PDF 原檔:260610_3008_大立光_jpm_largan_original.pdf

原始內容

Value

Growth

Momentum

ESGQ

Current

%Rank

16

50

44

39

23

Hist %Rank (1=Top) 6M 1Y 3Y 9 11 19 57 79 79 5Y 24 80

52

26

96

29

55

47

53

Largan Precision Co Ltd 43 50 60 57

Downgrade to Neutral; As good as it gets

After Largan's 50% share price rise in the past 1M (45% outperformance vs Taiex), we downgrade to Neutral, as we think the company's growth potential from variable aperture lens upgrade and solid iPhone demand has been priced in, and the market has somewhat turned too positive on its co-packaged optics (CPO) progress. Longer term, we still like the company's efforts into CPO, as this is a new addressable market for Largan and would require Largan's expertise in precision requirements. However, we think there are still uncertainties on how Largan could turn this opportunity into real earnings (at least not in the next 1-2 years, in our view) given the high competition and the incompatibility of Largan's FAU product with the current chip design ecosystem; we suggest waiting on the sidelines for more concrete progress. Our new 2026E/27E EPS are still 7%/5% above BBGe due to better iPhone demand estimates, but we think valuation would become demanding for further re-rating (currently already trading at 20x 12M fwd P/E, above historical avg. of 16-17x) as CPO is at least 1.5-2 years away for Largan.

- Silicon Photonics or CPO . Although Largan declined to comment, we believe the company is trying to make the Fiber Array Unit (FAU) with in-house components for IC design vendors, based on our latest industry checks. According to the Chairman's public comments at the AGM yesterday (link), Largan will invite potential customers to the fab in September to see Largan's products. In our view, this indicates that no customer has signed a contract or MOU with Lagan's FAU to date. We agree that Largan's strength could be its solid manufacturing capabilities with high precision requirements, while a weakness could be its lack of track record and customer relationships as a newcomer into silicon photonics. Lastly, Largan showcased its FAU during the latest Computex, which we consider very innovative. However, this design is not compatible with the current ecosystem of chip design. Thus, Largan will need IC design companies to change/adjust/create ICs that can be compatible with its FAU. This leads us to believe it will take a long time for its FAU business to bear fruit, even if customers agree to do so.

- iPhone lens upgrade . Largan is a major beneficiary of the upcoming iPhone camera upgrade to the iPhone 18 Pro and Pro Max, as the variable aperture camera adoption will be one of the highlights. We estimate Largan's content could see a meaningful increase (including lens and blade) compared to the main camera of the iPhone 17 Pro and Pro Max. However, we don't think the foldable iPhone would benefit Largan much, as there will be no periscope camera in it, and the rear camera will still pop up (less precision requirement).

- Implications . We increase our EPS estimates by 8% and 12% in 2026E and 2027E to factor in stronger iPhone demand vs our previous assumptions. However, we downgrade our rating to Neutral as we believe these have been priced in, and its CPO progress is still too early to see any real contribution. Our new Dec-26 PT of NT$3,600 is still based on a 17x 2027E P/E, in line with the average P/E since 2012. We believe it is too early to call a share price re-rating.

Sources for: Style Exposure -J.P. Morgan Global Markets Strategy; all other tables are company data and J.P. Morgan estimates.

See page 8 for analyst certification and important disclosures, including non-US analyst disclosures.

▼ Neutral

Previous: Overweight 3008.TW, 3008 TT Price (10 Jun 26):NT$4,130.00

▲ Price Target (Dec-26):NT$3,600.00

Prior (Dec-26):NT$3,200.00

Technology

William Yang AC (886-2) 2725-9899 william.yang@jpmorgan.com

Megan Hsueh (886-2) 2725-9249 megan.hsueh@jpmorgan.com J.P. Morgan Securities (Taiwan) Limited

| Key Changes (FYE Dec) | Key Changes (FYE Dec) | Key Changes (FYE Dec) | Key Changes (FYE Dec) |

|---|---|---|---|

| Prev | Cur | Δ | |

| Adj. EPS - 26E (NT$) | 185.34 | 200.82 | 8.4% |

| Adj. EPS - 27E (NT$) | 188.46 | 211.49 | 12.2% |

| Quarterly Forecasts (FYE Dec) | Quarterly Forecasts (FYE Dec) | Quarterly Forecasts (FYE Dec) | Quarterly Forecasts (FYE Dec) |

