PDF 原檔:260616_3231_緯創_gs_wistron_original.pdf

原始內容

Wistron (3231.TW): Monthly revenues preview: AI servers global capacity ramping up; Model transition could weigh on 3Q26E; Buy

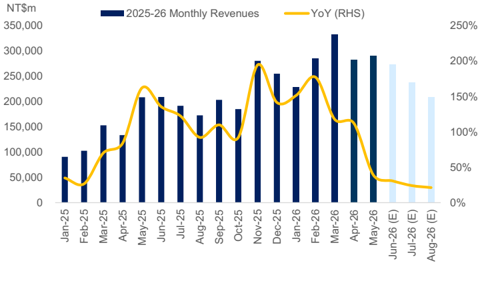

Wistron's May revenue was fl at MoM, or 13% above our estimate, which we attribute to the company's strong rack-level AI server and general servers solid demand. We model sequential revenue declines in Jun-Aug, considering PC consumption pull-in in 1H26 and rack-level AI server model transition. Despite the MoM decline, our estimate still assumes double-digit YoY growth for Jun-Aug revenues, re fl ecting our positive view on Wistron serving global leading brand makers, better riding on the growing AI infrastructure trend. The company's global capacity expansion in Vietnam and US (link) should also support their AI servers business in coming years. Maintain Buy.

Exhibit 1: Wistron monthly revenues

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 2: Wistron 3-month revenue preview

| 26-Apr | 26-May | Jun-26 (E) | Jul-26 (E) | Aug-26 (E) | Sep-26 (E) | 2Q26 (E) | 3Q26 (E) | |

|---|---|---|---|---|---|---|---|---|

| Rev (NT$m) | 283,437 | 290,183 | 273,451 | 237,902 | 209,354 | 214,543 | 847,071 | 661,799 |

| Rev YoY | 112% | 39% | 31% | 24% | 21% | 5% | 54% | 17% |

| RevMoM/QoQ | -15% | 2% | -6% | -13% | -12% | 2% | 0% | -22% |

| GS estimates | 249,782 | 257,276 | ||||||

| Act. Vs. GS | 13% | 13% |

Source: Company data, Goldman Sachs Global Investment Research

Earnings revision: We factor in Wistron's 1Q26 result and May revenue and raise our 2026E-28E net income forecasts by 20% / 17% / 20%, mainly on higher revenues. We raise our 2026E-28E revenues by 9% / 19% / 18%, re fl ecting (1) stronger-than-expected revenue growth in 1Q26, supported by strong AI server business performance, and (2) rising GPU and ASIC AI server shipments growth, along with new models entering in 2H26. Our 2026E opex ratio is slightly revised down to re fl ect the lower-than-expected 1Q26 opex ratio, mainly on higher revenue

Goldman Sachs does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the fi rm may have a con fl ict of interest that could a ff ect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certi fi cation and other important disclosures, see the Disclosure Appendix, or go to www.gs.com/research/hedge.html. Analysts employed by non-US a ffi liates are not registered/quali fi ed as research analysts with FINRA in the U.S.

Verena Jeng

+852-2978-1681 | verena.jeng@gs.com Goldman Sachs (Asia) L.L.C.

Allen Chang +852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Yifan Hu

+852-2978-0996 | yifan.hu@gs.com Goldman Sachs (Asia) L.L.C.

e92c7a75ab8b4efbba794e6b187208c8

scale. Our 2026E-28E GMs are largely unchanged.

Exhibit 3: Earnings revision

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| NT m | Old | New | Chg | Old | New | Chg | Old | New | Chg |

| Revenue | 3,029,057 | 3,291,847 | 9% | 3,601,540 | 4,285,249 | 19% | 4,228,156 | 4,989,536 | 18% |

| GP | 178,040 | 196,001 | 10% | 220,816 | 260,686 | 18% | 256,248 | 305,540 | 19% |

| OP | 117,284 | 134,761 | 15% | 150,586 | 177,124 | 18% | 169,571 | 203,255 | 20% |

| Net income | 41,704 | 49,880 | 20% | 54,279 | 63,536 | 17% | 63,044 | 75,483 | 20% |

