PDF 原檔:260630_2383_台光電_Nomura_original.pdf

圖片清單(已驗證 2026-07-01)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

_001.png |

36KB | 裝飾 | 相對績效走勢小圖(<40KB) |

_002.png |

264KB | 真資料圖 | CCL 產能擴充表 EMC vs TUC(2023–2028E k sheets/月):EMC 總產能 4,200→11,100,含觀音/崑山/中山/檳城/黃石各廠與擴產註記(可嵌) |

_003.png |

41KB | 真資料圖 | EMC forward P/E band(20/30/40x) |

_004.png |

40KB | 真資料圖 | EMC forward P/B band |

_005.png |

158KB | 真資料圖 | 評等/目標價 3 年沿革表(TP 29-Apr-26 5,285,本次升 6,880) |

除 _002 外皆為估值/沿革圖,lib 不嵌。

原始內容

Relative performance chart

EQUITY: TECHNOLOGY

Price

(TWD)

60001

5000-

40001

3000-

2000

1000 - 14

+300

- 250.

-200

-150

2383.TW 2383 TT

Elite Material

EQUITY: TECHNOLOGY

Churra. I CEC Namura

Earnings uptrend backed by pricing tailwinds

Google's AI demand in spotlight; industry pricing dynamics remain favorable

Action: Reiterate Buy; raise TP to TWD6,880, implying ~31% upside

Elite Material's (EMC) strong QTD revenue is a clear manifestation of strong AI demand (notably Google Ironwood and AWS Trainium 3), in our view, and more importantly, a smoother-thanexpected pricing uplift. We estimate 2Q26 revenue will grow +37% q-q with GM likely to further expand to 32.4%. While AI PCB/CCL industry supply is already tight loaded by existing projects, we note that most new AI platforms (e.g. Google TPU 8t/8i and nVidia VR) would only start to ramp up production in 3Q26 , spanning not only main boards but also large peripheral boards carrying content such as CPUs and switches (usually >20L; Fig. 1 ). This might further worsen the supply/demand imbalance into 2H26F, driving potentially another round of price actions by CCL makers as they strategically allocate more resources to more profitable AI PCB customers. We believe EMC is best positioned to benefit given its large capacity scale, and we observe that the company is mulling extra capacity expansion in China beyond 2027 (subject to the board approval; Fig. 2 ). Although we are aware of EMC's attempts to broaden its business scope by building high standard new capacity to prepare for ABF substrate CCL opportunities amid current industry shortages, we have not yet factored in the potential. We assume it is still focused on high-speed CCL production (the production line is fungible). Net, we raise 2026F/27F/28F EPS by 18%/22%/19% to factor in a stronger AI demand profile (particularly Google) and better profitability, and reiterate Buy with a higher TP of TWD6,880 (from TWD5,285), based on 32x 2027F EPS of TWD215 (from 30x 2027F EPS TWD176), which is at the higher end of EMC's historical band of 8-36x since 2017. We expect a continued re-rating given EMC's dominant position in the AI upcycle and persisting CCL industry shortage. EMC currently trades at 24x 2027F P/E.

Robust Google demand more than offset lukewarm demand for AWS units

Along with our Asia AI Semi & Server Anchor Report , we refresh our unit assumptions of major AI platforms - we anticipate a rather flattish chip unit demand pattern for AWS Trainium but stronger Google TPU/CPU demand backed by more upstream resources secured. We estimate CCL content opportunities from Google's TPU/CPU boards and switches could almost triple in 2027F to make up 58% of EMC's AI revenue in 2027F (vs. 38% in 2026F).

| Year-end 31 Dec Currency (TWD) | FY25 | FY26F New | Old | FY27F New | Old | FY28F New | |

|---|---|---|---|---|---|---|---|

| Actual | Old | ||||||

| Revenue (mn) | 94,261 | 176,103 | 197,788 | 270,604 | 312,625 | 366,987 | 418,200 |

| Reported net profit (mn) | 14,649 | 34,879 | 41,087 | 63,114 | 77,024 | 88,678 | 105,384 |

| Normalised net profit (mn) | 14,649 | 34,879 | 41,087 | 63,114 | 77,024 | 88,678 | 105,384 |

| FD normalised EPS | 41.67 | 97.35 | 114.67 | 176.15 | 214.96 | 247.50 | 294.11 |

| FD norm. EPS growth (%) | 49.8 | 133.6 | 175.2 | 80.9 | 87.5 | 40.5 | 36.8 |

| FD normalised P/E (x) | 126.1 | - | 45.8 | - | 24.4 | - | 17.9 |

| EV/EBITDA (x) | 89.7 | - | 32.1 | - | 17.6 | - | 12.7 |

| Price/book (x) | 37.3 | - | 24.5 | - | 14.6 | - | 10.1 |

| Dividend yield (%) | 0.5 | - | 1.3 | - | 2.5 | - | 3.4 |

| ROE (%) | 34.3 | 57.7 | 64.6 | 69.0 | 75.0 | 64.5 | 66.7 |

| Net debt/equity (%) | net cash | net cash | net cash | net cash | net cash | net cash | net cash |

