PDF 原檔:6488_20260630_Nomura_original.pdf

圖片清單(已驗證 2026-06-30)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

| 6488_20260630_Nomura_001.png | 36KB | 裝飾·logo·banner | 股價相對表現縮圖,無座標標示 |

| 6488_20260630_Nomura_002.png | 81KB | 真資料圖 | Fig.1 nVidia Feynman GPU 樓層圖與剖面圖:Feynman(A16?) die 兩兩堆疊、左右側 HBM4E 與 I/O;剖面標 Carrier silicon→SiC(?)、GPU die(A16?) hybrid bond、reconstituted interposer(6-7x ret.)、microbump、LSI |

| 6488_20260630_Nomura_003.png | 42KB | 真資料圖 | Fig.5 GWC P/E band 歷史走勢圖 |

| 6488_20260630_Nomura_004.png | 52KB | 真資料圖 | Fig.6 GWC P/B vs ROE 歷史走勢圖 |

| 6488_20260630_Nomura_005.png | 110KB | 真資料圖 | 三年評等與目標價歷史圖:股價走勢 + 表列 21-May-26 Buy TP850、05-Nov-24 Neutral TP480、24-Jul-23 Buy TP600,收盤 936(26-Jun-26) |

原始內容

Relative performance chart

EQUITY: TECHNOLOGY

Price

(TWD)

10001

7501

5001

150

-125

-100

GlobalWafers 6488.TWO 6488 TT

EQUITY: TECHNOLOGY

Churra. I CEC Namura

Refreshed semi wafer cycle and material

Continued improvement in semi wafer supply/demand dynamics; new SiC opportunity in sight

Action: maintain Buy and raise TP to TWD1,200, implying 28% upside

In our Anchor Report of May 2026, 'Greater China Semi - A guide to Semi renaissance in 2026-30F,' we highlighted a variety of emerging semiconductor technologies for 2027F, such as wafer-bonded NAND, backside power deliver (BPD), and photonics SOI demand, and noted that improving semiconductor wafer supply/demand dynamics had us believe that some related supply-chain names including Globalwafers (GWC) could be among the key beneficiaries of such technologies. We see potential upside for GWC's fundamentals in the near and long term, including: (1) continued improvement in the semiconductor wafer cycle and pricing environment; and (2) SiC possibly acting as an emerging new material in advanced packaging toward 2028F. We thus raise our TP for GWC to TWD1,200 (from TWD850), based on 4.8x 2028F BVPS of TWD252 (previously 3.2x 2028F BVPS). We raise our 2026-28F earnings by 11-41%. The stock is trading at 3.7x 2028F BVPS of TWD252.

Semi wafer supply/demand: rising demand with continuously improving spot price

In our previously published reports (link 1 , link 2 ), we had indicated some bottom-up checks, including: (1) a spot price recovery of around 5-10% h-h in 1H26F, and another 10% h-h recovery in 2H26F; and (2) the leading semi wafer companies potentially running at tight utilization rates for 12″ semi wafers. We now expect the magnitude of spot price hikes in 2H26F to surpass our previous estimates as now both memory companies and logic foundries are procuring increasingly more semi wafers (vs previously procurement was mainly driven by memory companies). With customers procuring higher volumes than previously committed, we expect companies such as GWC to hike prices. As the spot price was 20% lower than the LTA price during 2023-25, after the spot price hike in 2026F, we expect some semi wafers' spot prices to be on par with the LTA price by end-2026F.

