標題用字

原檔名誤植「文華」,正名為「文曄」(3036 WT Microelectronics)。lib 頁與 wikilink 一律使用

文曄。

報告_MS_大聯大3702文華3036_20260519

PDF 原檔:報告_MS_大聯大3702文華3036_20260519_original.pdf

原始內容

M May 19, 2026 04:27 PM GMT

Greater China Semiconductors | Asia Pacific

Semi Distributors: AI Continues to Drive a Stronger Outlook

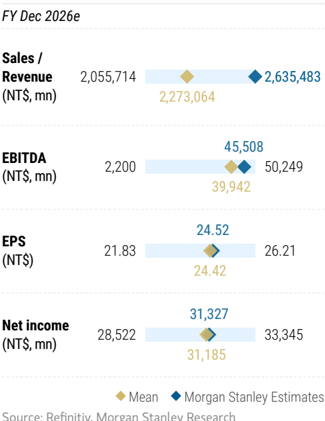

We raise our PT for WPG from after a strong 1Q beat and 2Q guidance. Raise PT for WT in light of a stronger outlook.

Key Takeaways

- WPG reported strong 1Q earnings with EPS 12% above MSe.

- WPG 2Q mid-point guidance implies 12% Q/Q revenue growth and 17% Q/Q EPS growth.

- WPG management remains positive on the secular AI-driven demand.

WPG reported strong 1Q earnings: WPG reported its 1Q results. The 1Q revenue was NT14.2bn, gross margin was 4.5%, +0.2ppt Q/Q and +0.8ppt Y/Y, 0.2ppt above our forecast. 1Q operating profit was NT3.17, +95% Q/Q and +192% Y/Y, 12% above our estimate. ROWC reached 15.2%, up from 11.5% in 4Q25. This follows the strong 1Q results of WT Micro: Scale drives operating leverage .

Strong 2Q guidance by WPG : The company guided for mid-point 2Q revenue of NT 3.86. The strong outlook is driven by continued global AI demand and capex guidance, and management expects continued strong demand from inference and edge AI.

Other highlights from WPG 1Q earnings : By application type, compute,

communication, consumer, industrial and auto accounted for 49%, 15%, 8%, 7% and 7%, respectively, which shows strong growth for compute and moderate growth for industrial and auto. By device type, memory and core component accounted for 45% and 23%, respectively. The reduction in the core component mix from 31% in 4Q25 represents the company’s drive to improve margins.

The AI story lifts earnings for both WT and WPG: Based on the actual 1Q results for WPG and strong guidance for 2Q forward, we raise our earnings estimates:

- WT - EPS up 12%, 17% and 16% for 2026-28, respectively;

- WPG - EPS up 32% for each 2026-28.

We raise price targets for WT from NT349 and for WPG from NT 160: We continue to use residual income valuation models; PT changes reflect our earnings estimate revisions.

Idea

Morgan Stanley Taiwan Limited+

Daniel Yen, CFA

Equity Analyst

+886 2 2730-2863

Charlie Chan

Equity Analyst

Charlie.Chan@morganstanley.com

+886 2 2730-1725

Morgan Stanley Asia Limited+

Daisy Dai, CFA

Equity Analyst

+852 2848-7310

Morgan Stanley Taiwan Limited+

Tiffany Yeh

Equity Analyst

+886 2 7712-3032

Morgan Stanley Asia Limited+

Ethan Jia

Research Associate

+852 3963-2287

Greater China Technology Semiconductors

Asia Pacific

Industry View

Attractive

What’s Changed

WT Microelectronics Co. Ltd.

(3036.TW)

From

To

Price Target

NT$299.00

NT$349.00

WPG Holdings (3702.TW) Price Target

From

To

NT$121.00

NT$160.00

Morgan Stanley does and seeks to do business with companies covered in Morgan Stanley Research. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of Morgan Stanley Research. Investors should consider Morgan Stanley Research as only a single factor in making their investment decision.

For analyst certification and other important disclosures, refer to the Disclosure Section, located at the end of this report.

+= Analysts employed by non-U.S. affiliates are not registered with FINRA, may not be associated persons of the member and may not be subject to FINRA restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account.