| Margins | |||||||||

| GM | 5.9% | 6.0% | 6.1% | 6.1% | 6.1% | 6.1% | |||

| OPM | 3.9% | 4.1% | 4.2% | 4.1% | 4.0% | 4.1% | |||

| NM | 1.4% | 1.5% | 1.5% | 1.5% | 1.5% | 1.5% |

Source: Company data, Goldman Sachs Global Investment Research

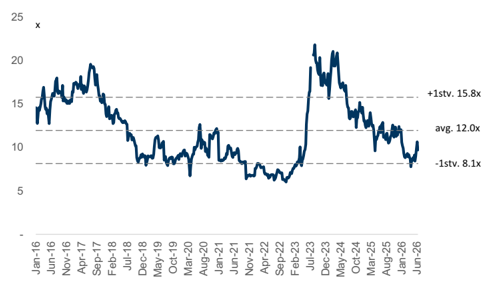

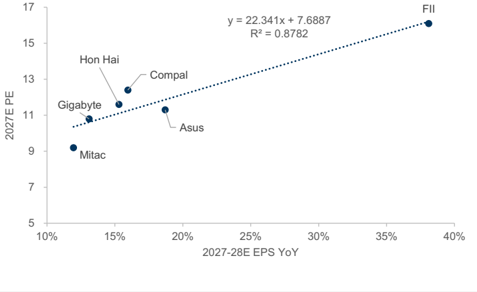

Valuation: We continue to use near-term P/E to derive our 12M TP. Our target multiple is updated to 13.2x 2027E EPS (vs. 13.9x previously), which is derived from the refreshed peers' correlation between forward trading P/E and earnings growth. With our updated earnings estimates and target multiple, our 12M TP is unchanged at NT$246. Our target P/E is still between the company's historical avg. and avg.+1stv. trading P/E, re fl ecting our positive view on Wistron's market leading position in AI server ODM. Maintain Buy.

Exhibit 4: Wistron 12m forward P/E

Source: Company data, Goldman Sachs Global Investment Research

Exhibit 6: Wistron's QFII

Source: TEJ

Exhibit 5: Wistron peers' 2027E P/E vs. 2027-28E avg. EPS YoY

Source: Company data, Goldman Sachs Global Investment Research

e92c7a75ab8b4efbba794e6b187208c8

Exhibit 7: Wistron P&L summary

| (NT$ m) | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 346,485 | 551,291 | 567,805 | 720,941 | 846,303 | 847,071 | 661,799 | 936,673 | 984,619 | 867,057 | 1,049,256 | 2,186,523 | 3,291,847 | 4,285,249 | 4,989,536 |

| Gross profit | 27,056 | 24,453 | 41,965 | 40,509 | 44,094 | 45,901 | 48,130 | 57,876 | 69,729 | 68,983 | 84,091 | 133,983 | 196,001 | 260,686 | 305,540 |

| Operating expense | (5,564) | (5,881) | (5,909) | (6,705) | (7,323) | (7,329) | (5,354) | (7,577) | (42,257) | (41,593) | (45,112) | (55,430) | (61,240) | (83,562) | (102,285) |

| Operating income | 15,150 | 10,787 | 27,142 | 25,474 | 29,137 | 30,931 | 35,166 | 39,527 | 27,472 | 27,390 | 38,979 | 78,553 | 134,761 | 177,124 | 203,255 |

| Net income | 5,331 | 6,504 | 7,406 | 8,167 | 9,631 | 11,789 | 13,108 | 15,352 | 11,162 | 11,472 | 17,446 | 27,408 | 49,880 | 63,536 | 75,483 |

| EPS, diluted (NT$) | 1.82 | 2.19 | 2.34 | 2.05 | 2.83 | 3.46 | 3.85 | 4.50 | 3.84 | 3.98 | 5.99 | 8.40 | 14.63 | 18.64 | 22.14 |

| Margins / ratio | |||||||||||||||

| Gross margin | 7.8% | 4.4% | 7.4% | 5.6% | 5.2% | 5.4% | 7.3% | 6.2% | 7.1% | 8.0% | 8.0% | 6.1% | 6.0% | 6.1% | 6.1% |

| Opex ratio | -3.4% | -2.5% | -2.6% | -2.1% | -1.8% | -1.8% | -2.0% | -2.0% | -4.3% | -4.8% | -4.3% | -2.5% | -1.9% | -2.0% | -2.1% |

| Operating margin | 4.4% | 2.0% | 4.8% | 3.5% | 3.4% | 3.7% | 5.3% | 4.2% | 2.8% | 3.2% | 3.7% | 3.6% | 4.1% | 4.1% | 4.1% |

| Net margin | 1.5% | 1.2% | 1.3% | 1.1% | 1.1% | 1.4% | 2.0% | 1.6% | 1.1% | 1.3% | 1.7% | 1.3% | 1.5% | 1.5% | 1.5% |

| QoQ | |||||||||||||||

| Revenue | 17% | 59% | 3% | 27% | 17% | 0% | -22% | 42% | |||||||

| Gross profit | 13% | -10% | 72% | -3% | 9% | 4% | 5% | 20% | |||||||

| Operating income | 28% | -29% | 152% | -6% | 14% | 6% | 14% | 12% | |||||||

| Net income | 0% | 22% | 14% | 10% | 18% | 22% | 11% | 17% | |||||||

| EPS | 2% | 20% | 7% | -12% | 38% | 22% | 11% | 17% | |||||||

| YoY | |||||||||||||||

| Revenue | 45% | 130% | 108% | 143% | 144% | 54% | 17% | 30% | 14% | -12% | 21% | 108% | 51% | 30% | 16% |