SiC for advanced packaging may start with chip-level thermal plate in Feynman

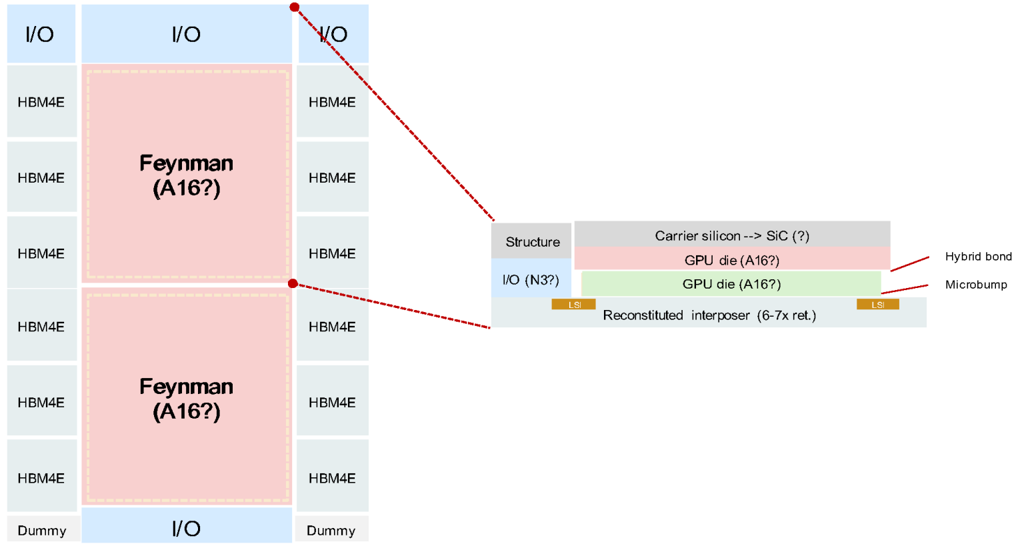

We expect nVidia's (NVDA US, Not rated) next-gen GPU (Feynman) to target the GPU-onGPU SoIC stack which would lead to higher computational power even with limited growth interposer reticle size. Given rising heat dissipation requirements, Feynman could start adopting SiC thermal plates which function as an integrated silicon carrier (fill up the height gap in between GPU and HBM) and thermal interface material (TIM); Fig. 1 . We believe this will contribute around 5-10% to GWC's total revenue from 2028F at the earliest (Fig. 2 ).

| Year-end 31 Dec Currency (TWD) | FY25 Actual | Old | FY26F New | Old | FY27F New | Old | FY28F New |

|---|---|---|---|---|---|---|---|

| Revenue (mn) | 60,598 | 61,159 | 61,726 | 71,372 | 73,535 | 83,460 | 88,666 |

| Reported net profit (mn) | 7,311 | 8,248 | 11,633 | 10,825 | 12,082 | 15,322 | 19,163 |

| Normalised net profit (mn) | 7,311 | 8,248 | 11,633 | 10,825 | 12,082 | 15,322 | 19,163 |

| FD normalised EPS | 15.36 | 17.25 | 24.33 | 22.64 | 25.27 | 32.05 | 40.08 |

| FD norm. EPS growth (%) | -29.8 | 12.3 | 58.4 | 31.3 | 3.9 | 41.5 | 58.6 |

| FD normalised P/E (x) | 60.9 | - | 38.5 | - | 37.0 | - | 23.4 |

| EV/EBITDA (x) | 32.7 | - | 34.6 | - | 24.3 | - | 16.0 |

| Price/book (x) | 4.8 | - | 4.5 | - | 4.2 | - | 3.7 |

| Dividend yield (%) | 0.7 | - | 1.2 | - | 1.2 | - | 1.6 |

| ROE (%) | 7.9 | 8.6 | 12.0 | 10.6 | 11.7 | 13.9 | 16.9 |

| Net debt/equity (%) | 7.1 | 3.8 | net cash | 0.3 | net cash | net cash | net cash |

Source: Company data, Nomura estimates

Global Markets Research 30 June 2026

| Rating Remains | Buy |

|---|---|

| Target price Increased from TWD 850.00 | TWD 1,200.00 |

| Closing price 26 June 2026 | TWD 936.00 |

| Implied upside | +28.2% |

| Market Cap (USD mn) | 14,033.5 |

| ADT (USD mn) | 161.7 |

Relative performance chart

Source: LSEG, Nomura

Research Analysts

Semiconductor

Donnie Teng - NIHK donnie.teng@nomura.com +852 2252 1439

Aaron Jeng, CFA - NITB

aaron.jeng@nomura.com +886(2) 21769962

Production Complete: 2026-06-29 20:30 UTC

Key data on GlobalWafers

Performance

| (%) | 1M | 3M | 12M | ||

|---|---|---|---|---|---|

| Absolute (TWD) | 8.1 | 105.9 | 194.3 | M cap (USDmn) | 14,033.5 |

| Absolute (USD) | 6.6 | 106.1 | 167.8 | Free float (%) | 27.5 |

| Rel to Taiwan TAIEX Index | 5.7 | 72.2 | 96.2 | 3-mth ADT (USDmn) | 161.7 |

Income statement (TWDmn)

