報告_大和_川湖2059_20260507

PDF 原檔:報告_大和_川湖2059_20260507_original.pdf

原始內容

Taiwan

King Slide Works (2059 TT)

Target price:

TWD5,888.00 (from TWD3,880.00)

Share price (7 May):

TWD4,840.00

|

Up/downside:

+21.7%

Upgrading: 1Q26 review; riding a growing TAM

- Amazon ASIC ramp-up and TPU mix shift drive strong growth

- Leading market share position benefits from regular server demand

- Upgrading to Buy (1) rating; raising 12M TP to TWD5,888

What’s new: We review King Slide’s 1Q26 results after its earnings call.

What’s the impact: 1Q26 results beat expectations on FX gains. King Slide’s 1Q26 earnings came in at TWD3.5bn (EPS: TWD36.6), which was 10% and 18% higher than our and street expectations, respectively, due to higher-than-expected FX gains. While revenue was TWD5.5bn (up 10% QoQ and 38% YoY), largely on track with our expectations, the gross margin rose by 1.6pp QoQ due to the favourable FX trend (avg. USD/TWD FX rate was +2% in 1Q26 vs. +4% in 4Q25). However, the operating margin declined by 2.1pp to 67.1% due to a one-time freight expense of c.TWD200m. Lastly, net profit was boosted by higher-than-expected nonoperating gains of TWD697m (mainly FX gains of TWD476m).

Business outlook. As we highlighted in our first-take memo (link here), we expect King Slide’s market share loss with Nvidia to be fully priced in, while rising demand for regular servers and its dominant c.70% share in the AI server rail kit market position the company well to sustain positive revenue momentum. We believe King Slide’s April sales strength was driven by its role as the main rail kit supplier for Amazon’s new ASIC AI servers, a contribution we expect to become a key growth driver into 2026. On the ASIC front, we forecast revenue to grow 73% YoY in 2026, reflecting shipment volume increases and ASP expansion, with TPU potentially playing a meaningful role in the ASIC revenue mix by 2027 as the overall TAM continues to scale. For CPUs, expanding demand further benefits King Slide, given its commanding c.60% global share of the regular server market, which underpins our 78%/41% regular server revenue YoY growth estimates for 2026/27E, reflecting the strength we are seeing in the server supply chain. Beyond compute, Nvidia’s GTC showcase of comprehensive rack solutions, including switches and power, could generate an extra 300600k sets of rail kit demand by 2028E, representing an upside opportunity for King Slide. Taken together, these tailwinds across AI and regular server markets reinforce our positive outlook on King Slide.

What we recommend: We raise our 2026-27E EPS by 21-27% to factor in the 1Q26 results. Therefore, we raise our 12M TP to TWD5,888, based on a PER of 30x (high end of its past-3-year range of 10-32x; raised from 26x on a higher earnings growth trajectory), applied to our 4-quarter forward EPS forecast. Given the 2025-28E earnings CAGR of 30%, implying a PEG of 1.0, we think our valuation is not demanding and upgrade King Slide to Buy (1). Key downside risk: worse-than-expected demand for AI servers.

How we differ: Our 2026-27E EPS are 15-19% above consensus, likely as we are more positive on King Slide’s revenue.

7 May 2026

Daiwa

5

3

2

1

Buy

Sheng Cheng

(886) 2 8758 6253

sheng.cheng@daiwacm-cathay.com.tw

Allan Wang

(886) 2 8758 6249 allan.wang@daiwacm-cathay.com.tw

Forecast revisions (%)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue change | 16.1 | 25.6 | n.a. |

| Net profit change | 21.3 | 27 | n.a. |

| Core EPS (FD) change | 21.3 | 27 | n.a. |

Source: Daiwa forecasts

Share price performance

| 12-month range | 1,880.00-4,840.00 |

|---|---|

| Market cap (USDbn) | 14.66 |

| 3m avg daily turnover (USDm) | 87.22 |

| Shares outstanding (m) | 95 |

| Major shareholder | Ming Wei Global Co., Ltd. (6.7%) |

Financial summary (TWD)

