PDF 原檔:260630_6269_台郡_citi_flexium_original.pdf

圖片清單(已驗證 2026-07-01)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

_001.png |

30KB | 裝飾 | 股價走勢小圖(<40KB) |

_002.png |

154KB | 真資料圖 | 12M forward P/E band + P/B band(負 EPS 下 P/E 失義,不嵌) |

_003.png |

97KB | 真資料圖 | Bull/Base/Bear 情境圖:Bull NT$80(+13%)/Base NT$75(+5.6%)/Bear NT$60(-15%),現價 NT$71(可嵌) |

_004.png |

183KB | 真資料圖 | 評等/目標價 3 年沿革 + Short-Term View/Catalyst Watch 紀錄(不嵌) |

<40KB 未列者預設 logo/裝飾。

原始內容

(RIC: 0209.1W, BD: 0209 11)

TWD

85

80

75

70

65

60

55

50

45

30

Jun

30 Jun 2026 11:54:24 ET │ 14 pages

Sep

Dec

Mar

Jun

Flexium Interconnect (6269.TW)

No Clear Catalyst in Sight; Neutral

CITI'S TAKE

Despite regaining its market share in FPCB for iPhone and computers, we think the recent decision by Apple to hike prices of its products would negatively impact unit shipments of consumer electronics, pressuring Flexium's sales momentum in 2H. The company is currently making slow progress in AI servers with FPCB-based leakage detect sensors and even though the progress is slow, we think it could still help Flexium to partially offset the negative impact from weak consumer electronics demand. We lift our DCF-based TP to NT$75 from NT$67 owing to earnings recovery and maintain our Neutral rating.

Sales momentum still sluggish -Year to date, the company's sales momentum has remained weak with 5M26 sales YoY growth of +2%. We attribute the weak sales to its higher exposure to consumer electronics demand, which currently is negatively impacted by the rise in memory costs. We expect 2Q26E sales to be flat QoQ due to continued headwinds.

Apple: recovery in market share but outlook dampened by rising memory costs -Although the company is positive on regaining its market share in iPhone with 30% YoY sales growth along with growth in computer segment, we think the growth might be impacted by Apple's recent decision to raise the prices of Mac/iPad products. We think the price hike would lead to low unit shipments and thus estimate 16% QoQ (+4% YoY) sales growth in 3Q26.

AI server seeing gradual contribution -FPCB is currently seeing adoption of leakage detect sensors for AI servers, with sales gradually ramping up. The company targets sales mix from servers to reach 10% in 2026E with a wider adoption among customers. In the next 2-3 years, the company plans to reduce its sales dependence on Apple, and increase its sales contribution from non-Apple customers to 20-30% of the overall sales mix.

Earnings cut; maintain Neutral -We cut our 2026/27E earnings by ~211%/101% to factor in the headwinds from the rise in memory costs impacting consumer electronics. We also introduce our 2028E earnings forecast. We roll over our DCFbased TP to 2027 from 2026 and thus raise our TP to NT$75 from NT$67 on revised estimates. Maintain our Neutral rating considering the cycle would likely bottom in 1H26.

Earnings Summary

| Year to 31Dec | Net Profit (NT$M) | DilutedEPS (NT$) | EPSgrowth (%) | P/E (x) | P/B (x) | ROE (%) | Yield (%) |

|---|---|---|---|---|---|---|---|

| 2024A | -826 | -2.56 | -140.2 | na | 0.9 | -3.4 | 6.6 |

| 2025A | -2,229 | -6.95 | -171.1 | -10.2 | 1 | -9.8 | 6.4 |

| 2026E | -1,556 | -4.87 | 29.9 | -14.6 | 1.1 | -7.5 | 6.3 |

| 2027E | -25 | -0.09 | 98.2 | na | 1.1 | -0.1 | 6.1 |

| 2028E | 1,357 | 4.25 | na | 16.7 | 1 | 6.5 | 6 |

Source: Powered by dataCentral

See Appendix A-1 for Analyst Certification, Important Disclosures and Research Analyst Affiliations.