|---|---|---|---|

| Adj. EPS (NT$) | 2025A | 2026E | 2027E |

| Q1 | 48.28 | 46.63A | 47.83 |

| Q2 | 7.73 | 38.36 | 42.28 |

| Q3 | 53.05 | 56.84 | 60.35 |

| Q4 | 50.35 | 58.99 | 61.02 |

| FY | 159.41 | 200.82 | 211.49 |

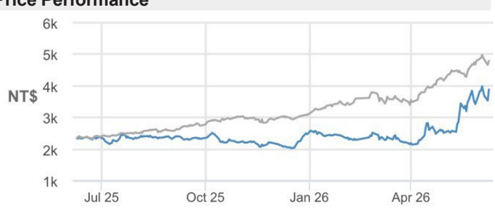

Style Exposure

Flice renomilanice

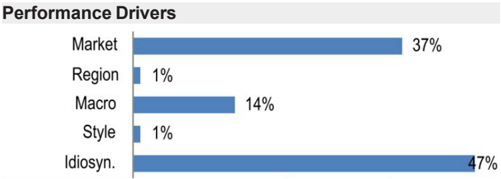

Fertormance Urivers

6k

Market

5k

J.P. Morgan

/ 1%

3k

2k

1k

Region

Idiosyn.

Factors

Jul 25

Oct 25

Price Performance

Macro:

US 10 Year Yield

HSI Volatility Index

Momentum

Quant Styles:

DivYld

Growth

14%

Jan 26

37%

47%

1Y Corr

0.57

Apr 26

6M Corr

0.43

0.07

— TSE (rebased)

0.16

Company Data

| Shares O/S (mn) | 131 |

|---|---|

| 52-week range (NT$) | 4,270.00-2,020.00 |

| Market cap ($ mn) | 17,074 |

| Exchange rate | 31.64 |

| Free float (%) | 58.1% |

| 3M ADV (mn) | 1.72 |

| 3M ADV ($ mn) | 161.1 |

| Volatility (90 Day) | 62 |

| Index | TAIEX |

| BBG ANR (Buy | Hold | Sell) | 10|12|1 |

Key Metrics (FYE Dec)

| NT$ in millions | FY25A | FY26E | FY27E |

|---|---|---|---|

| Financial Estimates | |||

| Revenue | 61,148 | 72,082 | 73,872 |

| Adj. EBIT | 23,558 | 27,482 | 29,174 |

| Adj. EBITDA | 31,290 | 36,143 | 38,144 |

| Adj. net income | 21,275 | 26,371 | 27,772 |

| Adj. EPS | 159.41 | 200.82 | 211.49 |

| BBG EPS | 156.30 | 186.81 | 200.54 |

| Cashflow from operations | 27,820 | 34,576 | 36,665 |

| FCFF | 12,006 | 25,697 | 28,745 |

| Margins and Growth | |||

| Revenue Growth Y/Y (%) | 2.8% | 17.9% | 2.5% |

| EBIT margin | 38.5% | 38.1% | 39.5% |

| EBIT Growth Y/Y (%) | (2.0%) | 16.7% | 6.2% |

| EBITDA margin | 51.2% | 50.1% | 51.6% |

| EBITDA Growth Y/Y (%) | 3.4% | 15.5% | 5.5% |

| Net margin | 34.8% | 36.6% | 37.6% |

| Adj. EPS growth | (18.8%) | 26.0% | 5.3% |

| Ratios | |||

| Adj. tax rate | 16.8% | 17.3% | 17.6% |

| Interest cover | NM | NM | NM |

| Net debt/Equity | NM | NM | NM |

| Net debt/EBITDA | NM | NM | NM |

| ROE | 11.3% | 13.6% | 13.6% |

| Valuation | |||

| FCFF yield | 2.2% | 4.7% | 5.3% |

| Dividend yield | 1.9% | 2.4% | 2.6% |

| EV/Revenue | 6.7 | 5.6 | 5.2 |

| EV/EBITDA | 13.1 | 11.1 | 10.0 |

| Adj. P/E | 25.9 | 20.6 | 19.5 |

Summary Investment Thesis and Valuation

Investment Thesis

We have a Neutral rating on the shares, as we think the company's stable sales growth from the variable aperture lens upgrade and resilient iPhone demand has been priced in, and the market has somewhat turned too positive on its CPO progress. We think there are still uncertainties on how quickly Largan could turn this opportunity into real earnings (at least not in the next 1-2 years) given the high competition and the company's lack of track record (vs comps), so we would suggest waiting on the sidelines for more concrete progress.

