報告_MS_愛普6531_20260512

PDF 原檔:報告_MS_愛普6531_20260512_original.pdf

原始內容

M May 12, 2026 04:57 PM GMT

AP Memory Technology Corp | Asia Pacific

1Q26 Beat; Multiple Drivers Ahead

| What’s Changed AP Memory Technology | From | To |

|---|---|---|

| Price Target | NT$1,000.00 | NT$1,555.00 |

We raise 2026/27/28 EPS by 9%/26%/39% and lift our PT to NT $1,555, implying 88x 2026e P/E, after a 1Q beat and a strong outlook across all business segments.

1Q26 earnings beat: 1Q26 revenue was NT970mn, GM was 46.2%, -3.7ppt Q/Q, -0.3ppt Y/Y, 1.6ppt below MSe; GM was impacted by the decreasing revenue mix of the VHM product line. 1Q26 operating profit was NT4.15, -12% Q/Q, +103% Y/Y, 19% above MSe.

Key takeaways : IoTRAM saw increasing demand across applications with relatively stable pricing vs standard memory. Multiple ApSRAM use cases have entered into mass production with more in the process of design-in, including wearable, display, and MCU. Management expects ApSRAM to contribute to revenue meaningfully in the next 1-2 years. S-SiCap business was driven mainly by IPC product, and accounted for 27% of the 1Q revenue. The new S-SiCap product, LSC (landside capacitor), is expected to enter into mass production in 2Q. IPC production will be affected in the near-term by PSMC capacity migration. Management also expects to see significant revenue contribution from VHM as use cases for edge AI and server are under development. Long-term, management expects 1:1:1 revenue contribution across IoTRAM, S-SiCap and VHM.

Remain OW: We revise up AP Memory’s PT to NT$1,555; we estimate its earnings will grow 60%+ in both 2027 and 2028, boosted by SiCap and WoW. We estimate 74% of revenue will come from these new opportunities in 2028.

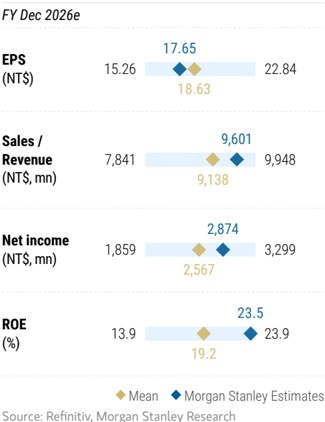

12/26e

17.65

16.16

18.63

9,601

3,037

2,874

59.8

23.5

51.9

Idea

| Morgan Stanley Taiwan Limited+ Daniel Yen, CFA Equity Analyst Daniel.Yen@morganstanley.com | +886 2 2730-2863 |

|---|---|

| Charlie Chan Equity Analyst Charlie.Chan@morganstanley.com Morgan Stanley Asia Limited+ | +886 2 2730-1725 |

| Daisy Dai, CFA Equity Analyst Daisy.Dai@morganstanley.com Morgan Stanley Taiwan Limited+ | +852 2848-7310 |

| Tiffany Yeh Equity Analyst Tiffany.Yeh@morganstanley.com Morgan Stanley Asia Limited+ Ethan Jia | +886 2 7712-3032 |

AP Memory Technology Corp (6531.TW, 6531 TT)

Greater China Technology Semiconductors | Taiwan

Stock Rating

Industry View

Price target

Up/downside to price target (%)

Shr price, close (May 12, 2026)

52-Week Range

Mkt cap, curr (mn)

Avg daily trading value (mn)

Fiscal Year Ending

12/25

EPS (NT$)**

Prior EPS (NT$)**

EPS (NT$)§

Revenue, net (NT$ mn)

EBITDA (NT$ mn)

ModelWare net inc (NT

$ mn)

P/E

ROE (%)

EV/EBITDA

Div yld (%)

7.74

7.63

6.30

5,658

1,474

1,258

57.9

10.6

41.3

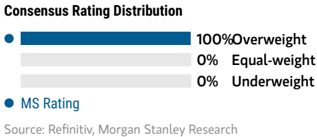

Overweight

Attractive

NT$1,555.00

47

NT$1,055.00

NT$1,055.00-244.50

NT$170,724

NT$1,839

12/27e

12/28e

34.34

27.19

27.22

17,829

6,491

5,591

30.7

39.2

24.0

60.74

43.68

41.05

30,478

11,733

9,888

17.4

55.2

13.0

1.2

1.1

0.0

0.0

Unless otherwise noted, all metrics are based on Morgan Stanley ModelWare framework

** = Based on consensus methodology

- § = Consensus data is provided by Refinitiv Estimates

e = Morgan Stanley Research estimates

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

+= Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to FINRA restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

M

AP Memory: Estimate Revisions Summary

We raise our 2026/27/28e EPS estimates by 9%/26%/39%: We factor in 1Q26 actual results. We also raise our shipment estimates for IoTRAM products as the company’s new ApSRAM product has entered mass production with continued design-in with new application, covering wearable, display, MCU, driving IoTRAM shipment growth. We also now estimate larger VHM shipments as the company expects VHM products to enter mass production in the following 2 years to drive significant revenue growth.