| n Neutral | |

|---|---|

| Price (30 Jun 2613:30) | NT$71.00 |

| Target price | NT$75.00↑ |

| fromNT$67.00 | |

| Expected share price return | 5.6% |

| Expected dividend yield | 0.0% |

| Expected total return | 5.6% |

| MarketCap | NT$22,992M |

| US$726M |

Jack Chen AC

+886-2-8726-9091 jack1.chen@citi.com

Laura (Chia Yi) Chen +886-2-8726-9090 laura.cy.chen@citi.com

Nicholas Lai +886-2-8726-9093 nicholas.lai@citi.com

| 6269.TW: Fiscalyearend31-Dec | Price: NT$71.00; TP: NT$75.00; MarketCap:NT$22,992m; Recomm:Neutral | Price: NT$71.00; TP: NT$75.00; MarketCap:NT$22,992m; Recomm:Neutral | Price: NT$71.00; TP: NT$75.00; MarketCap:NT$22,992m; Recomm:Neutral | Price: NT$71.00; TP: NT$75.00; MarketCap:NT$22,992m; Recomm:Neutral | Price: NT$71.00; TP: NT$75.00; MarketCap:NT$22,992m; Recomm:Neutral | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Profit&Loss(NT$m) | 2024 | 2025 | 2026E | 2027E | 2028E | Valuation ratios | 2024 | 2025 | 2026E | 2027E | 2028E |

| Sales revenue | 26,444 | 22,350 | 23,793 | 25,435 | 27,733 | PE(x) | -27.7 | -10.2 | -14.6 | na | 16.7 |

| Cost of sales | -24,924 | -22,054 | -23,268 | -23,332 | -23,841 | PB(x) | 0.9 | 1.0 | 1.1 | 1.1 | 1.0 |

| Gross profit | 1,520 | 295 | 526 | 2,103 | 3,892 | EV/EBITDA(x) | 21.3 | -31.4 | -83.8 | 13.0 | 6.7 |

| Gross Margin (%) | 5.7 | 1.3 | 2.2 | 8.3 | 14.0 | FCFyield (%) | -14.3 | 7.8 | 25.1 | 3.1 | 7.0 |

| EBITDA(Adj) | 1,103 | -795 | -257 | 1,400 | 2,541 | Dividend yield (%) | 6.6 | 6.4 | 6.3 | 6.1 | 6.0 |

| EBITDAMargin(Adj) (%) | 4.2 | -3.6 | -1.1 | 5.5 | 9.2 | Payout ratio (%) | -182 | -65 | -91 | na | 100 |

| Depreciation | -2,917 | -2,506 | -2,087 | -1,706 | -1,276 | ROE(%) | -3.4 | -9.8 | -7.5 | -0.1 | 6.5 |

| Amortisation | 0 | 0 | 0 | 0 | 0 | Cashflow(NT$m) | 2024 | 2025 | 2026E | 2027E | 2028E |

| EBIT (Adj) | -1,814 | -3,302 | -2,344 | -306 | 1,266 | EBITDA | 1,103 | -795 | -257 | 1,400 | 2,541 |

| EBIT Margin (Adj) (%) | -6.9 | -14.8 | -9.9 | -1.2 | 4.6 | Working capital | 1,789 | -208 | -37 | -419 | -493 |

| Net interest | 223 | 159 | 174 | 246 | 306 | Other | -5,220 | 3,475 | 6,598 | 429 | 243 |

| Associates | 40 | 81 | -2 | 0 | 0 | Operating cashflow | -2,328 | 2,472 | 6,304 | 1,410 | 2,292 |

| Non-Op/Except/Other Adj | 350 | 175 | 46 | 76 | 76 | Capex | -957 | -703 | -619 | -700 | -700 |

| Pre-tax profit | -1,200 | -2,887 | -2,125 | 16 | 1,648 | Net acq/disposals | 0 | 0 | 0 | 0 | 0 |

