PDF 原檔:260630_2454_聯發科_廣發_original.pdf

圖片清單(已驗證 2026-07-01)

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

_001.png |

73KB | 真資料圖 | MTK 股價 vs 營收 YoY vs 營業利益 YoY(1Q22–4Q26E),2026 起股價與成長回升 |

_002.png |

51KB | 真資料圖 | MTK 12 個月 forward PER(2010–2026),Avg 18.3x,近期衝至約 58x |

兩張皆為估值/股價走勢圖,lib 不嵌(公司頁已具內容)。報告核心資料為文字表格(Google TPU Roadmap、Meta ASIC Roadmap、TPU 獲利假設)。 <40KB 未列者預設 logo/裝飾。

原始內容

MediaTek (2454 TT)

Triggerfish Implications & Contribution to be Significant

C Progress Intact, with >$170 Annualized EPS Potential

Raise TP to NT$6,420: Despite sell-side's raise for MTK's TP, the share price pulled back by 17% in the past one week due to broad market weakness, Qualcomm's entry into datacenter ASIC and speculated 2nm/Bladerunner project from Broadcom. In our view, Qualcomm's AI250 has little overlap with MTK, due to significant differences in client base and performance. Additionally, we believe the rumored Bladerunner hasn't been started as a project and still expect Broadcom to have only one new TPU SKU, Whalefish (or Sunfish x2), in 2028, suggesting a positioning disadvantage, vs. MTK's. On the other hand, we believe the Street underestimated MTK's Triggerfish's potential on much higher ASP/content and the large SRAM design, extending MTK's positioning from training (v8t) to inferencing which is Broadcom's market. Moreover, we reiterate our earlier report of Likely SpaceX's Win on May 27 of MTK's 2 nd datacenter ASIC in late-2028, adding momentum on top of TPU's Icefish at the same timeframe. As such, we raise the ASIC revenue to $2.5bn/$18bn/$73bn in 2026/27/28; accordingly revise our EPS estimates +0%/+3% in 2026E/2027E and lift TP from NT$5,520 to NT$6,420, now based on a 45x 2027E EPS or 19x 2028E EPS.

Triggerfish to boost ASPs and positioning in TPU: Despite the MTK Triggerfish's news come-out a week ago, the share price didn't react, yet, we expect upside to Triggerfish in: 1) ASPs of $18k , vs. Humufish's $13k or Zebrafish's $5.5k; 2) Triggerfish's mix of v9 (incl. Humufish and Triggerfish) to ~50%; 3) MTK's content of 4x companion compute core embedded large SRAM (~250MB x 4), one simulator based on 5nm, 4x I/O cores and backend; 4) MTK's positioning in TPU , as the large SRAM and the simulator CPU, which manages workload between large-SRAM cores and performance cores, will help MTK extend from training (v8t) to inferencing.

Accelerated share gains in TPU: For v8, we expect MTK's v8t to be in mass volume at earlier timeframe, vs. v8i which could be in late-2026. For v9, we still believe MTK's Humufish is the only SKU in 2nm; that said, we see little chance for its competitor to come out 2nm at that time and believe the speculated Bladerunner (i.e., 2nm) hasn't been progressed as a project. Having said that, its competitor's new SKU, Whalefish (Sunfish x2), in 2028 could be a small volume SKU due to disadvantages in process node and HBM. Looking ahead, we believe MTK's Icefish for v10 is solid, while other projects of v10 aren't clear by now.

Risks: 1) AI demand slowdown; 2) consumer demand; 3) peer competition.

Profit forecast

| 2024 | 2025 | 2026E | 2027E | 2028E | |

|---|---|---|---|---|---|

| Revenue (m) | 530,586 | 595,966 | 687,364 | 1,305,124 | 3,166,080 |

| Revenue YoY ( % ) | 22.4 | 12.3 | 15.3 | 89.9 | 142.6 |

| Net profit (m) | 106,387 | 105,319 | 106,488 | 227,075 | 527,268 |

| Net profit YoY ( % ) | 38.2 | -1.0 | 1.1 | 113.2 | 132.2 |

| EPS (NT$) | 66.9 | 66.2 | 66.9 | 142.6 | 331.2 |

| P/E | 39.0 | 39.5 | 39.0 | 18.3 | 7.9 |

| ROE ( % ) | 26.3 | 25.7 | 26.5 | 55.7 | 168.6 |

Source: Company data, GF Securities (Hong Kong) Brokerage.