| Year-end 31 Dec | FY24 | FY25 | FY26F | FY27F | FY28F |

|---|---|---|---|---|---|

| Revenue | 62,626 | 60,598 | 61,726 | 73,535 | 88,666 |

| Cost of goods sold | -42,823 | -45,974 | -48,565 | -54,686 | -60,324 |

| Gross profit | 19,804 | 14,624 | 13,162 | 18,850 | 28,342 |

| SG&A | -3,365 | -3,770 | -3,988 | -4,412 | -5,024 |

| Employee share expense | -2,320 | -2,218 | -2,109 | -2,427 | -2,834 |

| Operating profit | 14,119 | 8,636 | 7,065 | 12,011 | 20,485 |

| EBITDA | 18,987 | 13,797 | 12,587 | 17,870 | 26,559 |

| Depreciation | -4,829 | -5,120 | -5,478 | -5,812 | -6,026 |

| Amortisation | -39 | -41 | -44 | -47 | -48 |

| EBIT | 14,119 | 8,636 | 7,065 | 12,011 | 20,485 |

| Net interest expense | 2,489 | 1,124 | 3,386 | 3,479 | 4,083 |

| Associates & JCEs | 186 | 85 | 15 | 0 | 0 |

| Other income | -4,364 | -329 | 4,365 | 0 | 0 |

| Earnings before tax | 12,429 | 9,516 | 14,831 | 15,490 | 24,568 |

| Income tax | -2,590 | -2,205 | -3,197 | -3,408 | -5,405 |

| Net profit after tax | 9,840 | 7,311 | 11,633 | 12,082 | 19,163 |

| Minority interests | 7 | 0 | 0 | 0 | 0 |

| Other items | 0 | 0 | 0 | 0 | 0 |

| Preferred dividends | 0 | 0 | 0 | 0 | 0 |

| Normalised NPAT | 9,847 | 7,311 | 11,633 | 12,082 | 19,163 |

| Extraordinary items | 0 | 0 | 0 | 0 | 0 |

| Reported NPAT | 9,847 | 7,311 | 11,633 | 12,082 | 19,163 |

| Dividends | -5,259 | -3,290 | -5,235 | -5,437 | -7,068 |

| Transfer to reserves | 4,588 | 4,021 | 6,398 | 6,645 | 12,095 |

| Valuations and ratios | |||||

| Reported P/E (x) | 42.3 | 60.9 | 38.5 | 37.0 | 23.4 |

| Normalised P/E (x) | 42.3 | 60.9 | 38.5 | 37.0 | 23.4 |

| FD normalised P/E (x) | 42.7 | 60.9 | 38.5 | 37.0 | 23.4 |

| Dividend yield (%) | 1.2 | 0.7 | 1.2 | 1.2 | 1.6 |

| Price/cashflow (x) | 16.2 | - | 9.7 | 28.4 | 19.8 |

| Price/book (x) | 4.9 | 4.8 | 4.5 | 4.2 | 3.7 |

| EV/EBITDA (x) | 23.3 | 32.7 | 34.6 | 24.3 | 16.0 |

| EV/EBIT (x) | 31.2 | 52.1 | 61.7 | 36.1 | 20.8 |

| Gross margin (%) | 31.6 | 24.1 | 21.3 | 25.6 | 32.0 |

| EBITDA margin (%) | 30.3 | 22.8 | 20.4 | 24.3 | 30.0 |

| EBIT margin (%) | 22.5 | 14.3 | 11.4 | 16.3 | 23.1 |

| Net margin (%) | 15.7 | 12.1 | 18.8 | 16.4 | 21.6 |

| Effective tax rate (%) | 20.8 | 23.2 | 21.6 | 22.0 | 22.0 |

| Dividend payout (%) | 53.4 | 45.0 | 45.0 | 45.0 | 36.9 |