| Year to 31 Dec | 26E | 27E | 28E |

|---|---|---|---|

| Revenue (m) | 27,589 | 33,514 | 38,185 |

| Operating profit (m) | 18,855 | 22,841 | 26,018 |

| Net profit (m) | 16,442 | 19,227 | 21,453 |

| Core EPS (fully-diluted) | 172.529 | 201.763 | 225.115 |

| EPS change (%) | 67.0 | 16.9 | 11.6 |

| Daiwa vs Cons. EPS (%) | 19.3 | 14.5 | (10.6) |

| PER (x) | 28.1 | 24.0 | 21.5 |

| Dividend yield (%) | 1.1 | 1.2 | 1.4 |

| DPS | 51.0 | 60.0 | 66.0 |

| PBR (x) | 11.6 | 8.7 | 6.8 |

| EV/EBITDA (x) | 22.0 | 17.6 | 14.9 |

| ROE (%) | 48.6 | 41.4 | 35.3 |

Source: FactSet, Daiwa forecasts

King Slide Works (2059 TT): 7 May 2026

King Slide: Daiwa revenue and earnings forecasts revisions vs. the consensus

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | Previous | New | Consensus | Previous | New | Consensus | Previous | New | Consensus |

| Revenue | 23,764 | 27,589 | 23,990 | 26,691 | 33,514 | 28,594 | n.a. | 38,185 | 41,802 |

| Diff (%) | 16.1% | 15.0% | 25.6% | 17.2% | n.a. | -8.7% | |||

| Gross Margin (%) | 75.1% | 76.1% | 76.2% | 74.9% | 75.1% | 75.7% | n.a. | 75.1% | 75.5% |

| Operating profit | 16,159 | 18,855 | 16,615 | 18,139 | 22,841 | 20,416 | n.a. | 26,018 | 27,436 |

| Op Margin (%) | 68.0% | 68.3% | 69.3% | 68.0% | 68.2% | 71.4% | n.a. | 68.1% | 65.6% |

| Net profit | 13,554 | 16,442 | 13,784 | 15,146 | 19,227 | 16,799 | n.a. | 21,453 | 23,991 |

| EPS (TWD) | 142.23 | 172.53 | 144.65 | 158.93 | 201.76 | 176.29 | n.a. | 225.11 | 251.75 |

| Diff (%) | 21.3% | 19.3% | 27.0% | 14.5% | n.a. | -10.6% |

Source: Bloomberg, Daiwa forecasts

King Slide: quarterly and annual P&L statement

| 2026E | 2026E | 2026E | 2026E | 2027E | 2025 | 2026E | 2027E | 2028E | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (TWDm) | 1Q | 2QE | 3QE | 4QE | 1QE | 2QE | 3QE | 4QE | ||||

| Net revenue | 5,450 | 7,195 | 7,122 | 7,822 | 7,775 | 8,578 | 8,463 | 8,698 | 17,501 | 27,589 | 33,514 | 38,185 |

| COGS | -1,213 | -1,747 | -1,729 | -1,906 | -1,908 | -2,123 | -2,096 | -2,209 | -4,192 | -6,594 | -8,336 | -9,495 |

| Gross profit | 4,237 | 5,449 | 5,393 | 5,916 | 5,868 | 6,455 | 6,367 | 6,488 | 13,309 | 20,994 | 25,178 | 28,690 |

| Operating expenses | -582 | -504 | -506 | -548 | -544 | -596 | -588 | -609 | -1,220 | -2,139 | -2,337 | -2,672 |

| Operating profit | 3,654 | 4,945 | 4,887 | 5,368 | 5,323 | 5,859 | 5,779 | 5,879 | 12,089 | 18,855 | 22,841 | 26,018 |

| Non-operating profit | 697 | 195 | 398 | 399 | 396 | 398 | 198 | 198 | 343 | 1,689 | 1,191 | 795 |