M

Reaction to earnings

Impact to our thesis

WPG Holdings

(3702.TW)

Strengthens our thesis

Financial results versus consensus

Modest upside

Source: Company data, Morgan Stanley Research

Direction of next 12-month consensus EPS

Modest revision higher

Idea

vI Mulo. Lammlys Lottate neviolullo cxmbll L. yudrtelly Tmlanlclal olatellelll

NT$ in million (YE Dec3!)

1Q25

Total Revenues

NT$ mn

Sequential Change

Net sales

Change us Year Alga

Cost of Sales

COGS

Gross Profit

Total Opex

R&D

Taxes

4Q27E

3Q27E

903,871

907,644

Old ‘27E

2.05

A43

24.000

3,190,724

1R.0

874,876

878,393

97%

3,089,720

97%

28,995

22k%

101,004

29,251

2222:

57,410

16,065

43,594

(5,014)

1Q28E

2Q28E

905,819

Diff.

912,276

10%

4.900

876,572

882.688

197%

29,246

12%

97%

29,587

2222

224%

15,782

17%

639

3Q25

4Q25

328,934

342,087

New ‘26E

4.00

25.80

2,635,483

306%

1Q26

2Q26E

494,273

636,710|

Old ‘26E

44.50

R2RE

2,432,079

14543

3Q26E

4Q26E

729,020

Diff.

775,480

14.56:

121 60%

8%

&4:

20.92

1Q27E

2Q27E

834,243

869,633

New ‘27E

26%

3,515,391

247,424

-FEZ

284.3

2Q25

259,503

4.20

6.50:

M

202

194

213

395

201

WT Micro: Estimate Revisions Summary

Percent oó Revenues

Operating Income

Percent of Revenues

Reported EPS

Total Non-operating Income(Loss)

Profit Before Taxes

Percent oó Revenues

Margins

Taxes

Tar Rate

13,105

2.00%

0.8%

9.944

2.002

21.83

(922)

s022

14%

5,660

1,722

1.50

5,991

1,25%

24.52

(862)

(843)

4,798

15%:

5,148

15%

(1,148)

11,957

1.82

20%

4,571

1852

(1,069)

3,501

14.2

1.82

4,660

180:

(710)

3,951

1.5:

Exhibit 1: WT Micro: Earnings Estimate Revisions

Percent oó Revenues

Ohange us Y’ear Ago

Pretax margin

Reported EPS (NT$. TV GAAP)

Oange us Y’ear Ago

242

10,388

143

10,881

12,816

1.22

13,186

1.2e

13,805

3Q28E

4Q28E

918,952

923,111

New ‘28E

3,660, 157

889.013

892,893

87%

1970%

3,541,167

29,939

118,990

30,218

.226%

62,949

227%

56,041

15,601

(5,294)

50,747

#8 s0a

3,676

3,692

Q4X

10,657

11,395

11,262

12%

40,068

14,224

2025

2026E

1,177,949

2,635,483

Old ‘28E

22.83

3,317,994

122.83

1,130,325

2,548,000

197%

3,212,067

47,624

87,483

4,04.3

105,927

2.22%

27%

57,064

841

26,742

43,165

2.26

16%

48,863

810

1,894

(5,294)

a.t:

6,538

43,568

9,149

10,920

19,393

30,351

16%

34,397

20,882

121

44,318

122

14,617

2027E

2028E

3,515,391

3,660,157

Diff.

10%

224.3

4.k3

3,402,122

3.541,167

9,7%

113,269

12%

970%

118,990

2222

63,252

182

15%

2.461

14,062

16%

226%

4.8

62,949

2,562

ati

14,641

Q43:

46,729

1.2

50,018

16%

45,746

122:

56,041

We raise EPS estimates 12%, 17% and 16% for 2026-28, respectively: We raise our expectations for the company’s data center business to reflect a stronger outlook.

nả ahã Nã

3.22%

1.42%

1.28%

3.17%

2,505

2ts

1.37%

1.21%

2,622

2130

0.1 ppt

0.1 ppt aỗ anà

0.1 ppt

2,791

213

1.53%

3.25%

1.39%

n° asl

3.19%

3,833

8,496

223:

215:

13,544

1.47%

1.31%

2,698

2t%

10,148

9,451

215:

0.1 ppt

35,549

10,657

0.1 ppt

0.1 ppt

31,327

205:

40,068

| 1.19% 1.64% 1.22% 1.63% 3.40 3.67 5.30 | 0.0 ppt | 1.01% 1.80% 0.96% 1.80% | 0.1 ppt | nế 3ã | 1.09% 1.72% 12 | 1.04% 1.72% 0.1 ppt 24.52 1043 28.10 31.69 |

|---|---|---|---|---|---|---|

| 0.0 ppt | 0.0 ppt | 0.0 ppt |

Net margin

Opex %

Source: Company data, Morgan Stanley Research estimates

Exhibit 2: Quarterly Financial Statement

Source: Company data, Morgan Stanley Research estimates

Hã anã

1.12:

12%

122

1.51%

143:

1.54%

0.0 ppt

1.20

4.23

841,624

28.009

2222

2RR:

15%

RỮ азі

CxmDIL 4.

NT$million

Total Equity

23

21

Net Profit

ROAE

Spread

PE (x)

vur o. neoluual muottle muuel vI. Mistoncal f/c

2026E

31,327

2027E

153,407

35,549

2028E

174,472

40,068

2029E

184,830

44,075

2030E

196,223

48,482

M

13

WT Micro: Valuation Methodology

Equity Value

No. of Shares

7

5

Projected Price (NT$)

3

2018

2019

2020

2022

Exhibit 3: WPG: Residual Income Model

Source: Morgan Stanley Research estimates

441,043

349

1,265

134,612

2031E

2033E

208,756

2032E

222,542

53,331

58,664

237,706

64,530

26.3% 27.2% 28.0%

28.0%

27,005

30,537

34,419

13.8%

14.6%

15.5%

2034E

254,387

70,983

28.8%

38,685

16.3%

2036E

292,920

85,889

30.4%

48,528

17.8%

2037E

315,123

94,478

31.1%

54,194

18.5%

Our updated price target is NT$349: We update our residual income model to reflect earnings estimate revisions. Our key RI assumptions are unchanged: cost of equity of 12.6% (2.0% risk-free rate, 11.8% risk premium, 0.9 beta), cash dividend payout ratio of 85%, intermediate growth rate of 10.0% and a long-term growth rate of 3.0%.

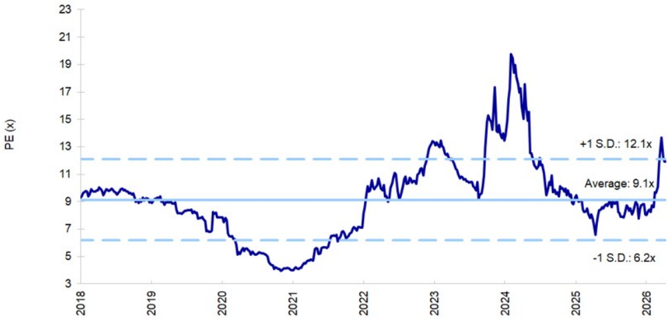

Exhibit 4: WT: Historical P/E

Source: Factset, company data, Morgan Stanley Research estimates

2035E

272,736

78,081

29.6%

43,374

17.1%

M

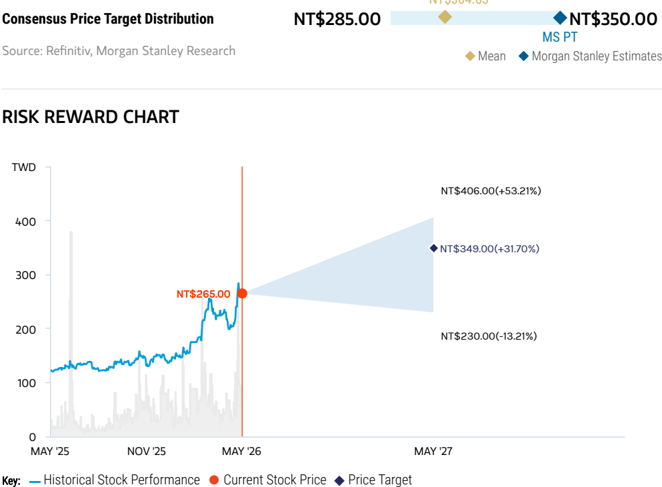

Risk Reward - WT Microelectronics Co. Ltd. (3036.TW) Risk Reward - WT Microelectronics Co. Ltd. (3036.TW)

Outgrowth from non-GPU components to drive distributors’ ongoing outperformance

NT$349.00 PRICE TARGET

Base case, residual income model. We assume a cost of equity of 12.6% (2% risk-free rate, 11.8% risk premium, 0.9 beta), a medium-term growth rate of 10% and a long-term growth rate of 3%.