Source: Company data, Nomura estimates

Global Markets Research 30 June 2026

| Rating Remains | Buy |

|---|---|

| Target price Increased from TWD 5,285.00 | TWD 6,880.00 |

| Closing price 26 June 2026 | TWD 5,255.00 |

| Implied upside | +30.9% |

| Market Cap (USD mn) | 59,047.8 |

| ADT (USD mn) | 393.2 |

Relative performance chart

Source: LSEG, Nomura

Research Analysts

Taiwan Technology

Eric Chen, CFA - NITB eric.chen@nomura.com +886(2) 21769965

Anne Lee, CFA - NITB

anne.lee@nomura.com +886(2) 21769966

Carol Hu - NITB

carol.r.hu@nomura.com +886(2) 21769963

Production Complete: 2026-06-29 20:31 UTC

Key data on Elite Material

Performance

| (%) | 1M | 3M | 12M | ||

|---|---|---|---|---|---|

| Absolute (TWD) | -0.7 | 78.4 | 514.6 | M cap (USDmn) | 59,047.8 |

| Absolute (USD) | -2 | 78.6 | 459.3 | Free float (%) | 86.1 |

| Rel to Taiwan TAIEX Index | -3.1 | 44.7 | 416.5 | 3-mth ADT (USDmn) | 393.2 |

Income statement (TWDmn)

| Year-end 31 Dec | FY24 | FY25 | FY26F | FY27F | FY28F |

|---|---|---|---|---|---|

| Revenue | 64,377 | 94,261 | 197,788 | 312,625 | 418,200 |

| Cost of goods sold | -46,407 | -66,141 | -131,625 | -199,186 | -265,794 |

| Gross profit | 17,970 | 28,120 | 66,163 | 113,438 | 152,406 |

| SG&A | -5,818 | -9,012 | -11,468 | -13,351 | -15,487 |

| Employee share expense | |||||

| Operating profit | 12,152 | 19,108 | 54,696 | 100,087 | 136,919 |

| EBITDA | 13,921 | 20,958 | 58,345 | 105,737 | 144,568 |

| Depreciation | -1,769 | -1,849 | -3,649 | -5,649 | -7,649 |

| Amortisation | |||||

| EBIT | 12,152 | 19,108 | 54,696 | 100,087 | 136,919 |

| Net interest expense | -315 | -216 | -261 | -261 | -261 |

| Associates & JCEs | 0 | 0 | 0 | 0 | 0 |

| Other income | 297 | -16 | -819 | 200 | 200 |

| Earnings before tax | 12,133 | 18,876 | 53,616 | 100,026 | 136,857 |

| Income tax | -2,564 | -4,231 | -12,532 | -23,006 | -31,477 |

| Net profit after tax | 9,569 | 14,645 | 41,083 | 77,020 | 105,380 |

| Minority interests | 9 | 4 | 4 | 4 | 4 |

| Other items | |||||

| Preferred dividends | |||||

| Normalised NPAT | 9,578 | 14,649 | 41,087 | 77,024 | 105,384 |

| Extraordinary items | 0 | 0 | 0 | 0 | 0 |

| Reported NPAT | 9,578 | 14,649 | 41,087 | 77,024 | 105,384 |

| Dividends | -5,894 | -8,958 | -25,063 | -46,985 | -64,284 |

| Transfer to reserves | 3,685 | 5,691 | 16,024 | 30,039 | 41,100 |

| Valuations and ratios | |||||

| Reported P/E (x) | 189.0 | 126.1 | 45.8 | 24.4 | 17.9 |

| Normalised P/E (x) | 189.0 | 126.1 | 45.8 | 24.4 | 17.9 |

| FD normalised P/E (x) | 189.0 | 126.1 | 45.8 | 24.4 | 17.9 |

| Dividend yield (%) | 0.3 | 0.5 | 1.3 | 2.5 | 3.4 |

| Price/cashflow (x) | 249.2 | 154.4 | 53.1 | 31.8 | 20.4 |

| Price/book (x) | 51.9 | 37.3 | 24.5 | 14.6 | 10.1 |

| EV/EBITDA (x) | 135.2 | 89.7 | 32.1 | 17.6 | 12.7 |

| EV/EBIT (x) | 154.9 | 98.4 | 34.2 | 18.6 | 13.4 |

| Gross margin (%) | 27.9 | 29.8 | 33.5 | 36.3 | 36.4 |

| EBITDA margin (%) | 21.6 | 22.2 | 29.5 | 33.8 | 34.6 |

| EBIT margin (%) | 18.9 | 20.3 | 27.7 | 32.0 | 32.7 |

| Net margin (%) | 14.9 | 15.5 | 20.8 | 24.6 | 25.2 |

| Effective tax rate (%) | 21.1 | 22.4 | 23.4 | 23.0 | 23.0 |

| Dividend payout (%) | 61.5 | 61.2 | 61.0 | 61.0 | 61.0 |

| ROE (%) | 30.9 | 34.3 | 64.6 | 75.0 | 66.7 |

| ROA (pretax %) | 23.1 | 25.6 | 51.9 | 65.3 | 64.7 |

| Growth (%) | |||||

| Revenue | 55.9 | 46.4 | 109.8 | 58.1 | 33.8 |

| EBITDA | 61.0 | 50.5 | 178.4 | 81.2 | 36.7 |

| Normalised EPS | 70.1 | 49.8 | 175.2 | 87.5 | 36.8 |

| Normalised FDEPS | 70.1 | 49.8 | 175.2 | 87.5 | 36.8 |

Source: Company data, Nomura estimates

Cashflow statement (TWDmn)