| Tax | 383 | 678 | 592 | -40 | -311 | Other | -751 | -739 | 580 | 146 | 73 |

| Extraord./Min.Int./Pref.div. | -10 | -20 | -23 | 0 | 20 | Investing cashflow | -1,707 | -1,442 | -39 | -554 | -627 |

| Reported net profit | -826 | -2,229 | -1,556 | -25 | 1,357 | Dividends paid | -1,651 | -43 | 0 | 0 | 0 |

| Net Margin (%) | -3.1 | -10.0 | -6.5 | -0.1 | 4.9 | Financing cashflow | 1,229 | -931 | 145 | -17 | -6 |

| CoreNPAT | -826 | -2,229 | -1,556 | -25 | 1,357 | Net change in cash | -2,806 | 99 | 6,411 | 839 | 1,659 |

| Per share data | 2024 | 2025 | 2026E | 2027E | 2028E | Free cashflow to s/holders | -3,284 | 1,768 | 5,686 | 710 | 1,592 |

| Reported EPS($) | -2.56 | -6.95 | -4.87 | -0.09 | 4.25 | ||||||

| Core EPS($) | -2.56 | -6.95 | -4.87 | -0.09 | 4.25 | ||||||

| DPS($) | 4.66 | 4.55 | 4.44 | 4.34 | 4.24 | ||||||

| CFPS($) | -7.22 | 7.71 | 19.74 | 4.41 | 7.18 | ||||||

| -10.18 | 5.51 | 17.80 | 2.22 | 4.98 | |||||||

| FCFPS($) | |||||||||||

| Wtdavgordshares(m) | 323 | 321 | 319 | 319 | 319 | ||||||

| Wtdavgdiluted shares (m) | 323 | 321 | 319 | 319 | 319 | ||||||

| Growthrates | 2024 | 2025 | 2026E | 2027E | 2028E | ||||||

| Sales revenue (%) EBIT (Adj) (%) | -19.2 | -15.5 | 6.5 | 6.9 | 9.0 | ||||||

| -210.8 | -82.0 | 29.0 | 86.9 | 513.1 | |||||||

| CoreNPAT(%) | -140.0 | -169.7 | 30.2 | 98.4 | na | ||||||

| CoreEPS(%) | -140.2 | -171.1 | 29.9 | 98.2 | na | ||||||

| BalanceSheet(NT$m) | 2024 | 2025 | 2026E | 2027E | 2028E | ||||||

| Cash&cashequiv. | 3,195 | 3,293 | 9,704 | 10,543 | 12,202 | ||||||

| Accounts receivables | 3,750 | 4,095 | 4,187 | 4,549 | 4,973 | ||||||

| Inventory | 3,057 | 3,443 | 2,980 | 3,237 | 3,539 | ||||||

| Net fixed &other tangibles | 18,801 | 17,139 | 16,182 | 15,176 | 14,600 | ||||||

| Goodwill &intangibles | 0 | 0 | 0 | 0 | 0 | ||||||

| Financial &other assets | 9,791 | 8,208 | 1,864 | 1,854 | 1,940 | ||||||

| Total assets | 38,594 | 36,178 | 34,917 | 35,359 | 37,253 | ||||||

| Accounts payable | 3,979 | 4,502 | 4,095 | 4,295 | 4,527 | ||||||

| Short-term debt | 660 | 467 | 347 | 330 | 323 | ||||||

| Long-term debt | 4,119 | 3,713 | 3,647 | 3,647 | 3,647 | ||||||

| Provisions &other liab | 4,249 | 4,504 | 5,013 | 5,296 | 5,628 | ||||||

| 13,007 | 13,185 | 13,101 | 14,125 | ||||||||

| Total liabilities | 13,567 | 21,535 | |||||||||

| Shareholders' equity | 23,944 1,644 | 21,362 1,630 | 20,203 1,613 | 20,178 1,613 | 1,593 | ||||||

| Minority interests Total equity | 25,588 | 22,992 | 21,816 | 21,792 | 23,128 | ||||||

| Net debt (Adj) | 1,584 | 886 | -5,711 | -6,567 | -8,232 | ||||||

| Net debt to equity (Adj) (%) | 6.2 | 3.9 | |||||||||

| For definitions of the items in this table, | please click here. | -26.2 | -30.1 | -35.6 |