Please be sure to read the disclosures at the end of this report carefully.

数据来源:公司

财务报

表,广

发证

券

发

展研究中心

Maintained Target price

Buy NT$ 6,420

Jeff Pu, CFA SFC CE No. BNO719 jeffpu@gfgroup.com.hk

Henry Huang SFC CE No. BYA749 henryhuang@gfgroup.com.hk

Earnings Forecast

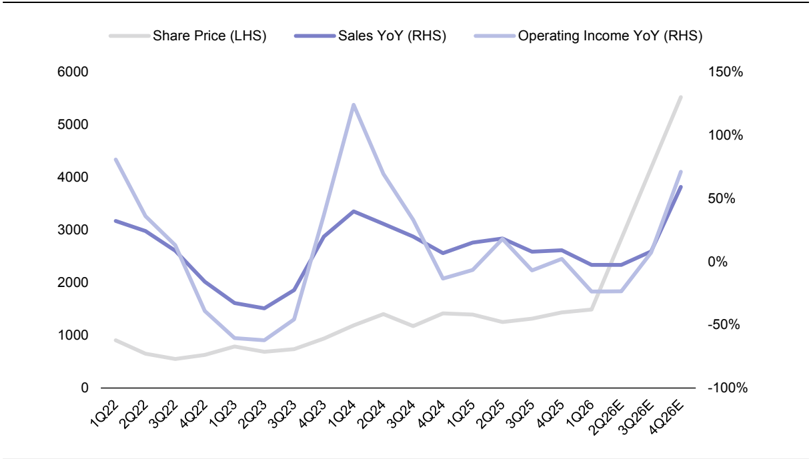

Figure 1: MTK share price (NT$), vs. revenue YoY (%), OP YoY (%)

Sources: Company data, GF Securities (Hong Kong) Brokerage

Figure 2: Google TPU Roadmap

| TPU v5e | TPU v5p | TPU v6e | TPU v7 Ironwood | TPU 8i | TPU 8t | TPU v9x | TPU v9x | TPU v8.5 | TPU v10ax | TPU v10x | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Code name | Viperlite | Viperfish | Trillium / Ghostlite | Ghostfish | Sunfish | Zebrafish | Humufish | Triggerfish | Whalefish | Merope | Icefish |

| Time | 2Q23 | 1Q24 | 4Q24 | 4Q25 | 4Q26 | 4Q26 | 4Q27 | 4Q27 | 1Q28 | 3Q28 | 4Q28 |

| Design Service - compute | BRCM | BRCM | BRCM | BRCM | BRCM | GOOG | GOOG | GOOG | BRCM | BRCM or MRVL | GOOG |

| Design Service - I/O | BRCM | BRCM | BRCM | BRCM | BRCM | MTK | MTK | MTK | BRCM | BRCM Or MRVL | MTK |

| Design Service - back-end | BRCM | BRCM | BRCM | BRCM | BRCM | MTK | MTK | MTK | BRCM | BRCM or MRVL | MTK |

| Compute | 1*N5 | 1*N5 | 1*N5P | 2*N3E | 2*N3P | 1*N3P | (4N2)2 | (4N2)2 | 2x Sunfish | SF2 | N2P8+N2P 16 |

| I/O | 1*N5 | 2*N3P | 1*N3P | (2N3)2 | (2N3)2 | SF2 | N2P*6 | ||||

| On-chip SRAM | 384MB | 128MB | 4*250MB | ||||||||

| Memory | 2*HBM2e 4hi | 6*HBM2e 4hi | 6*HBM3 8hi | 8*HBM3e 12hi | 8*HBM3e 8hi | 6*HBM3e 8hi | (6HBM4e 8Hi)2 | (6HBM4e 8Hi)2 | 16*HBM5 12hi | ||

| Memory Spec | 16GB | 95GB | 32GB | 192GB | 288GB | 216GB | 288GB | 288GB | |||

| MemoryBW (TB/s) | 0.82 | 2.77 | 1.64 | 7.4 | 8.6 | 6.5 | |||||

| Back-end | 300 | 550 | 390 | 980 | |||||||

| Back-end | CoWoS-S | CoWoS-S | CoWoS-S | CoWoS-S | CoWoS-L | CoWoS-S | EMIB-T | EMIB-T | CoWoS- S/SOIC | EMIB-T or CoWoS | |

| Pod | 256 | 8960 | 256 | 9216 | 1152 | 9600 |

Sources: Company data, GF Securities (Hong Kong) Brokerage

Please be sure to read the disclosures at the end of this report carefully.