Valuation

Our Dec-26 PT of NT$3,600 is based on a 17x 2027E P/E, in line with the average P/E since 2012.

Table 1: J.P. Morgan estimates: New vs old

| NT$mn, NT$,% | Revised | Revised | Revised | Revised | Prior | Prior | Prior | Prior | Change | Change | Change | Change |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2Q26E | 3Q26E | 2026E | 2027E | 2Q26E | 3Q26E | 2026E | 2027E | 2Q26E | 3Q26E | 2026E | 2027E | |

| Sales | 14,702 | 20,241 | 72,082 | 73,872 | 13,828 | 17,838 | 64,389 | 64,492 | 6% | 13% | 12% | 15% |

| Gross profit | 7,316 | 10,088 | 35,745 | 37,614 | 6,883 | 8,902 | 32,025 | 32,802 | 6% | 13% | 12% | 15% |

| Gross margin | 49.8% | 49.8% | 49.6% | 50.9% | 49.8% | 49.9% | 49.7% | 50.9% | -1 bps | -7 bps | -15 bps | 5 bps |

| OP profit | 5,522 | 7,861 | 27,482 | 29,174 | 5,127 | 6,940 | 24,549 | 25,339 | 8% | 13% | 12% | 15% |

| OP margin | 37.6% | 38.8% | 38.1% | 39.5% | 37.1% | 38.9% | 38.1% | 39.3% | 49 bps | -7 bps | 0 bps | 20 bps |

| Net income | 5,037 | 7,464 | 26,371 | 27,772 | 4,818 | 6,808 | 24,337 | 25,152 | 5% | 10% | 8% | 10% |

| EPS (NT$) | 38.4 | 56.8 | 200.8 | 211.5 | 36.7 | 51.8 | 185.3 | 188.5 | 5% | 10% | 8% | 12% |

Source: J.P. Morgan estimates.

Table 2: J.P. Morgan estimates vs. Bloomberg consensus

| NT$mn, NT$,% | JPMe | JPMe | JPMe | JPMe | Bloomberg | Bloomberg | Bloomberg | Bloomberg | Differences | Differences | Differences | Differences |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2Q26E | 3Q26E | 2026E | 2027E | 2Q26E | 3Q26E | 2026E | 2027E | 2Q26E | 3Q26E | 2026E | 2027E | |

| Sales | 14,702 | 20,241 | 72,082 | 73,872 | 13,248 | 18,439 | 65,874 | 69,808 | 11% | 10% | 9% | 6% |

| Gross profit | 7,316 | 10,088 | 35,745 | 37,614 | 6,598 | 9,214 | 33,221 | 36,055 | 11% | 9% | 8% | 4% |

| Gross margin | 49.8% | 49.8% | 49.6% | 50.9% | 49.8% | 50.0% | 50.4% | 51.6% | -5 bps | -13 bps | -84 bps | -73 bps |

| OP profit | 5,522 | 7,861 | 27,482 | 29,174 | 5,023 | 7,102 | 25,646 | 27,984 | 10% | 11% | 7% | 4% |

| OP margin | 37.6% | 38.8% | 38.1% | 39.5% | 37.9% | 38.5% | 38.9% | 40.1% | -36 bps | 32 bps | -81 bps | -60 bps |

| Net income | 5,037 | 7,464 | 26,371 | 27,772 | 4,736 | 6,846 | 24,828 | 26,522 | 6% | 9% | 6% | 5% |

| EPS (NT$) | 38.4 | 56.8 | 200.8 | 211.5 | 35.8 | 51.8 | 186.8 | 201.0 | 7% | 10% | 7% | 5% |

Source: Bloomberg Finance L.P., J.P. Morgan estimates.

Estimate revisions

5

0

0

0

5

0

0

0

5

0

0

0

0

5

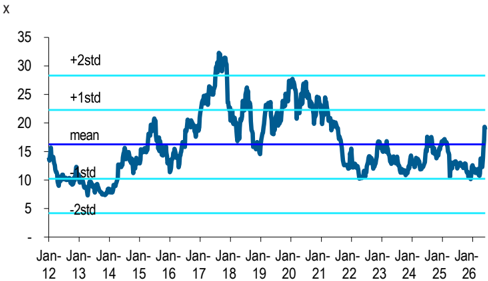

+2std

J.P. Morgan

+2std

- 1std

+1 std mean

mean

-2std

6

5

Valuation

Our Dec-26 PT of NT$3,600 is based on a 17x 2027E P/E, in line with the average P/E since 2012.