| Year-end 31 Dec | FY24 | FY25 | FY26F | FY27F | FY28F |

|---|---|---|---|---|---|

| EBITDA | 13,921 | 20,958 | 58,345 | 105,737 | 144,568 |

| Change in working capital Other operating cashflow | -5,974 | -4,651 | -9,273 | -23,438 -23,063 | -20,739 |

| Cashflow from operations | -683 7,263 | -4,339 11,968 | -13,609 35,463 | 59,235 | -31,534 92,294 |

| Capital expenditure | -5,865 | -9,488 | -18,000 | -20,000 | -20,000 |

| 1,398 | 2,480 | 17,463 | 39,235 | 72,294 | |

| Free cashflow | |||||

| Reduction in investments | 0 | 0 | 0 | 0 | 0 |

| Net acquisitions | 0 | 0 | 0 | 0 | 0 |

| Dec in other LT assets Inc in other LT liabilities | 0 | 0 | 0 | 0 | 0 0 |

| Adjustments | 0 -36 | 0 | 0 | 0 | |

| -400 | 0 | 0 | 0 | ||

| CF after investing acts | 1,363 | 2,080 | 17,463 | 39,235 | 72,294 |

| Cash dividends | -3,439 | -5,894 | -8,958 | -25,063 | -46,985 |

| Equity issue | 0 | 0 | 0 | 0 | 0 |

| Debt issue | 1,148 | 8,721 | 0 | 0 | 0 |

| Convertible debt issue | 0 | 0 | 0 | 0 | 0 |

| Others acts | 6,658 | 112 | 0 | 0 | 0 |

| CF from financial | 4,367 | 2,939 | -8,958 | -25,063 | -46,985 |

| Net cashflow | 5,729 | 5,020 | 8,505 | 14,172 | 25,310 |

| Beginning cash | 9,259 | 14,988 | 20,008 | 28,513 | 42,685 |

| Ending cash | 14,988 | 20,008 | 28,513 | 42,685 | 67,995 |

| Ending net debt | -50,496 | ||||

| -170 | -2,509 | -11,015 | -25,186 | ||

| Balance sheet (TWDmn) | |||||

| As at 31 Dec | FY24 | FY25 | FY26F | FY27F | FY28F |

| Cash & equivalents | 14,988 | 20,008 | 28,513 | 42,685 | 67,995 |

| Marketable securities | 1 | 0 | 0 | 0 | 0 |

| Accounts receivable | 25,897 | 36,115 | 61,314 | 96,914 | 129,642 |

| Inventories | 9,437 | 16,752 | 21,060 | 31,870 | 42,527 |

| Other current assets | 1,171 | 1,106 | 1,106 | 1,106 | 1,106 |

| Total current assets | 51,494 | 73,980 | 111,993 | 172,574 | 241,269 |

| LT investments | 0 | 0 | 0 | 0 | 0 |

| Fixed assets | 21,387 | 30,864 | 45,215 | 59,565 | 71,916 |

| Goodwill | 0 | 0 | 0 | 0 | 0 |

| Other intangible assets | |||||

| Other LT assets | 3,199 | 3,069 | -5,780 | -5,780 | -5,780 |

| Total assets | 76,080 | 107,913 | 151,427 | 226,359 | 307,405 |

| Short-term debt | 6,047 | 9,279 | 9,279 | 9,279 | 9,279 |

| Accounts payable | 15,963 | 24,518 | 44,752 | 67,723 | 90,370 |

| Other current liabilities | 8,172 | 12,434 | 12,434 | 12,434 | 12,434 |

| Total current liabilities | 30,182 | 46,231 | 66,466 | 89,437 | 112,083 |

| Long-term debt | 8,772 | 8,219 | 8,219 | 8,219 | 8,219 |

| Convertible debt | 2,032 | 3,027 | 0 | 0 | 0 |

| Other LT liabilities Total liabilities | |||||

| 40,986 | 57,477 | 74,685 | 97,656 | 120,302 | |

| Minority interest | |||||

| Preferred stock | |||||

| Common stock | 3,466 | 3,583 | 3,583 | 3,583 | 3,583 |

| Retained earnings | 31,673 | 46,250 | 72,557 | 124,518 | 182,917 |

| Proposed dividends Other equity and | -45 | 602 | 602 | 602 | 602 |

| reserves Total shareholders' equity Total equity & liabilities | 35,094 76,080 | 50,435 107,913 | 76,742 151,427 | 128,703 226,359 | 187,103 307,405 |

