PDF 原檔:260607_3665_貿聯_ms_bizlink_original.pdf

原始內容

M June 7, 2026 08:06 AM GMT

Bizlink | Asia Pacific

May Sales Flat MoM/+41% YoY

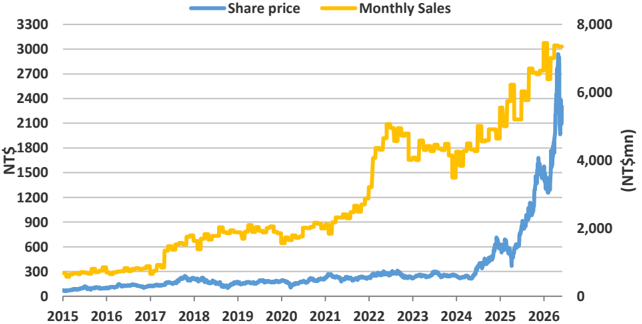

In this report, we focus on Bizlink's monthly sales, which we believe could be a catalyst for its share price.

Details:

- May sales came in at NT$7,352mn (flat MoM/+41% YoY).

- QTD reached 65% of both our 2Q26 estimate of NT$22,836mn (+9% QoQ/ +35% YoY) and consensus at NT$22,832mn (+9% QoQ/+35% YoY).

Our view:

- 2Q26 revenue tracking in line with market expectations, in our view.

- We believe 1Q26 GM of 28.8% (-3.2ppt QoQ) should prove temporary, as the impact of a less favorable HPC revenue mix should ease in the coming quarters amid the new model ramp.

- Power interconnect products should benefit from server rack shipment growth in 2026, while higher dollar content from next-generation GPU servers and HVDC architecture should emerge mainly from 2027.

- Data interconnect products should continue to grow on wider AEC adoption into 2026-27, with potential incremental contribution from optical solutions (e.g., shuffle box, ALC) from 2027.

- Power interconnects should benefit from GB rack ramp-up this year, along with higher dollar content from Rubin racks from 2026 and standalone HVDC power racks from 2027, while data interconnects should continue to grow on broader AEC adoption into 2026-27.

- We remain constructive on Bizlink as a beneficiary of AI, driven by data/ power interconnect and semi cap equipment businesses. Stay OW.

Exhibit 1 : Bizlink's monthly sales vs. its share price since 2015

Note: Past performance is no guarantee of future results. Results shown do not include transaction costs. Source: Company data, TEJ, Morgan Stanley Research.

Morgan Stanley Taiwan Limited+

Derrick Yang

Equity Analyst

Derrick.Yang@morganstanley.com

+886 2 2730-2862

Vivi Huang

Research Associate

Vivi.Huang@morganstanley.com

+886 2 2730-2860

Sharon Shih

Equity Analyst

Sharon.Shih@morganstanley.com

+886 2 2730-2865

Bizlink (3665.TW, 3665 TT)

Greater China Technology Hardware | Taiwan

| Stock Rating | Overweight |

|---|---|

| Industry View | In-Line |

| Price target | NT$3,665.00 |

| Up/downside to price target (%) | 67 |

| Shr price, close (Jun 5, 2026) | NT$2,200.00 |

| 52-Week Range | NT$3,010.00-605.02 |

| Sh out, dil, curr (mn) | 193 |

| Mkt cap, curr (mn) | NT$425,405 |

| EV, curr (mn) | NT$430,982 |

| Avg daily trading value (mn) | NT$5,633 |

| Fiscal Year Ending | 12/25 | 12/26e | 12/27e | 12/28e |

|---|---|---|---|---|

| EPS (NT$)** | 46.57 | 63.77 | 120.77 | 143.77 |

| EPS (NT$)§ | 47.71 | 67.27 | 109.42 | 144.28 |

| Revenue, net (NT$ mn) | 71,247 | 97,108 | 149,307 | 173,575 |

| EBITDA (NT$ mn) | 15,154 | 19,697 | 34,427 | 41,565 |

| ModelWare net inc (NT | 9,005 | 12,331 | 23,352 | 27,800 |

| $ mn) | ||||

| P/E | 32.6 | 34.5 | 18.2 | 15.3 |

| P/BV | 6.4 | 7.7 | 5.7 | 4.5 |

| RNOA (%) | 24.2 | 24.1 | 40.5 | 42.1 |

| ROE (%) | 24.9 | 26.4 | 41.6 | 36.8 |

| EV/EBITDA | 20.1 | 21.7 | 12.1 | 9.6 |

| Div yld (%) | 0.8 | 0.7 | 0.9 | 1.8 |

| FCF yld ratio (%)** | (0.8) | 1.6 | 3.2 | 5.7 |

| Leverage (EOP) (%) | (0.9) | (8.0) | (18.9) | (32.3) |

Unless otherwise noted, all metrics are based on Morgan Stanley ModelWare framework

§ = Consensus data is provided by Refinitiv Estimates

** = Based on consensus methodology

e = Morgan Stanley Research estimates

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260607_3665_貿聯_ms_bizlink_001.png |

51KB | 真資料圖 | 股價與月營收雙軸走勢圖,左軸(NT$)0-3300藍色股價折線、右軸(NT$mn)0-8000黃色月營收折線,X軸2015-2026 |

260607_3665_貿聯_ms_bizlink_003.png |

60KB | 真資料圖 | 評等/目標價沿革圖,藍色股價折線疊加紅色階梯狀目標價線(標示336.49/882.37/900/1200/1750/1900/2150/3665等數值),X軸2023/06-2026/06,上方標示O/I、NA/I等評等變動記號 |