| Pre-tax profit | 4,352 | 5,139 | 5,286 | 5,768 | 5,720 | 6,257 | 5,977 | 6,078 | 12,423 | 20,545 | 24,031 | 26,813 |

| Income taxes | -866 | -1,027 | -1,057 | -1,153 | -1,143 | -1,251 | -1,195 | -1,215 | -2,586 | -4,103 | -4,804 | -5,360 |

| Net profit | 3,486 | 4,112 | 4,229 | 4,615 | 4,576 | 5,006 | 4,782 | 4,863 | 9,837 | 16,442 | 19,227 | 21,453 |

| Net EPS (TWD) | 36.58 | 43.15 | 44.38 | 48.42 | 48.02 | 52.53 | 50.18 | 51.03 | 103.23 | 172.53 | 201.76 | 225.11 |

| Operating Ratios | ||||||||||||

| Gross margin | 77.7% | 75.7% | 75.7% | 75.6% | 75.5% | 75.3% | 75.2% | 74.6% | 76.0% | 76.1% | 75.1% | 75.1% |

| Operating margin | 67.1% | 68.7% | 68.6% | 68.6% | 68.5% | 68.3% | 68.3% | 67.6% | 69.1% | 68.3% | 68.2% | 68.1% |

| Pre-tax margin | 79.9% | 71.4% | 74.2% | 73.7% | 73.6% | 72.9% | 70.6% | 69.9% | 71.0% | 74.5% | 71.7% | 70.2% |

| Net margin | 64.0% | 57.1% | 59.4% | 59.0% | 58.9% | 58.4% | 56.5% | 55.9% | 56.2% | 59.6% | 57.4% | 56.2% |

| YoY (%) | ||||||||||||

| Net revenue | 38% | 70% | 63% | 58% | 43% | 19% | 19% | 11% | 73% | 58% | 21% | 14% |

| Gross profit | 41% | 66% | 66% | 57% | 38% | 18% | 18% | 10% | 90% | 58% | 20% | 14% |

| Operating profit | 34% | 67% | 64% | 57% | 46% | 18% | 18% | 10% | 98% | 56% | 21% | 14% |

| Pre-tax profit | 39% | 472% | 32% | 31% | 31% | 22% | 13% | 5% | 59% | 65% | 17% | 12% |

| Net profit | 39% | 570% | 32% | 31% | 31% | 22% | 13% | 5% | 60% | 67% | 17% | 12% |