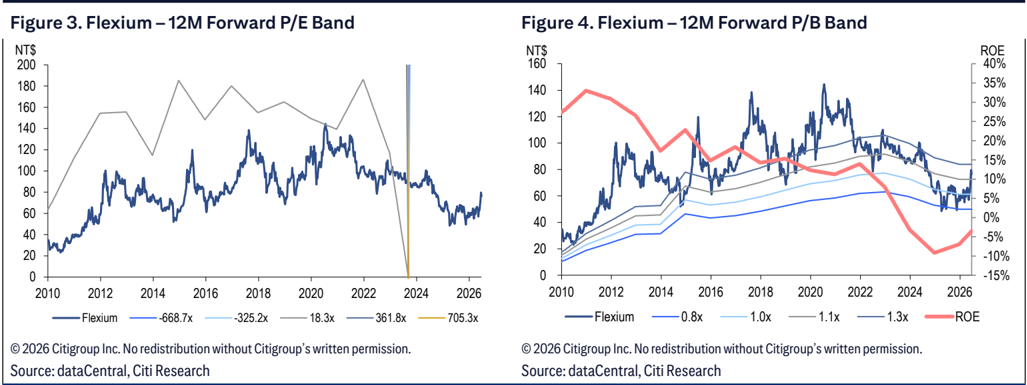

Figure 1. Flexium - Earnings Revision

| 2Q26E | 2Q26E | 2Q26E | 3Q26E | 3Q26E | 3Q26E | 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (NT$mn) | New | Old | Chg. | New | Old | Chg. | New | Old | Chg. | New | Old | Chg. | New |

| Sales | 5,446 | 6,348 | -14% | 6,328 | 7,745 | -18% | 23,793 | 28,168 | -16% | 25,435 | 30,238 | -16% | 27,733 |

| Sequential growth (%) | 0% | 7% | 16% | 22% | 6% | 21% | 7% | 7% | 9% | ||||

| Gross profit | 4 | 684 | -99% | 237 | 1,509 | -84% | 526 | 4,168 | -87% | 2,103 | 4,726 | -55% | 3,892 |

| Opex | 664 | 774 | -14% | 645 | 790 | -18% | 2,870 | 3,102 | -7% | 2,410 | 2,866 | -16% | 2,627 |

| Operating profit | -660 | -90 | 633% | (409) | 718 | -157% | -2,344 | 1,066 | -320% | (306) | 1,861 | -116% | 1,266 |

| Pre-tax profit | -599 | 16 | -3856% | (339) | 949 | -136% | -2,125 | 1,770 | -220% | 16 | 2,294 | -99% | 1,648 |

| Net income | -395 | 11 | -3728% | (206) | 755 | -127% | -1,556 | 1,399 | -211% | (25) | 1,916 | -101% | 1,357 |

| EPS(NT$) | -1.24 | 0.03 | -3763% | (0.65) | 2.34 | -128% | -4.87 | 4.34 | -212% | (0.08) | 5.94 | -101% | 4.25 |

| Gross margin (%) | 0.1% | 10.8% | -10.7 ppt | 3.7% | 19.5% | -15.7 ppt | 2.2% | 14.8% | -12.6 ppt | 8.3% | 15.6% | -7.4 ppt | 14.0% |

| Opexratio (%) | 12.2% | 12.2% | +0.0ppt | 10.2% | 10.2% | -0.0 ppt | 12.1% | 11.0% | +1.0 ppt | 9.5% | 9.5% | -0.0 ppt | 9.5% |

| Operating margin (%) | -12.1% | -1.4% | -10.7 ppt | -6.5% | 9.3% | -15.7 ppt | -9.9% | 3.8% | -13.6 ppt | -1.2% | 6.2% | -7.4 ppt | 4.6% |

| Net margin (%) | -7.3% | 0.2% | -7.4 ppt | -3.3% | 9.7% | -13.0 ppt | -6.5% | 5.0% | -11.5 ppt | -0.1% | 6.3% | -6.4 ppt | 4.9% |

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission.