NT$304.83

NT$349.00

14.2x 2026e EPS

BASE CASE

Strong AI ASIC growth in 2026: The AI semis industry continues to thrive in 2026 and 2027. WT Micro generates a revenue CAGR of 45%+ from 2025-28. Gross margin to be slightly diluted, to 3.3%+ in 2026, as a result of unfavorable product mix.

Source: Refinitiv, Morgan Stanley Research

BULL CASE

16.6x 2026e EPS

Stronger AI semi consumption with improved gross margin: The AI semis industry shows + 60% Y/Y growth in 2026. WT Micro generates a revenue CAGR of 60%+ from 2025-28. Gross margin remains at 4% despite growth in low-margin business. Opex is lighter, given productivity improvement. Market share and ROWC expand further. WT Micro enjoys cost savings and product line enhancement from more efficient use of capital.

NT$406.00

OVERWEIGHT THESIS

- We see continual value growth for semi distributors amid increasing supply chain complexity.

- WT Micro has expanded its business into the fast-growing AI industry, especially data center-related component distribution. We estimate that WT’s data center segment could contribute 64% of the company’s revenue in 2028.

- Our price target implies 14.2x our 2026 EPS estimate, above its 8.9x average oneyear forward P/E since 2018, which we find justified by improving demand and the company’s continued progress in penetrating the AI supply chain.

NT$230.00

9.4x 2026e EPS

BEAR CASE

Disappointing end demand, with share loss; ASIC business faces challenges: Revenue growth decelerates amid data center demand slowdown and share loss amid a weakening macro environment.

M

Risk Reward - WT Microelectronics Co. Ltd. (3036.TW)

KEY EARNINGS INPUTS

| Drivers | 2025 | 2026e | 2027e | 2028e |

|---|---|---|---|---|

| Gross margin rate (%) | 4.04 | 3.32 | 3.22 | 3.25 |

| Operating margin rate (%) | 1.8 | 1.7 | 1.4 | 1.5 |

INVESTMENT DRIVERS

- Growth in dividend payout

- Operating margin expansion

- Progress of ASIC business

- Continual expansion of market share

GLOBAL REVENUE EXPOSURE

Source: Morgan Stanley Research Estimate View explanation of regional hierarchies here

MS ALPHA MODELS

1/5

MOST

3 Month

Horizon

Source: Refinitiv, FactSet, Morgan Stanley Research; 1 is the highest favored Quintile and 5 is the least favored Quintile

RISKS TO PT/RATING

RISKS TO UPSIDE

- Margin trends up even amid low-margin AI business.

- Global semi inventory drops, reflecting strong mobile device demand.

- Market share expands.

RISKS TO DOWNSIDE

- Margin trends down dramatically amid slowerthan-expected AI-semi development.

- Global semi inventory rises, reflecting poor mobile/PC device demand.

- Market share lost.

OWNERSHIP POSITIONING

Inst. Owners, % Active

73.6%

Source: Refinitiv, Morgan Stanley Research

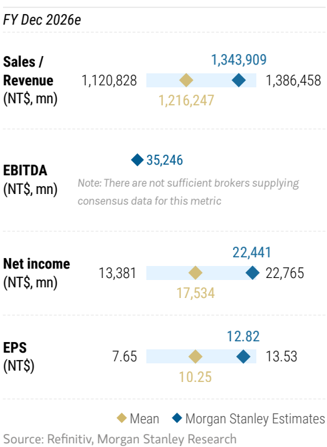

MS ESTIMATES VS. CONSENSUS

Cambio. vro. Lammys Cotale neviolullo

NTS in million (YE Dec3/)

Total Revenues

NTS mn

Sequential Change

Change us Year Ago

Net sales

COGS

Cost of Sales

Gross Profit

Total Opex

2Q25

250,452

2043

1Q25

248,834

2.4%

26.05

3Q25

244,467

-2.43€

•FRE

Old ‘26E

2Q26E

3Q26E

342,144

1,201,529

New ‘26E

4Q25

255.356|

4.50

1R.25

1026

1,343,909

4Q26E

330,264

Diff.

