | -6,981 | -9,773 | -15,357 | -18,149 | -27,922 | -33,506 |

| Treasury Stock | -3 | 15,696 | 7 | 27 | -711 | 22 | 138 | 143 | -514 | 45 | 0 | 0 | 0 | 0 | 0 |

| CF from Other Financial Activities | -3,308 | 2,293 | -8,758 | -9,009 | 27,494 | 12,992 | 9,320 | 49,660 | -32,055 | 2,801 | 0 | 0 | 0 | 0 | 0 |

| CF | -56,416 | 15,417 | -6,628 | 55,643 | -49,843 | 62,028 | 121,524 | 142,197 | -104,354 | -115,453 | 12,894 | 73,636 | 120,416 | 61,614 | 194,501 |

| Cash and Cash Equivalents | 104,181 | 117,760 | 113,492 | 175,151 | 126,884 | 185,592 | 302,419 | 443,583 | 390,656 | 295,681 | 308,575 | 382,211 | 502,627 | 564,242 | 758,743 |

| Key financial index | |||||||||||||||

| ROE | -21.53% | 4.31% | 1.20% | 4.20% | 8.80% | 12.12% | 13.32% | 6.89% | 6.84% | 12.25% | 13.72% | 16.37% | 18.76% | 23.79% | 23.70% |

| ROA | -14.25% | 2.75% | 0.77% | 2.41% | 4.68% | 6.64% | 6.86% | 3.17% | 3.05% | 6.24% | 7.65% | 8.42% | 9.06% | 11.42% | 11.68% |

| Total Asset Turnover | 0.604 | 0.713 | 0.677 | 0.629 | 0.590 | 0.646 | 0.549 | 0.373 | 0.334 | 0.408 | 0.509 | 0.498 | 0.465 | 0.505 | 0.485 |

| Equity Ratio | 63.22% | 64.43% | 64.03% | 51.74% | 54.61% | 54.88% | 48.89% | 43.80% | 45.35% | 57.27% | 54.43% | 49.13% | 47.60% | 48.30% | 50.13% |

| DuPont System | |||||||||||||||

| ROE | -21.53% | 4.31% | 1.20% | 4.20% | 8.80% | 12.12% | 13.32% | 6.89% | 6.84% | 12.25% | 13.72% | 16.37% | 18.76% | 23.79% | 23.70% |

| Net Profit Margin | -23.59% | 3.86% | 1.14% | 3.83% | 7.94% | 10.28% | 12.50% | 8.50% | 9.12% | 15.31% | 15.03% | 16.92% | 19.47% | 22.63% | 24.11% |

| Total Asset Turnover | 60.43% | 71.34% | 67.74% | 62.87% | 58.96% | 64.55% | 54.87% | 37.28% | 33.41% | 40.76% | 50.88% | 49.79% | 46.53% | 50.46% | 48.47% |

| Financial Leverage Ratio | 1.58 | 1.55 | 1.56 | 1.93 | 1.83 | 1.82 | 2.05 | 2.28 | 2.21 | 1.75 | 1.84 | 2.04 | 2.10 | 2.07 | 1.99 |

Source: Company data, J.P. Morgan estimates.

Asia Pacific Equity Research 15 July 2026

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

ROIC Valuation

| ROIC Valuation | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| FY | FY3/2016 | FY3/2017 | FY3/2018 | FY3/2019 | FY3/2020 | FY3/2021 | FY3/2022 | FY3/2023 | FY3/2024 | FY3/2025 | FY3/2026 | FY3/2027E | FY3/2028E | FY3/2029E | FY3/2030E | FY3/2031E |

| JPY mn | ||||||||||||||||

| NOPAT | 15,405 | 8,604 | 11,786 | 4,958 | 14,018 | 32,108 | 50,809 | 54,901 | 34,180 | 34,999 | 46,697 | 83,983 | 112,890 | 149,657 | 227,096 | 278,041 |