Source: Citi Research Estimates

Figure 2. Flexium - Forecast Summary

| Flexium (NT$ inMn, year-endDec) | 1Q | 2QE 2026 | 3QE | 4QE | 1QE | 2QE 2027 | 3QE | 4QE | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 5,467 | 5,446 | 6,328 | 6,553 5,576 | 5,837 | 6,902 | 7,119 | 19,096 | 25,846 | 26,770 | 26,033 | 29,898 | 35,569 | 40,070 | 32,729 | 26,444 22,350 | 23,793 | 25,435 | 27,733 | |

| COGS | -5,543 | -5,442 | -6,091 | -6,192 | -5,313 | -5,404 | -6,252 | -6,363 | -14,557 | -20,185 | -21,650 | -20,088 | -23,764 | -29,239 | -33,247 -27,875 | -24,924 | -22,054 | -23,268 | -23,332 | -23,841 |

| GrossProfit | -76 | 4 | 237 | 361 | 263 | 434 | 650 | 756 | 4,539 | 5,662 | 5,120 | 5,945 | 6,134 | 6,329 | 6,823 | 4,854 1,520 | 295 | 526 | 2,103 | 3,892 |

| Operating Expense | -924 | -664 | -645 | -636 | -552 | -613 | -718 | -527 | -1,487 | -1,701 | -1,967 | -2,148 | -2,695 | -3,057 -3,293 | -3,216 | -3,334 | -3,597 | -2,870 | -2,410 | -2,627 |

| SG&Aexpenses | -270 | -251 | -240 | -229 | -190 | -193 | -242 | -235 | -580 | -695 | -756 | -727 | -868 | -1,001 -1,242 | -1,302 | -1,171 | -1,042 | -991 | -859 | -936 |

| R&D expenses | -654 | -414 | -405 | -406 | -362 | -420 | -476 | -292 | -907 | -1,006 | -1,211 | -1,421 | -1,826 | -2,055 | -2,051 | -1,914 -2,163 | -2,555 | -1,879 | -1,551 | -1,691 |

| EBIT | -1,000 | -660 | -409 | -275 | -289 | -179 | -68 | 229 | 3,052 | 3,961 | 3,153 | 3,797 | 3,439 | 3,273 | 3,530 | 1,638 -1,814 | -3,302 | -2,344 | -306 | 1,266 |

| Net Interest Income | 30 | 42 | 51 | 51 | 62 | 62 | 61 | 61 | 55 | 81 | 106 | 60 | 95 | 152 251 | 337 223 | 159 | 174 | 246 | 306 | |

| Net Other Income | -12 | 19 | 19 | 19 | 19 | 19 | 19 | 19 | -148 | -165 | 222 | 145 | 263 | 389 | 530 | 353 391 | 256 | 45 | 76 | 76 |

| Pre-Tax Profit | -982 | -599 | -339 | -205 | -208 | -98 | 12 | 309 | 2,960 | 3,877 | 3,481 | 4,002 | 3,797 3,814 | 4,312 | 2,328 | -1,200 | -2,887 | -2,125 | 16 | 1,648 |

| Tax | -164 | -210 | -136 | -82 | -21 | -10 | 3 | 68 | -685 | -820 | -836 | -849 | -863 | -934 | -790 | -272 383 | 678 | 592 | -40 | -311 |

| Net Profit | -830 | -395 | -206 | -125 | -190 | -90 | 10 | 245 | 2,275 | 3,057 | 2,645 | 3,153 | 2,934 | 2,880 | 3,522 | 2,067 -826 | -2,229 | -1,556 | -25 | 1,357 |