Figure 3: Meta's ASIC Roadmap

| MTIA 200 | MTIA 300 | MTIA 400 | MTIA 450 | MTIA 500 | MTIA 600 | |

|---|---|---|---|---|---|---|

| Code name | Artemis | Athena | Iris Plus | ARKE | Astrid | Apollo |

| Time | 4Q24 | 2Q26 | 4Q26 | 1Q27 | 3Q27 | 2Q28 |

| Design Service - compute | BRCM | BRCM | BRCM | BRCM | TBD | TBD |

| Design Service - I/O | BRCM | BRCM | BRCM | BRCM | TBD | TBD |

| Design Service - back-end | BRCM | BRCM | BRCM | BRCM | TBD | TBD |

| Compute | N5 | 1*N3E | 2*N3E | 1*N2 | N2 | N2P |

| I/O | 2*N4 | 2*N4 (+1 SoC) | 1*N3 | N3 | N3 | |

| Memory | LPDDR5 | 6*HBM3e 12Hi | 8*HBM3e 12Hi | 8*HBM3e 12Hi | 8*HBM4e 12Hi | TBD |

| Memory Spec | 128GB | 216GB | 288GB | 288GB | 384GB | TBD |

| MemoryBW (TB/s) | 0.2 | 6.1 | 9.2 | 18.4 | 27.6 | TBD |

| TDP (W) | 90 | 800 | 1200 | 1400 | 1700 | TBD |

| Back-end | FC | CoWoS-S | CoWoS-L | CoWoS-L | CoWoS-L | CoWoS-L |

Sources: Company data, GF Securities (Hong Kong) Brokerage

Figure 4: MTK's TPU earnings assumptions

| 2026 | 2027 | 2028 | |

|---|---|---|---|

| Revenue analysis (Units in m, USD) | |||

| TPU v8x (A5921/Zebrafish) | 0.5 | 3.4 | 0.1 |

| TPU v8e (Humufish) | 0.0 | 2.4 | |

| TPU v9x (Triggerfish) | 0.0 | 2.4 | |

| TPU v8x - USD | 5500 | 5418 | 5125 |

| TPU v8e - USD | 13000 | 12806 | |

| TPU v9x - USD | 17732 | ||

| Revenue (USD bn) | 2.5 | 18.4 | 73.4 |

| Revenue (NTD bn) | 78 | 579 | 2313 |

| % | 11% | 44% | 73% |

| Net margin | 18% | 19% | 18% |

| Net earnings (NTD bn) | 14 | 110 | 405 |

| % | 13% | 48% | 77% |

| EPS (DC ASIC, NTD) | 9 | 69 | 254 |

Sources: Company data, GF Securities (Hong Kong) Brokerage

Earnings revision

We estimate the ASIC revenue to be $2.5bn/$18bn/$73bn in 2026/27/28, from earlier $2.2bn/18bn/$48bn, to factor in Triggerfish's mix and higher ASPs. Hence, we revise our EPS estimates +0%/+3% in 2026E/2027E and expect a strong earnings growth in 2028E.

