PDF 原檔:報告_Daiwa_南亞科2408_20260710_original.pdf

圖片清單(已驗證 2026-07-13)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Daiwa_南亞科2408_20260710_001.png |

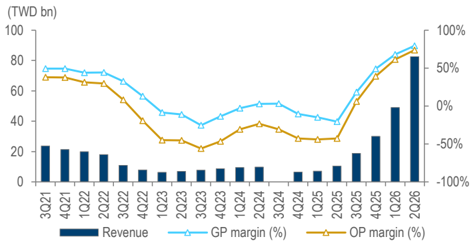

43KB | 真資料圖 | 南亞科季度營收(TWD bn,深藍柱)+ GP margin/OP margin 折線(3Q21-2Q26),margin 由負轉正大幅上揚至近90% |

報告_Daiwa_南亞科2408_20260710_002.png |

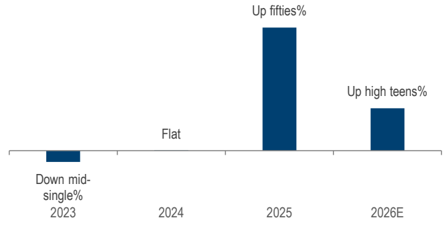

15KB | 真資料圖 | 位元出貨年增率長條圖(2023 個位數負成長/2024 持平/2025 up fifties%/2026E up high teens%) |

報告_Daiwa_南亞科2408_20260710_003.png |

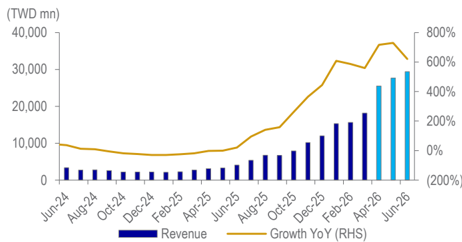

37KB | 真資料圖 | 南亞科月營收(TWD mn,柱狀)+ YoY 成長率折線(Jun-24~Jun-26),2026 上半年營收與成長率同步陡升至 600%+ |

報告_Daiwa_南亞科2408_20260710_004.png |

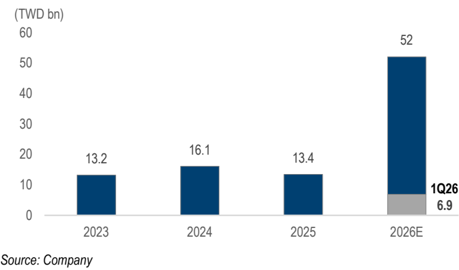

11KB | 真資料圖 | 年度資本支出長條圖(2023 13.2/2024 16.1/2025 13.4/2026E 52,單位 TWD bn),2026E 含 1Q26 已執行 6.9 |

4 張圖尺寸雖多數 <40KB,但經逐張核對均為報告內真實圖表(非 logo/banner),故列入真資料圖。

原始內容

Nanya Technology (2408 TT)

Share price (10 Jul): TWD435.50

12-mth rating: Buy (1)

2Q26 review: Intact solid earnings and positive outlook

SK Kim (82) 2 787 9173 sk.kim@kr.daiwacm.com

Summary: Nanya Technology (Nanya) announced its 2Q26 earnings after market hours on 10 July. Its revenue of TWD82.5bn (+68% QoQ, 684% YoY) and operating profit of TWD60.8bn (+102% QoQ, positive turnaround YoY) were in line with our estimates while outweighing the market consensus by 13% / 16%, respectively. While the DRAM shipment increase remained flat, ASP, which rose > 60%, drove the solid earnings. Management expects the price uptrend to persist through 3Q26, boosting the earnings further. In addition, they mentioned plans to allocate capacity toward DDR3/DDR4, where strong demand persists, to actively respond to customer demand. Though it did not announce a new shareholder return policy, the management expects to sustain a 40% level of dividend payout ratio.

Key highlights

- 2Q26 results review. Nanya's 2Q26 revenue of TWD82.5bn (+68% QoQ, 684% YoY) and operating profit of TWD60.8bn (+102% QoQ, positive turnaround YoY) were in line with our estimates while outweighing the market consensus by 13% / 16%, respectively. Its rapid earnings growth was mainly driven by a sharp increase in ASP. Its DRAM ASP increased by over 60% QoQ in 2Q26, while its shipments remained flat QoQ. The DDR5 portion accounted for over 10% of 2Q26 revenue with a rising trend. Meanwhile, management also mentioned they will allocate capacity to DDR3/DDR4, where constrained supply continues to make the market attractive. Management guided for sustainable earnings growth in 3Q26 led by strong price increases.

- Outlook for 3Q26 and cash management. For 3Q26, management guided for ASP to increase further, sustaining the earnings improvement. While LTA customers' prices will remain stable, management expects the short-term contract ASP to rise more rapidly. Management noted that the 1H26 AI revenue portion accounted for 20% and expects to expand its sales for AI going forward, while also announcing plans to actively respond to non-AI and strong DDR3/DDR4 demand. Its DDR4/LPDDR4 combined portion accounted for c.70%, while DDR3 and DDR5 each held c.10%. For FY2026 capex, Nanya guided for TWD52bn, with wafer equipment accounting for 30%, while guiding to spend USD16bn (c.TWD514bn) for a new 45k/month capacity build-out with the first phase ramp of 30k/month targeted until 2028. Given TWD216.7bn (+151% QoQ) in retained cash by the end of 2Q26, Nanya guided to maintain a 40% level of payout ratio while considering its need for future growth capex.

Recommendation

We have a Buy (1) call on Nanya with a 12M TP of TWD650. We expect the robust 2Q26 earnings and positive earnings outlook to drive positive investor sentiment. Key risk: weaker-than-expected commodity DRAM demand due to delays in data centre build-outs.

10 July 2026

Information Technology: Taiwan

To see our 2Q26 preview flash note on Nanya, please click here

Solid 2Q26 revenue: intact earnings momentum

- 2Q26 revenue exceeds Bloomberg consensus on DRAM price hikes

- Further earnings upside in 2H26E; DDR4 price momentum until 2027E

- Reaffirming our Buy (1) rating; raising 12-month TP to TWD 650

Nanya: 2Q26 results overview

| (TWDm) | 2Q26 | 1Q26 | QoQ growth | 2Q25 | YoY growth | Daiwa estimates | Diff | BBG consensus | Diff |

|---|---|---|---|---|---|---|---|---|---|

| Revenue | 82,549 | 49,087 | 68% | 10,526 | 684% | 82,549 | 0% | 72,871 | 13% |

| Operating Profit | 60,826 | 30,111 | 102% | -4,501 | Positive turnaround | 60,570 | 0% | 52,272 | 16% |

| OP margin | 73.7% | 61.3% | -42.8% | 73.4% | 71.7% |

Source: Company, Bloomberg

Note: Bloomberg standard consensus as of 10 July 2026

Nanya: revenue and gross/operating margin trend

Source: Company

Nanya: bit shipment growth YoY trend

Source: Company

Nanya: monthly revenue and growth YoY trend

Source: Company

Nanya: annual capex trend

In the interests of timeliness, this document has not been edited.