| Liquidity | |||||

| (x) | |||||

| Current ratio | 1.71 | 1.60 | 1.68 | 1.93 | |

| Interest cover | 38.5 | 88.3 | 209.3 | 382.9 | 523.8 |

| 2.15 | |||||

| Leverage Net debt/EBITDA (x) | net cash | net cash | net cash | net cash | net cash |

| Net debt/equity (%) | net cash | net cash | net cash | net cash | net cash |

| Per share | |||||

| Reported EPS (TWD) | 27.81 | 41.67 | 114.67 | 214.96 | 294.11 |

| Norm EPS (TWD) | 27.81 | 41.67 | 114.67 | 214.96 | 294.11 |

| FD norm EPS (TWD) | 27.81 | 41.67 | 114.67 | 214.96 | 294.11 |

| 140.75 | 214.17 | ||||

| BVPS (TWD) | 101.24 | 359.18 | 522.16 | ||

| DPS (TWD) Activity | 17.00 | 25.00 | 69.95 | 131.12 | 179.40 |

| (days) Days receivable | 122.5 | 120.1 | 89.9 | 92.4 | 99.1 |

| Days inventory | 61.2 | 72.3 | 52.4 | 48.5 | 51.2 |

| Days payable | 104.0 | 111.7 | 96.0 | 103.1 | 108.8 |

| Cash cycle | 79.7 | 80.6 | 46.3 | 37.8 | 41.5 |

Source: Company data, Nomura estimates

Company profile

Elite Material manufactures and sells CCLs and PP, and providing the Mass Lam service for the downstream PCB makers. Applications of its products include communication devices, networking infrastructure products and 5G communication products.

Valuation Methodology

Our TP of TWD6,880 is based on 32x 2027F EPS of TWD215. Our target multiple is at the high end of its historical P/E range of 8-36x since 2017. The benchmark of this stock is TAIEX.

Risks that may impede the achievement of the target price

Downside/upside risks: 1) smartphone demand is weaker/stronger than expected; 2) EMC's progress in high speed CCL/RCC is slower/faster than expected; 3) the adoption of HDI in vehicles is slower/faster than expected; and 4) unexpected share loss/gains in AI server/switch, 5) weaker/stronger-than-expected demand from AI server/switch.

ESG

EMC is committed to sustainability management and minimizing the impact of its operations to the environment. EMC adopts ESH (Environmental, Safety, and Health) philosophy and management system. The waste of the production process is classified, and the materials can be recycled and reused are properly stored and consumed again internally.

Fig. 1: A summary of AI PCB/CCL specs and supply chain

nVidia

| Generation | Content | Time | Structure | CCL Material | CCL Supplier(s) | PCB Supplier(s) | PCB Supplier(s) |

|---|---|---|---|---|---|---|---|

| H100 | OAM UBB | 2H23-1Q25 | 5+8+5 HDI (18L) 24L PCB | M7 M7 | EMC EMC | Unimicron (major), VGT, others | WUS, ISU, TTM, |

| B200 | OAM | 2H24~ | 5+10+5 HDI (20L) 18L PCB | M8+M4 | Doosan | Unimicron, VGT, others | WUS, ISU, TTM, |

| UBB | 2H25~ | 5+10+5 HDI (20L) | M7+M4 M8+M4 | Doosan | |||

| B300 | OAM UBB | 2H24~ | 22L PCB | M8+M4 | Doosan Doosan | Unimicron, VGT, others WUS, ISU, TTM, others | Unimicron, VGT, others WUS, ISU, TTM, others |

| GB200 | Bianca board Switch tray | 5+12+5 HDI (22L) 6+12+6 HDI (24L) | M8 (HVLP3) +M4 M7 (HVLP2)+M2 | Doosan EMC | VGT (major), Unimicron, others | VGT (major), Unimicron, others | |

| GB300 (Bianca) | 2H24~ | 22L PCB | M8/8.5 (HVLP2) hybrid | EMC, SYTECH | VGT (major), Unimicron, others WUS (major), VGT, Unimicron, others | VGT (major), Unimicron, others WUS (major), VGT, Unimicron, others | |

| (Bianca) | Bianca board Switch tray | 2Q25~ | 5+12+5 HDI (22L) 22L PCB | M8 (HVLP3) +M4 | Doosan EMC, SYTECH, | WUS (major), VGT, Unimicron, | WUS (major), VGT, Unimicron, |

| VR200 (Bianca) | Bianca board Mid-plane boards in trays | 2Q25~ 2Q26~ | 6+14+6 HDI (26L) | M8/8.5 (HVLP2) hybrid M8 (HVLP4) +M4 | Doosan Doosan | others VGT (major), Unimicron, others? | others VGT (major), Unimicron, others? |