| QoQ (%) | ||||||||||||

| Net revenue | 10% | 32% | -1% | 10% | -1% | 10% | -1% | 3% | ||||

| Gross profit | 12% | 29% | -1% | 10% | -1% | 10% | -1% | 2% | ||||

| Operating profit | 7% | 35% | -1% | 10% | -1% | 10% | -1% | 2% | ||||

| Pre-tax profit | -1% | 18% | 3% | 9% | -1% | 9% | -4% | 2% | ||||

| Net profit | -1% | 18% | 3% | 9% | -1% | 9% | -4% | 2% |

Source: Company, Daiwa forecasts

King Slide: 1Q26 comparison table

| (TWDm) | Actual | QoQ% | YoY% | Daiwa | Diff% | Consensus | Diff% |

|---|---|---|---|---|---|---|---|

| Revenue | 5,450 | 10% | 38% | 5,495 | -1% | 5,114 | 7% |

| Gross profit | 4,237 | 12% | 41% | 4,156 | 2% | 3,874 | 9% |

| Gross margin (%) | 77.7% | 75.6% | 75.8% | ||||

| Operating profit | 3,654 | 7% | 34% | 4,048 | -10% | 3,520 | 4% |

| Operating margin (%) | 67.1% | 68.4% | 68.8% | ||||

| Pre-tax profit | 4,352 | -1% | 39% | 3,951 | 10% | 4,742 | -8% |

| Net profit | 3,486 | -1% | 39% | 3,161 | 10% | 2,945 | 18% |

| EPS (TWD) | 36.58 | -1% | 39% | 33.17 | 10% | 30.91 | 18% |

Source: Company data, Daiwa forecasts, Bloomberg

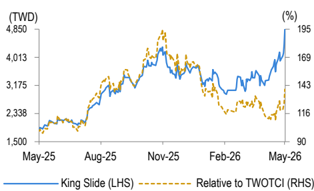

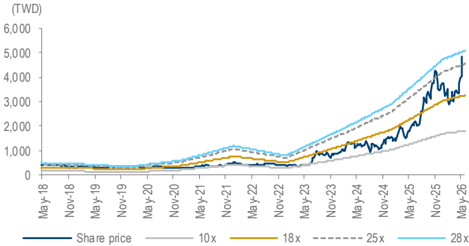

King Slide: 1-year forward PER bands

Source: TEJ, Daiwa forecasts

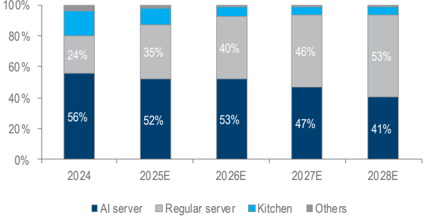

King Slide: revenue breakdown

Source: Company, Daiwa forecasts

Daiwa

Financial summary

Key assumptions

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Server railkit shipment (k) | 3,938.0 | 4,477.0 | 3,556.9 | 2,711.9 | 6,021.2 | 10,264.3 | 14,291.6 | 17,836.8 |

| HGX railkit shipment (k) | 0.0 | 0.0 | 90.0 | 360.0 | 270.0 | 248.5 | 180.0 | 85.0 |

| NVL railkit shipment (k) | 0.0 | 0.0 | 0.0 | 0.0 | 636.7 | 1,392.2 | 1,560.8 | 1,522.5 |

Profit and loss (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Regular server railkit sales | 4,489 | 5,081 | 2,678 | 2,451 | 6,126 | 10,934 | 15,435 | 20,334 |

| AI server railkit sales | 0 | 0 | 982 | 5,668 | 9,122 | 14,542 | 15,785 | 15,470 |

| Other Revenue | 1,853 | 2,717 | 2,103 | 2,011 | 2,252 | 2,112 | 2,294 | 2,381 |

| Total Revenue | 6,342 | 7,799 | 5,763 | 10,129 | 17,501 | 27,589 | 33,514 | 38,185 |

| Other income | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| COGS | (2,987) | (3,333) | (2,231) | (3,128) | (4,192) | (6,594) | (8,336) | (9,495) |

| SG&A | (386) | (474) | (408) | (550) | (743) | (1,332) | (1,332) | (1,527) |

| Other op.expenses | (250) | (239) | (235) | (351) | (477) | (807) | (1,005) | (1,146) |

| Operating profit | 2,720 | 3,753 | 2,888 | 6,101 | 12,089 | 18,855 | 22,841 | 26,018 |

| Net-interest inc./(exp.) | 10 | 159 | 495 | 653 | 692 | 711 | 716 | 716 |

| Assoc/forex/extraord./others | (134) | 1,162 | 43 | 1,035 | (350) | 978 | 475 | 78 |

| Pre-tax profit | 2,596 | 5,073 | 3,426 | 7,789 | 12,431 | 20,545 | 24,031 | 26,813 |

| Tax | (523) | (1,017) | (721) | (1,633) | (2,586) | (4,103) | (4,804) | (5,360) |

| Min. int./pref. div./others | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Net profit (reported) | 2,073 | 4,056 | 2,704 | 6,156 | 9,845 | 16,442 | 19,227 | 21,453 |

| Net profit (adjusted) | 2,073 | 4,056 | 2,704 | 6,156 | 9,845 | 16,442 | 19,227 | 21,453 |

| EPS (reported)(TWD) | 21.748 | 42.563 | 28.378 | 64.594 | 103.309 | 172.529 | 201.763 | 225.115 |