Figure 5: Earnings revision

| NTDm | 2025 | 2026E | 2026E | 2027E | 2027E | Change (%) | Change (%) |

|---|---|---|---|---|---|---|---|

| NTDm | 2025 | Old | New | Old | New | 2026E | 2027E |

| Net sales | 595,966 | 680,816 | 687,364 | 1,307,612 | 1,305,124 | 1% | 0% |

| Gross profit | 283,080 | 309,840 | 312,192 | 570,592 | 565,298 | 1% | -1% |

| EBIT | 103,470 | 106,582 | 106,332 | 236,425 | 245,173 | 0% | 4% |

| Pre-tax Income | 124,888 | 123,096 | 122,846 | 254,074 | 262,742 | 0% | 3% |

| Net profit | 105,319 | 106,708 | 106,488 | 219,673 | 227,075 | 0% | 3% |

| EPS (NT$) | 66.2 | 67.0 | 66.9 | 138.0 | 142.6 | 0% | 3% |

| Key ratios (%) | |||||||

| Gross margin | 47.5% | 45.5% | 45.4% | 43.6% | 43.3% | ||

| Operating margin | 17.4% | 15.7% | 15.5% | 18.1% | 18.8% | ||

| Pre-tax margin | 21.0% | 18.1% | 17.9% | 19.4% | 20.1% | ||

| Net profit margin | 17.7% | 15.7% | 15.5% | 16.8% | 17.4% |

Sources: Company data, GF Securities (Hong Kong) Brokerage

Figure 6: MTK's P&L forecast

| (NTD m) | 2025 | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 2026E | 1Q27E | 2Q27E | 3Q27E | 4Q27E | 2027E |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Sales | 595,966 | 149,151 | 146,166 | 153,711 | 238,336 | 687,364 | 268,733 | 326,745 | 360,212 | 349,433 | 1,305,124 |

| COGS | 312,886 | 80,096 | 78,432 | 82,393 | 134,251 | 375,172 | 151,406 | 184,451 | 204,831 | 199,138 | 739,826 |

| Gross profit | 283,080 | 69,055 | 67,734 | 71,318 | 104,085 | 312,192 | 117,327 | 142,295 | 155,381 | 150,295 | 565,298 |

| Opex | 179,611 | 46,164 | 45,311 | 47,650 | 66,734 | 205,860 | 69,871 | 81,686 | 86,451 | 82,117 | 320,125 |

| Operating profit | 103,469 | 22,891 | 22,423 | 23,668 | 37,351 | 106,332 | 47,456 | 60,609 | 68,931 | 68,178 | 245,173 |

| Non-op profit | 21,419 | 4,129 | 4,129 | 4,129 | 4,129 | 16,514 | 4,392 | 4,392 | 4,392 | 4,392 | 17,569 |

| Pre-tax profit | 124,888 | 27,019 | 26,551 | 27,796 | 41,479 | 122,846 | 51,849 | 65,001 | 73,323 | 72,570 | 262,742 |

| Tax & Minority | 19,569 | 2,865 | 4,736 | 3,558 | 5,200 | 16,358 | 6,444 | 11,272 | 9,021 | 8,930 | 35,667 |

| Net Income | 105,320 | 24,154 | 21,815 | 24,239 | 36,280 | 106,488 | 45,405 | 53,729 | 64,302 | 63,640 | 227,075 |

| EPS (NTD) | 66.2 | 15.2 | 13.7 | 15.2 | 22.8 | 66.9 | 28.5 | 33.8 | 40.4 | 40.0 | 142.6 |

| Outstanding shares | 1,592 | 1,592 | 1,592 | 1,592 | 1,592 | 1,592 | 1,592 | 1,592 | 1,592 | 1,592 | 1,592 |

| Margin analysis | |||||||||||

| Gross margin | 47.5% | 46.3% | 46.3% | 46.4% | 43.7% | 45.4% | 43.7% | 43.5% | 43.1% | 43.0% | 43.3% |

| Operating margin | 17.4% | 15.3% | 15.3% | 15.4% | 15.7% | 15.5% | 17.7% | 18.5% | 19.1% | 19.5% | 18.8% |

| Pre-tax margin | 21.0% | 18.1% | 18.2% | 18.1% | 17.4% | 17.9% | 19.3% | 19.9% | 20.4% | 20.8% | 20.1% |

| Effective tax rate | 15.7% | 10.6% | 17.8% | 12.8% | 12.5% | 13.3% | 12.4% | 17.3% | 12.3% | 12.3% | 13.6% |

| Growth (YoY%) | |||||||||||

| Sales | 12% | -3% | -3% | 8% | 59% | 15% | 80% | 124% | 134% | 47% | 90% |

| Operating profit | 1% | -24% | -24% | 7% | 71% | 3% | 107% | 170% | 191% | 83% | 131% |