Exhibit 1: AP Memory - Estimate revisions

Source: Company data, Morgan Stanley Research (e) estimates

Exhibit 2: AP Memory - Quarterly financial summary

Source: Company data, Morgan Stanley Research (e) estimates

M

AP Memory: Valuation Methodology

We raise our price target to NT1,000 to factor in our earnings estimate changes. We also lift our intermediate growth rate from 14.3% to 16.0% as we factor in the larger growth rate driven by the progress of ApSRAM and VHM businesses.

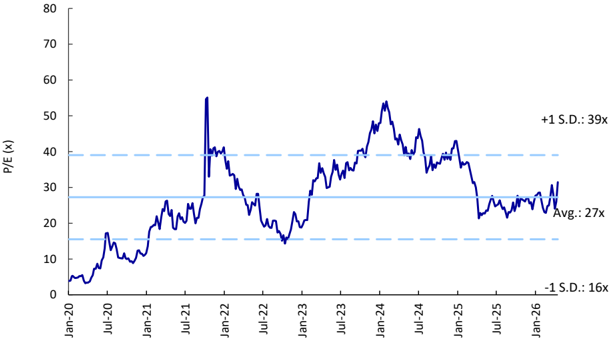

Aside from intermediate growth, our other residual income model assumptions are unchanged, including: 1) cost of equity unchanged at 9.2% (2.0% risk-free rate, 6% risk premium, 1.2 beta); 2) payout ratio of 67%; and 3) terminal growth rate of 3% to be more in line with the long-term macro growth rate. Our new PT implies 2026e P/E of 88x and 2027e P/E of 45x - more than 1 s.d. above the historical average since 2020. Our bull and bear case values rise to NT1,175) and NT400), respectively.

Exhibit 3: AP Memory: Residual Income model

Source: Company data, Morgan Stanley Research (e) estimates

Exhibit 4: AP Memory: Historical forward P/E

Source: Company data, Morgan Stanley Research

M

Source: Company data, Morgan Stanley Research estimates

M

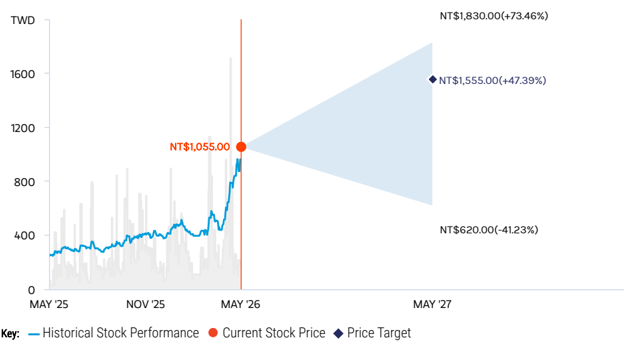

Risk Reward - AP Memory Technology Corp (6531.TW) Risk Reward - AP Memory Technology Corp (6531.TW)

1Q26 beat; multiple drivers ahead

NT$1,555.00 PRICE TARGET

Base case, derived from a residual income model. Key RI model assumptions include 1) cost of equity constant at 9.2% (2.0% risk-free rate, 6% risk premium, 1.2 beta); 2) payout ratio of 67%; 3) terminal growth rate of 3.0%; and 4) medium-term growth rate of 16.0%.

RISK REWARD CHART

Source: Refinitiv, Morgan Stanley Research

BULL CASE

104x 2026e EPS

Faster-than-expected AI and IPD business progress with PSRAM generating more cash

fl ow: We assume: 1) WoW packaging revenue to reach >NT10bn, and IPD revenue to reach <NT8bn by 2028; 2) total revenue to rise at a 55%+ CAGR, 2025-28; and 3) gross margin to increase from 46.5% in 2025 to 60%+ by 2028.

NT$1,830.00

BASE CASE

88x 2026e EPS

Fast-growing AI and IPD business, with PSRAM generating stable cash fl ows: We expect: 1) WoW revenue to reach NT10bn+ by 2028; 2) total revenue to rise at a 75% CAGR, 2025-28; and 3) gross margin to increase from 46.5% in 2025 to over 52% in 2028.

NT$1,555.00

OVERWEIGHT THESIS

- S-SiCap revenue is likely to ramp in 202627, and be further driven by new IPD interposer opportunities into 2028.

- Memory bandwidth and power consumption are the next issues to be resolved in AI computing, and we believe AP Memory’s wafer-on wafer (WoW) packaging technology could be an effective solution.

- The company expects memory business to be stable in the near term.

- Overall AI business should continue to rise in the mix - a positive read for the margin profile.

- Our PT implies 88x 2026e P/E and 45x 2027e P/E - more than 1 s.d. above the average level since 2020.

Risk Reward Themes

Secular Growth: Technology Diffusion:

Positive

Positive

View descriptions of Risk Rewards Themes

here

BEAR CASE

35x 2026e EPS

Slower-than-expected AI and IPD business progress, with PSRAM facing intensifying competition: We assume: 1) WoW packaging revenue of ~NT2bn by 2028; 2) total revenue to rise at a 10-15% CAGR, 2025-28; and 3) gross margin to remain at ~51% by 2028.

