PDF 原檔:報告_Citi_鴻勁7769_20260708_original.pdf

圖片清單(已驗證 2026-07-09)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

報告_Citi_鴻勁7769_20260708_001.png |

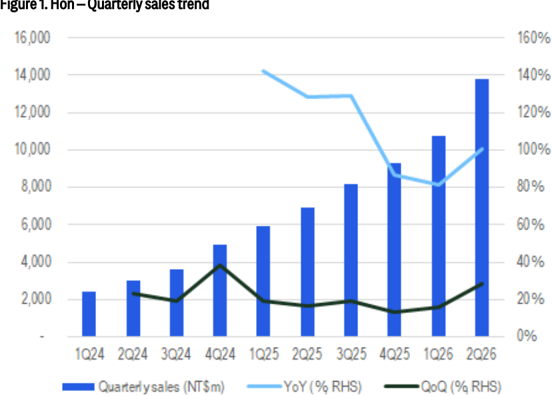

60KB | 真資料圖 | 鴻勁精密季營收趨勢圖(1Q24–2Q26),藍色柱狀為季營收 NT$m,搭配 YoY%/QoQ% 雙折線 |

報告_Citi_鴻勁7769_20260708_002.png |

118KB | 真資料圖 | 兩張股價圖:上圖「Ratings and Target Price History」股價 vs 目標價沿革(最新 2026-05-28 目標價 NT$11,000、收盤 NT$7,700);下圖「Short-Term View/Catalyst Watch」股價走勢圖 |

原始內容

citivelocity.com

08 Jul 2026 07:24:58 ET │ 12 pages

Hon Precision (7769.TW)

Record 2Q26 revenues with margin upside potential

CITI'S TAKE

Hon's Jun revenues came in stronger than expected at NT$5,302mn (+106% YoY and +28% MoM), concluding 2Q26 sales at a record high of NT$13,794mn (+101% YoY/+29% QoQ), beating our and street's (Bloomberg) forecast by 19%/12%. We believe the strong performance is mainly driven by better than expected demand from cold plates product and solid ATC handler sales for its key GPU and ASIC clients. With better sales mix (higher cold plates contribution) and stronger operating leverage, we see upside potential to Street's 2Q margin numbers. Looking ahead, with continued workforce additions and new capacity ramp (stronger ramps from 4Q26 with its newly acquired Daya plant to start production), we expect Hon's QoQ revenues growth to accelerate in the coming quarters. Long-term, we are constructive on Hon's growth outlook supported by its multi-year AI GPU/ASIC and CPU projects, and see upside opportunity from its strong development in CPO insertion 4 business.

Prepared for Kevin Lu

| Buy | Buy |

|---|---|

| Catalyst Watch: Upside, expires27-AUG-26 | Catalyst Watch: Upside, expires27-AUG-26 |

| Price (08 Jul 2613:30) | NT$6,055.00 |

| Target price | NT$11,000.00 |

| Expected share price return | 81.7% |

| Expected dividend yield | 0.6% |

| Expected total return | 82.2% |

| MarketCap | NT$1,089,476M |

| US$34,109M |

Nicholas Lai AC

+886-2-8726-9093 nicholas.lai@citi.com

Laura (Chia Yi) Chen +886-2-8726-9090 laura.cy.chen@citi.com

Jack Chen +886-2-8726-9091 jack1.chen@citi.com

Michael Hung +886-2-8726-9092 michael.hung@citi.com

See Appendix A-1 for Analyst Certification, Important Disclosures and Research Analyst Affiliations

Figure 1. Hon - Quarterly sales trend

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

- Quarterly sales (NTSm) -

@ 2026 Citioroun Ine No redistribution without Citioroun's written nermission

160%

140%

120%

100%

80%

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission.

Source: Citi Research

Prepared for Kevin Lu

Prepared for Kevin Lu

Catalyst Watch on Hon Precision (7769.TW)

Direction:

Upside

Duration:

Within 90 Days (expires 27 Aug 2026)

Date Added:

28 May 2026

Catalyst:

Thematic driven

We are constructive on Hon Precision's earnings growth outlook driven by its solid engagement in global leading AI projects. For 2Q earnings, our estimates are higher than consensus as we expect higher margins from a better sales mix and operating leverage, which we believe could drive strong >100% YoY earnings growth. Also, though a long-term opportunity, we believe co-packaged optics (CPO) engagement with key customers could also drive significant upside potential.

Prepared for Kevin Lu

Hon Precision

Valuation

Our target price of NT$11,000 is based on a target PER multiple of 36x applied to the average of our 2027E/28E EPS estimates. Our PER target of 36x is set at 1-std above its 1-year PER average, justified by its high share of the AI/HPC testing handler market, which we estimate could support an earnings CAGR of 77% in 2025-28, higher than its 3-year CAGR at c40% in 202225. Our estimated 77% earning CAGR is also higher than the +40% average (Bloomberg consensus) of its global testing equipment peers. As its peers have been trading at average 36x PER on 2027/28 consensus EPS in the past 1 year, we believe Hon Precision deserves a further re-rating to our target PER of 36x.

Risks

Our quantitative risk rating system, which looks at historical share price volatility, rates Hon Precision High Risk. However, we are not assigning a High Risk rating as we forecast an earnings CAGR of >75%, significantly stronger than the growth outlook for its global peers. Also, we note its dominant position in AI/HPC handler market and expanding market TAM opportunity, which support our constructive view over its growth outlook.

Key downside risks that could impede the shares from reaching our target price: 1) Global AI demand slowdown driving weaker capacity build for semiconductor equipment; 2) unexpected share losses at its major AI projects; 3) slower-than-expected capacity ramp at its new facilities, or the company taking a long time to find/secure new sites; 4) slower-than-expected development of its CPO business; 5) shorter-than-expected testing time leading to lower demand for its products; 6) weak adoption of high-premium cold plate products; and 7) increasing competition from new entrants.

Hon Precision (7769.TW)

Analyst: Nicholas Lai

TWD

7,500

5,000

If you are visually impaired and would like to speak to a Citi representative regarding the details of the graphics in this document, please call USA 1-888-500-5008 (TTY: 711), from outside the US +1-210-677-3788

Date

Appendix A-1

*Indicates Change