| ROE (%) | 12.5 | 7.9 | 12.0 | 11.7 | 16.9 |

| ROA (pretax %) | 8.2 | 4.5 | 3.7 | 6.3 | 10.5 |

| Growth (%) | |||||

| Revenue | -11.4 | -3.2 | 1.9 | 19.1 | 20.6 |

| EBITDA | -24.0 | -27.3 | -8.8 | 42.0 | 48.6 |

| Normalised EPS | -51.8 | -30.6 | 58.4 | 3.9 | 58.6 |

| Normalised FDEPS | -51.8 | -29.8 | 58.4 | 3.9 | 58.6 |

Source: Company data, Nomura estimates

Cashflow statement (TWDmn)

| Year-end 31 Dec | FY24 | FY25 | FY26F | FY27F | FY28F | FY28F |

|---|---|---|---|---|---|---|

| EBITDA | 18,987 | 13,797 | 12,587 | 17,870 | 26,559 | 26,559 |

| Change in working capital Other operating cashflow | 11,289 -4,298 | -28,021 | 28,805 | -2,179 | -2,649 | -2,649 |

| Cashflow from operations | 25,978 | -1,297 | 4,570 | 71 15,762 | -1,322 22,589 | -1,322 22,589 |

| Capital expenditure | -48,319 | -15,520 | 45,962 -25,033 | -20,956 | -17,398 | -17,398 |

| -22,342 | -33,130 -48,650 | 20,929 | -5,193 | 5,190 | 5,190 | |

| Free cashflow | ||||||

| Reduction in investments | -6,052 | 498 | -127 | 0 | 0 | 0 |

| Net acquisitions | 0 | 0 | 0 | 0 | 0 | 0 |

| Dec in other LT assets | 4,302 | 39,845 | 14,538 | 13,418 | 8,679 | 8,679 |

| Inc in other LT liabilities | 0 | 0 | 0 | 0 | ||

| Adjustments | 0 | 0 | 0 | 0 | 0 | 0 |

| CF after investing acts | -24,092 | -8,307 | 35,339 | 8,224 | 13,869 | 13,869 |

| Cash dividends | -8,748 | -5,259 | -3,290 | -5,235 | -5,437 | -5,437 |

| Equity issue | 0 | 0 | 0 | 0 | 0 | 0 |

| Debt issue | 9,776 | -11,511 | -7,141 | 0 | 0 | 0 |

| Convertible debt | 0 | 0 | 0 | 0 | 0 | 0 |

| issue Others | 35,829 | 5,632 | -14,495 | 0 | 0 | 0 |

| CF from financial | acts 36,857 | -11,139 | -24,927 | -5,235 | -5,437 | -5,437 |

| Net cashflow | 12,765 | -19,445 | 10,413 | 2,989 | 8,432 | 8,432 |

| Beginning cash | 26,165 | 29,896 | 32,886 | 32,886 | ||

| Ending cash | 38,929 | 38,929 | 19,484 | |||

| Ending net debt | 19,484 | 29,897 | 32,886 | 41,318 | 41,318 | |

| Balance sheet | -13,891 | |||||

| (TWDmn) | -1,282 | 6,652 | -10,901 | -22,323 | -22,323 | |

| As at 31 Dec Cash & equivalents | FY24 38,929 29 | FY25 | FY26F 19,484 29,896 | FY27F 32,886 | FY28F 41,318 0 | FY28F 41,318 0 |

| Marketable securities Accounts receivable | 10,265 | 1 | 0 9,586 | 0 11,497 | ||

| Inventories | 10,113 10,399 | 10,148 | 11,090 | 13,889 12,114 | 13,889 12,114 | |

