PDF 原檔:260610_4938_和碩_ms_pegatron_original.pdf

原始內容

M June 10, 2026 06:25 PM GMT

Pegatron Corporation | Asia Pacific

May Sales Rose 10% m/m, 12% y/y

Key Takeaways

- May sales were NT$96B (+10% m/m, +12% y/y).

- Unaudited April + May revenues are 58% of our 2Q26 estimate of NT$316B (+30% q/q, +18% y/y) and 64% of consensus at NT$284B (+16% q/q, +6% y/y).

- May notebook shipments were 0.575M units (+10% m/m, -26% y/y), 8% below MSe.

Our view:

- Unaudited April + May revenues are tracking below 2Q revenue estimate, but roughly in line with the Street's.

- May notebook shipments came in 8% below our estimate of 0.625M units (+19% m/m, -19% y/y); we continue to attribute the underperformance to difficulties to procure sufficient memory and even CPU, particularly for smaller PC OEMs. The stronger-than-expected pull-ins in 1Q may have led to the underperformance quarter-to-date as well, in our view.

- The company will not be providing guidance on notebook shipment volumes going forward, as it believes the mix within the Computing segment has been evolving with a greater emphasis on the server business.

- We remain EW on Pegatron.

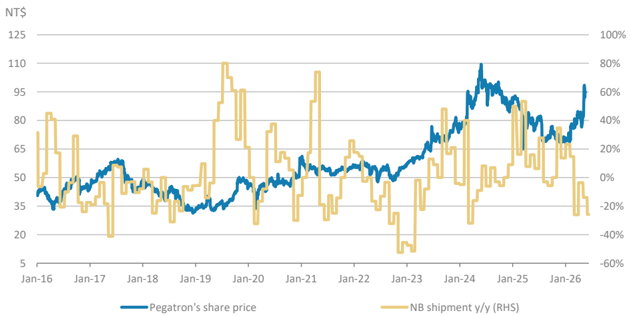

Exhibit 1 : Pegatron's NB shipments vs. its share price

Note: Past performance is no guarantee of future results. Results shown do not include transaction costs. Source: Company data, TEJ, Morgan Stanley Research.

Morgan Stanley Taiwan Limited+

Howard Kao

Equity Analyst

Howard.Kao@morganstanley.com

+886 2 2730-2989

Sharon Shih

Equity Analyst

Sharon.Shih@morganstanley.com

+886 2 2730-2865

Irene Yen

Research Associate

Irene.Yen@morganstanley.com

+886 2 2730-2869

Pegatron Corporation (4938.TW, 4938 TT)

Greater China Technology Hardware | Taiwan

| Stock Rating | Equal-weight |

|---|---|

| Industry View | In-Line |

| Price target | NT$85.00 |

| Up/downside to price target (%) | (10) |

| Shr price, close (Jun 10, 2026) | NT$94.80 |

| 52-Week Range | NT$102.50-67.50 |

| Sh out, dil, curr (mn) | 2,614 |

| Mkt cap, curr (mn) | NT$247,786 |

| EV, curr (mn) | NT$213,672 |

| Avg daily trading value (mn) | NT$824 |

| Fiscal Year Ending | 12/25 | 12/26e | 12/27e | 12/28e |

|---|---|---|---|---|

| EPS (NT$)** | 5.39 | 5.39 | 7.61 | 8.04 |

| EPS (NT$)§ | 4.92 | 5.66 | 6.83 | 7.43 |

| Revenue, net (NT$ mn) | 1,117,16 | 1,315,91 | 1,858,12 | 2,006,04 |

| EBITDA (NT$ mn) | 27,307 | 35,257 | 45,062 | 48,368 |

| ModelWare net inc (NT | 14,403 | 14,415 | 20,347 | 21,491 |

| $ mn) | ||||

| P/E | 12.7 | 17.6 | 12.4 | 11.8 |

| P/BV | 0.7 | 0.9 | 0.9 | 0.9 |

| RNOA (%) | 5.5 | 7.3 | 10.2 | 10.3 |

| ROE (%) | 6.0 | 5.8 | 7.6 | 7.8 |

| EV/EBITDA | 5.5 | 5.6 | 4.3 | 4.2 |

| Div yld (%) | 6.1 | 0.0 | 0.0 | 0.0 |

| FCF yld ratio (%)** | 5.3 | 3.5 | 3.3 | 0.0 |

| Leverage (EOP) (%) | (21.9) | (26.8) | (26.0) | (22.1) |

Unless otherwise noted, all metrics are based on Morgan Stanley ModelWare framework

§ = Consensus data is provided by Refinitiv Estimates

** = Based on consensus methodology

e = Morgan Stanley Research estimates

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260610_4938_和碩_ms_pegatron_001.png |

59KB | 真資料圖 | 雙軸折線圖,橫軸Jan-16至Jan-26,左軸NT$(5-125)為藍線「Pegatron's share price」,右軸-60%~100%為黃線「NB shipment y/y (RHS)」 |