| yoy %chg. | - | -44.15% | 37.00% | -57.94% | 182.76% | 129.06% | 58.24% | 8.05% | -37.74% | 2.40% | 33.42% | 79.85% | 34.42% | 32.57% | 51.74% | 22.43% |

| Invested Capital | 402,441 | 332,668 | 359,036 | 345,394 | 421,145 | 475,666 | 541,902 | 690,928 | 854,452 | 834,130 | 732,841 | 803,661 | 897,872 | 1,026,058 | 1,222,172 | 1,463,647 |

| yoy %chg. | - | -17.34% | 7.93% | -3.80% | 21.93% | 12.95% | 13.92% | 27.50% | 23.67% | -2.38% | -12.14% | 9.66% | 11.72% | 14.28% | 19.11% | 19.76% |

| ROIC | 3.83% | 2.34% | 3.41% | 1.41% | 3.66% | 7.16% | 9.99% | 8.91% | 4.42% | 4.15% | 5.96% | 10.93% | 13.27% | 15.56% | 20.20% | 20.70% |

| WACC | 8.00% | 7.11% | 7.41% | 7.08% | 6.66% | 7.09% | 4.81% | 5.76% | 8.34% | 6.49% | 11.65% | 5.90% | 5.90% | 5.90% | 5.90% | 5.90% |

| ROIC-WACC | -4.18% | -4.77% | -4.01% | -5.68% | -3.00% | 0.08% | 5.18% | 3.15% | -3.92% | -2.35% | -5.69% | 5.04% | 7.37% | 9.66% | 14.31% | 14.81% |

| ROIC/WACC | 0.48 | 0.33 | 0.46 | 0.20 | 0.55 | 1.01 | 2.08 | 1.55 | 0.53 | 0.64 | 0.51 | 1.85 | 2.25 | 2.64 | 3.43 | 3.51 |

| EV/IC | 0.41 | 0.35 | 0.43 | 0.42 | 0.59 | 1.04 | 1.39 | 0.82 | 1.12 | 0.89 | 1.15 | 1.16 | 1.19 | 1.10 | 1.01 | 0.81 |

| EV | 165,811 | 117,326 | 153,855 | 144,332 | 246,870 | 493,595 | 753,626 | 565,241 | 960,706 | 743,545 | 845,796 | 932,902 | 1,069,266 | 1,128,849 | 1,232,235 | 1,187,734 |

| MV | 242,708 | 195,552 | 253,564 | 226,936 | 306,452 | 538,503 | 833,826 | 658,972 | 1,090,881 | 757,938 | 900,336 | 900,336 | 900,336 | 900,336 | 900,336 | 900,336 |

| Theoretical Enterprise Value | 192,440 | 109,500 | 165,026 | 68,630 | 231,427 | 480,738 | 1,125,944 | 1,068,419 | 453,126 | 532,711 | 374,891 | 1,490,139 | 2,020,800 | 2,707,528 | 4,187,895 | 5,139,999 |

| ΔTheoretical Enterprise Value | - | -82,940 | 55,525 | -96,395 | 162,797 | 249,311 | 645,206 | -57,525 | -615,293 | 79,585 | -157,820 | 1,115,248 | 530,660 | 686,728 | 1,480,367 | 952,103 |

| ΔIC | - | -69,773 | 26,368 | -13,642 | 75,751 | 54,521 | 66,236 | 149,026 | 163,524 | -20,322 | -101,289 | 70,820 | 94,212 | 128,186 | 196,114 | 241,475 |

| ΔEVA/WACC | - | -13,167 | 29,157 | -82,753 | 87,046 | 194,790 | 578,970 | -206,551 | -778,817 | 99,907 | -56,531 | 1,044,428 | 436,449 | 558,542 | 1,284,253 | 710,629 |

| Total | - | -82,940 | 55,525 | -96,395 | 162,797 | 249,311 | 645,206 | -57,525 | -615,293 | 79,585 | -157,820 | 1,115,248 | 530,660 | 686,728 | 1,480,367 | 952,103 |