| Gross profit | 57% | 22% | 85% | 69% | 63% | 88% | 15% | 43% | 36% | -1% | 22% | 59% | 46% | 33% | 17% |

| Operating income | 115% | 25% | 138% | 115% | 92% | 187% | 30% | 55% | 68% | 0% | 42% | 102% | 72% | 31% | 15% |

| Net income | 51% | 47% | 76% | 54% | 81% | 81% | 77% | 88% | 7% | 3% | 52% | 57% | 82% | 27% | 19% |

| EPS | 49% | 43% | 61% | 15% | 55% | 58% | 65% | 120% | 2% | 4% | 51% | 40% | 74% | 27% | 19% |

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - Wistron

Our 12-month target price of NT$246 is based on a 13.2x 2027E P/E, which is derived from PC/server peer EPS growth vs. P/E multiple correlation. We see EPS growth as a major factor for the stock's share price performance.

Key downside risks: 1) weaker-than-expected PC market recovery, 2) slower-than-expected AI server demand ramp-up, and 3) weaker-than-expected demand on general servers.

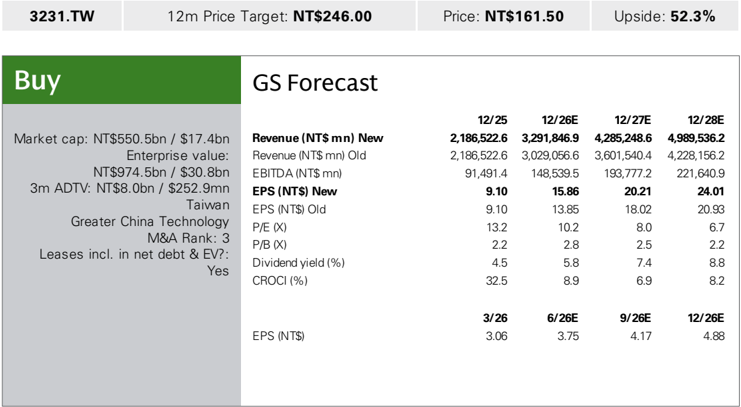

| 3231.TW | 12m Price Target: NT$246.00 | 12m Price Target: NT$246.00 | Price: NT$161.50 | Price: NT$161.50 | Upside: 52.3% | Upside: 52.3% |

|---|---|---|---|---|---|---|

| Buy | Buy | GS Forecast | ||||

| Market c ap: NT$550.5bn / $ 17 . 4 bn E nterpr is e v a lu e: NT$ 974 .5bn / $ 3 0. 8 bn 3m AD T V : G reater L ea s e s i n | Market c ap: NT$550.5bn / $ 17 . 4 bn E nterpr is e v a lu e: NT$ 974 .5bn / $ 3 0. 8 bn 3m AD T V : G reater L ea s e s i n | Revenue (NT$m n ) N e w Revenue (NT$ mn) Old EBITDA (NT$ mn) E PS(NT$) N e w EPS (NT$) Old P/E (X) P/B (X) Dividend yield (%) CROCI (%) | 1 2 / 2 5 2, 186 , 5 22. 6 2,186,522.6 91,491.4 9. 1 0 9.10 13.2 2.2 4.5 32.5 3 / 2 6 | 1 2 / 2 6E 3,29 1 , 8 4 6 .9 3,029,056.6 148,539.5 15 . 86 13.85 10.2 2.8 5.8 8.9 6/ 2 6E | 1 2 / 2 7E 4,2 85 ,24 8 . 6 3,601,540.4 193,777.2 20.2 1 18.02 8.0 2.5 7.4 6.9 9 / 2 6E | 1 2 / 2 8E 4,9 8 9, 5 3 6 .2 4,228,156.2 221,640.9 24.0 1 20.93 6.7 2.2 8.8 8.2 1 2 / 2 6E |

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 15 Jun 2026 close.

e92c7a75ab8b4efbba794e6b187208c8

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260616_3231_緯創_gs_wistron_001.png |

40KB | 真資料圖 | 2025-26 月營收長條圖(左軸 NT$m)+ YoY 折線圖(右軸 %),X 軸 Jan-25 至 Aug-26(E) |

260616_3231_緯創_gs_wistron_004.png |

22KB | 真資料圖 | 2027E PE vs 2027-28E EPS YoY 散佈圖,比較 FII、Hon Hai、Compal、Gigabyte、Asus、Mitac,含迴歸線與 R²=0.8782 |