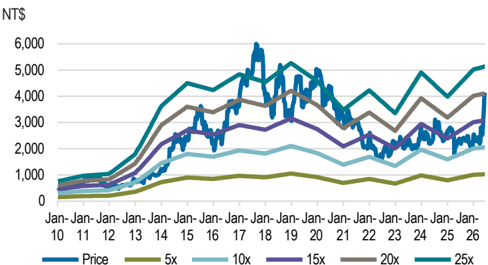

Figure 1: Largan's share price vs 1yr forward P/E

Source: Bloomberg Finance L.P.

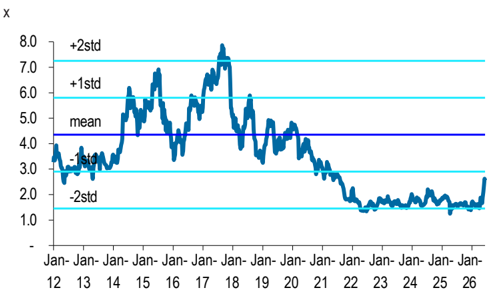

Figure 3: Largan's share price vs historical mean 1yr forward P/E

Source: Bloomberg Finance L.P.

Source: Bloomberg Finance L.P.

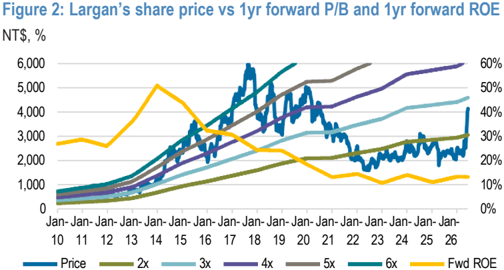

Figure 4: Largan's share price vs historical mean 1yr forward P/B

Source: Bloomberg Finance L.P.,

Table 3: Earnings table

| 2023 | 2023 | 2023 | 2023 | 2024 | 2024 | 2024 | 2024 | 2025 | 2025 | 2025 | 2025 | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2022 | 2024 2025 | 2023 | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | 2026E 2027E | |||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| NT$mn, NT$, % | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q | 1Q | 2Q | 3Q | 4Q 1Q | 2QE | 3QE | 4QE | 1QE | 2QE | 3QE | 4QE | 2021 | ||||||||||||||||||||||

| Revenue | 9,136 | 8,194 | 13,629 | 17,883 11,313 | 10,985 18,949 | 18,210 | 14,579 11,673 | 17,677 | 17,219 | 15,544 | 14,702 | 20,241 | 21,594 | 16,794 | 15,547 | 20,557 | 20,974 | 46,962 | 48,842 | 61,148 | 47,675 | 72,082 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | 73,872 | ||||

| Depreciation | 1,326 | 1,342 | 1,368 | 1,385 | 1,452 | 1,475 | 1,533 1,770 | 1,772 | 1,847 1,971 | 2,142 | 2,136 | 2,156 | 2,175 | 2,194 | 2,214 | 2,233 | 2,252 | 2,272 | 4,745 5,118 | 6,230 7,732 | 8,661 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | 8,971 | |||||

| COGS | 4,623 | 4,156 | 7,828 | 8,441 | 5,750 | 5,669 | 9,433 7,396 | 6,615 | 5,413 9,325 | 8,958 | 7,865 | 7,386 10,154 | 10,932 | 8,326 | 7,573 | 10,092 | 10,267 | 18,813 | 25,049 | 28,248 | 21,593 30,311 | 36,337 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | 36,258 | ||||

| Gross Profit | 4,513 | 4,039 | 5,801 | 9,442 | 5,563 | 5,316 | 9,516 10,814 | 7,965 | 6,260 | 8,352 8,260 | 7,680 | 7,316 | 10,088 | 10,662 | 8,467 | 7,973 | 10,465 | 10,708 | 28,150 | 26,083 | 23,794 | 31,209 30,837 | 35,745 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | 37,614 | |||

| Operating Expense | 1,244 | 1,287 | 1,919 | 1,541 | 1,602 | 1,426 | 1,715 2,433 | 1,878 | 1,381 | 2,088 | 1,932 | 1,867 | 1,794 2,227 | 2,375 | 2,032 | 1,943 | 2,244 | 2,220 5,002 | 5,704 | 7,177 | 7,279 | 8,263 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | 8,440 | ||||

| EBIT | 3,269 | 2,751 | 3,882 | 7,900 | 3,961 | 3,890 | 7,801 8,381 | 6,086 | 4,879 | 6,265 6,329 | 5,812 | 5,522 | 7,861 | 8,287 | 6,435 | 6,030 | 8,245 | 8,463 | 23,148 | 20,379 | 17,802 | 24,033 23,558 | 27,482 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | 29,174 | |||