| Other current | 11,238 20,030 | 46,632 | 31,636 | 31,636 | 31,636 | 31,636 |

| assets Total current assets | 80,492 | 87,109 | 98,956 | 98,956 | ||

| LT investments | 7,445 | 86,629 6,947 | 81,266 7,074 | 7,074 | 7,074 | 7,074 |

| Fixed assets | 119,074 0 | 107,241 | 111,560 | 113,239 0 | 115,885 | 115,885 |

| Goodwill Other | 0 | 0 | 0 | 0 | ||

| intangible assets Other LT assets | 0 | 0 | 0 | 0 | 0 | 0 |

| 17,570 | 18,179 | 18,179 | 18,179 | 18,179 | ||

| Total assets | 224,581 | 17,525 218,343 | 218,080 | 225,602 | 240,094 | 240,094 |

| Short-term debt | 27,117 | 18,571 | 14,252 | 14,252 | 14,252 | 14,252 |

| Accounts payable | 4,464 | 5,138 | 5,905 | 5,905 | ||

| Other current | 5,371 | 4,161 | 44,105 | 44,105 | 44,105 | 44,105 |

| liabilities Total current liabilities | 32,577 | 31,377 54,109 | 63,495 | 64,262 | 64,262 | |

| Long-term debt | 65,065 10,531 | 7,565 | 62,821 | 4,743 | 4,743 | 4,743 |

| Convertible debt | 0 | 0 | 4,743 0 | 0 | 0 | 0 |

| Other LT liabilities Total liabilities | 57,958 | 63,374 125,048 | 50,690 118,254 | 50,690 118,929 | 50,690 119,695 | 50,690 119,695 |

| 133,553 | -4 | -4 | -4 | -4 | ||

| Minority interest | -3 | -3 0 | 0 | 0 | 0 | |

| Preferred stock | 0 | 0 4,781 | 4,781 | 4,781 | 4,781 | |

| Common stock Retained | 4,781 | 4,781 | 47,769 | 59,864 | 59,864 | |

| earnings Proposed | 37,451 3,290 | 41,124 5,235 | 5,437 | 7,068 | 7,068 | |

| dividends | 31,640 5,259 | 48,690 | 48,690 | |||

| Other equity and Total shareholders' | 49,350 91,030 | 47,776 93,298 | 48,690 99,830 | 48,690 106,677 | 120,403 | 120,403 |

| reserves equity | ||||||

| Total equity & liabilities | 224,580 | 218,342 | 225,602 | 240,094 | 240,094 | |

| Liquidity (x) | ||||||

| 218,080 | ||||||

| Current ratio | net cash net cash | 0.48 7.1 | 1.24 1.60 1.29 - - - net cash cash | 1.37 - net cash net cash | 1.54 - net cash net cash | 1.54 - net cash net cash |

| Interest cover Leverage Net debt/EBITDA | (x) | net | ||||

| Net debt/equity (%) Per share Reported EPS (TWD) | 22.14 22.14 21.90 | 15.36 15.36 15.36 | 24.33 24.33 | 25.27 25.27 | 40.08 40.08 | 40.08 40.08 |

| Norm EPS (TWD) FD norm EPS (TWD) BVPS (TWD) | 190.39 | 195.14 6.88 | 24.33 | 223.12 | 251.83 | 251.83 |

| DPS (TWD) | 11.00 | 25.27 | 40.08 | 40.08 | ||

| 11.37 | 14.78 | 14.78 | ||||

| (days) | 208.80 10.95 | |||||

| Activity | 58.2 | 52.4 | 52.4 | |||

| 59.4 | 61.4 | 77.2 | 52.3 70.9 | 70.4 | 70.4 | |

| Days receivable Days inventory | 87.8 | 85.9 37.8 | 32.4 | 32.0 | 33.5 | 33.5 |

| Days payable Cash cycle | 44.3 | 109.4 | ||||

| 102.9 | ||||||

| 103.0 | ||||||

| 89.3 | ||||||

| 91.2 |

Source: Company data, Nomura estimates

Company profile

GlobalWafers is the world's third-largest and largest non-Japanese wafer manufacturer that specializing in 3' to 12' silicon wafer manufacturing, possessing a complete production line from ingot growth, slicing, etching, diffusion, polishing and epitaxy.