| 26Lx3=78L?, ? Rubin Ultra | (New) Switch tray Backplane? (New) 2027? Compute board 2027? | 2Q26~ 2Q26~ ? | 44L PCB 32L PCB 104L? | M9K2 M8.5 (k2, HVLP4) M9Q? PTFE+M8? | EMC, others? EMC, others? EMC, SYTECH? | VGT, WUS, Kinwong, Unimicron? WUS, VGT, others? | WUS. Unimicron, |

| 2027? CoWoP board? Content OAM | TBD? Time | ? HDI/mSAP? Structure | M8? M9Q? | EMC or new | ZDT, Unimicron? Others? | ZDT, Unimicron? Others? | |

| AWS Generation | Switch board | ||||||

| Trainium 2 | UBB | 2H24~4Q25 | HDI+3 26L PCB (2 ASICs per board, air cool) HDI+4 (22L) | CCL Material M6? (HVLP2, RTF) | materials? CCL Supplier(s) Panasonic | PCB Supplier(s) | Shengyi |

| PCB (2 ASICs - Trainium 2.5 & 3 | UBB Trn2.5: 1Q26~ Trn3: 2Q26~ | 26L or 4 | ASICs - liquid-cooled) | M8 (HVLP2) M6?M7? (HVLP2, RTF) | EMC, TUC (starting Panasonic | from June 2025) | GCE, Shengyi, FHE Shengyi, ZDT |

| HLC Structure PCB (16+18, | OAM Time TPU UBB 2H25~ CPU board (New) - x86 CPU 4Q25~ | 22L/26L 34L 16-18L | PCB N+M) Structure 36L+? 40L+? | air-cooled, M8 (HVLP4) M7, HVLP2 M6 | EMC, TUC, others? EMC CCL Supplier(s) Panasonic, EMC | GCE, Shengyi, FHE | PCB Supplier(s) |

| Google Generation | PDS switch (New) | 2Q26~ | ? HDI 46-48L HDI+HLC PCB, wide | M8+M4 M8.5? M9Q? | WUS, Shengyi, ZDT, GCE? | WUS, Shengyi, ZDT, GCE? | |

| Content | Time 2H26~ | size | CCL Material | ||||

| TPU 7x TPU 8t, 8i | TPU UBB CPU board (New) - Axion 8i all-to-all switch (New) | mid-26~ 2Q26~ mid-26~ | 36~40L+ PCB 22L PCB 22L PCB 24~26L? HDI? | M8+M6, HVLP3 M6 | Panasonic Panasonic, EMC EMC, Panasonic EMC | WUS, ISU, TTM, VGT WUS, TTM, GCE? WUS, ISU, TTM, LCS, VGT? | WUS, ISU, TTM, VGT WUS, TTM, GCE? WUS, ISU, TTM, LCS, VGT? |

| TPU UBB? More other boards? | 2028? | M8? | Panasonic? EMC? | VGT, WUS, ISU, TTM, GCE, VGT, ZDT, others? | VGT, WUS, ISU, TTM, GCE, VGT, ZDT, others? | ||

| TPU next? Meta | Content OAM, UBB OAM, UBB | Time | Structure | CCL Material CCL Material | CCL Supplier(s) | PCB Supplier(s) WUS, ISU, TTM | PCB Supplier(s) WUS, ISU, TTM |

| Generation | Content | 2Q26? | M8? | CCL Supplier(s) EMC | others? WUS, ISU, Unimicron, others? | others? WUS, ISU, Unimicron, others? | |