| EPS (NT$)- diluted | -2.60 | -1.24 | -0.65 | -0.39 | -0.59 | -0.28 | 0.03 | 0.77 | 8.09 | 9.82 | 8.46 | 9.01 | 8.16 | 7.60 | 10.14 | 6.38 -2.56 | -6.95 | -4.87 | -0.08 | 4.25 |

| Margins (%) | ||||||||||||||||||||

| GrossMargin | -1.4 | 0.1 | 3.7 | 5.5 | 4.7 | 7.4 | 9.4 | 10.6 | 23.8 | 21.9 | 19.1 | 22.8 | 20.5 | 17.8 | 17.0 | 14.8 5.7 | 1.3 | 2.2 | 8.3 | 14.0 |

| Operating Margin | -18.3 | -12.1 | -6.5 | -4.2 | -5.2 | -3.1 | -1.0 | 3.2 | 16.0 | 15.3 | 11.8 | 14.6 | 11.5 | 9.2 | 8.8 | 5.0 -6.9 | -14.8 | -9.9 | -1.2 | 4.6 |

| Net Margin | -15.2 | -7.3 | -3.3 | -1.9 | -3.4 | -1.5 | 0.1 | 3.4 | 11.9 | 11.8 | 9.9 | 12.1 | 9.8 | 8.1 | 8.8 | 6.3 -3.1 | -10.0 | -6.5 | -0.1 | 4.9 |

| Sequential Growth (%) | ||||||||||||||||||||

| Revenue | (2) | (0) | 16 | 4 | (15) | 5 | 18 | 3 | 6 | 35 | 4 | (3) | 15 | 19 | 13 | (18) | (19) (15) | 6 | 7 | 9 |

| GrossProfit | n.m. | n.m. | 5,660 | 52 | (27) | 65 | 50 | 16 | (6) | 25 | (10) | 16 | 3 | 3 | 8 | (29) (69) | (81) | 78 | 300 | 85 |

| EBIT | n.m. | n.m. | n.m. | n.m. | n.m. | n.m. | n.m. | n.m. | (10) | 30 | (20) | 20 | (9) | (5) | 8 (54) | n.m. | n.m. | n.m. | n.m. | n.m. |

| Net Profit | n.m. | n.m. | n.m. | n.m. | n.m. | n.m. | n.m. | 2,383 | (18) | 34 | (13) | 19 | (7) | (2) | 22 | (41) n.m. | n.m. | n.m. | n.m. | n.m. |

| EPS - basic | n.m. | n.m. | n.m. | n.m. | n.m. | n.m. | n.m. | 2,383 | (23) | 20 | (17) | 18 | (14) | (5) | 32 | (40) | n.m. | n.m. n.m. | n.m. | n.m. |

| EPS - diluted | n.m. | n.m. | n.m. | n.m. | n.m. | n.m. | n.m. | 2,383 | (20) | 21 | (14) | 7 | (9) | (7) | 33 | (37) n.m. | n.m. | n.m. | n.m. | n.m. |

© 2026 Citigroup Inc. No redistribution without Citigroup's written permission.