12%

2Q27E

3Q27E

New ‘27E

346,984

1,405,714

M

RED

Percent of Revenues

Taxes ace:

o

ads aces

WPG: Estimate Revisions Summary

Operating Income

Percent of Revenues

Reported EPS

Total Non-operating Income(Loss)

Profit Before Taxes

Percent of Revenues

Margins

Taxes

Gross margin

Tar Rate

Reported Income (TV GAAP)

Operating margin

Percent of Revenues

Change ys Year Ago

Pretax margin

Reported EPS (NT$. TV GAAP)

Net margin

Opex %

32%

12.51

9.50

Diff.

2Q28E

3Q28E

383,005

392,581

16%

16%

29%

30%

32%

32%

New ‘28E

4Q28E

2024

402,395

880,552

- 23

1,551,645

1,485,268

66,377

31,991

34,386

(5,105)

29,281

5,913

23,076

13.18

Old ‘28E

2025

2026E

999,110

1,343,909

- 555

1,337,407

1,280,271

57,136

30,768

26,368

(3,808)

22,560

4,738

17,531

10.01

Diff.

2027E

2028E

1,405,714

1,551,645

16%

4.603

1243:

16%

30%

30%

32%

32%

We raise 2026-28e EPS by 32% each: This factors in the 1Q26 revenue result and 2Q26 guidance. We expect the strong AI computing-driven growth to more than offset a weak non-AI outlook, driving 34.5% Y/Y revenue growth in 2026, and maintain that growth into 2028. We also expect AI supply chain to drive elevated gross margin levels, from 3.96% in 2025 to ~4.3% from 2026 to 2028. 0.2 ppt -0.2 ppt 1.49% 2.06% 1.31% 2.30% 0.2 ppt -0.2 ppt

9.68

4.28%

2.32%

1.82%

1.41%

12.82

5,430

2.10%

(1,521)

3,909

1.5%

878

4.35%

22%

2,843

2.55%

Lt:

2.13%

1.62

1.67%

4,906

1.90%

(1,795)

3,111

12%

833

27%

2.136

aste

1.25

20:

1.96%

1.80%

Change us Year Ago

5,350

2K0:

(1.311)

4,039

1736

781

3.178

1.2r

1.81

4,284

152%

(1,688)

2,596

100:

618

243:

1,898

1.08

403

Exhibit 6: WPG: Earnings Estimate Revisions

Source: Company data, Morgan Stanley Research estimates

Exhibit 7: Quarterly Financial Statement

Source: Company data, Morgan Stanley Research estimates

1Q27E

338,521

4Q27E

1Q28E

364,550

Old ‘27E

1,211,624

1,159,862

51,762

25,994

25,768

(4,336)

CAmole 7.

NT$million

Total Equity

22

Net Profit

ROAE

vur o. neoluual mootte mouel vr o. Tlolutival r/L

2026E

108,449

2028E

117,014

2029E

123,831

131,022

M

Spread

14.5%

11.0%

2030E

25,684

20.2%

13,203

10.7%

WPG: Valuation Methodology

12

PV of Continuing Value

Equity Value

No. of Shares

Projected Price (NTS)

8

6

Exhibit 8: WPG: Residual Income Model

Source: Morgan Stanley Research estimates

98,738

1,751

280,247

160

101,426

2027E

2031E

138,609

27,097

20.1%

13,895

10.6%

2032E

146,614

28,587

20.0%

14,625

10.6%

2034E

163,968

31,818

19.9%

16,208

10.5%

2035E

173,367

33,568

19.9%

17,065

10.4%

2036E

35,415

183,283

19.9%

17,970

10.4%

Our updated price target is NT$160: We update our residual income model to reflect earnings estimate revisions. Our key RI assumptions remain: cost of equity of 9.5% (1.5% risk-free rate, 6% risk premium, 1.34 beta), cash dividend payout ratio of 80%, mediumterm growth rate of 5.5% and long-term growth rate of 2.0%.