| Athena Iris | OAM, UBB | PCB Supplier(s) | PCB Supplier(s) | ||||

| AMD | EMC? | others? | others? | ||||

| EMC | |||||||

| M8+M4 | WUS, ISU, TTM | WUS, ISU, TTM | |||||

| 2H26~ | M8+M4 | ||||||

| Generation | |||||||

| MI450 | |||||||

| UBB | 2H26~ | M8 hybrid | Unimicron, | Unimicron, | |||

| EMC, Doosan | SCC, Others? | SCC, Others? |

Source: Company data, Nomura estimates

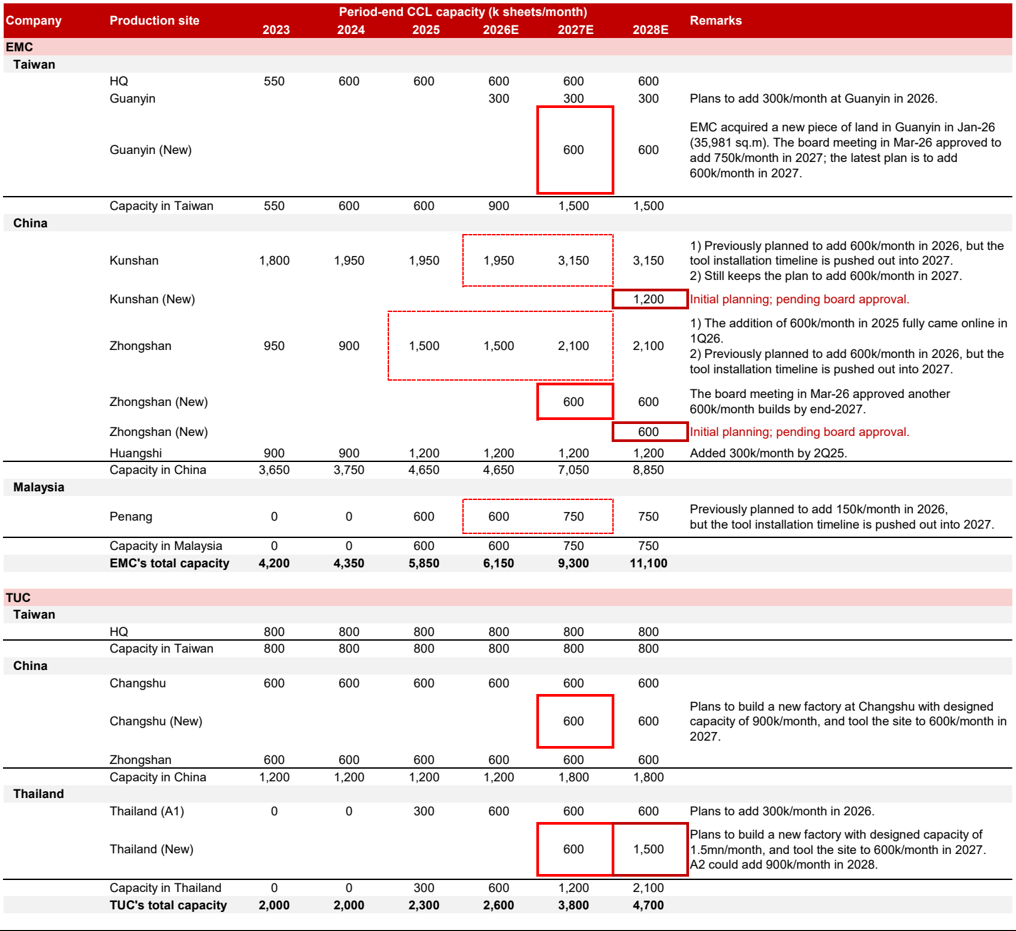

Fig. 2: CCL capacity expansion: EMC vs TUC

| Company | Production site | 2023 | 2024 Period-end | 2025 CCL capacity | 2026E (k sheets/month) | 2027E | 2028E | Remarks |

|---|---|---|---|---|---|---|---|---|

| EMC | ||||||||

| Taiwan | HQ | 550 | 600 | 600 | 600 | 600 | 600 | |

| Guanyin | 300 | 300 | 300 | Plans to add 300k/month at Guanyin in 2026. | ||||

| Guanyin (New) | 600 | 600 | EMC acquired a new piece of land in Guanyin in Jan-26 (35,981 sq.m). The board meeting in Mar-26 approved to add 750k/month in 2027; the latest plan is to add 600k/month in 2027. | |||||

| Capacity in Taiwan | 550 | 600 | 600 | 900 | 1,500 | 1,500 | ||

| China | ||||||||

| Kunshan | 1,800 | 1,950 | 1,950 | 1,950 | 3,150 | 3,150 | 1) Previously planned to add 600k/month in 2026, but the tool installation timeline is pushed out into 2027. 2) Still keeps the plan to add 600k/month in 2027. | |

| Kunshan (New) | 1,200 | Initial planning; pending board approval. | ||||||

| Zhongshan | 950 | 900 | 1,500 | 1,500 | 2,100 | 2,100 | 1Q26. 2) Previously planned to add 600k/month in 2026, but the tool installation timeline is pushed out into 2027. | |

| Zhongshan (New) | 600 | 600 | The board meeting in Mar-26 approved another 600k/month builds by end-2027. | |||||

| Zhongshan (New) | 600 | Initial planning; pending board approval. | ||||||

| Huangshi | 900 | 900 | 1,200 | 1,200 | 1,200 | 1,200 | Added 300k/month by 2Q25. | |

| Capacity in China | 3,650 | 3,750 | 4,650 | 4,650 | 7,050 | 8,850 | ||

| Malaysia | ||||||||

| Penang | 0 | 0 | 600 | 600 | 750 | 750 | Previously planned to add 150k/month in 2026, but the tool installation timeline is pushed out into 2027. | |

| Capacity in Malaysia | 0 | 0 | 600 | 600 | 750 | 750 | ||

| EMC's total capacity | 4,200 | 4,350 | 5,850 | 6,150 | 9,300 | 11,100 | ||

| TUC | ||||||||

| Taiwan | HQ | 800 | 800 | 800 | 800 | 800 | 800 | |

| Capacity in Taiwan | 800 | 800 | 800 | 800 | 800 | 800 | ||

| China | Changshu | 600 | 600 | 600 | 600 | 600 | 600 | |

| Changshu (New) | 600 | 600 | Plans to build a new factory at Changshu with designed capacity of 900k/month, and tool the site to 600k/month in 2027. | |||||