Valuation Methodology

Our TP of TWD1200 is based on 4.8x 2028F BVPS TWD252. The 4.8x P/B is based on the upper-half of 2-6x P/B range during the full Semi wafer cycle in 2017-2020. The benchmark index is TAIEX.

Risks that may impede the achievement of the target price

Downside risks include: · Faster-than-expected entry of China into the 12' semi wafer market. · Slower-than-expected of market consolidation. · Worse-than-expected end-demand for the semi industry. · Less favorable demand/supply dynamics in the semi wafer industry. · Less favorable FX volatility and rising material/utility costs.

ESG

In response to global climate change and latest development trends in corporate social responsibilities (CSR), GlobalWafers has taken the initiative to compile a CSR report. Based on long-term in-depth interactions with local communities and engagement with stakeholders, GlobalWafers discloses in the report relevant information on material issues regarding the four aspects of corporate governance, economy, environment, and society, as well as execution & improvement results, in addition to presenting the the future vision and goals in terms of sustainable development.

Ur u anu Trom anle motmet mohlaue matchlatrniwy

Note

11 Annual shipment

Ulu tlelmal plate lo lunlutlol do alt mel g'aleu omuun valel a up tie helgm yap m wetweeh

I/0

HBM4E

HBM4E

ASP per 12" SiC substrate (USD)(5)

HBM4E

GWC market share (%)(7)

HBM4E

HBM4E

HBM4E

Dummy

1/0

VO

Feynman shipment (mn)(1)

Fig. 1: The floor plan and cross-section chart of nVidia's Feynman GPU

SiC thermal plate to function as an intergrated silicon carrier (fill up the height gap in between GPU and HBM) and thermal interface material (TIM)

Source: Nomura estimates, Company data

Fig. 2: The revenue contribution assumption for SiC thermal plate for Feynman

Source: Nomura estimates

Net Sales

(TWD mn)

Net Sales

Gross profit

15,595

Previous

2Q25

3Q25

2026F

16,008

61,159

Revised

1Q26

4Q25

14,493

Change (%; pp) Previous

14,502

13,985

61,726

4,112

4,123

2,662

3,726

0.9

2,914

71,372

Earnings forecast revisions

2027F

2Q26F 3Q26F 4Q26F

15,396

15,762

16,584

2025

60,598

8,636

14,624

83,460

9,516

3,358

Revised Change (%; pp) Previous

3,208

18,850

23,593

16,752

1,669

73,535

1,797

6,445

We revise up our 2026-28F earnings forecasts by 11-41%. We expect a moderate revenue recovery in 2026F, but believe revenues will accelerate from 2H26F onward, as well as a more favorable supply-demand environment in 2027-28F. YTD 2026, GWC has also recognized meaningful non-operating gains from its investment in Siltronic (WAF GR, Not rated) due to the sharp rise in Siltronic's share price. We have not yet factored any Siltronic stock price impact into our forecasts from 2H26F onward. 19,644 1.3 20.1 18.4 4.75 7,312 5.11 15.36

EPS

EPS

In the near term, we believe GWC's profitability is still under pressure due to rising depreciation costs from new capacity expansion, but as market demand continues to grow, we believe price hike potential is also likely to increase. 4.7%

Op income

Fig. 3: GWC: earnings estimate revisions

204.2%

2,909

12,011

7.7%

-54.9%

-54.9%

3.0

3,682

2,123

7.0

3,129

4.1

18.1%

7.6%

7.6%

15.5%

17.1%

12.0%

-19.3%

-14.0%

174.7%

165.2%

| 3.4% | -8.7% -11.3% -10.3% | -8.7% -11.3% -10.3% | -8.7% -11.3% -10.3% | 8.8% 14.4% -3.2% | 8.8% 14.4% -3.2% | 8.8% 14.4% -3.2% | 19.1% 20.6% | 19.1% 20.6% | 19.1% 20.6% |