| EPS (adjusted)(TWD) | 21.748 | 42.563 | 28.378 | 64.594 | 103.309 | 172.529 | 201.763 | 225.115 |

| EPS (adjusted fully-diluted)(TWD) | 21.748 | 42.563 | 28.378 | 64.594 | 103.309 | 172.529 | 201.763 | 225.115 |

| DPS (TWD) | 6.120 | 10.880 | 20.000 | 14.190 | 32.200 | 51.000 | 60.000 | 66.000 |

| EBIT | 2,720 | 3,753 | 2,888 | 6,101 | 12,089 | 18,855 | 22,841 | 26,018 |

| EBITDA | 2,934 | 3,977 | 3,157 | 6,429 | 12,552 | 19,459 | 23,665 | 27,030 |

Cash flow (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Profit before tax | 2,596 | 5,073 | 3,426 | 7,789 | 12,431 | 20,545 | 24,031 | 26,813 |

| Depreciation and amortisation | 214 | 224 | 269 | 328 | 464 | 604 | 824 | 1,012 |

| Tax paid | (523) | (1,017) | (721) | (1,633) | (2,586) | (4,103) | (4,804) | (5,360) |

| Change in working capital | (997) | (209) | 52 | (1,598) | 2,097 | (1,079) | (649) | (502) |

| Other operational CF items | 228 | (133) | 252 | 301 | 0 | 0 | 0 | (0) |

| Cash flow from operations | 1,518 | 3,938 | 3,278 | 5,187 | 12,405 | 15,966 | 19,403 | 21,963 |

| Capex | (768) | (824) | (375) | (354) | (1,750) | (2,759) | (2,346) | (2,673) |

| Net (acquisitions)/disposals | (1,495) | 389 | 215 | 884 | 0 | 0 | 0 | 0 |

| Other investing CF items | 1 | (1) | (0) | (0) | 0 | 0 | 0 | 0 |

| Cash flow from investing | (2,261) | (436) | (161) | 530 | (1,750) | (2,759) | (2,346) | (2,673) |

| Change in debt | 257 | 448 | (32) | (130) | 0 | 0 | 0 | 0 |

| Net share issues/(repurchases) | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Dividends paid | (583) | (1,037) | (1,906) | (1,352) | (3,069) | (4,860) | (5,718) | (6,290) |

| Other financing CF items | (33) | (35) | (28) | (26) | 0 | 0 | 0 | 0 |

| Cash flow from financing | (359) | (624) | (1,966) | (1,508) | (3,069) | (4,860) | (5,718) | (6,290) |

| Forex effect/others | (22) | 788 | (141) | 676 | 0 | 0 | 0 | 0 |

| Change in cash | (1,124) | 3,666 | 1,010 | 4,886 | 7,587 | 8,347 | 11,339 | 13,000 |

| Free cash flow | 751 | 3,114 | 2,903 | 4,833 | 10,655 | 13,207 | 17,057 | 19,290 |

Source: FactSet, Daiwa forecasts

King Slide Works (2059 TT): 7 May 2026

Daiwa

Financial summary continued …

Balance sheet (TWDm)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Cash & short-term investment | 9,421 | 12,698 | 13,494 | 17,495 | 25,074 | 33,421 | 44,759 | 57,760 |

| Inventory | 926 | 920 | 1,012 | 1,231 | 919 | 1,445 | 1,827 | 2,081 |

| Accounts receivable | 1,774 | 1,866 | 1,656 | 3,180 | 1,678 | 2,645 | 3,214 | 3,662 |

| Other current assets | 31 | 36 | 40 | 43 | 43 | 43 | 43 | 43 |

| Total current assets | 12,151 | 15,520 | 16,202 | 21,949 | 27,713 | 37,554 | 49,843 | 63,545 |

