PDF 原檔:260617_gs_quanta_original.pdf

原始內容

Quanta (2382.TW): AI server racks ramping up; Model transition and PC pull in may weigh on 3Q26; Neutral

Quanta's May revenue was down 8% MoM, or 11% below our estimate, which we attribute to the customers pulling forward PC orders amid rising memory cost in Jan-Apr, weighing on the end demand in May. The company's PC shipment in May declined by 8% YoY, or fl at MoM. We expect 21% MoM revenue growth for Jun, considering the low base in May, solid rack-level AI server demand and improved PC consumption by the quarter end. However, the growth momentum would slow down in Jul-Aug, mainly on the rack-level AI server model transition in 3Q26E weighing on Quanta's rack-level AI server shipments. Overall, we remain positive on Quanta's AI server racks ramp up, while we continue to prefer global leader, Hon Hai (report link), given the continuous speci fi cation migration would raise R&D requirement, consume more capacity (space and electricity), and customers would need more supports on AI data center deployment given the rising complexity. Maintain Neutral rating on Quanta.

Exhibit 1: We model Quanta's Jun 2026E revenue +98% YoY, or +21% MoM

| Apr-26 | May-26 | Jun-26(E) | Jul-26(E) | Aug-26(E) | Sep-26(E) | 2Q26E | 3Q26E | |

|---|---|---|---|---|---|---|---|---|

| Rev (NT$m) | 339,921 | 311,481 | 376,830 | 301,464 | 256,244 | 266,276 | 1,028,232 | 823,985 |

| YoY | 121% | 94% | 98% | 90% | 68% | 45% | 104% | 66% |

| MoM/QoQ | -6% | -8% | 21% | -20% | -15% | 4% | 27% | -20% |

| GS (NT$m) | 257,590 | 350,119 | ||||||

| Actual vs. GS | 32% | -11% |

Source: Company data, Goldman Sachs Global Investment Research

Earnings revision: We factor in Quanta's May revenue and raise our 2026-28E net incomes by 5% / 2% / 8%, mainly on higher revenues. Our 2026-28E revenues are raised to 8% / 10% / 21%, driven by (1) AI server racks ramping up along with growing AI infrastructure investments from global leading CSPs, and (2) general servers ASP increase on product mix upgrade and higher raw material costs. Our 2027-28E GMs are slightly revised up due to a higher revenue contribution from general servers, which carry a higher margin than AI server racks. We raise our 2027-28E opex ratios, mainly on higher R&D on AI servers.

Allen Chang

+852-2978-2930 | allen.k.chang@gs.com Goldman Sachs (Asia) L.L.C.

Verena Jeng

+852-2978-1681 | verena.jeng@gs.com Goldman Sachs (Asia) L.L.C.

Yifan Hu

+852-2978-0996 | yifan.hu@gs.com Goldman Sachs (Asia) L.L.C.

e92c7a75ab8b4efbba794e6b187208c8

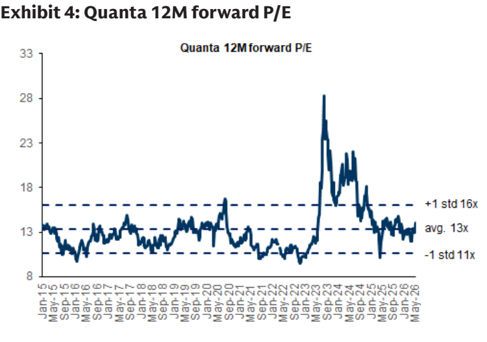

Exmbl4. Cudilla IeM lorWaraf/e

33

Quanta 12M forward P/E

28

23

18

Exhibit 2: Earnings revision

| 2026E | 2026E | 2026E | 2027E | 2027E | 2027E | 2028E | 2028E | 2028E | |

|---|---|---|---|---|---|---|---|---|---|

| NT m | Old | New | Chg | Old | New | Chg | Old | New | Chg |

| Revenue | 3,305,340 | 3,565,401 | 8% | 3,680,856 | 4,046,374 | 10% | 3,823,237 | 4,640,012 | 21% |

| GP | 175,730 | 185,247 | 5% | 200,371 | 225,105 | 12% | 208,041 | 259,587 | 25% |

| OP | 111,784 | 118,926 | 6% | 133,792 | 138,074 | 3% | 139,064 | 156,935 | 13% |

| Net income | 90,882 | 95,856 | 5% | 104,627 | 106,421 | 2% | 111,464 | 120,324 | 8% |

| Margins | |||||||||

| GM | 5.3% | 5.2% | 5.4% | 5.6% | 5.4% | 5.6% | |||

| OPM | 3.4% | 3.3% | 3.6% | 3.4% | 3.6% | 3.4% | |||

| NM | 2.7% | 2.7% | 2.8% | 2.6% | 2.9% | 2.6% |

Source: Goldman Sachs Global Investment Research

Valuation: We continue to use near-term P/E to derive our 12M TP. Our target multiple is updated to 11.4x 2027E EPS (vs. 11.3x previously), which is derived from the refreshed peers' correlation between forward trading P/E and earnings growth. With our updated earnings estimates and target multiple, our 12M TP is unchanged at NT$299. Our target P/E is still between the company's historical avg. and avg.-1stv. trading P/E, re fl ecting lower GM level. Maintain Neutral.