| Net income | -1% | -18% | -22% | -4% | 58% | 1% | 88% | 146% | 165% | 75% | 113% |

| EPS | -1% | -18% | -22% | -4% | 58% | 1% | 88% | 146% | 165% | 75% | 113% |

| Product mix (%) | |||||||||||

| Mobile | 55% | 49% | 43% | 41% | 30% | 39% | 28% | 23% | 24% | 28% | 26% |

| Smart edge | 40% | 46% | 52% | 53% | 66% | 56% | 69% | 74% | 73% | 69% | 71% |

| PMIC | 5% | 5% | 6% | 6% | 4% | 5% | 3% | 3% | 3% | 3% | 3% |

Sources: Company data, GF Securities (Hong Kong) Brokerage

Valuation and Recommendation

Maintain Buy with TP of $6,420

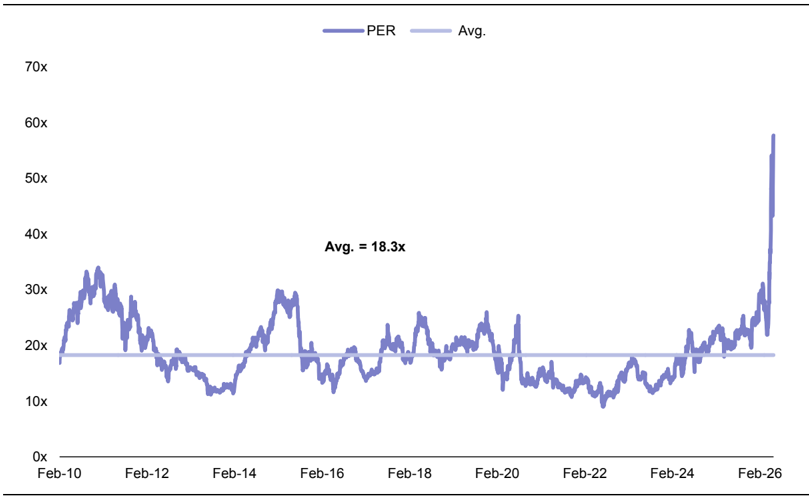

We rate MTK (2454 TT) Buy and set our TP at NT$6,420 which is based on 45x our 2027E EPS estimate or 19x 2028E EPS. We raise our 2027 multiple to reflect higher earnings growth in 2027/2028, but it suggests an undemanding valuation for 2028. MTK's P/E traded at an average of 18x since 2021 but was up to an average of 22x since 1Q24 when the company starts to see the AI opportunity. Our target multiple for 2027 is much higher than the mid-cycle level given Google TPU momentum and our bullish estimate of its 2027E/2028E earnings growth.

We adopt 2027 and/or 2028 as valuation basis to capture its datacenter ASIC potential which is the key market focus and expect the business to take off starting 2027. We adopt P/E methodology as we believe the market now mainly focuses on the company's earnings outlook, and we usually apply P/E method to downstream firms.

Fundamentally, we are positive on MTK, as it is well-positioned to expand its value position in smartphone SoCs amid the edge-AI trend, as well as the expansion into datacenter/enterprise ASICs and smart automotive solutions. The datacenter ASIC business is the key for upside, in our view, and we expect TPU to provide a volume boost for MTK, while the market will continue to monitor for its execution.

Figure 7: MTK's 12-month forward P/E

Sources: Company data, GF Securities (Hong Kong) Brokerage

Risks

1) AI demand slowdown; 2) consumer demand; 3) peer competition.

| Balance Sheet | [Table_FinanceDetail] | [Table_FinanceDetail] | [Table_FinanceDetail] | [Table_FinanceDetail] | NTD mn |

|---|---|---|---|---|---|

| 2024 | 2025 | 2026E | 2027E | 2028E | |

| Current assets | 351,025 | 397,456 | 431,623 | 740,792 | 1,595,866 |

| Cash and cash equivalents | 208,967 | 237,128 | 226,917 | 291,344 | 406,695 |

| Inventory | 44,713 | 62,121 | 84,743 | 196,663 | 520,451 |

| Accounts Receivable | 58,414 | 67,235 | 84,239 | 184,957 | 504,175 |

| Other current assets | 38,931 | 30,973 | 35,723 | 67,828 | 164,544 |

| Non-current assets | 346,842 | 346,329 | 352,651 | 357,824 | 361,889 |

| Long-term equity investment | 169,970 | 168,912 | 173,912 | 178,912 | 183,912 |