Source: Citi Research Estimates, Company Reports

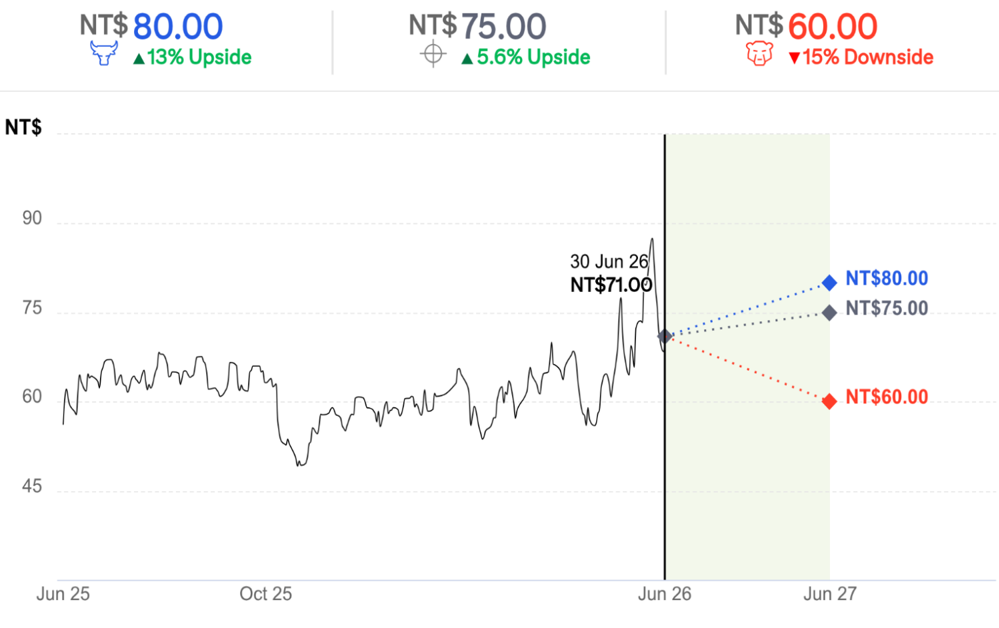

NT$

90

75

45

Jun 25

• Better than expected gross margin from MPI/LCP will increase UTR and efficiency

413% Upside

4 5.6% Upside

NT$ 60.00

v15% Downside

Bull/Bear: Flexium Interconnect (6269.TW)

BASE Assumptions

• +6%/ +7% revenue growth in 2026/27E

- 2.2%/8.3% gross margin in 2026/27E

BEAR Assumptions

• Weaker than expected top line growth with soft demand or tougher competition

- Worse than expected impact from gross margin

NT$ 75.00

Flexium Interconnect

Company description

Established in 1997 and headquartered in Kaohsiung, Taiwan, Flexium is one of the world's key flexible PCB makers. In recent years, Flexium has been gaining market share at the expense of Japanese players. Flexium has manufacturing sites in Kaohsiung, Taiwan and Kunshan, China. Flexium has over 50% of revenue exposed to smartphone application.

Investment strategy

We have a Neutral rating on Flexium as we expect: 1) a recovery of its iPhone business with likely stabilizing ASP; 2) the start of margin profile improvements; 3) potentially higher adoption of LCP in AI servers; and 4) more FPCB content in tablets, wearables and auto. However, we believe 1) likely slower-than-expected iPhone sell-through, 2) fierce ASP pressure from its main customer, and 3) less-than-expected LCP adoption in AI server could dampen its GM profile.

Valuation

We set a DCF-based target price of NT$75 for Flexium. We use a DCF-based valuation to reflect Flexium's capability to generate stable cash. With a riskfree rate of 4.4% (current 10-year government bond rate), a market risk premium of 7%, and an equity beta of 0.95 (based on the last 5-year share price, to reflect its long-term development), we calculate Flexium's WACC as 8.9%. Our model assumes c.4% long-term revenue growth from 2028E, and a 4.6% EBIT margin from 2027E with a mild improvement annually.

Risks

Key upside risks that could mean the shares trade above our TP include: 1) stabilizing pricing competition from FPC peers; 2) better-than-expected high-end smartphone demand and penetration; 3) better-than-expected margin improvement given gradually exiting SMT business, and 4) potentially higher adoption of LCP in AI servers. Key downside risks that could mean the shares trade below our target price include: 1) aggressive pricing competition from FPC peers; 2) worse-than-expected high-end smartphone demand; 3) less-than-expected adoption of LCP in AI servers; and 4) capacity overbuild in the FPC industry.

If you are visually impaired and would like to speak to a Citi representative regarding the details of the graphics in this document, please call USA 1-888-500-5008 (TTY: 711), from outside the US +1-210-677-3788