| Zhongshan | 600 | 600 | 600 | 600 | 600 | 600 | ||

| Capacity in China | 1,200 | 1,200 | 1,200 | 1,200 | 1,800 | 1,800 | ||

| Thailand | Thailand (New) | 600 | 1,500 | Plans to add 300k/month in 2026. Plans to build a new factory with designed capacity of 1.5mn/month, and tool the site to 600k/month in 2027. | ||||

| Thailand (A1) | 0 | 0 | 300 | 600 | 600 | 600 | ||

| Capacity in Thailand | 0 | 0 | 300 | 600 | 1,200 | 2,100 | ||

| TUC's total capacity | 2,000 | 2,000 | 2,300 | 2,600 | 3,800 | 4,700 |

Source: Company data, Nomura estimates

Fig. 3: EMC: Earnings estimate revisions

| New forecasts | New forecasts | New forecasts | Previous forecasts | Previous forecasts | Previous forecasts | Change (%) | Change (%) | Change (%) | |

|---|---|---|---|---|---|---|---|---|---|

| TWD mn | 2026F | 2027F | 2028F | 2026F | 2027F | 2028F | 2026F | 2027F | 2028F |

| Revenue | 197,788 | 312,625 | 418,200 | 176,103 | 270,604 | 366,987 | 12.3 | 15.5 | 14.0 |

| Gross profit | 66,163 | 113,438 | 152,406 | 58,069 | 95,329 | 130,674 | 13.9 | 19.0 | 16.6 |

| Operating profit | 54,696 | 100,087 | 136,919 | 46,633 | 82,022 | 115,221 | 17.3 | 22.0 | 18.8 |

| Pretax profit | 53,616 | 100,026 | 136,857 | 45,553 | 81,962 | 115,161 | 17.7 | 22.0 | 18.8 |

| Net profit | 41,087 | 77,024 | 105,384 | 34,879 | 63,114 | 88,678 | 17.8 | 22.0 | 18.8 |

| EPS (TWD) | 114.7 | 215.0 | 294.1 | 97.3 | 176.1 | 247.5 | 17.8 | 22.0 | 18.8 |

| Margins (%) | |||||||||

| Gross margin | 33.5 | 36.3 | 36.4 | 33.0 | 35.2 | 35.6 | 0.5 | 1.1 | 0.8 |

| Operating margin | 27.7 | 32.0 | 32.7 | 26.5 | 30.3 | 31.4 | 1.2 | 1.7 | 1.3 |

| Pretax margin | 27.1 | 32.0 | 32.7 | 25.9 | 30.3 | 31.4 | 1.2 | 1.7 | 1.3 |

| Net margin | 20.8 | 24.6 | 25.2 | 19.8 | 23.3 | 24.2 | 1.0 | 1.3 | 1.0 |

Source: Nomura estimates

(TWD)

6,000

5,000

4,000

3,000

2,000

1,000

0

Fig. 4: EMC: Quarterly financial report

(TWD)

6,000

5,000

| (TWD mn) | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 2025 | 1Q26 | 2Q26F | 3Q26F | 4Q26F | 2026F | 1Q27F | 2Q27F | 3Q27F | 4Q27F | 2027F | 2028F |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Net revenue | 21,680 | 22,508 | 25,146 | 24,927 | 94,261 | 33,067 | 45,143 | 55,394 | 64,184 | 197,788 | 67,056 | 74,981 | 83,471 | 87,117 | 312,625 | 418,200 |

| COGS | 15,090 | 15,678 | 17,570 | 17,803 | 66,141 | 23,338 | 30,500 | 36,411 | 41,375 | 131,625 | 43,019 | 47,714 | 53,043 | 55,411 | 199,186 | 265,794 |

| Gross profit | 6,590 | 6,829 | 7,576 | 7,125 | 28,120 | 9,729 | 14,642 | 18,983 | 22,809 | 66,163 | 24,037 | 27,267 | 30,428 | 31,706 | 113,438 | 152,406 |

| Op expenses | 2,051 | 2,186 | 2,586 | 2,190 | 9,012 | 2,601 | 2,826 | 3,010 | 3,031 | 11,468 | 3,086 | 3,269 | 3,485 | 3,511 | 13,351 | 15,487 |

| Op profit | 4,540 | 4,644 | 4,990 | 4,935 | 19,108 | 7,128 | 11,817 | 15,972 | 19,779 | 54,696 | 20,952 | 23,998 | 26,942 | 28,195 | 100,087 | 136,919 |

| Non-op income | 128 | (177) | 131 | (314) | (232) | 66 | (565) | (565) | (15) | (1,080) | (15) | (15) | (15) | (15) | (61) | (61) |

| Pretax profit | 4,667 | 4,467 | 5,121 | 4,620 | 18,876 | 7,194 | 11,251 | 15,407 | 19,763 | 53,616 | 20,936 | 23,983 | 26,927 | 28,180 | 100,026 | 136,857 |