| Net Interest Income | 923 | 990 | 1,023 | 996 1,098 | 1,101 | 1,072 1,133 | 1,137 | 1,061 | 1,031 1,029 | 970 | 1,020 | 958 | 1,042 | 1,025 1,180 | 1,190 | 1,099 | 949 | 1,690 | 3,934 | 4,404 | 4,259 | 4,512 | 3,973 | 3,973 | 3,973 | 3,973 | 3,973 | 3,973 | 3,973 | 3,973 | 3,973 | 3,973 | 3,973 | |||||||||

| Net Other Income | -283 | 1,281 | 2,138 | -2,775 | 2,371 | 815 | -1,024 1,575 | 493 | -4,146 | 859 | 878 | 505 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | -1,073 | 5,702 | 3,738 | -1,917 | 361 | 505 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||

| Pre Tax Profit | 3,909 | 5,023 | 7,043 | 6,122 | 7,430 | 5,806 | 7,849 11,089 | 7,716 | 1,794 | 8,155 | 8,236 | 7,288 | 6,542 | 8,886 | 9,244 | 7,477 | 7,210 | 9,435 | 9,563 | 23,024 | 27,771 | 22,097 | 32,174 | 25,900 31,960 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | 33,686 | |||

| Tax | 620 | 1,328 | 1,093 | 1,159 | 1,319 | 1,308 | 1,219 | 2,117 | 1,173 | 738 996 | 1,434 | 1,112 | 1,505 | 1,422 | 1,498 | 1,196 | 1,658 | 1,510 | 1,549 | 4,355 | 5,202 | 4,200 | 5,963 | 4,340 | 5,914 | 5,914 | 5,914 | 5,914 | 5,914 | 5,914 | 5,914 | 5,914 | 5,914 | 5,914 | 5,914 | 5,914 | 5,914 | |||||

| Net Profit (reported) | 3,289 | 3,695 | 5,951 | 4,963 | 6,111 | 4,498 | 6,630 | 8,972 | 6,443 | 1,032 | 7,080 | 6,720 | 6,123 | 5,037 | 7,464 | 7,747 | 6,281 | 5,552 | 7,926 | 8,014 | 18,668 | 22,569 | 17,897 | 26,211 | 21,275 26,371 | 27,772 | 27,772 | 27,772 | 27,772 | 27,772 | 27,772 | 27,772 | 27,772 | |||||||||

| EPS (NT$) | 24.6 | 27.7 | 44.6 | 37.2 | 45.8 | 33.7 | 49.7 | 67.2 | 48.28 | 7.73 | 53.05 | 50.35 | 46.6 | 38.4 | 56.8 | 59.0 | 47.8 | 42.3 | 60.4 | 61.0 | 139.2 | 169.1 | 134.1 | 196.4 | 159.4 | 200.8 | 211.5 | 211.5 | 211.5 | 211.5 | 211.5 | 211.5 | 211.5 | 211.5 | 211.5 | |||||||

| Margins (%) | ||||||||||||||||||||||||||||||||||||||||||

| Gross Margin | 49.4 | 49.3 | 42.6 | 52.8 | 49.2 | 48.4 | 50.2 59.4 | 54.6 | 53.6 | 47.2 | 48.0 | 49.4 | 49.8 | 49.8 | 49.4 | 50.4 | 51.3 | 50.9 | 51.1 | 59.9 | 54.7 | 48.7 | 52.5 | 50.4 | 49.6 | 50.9 | 50.9 | 50.9 | ||||||||||||||

| Opex ratio | 13.6 | 15.7 | 14.1 | 8.6 | 14.2 | 13.0 | 9.1 | 13.4 | 12.9 | 11.8 | 11.8 | 11.2 | 12.0 | 12.2 | 11.0 | 11.0 | 12.1 | 12.5 | 10.8 | 10.7 | 10.7 | 12.0 | 12.3 | 12.1 | 11.9 | 11.4 | 11.4 | 11.4 | 11.4 | 11.4 | 11.4 | 11.4 | 11.4 | 11.4 | 11.4 | 11.4 | ||||||