|---|---|---|---|---|---|---|---|---|---|

| -20.4% | 4.5% -16.7% | 44.2% | -24.2% -29.1% | -3.8% -22.2% | 26.1% | -1.2% -26.2% | 1.9% -10.0% | 43.2% | 50.4% |

| -34.7% | -27.6% | -61.6% -33.6% | 43.0% | -31.6% | 46.2% -10.8% | -38.8% | -18.2% | 70.0% | 70.6% |

| -35.2% | -38.3% 265.2% | 10.0% | 181.6% | 33.0% | 7.6% -23.4% | 55.8% | 4.4% | 58.6% | |

| -53.2% -58.8% | 41.6% | -33.3% 360.5% | 30.2% | 198.9% | 15.2% 10.7% | -25.7% | 59.1% | 3.9% | 58.6% |

Growth (YoY)

Net Sales

Gross profit

Op income

Pretax income

Net income

Source: Nomura estimates

Fig. 4: GWC: P&L

Source: Company data, Nomura estimates

2026F

2028F

2027F

Revised Change (%; pp)

73,535

88,666

88,666

61,726

6.2

7,065

28,342

12,011

14,831

15,490

11,633

20,485

12,082

19,163

24,568

21.3%

25.6%

11.4%

40.1

16.3%

24.0%

21.1%

18.8%

32.0

23.1

16.4%

24.33

25.27

21.6

13,162

18,850

28,342

20.1

20,485

24,568

19,163

25.1

22.3

25.1

32.0%

- 1%

25.1

27.7%

21.6%

3.0

3.7

3.3

40.08

50

45

40

35

30

25

20

15

10

5

10/28/2014

Valuation methodology and risks

9

6

5

Our new TP of TWD1,200 is based on 4.8x 2028F BVPS of TWD252. The 4.8x target multiple is at the upper-half of the historical P/B range of 2-6x during the full semi wafer cycle in 2017-20. 2

Downside risks include:

- Faster-than-expected entry of China into the 12' semi wafer market.

- Slower-than-expected of market consolidation.

- Worse-than-expected end-demand for the semi industry.

- Less favorable demand/supply dynamics in the semi wafer industry.

- Less favorable FX volatility and rising material/utility costs.

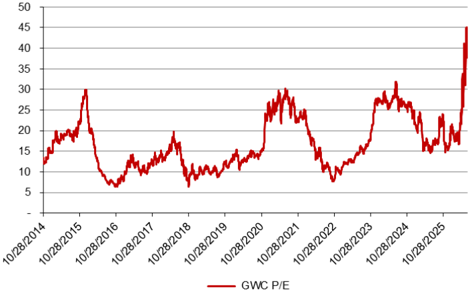

Fig. 5: GWC: P/E

Source: Bloomberg, Nomura estimates

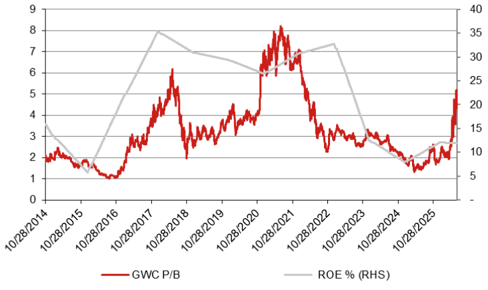

Fig. 6: GWC: P/B

Source: Bloomberg, Nomura estimates

10/28/2018

10/28/2017

10/28/2019

GWC P/B

10/28/2020

1

10/28/2021

10/28/2022

10/28/2023

10/28/2024

10/28/2025

ROE % (RHS)

35

30

25

20

15

10

5

Rating and target price chart (three year history)

GlobalWafers

Appendix A-1

1100.00

1000.00

900.00

800.00

700.00

600.00

400.00

300.00

200.00

100.00

As of 29-Jun-2026

Currency = TWD

Di

21

21

05

05

24

24

This report has been produced by Nomura International (Hong Kong) Ltd. (NIHK), Hong Kong.

See Disclaimers for Nomura Group entity details.