| Net profit | 3,469 | 3,478 | 3,965 | 3,737 | 14,649 | 5,340 | 8,665 | 11,864 | 15,219 | 41,087 | 16,122 | 18,468 | 20,735 | 21,700 | 77,024 | 105,384 |

| EPS (TWD) | 10.01 | 10.02 | 11.19 | 10.63 | 41.67 | 14.90 | 24.18 | 33.11 | 42.47 | 114.67 | 44.99 | 51.54 | 57.87 | 60.56 | 214.96 | 294.11 |

| Operating ratios (%) | ||||||||||||||||

| Gross margin | 30.4% | 30.3% | 30.1% | 28.6% | 29.8% | 29.4% | 32.4% | 34.3% | 35.5% | 33.5% | 35.8% | 36.4% | 36.5% | 36.4% | 36.3% | 36.4% |

| Operating margin | 20.9% | 20.6% | 19.8% | 19.8% | 20.3% | 21.6% | 26.2% | 28.8% | 30.8% | 27.7% | 31.2% | 32.0% | 32.3% | 32.4% | 32.0% | 32.7% |

| Pretax profit margin | 21.5% | 19.8% | 20.4% | 18.5% | 20.0% | 21.8% | 24.9% | 27.8% | 30.8% | 27.1% | 31.2% | 32.0% | 32.3% | 32.3% | 32.0% | 32.7% |

| Net profit margin | 16.0% | 15.5% | 15.8% | 15.0% | 15.5% | 16.1% | 19.2% | 21.4% | 23.7% | 20.8% | 24.0% | 24.6% | 24.8% | 24.9% | 24.6% | 25.2% |

| Year-to-year (%) | ||||||||||||||||

| Net revenue | 68% | 46% | 44% | 34% | 46% | 53% | 101% | 120% | 157% | 110% | 103% | 66% | 51% | 36% | 58% | 34% |

| Gross profit | 76% | 61% | 61% | 35% | 56% | 48% | 114% | 151% | 220% | 135% | 147% | 86% | 60% | 39% | 71% | 34% |

| Operating profit | 79% | 59% | 58% | 40% | 57% | 57% | 154% | 220% | 301% | 186% | 194% | 103% | 69% | 43% | 83% | 37% |

| Pre-tax profit | 79% | 50% | 61% | 37% | 56% | 54% | 152% | 201% | 328% | 184% | 191% | 113% | 75% | 43% | 87% | 37% |

| Net profit | 75% | 43% | 58% | 41% | 53% | 54% | 149% | 199% | 307% | 180% | 202% | 113% | 75% | 43% | 87% | 37% |

| Qtr-to-Qtr (%) | ||||||||||||||||

| Net revenue | 17% | 4% | 12% | -1% | 33% | 37% | 23% | 16% | 4% | 12% | 11% | 4% | ||||

| Gross profit | 25% | 4% | 11% | -6% | 37% | 51% | 30% | 20% | 5% | 13% | 12% | 4% | ||||

| Operating profit | 29% | 2% | 7% | -1% | 44% | 66% | 35% | 24% | 6% | 15% | 12% | 5% | ||||

| Pre-tax profit | 38% | -4% | 15% | -10% | 56% | 56% | 37% | 28% | 6% | 15% | 12% | 5% | ||||

| Net profit | 31% | 0% | 14% | -6% | 43% | 62% | 37% | 28% | 6% | 15% | 12% | 5% |

Source: Company data, Nomura estimates

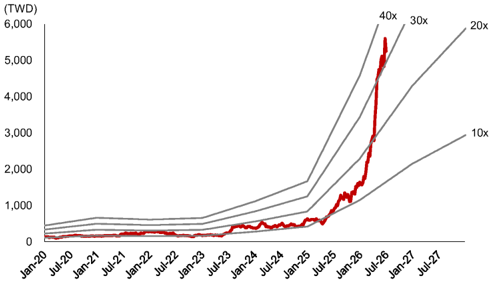

Fig. 5: EMC: forward P/E band

Source: TEJ, Nomura estimates

40x 30x

, 20x

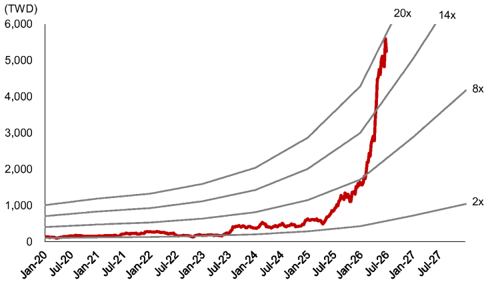

Fig. 6: EMC: forward P/B band

Source: TEJ, Nomura estimates

20x

Rating and target price chart (three year history)

6000.00

5500.00

5000.00

4500.00 •

4000.00

3500.00

3000.00

2500.00

2000.00

1500.00

1000.00

500.00

0.00

Elite Material

Appendix A-1

Di

11

31

30

28

This report has been produced by Nomura International (Hong Kong) Ltd., Taipei Branch (NITB), Taiwan. See Disclaimers for Nomura Group entity details.