Exhibit 9: WPG: Historical P/E

Source: Factset, company data, Morgan Stanley Research estimates

2033E

155,059

30,160

20.0%

15,395

10.5%

M

Risk Reward - WPG Holdings (3702.TW) Risk Reward - WPG Holdings (3702.TW)

Outgrowth from non-GPU components to drive distributors’ ongoing outperformance

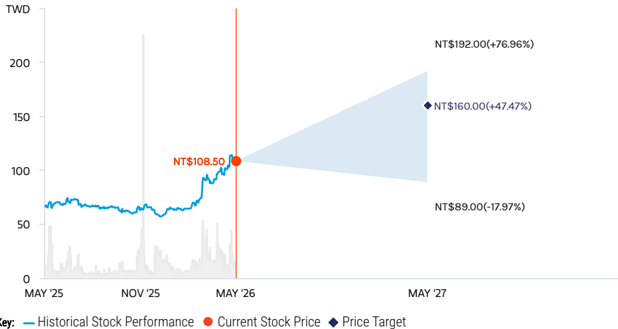

NT$160.00 PRICE TARGET

Base case, residual income model. We assume a cost of equity of 9.5% (1.5% risk-free rate, 6% risk premium, 1.34 beta), a medium-term growth rate of 5.5% and a long-term growth rate of 2.0%.

RISK REWARD CHART

Key:

Source: Refinitiv, Morgan Stanley Research

15.0x 2026e EPS

BULL CASE

NT$192.00

Stronger non - AI semi consumption with improved gross margin : The semis industry shows +40% Y/Y growth in 2026. WPG generates revenue growth of +40% Y/Y in 2026. Gross margin rises to 5%+ vs. 3.96% in 2025. Opex is lighter given productivity improvement. Market share and ROWC expand further. WPG enjoys cost savings and product line enhancement from more efficient use of capital.

OVERWEIGHT THESIS

- WPG still has high revenue exposure to consumer markets, which are likely to remain weak given high memory costs.

- However, the AI story is now strong enough to lift earnings for WPG.

- WPG has limited exposure to AI GPUs (most of which go through direct sales) and AI ASICs, but has good exposure to AI computing. 1Q26 revenue featured demand from CPU, networking, memory and PMIC.

- Our PT implies 12.5x 2026e EPS vs. 100%+ EPS growth in 2026

▪ ▪ ▪ ▪

Risk Reward Themes

Pricing Power:

Positive

Secular Growth:

Positive

View descriptions of Risk Rewards Themes here

BEAR CASE

6.9x 2026e EPS

Non - AI semi demand contracts in view of macro risk : The non-AI semis industry shows a 15% Y/Y decline in 2026. WPG’s revenue decreases -15% Y/Y in 2026. Gross margin is down to 3.0% vs. 3.96% in 2025. Opex increases. Market share is lost to competitors.

NT$89.00

BASE CASE

NT$160.00

12.5x 2026e EPS

AI lifts earnings in 2026: The non-AI semis industry remains sluggish in 2026. WPG generates revenue growth of 34.5% Y/Y in 2026. Gross margin rises to 4.35% in 2026 vs. 3.96% in 2025.

M

Risk Reward - WPG Holdings (3702.TW)

KEY EARNINGS INPUTS

| Drivers | 2025 | 2026e | 2027e | 2028e |

|---|---|---|---|---|

| Gross margin rate (%) | 3.96 | 4.35 | 4.28 | 4.28 |

| Operating margin rate (%) | 2.0 | 2.5 | 2.4 | 2.2 |

| Automotive revenue (NT$, mn) | 34,969 | 47,037 | 49,200 | 54,308 |

| Industrial revenue (NT$, mn) | 89,920 | 120,952 | 126,514 | 139,648 |

| IoT and other revenue (NT$, mn) | 109,902 | 147,830 | 154,629 | 170,681 |

INVESTMENT DRIVERS

- Growth in dividend payout

- Operating margin expansion

- Progress of non-3C business

- Continual non-operating investments

GLOBAL REVENUE EXPOSURE

Source: Morgan Stanley Research Estimate View explanation of regional hierarchies here

MS ALPHA MODELS

3 Month

Horizon

Source: Refinitiv, FactSet, Morgan Stanley Research; 1 is the highest favored Quintile and 5 is the least favored Quintile

RISKS TO PT/RATING

RISKS TO UPSIDE

- Margin trends up amid better-than-expected non-AI business.