| Theoretical Market Capitalization | 230,277 | 143,620 | 212,781 | 112,092 | 256,548 | 457,448 | 1,141,506 | 1,100,808 | 473,135 | 488,307 | 397,146 | 1,425,288 | 1,819,584 | 2,446,729 | 3,823,711 | 4,820,315 |

| Valuation per share (JPY) | 1,000 | 1,000 | 1,000 | 0 | 1,000 | 2,000 | 4,000 | 4,000 | 2,000 | 2,000 | 1,000 | 5,000 | 6,200 | 8,300 | 12,900 | 16,300 |

| yoy %chg. | - | 0.00% | 0.00% | -100.00% | #DIV/0! | 100.00% | 100.00% | 0.00% | -50.00% | 0.00% | -50.00% | 400.00% -72.87% | 24.00% | 33.87% | 55.42% | 26.36% |

| Deviation from Actual Stock Price | 9.66% | 36.11% | 10.20% | -100.00% | -8.80% | 3.69% | 33.94% | 69.54% | -45.78% | -22.00% | -67.17% | -66.36% | -54.96% | -30.01% | -11.56% | |

| Implied P/E (x) | 30.58 | -2.29 | 18.37 | 33.91 | 22.65 | 17.80 | 27.68 | 21.09 | 15.02 | 14.49 | 6.23 | 17.75 | 16.65 | 16.75 | 17.09 | 17.55 |

| Implied EV/EBITDA (x) | 2.89 | 2.72 | 4.00 | 1.95 | 5.27 | 6.49 | 9.11 | 8.39 | 4.84 | 5.23 | 2.92 | 7.59 | 7.95 | 8.56 | 9.54 | 9.85 |

| Implied PBR (x) | 0.70 | 0.56 | 0.76 | 0.41 | 0.96 | 1.45 | 3.13 | 2.63 | 0.96 | 1.00 | 0.72 | 2.30 | 2.55 | 2.90 | 3.68 | 3.77 |

Source: Company report, Bloomberg Finance L.P., J.P. Morgan estimates.

Note: Market capitalization as of July 13. Implied P/E is on a fully diluted basis.

Risks to Rating and Price Target Upside Scenario to Target Price/Rating

- Better-than-expected profitability improvement for FC-BGA substrates for major CPU makers

- Yen depreciation

- Further market share growth for AI GPU substrates, volume upside for ASIC substrates

Downside Scenario to Target Price/Rating

Asia Pacific Equity Research 15 July 2026

Investment Thesis, Valuation and Risks

Ibiden (4062) (Overweight; Price Target: ¥28,500)

Investment Thesis

In addition to the company's dominant market share in substrates for GPUs for AI servers, we also expect the company to see major earnings growth in EMIB substrates for ASICs and in standard ABF substrates from growing demand for AI servers. We believe Ibiden is wellpositioned to maximize benefits from the shift to larger and higher multi-layered FC-BGA substrates for AI server-use GPUs because of its strong technological abilities.

Valuation

Our December 2027 price target of ¥28,500 is based on (1) the ¥16,300 value derived from a zero-growth ROIC model (EV/IC = ROIC/WACC) using our FY2030 estimates (Rf = 2.57%, Rp = 5.15%, beta = 1.30, WACC = 5.9%) plus (2) Ibiden's 75% premium to the sector-average P/E (from August 2025 to July 2026, 12-month forward Bloomberg consensus basis), reflecting the rise in Ibiden's share price since August 2025 on expectations for earnings growth for AI server applications. Our price target is equivalent to a P/E of 31x our FY2030 EPS estimate.

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

Asia Pacific Equity Research 15 July 2026

- Inventory adjustments for AI servers, peaking-out of AI investment cycle

- Market share decline for BGA substrates for AI GPUs

- Procurement difficulties for core materials

- Roadmap delays in logic semiconductors, AI servers, etc.