| Fixed assets | 56,917 | 60,427 | 61,750 | 61,922 | 60,987 |

| Other long-term assets | 119,955 | 116,990 | 116,990 | 116,990 | 116,990 |

| Total assets | 697,868 | 743,785 | 784,273 | 1,098,615 | 1,957,754 |

| Current liabilities | 266,902 | 303,350 | 351,301 | 664,537 | 1,619,847 |

| Accounts Payable | 40,777 | 48,710 | 58,407 | 115,176 | 290,412 |

| Short-term borrowings | 8,919 | 4,481 | 4,371 | 1,530 | 459 |

| Other current liabilities | 217,207 | 250,159 | 288,524 | 547,831 | 1,328,975 |

| Non-current liabilities | 25,910 | 31,240 | 31,073 | 26,765 | 25,141 |

| Long-term Debt | - | 6,795 | 6,629 | 2,320 | 696 |

| Other non-current liabilities | 25,910 | 24,444 | 24,444 | 24,444 | 24,444 |

| Total liabilities | 292,812 | 334,590 | 382,375 | 691,302 | 1,644,987 |

| Total Equity | 405,055 | 409,195 | 401,899 | 407,314 | 312,767 |

| Share Capital | 16,017 | 16,039 | 16,039 | 16,039 | 16,039 |

| Additional Paid-in Capital | 80,703 | 65,023 | 45,023 | 5,023 | -194,977 |

| Retained earnings | 299,907 | 319,539 | 332,243 | 377,658 | 483,111 |

| Minority interests | 8,428 | 8,594 | 8,594 | 8,594 | 8,594 |

| Total Liabilities & Equity | 697,868 | 743,785 | 784,273 | 1,098,615 | 1,957,754 |