| Operating Margin | 35.8 | 33.6 | 28.5 | 44.2 | 35.0 | 35.4 | 41.2 | 46.0 | 41.7 | 41.8 | 35.4 | 36.8 | 37.4 | 37.6 | 38.8 | 38.4 | 38.3 | 38.8 | 40.1 49.3 | 40.4 | 36.4 | 42.7 | 40.4 | 38.5 | 39.5 | 39.5 | 39.5 | 39.5 | 39.5 | 39.5 | 39.5 | 39.5 | 39.5 | |||||||||

| Net Margin | 36.0 | 45.1 | 43.7 | 27.8 | 54.0 | 40.9 | 35.0 | 49.3 | 44.2 | 8.8 | 40.1 | 39.0 | 39.4 | 34.3 | 36.9 | 35.9 | 37.4 | 35.7 | 38.6 | 38.2 | 39.8 | 47.3 | 36.6 | 44.1 | 34.8 | 37.6 | 37.6 | 37.6 | 37.6 | 37.6 | 37.6 | 37.6 | 37.6 | 37.6 | 37.6 | 37.6 | 37.6 | |||||

| Sequential Growth (%) | ||||||||||||||||||||||||||||||||||||||||||

| Revenue | -37 | -10 | 66 | 31 | -37 | -3 | 72 | -4 | -20 | -20 | 51 | -3 | -10 | -5 | 38 | 7 | -22 | -7 | 32 | 2 | ||||||||||||||||||||||

| Gross Profit | -44 | -11 | 44 | 63 | -41 | -4 | 79 | 14 | -26 | -21 | 33 | -1 | -7 | -5 | 38 | 6 | -21 | -6 | 31 | 2 | ||||||||||||||||||||||

| EBIT | -52 | -16 | 41 | 104 | -50 | -2 | 101 | 7 | -27 | -20 28 | 1 | -8 | -5 | 42 | 5 | -6 | -22 | 37 | 3 | |||||||||||||||||||||||

| EPS (reported) | -18 | 12 | 61 | -17 | 23 | -26 | 47 | 35 -28 | -84 | 586 | -5 | -7 | -18 | 48 | 4 | -12 | -19 | 43 | 1 | |||||||||||||||||||||||

| YoY Growth (%) | ||||||||||||||||||||||||||||||||||||||||||

| Revenue | -10 | -15 | 1 | 24 | 24 | 34 | 39 | 2 | 29 | 6 | -7 | -5 | 7 | 26 | 15 | 25 | 8 | 6 | 2 | -3 | -16 | 2 | 2 | 22 | 18 | 3 | ||||||||||||||||

| Gross Profit | -17 | -25 | -20 | 17 | 23 | 32 | 64 | 15 | 43 18 | -12 -24 | -4 | 17 | 21 | 29 | 10 9 | 4 | 0 | -25 | -7 | -9 | 31 | -1 | 16 | 16 | 16 | 16 | 16 | 16 | 16 | 16 | ||||||||||||

| EBIT | -18 | -32 | -30 | 16 | 21 | 41 | 6 | 54 | 25 | -20 -24 | -5 | 13 | 25 | 11 | 2 | -12 | -28 | -13 | -2 | 35 | 17 | |||||||||||||||||||||

| EPS (reported) | -40 | -25 | -27 | 23 | 86 | 22 | 101 | 11 | 81 | 5 -77 | 7 -25 | -3 | 396 | 31 7 | 10 | 9 6 | 5 3 | -24 | 21 | -21 | 46 | -19 | 26 | 26 | 26 | 26 | 26 | 26 | 26 | 26 | ||||||||||||

| Sales mix (%) | 17 | 3 | ||||||||||||||||||||||||||||||||||||||||

| iPhone camera lens | 57 | 46 42 | 42 | 40 | 37 | 42 | 40 | 43 | 41 46 | 44 | 45 | 43 | 49 | 50 | 51 | 48 60 | 50 | 51 | 56 | 46 | 40 50 | 44 | 47 |

Source: Company data, J.P. Morgan estimates.

Investment Thesis, Valuation and Risks

Largan Precision Co Ltd (Neutral; Price Target: NT$3,600.00)

Investment

Thesis

We have a Neutral rating on the shares, as we think the company's stable sales growth from the variable aperture lens upgrade and resilient iPhone demand has been priced in, and the market has somewhat turned too positive on its CPO progress. We think there are still uncertainties on how quickly Largan could turn this opportunity into real earnings (at least not in the next 1-2 years) given the high competition and the company's lack of track record (vs comps), so we would suggest waiting on the sidelines for more concrete progress.

Valuation

Our Dec-26 PT of NT$3,600 is based on a 17x 2027E P/E, in line with the average P/E since 2012.