NT$620.00

M

Risk Reward - AP Memory Technology Corp (6531.TW)

KEY EARNINGS INPUTS

| Drivers | 2025 | 2026e | 2027e | 2028e |

|---|---|---|---|---|

| 1. Wifi Sales (%) (%) | 73.7 | 56.1 | 42 | 33 |

| 2. Ethernet Sales (%) (%) | 7.1 | 9.3 | 25.7 | 34 |

INVESTMENT DRIVERS

- Demand for AI applications

- Consumer tech demand, especially from the IoT market

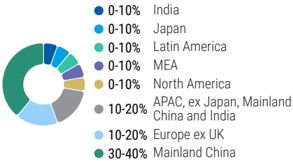

GLOBAL REVENUE EXPOSURE

Source: Morgan Stanley Research Estimate View explanation of regional hierarchies here

RISKS TO PT/RATING

RISKS TO UPSIDE

- Stronger-than-expected consumer demand

- Faster-than-expected IPD ramp and WoW packaging development

- Milder competition from partners (foundry, memory house, GPU vendor) or other design houses

RISKS TO DOWNSIDE

- Weaker-than-expected consumer demand

- Slower-than-expected IPD ramp and WoW packaging development

- Intensifying competition from partners (foundry, memory house, GPU vendor) or other design houses

OWNERSHIP POSITIONING

Inst. Owners, % Active

56.2%

Source: Refinitiv, Morgan Stanley Research

MS ESTIMATES VS. CONSENSUS

M

AP Memory: Financial Summary

Exhibit 6: Financial summary

M

Risk Reward Reference links

- View explanation of Options Probabilities methodology -

Options_Probabilities_Exhibit_Link.pdf

-

View descriptions of Risk Rewards Themes - RR_Themes_Exhibit_Link.pdf

-

View explanation of regional hierarchies - GEG_Exhibit_Link.pdf

-

View explanation of Theme/Exposure methodology -

- ESG_Sustainable_Solutions_External_Link.pdf

- View explanation of HERS methodology - ESG_HERS_External_Link.pdf

M

Disclosure Section

The information and opinions in Morgan Stanley Research were prepared or are disseminated by Morgan Stanley Asia Limited (which accepts the responsibility for its contents) and/or Morgan Stanley Asia (Singapore) Pte. (Registration number 199206298Z) and/or Morgan Stanley Asia (Singapore) Securities Pte Ltd (Registration number 200008434H), regulated by the Monetary Authority of Singapore (which accepts legal responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research), and/or Morgan Stanley Taiwan Limited and/or Morgan Stanley & Co International plc, Seoul Branch, and/or Morgan Stanley Australia Limited (A.B.N. 67 003 734 576, holder of Australian financial services license No. 233742, which accepts responsibility for its contents), and/or Morgan Stanley Wealth Management Australia Pty Ltd (A.B.N. 19 009 145 555, holder of Australian financial services license No. 240813, which accepts responsibility for its contents), and/or Morgan Stanley India Company Private Limited having Corporate Identification No (CIN) U22990MH1998PTC115305, regulated by the Securities and Exchange Board of India (‘SEBI’) and holder of licenses as a Research Analyst (SEBI Registration No. INH000001105); Stock Broker (SEBI Stock Broker Registration No. INZ000244438), Merchant Banker (SEBI Registration No. INM000011203), and depository participant with National Securities Depository Limited (SEBI Registration No. IN-DP-NSDL-567-2021) having registered office at Altimus, Level 39 & 40, Pandurang Budhkar Marg, Worli, Mumbai 400018, India; Telephone no. +91-22-61181000; Compliance Officer Details: Mr. Tejarshi Hardas, Tel. No.: +91-22-61181000 or Email: tejarshi.hardas@morganstanley.com; Grievance officer details: Mr. Tejarshi Hardas, Tel. No.: +91-22-61181000 or Email: msic-compliance@morganstanley.com which accepts the responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research, and their affiliates (collectively, “Morgan Stanley”). Morgan Stanley India Company Private Limited (MSICPL) may use AI tools in providing research services. All recommendations contained herein are made by the duly qualified research analysts.

For important disclosures, stock price charts and equity rating histories regarding companies that are the subject of this report, please see the Morgan Stanley Research Disclosure Website at www.morganstanley.com/eqr/disclosures/webapp/generalresearch, or contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY, 10036 USA.

For valuation methodology and risks associated with any recommendation, rating or price target referenced in this research report, please contact the Client Support Team as follows: US/Canada +1 800 303-2495; Hong Kong +852 2848-5999; Latin America +1 718 754-5444 (U.S.); London +44 (0)20-7425-8169; Singapore +65 6834-6860; Sydney +61 (0)2-9770-1505; Tokyo +81 (0)3-6836-9000. Alternatively you may contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY 10036 USA.