| Income Statement | NTD mn | ||||

|---|---|---|---|---|---|

| 2024 | 2025 | 2026E | 2027E | 2028E | |

| Revenue | 530,586 | 595,966 | 687,364 | 1,305,124 | 3,166,080 |

| Cost of sales | 267,200 | 312,886 | 375,172 | 739,826 | 1,865,449 |

| Gross profit | 263,386 | 283,080 | 312,192 | 565,298 | 1,300,631 |

| Operating Expense | 160,974 | 179,610 | 205,860 | 320,125 | 713,500 |

| Operating profit | 102,412 | 103,470 | 106,332 | 245,173 | 587,131 |

| Interest Income | 11,150 | 10,819 | 6,961 | 7,774 | 10,471 |

| Interest Expense | 453 | 652 | 724 | 483 | 163 |

| Net other Non-op. Income/(Loss) | 6,410 | 11,251 | 10,277 | 10,277 | 10,277 |

| Pre-tax profit | 119,519 | 124,888 | 122,846 | 262,742 | 607,716 |

| Income tax | 12,378 | 18,770 | 15,470 | 34,779 | 79,560 |

| Profit for the year | 107,141 | 106,118 | 107,376 | 227,963 | 528,156 |

| Minority interest | 754 | 798 | 888 | 888 | 888 |

| Net profit to ord. equity | 106,387 | 105,319 | 106,488 | 227,075 | 527,268 |

| EPS (NT$) | 66.9 | 66.2 | 66.9 | 142.6 | 331.2 |

| Cash Flow Statement | NTD mn | NTD mn | |||

|---|---|---|---|---|---|

| 2024 | 2025 | 2026E | 2027E | 2028E | |

| Operating cash flow | 141,801 | 155,333 | 133,898 | 323,285 | 769,908 |

| Profit for the year | 106,387 | 105,319 | 106,488 | 227,075 | 527,268 |

| Depreciation & amortization | 20,936 | 22,974 | 23,325 | 24,475 | 25,583 |

| Change in working capital | 11,573 | 22,616 | 3,684 | 71,335 | 216,658 |

| Others | 2,905 | 4,424 | 400 | 400 | 400 |

| Investing cash flow | -26,534 | -26,885 | -30,048 | -30,048 | -30,048 |

| Capex | -16,186 | -16,846 | -15,009 | -15,009 | -15,009 |

| Change in investment | 12,522 | -6,674 | -9,639 | -9,639 | -9,639 |

| Others | -22,870 | -3,365 | -5,400 | -5,400 | -5,400 |

| Free cash flow | 115,268 | 128,449 | 103,850 | 293,237 | 739,861 |

| Financing cash flow | -77,368 | -100,288 | -114,061 | -228,810 | -624,509 |

| Change in Capital | -75,537 | -101,180 | -113,785 | -221,660 | -621,814 |

| Net Change in Debt | 1,093 | 2,357 | -276 | -7,150 | -2,695 |

| Others | -2,924 | -1,465 | - | - | - |

| Exchange influence | 8,292 | -5,770 | - | - | - |

| Net increase in cash | 37,900 | 28,161 | -10,211 | 64,427 | 115,351 |

| Key Financial Ratios | |||||

|---|---|---|---|---|---|

| Growth | |||||

| Revenue growth | 22.4 | 12.3 | 15.3 | 89.9 | 142.6 |

| Operating profit growth | 27.0 | 7.5 | 10.3 | 81.1 | 130.1 |

| Net profit growth | 38.2 | -1.0 | 1.1 | 113.2 | 132.2 |

| Profitability | |||||

| Gross profit margin | 49.6 | 47.5 | .45.4 | 43.3 | 41.1 |

| Operating Profit Margin | 19.3 | 17.4 | 15.5 | 18.8 | 18.5 |

| Net profit margin | 20.1 | 17.7 | 15.5 | 17.4 | 16.7 |

| Key Ratio | |||||

| ROA | 15.2 | 14.2 | 13.6 | 20.7 | 26.9 |

| ROE | 26.3 | 25.7 | 26.5 | 55.7 | 168.6 |

| Stability | |||||

| Gross debt/equity | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Interest Coverage | 226 | 159 | 147 | 508 | 3,610 |

| Current Ratio | 1.3 | 1.3 | 1.2 | 1.1 | 1.0 |

| Quick Ratio | 1.1 | 1.1 | 1.0 | 0.8 | 0.7 |

| Net debt/equity | Net Cash | Net Cash | Net Cash | Net Cash | Net Cash |

Rating definitions

Benchmark: Hang Seng Index (Hong Kong)

Company ratings Buy

Stock expected to outperform benchmark by more than 10 %

Hold

Expected stock relative performance ranges between -10 % and 10 %

Underperform

Stock expected to underperform benchmark by more than 10 %

Sector ratings Positive

Sector expected to outperform benchmark by more than 10%

Neutral

Expected sector relative performance ranges between -10% and 10%

Cautious

Sector expected to underperform benchmark by more than 10%

Hong Kong Company

GF Securities (Hong Kong) Brokerage Limited

Address

27/F, GF Tower, 81 Lockhart Road, Wan Chai, Hong Kong

Telephone

(852) 37191111

evanlee@gfgroup.com.hk

Disclaimer

This report has been prepared by GF Securities (Hong Kong) Brokerage Limited ('GF Securities (Hong Kong) Brokerage'). According to the laws, regulations and regulatory requirements in different countries and regions, this report is distributed by GF Securities (Hong Kong) Brokerage with relevant legal and compliant operation qualifications in these countries and regions.

GF Securities (Hong Kong) Brokerage is licensed by the Securities and Futures Commission of Hong Kong ('SFC') to conduct Type 4 Regulated Activity 'Advising on Securities'. It is regulated by the SFC, and is responsible for the distribution of this report in Hong Kong. Information about the qualifications of the research analyst(s) who is(are) the author(s) of this report as licensed by the SFC are disclosed in the section where research analyst names are shown.

The research analyst(s) primarily responsible for the content of this report, in whole or in part, certifies that with respect to the company or relevant securities that the analyst(s) covered in this report: 1) all of the views expressed accurately reflect his or her personal views on the company or relevant securities mentioned herein; and 2) no part of his or her remuneration was, is, or will be, directly or indirectly, in connection with his or her specific recommendations or views expressed in this report.

This report is published solely for information purpose and does not constitute an offer to buy or sell any securities or a solicitation of an offer to buy, or recommendation for investment in, any securities.