| Fixed assets | 2,446 | 2,955 | 3,192 | 3,287 | 4,574 | 6,729 | 8,251 | 9,911 |

| Goodwill & intangibles | 3 | 2 | 3 | 2 | 2 | 2 | 2 | 2 |

| Other non-current assets | 832 | 759 | 1,184 | 1,234 | 1,234 | 1,234 | 1,234 | 1,234 |

| Total assets | 15,433 | 19,236 | 20,581 | 26,472 | 33,523 | 45,519 | 59,330 | 74,693 |

| Short-term debt | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Accounts payable | 469 | 374 | 309 | 441 | 724 | 1,138 | 1,439 | 1,639 |

| Other current liabilities | 1,211 | 1,599 | 1,866 | 2,708 | 2,708 | 2,708 | 2,708 | 2,708 |

| Total current liabilities | 1,680 | 1,973 | 2,174 | 3,149 | 3,432 | 3,846 | 4,147 | 4,347 |

| Long-term debt | 452 | 895 | 741 | 615 | 615 | 615 | 615 | 615 |

| Other non-current liabilities | 698 | 730 | 1,229 | 1,416 | 1,416 | 1,416 | 1,416 | 1,416 |

| Total liabilities | 2,830 | 3,598 | 4,145 | 5,180 | 5,462 | 5,877 | 6,178 | 6,378 |

| Share capital | 953 | 953 | 953 | 953 | 953 | 953 | 953 | 953 |

| Reserves/R.E./others | 11,650 | 14,685 | 15,483 | 20,339 | 27,108 | 38,689 | 52,199 | 67,362 |

| Shareholders’ equity | 12,603 | 15,638 | 16,436 | 21,292 | 28,061 | 39,642 | 53,152 | 68,315 |

| Minority interests | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Total equity & liabilities | 15,433 | 19,236 | 20,581 | 26,472 | 33,523 | 45,519 | 59,330 | 74,693 |

| EV | 452,269 | 449,434 | 448,485 | 444,358 | 436,779 | 428,432 | 417,093 | 404,093 |

| Net debt/(cash) | (8,969) | (11,804) | (12,753) | (16,880) | (24,459) | (32,806) | (44,145) | (57,145) |

| BVPS (TWD) | 132.253 | 164.101 | 172.473 | 223.431 | 294.457 | 415.986 | 557.749 | 716.864 |

Key ratios (%)

| Year to 31 Dec | 2021 | 2022 | 2023 | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|

| Sales (YoY) | 32.1 | 23.0 | (26.1) | 75.8 | 72.8 | 57.6 | 21.5 | 13.9 |

| EBITDA (YoY) | 36.0 | 35.5 | (20.6) | 103.6 | 95.3 | 55.0 | 21.6 | 14.2 |

| Operating profit (YoY) | 38.6 | 38.0 | (23.0) | 111.2 | 98.2 | 56.0 | 21.1 | 13.9 |

| Net profit (YoY) | 78.0 | 95.7 | (33.3) | 127.6 | 59.9 | 67.0 | 16.9 | 11.6 |

| Core EPS (fully-diluted) (YoY) | 78.0 | 95.7 | (33.3) | 127.6 | 59.9 | 67.0 | 16.9 | 11.6 |

| Gross-profit margin | 52.9 | 57.3 | 61.3 | 69.1 | 76.0 | 76.1 | 75.1 | 75.1 |

| EBITDA margin | 46.3 | 51.0 | 54.8 | 63.5 | 71.7 | 70.5 | 70.6 | 70.8 |

| Operating-profit margin | 42.9 | 48.1 | 50.1 | 60.2 | 69.1 | 68.3 | 68.2 | 68.1 |