Risks to Rating and Price Target

Key upside risks to our rating and price target include: 1) faster progress in the new CPO/ FAU business; and 2) better-than-feared smartphone demand.

Key downside risks to our rating and price target include: 1) a much-faster-than-expected loss of market share to rivals, especially in the high-end lens market; 2) weaker smartphone sell-through; and 3) slower camera lens spec migration.

Largan Precision Co Ltd: Summary of Financials

| Income Statement | FY24A | FY25A | FY26E | FY27E | FY28E | Cash Flow Statement | FY24A | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Revenue | 59,458 | 61,148 | 72,082 | 73,872 | - | Cash flow from operating activities | 28,678 | 27,820 | 34,576 | 36,665 | - |

| COGS | (28,248) | (30,311) | (36,337) | (36,258) | - | o/w Depreciation & amortization | 6,230 | 7,732 | 8,661 | 8,971 | - |

| Gross profit | 31,209 | 30,837 | 35,745 | 37,614 | - | o/w Changes in working capital | (3,763) | (2,059) | (587) | (78) | - |

| SG&A | (1,930) | (1,985) | (2,162) | (2,286) | - | ||||||

| Adj. EBITDA | 30,262 | 31,290 | 36,143 | 38,144 | - | Cash flow from investing activities | (16,176) | (3,471) | (6,074) | (4,200) | - |

| D&A | (6,230) | (7,732) | (8,661) | (8,971) | - | o/w Capital expenditure | (12,031) | (12,269) | (5,594) | (4,200) | - |

| Adj. EBIT | 24,033 | 23,558 | 27,482 | 29,174 | - | as% of sales | 20.2% | 20.1% | 7.8% | 5.7% | - |

| Net Interest | 4,404 | 4,259 | 3,973 | 4,512 | - | ||||||

| Adj. PBT | 32,174 | 25,900 | 31,960 | 33,686 | - | Cash flow from financing activities | (5,679) | (16,674) | (20,904) | (13,451) | - |

| Tax | (5,963) | (4,340) | (5,536) | (5,914) | - | o/w Dividends paid | (9,009) | (12,728) | (10,486) | (13,451) | - |

| Minority Interest | 0 | (285) | (53) | 0 | - | o/w Shares issued/(repurchased) | 0 | 0 | 0 | 0 | - |

| Adj. Net Income | 26,211 | 21,275 | 26,371 | 27,772 | - | o/w Net debt issued/(repaid) | 203 | (203) | 0 | (0) | - |

| Reported EPS | 196.38 | 159.41 | 200.82 | 211.49 | - | Net change in cash | 6,823 | 7,675 | 7,598 | 19,014 | - |

| Adj. EPS | 196.38 | 159.41 | 200.82 | 211.49 | - | ||||||

| Adj. Free cash flow to firm | 13,060 | 12,006 | 25,697 | 28,745 | - | ||||||

| DPS | 98.85 | 79.14 | 100.78 | 106.14 | - | y/y Growth | 51.4% | (8.1%) | 114.0% | 11.9% | - |

| Payout ratio | 50.3% | 49.6% | 50.2% | 50.2% | - | ||||||

| Shares outstanding | 133 | 133 | 131 | 131 | - | ||||||

| Balance Sheet | FY24A | FY25A | FY26E | FY27E | FY28E | Ratio Analysis | FY24A | FY25A | FY26E | FY27E | FY28E |

| Cash and cash equivalents | 123,620 | 131,295 | 138,893 | 157,907 | - | Gross margin | 52.5% | 50.4% | 49.6% | 50.9% | - |

| Accounts receivable | 10,360 | 10,462 | 13,016 | 12,642 | - | EBITDA margin | 50.9% | 51.2% | 50.1% | 51.6% | - |

| Inventories | 5,733 | 6,713 | 8,192 | 7,694 | - | EBIT margin | 40.4% | 38.5% | 38.1% | 39.5% | - |

| Other current assets | 6,051 | 5,816 | 8,638 | 8,390 | - | Net profit margin | 44.1% | 34.8% | 36.6% | 37.6% | - |

| Current assets | 145,764 | 154,285 | 168,738 | 186,633 | - | ||||||

| PP&E | 46,936 | 51,472 | 48,406 | 43,635 | - | ROE | 14.9% | 11.3% | 13.6% | 13.6% | - |

| LT investments | 12,460 | 8,517 | 9,924 | 9,924 | - | ROA | 12.7% | 9.7% | 11.6% | 11.6% | - |