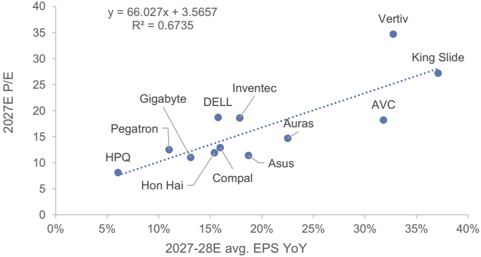

Exhibit 3: Quanta peers' 2027E P/E vs. 2027E-28E EPS YoY

Source: Company data, Goldman Sachs Global Investment Research, Re fi nitiv Eikon

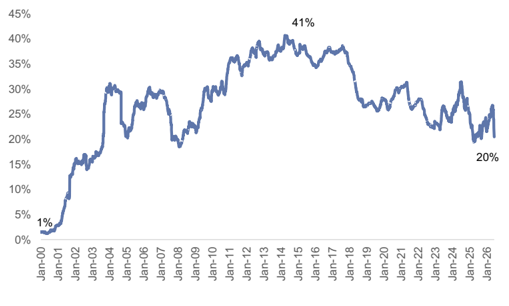

Exhibit 5: Quanta's QFII

Source: TEJ

Source: Re fi nitiv Eikon

e92c7a75ab8b4efbba794e6b187208c8

Exhibit 6: Quanta P&L summary

| (NT$ m) | 1Q25 | 2Q25 | 3Q25 | 4Q25 | 1Q26 | 2Q26E | 3Q26E | 4Q26E | 2024 | 2025 | 2026E | 2027E | 2028E |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 485,672 | 504,122 | 495,258 | 638,637 | 809,221 | 1,028,232 | 823,985 | 903,964 | 1,410,756 | 2,123,689 | 3,565,401 | 4,046,374 | 4,640,012 |

| Gross profit | 38,483 | 35,533 | 33,918 | 40,398 | 38,697 | 47,639 | 47,402 | 51,510 | 110,760 | 148,332 | 185,247 | 225,105 | 259,587 |

| Operating expense | (5,560) | (5,695) | (5,855) | (6,658) | (6,213) | (8,226) | (7,086) | (7,774) | (49,138) | (60,936) | (66,321) | (87,030) | (102,652) |

| Operating income | 24,600 | 20,403 | 18,374 | 24,019 | 23,024 | 29,130 | 32,076 | 34,696 | 61,622 | 87,396 | 118,926 | 138,074 | 156,935 |

| Pre tax profit | 25,269 | 21,617 | 20,909 | 27,478 | 24,537 | 27,756 | 30,501 | 36,494 | 73,167 | 95,273 | 119,288 | 138,298 | 157,209 |

| Net income | 19,498 | 16,861 | 16,431 | 22,197 | 21,192 | 21,872 | 24,035 | 28,757 | 59,702 | 74,988 | 95,856 | 106,421 | 120,324 |

| EPS (Diluted, NT$) | 4.91 | 4.26 | 4.14 | 5.44 | 5.24 | 5.40 | 5.94 | 7.10 | 15.29 | 18.75 | 23.68 | 26.29 | 29.66 |

| Margins / ratio | |||||||||||||

| Gross margin | 7.9% | 7.0% | 6.8% | 6.3% | 4.8% | 4.6% | 5.8% | 5.7% | 7.9% | 7.0% | 5.2% | 5.6% | 5.6% |

| Opex ratio | -2.9% | -3.0% | -3.1% | -2.6% | -1.9% | -1.8% | -1.9% | -1.9% | -3.5% | -2.9% | -1.9% | -2.2% | -2.2% |

| Operating margin | 5.1% | 4.0% | 3.7% | 3.8% | 2.8% | 2.8% | 3.9% | 3.8% | 4.4% | 4.1% | 3.3% | 3.4% | 3.4% |

| Net margin | 4.0% | 3.3% | 3.3% | 3.5% | 2.6% | 2.1% | 2.9% | 3.2% | 4.2% | 3.5% | 2.7% | 2.6% | 2.6% |

| QoQ | |||||||||||||

| Revenue | 16% | 4% | -2% | 29% | 27% | 27% | -20% | 10% | |||||

| Gross profit | 24% | -8% | -5% | 19% | -4% | 23% | 0% | 9% | |||||

| Operating income | 62% | -17% | -10% | 31% | -4% | 27% | 10% | 8% | |||||

| Pre tax profit | 42% | -14% | -3% | 31% | -11% | 13% | 10% | 20% | |||||

| Net income | 23% | -14% | -3% | 35% | -5% | 3% | 10% | 20% | |||||

| EPS | 24% | -13% | -3% | 31% | -4% | 3% | 10% | 20% | |||||

| YoY | |||||||||||||

| Revenue | 88% | 63% | 17% | 53% | 67% | 104% | 66% | 42% | 30% | 51% | 68% | 13% | 15% |