| Net profit margin | 32.7 | 52.0 | 46.9 | 60.8 | 56.3 | 59.6 | 57.4 | 56.2 |

| ROAE | 17.5 | 28.7 | 16.9 | 32.6 | 39.9 | 48.6 | 41.4 | 35.3 |

| ROAA | 14.4 | 23.4 | 13.6 | 26.2 | 32.8 | 41.6 | 36.7 | 32.0 |

| ROCE | 22.3 | 25.4 | 17.1 | 31.2 | 47.8 | 54.7 | 48.6 | 42.4 |

| ROIC | 73.5 | 80.3 | 60.7 | n.a | n.a | n.a | n.a | n.a |

| Net debt to equity | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Effective tax rate | 20.2 | 20.0 | 21.1 | 21.0 | 20.8 | 20.0 | 20.0 | 20.0 |

| Accounts receivable (days) | 83.0 | 85.2 | 111.6 | 87.1 | 50.7 | 28.6 | 31.9 | 32.9 |

| Current ratio (x) | 7.2 | 7.9 | 7.5 | 7.0 | 8.1 | 9.8 | 12.0 | 14.6 |

| Net interest cover (x) | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. | n.a. |

| Net dividend payout | 50.1 | 50.0 | 47.0 | 50.0 | 49.9 | 49.4 | 34.8 | 32.7 |

| Free cash flow yield | 0.2 | 0.7 | 0.6 | 1.0 | 2.3 | 2.9 | 3.7 | 4.2 |

Source: FactSet, Daiwa forecasts

Company profile

Founded in 1986, King Slide Works started as a rail kit manufacturer. Leveraging its years of mechanism design experience, the company soon started manufacturing server rail kit in 2000. With 40 years of development, King Slide’s product portfolio now comprises server rail kit, kitchen rail kit and hinge. The company is headquartered in Kaohsiung city with two production sites including King Slide Works Co., LTD (ball bearing slide and hinge) and King Slide Technology Co., LTD (server rail kit and functional kitchen rail kit). King Slide also owns sales offices in the US and China. It was listed on the Taiwan Stock Exchange in 2008.

King Slide Works (2059 TT): 7 May 2026

Daiwa

ESG analysis

ESG risks

| Risks | Management | Analyst comments | |

|---|---|---|---|

| G | Executive/board quality | 2 | King Slide’s board consists of 7 directors, including 4 independent directors. The total number of directors is lower than that of other listed companies in our coverage. King Slide held 6 board meetings in 2024; the actual attendee rate was 100%. Most of the board members are King Slide’s founder’s family members, which we believe presents downside risks to independent governance. However, the independent directors have diversified backgrounds with expertise in accounting and management, a positive for the board’s quality. |

| Capital management | 2 | King Slide declared a DPS of TWD32.2 in 2024, representing a payout ratio of 50%. The payout ratio was in line with the level of 46-53% during 2012-22. As a rail kit manufacturer, King Slide is set to deliver solid revenue growth and FCF over our forecast horizon amidst strong ASP increase in the AI server market. | |

| Related party & transaction | 1 | The company did not report any related-party transactions in 2024. We see limited risks from related party transactions. | |

| S | Product design & lifecycle management | 2 | King Slide applies life cycle thinking and the 3R principle (Reduce/Reuse/Recycle) across its product design to minimise environmental impact. Its green designs focus on controlling environmentally sensitive substances, using non toxic materials, and enabling easy assembly/disassembly to extend product lifespans. The company continues to advance its green product program. Based on 2024 shipments, carbon reductions amounted to 68,067 metric tons of CO2e versus 2023, underscoring progress in lowering the environmental footprint of its products. |

| S | GHG emissions | 2 | King Slide is cutting greenhouse-gas emissions through targeted energy-efficient upgrades and process improvements. Across its Works and Technology sites, the company is replacing older motors and lighting with more efficient alternatives, introducing a formal GHG-reducing inventory, and refining equipment controls to eliminate unnecessary idling. These practical measures reduce electricity use, improve operational efficiency and lower the company’s carbon footprint in a cost-effective, scalable way. |

Note: Management score represents a company’s ability to manage/benefit from certain ESG topics. The scores range from 1 to 3, with 1 being the strongest.

Update Date: 3 Feb 2026

Source: Daiwa, Company

King Slide Works (2059 TT): 7 May 2026

Daiwa