PDF 原檔:報告_Citi_穎崴_20260706_original.pdf

圖片清單(已驗證 2026-07-07)

ingest 時建立的「眼見為憑」圖片索引,是 lib/ 嵌圖的唯一真相來源;嵌入時只從這裡挑分類為「真資料圖」的,不照 trimmed 引用順序猜。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260706_citi_winway_001.png |

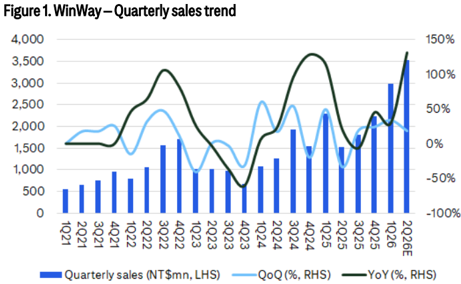

74KB | 真資料圖 | WinWay 季度銷售趨勢圖(1Q21-2Q26E):柱狀圖季度銷售 NT$mn(LHS),折線圖 QoQ%、YoY%(RHS),2Q26E 季度銷售約 NT$3,500mn,YoY 約 130% |

260706_citi_winway_002.png |

164KB | 真資料圖 | Citi 穎崴(6515.TW)評等與目標價歷史圖(上半部:Fundamental Research,目標價沿革 6,000→10,000→13,000;下半部:Short-Term View/Catalyst Watch 紀錄,含 Add CW/Remove CW 紀錄) |

原始內容

citivelocity.com

06 Jul 2026 04:56:42 ET │ 12 pages

WinWay Technology (6515.TW)

Record monthly revenue with momentum ahead

CITI'S TAKE

WinWay reported record Jun-26 revenues of NT$1.46bn (+36% MoM/+288% YoY). 2Q26 revenues reached NT$3.52bn (+18% QoQ/+131% YoY), beating Citi/cons forecasts by 2%/6%, driven by robust testing demand across AI GPU and HPC platforms. Looking ahead of 3Q26E, the further ramp of Renwu Phase 1 capacity implies continued revenue momentum and accelerated backlog digestion. Incremental growth should be further supported by ongoing AI GPU socket shipments and the approaching AI ASIC ramp. Based on our check, WinWay is actively pursuing price adjustments for next-generation product specs, which we view as a potential margin catalyst for 2027E and beyond. With positive industry trend and solid momentum ahead, we reiterate our Buy rating.

Prepared for Kevin Lu

| Buy/HighRisk | Buy/HighRisk |

|---|---|

| Catalyst Watch: Upside,expires25-AUG-26 | Catalyst Watch: Upside,expires25-AUG-26 |

| Price (06 Jul 2613:30) | NT$8,915.00 |

| Target price | NT$13,000.00 |

| Expected share price return | 45.8% |

| Expected dividend yield | 0.6% |

| Expected total return | 46.4% |

| MarketCap | NT$321,279M |

| US$10,059M |

Michael Hung AC

+886-2-8726-9092 michael.hung@citi.com

Laura (Chia Yi) Chen +886-2-8726-9090 laura.cy.chen@citi.com

Jack Chen +886-2-8726-9091 jack1.chen@citi.com

Nicholas Lai +886-2-8726-9093 nicholas.lai@citi.com

See Appendix A-1 for Analyst Certification, Important Disclosures and Research Analyst Affiliations

Figure 1. WinWay - Quarterly sales trend

4,000

3,500

3,000

2,500

2,000

1,500

1,000

500

- Quarterly sales (NT$mn, LHS)

350%

300%

250%

200%

150%

100%

50%

0%

-50%

Figure 2. WinWay - Monthly sales trend

May-:

Mar-26

Jan-26

— Monthly sales (NT$mn, LHS) -

- MoM (%, RHS) —YoY (%, RHS)

@ 2026 Citigroun Inc. No redistribution without Citigroup's written permission.

Figure 2. WinWay - Monthly sales trend

1,600

1,400

1,200

1,000

800

600

400

200

@ 2026 Citigroun Inc. No redistribution without Citigroun's written permission.

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission. Source: Company Reports, Citi Research

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission. Source: Company Reports, Citi Research

Prepared for Kevin Lu

150%

100%

50%

0%

-50%

-100%

Prepared for Kevin Lu

Catalyst Watch on WinWay Technology (6515.TW)

Direction:

Upside

Duration:

Within 90 Days (expires 25 Aug 2026)

Date Added:

26 May 2026

Catalyst:

Earnings

We have an accelerating earnings growth outlook for WinWay as a dominant beneficiary of the rising demand for AI GPUs and the SLT volume multiplier. Specifically, we believe the mass production of next-gen US AI GPU in 2Q26 and the upcoming AI ASIC project in 2H26 could be the catalysts. With leading positions in high-speed coaxial sockets and thermal management, combined with an improving sales mix from MEMS expansion, we are positive over WinWay's structural growth outlook.

Prepared for Kevin Lu

WinWay Technology

Valuation

We value WinWay using a PE-based approach that factors in earnings momentum and likely expansion of its addressable market. Our target price of NT$13,000 is derived from applying 45x to 2H27E-1H28E EPS, higher than the upper end of its longterm PE range, which we believe is justified given the company's entrenched position in the high-end AI GPU testing supply chain, rising contribution from coaxial socket and SLT solutions, and the increasing value of test content per module. With these structural drivers in place, and as we believe the market is starting to value it as an AI/HPC play (rather than a consumer electronics stock), we expect the multiple to hold at a premium relative to its historical averages.

Risks

Our quant rating system rates the WinWay stock High Risk based on its historical volatility.

Key downside risks that could impede the stock from reaching our target price, and to our earnings forecasts, include: 1) client and sector concentration - specifically any delays in US AI GPU product roadmap could impact the business outlook for WinWay; 2) intensifying competition in coaxial and hypersockets from global peers; 3) faster-than-expected testing algorithm optimization, which could shorten testing durations and reduce the anticipated hardware demand multiplier; and 4) delay of MEMS Phase 2 mass production.

WinWay Technology (6515.TW)

Analyst: Michael Hung

MEN

If you are visually impaired and would like to speak to a Citi representative regarding the details of the graphics in this document, please call USA 1-888-500-5008 (TTY: 711), from outside the US +1-210-677-3788 Донорада радоно ала тароковайті

Date

Appendix A-1

*Indicates Change