| Gross profit | 75% | 34% | 9% | 30% | 1% | 34% | 40% | 28% | 30% | 34% | 25% | 22% | 15% |

| Operating income | 110% | 34% | -6% | 58% | -6% | 43% | 75% | 44% | 41% | 42% | 36% | 16% | 14% |

| Pre tax profit | 74% | 10% | -2% | 55% | -3% | 28% | 46% | 33% | 41% | 30% | 25% | 16% | 14% |

| Net income | 62% | 11% | -1% | 40% | 9% | 30% | 46% | 30% | 50% | 26% | 28% | 11% | 13% |

| EPS | 58% | 9% | -3% | 37% | 7% | 27% | 43% | 31% | 50% | 23% | 26% | 11% | 13% |

Source: Company data, Goldman Sachs Global Investment Research

Price Target Risks and Methodology - Quanta

Our 12-month target price of NT$299 is based on an 11.4x 2027E P/E, which references PC/server peers' EPS growth vs. P/E multiple correlation. We see EPS growth as a major factor for the stock's performance.

Key upside/downside risks include: 1) stronger-/weaker-than-expected PC market recovery, 2) faster-/slower-than-expected AI server ramp-up, and 3) stronger-/weaker-than-expected demand on general server.

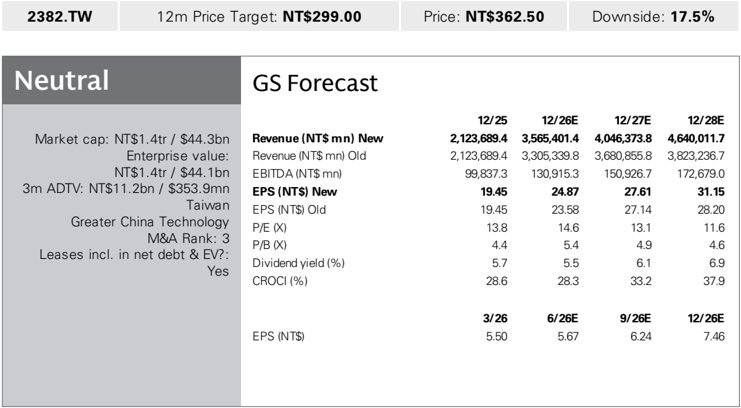

| 2382.TW 12m Price | Target: NT$299.00 | Price: NT$362.50 | Price: NT$362.50 | Downside: 17.5% | Downside: 17.5% |

|---|---|---|---|---|---|

| Neutral | GS Forecast | ||||

| Revenue ( NT$m n ) N e w Revenue (NT$ mn) Old EBITDA (NT$ mn) E PS ( NT$) N e w EPS (NT$) Old P/E (X) P/B (X) Dividend yield (%) | 12/25 2 , 12 3, 68 9.4 2,123,689.4 99,837.3 1 9.4 5 19.45 13.8 4.4 5.7 28.6 | 12/26E 3, 565 ,40 1 .4 3,305,339.8 130,915.3 2 4. 87 23.58 14.6 5.4 5.5 28.3 6/26E | 12/27E 4,04 6 ,3 7 3. 8 3,680,855.8 150,926.7 27 . 61 27.14 13.1 4.9 6.1 33.2 9 /26E | 12/28E 4, 6 40,0 11 . 7 3,823,236.7 172,679.0 3 1 . 15 28.20 11.6 4.6 6.9 37.9 | |

| Market c ap: NT$1.4tr / $44.3bn E nterpr is e v a lu e: NT$1.4tr / $44.1bn 3 | |||||

| m AD T V : NT$11. 2 bn / $3 5 3. 9m n | |||||

| Ta iw an | |||||

| G reater Chi na Te ch n ology | |||||

| M &A R ank: 3 | |||||

| L ea s e s i n cl . i n net d ebt & EV? : e s | |||||

| Y | CROCI (%) | ||||

| 3 /26 | 12/26E | ||||

| EPS (NT$) 5.50 | 5.67 | 6.24 | 7.46 |

Source: Company data, Goldman Sachs Research estimates, FactSet. Price as of 16 Jun 2026 close.

e92c7a75ab8b4efbba794e6b187208c8

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260617_gs_quanta_001.png |

33KB | 真資料圖 | 2027E P/E vs 2027-28E avg EPS YoY 散佈圖,比較 Vertiv、King Slide、Inventec、DELL、Gigabyte、Pegatron、HPQ、Hon Hai、Compal、Auras、Asus、AVC,含迴歸線與 R²=0.6735 |