Adam Chen report

JPMorgan Securities Japan Co., Ltd. Akinori Kanemoto AC (81-3) 6736 8628 akinori.kanemoto@jpmorgan.com

Asia Pacific Equity Research 15 July 2026

Ibiden (4062): Summary of Financials

| Income Statement | 2026/3A | 2027/3E | 2028/3E | 2029/3E | Cash Flow Statement | 2026/3A | 2027/3E | 2028/3E | 2029/3E |

|---|---|---|---|---|---|---|---|---|---|

| Revenue | 416,201.0 | 534,406.0 | 645,931.0 | 750,071.0 | Cash flow from operating activities | 77,016 | 232,667 | 388,993 | 408,566 |

| COGS | (284,532) | (342,784) | (407,014) | (452,630) | o/w Depreciation & amortization | 66,236 | 80,800 | 97,400 | 107,000 |

| Gross profit | 131,669 | 191,622 | 238,917 | 297,441 | o/w Changes in working capital | (12,084) | (28,725) | (27,976) | (24,770) |

| SG&A | (69,642) | (76,000) | (82,000) | (88,000) | |||||

| EBITDA | 128,263 | 196,422 | 254,317 | 316,441 | Cash flow from investing activities | (37,834) | (210,000) | (300,000) | (270,000) |

| D&A | (66,236) | (80,800) | (97,400) | (107,000) | o/w Capital expenditure | (64,277) | (210,000) | (300,000) | (270,000) |

| EBIT | 62,027.0 | 115,621.8 | 156,916.8 | 209,440.8 | as % of sales | 15.4% | 39.3% | 46.4% | 36.0% |

| Net Interest | 2,402 | 2,410 | 2,410 | 2,410 | |||||

| PBT | 91,092 | 115,132 | 156,527 | 209,051 | Cash flow from financing activities | (154,635) | (9,773) | (15,357) | (18,149) |

| Tax | (26,929) | (34,540) | (46,958) | (62,715) | o/w Dividends paid | (6,981) | (9,773) | (15,357) | (18,149) |

| Minority Interest | (449) | (280) | (280) | (280) | o/w Shares issued/(repurchased) | 0 | 0 | 0 | 0 |

| Net Income | 63,713 | 80,312 | 109,289 | 146,056 | o/w Net debt issued/(repaid) | (150,500) | 0 | 0 | 0 |

| Reported EPS | 215.6 | 271.7 | 369.7 | 494.1 | Net change in cash | (115,453) | 12,894 | 73,636 | 120,416 |

| DPS | 25.00 | 35.00 | 55.00 | 65.00 | Adj. Free cash flow to firm | 11,047 | 20,980 | 87,306 | 136,879 |

| Payout ratio | 11.6% | 12.9% | 14.9% | 13.2% | y/y Growth | -109.2% | 89.9% | 316.1% | 56.8% |

| Shares outstanding | 279 | 279 | 279 | 279 | |||||

| Balance Sheet | 2026/3A | 2027/3E | 2028/3E | 2029/3E | Ratio Analysis | 2026/3A | 2027/3E | 2028/3E | 2029/3E |

| Cash and cash equivalents | 295,681.0 | 308,575.1 | 382,210.8 | 502,627.3 | Gross margin | 31.6% | 35.9% | 37.0% | 39.7% |

| Accounts receivable | 81,810 | 105,045 | 126,967 | 147,437 | EBITDA margin | 30.8% | 36.8% | 39.4% | 42.2% |

| Inventories | 70,962 | 85,490 | 101,509 | 112,886 | EBIT margin | 14.9% | 21.6% | 24.3% | 27.9% |

| Other current assets | 169,860 | 207,623 | 245,564 | 277,410 | Net profit margin | 15.3% | 15.0% | 16.9% | 19.5% |

| Current assets | 465,541 | 516,198 | 627,774 | 780,038 | |||||

| PP&E | 437,704 | 566,904 | 769,504 | 932,504 | ROE | 12.2% | 13.7% | 16.4% | 18.8% |