PDF 原檔:260607_2360_致茂_ms_chroma_original.pdf

原始內容

M June 7, 2026 07:02 AM GMT

Chroma Ate Inc. | Asia Pacific

May Sales -6% MoM/+133% YoY

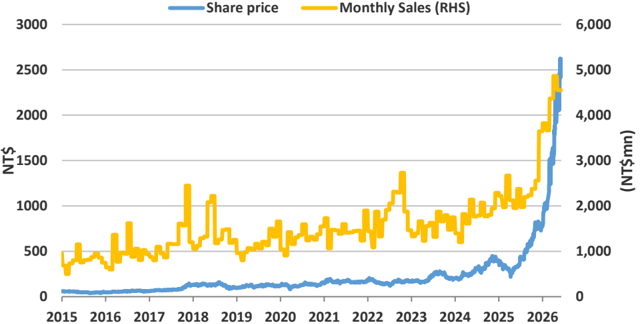

In this report, we focus on Chroma's monthly sales, which we believe could be a catalyst for share price movement.

Details:

- May revenue was NT$4,550mn (-6% MoM/+133% YoY).

- QTD revenue reached 75% of MSe at NT$12,575mn (+6% QoQ/+95% YoY) and 76% of consensus of NT$12,359mn (+4% QoQ/+91% YoY).

- Parent company revenue was NT$3,744mn (-5% QoQ/+135% YoY).

Our view:

- We see 2Q26 tracking ahead of market expectations.

- We expect Chroma to see strong revenue growth in 2026, driven the power testing (AI power product capacity expansions, emerging HVDC migration, and ESS upturn) and semi & photonics (new SLT capex cycle, metrology for advanced packaging and photonics testing for transceivers/CPO) businesses amid AI deployment.

- Moreover, FT handlers and burn-in ovens are under qualification, with revenue contribution expected in the coming years.

- Stay OW.

Exhibit 1 : Chroma's monthly sales vs. its share price since 2015

Source: Company data, TEJ, Morgan Stanley Research. Note: Past performance is no guarantee of future results. Results shown do not include transaction costs.

Morgan Stanley Taiwan Limited+

Update

| Derrick Yang Equity Analyst Derrick.Yang@morganstanley.com | +886 2 2730-2862 |

|---|---|

| Vivi Huang Research Associate Vivi.Huang@morganstanley.com | +886 2 2730-2860 |

| Sharon Shih Equity Analyst Sharon.Shih@morganstanley.com | +886 2 2730-2865 |

Chroma Ate Inc. (2360.TW, 2360 TT)

Greater China Technology Hardware | Taiwan

| Stock Rating | Overweight |

|---|---|

| Industry View | In-Line |

| Price target | NT$2,800.00 |

| Up/downside to price target (%) | 9 |

| Shr price, close (Jun 5, 2026) | NT$2,565.00 |

| 52-Week Range | NT$2,795.00-337.50 |

| Sh out, dil, curr (mn) | 425 |

| Mkt cap, curr (mn) | US$34,674 |

| EV, curr (mn) | US$34,329 |

| Avg daily trading value (mn) | US$123 |

| Fiscal Year Ending | 12/25 | 12/26e | 12/27e | 12/28e |

|---|---|---|---|---|

| EPS (NT$)** | 27.49 | 39.87 | 55.57 | 65.07 |

| Prior EPS (NT$)** | - | - | - | - |

| EPS (NT$)§ | 26.88 | 40.63 | 60.76 | 83.69 |

| Revenue, net (NT$ mn) | 28,311 | 50,215 | 66,629 | 77,450 |

| EBITDA (NT$ mn) | 10,038 | 21,153 | 28,956 | 33,826 |

| ModelWare net inc (NT | 11,692 | 16,957 | 23,631 | 27,669 |

| $ mn) | ||||

| P/E | 28.2 | 64.3 | 46.2 | 39.4 |

| P/BV | 10.1 | 26.1 | 20.1 | 16.5 |

| RNOA (%) | 49.4 | 75.0 | 87.8 | 91.4 |

| ROE (%) | 45.9 | 52.1 | 56.5 | 50.9 |

| EV/EBITDA | 31.8 | 50.8 | 36.8 | 31.2 |

| Div yld (%) | 1.2 | 0.8 | 1.1 | 1.5 |

| FCF yld ratio (%)** | 2.4 | 1.2 | 1.9 | 2.4 |

| Leverage (EOP) (%) | (33.4) | (37.6) | (45.8) | (52.2) |

Unless otherwise noted, all metrics are based on Morgan Stanley ModelWare framework

** = Based on consensus methodology

§ = Consensus data is provided by Refinitiv Estimates

e = Morgan Stanley Research estimates

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260607_2360_致茂_ms_chroma_001.png |

51KB | 真資料圖 | 雙軸折線圖,藍線為 Share price(左軸 NT$,0-3000),橙線為 Monthly Sales RHS(右軸 NT$mn,0-6000),橫軸年份 2015-2026 |

260607_2360_致茂_ms_chroma_003.png |

60KB | 真資料圖 | 股價(藍線)與目標價沿革(紅色虛線階梯,標示 O/I)對照圖,橫軸月份 2023/06 至 2026/06,各階梯標示目標價數值(225、320、350、300、285、320、360、470、455、400、515、490、880、825、1350、1530、2710、2800) |