The securities mentioned in this report may not be allowed to be sold in certain jurisdictions. No action has been taken to permit the distribution of the research report to any person in any jurisdiction that the circulation or distribution of such research report is unlawful. This report is distributed solely to clients or designated institutions authorized by GF Securities (Hong Kong) Brokerage, and is not distributed publicly. It is distributed to certain clients based on the conclusion that they are able to assess investment risks independently, execute investment decisions independently and assume corresponding risks independently.

This report has been issued and based on information obtained from sources generally available to the public and believed by the research analyst(s) to be reliable but which has not been independently verified. No representation or warranty, either express or implied, is made by GF Securities (Hong Kong) Brokerage as to their accuracy and completeness of the information contained in this report. GF Securities (Hong Kong) Brokerage accepts no liability for all loss arising from the use of the materials presented in this report, unless is excluded by applicable laws or regulations. Please be aware of the fact that investments involve risks and the price of securities may be fluctuated and therefore return may be varied, past results do not guarantee future performance. Any recommendation contained in this report does not have regard to the specific investment objectives, financial situation and the particular needs of any individuals. This report is not to be taken in substitution for the exercise of judgment by respective recipients of this report, where necessary, recipients should obtain professional advice before making investment decisions.

GF Securities (Hong Kong) Brokerage may have issued, and may in the future issue, other communications that are inconsistent with, and reach different conclusions from, the information presented in the research report. The points of view, opinions and analytical methods adopted in the research report are solely expressed by the analysts but not that of GF Securities (Hong Kong) Brokerage or its affiliates. The information, opinions and forecasts presented in the research report are the current opinions of the analysts as of the date appearing on this material only which may subject to change at any time without notice. The salesperson, dealer or other professionals of GF Securities (Hong Kong) Brokerage may deliver opposite points of view to their clients and the proprietary trading division with respect to market commentary or dealing strategy either in writing or verbally. The proprietary trading division of GF Securities (Hong Kong) Brokerage may have different investment decision which may be contrary to the opinions expressed in the research report. GF Securities (Hong Kong) Brokerage or its affiliates or respective directors, officers, analysts and employees related to research report business may have rights and interests in securities mentioned in the research report. Recipients should be aware of relevant disclosure of interest (if any) when reading this report.

GF Securities (Hong Kong) Brokerage and its affiliates may be seeking or building business relationships with company(ies) mentioned in this report. Therefore, investors should consider the impact on the independence of this report by GF Securities (Hong Kong) Brokerage and its affiliates due to potential conflicts of interests. Investors should not make any investment decisions based solely on the contents of this report. Investors should make their own investment decisions and bear their own risk. No written or verbal commitment of sharing gains or losses from securities investments in any form shall be effective.

This report may contain and/or describe/present factual historical information on prices of Futures contracts (the 'information'). Please note that this information is solely for the purpose of forming part of the argument/grounds/evidence in our research methodology/analysis to support our conclusion on our view of the relevant industry/company mentioned. It does not, by any means (express or implied) to be associated with or constituted as SFC Type 5 Regulated Activity (Advising on futures contracts).

Disclosure of Interests

- 1) The research analyst(s) and his/her associate has not served as an officer of the company(ies) mentioned in this report, and does not have any financial interests in the company(ies) mentioned in this report.

- 2) GF Securities (Hong Kong) Brokerage and/or its affiliates does not have any financial interests and has not invested in interests aggregate to an amount equal to or more than (i) 1 % of the market capitalization; or (ii) 1 % of the issued share capital, or issued units, in the company(ies) mentioned in this report.

- 3) GF Securities (Hong Kong) Brokerage and/or its affiliates does not have any market making activities, and has not employed any individual(s) serving as officer(s) of the company(ies) mentioned in this report.

- 4) GF Securities (Hong Kong) Brokerage and/or its affiliates does not have any investment banking relationship in Hong Kong with the company(ies) mentioned in this report in the past 12 months.

Copyright © GF Securities (Hong Kong) Brokerage

Without the prior written consent obtained from GF Securities (Hong Kong) Brokerage, any part of the materials contained herein should not (i) in any forms be copied or reproduced or (ii) be re-disseminated.