| Other non current assets | 11,367 | 6,512 | 5,586 | 5,586 | - | ROCE | 11.2% | 10.4% | 11.7% | 11.8% | - |

| Total assets | 216,527 | 220,787 | 232,653 | 245,777 | - | SG&A/Sales | 3.2% | 3.2% | 3.0% | 3.1% | - |

| Net debt/Equity | NM | NM | NM | NM | - | ||||||

| Short term borrowings | 203 | 0 | 0 | 0 | - | Net debt/EBITDA | NM | NM | NM | NM | - |

| Other short term liabilities | 28,520 | 28,021 | 33,222 | 32,268 | - | Sales/Assets (x) | 0.3 | 0.3 | 0.3 | 0.3 | - |

| Current liabilities | 30,578 | 29,749 | 36,095 | 34,897 | - | Assets/Equity (x) | 1.2 | 1.2 | 1.2 | 1.2 | 1.2 |

| Long-term debt | 0 | 0 | 0 | 0 | - | Interest cover (x) | NM | NM | NM | NM | - |

| Other long term liabilities | 561 | 171 | 226 | 226 | - | Operating leverage | 161.0% | (69.4%) | 93.2% | 247.8% | - |

| 31,139 | 29,919 | rate | 18.5% | 16.8% | 17.3% | 17.6% | - | ||||

| Total liabilities Shareholders' equity | 185,388 | 190,868 | 36,321 196,332 | 35,123 210,653 | - | Tax Revenue y/y Growth | 21.7% | 2.8% | 17.9% | 2.5% | - |

| Minority interests | - | - | - | - | EBITDA | 3.4% | 5.5% | - | |||

| - | 220,787 | - | y/y Growth | 30.3% | (18.8%) | 15.5% | - | ||||

| Total liabilities & equity | 216,527 | 232,653 | 245,777 | - | EPS y/y Growth | 46.5% FY24A | FY25A | 26.0% FY26E | 5.3% FY27E | FY28E | |

| BVPS | 1,389.00 | 1,430.06 | 1,471.00 | 1,604.15 | - | Valuation | |||||

| y/y Growth | 12.0% | 3.0% | 2.9% | 9.1% | - | P/E (x) | 21.0 | 25.9 | 20.6 | 19.5 2.6 | - - |

| P/BV (x) | 3.0 | 2.9 | 2.8 | 10.0 | - | ||||||

| Net debt/(cash) | (123,416)(131,295)(138,893)(157,907) | (123,416)(131,295)(138,893)(157,907) | (123,416)(131,295)(138,893)(157,907) | (123,416)(131,295)(138,893)(157,907) | - | EV/EBITDA (x) Dividend Yield | 13.8 2.4% | 13.1 1.9% | 11.1 2.4% | 2.6% | - |

Source: Company reports and J.P. Morgan estimates.

Note: NT$ in millions (except per-share data).Fiscal year ends Dec. o/w -out of which

• D

•N

oth

J.P. Morgan

Pre

Largan Precision Co Ltd (3008. TW, 3008 TT) Price Chart

•C

ent.

5500

4000

3000

Da

08

11

12

07

11

08

09

08

Analyst Certification: The Research Analyst(s) denoted by an 'AC' on the cover of this report certifies (or, where multiple Research Analysts are primarily responsible for this report, the Research Analyst denoted by an 'AC' on the cover or within the document individually certifies, with respect to each security or issuer that the Research Analyst covers in this research) that: (1) all of the views expressed in this report accurately reflect the Research Analyst's personal views about any and all of the subject securities or issuers; and (2) no part of any of the Research Analyst's compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the Research Analyst(s) in this report. For all Korea-based Research Analysts listed on the front cover, if applicable, they also certify, as per KOFIA requirements, that the Research Analyst's analysis was made in good faith and that the views reflect the Research Analyst's own opinion, without undue influence or intervention.

All authors named within this report are Research Analysts who produce independent research unless otherwise specified. In Europe, Sector Specialists (Sales and Trading) may be shown on this report as contacts but are not authors of the report or part of the Research Department.

圖片清單(已驗證 2026-07-02)

回補驗證:僅涵蓋已被 lib 頁嵌入的圖片,非全量驗證。

| 檔名 | size | 分類 | 親眼所見內容 |

|---|---|---|---|

260610_3008_大立光_jpm_largan_003.png |

68KB | 真資料圖 | 股價/PE 倍數區間圖(NT$),繪出 5x/10x/15x/20x/25x 本益比帶與實際股價線,時間範圍 Jan-10 至 Jan-26 |