- Global semi inventory drops, reflecting strong mobile device demand.

- Market share expands.

RISKS TO DOWNSIDE

- Margin trends down dramatically amid slowerthan-expected non-3C business development and pressure on client margins.

- Global semi inventory rises, reflecting poor mobile/PC device demand.

- Market share is lost.

OWNERSHIP POSITIONING

Inst. Owners, % Active

73.9%

Source: Refinitiv, Morgan Stanley Research

MS ESTIMATES VS. CONSENSUS

M

Risk Reward Reference links

- View explanation of Options Probabilities methodology -Options_Probabilities_Exhibit_Link.pdf

- View descriptions of Risk Rewards Themes - RR_Themes_Exhibit_Link.pdf

- View explanation of regional hierarchies - GEG_Exhibit_Link.pdf

- View explanation of Theme/Exposure methodology -ESG_Sustainable_Solutions_External_Link.pdf

- View explanation of HERS methodology - ESG_HERS_External_Link.pdf

M

Disclosure Section

The information and opinions in Morgan Stanley Research were prepared or are disseminated by Morgan Stanley Asia Limited (which accepts the responsibility for its contents) and/or Morgan Stanley Asia (Singapore) Pte. (Registration number 199206298Z) and/or Morgan Stanley Asia (Singapore) Securities Pte Ltd (Registration number 200008434H), regulated by the Monetary Authority of Singapore (which accepts legal responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research), and/or Morgan Stanley Taiwan Limited and/or Morgan Stanley & Co International plc, Seoul Branch, and/or Morgan Stanley Australia Limited (A.B.N. 67 003 734 576, holder of Australian financial services license No. 233742, which accepts responsibility for its contents), and/or Morgan Stanley Wealth Management Australia Pty Ltd (A.B.N. 19 009 145 555, holder of Australian financial services license No. 240813, which accepts responsibility for its contents), and/or Morgan Stanley India Company Private Limited having Corporate Identification No (CIN) U22990MH1998PTC115305, regulated by the Securities and Exchange Board of India (‘SEBI’) and holder of licenses as a Research Analyst (SEBI Registration No. INH000001105); Stock Broker (SEBI Stock Broker Registration No. INZ000244438), Merchant Banker (SEBI Registration No. INM000011203), and depository participant with National Securities Depository Limited (SEBI Registration No. IN-DP-NSDL-567-2021) having registered office at Altimus, Level 39 & 40, Pandurang Budhkar Marg, Worli, Mumbai 400018, India; Telephone no. +91-22-61181000; Compliance Officer Details: Mr. Tejarshi Hardas, Tel. No.: +91-22-61181000 or Email: tejarshi.hardas@morganstanley.com; Grievance officer details: Mr. Tejarshi Hardas, Tel. No.: +91-22-61181000 or Email: msic-compliance@morganstanley.com which accepts the responsibility for its contents and should be contacted with respect to any matters arising from, or in connection with, Morgan Stanley Research, and their affiliates (collectively, “Morgan Stanley”). Morgan Stanley India Company Private Limited (MSICPL) may use AI tools in providing research services. All recommendations contained herein are made by the duly qualified research analysts.

For important disclosures, stock price charts and equity rating histories regarding companies that are the subject of this report, please see the Morgan Stanley Research Disclosure Website at www.morganstanley.com/eqr/disclosures/webapp/generalresearch, or contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY, 10036 USA.

For valuation methodology and risks associated with any recommendation, rating or price target referenced in this research report, please contact the Client Support Team as follows: US/Canada +1 800 303-2495; Hong Kong +852 2848-5999; Latin America +1 718 754-5444 (U.S.); London +44 (0)20-7425-8169; Singapore +65 6834-6860; Sydney +61 (0)2-9770-1505; Tokyo +81 (0)3-6836-9000. Alternatively you may contact your investment representative or Morgan Stanley Research at 1585 Broadway, (Attention: Research Management), New York, NY 10036 USA.